Comprehensive Analysis of Management Accounting at Imda Tech Ltd

VerifiedAdded on 2020/01/23

|14

|4022

|61

Report

AI Summary

This report examines management accounting practices within Imda Tech Limited, a mobile charger manufacturer. It begins by defining management accounting, contrasting it with financial accounting, and highlighting its importance in managerial decision-making. The report explores various management accounting systems, including cost accounting, inventory management, and price optimization. It then delves into cost accounting methods, specifically marginal and absorption costing, illustrating their application with income statements. Furthermore, the report analyzes different types of budgets, discussing their advantages and disadvantages. Finally, it covers the balance scorecard approach and its role in achieving financial governance and strategic development within the company. The report provides a comprehensive overview of the tools and techniques used in management accounting to aid effective business decision-making.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1& P2 Management accounting. Its importance and difference between management and

financial accounting....................................................................................................................1

TASK 2 ...........................................................................................................................................4

P3 Income statements as per absorption and marginal costing...................................................4

TASK 3............................................................................................................................................6

P4 & D3 Budgets and its advantages and disadvantages............................................................6

TASK 4............................................................................................................................................7

P5,M4 & D3 Balance scorecard approach and its use in attain financial governance and

development of effective strategies.............................................................................................7

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1& P2 Management accounting. Its importance and difference between management and

financial accounting....................................................................................................................1

TASK 2 ...........................................................................................................................................4

P3 Income statements as per absorption and marginal costing...................................................4

TASK 3............................................................................................................................................6

P4 & D3 Budgets and its advantages and disadvantages............................................................6

TASK 4............................................................................................................................................7

P5,M4 & D3 Balance scorecard approach and its use in attain financial governance and

development of effective strategies.............................................................................................7

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................11

INTRODUCTION

Imda tech limited is one of the biggest manufacture of producing charger for mobile

phones and other gadgets. Under this report a detail description is given on the company. Under

this management accounting tool is described and how it is different from financial accounting is

described in this. How management accounting is useful and helps the manager of the firm in

making decision is described, other than this an explanation is given on various cost accounting

system used by the company. Absorption and marginal costing concepts given a light in this

report. This report contain important information about the various types of budgets used by a

firm and how a budget is prepared by them. What pricing strategy a firm should use in different

stages of their product life cycle is given light on. Other various tools used by the enterprise for

achieving its different kinds of objectives are described within this report.

TASK 1

P1& P2 Management accounting. Its importance and difference between management and

financial accounting

Management accounting is the process of preparing reports for the management that provide the

accurate financial and non financial information that are used by the mangers for taking various

decisions. Management accounting has wide scope. Financial accounting,cost accounting

revaluation,accounting control accounting and marginal accounting comes under the

management accounting Taxation,break even analysis,budgetary control,audit and taxation

comes under the scope of decision making of management accounting. It is prepared monthly

yearly and even on the day to day basis. The users of management accounting internal such as

department mangers and other officers(Zimmerman and Yahya-Zadeh2011). Management

accounting shows where the organisation stands at a particular point of time.

It gives detail of the cash in hand, debtors and the creditors, variance analysis etc.

management accounting is different from financial accounting. The main objectives of

management accounting are it helps in measuring the performances. With the help of

management accounting the performance of the employees are measured by comparing their

work with the desired results. Through this process control is kept on the performance as if the

results are not as that of the required than corrective actions are taken accordingly. It also helps

in maintaining efficiency in the organisation by keeping regular check. Another objective of

management accounting is to minimise the risk for the organisation. Through management

1

Imda tech limited is one of the biggest manufacture of producing charger for mobile

phones and other gadgets. Under this report a detail description is given on the company. Under

this management accounting tool is described and how it is different from financial accounting is

described in this. How management accounting is useful and helps the manager of the firm in

making decision is described, other than this an explanation is given on various cost accounting

system used by the company. Absorption and marginal costing concepts given a light in this

report. This report contain important information about the various types of budgets used by a

firm and how a budget is prepared by them. What pricing strategy a firm should use in different

stages of their product life cycle is given light on. Other various tools used by the enterprise for

achieving its different kinds of objectives are described within this report.

TASK 1

P1& P2 Management accounting. Its importance and difference between management and

financial accounting

Management accounting is the process of preparing reports for the management that provide the

accurate financial and non financial information that are used by the mangers for taking various

decisions. Management accounting has wide scope. Financial accounting,cost accounting

revaluation,accounting control accounting and marginal accounting comes under the

management accounting Taxation,break even analysis,budgetary control,audit and taxation

comes under the scope of decision making of management accounting. It is prepared monthly

yearly and even on the day to day basis. The users of management accounting internal such as

department mangers and other officers(Zimmerman and Yahya-Zadeh2011). Management

accounting shows where the organisation stands at a particular point of time.

It gives detail of the cash in hand, debtors and the creditors, variance analysis etc.

management accounting is different from financial accounting. The main objectives of

management accounting are it helps in measuring the performances. With the help of

management accounting the performance of the employees are measured by comparing their

work with the desired results. Through this process control is kept on the performance as if the

results are not as that of the required than corrective actions are taken accordingly. It also helps

in maintaining efficiency in the organisation by keeping regular check. Another objective of

management accounting is to minimise the risk for the organisation. Through management

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

accounting the future risk which can be anticipated in advance are studied and actions are taken

accordingly so that the degree of risk can be minimised. Decision regarding allocation of

resources are also taken by the company with the help of management accounting so that

resources can be effectively utilised. Financial accounting is done also for the external users of

the business like the share holders debtors stakeholder, government banks etc(Mitchell and

Nørreklit 2010). it gives them knowledge about the financial growth of the company which they

in decision taking of investment. The management reports are prepared on the basis of past

performance as per the requirement where as the financial reports are prepared on the present

financial situation of the company. These reports include cash flow outstanding debts day to day

management etc. it is not a legal requirement to prepare the management reports but financial

reports are necessary to be prepared by the limited companies. Where management accounting

provide only both the financial and non financial reports the financial reports give only the

financial information.

2.Importance of management accounting:

Management accounting plays a very important role in the process of decision making. Managers

are expected to take various dioecious each day andsions. Budgetary accounting helps mangers

to take the various financial decisions. These include deci there decisions have long as well

short term effects on the business. Therefore the management accounting provide the required

data to the different mangers which help them in taking the effective decision regarding the

allocation of finance in the different activities and also from where the company can raise its

funds after anaylising various alternatives available in the market. Management planning also

help the business in forecasting and planning. Data provided in the management make the

mangers aware about the various threats and opportunities of the business.

Therefore this helps in taking the decision of future expansion and other changes if

required in the existing process. Relevant cost accounting is a part of management

accounting(Lukka and Modell 2010). This help the mangers in taking the decision regarding

weather the the company should produce the product itself or should outsource it. Decision is

taken on the basis of the data provided by the accounting that which one is more beneficial for

the company. With the help of this accounting system the cash flow is anaylising ng and the

returns of every year is calculated and therefore it helps in analysing the change in the consume

2

accordingly so that the degree of risk can be minimised. Decision regarding allocation of

resources are also taken by the company with the help of management accounting so that

resources can be effectively utilised. Financial accounting is done also for the external users of

the business like the share holders debtors stakeholder, government banks etc(Mitchell and

Nørreklit 2010). it gives them knowledge about the financial growth of the company which they

in decision taking of investment. The management reports are prepared on the basis of past

performance as per the requirement where as the financial reports are prepared on the present

financial situation of the company. These reports include cash flow outstanding debts day to day

management etc. it is not a legal requirement to prepare the management reports but financial

reports are necessary to be prepared by the limited companies. Where management accounting

provide only both the financial and non financial reports the financial reports give only the

financial information.

2.Importance of management accounting:

Management accounting plays a very important role in the process of decision making. Managers

are expected to take various dioecious each day andsions. Budgetary accounting helps mangers

to take the various financial decisions. These include deci there decisions have long as well

short term effects on the business. Therefore the management accounting provide the required

data to the different mangers which help them in taking the effective decision regarding the

allocation of finance in the different activities and also from where the company can raise its

funds after anaylising various alternatives available in the market. Management planning also

help the business in forecasting and planning. Data provided in the management make the

mangers aware about the various threats and opportunities of the business.

Therefore this helps in taking the decision of future expansion and other changes if

required in the existing process. Relevant cost accounting is a part of management

accounting(Lukka and Modell 2010). This help the mangers in taking the decision regarding

weather the the company should produce the product itself or should outsource it. Decision is

taken on the basis of the data provided by the accounting that which one is more beneficial for

the company. With the help of this accounting system the cash flow is anaylising ng and the

returns of every year is calculated and therefore it helps in analysing the change in the consume

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

demand potential sale and related segment . Therefore management accounting helps the

manager in various fields of business by providing the relevant data.

(b) There are various types of management accounting system. Each provide reports for

assistance to the different departments of the business. With the help of these reports the process

of decision making becomes more easy and more effective. Different accounting system are as

follows:

Cost accounting system: Cost accounting refers to the system of allocation of different

expenditure in the production of different goods and services. This help in keeping

control over different expenditures of the company. It include various cost appropriation

like cost of production, selling and distribution. It helps in getting the exact figure of

expenditure in the different activities and this way those expense can be compared with

the past data and the changes are recorded for the purpose of making

comparisons(Weißenberger and Angelkort 2011). Apart from comparisons the data also

helps in taking the future decisions regarding the estimates. Cost accounting helps in

providing the right information too the right person so that the right decision can be taken

by the right time.

Inventory management system: This managements system help in keeping check on the

total inventory of the business. It is important for the business to maintain the required

inventory stock with themselves. Decision regarding the inventory are very important as

if the inventory is excess in stock than it will lead to increase in the cost of storing it.

Whereas if the inventory is in the deficit than availability of the product will result into

loss of sales and therefore the overall profit will get reduce.

Job costing system:Information related to the cost associated with different jobs are given

in this accounting system. In this the information of the cost of labour, overhead cost and

the cost of direct material is given. These costs are needed to be customised sometimes as

per the need of the customer. Sometimes the customer do not want all the cost to be

charged against them and pay for only certain jobs.

Price optimising system: It is a very important accounting system in this the report n how

customer respond to different prices are prepared(Macintosh and Quattrone 2010). The

customer is very price sensitive. Any change in the price has direct effect on the demand

3

manager in various fields of business by providing the relevant data.

(b) There are various types of management accounting system. Each provide reports for

assistance to the different departments of the business. With the help of these reports the process

of decision making becomes more easy and more effective. Different accounting system are as

follows:

Cost accounting system: Cost accounting refers to the system of allocation of different

expenditure in the production of different goods and services. This help in keeping

control over different expenditures of the company. It include various cost appropriation

like cost of production, selling and distribution. It helps in getting the exact figure of

expenditure in the different activities and this way those expense can be compared with

the past data and the changes are recorded for the purpose of making

comparisons(Weißenberger and Angelkort 2011). Apart from comparisons the data also

helps in taking the future decisions regarding the estimates. Cost accounting helps in

providing the right information too the right person so that the right decision can be taken

by the right time.

Inventory management system: This managements system help in keeping check on the

total inventory of the business. It is important for the business to maintain the required

inventory stock with themselves. Decision regarding the inventory are very important as

if the inventory is excess in stock than it will lead to increase in the cost of storing it.

Whereas if the inventory is in the deficit than availability of the product will result into

loss of sales and therefore the overall profit will get reduce.

Job costing system:Information related to the cost associated with different jobs are given

in this accounting system. In this the information of the cost of labour, overhead cost and

the cost of direct material is given. These costs are needed to be customised sometimes as

per the need of the customer. Sometimes the customer do not want all the cost to be

charged against them and pay for only certain jobs.

Price optimising system: It is a very important accounting system in this the report n how

customer respond to different prices are prepared(Macintosh and Quattrone 2010). The

customer is very price sensitive. Any change in the price has direct effect on the demand

3

of the product. Customer before buying any product from the market compares the price

of other substitute that are available in the market and than take the buying decision.

Therefore price of any product is kept after anylising the trend of the market for which

data is provided by the management accounting team to the mangers.

TASK 2

P3 Income statements as per absorption and marginal costing

Marginal costing: Marginal cost is the cost of producing one more unit. Marginal cost is

the that cost which arise one more product is made by the production department. One

can say the increase and that decrease in the total cost of production by making one more

unit of the product is known as marginal costing. When adding more unit in the

production process helps in decreasing the total cost of production than it helps the

organisation or is in the benefit of the enterprise to produce that unit otherwise making

another product in the will increase the total cost of production process.

Absorption costing: Absorption costing is the cost which arise on making a product or

all that direct expenses which arise on making a product comes the absorption costing.

Absorption costing does not include fixed cost occurred on making a product because it is

that cost which occurred when there is no sales or also when the production process is not

carry by the production department. Absorption costing concept only calculates the

variable cost which arise on making a product. In brief,Absorption costing adds all the

direct expenses and indirect cost which occur while making a product without adding

fixed in it.

Income statement as per absorption costing

Selling price per unit £35

Unit costs

Direct materials cost per unit £8

Direct Labour £5

Variable Production overhead £2

Fixed Production overhead £1

Budgeted production for the period is 36000 units per annum.

Production = 2000 units

4

of other substitute that are available in the market and than take the buying decision.

Therefore price of any product is kept after anylising the trend of the market for which

data is provided by the management accounting team to the mangers.

TASK 2

P3 Income statements as per absorption and marginal costing

Marginal costing: Marginal cost is the cost of producing one more unit. Marginal cost is

the that cost which arise one more product is made by the production department. One

can say the increase and that decrease in the total cost of production by making one more

unit of the product is known as marginal costing. When adding more unit in the

production process helps in decreasing the total cost of production than it helps the

organisation or is in the benefit of the enterprise to produce that unit otherwise making

another product in the will increase the total cost of production process.

Absorption costing: Absorption costing is the cost which arise on making a product or

all that direct expenses which arise on making a product comes the absorption costing.

Absorption costing does not include fixed cost occurred on making a product because it is

that cost which occurred when there is no sales or also when the production process is not

carry by the production department. Absorption costing concept only calculates the

variable cost which arise on making a product. In brief,Absorption costing adds all the

direct expenses and indirect cost which occur while making a product without adding

fixed in it.

Income statement as per absorption costing

Selling price per unit £35

Unit costs

Direct materials cost per unit £8

Direct Labour £5

Variable Production overhead £2

Fixed Production overhead £1

Budgeted production for the period is 36000 units per annum.

Production = 2000 units

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

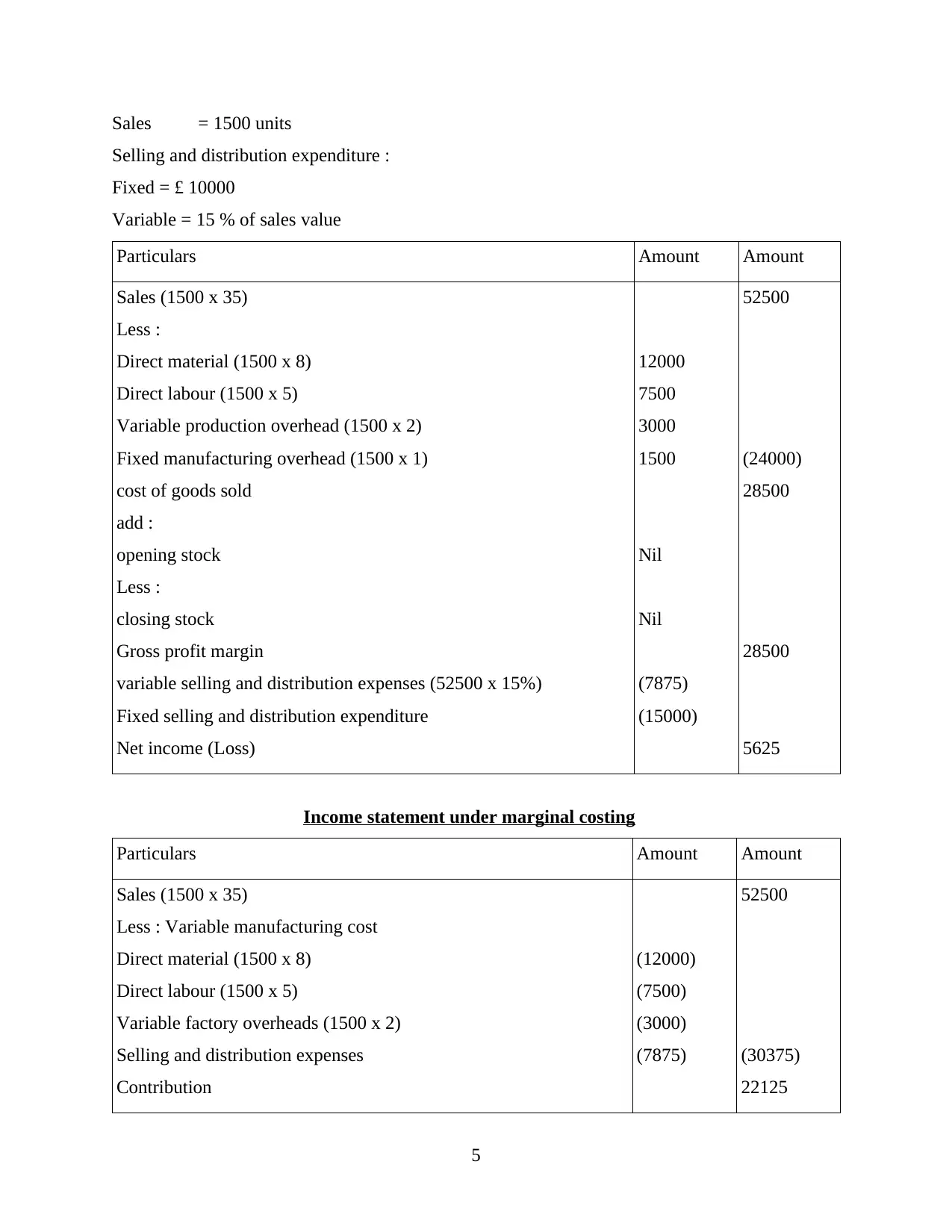

Sales = 1500 units

Selling and distribution expenditure :

Fixed = £ 10000

Variable = 15 % of sales value

Particulars Amount Amount

Sales (1500 x 35)

Less :

Direct material (1500 x 8)

Direct labour (1500 x 5)

Variable production overhead (1500 x 2)

Fixed manufacturing overhead (1500 x 1)

cost of goods sold

add :

opening stock

Less :

closing stock

Gross profit margin

variable selling and distribution expenses (52500 x 15%)

Fixed selling and distribution expenditure

Net income (Loss)

12000

7500

3000

1500

Nil

Nil

(7875)

(15000)

52500

(24000)

28500

28500

5625

Income statement under marginal costing

Particulars Amount Amount

Sales (1500 x 35)

Less : Variable manufacturing cost

Direct material (1500 x 8)

Direct labour (1500 x 5)

Variable factory overheads (1500 x 2)

Selling and distribution expenses

Contribution

(12000)

(7500)

(3000)

(7875)

52500

(30375)

22125

5

Selling and distribution expenditure :

Fixed = £ 10000

Variable = 15 % of sales value

Particulars Amount Amount

Sales (1500 x 35)

Less :

Direct material (1500 x 8)

Direct labour (1500 x 5)

Variable production overhead (1500 x 2)

Fixed manufacturing overhead (1500 x 1)

cost of goods sold

add :

opening stock

Less :

closing stock

Gross profit margin

variable selling and distribution expenses (52500 x 15%)

Fixed selling and distribution expenditure

Net income (Loss)

12000

7500

3000

1500

Nil

Nil

(7875)

(15000)

52500

(24000)

28500

28500

5625

Income statement under marginal costing

Particulars Amount Amount

Sales (1500 x 35)

Less : Variable manufacturing cost

Direct material (1500 x 8)

Direct labour (1500 x 5)

Variable factory overheads (1500 x 2)

Selling and distribution expenses

Contribution

(12000)

(7500)

(3000)

(7875)

52500

(30375)

22125

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Less : Fixed Cost

Manufacturing overheads (1500 x 1)

Selling and distribution overheads

Net Income/ (Loss)

(1500)

(15000) (16500)

5625

TASK 3

P4 & D3 Budgets and its advantages and disadvantages

a)Different types of budgets are prepared for the mangers. These budgets has their own

advantages and disadvantages on the business. Different budgets are prepared for different

departments depending upon the motive behind why they are prepared.

1 Master budget: It is the aggregate of the different budgets of the company. Through this budget

the complete knowledge about the companies finance can be taken out. It includes various

factors like the total assets sales assets sources of income etc. it is usually prepared in the big

companies and other budgets are made on the basis of this master budget.

2.Operating budget: These budgets are frequently prepared in the organisation. These are related

to the operating activities of any business like production sales manufacturing cost etc.

3.Cash flow budget: This budget gives the details of cash flows in and out of the business in a

particular period of time(Ward 2012 ). It helps in keeping check on the efficiency of cash

transactions. In the cash flow budgets details of cash outstanding with outsiders and cash

payable to the the outsiders are given which give the net amount of cash in hand with the

business. The cash flow budget help in taking decision regarding expansion of business or if any

change is required in the existing financial policy.

b)A set process is followed by the Inda tech company to prepare the budget for its company:

1.Obtaining estimates: The company gets the estimates of the future sales, cost that is expected

against them, resources available for the production etc. The head of the departments estimate

6

Manufacturing overheads (1500 x 1)

Selling and distribution overheads

Net Income/ (Loss)

(1500)

(15000) (16500)

5625

TASK 3

P4 & D3 Budgets and its advantages and disadvantages

a)Different types of budgets are prepared for the mangers. These budgets has their own

advantages and disadvantages on the business. Different budgets are prepared for different

departments depending upon the motive behind why they are prepared.

1 Master budget: It is the aggregate of the different budgets of the company. Through this budget

the complete knowledge about the companies finance can be taken out. It includes various

factors like the total assets sales assets sources of income etc. it is usually prepared in the big

companies and other budgets are made on the basis of this master budget.

2.Operating budget: These budgets are frequently prepared in the organisation. These are related

to the operating activities of any business like production sales manufacturing cost etc.

3.Cash flow budget: This budget gives the details of cash flows in and out of the business in a

particular period of time(Ward 2012 ). It helps in keeping check on the efficiency of cash

transactions. In the cash flow budgets details of cash outstanding with outsiders and cash

payable to the the outsiders are given which give the net amount of cash in hand with the

business. The cash flow budget help in taking decision regarding expansion of business or if any

change is required in the existing financial policy.

b)A set process is followed by the Inda tech company to prepare the budget for its company:

1.Obtaining estimates: The company gets the estimates of the future sales, cost that is expected

against them, resources available for the production etc. The head of the departments estimate

6

these activities and make the budget accordingly. Reports are prepared and then submitted to the

heads and approval is taken from them.

2.Coordinating estimates: At this step the different estimates are carefully analysed and then the

best suitable option is selected which gives the maximum profit and have more chances to be

practically implemented. It is estimated on the basis of available resources with the organisation.

3.Communicating budget: Once the budget is prepared it is communicated to the different

concern departments. The budget than act as a ground on which different activities take place. It

is helpful for the mangers to have budget for their work to be done as they get the idea as how

they have to carry out their activities.

4.Implementing the budget plan: Once the budget is communicated in the different departments

the budget is reviewed by the concern department heads. They go through the budget and then

the resources required to full fill that budget are also provided to them(Soin and Collier 2013).

After making all the resources available the implementation of the action for which the budget is

prepared take place.

(c)Pricing strategies: As the Inda company is deals with a product which has many substitutes

available in the market, the company has to adopt a very effective pricing strategy.Proper market

survey should be done before fixing the price(Otley and Emmanuel 2013). The price should not

exceed much from other similar products as this will bring loss of potential customer to the

company.

TASK 4

P5,M4 & D3 Balance scorecard approach and its use in attain financial governance and

development of effective strategies

Balanced score approach is a strategies performance management,in the balance score

including strategies planning and management system that is used large business and industry

governments and non profit entity(Abuazza and et. al., 2015). Imda Tech (UK) Ltd to use

balance score approach strategies to improve external and internal communication to monitor

and performance against strategies goals. Imda Tech (UK) Ltd the strategies evolved from use a

simple performance measurement to framework to strategic planning and managements.

The the entity balance scorecard approach transform organisation use a daily strategies

plan .the strategies is help to identify planners not only performance management. The balance

7

heads and approval is taken from them.

2.Coordinating estimates: At this step the different estimates are carefully analysed and then the

best suitable option is selected which gives the maximum profit and have more chances to be

practically implemented. It is estimated on the basis of available resources with the organisation.

3.Communicating budget: Once the budget is prepared it is communicated to the different

concern departments. The budget than act as a ground on which different activities take place. It

is helpful for the mangers to have budget for their work to be done as they get the idea as how

they have to carry out their activities.

4.Implementing the budget plan: Once the budget is communicated in the different departments

the budget is reviewed by the concern department heads. They go through the budget and then

the resources required to full fill that budget are also provided to them(Soin and Collier 2013).

After making all the resources available the implementation of the action for which the budget is

prepared take place.

(c)Pricing strategies: As the Inda company is deals with a product which has many substitutes

available in the market, the company has to adopt a very effective pricing strategy.Proper market

survey should be done before fixing the price(Otley and Emmanuel 2013). The price should not

exceed much from other similar products as this will bring loss of potential customer to the

company.

TASK 4

P5,M4 & D3 Balance scorecard approach and its use in attain financial governance and

development of effective strategies

Balanced score approach is a strategies performance management,in the balance score

including strategies planning and management system that is used large business and industry

governments and non profit entity(Abuazza and et. al., 2015). Imda Tech (UK) Ltd to use

balance score approach strategies to improve external and internal communication to monitor

and performance against strategies goals. Imda Tech (UK) Ltd the strategies evolved from use a

simple performance measurement to framework to strategic planning and managements.

The the entity balance scorecard approach transform organisation use a daily strategies

plan .the strategies is help to identify planners not only performance management. The balance

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

scorecard access the traditional measure(Spivacenco, 2015). In this approach provide feedback

related entity process and outcomes in order continue improve performance and results. Cited

enterprise disregard the traditional need of financial data,to Need to including additional

financial related data, cost benefits to effective the entity of financial statements. Balance

scorecards is very effective to analysis the aspect of entity performance(AlfantoroAnghelache

and et.al 2012). Imda Tech (UK) Limited has recently published for the last financial year a loss

of £1.5 million the effective to financial health and various points to impacts like customers

satisfaction is down employee training is deficient or that processes are outdated.

Balance scorecards approach only thing being future evaluated. Allow for stakeholders to

determine the health of long term objectives achieve. Finally by using a Balanced scorecards a

n enterprise can sure that if any strategies action implemented(SANGANİ, HADJİ and

NONAHAL-NAHR, 2015). The price of a product down help to bottom line in the long run the

process involves to creating a product make to the hight quality.

Imda Tech (UK) Ltd adopts a balance and comprehensive approach of judgement and

controlling an organisation performance to st up objectives and learning growth. Firm can

integrate financial and non financial goals measurement into a single system to considers

traditional techniques(Ciotină and CIOTINĂ, 2013). Business enterprise brings central

management focus to communicates and understanding business goals and strategies all the

level of organisation.

Poorly define metrics can be defined as a disadvantage of using balanced score card

approach. To collected at the ideal frequencies for making decision. lack of efficient data

collecting and reporting,no process improvements methodology , only focus on the internal and

review of structures related disadvantages impact to balance score card approach.

How it can be used to improve financial governance and development of effective strategies

Imda Tech (UK) limited used to improve governance and developing various effective

principals: The basis of an effective governance teamwork:

To promote efficient market be consistent with the rule of law and to promote division

among different super enforcement authorise

The board scorecards fretwork to financial objectives to maximize long term total return

to shareholders. Strengthen and motivate executive performance. Oversee succession

planning for try position(Delima and Kristanti, 2016).

8

related entity process and outcomes in order continue improve performance and results. Cited

enterprise disregard the traditional need of financial data,to Need to including additional

financial related data, cost benefits to effective the entity of financial statements. Balance

scorecards is very effective to analysis the aspect of entity performance(AlfantoroAnghelache

and et.al 2012). Imda Tech (UK) Limited has recently published for the last financial year a loss

of £1.5 million the effective to financial health and various points to impacts like customers

satisfaction is down employee training is deficient or that processes are outdated.

Balance scorecards approach only thing being future evaluated. Allow for stakeholders to

determine the health of long term objectives achieve. Finally by using a Balanced scorecards a

n enterprise can sure that if any strategies action implemented(SANGANİ, HADJİ and

NONAHAL-NAHR, 2015). The price of a product down help to bottom line in the long run the

process involves to creating a product make to the hight quality.

Imda Tech (UK) Ltd adopts a balance and comprehensive approach of judgement and

controlling an organisation performance to st up objectives and learning growth. Firm can

integrate financial and non financial goals measurement into a single system to considers

traditional techniques(Ciotină and CIOTINĂ, 2013). Business enterprise brings central

management focus to communicates and understanding business goals and strategies all the

level of organisation.

Poorly define metrics can be defined as a disadvantage of using balanced score card

approach. To collected at the ideal frequencies for making decision. lack of efficient data

collecting and reporting,no process improvements methodology , only focus on the internal and

review of structures related disadvantages impact to balance score card approach.

How it can be used to improve financial governance and development of effective strategies

Imda Tech (UK) limited used to improve governance and developing various effective

principals: The basis of an effective governance teamwork:

To promote efficient market be consistent with the rule of law and to promote division

among different super enforcement authorise

The board scorecards fretwork to financial objectives to maximize long term total return

to shareholders. Strengthen and motivate executive performance. Oversee succession

planning for try position(Delima and Kristanti, 2016).

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The enterprise balanced scorecard access information for executive management and the

board :

To improve financial grow revenue,provide customers financial solution for life, balance

score adopters to use the tools for interactive discussion with their board about the strategies

direction to keep the apprised of performance and other way essential provide members financial

and non financial information about balance score card and fulfilling their performance oversight

responsibilities the enterprise with supporting primary documents distributes board

meeting(Kendrick, 2012). The strategic is also provide accountabilities to the board primary

committees it is responsibilities for performance oversight. Primary oversight evaluating

motivating executive.

There are two types of governance strategies is the most create solid information

Governance strategies:safer or more secure data: The establishing effective

information governance strategies involves a rules and responsibilities, standard and

regulation to improve securities reliability integrating quality of data in improve in the

governance strategies.Improved collaborating data integral to the business modern

success to help business innovation to decision making(Marpaung, Marlina and Amelia,

2016).

Reduced cost: in this strategies to information more efficient use and to increase

productivity and reduce wastes. Cited enterprise with a comprehensive information

governance strategies also in cares ability to comply more effectively risk reducing.

CONCLUSION

As per the above mentioned facts and figures which are there in this report it can be

concluded that management accounting techniques can be used by any enterprise in order to

utilize the financial and non financial available sources of it. Through its techniques these

resources can generate better returns further methods like forecasting or budgeting Imda Tech

(UK) Ltd can plan their activities and future projects in an efficient way. Further balanced score

card approach can be used for sustaining the financial governance and effective strategy making.

As management accounting is a combination of accounting and managerial principles hence

through it better decision making can be there. As through it managerial personnels can utilize

balanced score card method which is basically a process through which strategies can be drafted

and made as per the required level of effectiveness and scope. Further in this file methods of

9

board :

To improve financial grow revenue,provide customers financial solution for life, balance

score adopters to use the tools for interactive discussion with their board about the strategies

direction to keep the apprised of performance and other way essential provide members financial

and non financial information about balance score card and fulfilling their performance oversight

responsibilities the enterprise with supporting primary documents distributes board

meeting(Kendrick, 2012). The strategic is also provide accountabilities to the board primary

committees it is responsibilities for performance oversight. Primary oversight evaluating

motivating executive.

There are two types of governance strategies is the most create solid information

Governance strategies:safer or more secure data: The establishing effective

information governance strategies involves a rules and responsibilities, standard and

regulation to improve securities reliability integrating quality of data in improve in the

governance strategies.Improved collaborating data integral to the business modern

success to help business innovation to decision making(Marpaung, Marlina and Amelia,

2016).

Reduced cost: in this strategies to information more efficient use and to increase

productivity and reduce wastes. Cited enterprise with a comprehensive information

governance strategies also in cares ability to comply more effectively risk reducing.

CONCLUSION

As per the above mentioned facts and figures which are there in this report it can be

concluded that management accounting techniques can be used by any enterprise in order to

utilize the financial and non financial available sources of it. Through its techniques these

resources can generate better returns further methods like forecasting or budgeting Imda Tech

(UK) Ltd can plan their activities and future projects in an efficient way. Further balanced score

card approach can be used for sustaining the financial governance and effective strategy making.

As management accounting is a combination of accounting and managerial principles hence

through it better decision making can be there. As through it managerial personnels can utilize

balanced score card method which is basically a process through which strategies can be drafted

and made as per the required level of effectiveness and scope. Further in this file methods of

9

absorption and marginal costing is used in order to compute the net profit of Imda Tech (UK)

Ltd.

10

Ltd.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.