Management Accounting Report: Imda Tech Financial Performance Analysis

VerifiedAdded on 2019/12/28

|17

|5015

|49

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles applied to Imda Tech, a UK-based charger and gadgets company. It begins with an introduction to management accounting, emphasizing its role in financial record-keeping, performance evaluation, and decision-making, particularly for internal stakeholders. Task 1 explores the functions of management accounting and its importance in decision-making for department managers, differentiating it from financial accounting. It also examines various types of management accounting systems, including cost accounting, inventory management, job costing, and price optimization, and their applications. Task 2 focuses on absorption and marginal costing methods, applying them to Imda Tech's financial data to determine production costs, inventory valuation, and profitability. The report includes detailed calculations and comparisons of both methods. Task 3 delves into planning tools, specifically budgeting, exploring different types of budgets, their advantages and disadvantages, and the budget preparation process. It also addresses pricing strategies. Finally, the report examines how management accounting, using the Balance Score Card method, can be used to identify and respond to financial problems, improve financial governance, and develop effective strategies for Imda Tech. The report concludes with a summary of key findings and recommendations.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Management Accounting.................................................................................................................1

INTRODUCTION...........................................................................................................................3

TASK 1 ...........................................................................................................................................3

(A) Functions of management accounting..................................................................................3

(B) Different types of management accounting and their usage by departments to improve

their reports.................................................................................................................................5

TASK 2............................................................................................................................................6

Absorption costing......................................................................................................................7

TASK 3..........................................................................................................................................10

Planning tools............................................................................................................................10

(A) Types of budget and their advantages and disadvantages..................................................10

(B) Process of preparing budgets .............................................................................................11

(C)Pricing strategies: ................................................................................................................12

Management accounting to respond to financial problems by using Balance Score Card

method.......................................................................................................................................13

(1) How it can be used to identify and respond to financial problems.....................................14

(2) Improve financial governance and development of effective strategies...........................15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

Management Accounting.................................................................................................................1

INTRODUCTION...........................................................................................................................3

TASK 1 ...........................................................................................................................................3

(A) Functions of management accounting..................................................................................3

(B) Different types of management accounting and their usage by departments to improve

their reports.................................................................................................................................5

TASK 2............................................................................................................................................6

Absorption costing......................................................................................................................7

TASK 3..........................................................................................................................................10

Planning tools............................................................................................................................10

(A) Types of budget and their advantages and disadvantages..................................................10

(B) Process of preparing budgets .............................................................................................11

(C)Pricing strategies: ................................................................................................................12

Management accounting to respond to financial problems by using Balance Score Card

method.......................................................................................................................................13

(1) How it can be used to identify and respond to financial problems.....................................14

(2) Improve financial governance and development of effective strategies...........................15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION

Management accounting is the method and technique to maintain the financial records

and statements of the company that help to identify and determine actual performance and

financial capability and skills of the company to invest money in the market and developing

business process. Management accounting help to achieve the decided targets and goals of the

company. Financial statements and records through easy to determine financial capability of the

company and employees are easy to take better and effective decision regarding company.

Management accounting in maintain the records only internal transactions of the business not

mention external transactions or public transactions. There is not require any formate to maintain

the records and prepare the financial statements(Baldvinsdottir, 2010). Imda Tech is the charger

and gadgets company in UK there is not provide financial informations to their employees in the

company so employees are not capable to take decision and not properly understand financial

status and position of the company. So company's mangers are want to provide all financial

information to the employees and provide them financial statements so employees are increase

their understanding level regarding company in the financial terms and take better and effective

decision (Ward, 2012).

TASK 1

(A) Functions of management accounting

Definitions of management accounting-

Management accounting is the systematic method of managing overall accounting system

of a Imda technology for appropriate estimation of a cost and capital which occurred in the

organization. Basically management accounting is all about controlling and regulating of all the

financial issues happens in the cited enterprise which means it is a effective source of a acquiring

data and information related to finance(Mitchell, 2010). Apart from this management accounting

is all about controlling of a capital invested in the company by analysing all the relevant facts

and figures with the useful data and information by adopting effective techniques and methods.

In other words management accounting is a method of calculating accurate profits and losses by

considering available assets and liability of the cited organization(Nørreklit, 2010). Last but not

the least it is a appropriate method of identifying the losses faced by the organization by

analysing all the relevant factors essential in a management accounting.

Management accounting is the method and technique to maintain the financial records

and statements of the company that help to identify and determine actual performance and

financial capability and skills of the company to invest money in the market and developing

business process. Management accounting help to achieve the decided targets and goals of the

company. Financial statements and records through easy to determine financial capability of the

company and employees are easy to take better and effective decision regarding company.

Management accounting in maintain the records only internal transactions of the business not

mention external transactions or public transactions. There is not require any formate to maintain

the records and prepare the financial statements(Baldvinsdottir, 2010). Imda Tech is the charger

and gadgets company in UK there is not provide financial informations to their employees in the

company so employees are not capable to take decision and not properly understand financial

status and position of the company. So company's mangers are want to provide all financial

information to the employees and provide them financial statements so employees are increase

their understanding level regarding company in the financial terms and take better and effective

decision (Ward, 2012).

TASK 1

(A) Functions of management accounting

Definitions of management accounting-

Management accounting is the systematic method of managing overall accounting system

of a Imda technology for appropriate estimation of a cost and capital which occurred in the

organization. Basically management accounting is all about controlling and regulating of all the

financial issues happens in the cited enterprise which means it is a effective source of a acquiring

data and information related to finance(Mitchell, 2010). Apart from this management accounting

is all about controlling of a capital invested in the company by analysing all the relevant facts

and figures with the useful data and information by adopting effective techniques and methods.

In other words management accounting is a method of calculating accurate profits and losses by

considering available assets and liability of the cited organization(Nørreklit, 2010). Last but not

the least it is a appropriate method of identifying the losses faced by the organization by

analysing all the relevant factors essential in a management accounting.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

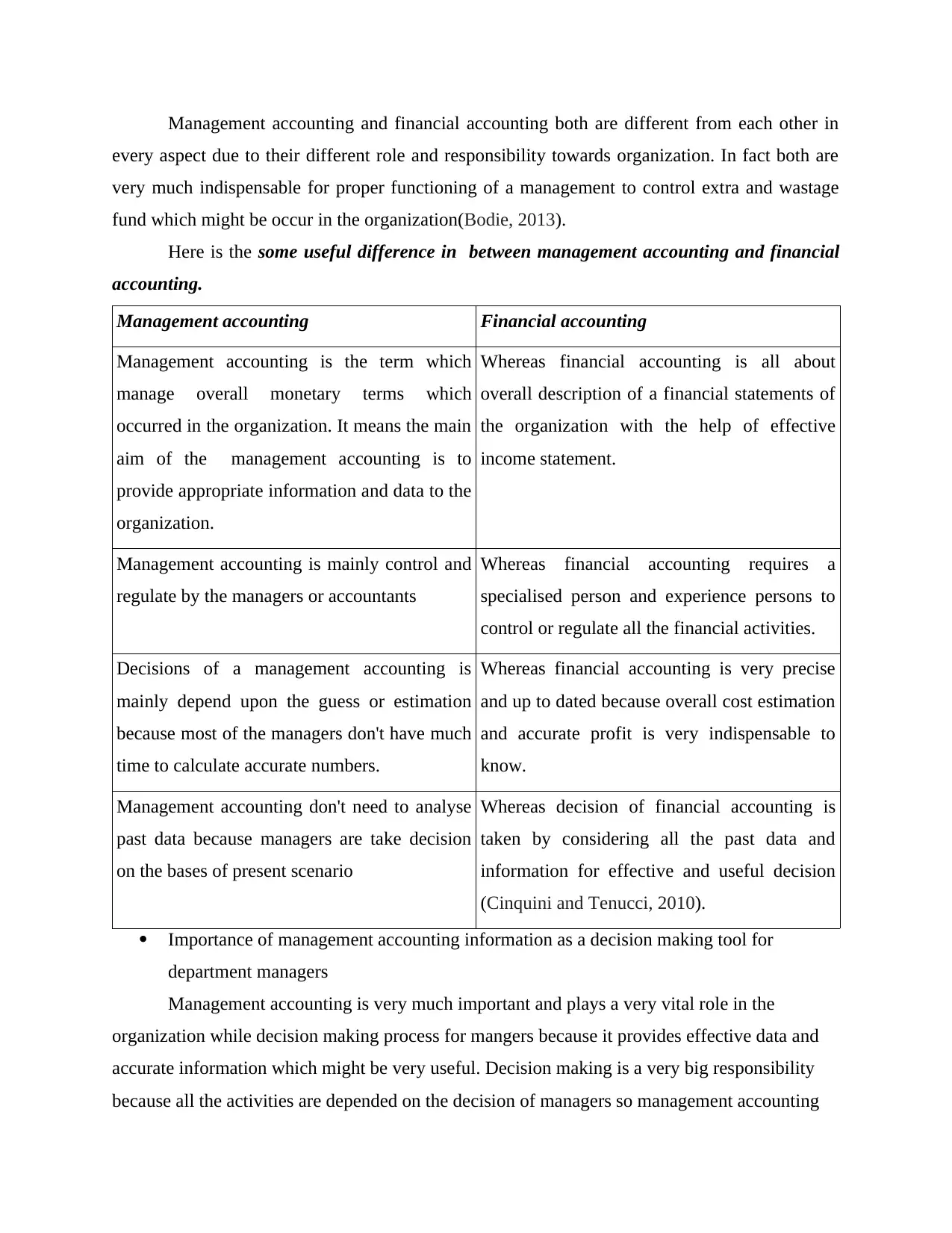

Management accounting and financial accounting both are different from each other in

every aspect due to their different role and responsibility towards organization. In fact both are

very much indispensable for proper functioning of a management to control extra and wastage

fund which might be occur in the organization(Bodie, 2013).

Here is the some useful difference in between management accounting and financial

accounting.

Management accounting Financial accounting

Management accounting is the term which

manage overall monetary terms which

occurred in the organization. It means the main

aim of the management accounting is to

provide appropriate information and data to the

organization.

Whereas financial accounting is all about

overall description of a financial statements of

the organization with the help of effective

income statement.

Management accounting is mainly control and

regulate by the managers or accountants

Whereas financial accounting requires a

specialised person and experience persons to

control or regulate all the financial activities.

Decisions of a management accounting is

mainly depend upon the guess or estimation

because most of the managers don't have much

time to calculate accurate numbers.

Whereas financial accounting is very precise

and up to dated because overall cost estimation

and accurate profit is very indispensable to

know.

Management accounting don't need to analyse

past data because managers are take decision

on the bases of present scenario

Whereas decision of financial accounting is

taken by considering all the past data and

information for effective and useful decision

(Cinquini and Tenucci, 2010).

Importance of management accounting information as a decision making tool for

department managers

Management accounting is very much important and plays a very vital role in the

organization while decision making process for mangers because it provides effective data and

accurate information which might be very useful. Decision making is a very big responsibility

because all the activities are depended on the decision of managers so management accounting

every aspect due to their different role and responsibility towards organization. In fact both are

very much indispensable for proper functioning of a management to control extra and wastage

fund which might be occur in the organization(Bodie, 2013).

Here is the some useful difference in between management accounting and financial

accounting.

Management accounting Financial accounting

Management accounting is the term which

manage overall monetary terms which

occurred in the organization. It means the main

aim of the management accounting is to

provide appropriate information and data to the

organization.

Whereas financial accounting is all about

overall description of a financial statements of

the organization with the help of effective

income statement.

Management accounting is mainly control and

regulate by the managers or accountants

Whereas financial accounting requires a

specialised person and experience persons to

control or regulate all the financial activities.

Decisions of a management accounting is

mainly depend upon the guess or estimation

because most of the managers don't have much

time to calculate accurate numbers.

Whereas financial accounting is very precise

and up to dated because overall cost estimation

and accurate profit is very indispensable to

know.

Management accounting don't need to analyse

past data because managers are take decision

on the bases of present scenario

Whereas decision of financial accounting is

taken by considering all the past data and

information for effective and useful decision

(Cinquini and Tenucci, 2010).

Importance of management accounting information as a decision making tool for

department managers

Management accounting is very much important and plays a very vital role in the

organization while decision making process for mangers because it provides effective data and

accurate information which might be very useful. Decision making is a very big responsibility

because all the activities are depended on the decision of managers so management accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

acts a very useful tool. Apart from this management accounting helps in identifying the hidden

problems and shows the effective method to overcome all the obstacles which comes while

decision making process. In fact decision making process requires a experience managers and

specialised persons because it is a very complex duty for which knowledge skills is very much

important.

Last but not the least management accounting shows the overall description or usage of

capital in the organization for effective decision by considering all the facts and figures. In other

words management accounting act as a very mandatory part in decision making process for all

the managers of different departments because it provides a accurate information and evidences.

At the end it also plays a very eminent role in the cited organization because of their usefulness

and positive results.

(B) Different types of management accounting and their usage by departments to improve

their reports

Cost accounting systems(actual, normal and standard costing) :- Cost accounting systems

is the appropriate method or techniques of determining all the relevant cost which might

be occur while performing all the activities in the organization. The main and foremost

motive of the cost accounting system is to determine overall cost incurred in the

organization to calculate the actual profit and loses earned by the enterprise. In fact this

systems is very helpful in describing the expenses faced by the enterprise with the help of

particular useful method.

Inventory management systems:- Inventory management systems is the term which

shows the overall management of the inventory by determining past and present stock to

avoid extra wastage. Apart from this inventory management controls the extra

manufacturing of a product by considering demand of a product. A cited organization

need to analyse the product demand by proper evaluation of a overall market for effective

management of the inventory by controlling extra stock. In additional inventory

management is a systematic computerised method of getting aware about the demand of a

product in the market.

Job costing systems :- Job costing systems is mainly used to determine the overall cost

incurred in the production of a particular product. Mainly job costing method is applied

by most of the organization just because of their quality of determining all the actual cost

problems and shows the effective method to overcome all the obstacles which comes while

decision making process. In fact decision making process requires a experience managers and

specialised persons because it is a very complex duty for which knowledge skills is very much

important.

Last but not the least management accounting shows the overall description or usage of

capital in the organization for effective decision by considering all the facts and figures. In other

words management accounting act as a very mandatory part in decision making process for all

the managers of different departments because it provides a accurate information and evidences.

At the end it also plays a very eminent role in the cited organization because of their usefulness

and positive results.

(B) Different types of management accounting and their usage by departments to improve

their reports

Cost accounting systems(actual, normal and standard costing) :- Cost accounting systems

is the appropriate method or techniques of determining all the relevant cost which might

be occur while performing all the activities in the organization. The main and foremost

motive of the cost accounting system is to determine overall cost incurred in the

organization to calculate the actual profit and loses earned by the enterprise. In fact this

systems is very helpful in describing the expenses faced by the enterprise with the help of

particular useful method.

Inventory management systems:- Inventory management systems is the term which

shows the overall management of the inventory by determining past and present stock to

avoid extra wastage. Apart from this inventory management controls the extra

manufacturing of a product by considering demand of a product. A cited organization

need to analyse the product demand by proper evaluation of a overall market for effective

management of the inventory by controlling extra stock. In additional inventory

management is a systematic computerised method of getting aware about the demand of a

product in the market.

Job costing systems :- Job costing systems is mainly used to determine the overall cost

incurred in the production of a particular product. Mainly job costing method is applied

by most of the organization just because of their quality of determining all the actual cost

occurred in the organization while manufacturing a product. In fact job costing method

shows the actual cost incurred while performing a particular job to complete a particular

task and activities.

Price optimising systems :- Price optimisation is a mathematical techniques of analysing

price of the product by determining the reaction of a customers towards particular price.

In fact price optimising systems is mainly invented to identify the actual price of the

product by considering all the relevant expenses which might be occurred while

manufacturing a product. Apart from this, this method is used to understand the profit

earned by the organization by introduction of product in the market according to the

customers opinion by meeting their needs and wants. In fact the main motive of this

system is to acquire appropriate data and information to predict the behaviour of the

buyers towards particular price decided by the organization.

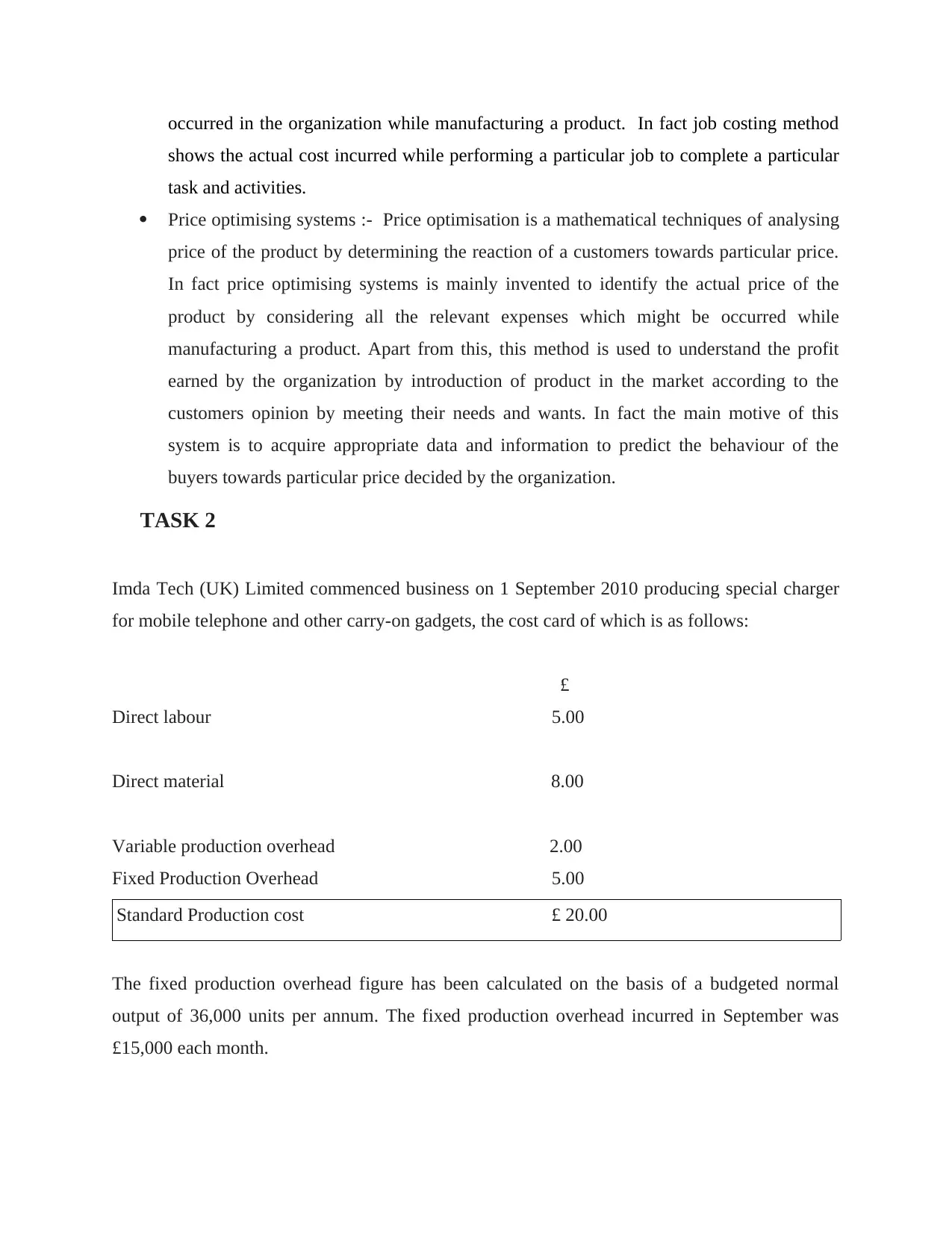

TASK 2

Imda Tech (UK) Limited commenced business on 1 September 2010 producing special charger

for mobile telephone and other carry-on gadgets, the cost card of which is as follows:

£

Direct labour 5.00

Direct material 8.00

Variable production overhead 2.00

Fixed Production Overhead 5.00

Standard Production cost £ 20.00

The fixed production overhead figure has been calculated on the basis of a budgeted normal

output of 36,000 units per annum. The fixed production overhead incurred in September was

£15,000 each month.

shows the actual cost incurred while performing a particular job to complete a particular

task and activities.

Price optimising systems :- Price optimisation is a mathematical techniques of analysing

price of the product by determining the reaction of a customers towards particular price.

In fact price optimising systems is mainly invented to identify the actual price of the

product by considering all the relevant expenses which might be occurred while

manufacturing a product. Apart from this, this method is used to understand the profit

earned by the organization by introduction of product in the market according to the

customers opinion by meeting their needs and wants. In fact the main motive of this

system is to acquire appropriate data and information to predict the behaviour of the

buyers towards particular price decided by the organization.

TASK 2

Imda Tech (UK) Limited commenced business on 1 September 2010 producing special charger

for mobile telephone and other carry-on gadgets, the cost card of which is as follows:

£

Direct labour 5.00

Direct material 8.00

Variable production overhead 2.00

Fixed Production Overhead 5.00

Standard Production cost £ 20.00

The fixed production overhead figure has been calculated on the basis of a budgeted normal

output of 36,000 units per annum. The fixed production overhead incurred in September was

£15,000 each month.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Selling, distribution and administration expenses are:

Fixed £10000 per month

Variable 15% of the sales value

The selling price per unit is £35 and the number of units produced and sold were:

September (Units)

Production 2000

Sales 1500

Absorption costing

Fixed cost for month are give under the below:

Budgeted cost Actual cost

Production overhead £15000 £15000

Administration cost £10000 £10000

Working note 1.

Apportioned of fix cost per unit

£25000/2000= 12.5 per unit

Working note 2.

Calculation of production cost.

Direct material £8

Direct labour £5

Variable cost £2

Prime cost £15

Fixed £10000 per month

Variable 15% of the sales value

The selling price per unit is £35 and the number of units produced and sold were:

September (Units)

Production 2000

Sales 1500

Absorption costing

Fixed cost for month are give under the below:

Budgeted cost Actual cost

Production overhead £15000 £15000

Administration cost £10000 £10000

Working note 1.

Apportioned of fix cost per unit

£25000/2000= 12.5 per unit

Working note 2.

Calculation of production cost.

Direct material £8

Direct labour £5

Variable cost £2

Prime cost £15

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

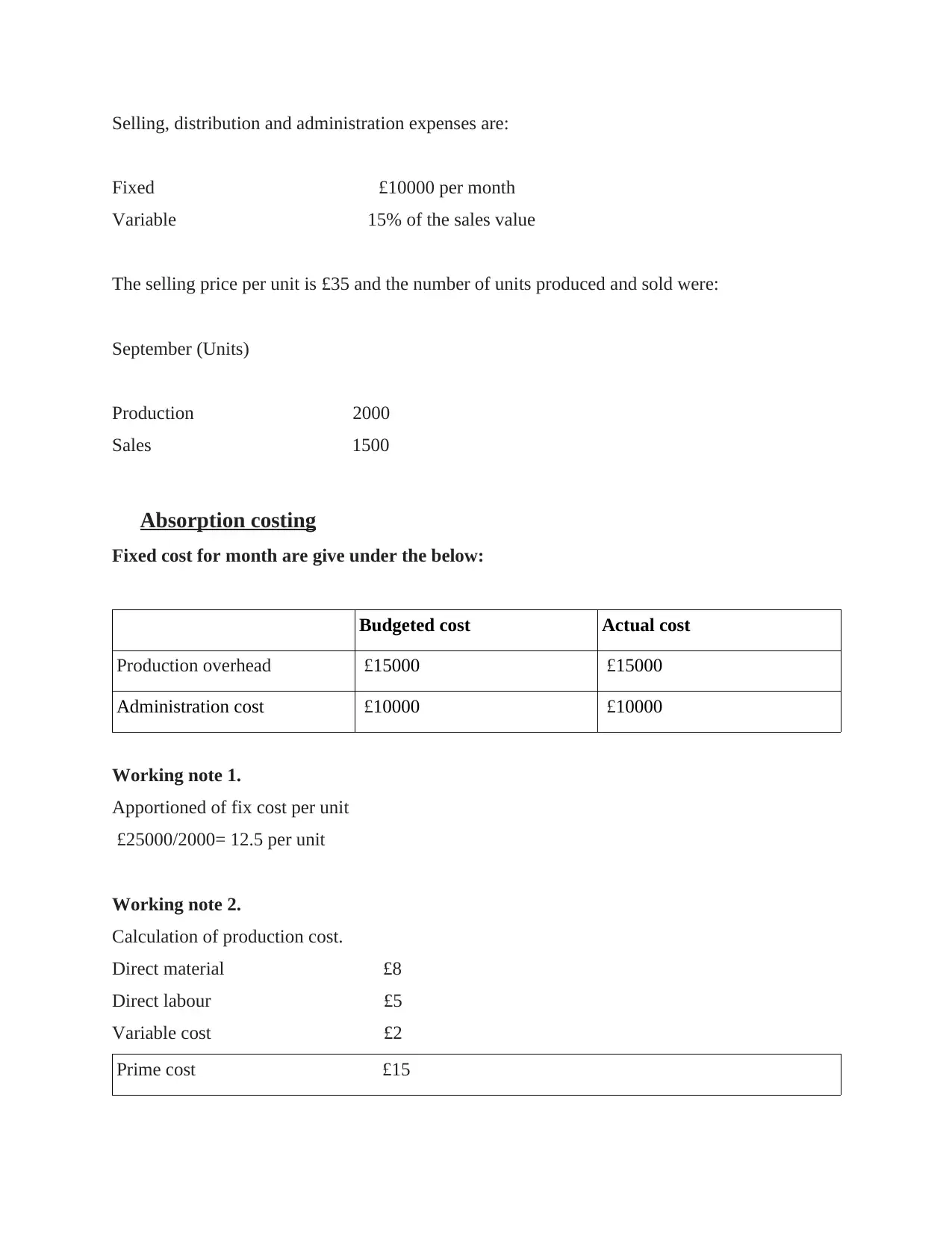

Fixed cost £12.5

Total £ 27.5

Working note 3.

Calculate value of inventory and production

Opening inventory Production Closing inventory

Nil 2000*27.5= £55000 500*27.5= £13750

Working note 4.

Actual fixed production £25000

Fixed overhead £25000

Total Nil

Net profit using absorption cost:

Sales £52500(1500*35)

(-) cost of sales:

Opening inventory 0

Production £55000

Closing inventory ( £13750)

Total cost 41250

Net profit £27500

Absorption costing method through calculate the production cost at per unit, total cost of the

company is £ 27.5, closing inventory of the company is £13750 also calculate and determine the

net profit of the company in this year is £27500 this method help to identify financial position of

the company and help to take better and effective decision by the employees.

Total £ 27.5

Working note 3.

Calculate value of inventory and production

Opening inventory Production Closing inventory

Nil 2000*27.5= £55000 500*27.5= £13750

Working note 4.

Actual fixed production £25000

Fixed overhead £25000

Total Nil

Net profit using absorption cost:

Sales £52500(1500*35)

(-) cost of sales:

Opening inventory 0

Production £55000

Closing inventory ( £13750)

Total cost 41250

Net profit £27500

Absorption costing method through calculate the production cost at per unit, total cost of the

company is £ 27.5, closing inventory of the company is £13750 also calculate and determine the

net profit of the company in this year is £27500 this method help to identify financial position of

the company and help to take better and effective decision by the employees.

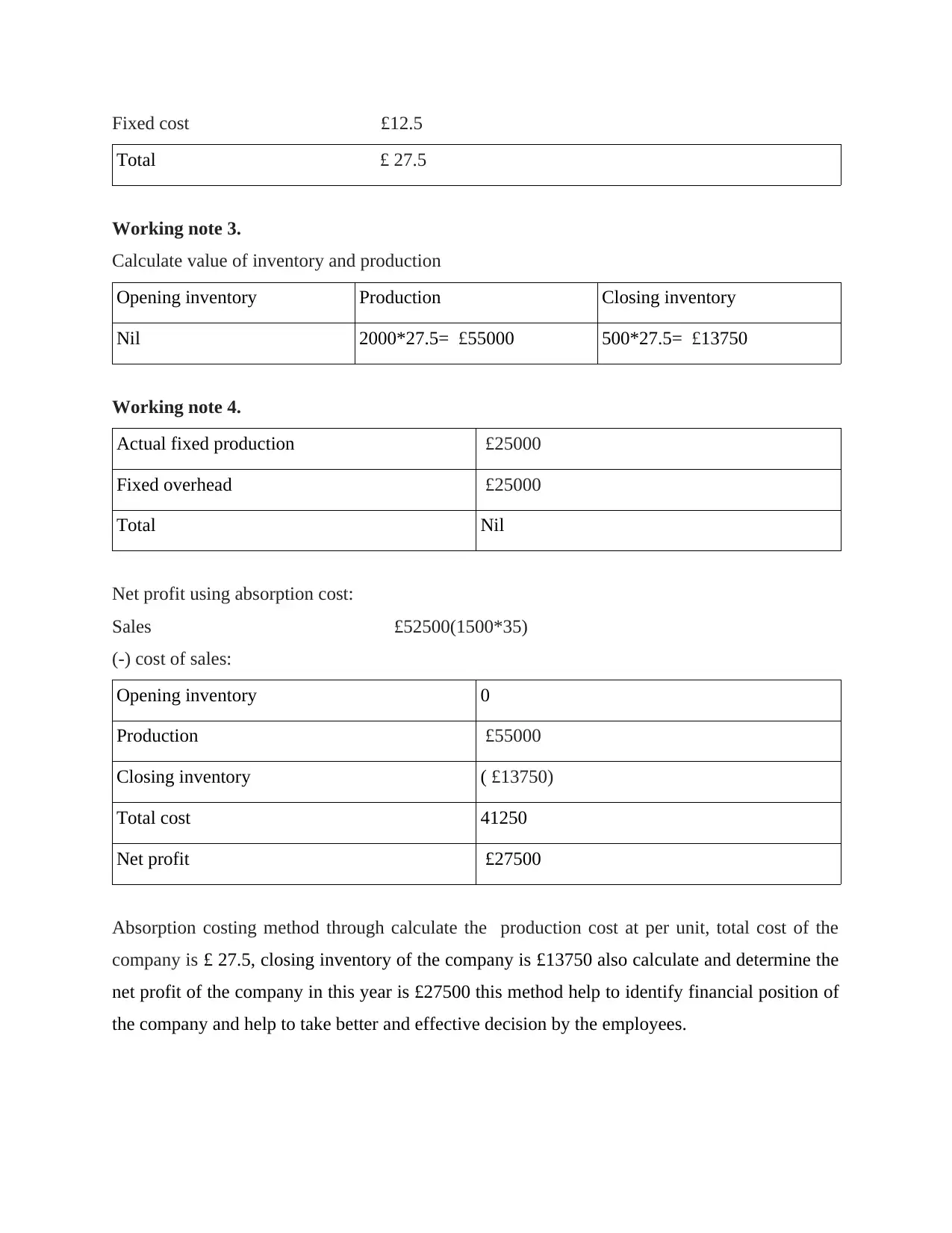

Marginal costing methods

Working note 1.

Calculate variable production cost

Direct material £ 8

Direct labour £ 5

Variable production cost £ 2

Total cost £ 15

Working note 2.

Opening inventory Production Closing inventory

nil 2000*15=30000 500*15=7500

Net profit using marginal costing

Sales £ 52500

Less variable cost

Opening inventory

Production 30000

Closing inventory -2500 -22250

Variable sales -10500

Contribution 12000

Less fixed cost

Fixed production overhead 10000

Selling and admin cost 10000 -12000

Net profit nil

Working note 1.

Calculate variable production cost

Direct material £ 8

Direct labour £ 5

Variable production cost £ 2

Total cost £ 15

Working note 2.

Opening inventory Production Closing inventory

nil 2000*15=30000 500*15=7500

Net profit using marginal costing

Sales £ 52500

Less variable cost

Opening inventory

Production 30000

Closing inventory -2500 -22250

Variable sales -10500

Contribution 12000

Less fixed cost

Fixed production overhead 10000

Selling and admin cost 10000 -12000

Net profit nil

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

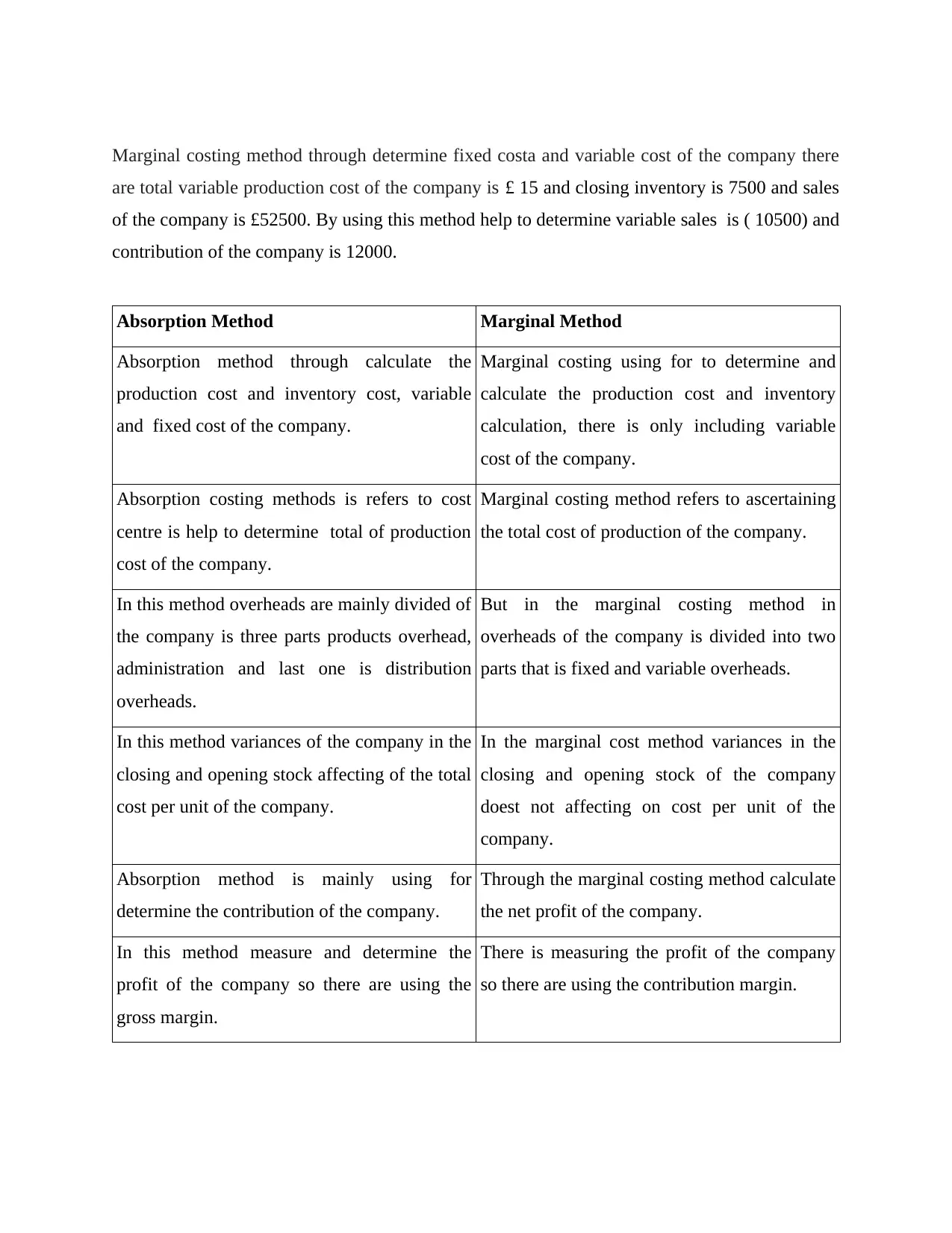

Marginal costing method through determine fixed costa and variable cost of the company there

are total variable production cost of the company is £ 15 and closing inventory is 7500 and sales

of the company is £52500. By using this method help to determine variable sales is ( 10500) and

contribution of the company is 12000.

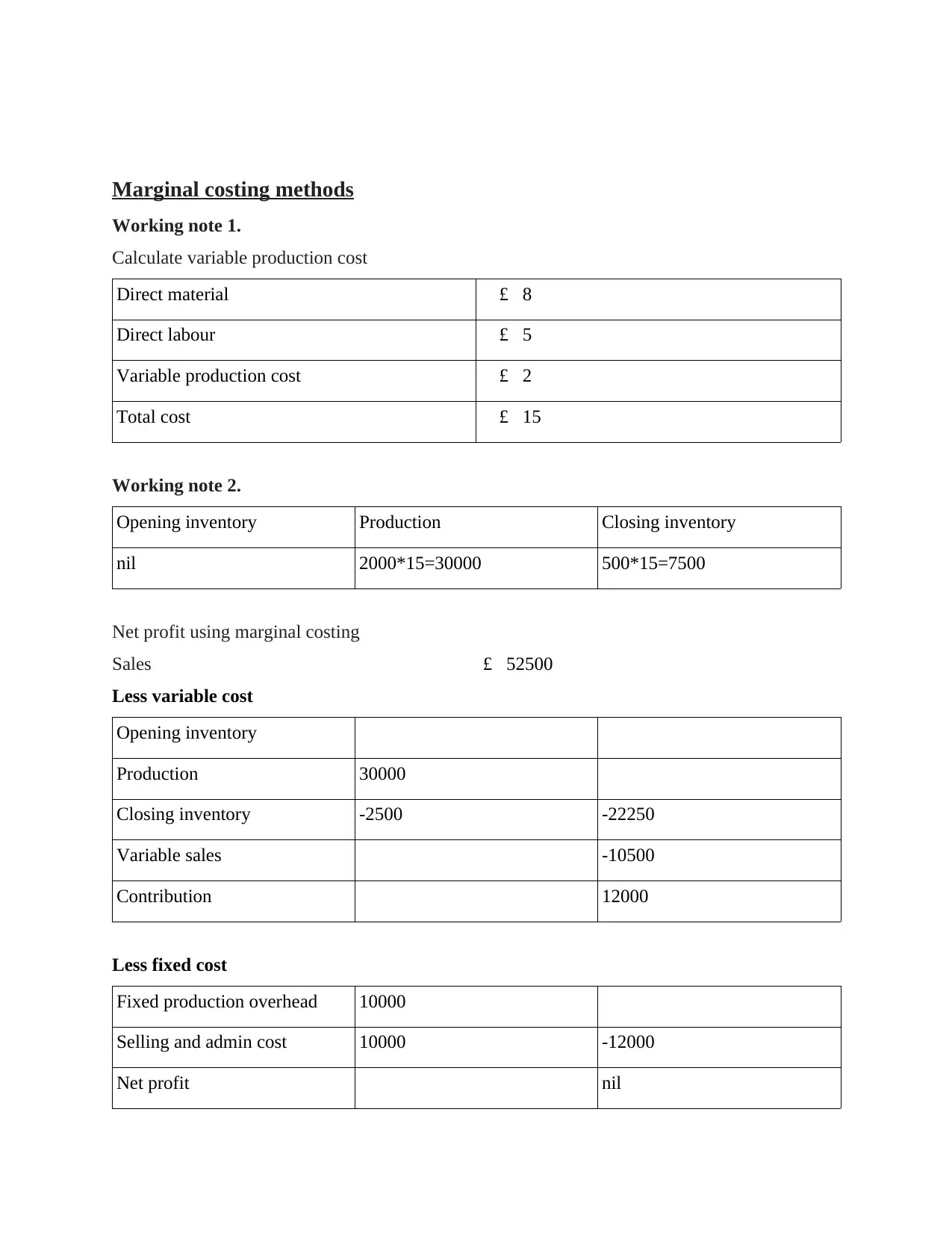

Absorption Method Marginal Method

Absorption method through calculate the

production cost and inventory cost, variable

and fixed cost of the company.

Marginal costing using for to determine and

calculate the production cost and inventory

calculation, there is only including variable

cost of the company.

Absorption costing methods is refers to cost

centre is help to determine total of production

cost of the company.

Marginal costing method refers to ascertaining

the total cost of production of the company.

In this method overheads are mainly divided of

the company is three parts products overhead,

administration and last one is distribution

overheads.

But in the marginal costing method in

overheads of the company is divided into two

parts that is fixed and variable overheads.

In this method variances of the company in the

closing and opening stock affecting of the total

cost per unit of the company.

In the marginal cost method variances in the

closing and opening stock of the company

doest not affecting on cost per unit of the

company.

Absorption method is mainly using for

determine the contribution of the company.

Through the marginal costing method calculate

the net profit of the company.

In this method measure and determine the

profit of the company so there are using the

gross margin.

There is measuring the profit of the company

so there are using the contribution margin.

are total variable production cost of the company is £ 15 and closing inventory is 7500 and sales

of the company is £52500. By using this method help to determine variable sales is ( 10500) and

contribution of the company is 12000.

Absorption Method Marginal Method

Absorption method through calculate the

production cost and inventory cost, variable

and fixed cost of the company.

Marginal costing using for to determine and

calculate the production cost and inventory

calculation, there is only including variable

cost of the company.

Absorption costing methods is refers to cost

centre is help to determine total of production

cost of the company.

Marginal costing method refers to ascertaining

the total cost of production of the company.

In this method overheads are mainly divided of

the company is three parts products overhead,

administration and last one is distribution

overheads.

But in the marginal costing method in

overheads of the company is divided into two

parts that is fixed and variable overheads.

In this method variances of the company in the

closing and opening stock affecting of the total

cost per unit of the company.

In the marginal cost method variances in the

closing and opening stock of the company

doest not affecting on cost per unit of the

company.

Absorption method is mainly using for

determine the contribution of the company.

Through the marginal costing method calculate

the net profit of the company.

In this method measure and determine the

profit of the company so there are using the

gross margin.

There is measuring the profit of the company

so there are using the contribution margin.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

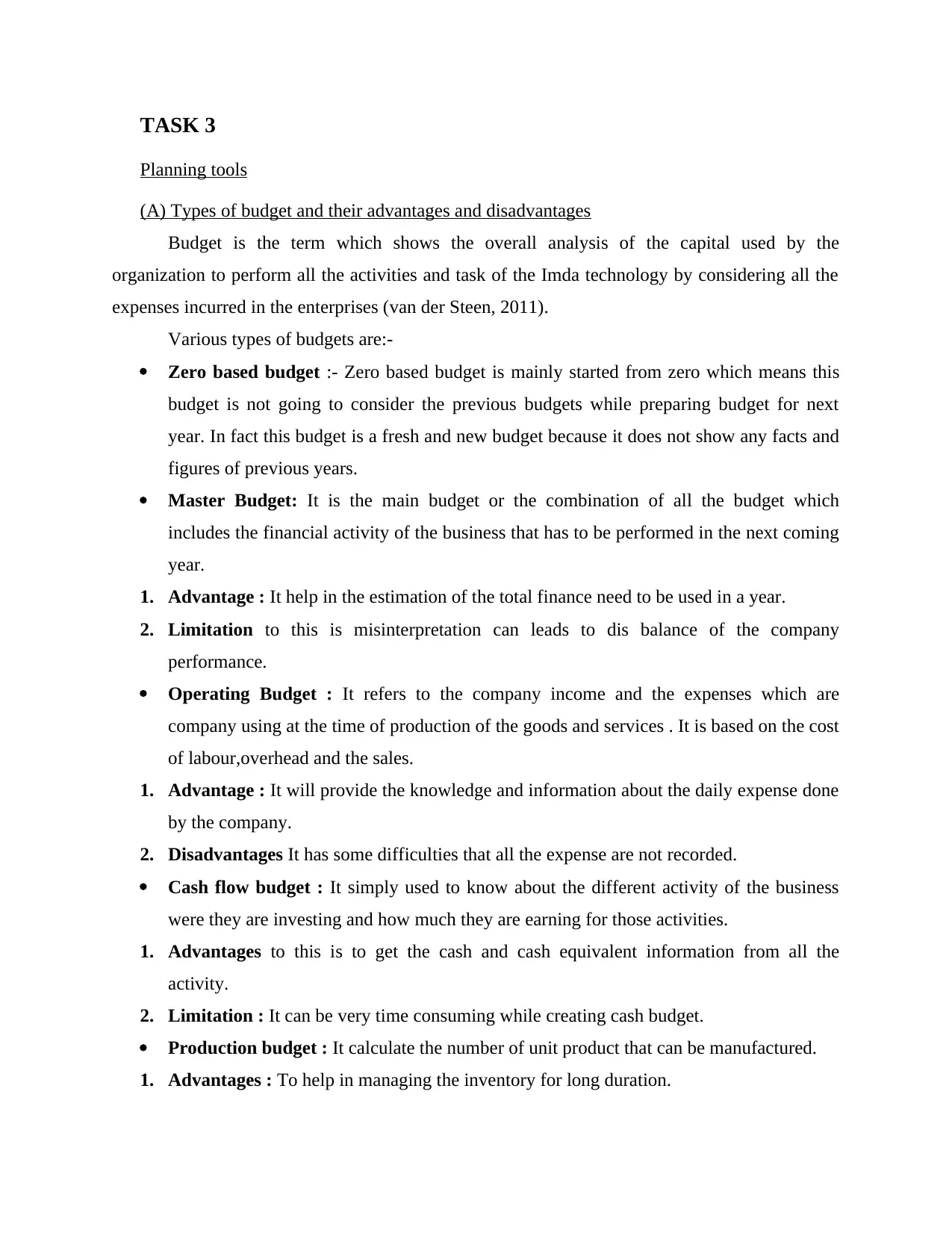

TASK 3

Planning tools

(A) Types of budget and their advantages and disadvantages

Budget is the term which shows the overall analysis of the capital used by the

organization to perform all the activities and task of the Imda technology by considering all the

expenses incurred in the enterprises (van der Steen, 2011).

Various types of budgets are:-

Zero based budget :- Zero based budget is mainly started from zero which means this

budget is not going to consider the previous budgets while preparing budget for next

year. In fact this budget is a fresh and new budget because it does not show any facts and

figures of previous years.

Master Budget: It is the main budget or the combination of all the budget which

includes the financial activity of the business that has to be performed in the next coming

year.

1. Advantage : It help in the estimation of the total finance need to be used in a year.

2. Limitation to this is misinterpretation can leads to dis balance of the company

performance.

Operating Budget : It refers to the company income and the expenses which are

company using at the time of production of the goods and services . It is based on the cost

of labour,overhead and the sales.

1. Advantage : It will provide the knowledge and information about the daily expense done

by the company.

2. Disadvantages It has some difficulties that all the expense are not recorded.

Cash flow budget : It simply used to know about the different activity of the business

were they are investing and how much they are earning for those activities.

1. Advantages to this is to get the cash and cash equivalent information from all the

activity.

2. Limitation : It can be very time consuming while creating cash budget.

Production budget : It calculate the number of unit product that can be manufactured.

1. Advantages : To help in managing the inventory for long duration.

Planning tools

(A) Types of budget and their advantages and disadvantages

Budget is the term which shows the overall analysis of the capital used by the

organization to perform all the activities and task of the Imda technology by considering all the

expenses incurred in the enterprises (van der Steen, 2011).

Various types of budgets are:-

Zero based budget :- Zero based budget is mainly started from zero which means this

budget is not going to consider the previous budgets while preparing budget for next

year. In fact this budget is a fresh and new budget because it does not show any facts and

figures of previous years.

Master Budget: It is the main budget or the combination of all the budget which

includes the financial activity of the business that has to be performed in the next coming

year.

1. Advantage : It help in the estimation of the total finance need to be used in a year.

2. Limitation to this is misinterpretation can leads to dis balance of the company

performance.

Operating Budget : It refers to the company income and the expenses which are

company using at the time of production of the goods and services . It is based on the cost

of labour,overhead and the sales.

1. Advantage : It will provide the knowledge and information about the daily expense done

by the company.

2. Disadvantages It has some difficulties that all the expense are not recorded.

Cash flow budget : It simply used to know about the different activity of the business

were they are investing and how much they are earning for those activities.

1. Advantages to this is to get the cash and cash equivalent information from all the

activity.

2. Limitation : It can be very time consuming while creating cash budget.

Production budget : It calculate the number of unit product that can be manufactured.

1. Advantages : To help in managing the inventory for long duration.

2. Disadvantages :sometime there is no control on the cost incurred in budget.

(B) Process of preparing budgets

Budget process is a appropriate method of preparing a effective budget created by the

government and approved for overall country to achieve their organization goals and objectives.

In fact budget process is a systematic procedure of preparing a effective budget with the help of

useful information and data by analysing all the facts and figures with the use of effective

techniques and methods (Soin and Collier, 2013). Budget is not an easy task as it requires a

experienced person and specialised members for effective implementation of budgets by getting

approval of central and state government by following appropriate procedure. The first and

foremost step in the budget process is to prepare a worksheet by financial service department to

prepare a budget by appropriate estimation. After that second step is to conduct a proper meeting

of all the mangers just to discuss the plans and present in front of them by explaining them

overall plan and cost of the budget to take effective decision. Third step is handled and regulate

by the managers which means they work with financial service department for appropriate

estimation of cost of the overall budget by considering all the facts and figures for upcoming

year.

In fourth step overall budget prepared by the managers is presented and shown to their

executive officers for review or suggest any changes if there is a need of reforms in the budget

plan to get approval. Second last step of preparation of budget is that managers is going to

discuss their budget requirements with their administrative officer for more suggestion if there is

a need of any adjustments (Simons, 2013). At the end budget may be implemented by getting

approval from all the officers and do specific changes or reforms if there is a need of reforms by

considering all the necessary facts and figures. The main motive of the budget is to covers all the

rules and regulation for all the departments of the country. Apart from this if there is a budget

preparation for a cited organization then also these above procedure must be followed to remove

errors and mistakes which might be come while preparing of budgets.

(C)Pricing strategies:

Pricing is the important element to sale products and goods in the market. Price of the

products are decided by the company's head by using m,any methods and strategies. Always

prices are decided with cost of the production as well as profit. To earn the profits company are

always using effective and suitable methods that help to achieve goals and objectives of the

(B) Process of preparing budgets

Budget process is a appropriate method of preparing a effective budget created by the

government and approved for overall country to achieve their organization goals and objectives.

In fact budget process is a systematic procedure of preparing a effective budget with the help of

useful information and data by analysing all the facts and figures with the use of effective

techniques and methods (Soin and Collier, 2013). Budget is not an easy task as it requires a

experienced person and specialised members for effective implementation of budgets by getting

approval of central and state government by following appropriate procedure. The first and

foremost step in the budget process is to prepare a worksheet by financial service department to

prepare a budget by appropriate estimation. After that second step is to conduct a proper meeting

of all the mangers just to discuss the plans and present in front of them by explaining them

overall plan and cost of the budget to take effective decision. Third step is handled and regulate

by the managers which means they work with financial service department for appropriate

estimation of cost of the overall budget by considering all the facts and figures for upcoming

year.

In fourth step overall budget prepared by the managers is presented and shown to their

executive officers for review or suggest any changes if there is a need of reforms in the budget

plan to get approval. Second last step of preparation of budget is that managers is going to

discuss their budget requirements with their administrative officer for more suggestion if there is

a need of any adjustments (Simons, 2013). At the end budget may be implemented by getting

approval from all the officers and do specific changes or reforms if there is a need of reforms by

considering all the necessary facts and figures. The main motive of the budget is to covers all the

rules and regulation for all the departments of the country. Apart from this if there is a budget

preparation for a cited organization then also these above procedure must be followed to remove

errors and mistakes which might be come while preparing of budgets.

(C)Pricing strategies:

Pricing is the important element to sale products and goods in the market. Price of the

products are decided by the company's head by using m,any methods and strategies. Always

prices are decided with cost of the production as well as profit. To earn the profits company are

always using effective and suitable methods that help to achieve goals and objectives of the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.