Imda Tech: Management Accounting Systems, Planning & Analysis

VerifiedAdded on 2024/06/07

|24

|5076

|396

Report

AI Summary

This management accounting report for Imda Tech Limited covers various aspects of management accounting, including its definition, differences from financial accounting, and the importance of management accounting information for decision-making. It evaluates different management accounting systems like cost accounting, inventory management, job costing, and price optimizing systems, highlighting their benefits and integration within organizational processes. The report includes income statements using absorption and marginal costing methods, reconciles profits, and analyzes the use of different planning tools for budgeting and forecasting. Furthermore, it discusses the Balance Scorecard approach and how management accounting can lead organizations to sustainable success by addressing financial problems, with a critical evaluation of planning tools' effectiveness in this context. The report emphasizes the role of management accounting in improving financial information for better decision-making within Imda Tech Limited.

Management Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction:.............................................................................................................................................................3

Task 1.......................................................................................................................................................................4

P1.........................................................................................................................................................................4

I: Definition of Management Accounting and to distinguish Management Accounting from Financial

Accounting..........................................................................................................................................................4

II: The importance of management accounting information as a decision making tool for department

managers..............................................................................................................................................................4

P2. Explain the different types of Management Accounting Systems................................................................6

M1. Evaluate the benefits of management accounting systems and their application within the context of

Imda Tech (UK) Limited.....................................................................................................................................7

D1. Critically evaluate how management accounting systems and management accounting reporting is

integrated within organisational processes..........................................................................................................8

Task 2.......................................................................................................................................................................9

P3. Income statements of September using; Absorption costing and Marginal costing.....................................9

M2. Calculate income Reconcile the profits.....................................................................................................11

D2. Accurate apply and interpret the data for the business activities...............................................................12

Task 3.....................................................................................................................................................................13

P4. Provide a written report on planning tools..................................................................................................13

M3 you will need to analyse the use of the different planning and their application for preparing and

forecasting budgets............................................................................................................................................15

Task 4:....................................................................................................................................................................16

Balance scorecard:.............................................................................................................................................16

M4 you will need to analyse how, in responding to financial problems, management accounting can lead

organisations to sustainable success..................................................................................................................19

D3: you will need to evaluate how planning tools for accounting respond appropriately to solving financial

problems to lead to sustainable success.`..........................................................................................................20

Conclusion:............................................................................................................................................................21

References:.............................................................................................................................................................22

2

Introduction:.............................................................................................................................................................3

Task 1.......................................................................................................................................................................4

P1.........................................................................................................................................................................4

I: Definition of Management Accounting and to distinguish Management Accounting from Financial

Accounting..........................................................................................................................................................4

II: The importance of management accounting information as a decision making tool for department

managers..............................................................................................................................................................4

P2. Explain the different types of Management Accounting Systems................................................................6

M1. Evaluate the benefits of management accounting systems and their application within the context of

Imda Tech (UK) Limited.....................................................................................................................................7

D1. Critically evaluate how management accounting systems and management accounting reporting is

integrated within organisational processes..........................................................................................................8

Task 2.......................................................................................................................................................................9

P3. Income statements of September using; Absorption costing and Marginal costing.....................................9

M2. Calculate income Reconcile the profits.....................................................................................................11

D2. Accurate apply and interpret the data for the business activities...............................................................12

Task 3.....................................................................................................................................................................13

P4. Provide a written report on planning tools..................................................................................................13

M3 you will need to analyse the use of the different planning and their application for preparing and

forecasting budgets............................................................................................................................................15

Task 4:....................................................................................................................................................................16

Balance scorecard:.............................................................................................................................................16

M4 you will need to analyse how, in responding to financial problems, management accounting can lead

organisations to sustainable success..................................................................................................................19

D3: you will need to evaluate how planning tools for accounting respond appropriately to solving financial

problems to lead to sustainable success.`..........................................................................................................20

Conclusion:............................................................................................................................................................21

References:.............................................................................................................................................................22

2

Introduction:

Being the trainee management accountant of the Imda Tech Limited, which is the producer of

the mobile telephone charger and the other gadgets for the retail outlets in UK, needs to

improve their financial information for the better decision making. According to the director

of finance, Mr Imda wants a report which should include the meaning of management

accounting and their difference with the financial accounting. The report includes the

different types of management accounting tools such as cost accounting systems, inventory

management systems, job costing systems and price optimising system. The report should

also state the importance of the management accounting system and how it integrates with the

organisational process. In this report, the calculation of marginal and absorption costing is

explained. In this report, it will also explain that departments should take the responsibility to

make budgets. The process of budget and pricing strategies are explained in this report. The

report also explains about the Balance Score Card Approach and how it helps in identifying

the financial problem.

3

Being the trainee management accountant of the Imda Tech Limited, which is the producer of

the mobile telephone charger and the other gadgets for the retail outlets in UK, needs to

improve their financial information for the better decision making. According to the director

of finance, Mr Imda wants a report which should include the meaning of management

accounting and their difference with the financial accounting. The report includes the

different types of management accounting tools such as cost accounting systems, inventory

management systems, job costing systems and price optimising system. The report should

also state the importance of the management accounting system and how it integrates with the

organisational process. In this report, the calculation of marginal and absorption costing is

explained. In this report, it will also explain that departments should take the responsibility to

make budgets. The process of budget and pricing strategies are explained in this report. The

report also explains about the Balance Score Card Approach and how it helps in identifying

the financial problem.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Task 1

P1.

I: Definition of Management Accounting and to distinguish Management Accounting

from Financial Accounting

Management accounting gives the information, records accounting data and helps in taking

the decisions regarding the financial matters. Management accounting does the proper

planning of the management and helps in improving the performance of the company and

achieving the organization strategy (REZNIQI, et. Al., 2015). It helps in giving the

information of the statistical data and also maintains the internal and external factors.

Management accounting Financial accounting

It gives the information to the people within

an organisation.

It gives the information to people outside

the organisation.

It is concerned with the products and cost

centres of the particular factor.

It is concerned with the entire organisation.

The report emphasis on the problems which

are occurring in the organisation and how to

solve them.

The report's emphasis on the profitability

and increases the efficiency of the business.

It can be measured in both the terms

quantitative and qualitative.

It can be measured in only quantitative

terms.

It doesn’t follow any rule and there is no

statutory requirement for this accounting.

This accounting has been prepared as per

the rules of GAAP or IFRS and it is

mandatory to be prepared by all the

companies.

4

P1.

I: Definition of Management Accounting and to distinguish Management Accounting

from Financial Accounting

Management accounting gives the information, records accounting data and helps in taking

the decisions regarding the financial matters. Management accounting does the proper

planning of the management and helps in improving the performance of the company and

achieving the organization strategy (REZNIQI, et. Al., 2015). It helps in giving the

information of the statistical data and also maintains the internal and external factors.

Management accounting Financial accounting

It gives the information to the people within

an organisation.

It gives the information to people outside

the organisation.

It is concerned with the products and cost

centres of the particular factor.

It is concerned with the entire organisation.

The report emphasis on the problems which

are occurring in the organisation and how to

solve them.

The report's emphasis on the profitability

and increases the efficiency of the business.

It can be measured in both the terms

quantitative and qualitative.

It can be measured in only quantitative

terms.

It doesn’t follow any rule and there is no

statutory requirement for this accounting.

This accounting has been prepared as per

the rules of GAAP or IFRS and it is

mandatory to be prepared by all the

companies.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

II: The importance of management accounting information as a decision-making tool

for department managers.

According to a Peter Drucker, a business can be successful only if the management has taken

the courageous decision.

i. Management accounting helps in taking the internal and external; decisions of the

business. Internal changes such as hierarchical change, changes on a global value,

mergers and acquisition, etc. External changes such as election, new policy and law

are created, etc. management helps in guiding how to take decisions when such

situations are arising.

ii. Management accounting collects the data and compares it with the current

performance so that we can analyse the performance of the company and take

decisions accordingly (Malmi, 2016).

iii. Management accounting uses various tools and techniques which helps in taking the

decisions and reduces the problems such as KPI, MIS, Balanced Scorecard, etc.

iv. Management accounting helps in analysing the expenses and revenues of the

company and also created budgets which help in taking the decisions.

5

for department managers.

According to a Peter Drucker, a business can be successful only if the management has taken

the courageous decision.

i. Management accounting helps in taking the internal and external; decisions of the

business. Internal changes such as hierarchical change, changes on a global value,

mergers and acquisition, etc. External changes such as election, new policy and law

are created, etc. management helps in guiding how to take decisions when such

situations are arising.

ii. Management accounting collects the data and compares it with the current

performance so that we can analyse the performance of the company and take

decisions accordingly (Malmi, 2016).

iii. Management accounting uses various tools and techniques which helps in taking the

decisions and reduces the problems such as KPI, MIS, Balanced Scorecard, etc.

iv. Management accounting helps in analysing the expenses and revenues of the

company and also created budgets which help in taking the decisions.

5

P2. Explain the different types of Management Accounting Systems

Cost accounting systems: This system helps in determining the cost of the company. It

estimates the profit, inventory valuation and also controls the cost of the company. Actual

cost is based on the product cost of material, labour and overhead (acharya, 2018). Normal

costing is used to derive the cost of the manufactured product. Standard cost is compared

with the actual cost they are the predetermined cost of the goods and services.

Inventory management systems: This cost includes the holding, ordering and managing the

stock of the business. To manage the inventory is very essential for any organisation. This

system controls the overseeing of ordering inventory, manages the storage of inventory and

also controls the price of the product of inventory (Ngubane, et. Al., 2015).

Job costing systems: This system involves a process which determines the cost of the

specific job or production. It tracks the cost of the labour. It assigns the indirect cost such as

depreciation, rent, etc. to more cost pools (Ingram, 2018).

Price optimising systems: It is a process through which it is analysed how the customer's

will response on different prices of goods and services. This system helps in meeting the

objectives of the company of maximising the operating profit. It is used in the company to

analyse the big data.

6

Cost accounting systems: This system helps in determining the cost of the company. It

estimates the profit, inventory valuation and also controls the cost of the company. Actual

cost is based on the product cost of material, labour and overhead (acharya, 2018). Normal

costing is used to derive the cost of the manufactured product. Standard cost is compared

with the actual cost they are the predetermined cost of the goods and services.

Inventory management systems: This cost includes the holding, ordering and managing the

stock of the business. To manage the inventory is very essential for any organisation. This

system controls the overseeing of ordering inventory, manages the storage of inventory and

also controls the price of the product of inventory (Ngubane, et. Al., 2015).

Job costing systems: This system involves a process which determines the cost of the

specific job or production. It tracks the cost of the labour. It assigns the indirect cost such as

depreciation, rent, etc. to more cost pools (Ingram, 2018).

Price optimising systems: It is a process through which it is analysed how the customer's

will response on different prices of goods and services. This system helps in meeting the

objectives of the company of maximising the operating profit. It is used in the company to

analyse the big data.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

M1. Evaluate benefits of management accounting within the context of Imda Tech (UK)

Management accounting helps in preparing the plan and executing the same plan in

the operations of the business. Budgets are prepared for making a plan for the future

and to forecast the unexpected event.

Management accounting helps in comparing the actual performance of the company

Imda Tech (UK) Limited with the standard or planned performance. If any deviations

are found then manage and control them with the help of standard costing and

budgetary control (Guinea, 2016).

Management accounting helps in improving the efficiency of the company by

eliminating the wastage, defectives and reducing the inefficiency and problems of the

company.

Management accounting helps in formulating the decisions and it also measures the

profit and put a value on inventory (Matambele, 2014).

Management accounting helps in solving the problem by monitoring the performance

of the company Imda Tech (UK) Limited.

Management accounting improves the communication between the different

departments and improved the coordination and integration of the activities of the

business.

7

Management accounting helps in preparing the plan and executing the same plan in

the operations of the business. Budgets are prepared for making a plan for the future

and to forecast the unexpected event.

Management accounting helps in comparing the actual performance of the company

Imda Tech (UK) Limited with the standard or planned performance. If any deviations

are found then manage and control them with the help of standard costing and

budgetary control (Guinea, 2016).

Management accounting helps in improving the efficiency of the company by

eliminating the wastage, defectives and reducing the inefficiency and problems of the

company.

Management accounting helps in formulating the decisions and it also measures the

profit and put a value on inventory (Matambele, 2014).

Management accounting helps in solving the problem by monitoring the performance

of the company Imda Tech (UK) Limited.

Management accounting improves the communication between the different

departments and improved the coordination and integration of the activities of the

business.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

D1. Critically evaluate how management accounting systems and management

accounting reporting is integrated within organisational processes.

Management accounting system is integrated with the accounting reports because it deals

with the monetary factors of the company and accounting reports deals with the quantitative

terms. Integrated accounting system records the transaction of the company and gives the

financial information of the company. Management accounting controls the organisation

functions of the company (Matambele, 2014). It helps in reaching the goals of the entity and

serves the strategic objectives of the company. Management accounting helps in preparing

the report such as job cost reports, inventory report, manufacturing and production report, etc.

which helps the organisation to evaluate the cost and perform the functions of the business

accurately. Management accounting records give the mathematical data of the company such

as balance sheet, income statement, cash flows, etc. through which we can find out the

financial position of the organisation.

8

accounting reporting is integrated within organisational processes.

Management accounting system is integrated with the accounting reports because it deals

with the monetary factors of the company and accounting reports deals with the quantitative

terms. Integrated accounting system records the transaction of the company and gives the

financial information of the company. Management accounting controls the organisation

functions of the company (Matambele, 2014). It helps in reaching the goals of the entity and

serves the strategic objectives of the company. Management accounting helps in preparing

the report such as job cost reports, inventory report, manufacturing and production report, etc.

which helps the organisation to evaluate the cost and perform the functions of the business

accurately. Management accounting records give the mathematical data of the company such

as balance sheet, income statement, cash flows, etc. through which we can find out the

financial position of the organisation.

8

Task 2

P3. Income statements of September using; Absorption costing and Marginal costing

Cost: term of cost can be explained as a monetary value which is paid by a person to get

something in ownership. It is a crucial matter for every business and various methods are

applied to measure and manage cost issues. On the basis of nature Different type of costs is as

follows:

Fixed cost: fixed cost can be defined as a period cost which doesn’t change with

production volume or sales volume. For example, the rent which remains same for a

period.

Variable costs: variable cost is those expenses which occur according to the volume.

For example, variable production overheads which occur according to the production

units.

Absorption costing: method of absorption costing is that which is applied to ascertain the cost

by including overall cost as product cost. This method comprises all flexible and fixed

charges as product charge if they are related to production (Medeiros, et. Al., 2017).

Absorption method of cost determination is a most useful method and it is also accepted

under accounting principles.

Marginal costing: marginal method of costing is applied to ascertain the cost of a product by

including only variable expenses as a cost which means that all fixed expenses are charged as

a period cost (S, 2018). This method is appropriate for budgeting purpose because it displays

costs in a wider manner.

9

P3. Income statements of September using; Absorption costing and Marginal costing

Cost: term of cost can be explained as a monetary value which is paid by a person to get

something in ownership. It is a crucial matter for every business and various methods are

applied to measure and manage cost issues. On the basis of nature Different type of costs is as

follows:

Fixed cost: fixed cost can be defined as a period cost which doesn’t change with

production volume or sales volume. For example, the rent which remains same for a

period.

Variable costs: variable cost is those expenses which occur according to the volume.

For example, variable production overheads which occur according to the production

units.

Absorption costing: method of absorption costing is that which is applied to ascertain the cost

by including overall cost as product cost. This method comprises all flexible and fixed

charges as product charge if they are related to production (Medeiros, et. Al., 2017).

Absorption method of cost determination is a most useful method and it is also accepted

under accounting principles.

Marginal costing: marginal method of costing is applied to ascertain the cost of a product by

including only variable expenses as a cost which means that all fixed expenses are charged as

a period cost (S, 2018). This method is appropriate for budgeting purpose because it displays

costs in a wider manner.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

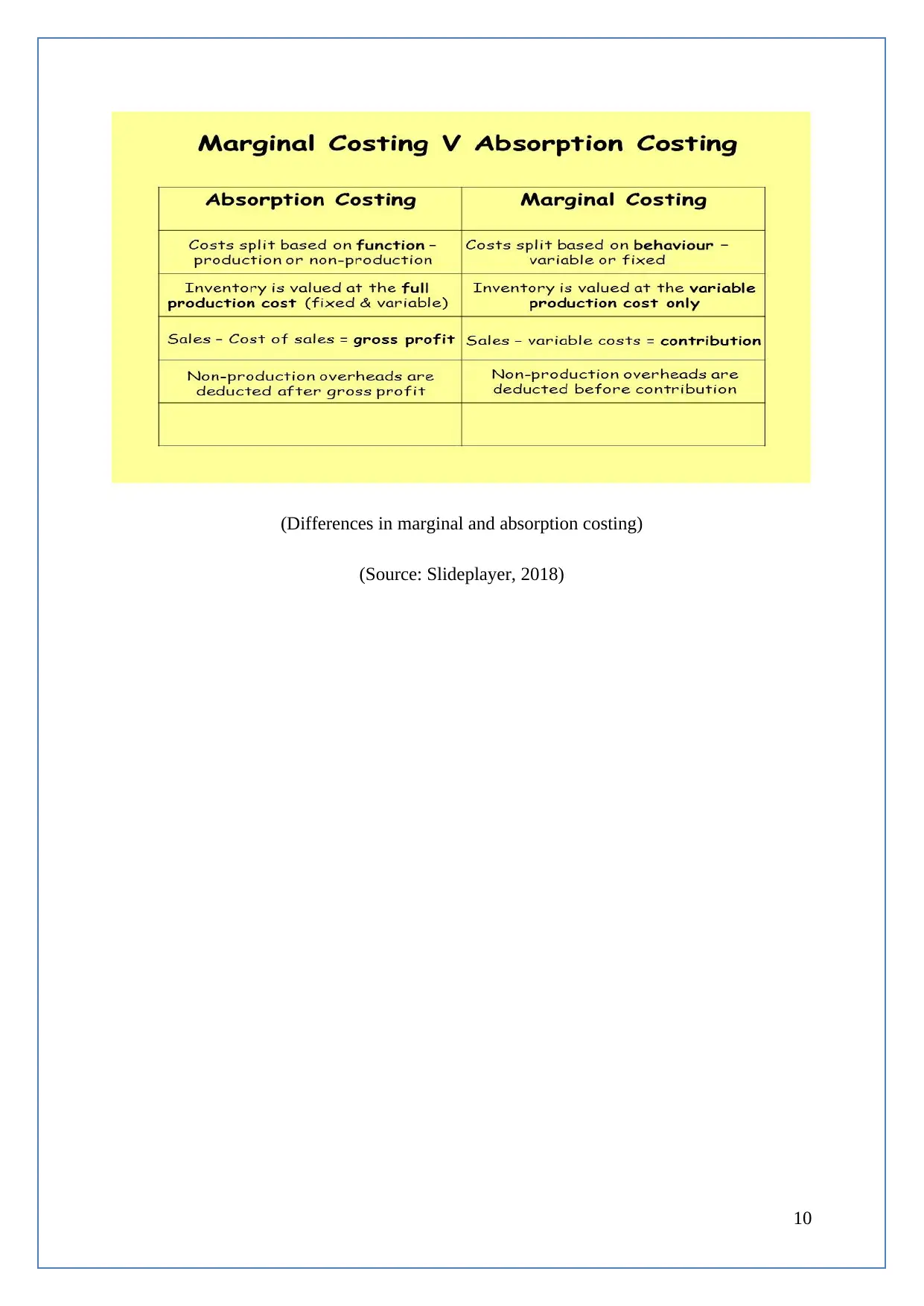

(Differences in marginal and absorption costing)

(Source: Slideplayer, 2018)

10

(Source: Slideplayer, 2018)

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

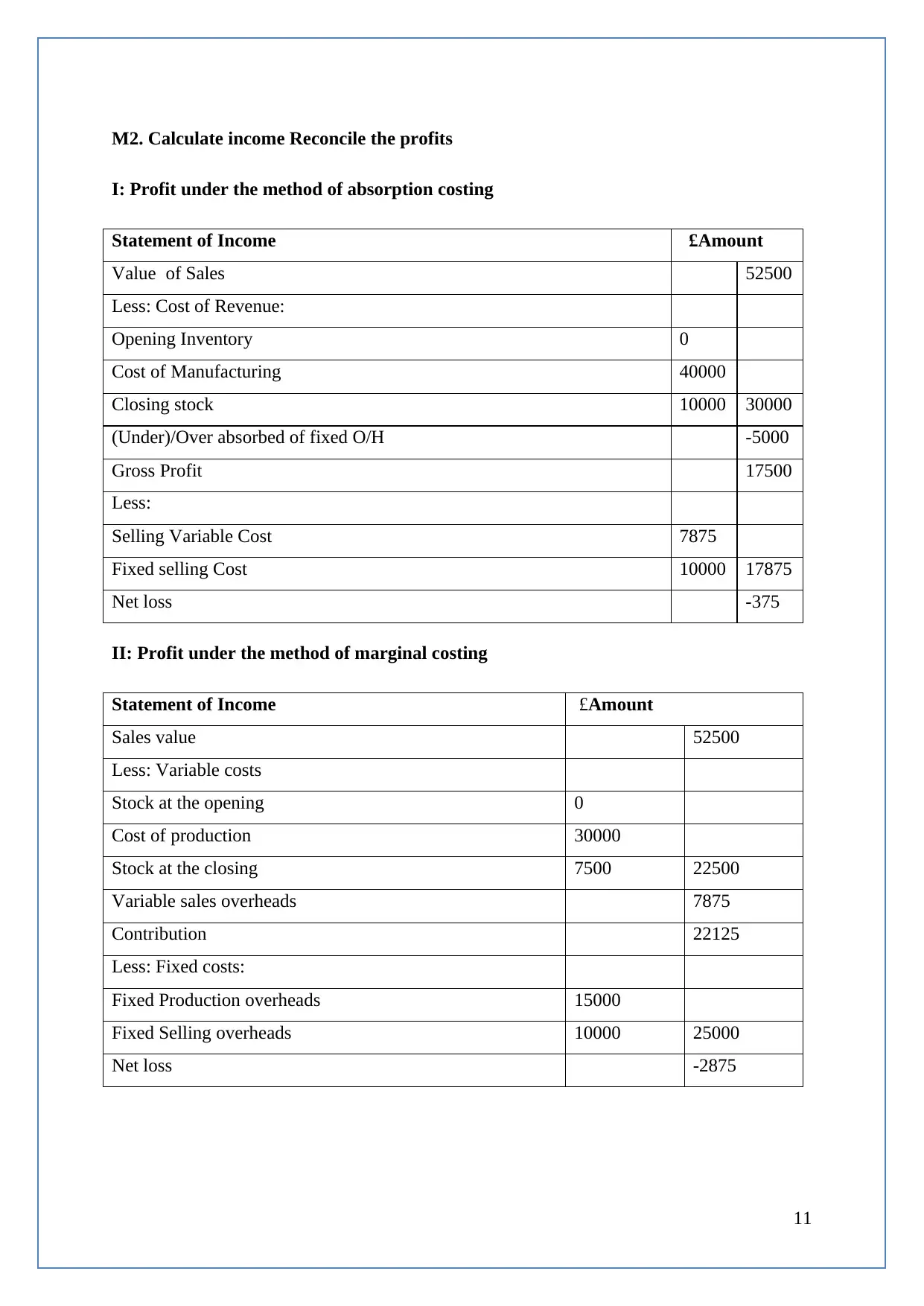

M2. Calculate income Reconcile the profits

I: Profit under the method of absorption costing

Statement of Income £Amount

Value of Sales 52500

Less: Cost of Revenue:

Opening Inventory 0

Cost of Manufacturing 40000

Closing stock 10000 30000

(Under)/Over absorbed of fixed O/H -5000

Gross Profit 17500

Less:

Selling Variable Cost 7875

Fixed selling Cost 10000 17875

Net loss -375

II: Profit under the method of marginal costing

Statement of Income £Amount

Sales value 52500

Less: Variable costs

Stock at the opening 0

Cost of production 30000

Stock at the closing 7500 22500

Variable sales overheads 7875

Contribution 22125

Less: Fixed costs:

Fixed Production overheads 15000

Fixed Selling overheads 10000 25000

Net loss -2875

11

I: Profit under the method of absorption costing

Statement of Income £Amount

Value of Sales 52500

Less: Cost of Revenue:

Opening Inventory 0

Cost of Manufacturing 40000

Closing stock 10000 30000

(Under)/Over absorbed of fixed O/H -5000

Gross Profit 17500

Less:

Selling Variable Cost 7875

Fixed selling Cost 10000 17875

Net loss -375

II: Profit under the method of marginal costing

Statement of Income £Amount

Sales value 52500

Less: Variable costs

Stock at the opening 0

Cost of production 30000

Stock at the closing 7500 22500

Variable sales overheads 7875

Contribution 22125

Less: Fixed costs:

Fixed Production overheads 15000

Fixed Selling overheads 10000 25000

Net loss -2875

11

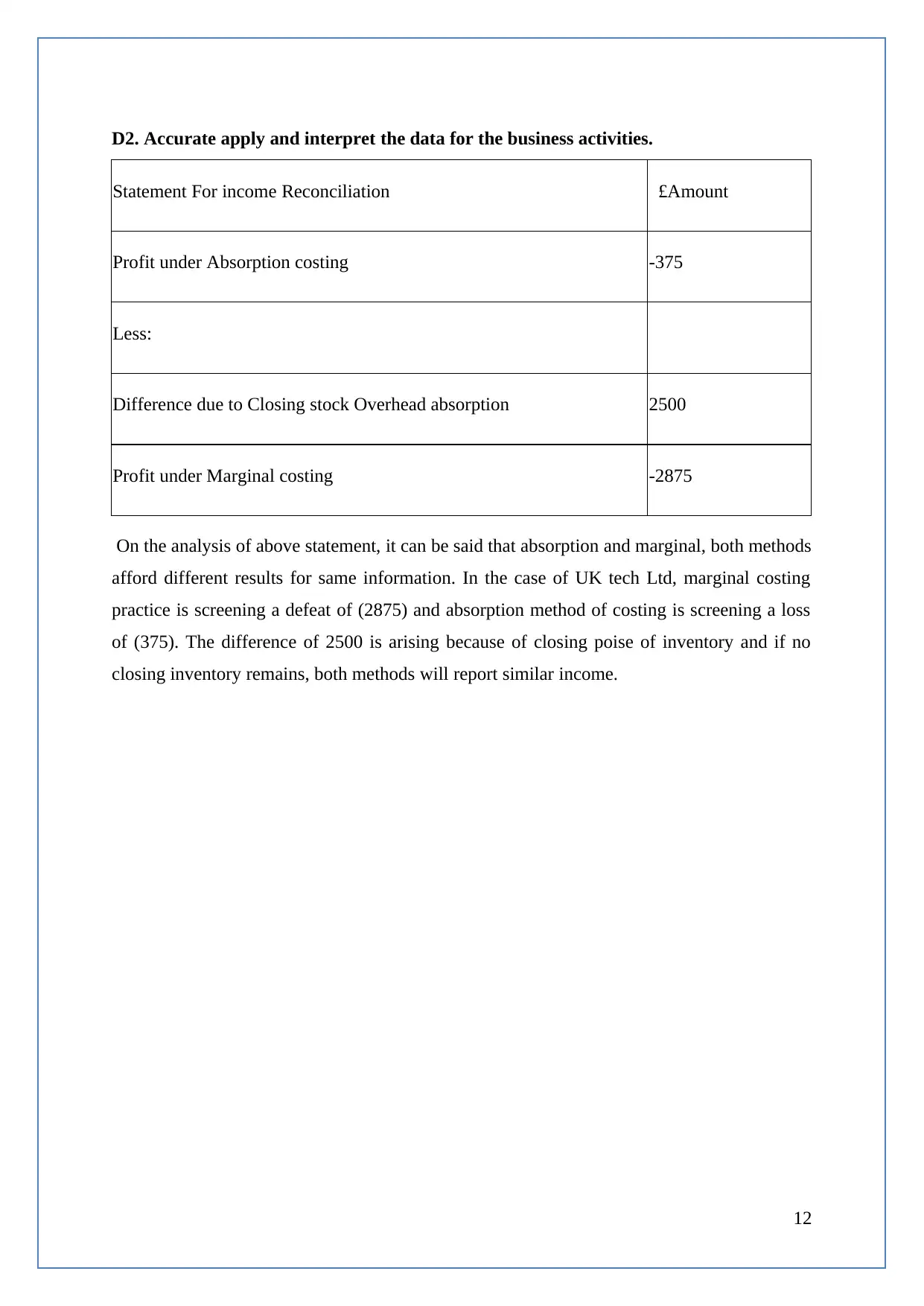

D2. Accurate apply and interpret the data for the business activities.

Statement For income Reconciliation £Amount

Profit under Absorption costing -375

Less:

Difference due to Closing stock Overhead absorption 2500

Profit under Marginal costing -2875

On the analysis of above statement, it can be said that absorption and marginal, both methods

afford different results for same information. In the case of UK tech Ltd, marginal costing

practice is screening a defeat of (2875) and absorption method of costing is screening a loss

of (375). The difference of 2500 is arising because of closing poise of inventory and if no

closing inventory remains, both methods will report similar income.

12

Statement For income Reconciliation £Amount

Profit under Absorption costing -375

Less:

Difference due to Closing stock Overhead absorption 2500

Profit under Marginal costing -2875

On the analysis of above statement, it can be said that absorption and marginal, both methods

afford different results for same information. In the case of UK tech Ltd, marginal costing

practice is screening a defeat of (2875) and absorption method of costing is screening a loss

of (375). The difference of 2500 is arising because of closing poise of inventory and if no

closing inventory remains, both methods will report similar income.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.