Detailed Report on Management Accounting for Imda Tech's Business

VerifiedAdded on 2020/01/07

|16

|4388

|157

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles and their application to Imda Tech, a company specializing in mobile phone chargers and electronic gadgets. The report begins by defining management accounting and differentiating it from financial accounting, highlighting its role in internal decision-making. It then explores the significance of management accounting for Imda Tech, emphasizing its ability to aid in strategic planning, cost management, and performance evaluation. The report delves into various management accounting systems, including cost accounting, inventory management, job costing, and price optimization. Furthermore, it examines profit and loss determination using absorption costing. The report also covers budget statements, pros and cons of different budgeting techniques, and methods for determining selling prices. Finally, it discusses the Balanced Scorecard (BSC) concept and its importance in the workplace, providing a holistic view of performance measurement and strategic alignment for Imda Tech.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

The method under which different number of financial transactions like as incomes and

outcomes are recorded, analysed, assessed, monitored etc. by the managers and responsible

employees for making business decisions is called as management accounting. All the business

entities which operate in the industry adopt the respective accounting system for make the firm

profitable along with taking decisions for the internal business environment. The current case

scenario is to be explained using the business like as Imda Tech which provide the products such

as specific kind of chargers for mobile phone and electronic gadgets. The report describes about

the systems which are beneficial for the Imda Tech which comes under the management

accounting as well as make difference of management as well as financial accounting. The

second part is all about the determining net profit by considering two costing ways such as

marginal and absorption. In the third task of the project, phases tgo making budget statements,

pros and cons of various budgets as well as the techniques to determine selling price of the

chargers for Imda Tech are explained. With the help of last part, the reader able to understand

about the Balanced Scorecard (BSC) concept and its importance at the workplace.

TASK 1

A) I. Explaining management accounting along with making difference with financial accounting

The process and method under accounting which supports to identify, assess, measure,

analyse, prepare as well as interpret the financial information and data to make effectual plan and

implement at the workplace is identified as the management accounting. In the world of

accounting there are two main concepts come which are like as the financial as well as

management by which Imda Tech external and internal decisions for business (Rossi, 2014).

Moreover, difference among such mentioned both the concepts of accounting is describes as

below:

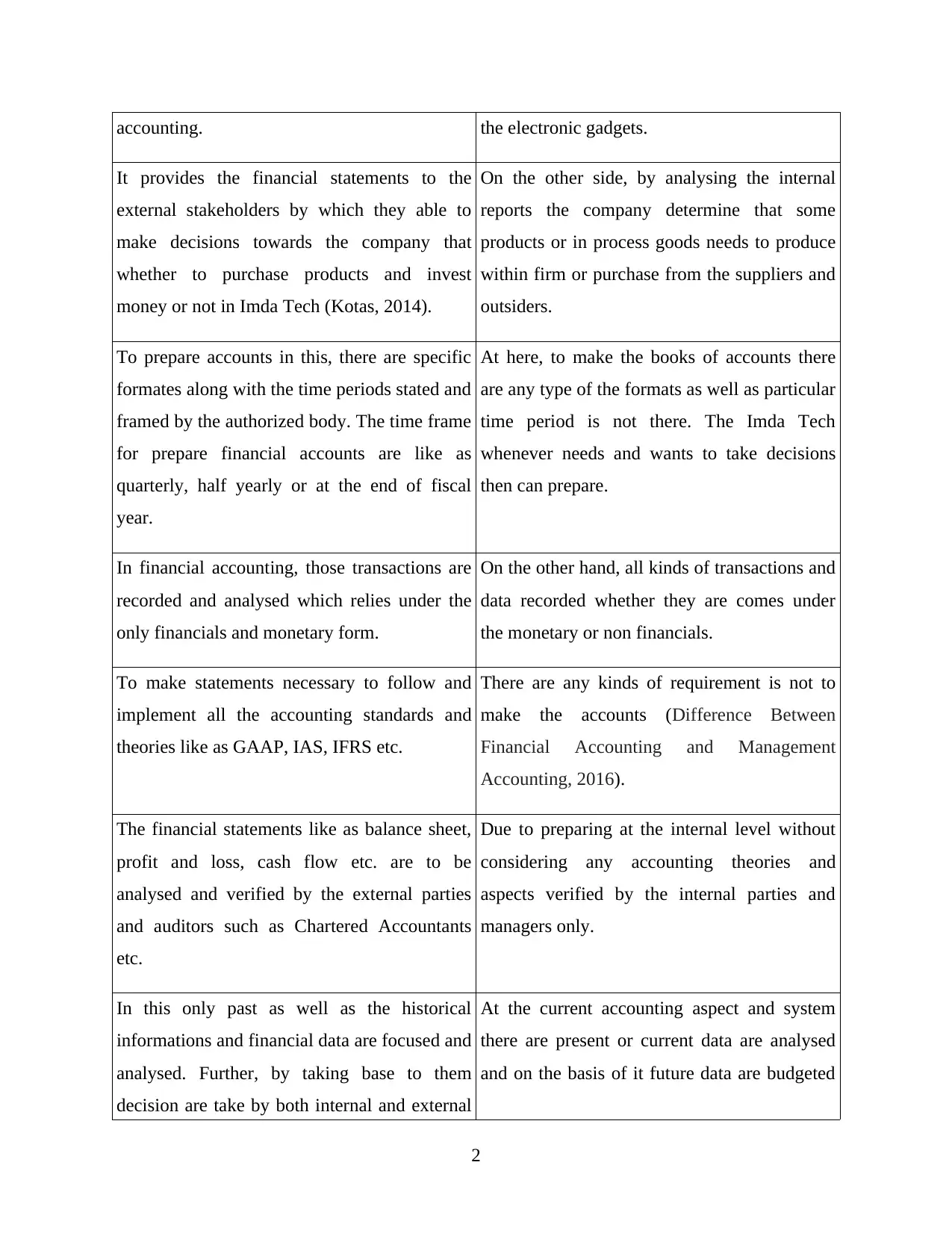

Financial Accounting Management Accounting

The concept which is used by the businesses in

order to assess the overall business

performance in terms of the financials and

profitability is identified as financial

The management accounting is used by only

internal stakeholders of Imda Tech to know

that how much costing is there for making the

mobile phone chargers and different types of

1

The method under which different number of financial transactions like as incomes and

outcomes are recorded, analysed, assessed, monitored etc. by the managers and responsible

employees for making business decisions is called as management accounting. All the business

entities which operate in the industry adopt the respective accounting system for make the firm

profitable along with taking decisions for the internal business environment. The current case

scenario is to be explained using the business like as Imda Tech which provide the products such

as specific kind of chargers for mobile phone and electronic gadgets. The report describes about

the systems which are beneficial for the Imda Tech which comes under the management

accounting as well as make difference of management as well as financial accounting. The

second part is all about the determining net profit by considering two costing ways such as

marginal and absorption. In the third task of the project, phases tgo making budget statements,

pros and cons of various budgets as well as the techniques to determine selling price of the

chargers for Imda Tech are explained. With the help of last part, the reader able to understand

about the Balanced Scorecard (BSC) concept and its importance at the workplace.

TASK 1

A) I. Explaining management accounting along with making difference with financial accounting

The process and method under accounting which supports to identify, assess, measure,

analyse, prepare as well as interpret the financial information and data to make effectual plan and

implement at the workplace is identified as the management accounting. In the world of

accounting there are two main concepts come which are like as the financial as well as

management by which Imda Tech external and internal decisions for business (Rossi, 2014).

Moreover, difference among such mentioned both the concepts of accounting is describes as

below:

Financial Accounting Management Accounting

The concept which is used by the businesses in

order to assess the overall business

performance in terms of the financials and

profitability is identified as financial

The management accounting is used by only

internal stakeholders of Imda Tech to know

that how much costing is there for making the

mobile phone chargers and different types of

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

accounting. the electronic gadgets.

It provides the financial statements to the

external stakeholders by which they able to

make decisions towards the company that

whether to purchase products and invest

money or not in Imda Tech (Kotas, 2014).

On the other side, by analysing the internal

reports the company determine that some

products or in process goods needs to produce

within firm or purchase from the suppliers and

outsiders.

To prepare accounts in this, there are specific

formates along with the time periods stated and

framed by the authorized body. The time frame

for prepare financial accounts are like as

quarterly, half yearly or at the end of fiscal

year.

At here, to make the books of accounts there

are any type of the formats as well as particular

time period is not there. The Imda Tech

whenever needs and wants to take decisions

then can prepare.

In financial accounting, those transactions are

recorded and analysed which relies under the

only financials and monetary form.

On the other hand, all kinds of transactions and

data recorded whether they are comes under

the monetary or non financials.

To make statements necessary to follow and

implement all the accounting standards and

theories like as GAAP, IAS, IFRS etc.

There are any kinds of requirement is not to

make the accounts (Difference Between

Financial Accounting and Management

Accounting, 2016).

The financial statements like as balance sheet,

profit and loss, cash flow etc. are to be

analysed and verified by the external parties

and auditors such as Chartered Accountants

etc.

Due to preparing at the internal level without

considering any accounting theories and

aspects verified by the internal parties and

managers only.

In this only past as well as the historical

informations and financial data are focused and

analysed. Further, by taking base to them

decision are take by both internal and external

At the current accounting aspect and system

there are present or current data are analysed

and on the basis of it future data are budgeted

2

It provides the financial statements to the

external stakeholders by which they able to

make decisions towards the company that

whether to purchase products and invest

money or not in Imda Tech (Kotas, 2014).

On the other side, by analysing the internal

reports the company determine that some

products or in process goods needs to produce

within firm or purchase from the suppliers and

outsiders.

To prepare accounts in this, there are specific

formates along with the time periods stated and

framed by the authorized body. The time frame

for prepare financial accounts are like as

quarterly, half yearly or at the end of fiscal

year.

At here, to make the books of accounts there

are any type of the formats as well as particular

time period is not there. The Imda Tech

whenever needs and wants to take decisions

then can prepare.

In financial accounting, those transactions are

recorded and analysed which relies under the

only financials and monetary form.

On the other hand, all kinds of transactions and

data recorded whether they are comes under

the monetary or non financials.

To make statements necessary to follow and

implement all the accounting standards and

theories like as GAAP, IAS, IFRS etc.

There are any kinds of requirement is not to

make the accounts (Difference Between

Financial Accounting and Management

Accounting, 2016).

The financial statements like as balance sheet,

profit and loss, cash flow etc. are to be

analysed and verified by the external parties

and auditors such as Chartered Accountants

etc.

Due to preparing at the internal level without

considering any accounting theories and

aspects verified by the internal parties and

managers only.

In this only past as well as the historical

informations and financial data are focused and

analysed. Further, by taking base to them

decision are take by both internal and external

At the current accounting aspect and system

there are present or current data are analysed

and on the basis of it future data are budgeted

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

stakeholders (Schaltegger, Gibassier and

Zvezdov, 2013).

and then strategies are to be framed.

A) II. Significance of management accounting for the Imda Tech to take business decisions

The current concept of management accounting is the very helpful and supportive for the

companies for making several kinds of decisions along with framing the strategies and

techniques to achieve goals. In the current market scenario, there are level of competition is very

high ans complex by which the companies are not able to operate in the industry in appropriate

and profitable way. Along with this, level of generating the amount in form of profit and revenue

also gets reduce. In this case, with the help of the management accounting concepts the Imda

Tech able to manage the costing and enhance revenue which helps to it for make more efficient.

It is used by the companies at the wider level within the workplace by which they can know

existing level of performance and on the basis of it fruitful and accountable tactics are made. In

this context, several advantages or the significance are described as below:

Through the management accounting various kinds of data and informations regarding to

the company are analysed and evaluated and in accordance to that Imda Tech highly able

to determine and fix aims as well as objectives. Every firm has common objective and

goal which is such as to improve the level of profit and maximize it in the industry

(Strumickas and Valanciene, 2015). By this accounting criteria firm know that how much

production is manufactured utilizing the raw materials and on the basis of it further

decisions and objectives are to be framed.

With the accounting, the company can make and prepare plan for the further periods of

the fiscal which is the most necessary for it to improve the production and sales level.

When there are the production goes down along with increasing the costs and

expenditures then by considering management accounting Imda Tech can prepare the

schedule for enhance outputs and mobile phone chargers with existing and same raw

materials.

In order to prepare budget for assessing the data of financials for future in the present

fiscal period the management accounting is one of the most helpful technique for Imda

3

Zvezdov, 2013).

and then strategies are to be framed.

A) II. Significance of management accounting for the Imda Tech to take business decisions

The current concept of management accounting is the very helpful and supportive for the

companies for making several kinds of decisions along with framing the strategies and

techniques to achieve goals. In the current market scenario, there are level of competition is very

high ans complex by which the companies are not able to operate in the industry in appropriate

and profitable way. Along with this, level of generating the amount in form of profit and revenue

also gets reduce. In this case, with the help of the management accounting concepts the Imda

Tech able to manage the costing and enhance revenue which helps to it for make more efficient.

It is used by the companies at the wider level within the workplace by which they can know

existing level of performance and on the basis of it fruitful and accountable tactics are made. In

this context, several advantages or the significance are described as below:

Through the management accounting various kinds of data and informations regarding to

the company are analysed and evaluated and in accordance to that Imda Tech highly able

to determine and fix aims as well as objectives. Every firm has common objective and

goal which is such as to improve the level of profit and maximize it in the industry

(Strumickas and Valanciene, 2015). By this accounting criteria firm know that how much

production is manufactured utilizing the raw materials and on the basis of it further

decisions and objectives are to be framed.

With the accounting, the company can make and prepare plan for the further periods of

the fiscal which is the most necessary for it to improve the production and sales level.

When there are the production goes down along with increasing the costs and

expenditures then by considering management accounting Imda Tech can prepare the

schedule for enhance outputs and mobile phone chargers with existing and same raw

materials.

In order to prepare budget for assessing the data of financials for future in the present

fiscal period the management accounting is one of the most helpful technique for Imda

3

Tech. When the future data and informations are assessed and determined then company

can know that how much sum of money needs to generate for making budgeted expenses.

In case the firm founds that it cannot generate the predetermined income for fulfil all the

expenses then require fund which is raised through sources of finance. In this condition

the management accounting will appropriately help to take decisions of choosing the

financing sources (Toluwalope, 2016).

Apart from this, it supports to the Imda Tech business organisation for understanding and

analysing the business performance by using the variance analysis of various kinds. The

method under which two kinds of results and data are compared like as expected and

actual is called variance analysis which is part of the management accounting. Hence, it

can be said that with this Imda Tech can evaluated that whether the objectives and

budgeted data are to be achieved or not. In case, it not able to meet with the expected data

then make the strategies for increase efficiency of individuals which lead to meet with

purposes and aims.

B) Different number of systems which rely under management accounting

In the management accounting criteria there are several numbers of the systems as well as

approaches are available which helps to the company for assessing performance and take

decisions. Moreover, the systems are highly beneficial for each company whether it operates in

the manufacturing or service or any other industry. The different systems along with their

importance are described as below:

Cost accounting system

In the management accounting, the system and approach where different kinds of the

level of cost and expenses are to be analysed as well as evaluated by the managers is known as

cost accounting or product costing system as well (Ng, Harrison and Akroyd, 2013). In such kind

of the method the business of Imda Tech collect, classify and segregate, evaluate etc. the

alternative costs and expenses which incur to manufacture the products like as electronic gadgets

and mobile phone chargers. After using this system the level of cost is to be determined that

whether it is effectual or enhance and in accordance to that strategies are framed to administering

the total costing. Higher the cost lead to reduce capability of Imda Tech to decline profit and

business performance in the overall industry which is the adverse aspect of it. On the basis of

4

can know that how much sum of money needs to generate for making budgeted expenses.

In case the firm founds that it cannot generate the predetermined income for fulfil all the

expenses then require fund which is raised through sources of finance. In this condition

the management accounting will appropriately help to take decisions of choosing the

financing sources (Toluwalope, 2016).

Apart from this, it supports to the Imda Tech business organisation for understanding and

analysing the business performance by using the variance analysis of various kinds. The

method under which two kinds of results and data are compared like as expected and

actual is called variance analysis which is part of the management accounting. Hence, it

can be said that with this Imda Tech can evaluated that whether the objectives and

budgeted data are to be achieved or not. In case, it not able to meet with the expected data

then make the strategies for increase efficiency of individuals which lead to meet with

purposes and aims.

B) Different number of systems which rely under management accounting

In the management accounting criteria there are several numbers of the systems as well as

approaches are available which helps to the company for assessing performance and take

decisions. Moreover, the systems are highly beneficial for each company whether it operates in

the manufacturing or service or any other industry. The different systems along with their

importance are described as below:

Cost accounting system

In the management accounting, the system and approach where different kinds of the

level of cost and expenses are to be analysed as well as evaluated by the managers is known as

cost accounting or product costing system as well (Ng, Harrison and Akroyd, 2013). In such kind

of the method the business of Imda Tech collect, classify and segregate, evaluate etc. the

alternative costs and expenses which incur to manufacture the products like as electronic gadgets

and mobile phone chargers. After using this system the level of cost is to be determined that

whether it is effectual or enhance and in accordance to that strategies are framed to administering

the total costing. Higher the cost lead to reduce capability of Imda Tech to decline profit and

business performance in the overall industry which is the adverse aspect of it. On the basis of

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

cost accounting, Imda Tech can raise and improve the extent of efficiency and productivity of

both such as company and organisational members.

Inventory management system

Stock is key aspect of every firm but higher the inventory remains within workplace lead

to reduce and hamper the profitability in the industry which lead to decline the business

performance. For this thing, it is necessary to manage, control and reduce the inventory in the

company for enhancing its current and existing business performance. Apart from this, when

there are all the inventories are utilized in appropriate manner then able to make more number of

chargers as well as sale at the lower rate in the market (Noreen, Garrison and Brewer, 2014). In

addition to this, it is also necessary to determine value of the inventory which is there with the

Imda Tech and for this various methods are available. Different techniques for valuing stock are

like as LIFO (last in first out), weighted average method as well as FIFO (first in first out).

Job costing system

The method and system where cost and expenses are analysed which are associated with

the each and every kind of product and services or batches is called as job costing system. With

this the Imda Tech is highly able to know that which kind of product incur how much amount of

the costs and expenses. In case, when the company adopt the job costing system then capable to

manage as well as administer all the costs which are relating with the different batches like as

electronic gadgets, mobile phone chargers etc. Moreover, this system is better and effectual for

the company to reduce the costing which is associated with all kinds of the product ranges

manufactured and offered in the firm.

Price optimisation system

Other than these all the explained systems there are price optimisation system is also one

of the best and highly effectual for the company which helps to analyse that at different level of

costs and prices customers are giving response in which ways (Jacobs and Cuganesan, 2014).

When the Imda Tech sales its gadgets and chargers in the market then able to know that

customers are purchase more or less number of products on which level of prices. For example:

at the cost of 250 GBP and 300 GBP the consumers are increasing or reduce the power of

purchasing it. On the basis of it, Imda Tech highly capable for making the decision that which

level of prices needs to charge from customers.

5

both such as company and organisational members.

Inventory management system

Stock is key aspect of every firm but higher the inventory remains within workplace lead

to reduce and hamper the profitability in the industry which lead to decline the business

performance. For this thing, it is necessary to manage, control and reduce the inventory in the

company for enhancing its current and existing business performance. Apart from this, when

there are all the inventories are utilized in appropriate manner then able to make more number of

chargers as well as sale at the lower rate in the market (Noreen, Garrison and Brewer, 2014). In

addition to this, it is also necessary to determine value of the inventory which is there with the

Imda Tech and for this various methods are available. Different techniques for valuing stock are

like as LIFO (last in first out), weighted average method as well as FIFO (first in first out).

Job costing system

The method and system where cost and expenses are analysed which are associated with

the each and every kind of product and services or batches is called as job costing system. With

this the Imda Tech is highly able to know that which kind of product incur how much amount of

the costs and expenses. In case, when the company adopt the job costing system then capable to

manage as well as administer all the costs which are relating with the different batches like as

electronic gadgets, mobile phone chargers etc. Moreover, this system is better and effectual for

the company to reduce the costing which is associated with all kinds of the product ranges

manufactured and offered in the firm.

Price optimisation system

Other than these all the explained systems there are price optimisation system is also one

of the best and highly effectual for the company which helps to analyse that at different level of

costs and prices customers are giving response in which ways (Jacobs and Cuganesan, 2014).

When the Imda Tech sales its gadgets and chargers in the market then able to know that

customers are purchase more or less number of products on which level of prices. For example:

at the cost of 250 GBP and 300 GBP the consumers are increasing or reduce the power of

purchasing it. On the basis of it, Imda Tech highly capable for making the decision that which

level of prices needs to charge from customers.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 2

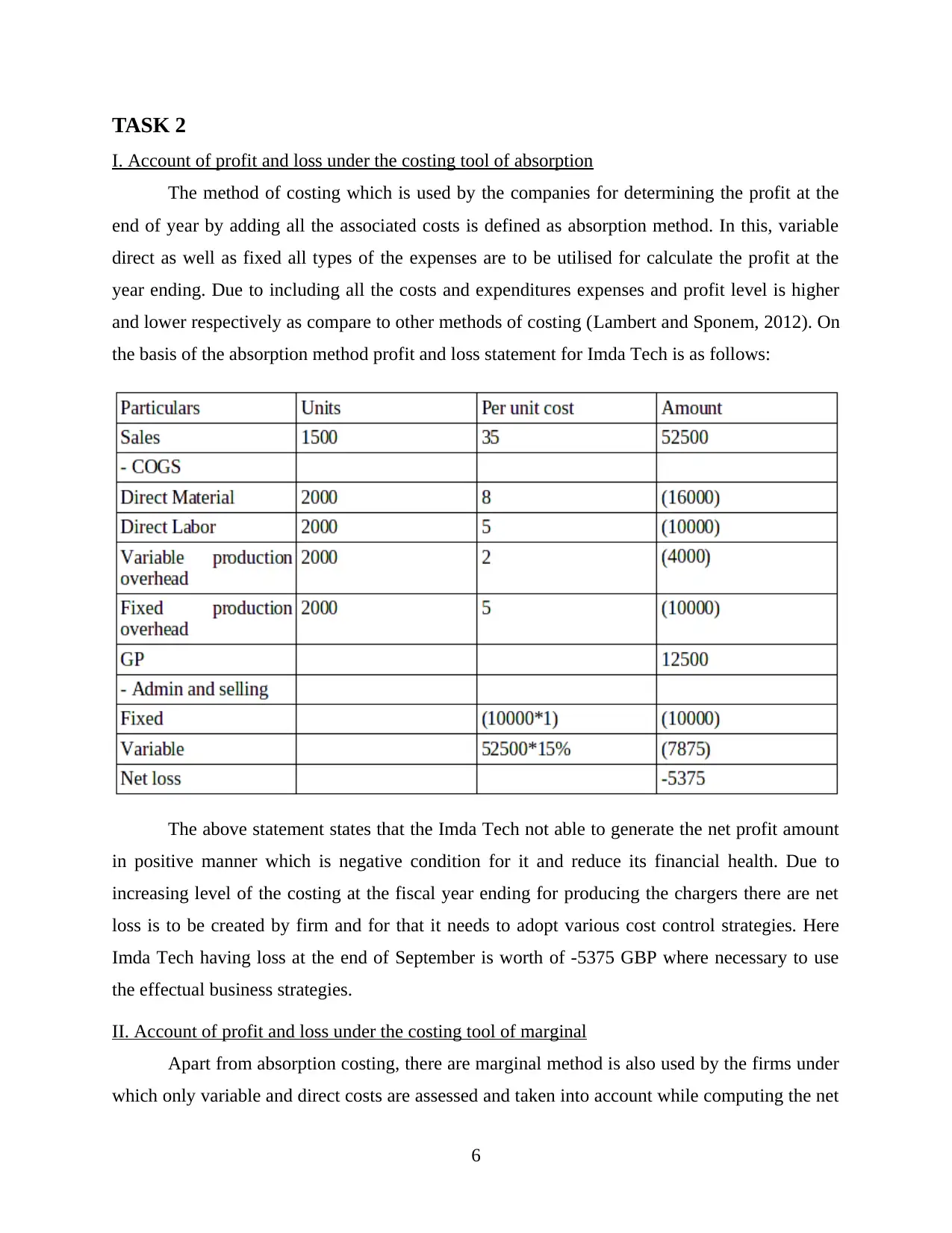

I. Account of profit and loss under the costing tool of absorption

The method of costing which is used by the companies for determining the profit at the

end of year by adding all the associated costs is defined as absorption method. In this, variable

direct as well as fixed all types of the expenses are to be utilised for calculate the profit at the

year ending. Due to including all the costs and expenditures expenses and profit level is higher

and lower respectively as compare to other methods of costing (Lambert and Sponem, 2012). On

the basis of the absorption method profit and loss statement for Imda Tech is as follows:

The above statement states that the Imda Tech not able to generate the net profit amount

in positive manner which is negative condition for it and reduce its financial health. Due to

increasing level of the costing at the fiscal year ending for producing the chargers there are net

loss is to be created by firm and for that it needs to adopt various cost control strategies. Here

Imda Tech having loss at the end of September is worth of -5375 GBP where necessary to use

the effectual business strategies.

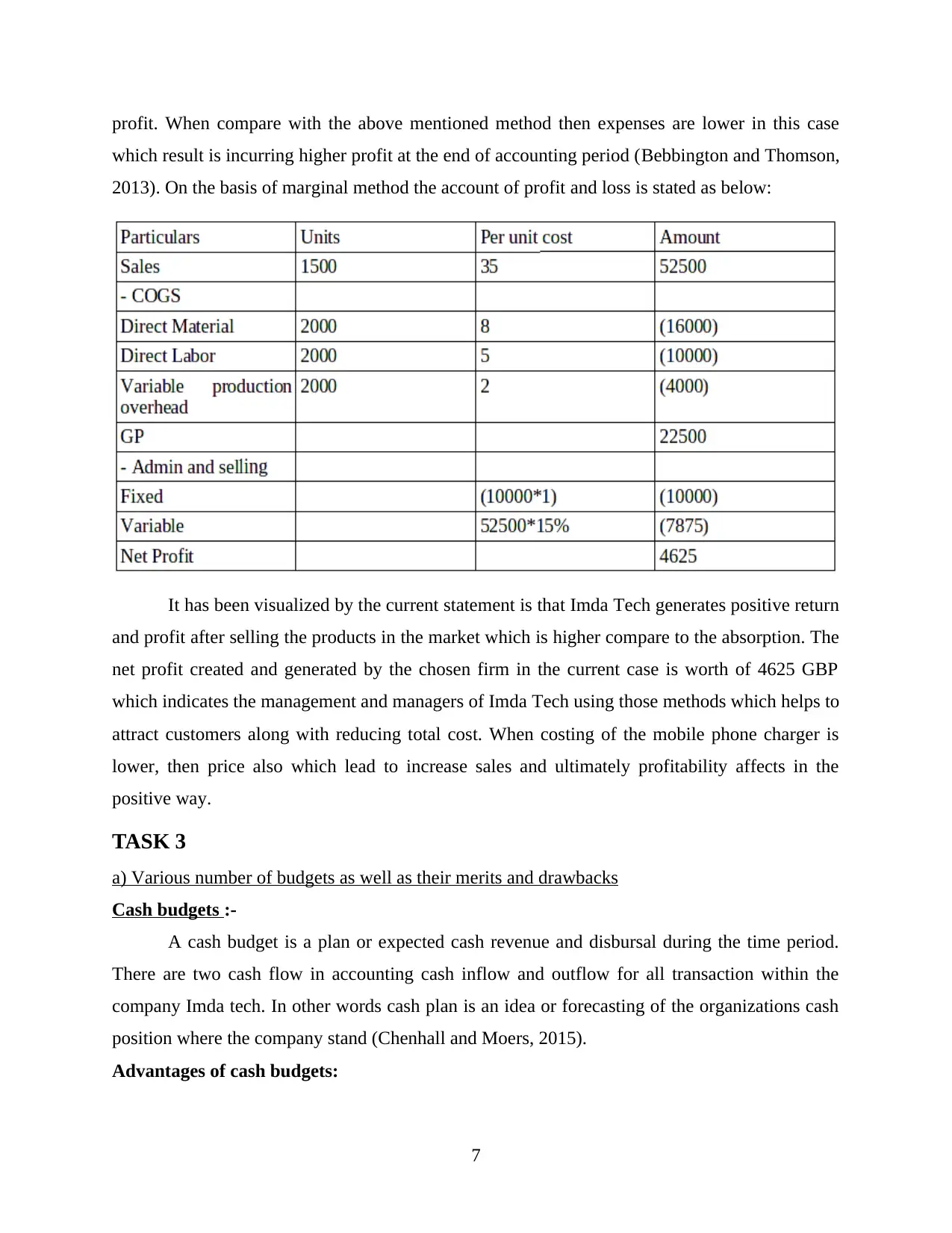

II. Account of profit and loss under the costing tool of marginal

Apart from absorption costing, there are marginal method is also used by the firms under

which only variable and direct costs are assessed and taken into account while computing the net

6

I. Account of profit and loss under the costing tool of absorption

The method of costing which is used by the companies for determining the profit at the

end of year by adding all the associated costs is defined as absorption method. In this, variable

direct as well as fixed all types of the expenses are to be utilised for calculate the profit at the

year ending. Due to including all the costs and expenditures expenses and profit level is higher

and lower respectively as compare to other methods of costing (Lambert and Sponem, 2012). On

the basis of the absorption method profit and loss statement for Imda Tech is as follows:

The above statement states that the Imda Tech not able to generate the net profit amount

in positive manner which is negative condition for it and reduce its financial health. Due to

increasing level of the costing at the fiscal year ending for producing the chargers there are net

loss is to be created by firm and for that it needs to adopt various cost control strategies. Here

Imda Tech having loss at the end of September is worth of -5375 GBP where necessary to use

the effectual business strategies.

II. Account of profit and loss under the costing tool of marginal

Apart from absorption costing, there are marginal method is also used by the firms under

which only variable and direct costs are assessed and taken into account while computing the net

6

profit. When compare with the above mentioned method then expenses are lower in this case

which result is incurring higher profit at the end of accounting period (Bebbington and Thomson,

2013). On the basis of marginal method the account of profit and loss is stated as below:

It has been visualized by the current statement is that Imda Tech generates positive return

and profit after selling the products in the market which is higher compare to the absorption. The

net profit created and generated by the chosen firm in the current case is worth of 4625 GBP

which indicates the management and managers of Imda Tech using those methods which helps to

attract customers along with reducing total cost. When costing of the mobile phone charger is

lower, then price also which lead to increase sales and ultimately profitability affects in the

positive way.

TASK 3

a) Various number of budgets as well as their merits and drawbacks

Cash budgets :-

A cash budget is a plan or expected cash revenue and disbursal during the time period.

There are two cash flow in accounting cash inflow and outflow for all transaction within the

company Imda tech. In other words cash plan is an idea or forecasting of the organizations cash

position where the company stand (Chenhall and Moers, 2015).

Advantages of cash budgets:

7

which result is incurring higher profit at the end of accounting period (Bebbington and Thomson,

2013). On the basis of marginal method the account of profit and loss is stated as below:

It has been visualized by the current statement is that Imda Tech generates positive return

and profit after selling the products in the market which is higher compare to the absorption. The

net profit created and generated by the chosen firm in the current case is worth of 4625 GBP

which indicates the management and managers of Imda Tech using those methods which helps to

attract customers along with reducing total cost. When costing of the mobile phone charger is

lower, then price also which lead to increase sales and ultimately profitability affects in the

positive way.

TASK 3

a) Various number of budgets as well as their merits and drawbacks

Cash budgets :-

A cash budget is a plan or expected cash revenue and disbursal during the time period.

There are two cash flow in accounting cash inflow and outflow for all transaction within the

company Imda tech. In other words cash plan is an idea or forecasting of the organizations cash

position where the company stand (Chenhall and Moers, 2015).

Advantages of cash budgets:

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cash budget is helpful for Imda tech in forecasting or idea of cash position in the

future.

Cash budget helps in how much cash require for future investment.

Cash budget also helpful for Imda tech in set up financially for seasonal change in

sales and expenditure.

Disadvantage of cash budget :-

The cash budget include subject matter regarding the organization expectable finance

needs.

According Imda tech Cash budget is use of estimation.

As per Imda tech Cash budget used to analysis fiscal needs and financing choice non

financial component are excluded.

Sales budget :-

A sales budget means estimation or plan of all sales activities in the organization for

production and sale of product and services. In other words sales budget is key function of sales

management for profit maximizing and solve dad stock problems in the company. Its presents

administrations the best estimation of sales tax revenue (CPIM, 2014).

Advantages of sales budget :-

According Imda tech sales budget helps in estimation of product production for

achieve the sales goal and targets.

As per Imda tech sales budget beneficial for achieve zero west production.

Sales budget is helpful in relocated of resources for increasing production of the

company

Disadvantage of sales budget :-

According the forecasters present time sales budget can't efficaciously forecast the

market trends

As per Imda tech sales budget can not much more beneficial in this competitive

market because customer are very fast switch from company to another.

Sales budget is highly expansive and time consuming process because more human

resource require for customer feedback and survey for forecasting.

According Imda tech in sales management require highly qualified employee for

forecasting.

8

future.

Cash budget helps in how much cash require for future investment.

Cash budget also helpful for Imda tech in set up financially for seasonal change in

sales and expenditure.

Disadvantage of cash budget :-

The cash budget include subject matter regarding the organization expectable finance

needs.

According Imda tech Cash budget is use of estimation.

As per Imda tech Cash budget used to analysis fiscal needs and financing choice non

financial component are excluded.

Sales budget :-

A sales budget means estimation or plan of all sales activities in the organization for

production and sale of product and services. In other words sales budget is key function of sales

management for profit maximizing and solve dad stock problems in the company. Its presents

administrations the best estimation of sales tax revenue (CPIM, 2014).

Advantages of sales budget :-

According Imda tech sales budget helps in estimation of product production for

achieve the sales goal and targets.

As per Imda tech sales budget beneficial for achieve zero west production.

Sales budget is helpful in relocated of resources for increasing production of the

company

Disadvantage of sales budget :-

According the forecasters present time sales budget can't efficaciously forecast the

market trends

As per Imda tech sales budget can not much more beneficial in this competitive

market because customer are very fast switch from company to another.

Sales budget is highly expansive and time consuming process because more human

resource require for customer feedback and survey for forecasting.

According Imda tech in sales management require highly qualified employee for

forecasting.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Production budget :-

Production budget means calculation or forecasting number of product unit produce or

manufacture for as per the market and customers demands with good quality and just in time

strategy with low inventory investment and covers all government rules and regulation for

running a successful organization (Ball, 2013).

Advantages of production budgets:-

According Imda tech production budget helps in reduce inventory storehouse costs of

the organization because adopts just in time strategy.

As per Imda Tech production budget helps in meet the customers and client demand

on time,

Production budget help in reduce dad stock problems because organization produce

according orders or demands than achieve zero percent dad stock.

According Imda tech production budget help in reduce creditors for the organization.

Disadvantage of production budgets:-

Production budget demerit is reduced employment in market.

Production budget is highly expansive process and time consuming process.

b) Process or method to make the budget statements

Budget is one kind of statement with the help of this the company forecast different kind

of the financial data to make the decisions and strategies for further financial years. In order to

prepare the budget there are particular kinds of the method and steps are there which are

explained as below: Obtaining the data – To prepare the budget very initially data are required due to which

at the first stage the manager obtain and assess reliable facts and figures. After obtaining

all the data and informations needed in the budget preparation the manager move forward

for further step (Seal, 2012). Coordinate data – After obtaining required data, these are coordinated and then arranged

in the proper structure formate which is compulsory for the budget preparation. Hence, at

the second phase of the budgeting process there are data for budget are arrange in the

proper formate which helps to make the budget in effectual manner.

9

Production budget means calculation or forecasting number of product unit produce or

manufacture for as per the market and customers demands with good quality and just in time

strategy with low inventory investment and covers all government rules and regulation for

running a successful organization (Ball, 2013).

Advantages of production budgets:-

According Imda tech production budget helps in reduce inventory storehouse costs of

the organization because adopts just in time strategy.

As per Imda Tech production budget helps in meet the customers and client demand

on time,

Production budget help in reduce dad stock problems because organization produce

according orders or demands than achieve zero percent dad stock.

According Imda tech production budget help in reduce creditors for the organization.

Disadvantage of production budgets:-

Production budget demerit is reduced employment in market.

Production budget is highly expansive process and time consuming process.

b) Process or method to make the budget statements

Budget is one kind of statement with the help of this the company forecast different kind

of the financial data to make the decisions and strategies for further financial years. In order to

prepare the budget there are particular kinds of the method and steps are there which are

explained as below: Obtaining the data – To prepare the budget very initially data are required due to which

at the first stage the manager obtain and assess reliable facts and figures. After obtaining

all the data and informations needed in the budget preparation the manager move forward

for further step (Seal, 2012). Coordinate data – After obtaining required data, these are coordinated and then arranged

in the proper structure formate which is compulsory for the budget preparation. Hence, at

the second phase of the budgeting process there are data for budget are arrange in the

proper formate which helps to make the budget in effectual manner.

9

Prepare raw budget – At this stage, after considering the arranged and formatted data

raw budget statement is made by the responsible manager which will be shown to the

senior authorities. Communicate budget – After making he raw budget for the Imda Tech it is shown to

those managers and seniors who provide approval for implementing (Ward, 2012). In

this, the budget prepared as a raw is to be communicated with the senior managers of the

company and wait for their approval and acceptance. Taking approval – In this stage, when the seniors analyse the raw budget then approval

and permission is to be given to the managers who prepare this within workplace. Budget implementation – At the second last stage of the budget preparation, it is

implemented in the Imda Tech and all the employees and workers follows this for

achieving all the expected and budgeted data. It is the important stage among all the steps

because here it implemented and then followed.

Budget evaluation – At the last implemented budget in the above step is reviewed as well

as evaluated by the top managers that whether the objectives are achieved or not. If the

negative aspects are found then corrective actions are taken (Arroyo, 2012).

c) Different kinds of strategies to assess selling price Cost plus pricing – The method of pricing in which firstly cost of one unit is determined

and then manager go for calculating the price. After assessing cost of each and every unit

the percentage of profit which Imda Tech wants to charge is to be included in cost and

then price derived for selling in the market. For example: If the management of Imda

Tech calculate that cost of one mobile phone charger is 500 GBP and agreed profit is like

as 19% then price will be 500 + 19% = 595 GBP. Absorption cost pricing method – Another method of the pricing is absorption under

which all incurred and associated costs are to be used for making the decision of pricing.

For instance there are variable and fixed cost are like as 400 and 500 GBP respectively

then both are used in such strategy. Marginal cost pricing method – In this kind of method there are only variables as well as

direct costs are considered and on the basis of which further decision for charging prices

10

raw budget statement is made by the responsible manager which will be shown to the

senior authorities. Communicate budget – After making he raw budget for the Imda Tech it is shown to

those managers and seniors who provide approval for implementing (Ward, 2012). In

this, the budget prepared as a raw is to be communicated with the senior managers of the

company and wait for their approval and acceptance. Taking approval – In this stage, when the seniors analyse the raw budget then approval

and permission is to be given to the managers who prepare this within workplace. Budget implementation – At the second last stage of the budget preparation, it is

implemented in the Imda Tech and all the employees and workers follows this for

achieving all the expected and budgeted data. It is the important stage among all the steps

because here it implemented and then followed.

Budget evaluation – At the last implemented budget in the above step is reviewed as well

as evaluated by the top managers that whether the objectives are achieved or not. If the

negative aspects are found then corrective actions are taken (Arroyo, 2012).

c) Different kinds of strategies to assess selling price Cost plus pricing – The method of pricing in which firstly cost of one unit is determined

and then manager go for calculating the price. After assessing cost of each and every unit

the percentage of profit which Imda Tech wants to charge is to be included in cost and

then price derived for selling in the market. For example: If the management of Imda

Tech calculate that cost of one mobile phone charger is 500 GBP and agreed profit is like

as 19% then price will be 500 + 19% = 595 GBP. Absorption cost pricing method – Another method of the pricing is absorption under

which all incurred and associated costs are to be used for making the decision of pricing.

For instance there are variable and fixed cost are like as 400 and 500 GBP respectively

then both are used in such strategy. Marginal cost pricing method – In this kind of method there are only variables as well as

direct costs are considered and on the basis of which further decision for charging prices

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.