Comprehensive Management Accounting Report for IMDA Tech Ltd Analysis

VerifiedAdded on 2020/01/28

|16

|4442

|86

Report

AI Summary

This report provides a comprehensive analysis of management accounting practices for IMDA Tech Ltd, a mobile phone charger producer in the UK. The report explores various accounting functions, comparing financial and management accounting, and highlighting the importance of management accounting in determining goals, planning, and performance measurement. It delves into different types of accounting systems like cost accounting, inventory management, job costing, and price optimization. The report further examines the benefits of management accounting, including performance measurement, business efficiency, and planning. It then critically evaluates management accounting and reporting systems and details costing methods used, such as absorption and marginal costing, providing income statements based on both methods. Various financial reporting techniques are also discussed. The report concludes with an analysis of the company's performance, budget preparation, and an evaluation of planning tools, including the balance scorecard, to address financial issues and provide recommendations for the company's future.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P.1 Accounting Functions ..........................................................................................................1

P.2 Types of accounting system..................................................................................................2

M.1 Benefits of Management accounting...................................................................................3

D.1 Critical evaluation about management accounting and reporting system............................4

TASK 2............................................................................................................................................4

P.3 Costing method used by company........................................................................................4

M.2 Techniques for financial reporting......................................................................................7

D.2 Data interpretation of company performances.....................................................................7

TASK 3 ...........................................................................................................................................7

P.4 Budget preparation................................................................................................................7

M.3 Analysis of planning and application of budget..................................................................9

D.3 Evaluate planning tool for overcome financial issues..........................................................9

TASK 4............................................................................................................................................9

P.5 Balance scorecard and its respond to financial issues..........................................................9

M.4 Analysed accounting problem..........................................................................................11

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

.......................................................................................................................................................13

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P.1 Accounting Functions ..........................................................................................................1

P.2 Types of accounting system..................................................................................................2

M.1 Benefits of Management accounting...................................................................................3

D.1 Critical evaluation about management accounting and reporting system............................4

TASK 2............................................................................................................................................4

P.3 Costing method used by company........................................................................................4

M.2 Techniques for financial reporting......................................................................................7

D.2 Data interpretation of company performances.....................................................................7

TASK 3 ...........................................................................................................................................7

P.4 Budget preparation................................................................................................................7

M.3 Analysis of planning and application of budget..................................................................9

D.3 Evaluate planning tool for overcome financial issues..........................................................9

TASK 4............................................................................................................................................9

P.5 Balance scorecard and its respond to financial issues..........................................................9

M.4 Analysed accounting problem..........................................................................................11

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

.......................................................................................................................................................13

INTRODUCTION

The project assignment is about management accounting. Under which various

accounting function are explain and how they are beneficial for the IMDA Tech Ltd. The

company is major producer of mobile ,telephone charger for retail outlets in UK (Kaplan and

Atkinson, 2015). As a manger of this company I have tried to overcome the financial issues that

are arises in company and provide valuable recommendation to make strong decision regarding

stability of department.

For this many cost accounting system and calculation to solve problem of net profit by

using marginal and absorption costing method. To improve financial impact, we have prepared

budgets with its advantages and disadvantages to the company. Based on our analysis we have

given so many findings and recommendation that the company may follow to improve its

positions in comping future. The report is based on entire accounting system of IMDA Tech Ltd

as to improve the performance of the company.

TASK 1

P.1 Accounting Functions

Management accounting: It refers to the process of collecting, sourcing,

communicating, analysing and evaluating monetary and non-monetary transactions or

information to return and create value for the company (Ward, 2012). It combines finance,

accounting and management systems with the business skills and techniques that will help

organisation grow. The accountants use this information of all kinds, not only financial to lead

business strategies and desired from sustainable success.

Comparison between financial and management accounting.

Financial Accounting Management Accounting

1. The report are prepared those are based on

previous performance which is in line to

requirement.

2. It produce required financial data to use by

other departments within the organisation like

for examples, Department manager.

1.The information collected like surplus, cash

flows and outstanding liabilities to prepare

trend report which help in taking important

decision.

2. It combines both monetary and no-monetary

information to brought complete image of the

1

The project assignment is about management accounting. Under which various

accounting function are explain and how they are beneficial for the IMDA Tech Ltd. The

company is major producer of mobile ,telephone charger for retail outlets in UK (Kaplan and

Atkinson, 2015). As a manger of this company I have tried to overcome the financial issues that

are arises in company and provide valuable recommendation to make strong decision regarding

stability of department.

For this many cost accounting system and calculation to solve problem of net profit by

using marginal and absorption costing method. To improve financial impact, we have prepared

budgets with its advantages and disadvantages to the company. Based on our analysis we have

given so many findings and recommendation that the company may follow to improve its

positions in comping future. The report is based on entire accounting system of IMDA Tech Ltd

as to improve the performance of the company.

TASK 1

P.1 Accounting Functions

Management accounting: It refers to the process of collecting, sourcing,

communicating, analysing and evaluating monetary and non-monetary transactions or

information to return and create value for the company (Ward, 2012). It combines finance,

accounting and management systems with the business skills and techniques that will help

organisation grow. The accountants use this information of all kinds, not only financial to lead

business strategies and desired from sustainable success.

Comparison between financial and management accounting.

Financial Accounting Management Accounting

1. The report are prepared those are based on

previous performance which is in line to

requirement.

2. It produce required financial data to use by

other departments within the organisation like

for examples, Department manager.

1.The information collected like surplus, cash

flows and outstanding liabilities to prepare

trend report which help in taking important

decision.

2. It combines both monetary and no-monetary

information to brought complete image of the

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3. It mainly focused on outside like

shareholders.

4. Financial accounting is based on certain law

that has to be followed by every manager.

5. Under this information is related to various

data collection from financial transaction done

by the company.

6. Every financial accounting has set format

that has to be followed by manger while

preparing statements.

company position.

3. It provide information as internal level to the

people.

4. While management accounting doesn't need

law because these are generally excepted.

5. It helps organisation to plan its aims and

objectives.

6. The demand of management that if they

need a kind of format then they use it

otherwise not fixed format followed.

Importance of Management accounting

Determine Aim: on the basis of information available with management they determine

its goal and tries to search route through which they can reached to its goals (Burritt,

Schaltegger and Zvezdov, 2011).

Help in formulation of plan: The manager must prepare plan which should identified

present and future stability and existence of the company.

East to take financial judgement: Before taking any important decision regarding

financial impact. We must choose right plan which can help to decide whether company

may get most out from this plan or polices.

Measurement of performance: There are various standard costing which enable the

organisation to measure performance. It also enables to find out derivations among

standard and actual costing.

Increase efficiency of business: Management accounting helps to maximise the efficiency

of the company. The target is set in advance and achievements are taken as important

techniques to measure its efficiency of the company performance.

P.2 Types of accounting system

To make appropriate decision regarding maximising the financial stability and managing

accounting system the company may use various types of accounting system to analysed their

financial position. The IMDA Tech Ltd has using cost accounting, and Price optimising system,

in their business to manage its retail outlet in UK (Parker, 2012). It helps to identified various

2

shareholders.

4. Financial accounting is based on certain law

that has to be followed by every manager.

5. Under this information is related to various

data collection from financial transaction done

by the company.

6. Every financial accounting has set format

that has to be followed by manger while

preparing statements.

company position.

3. It provide information as internal level to the

people.

4. While management accounting doesn't need

law because these are generally excepted.

5. It helps organisation to plan its aims and

objectives.

6. The demand of management that if they

need a kind of format then they use it

otherwise not fixed format followed.

Importance of Management accounting

Determine Aim: on the basis of information available with management they determine

its goal and tries to search route through which they can reached to its goals (Burritt,

Schaltegger and Zvezdov, 2011).

Help in formulation of plan: The manager must prepare plan which should identified

present and future stability and existence of the company.

East to take financial judgement: Before taking any important decision regarding

financial impact. We must choose right plan which can help to decide whether company

may get most out from this plan or polices.

Measurement of performance: There are various standard costing which enable the

organisation to measure performance. It also enables to find out derivations among

standard and actual costing.

Increase efficiency of business: Management accounting helps to maximise the efficiency

of the company. The target is set in advance and achievements are taken as important

techniques to measure its efficiency of the company performance.

P.2 Types of accounting system

To make appropriate decision regarding maximising the financial stability and managing

accounting system the company may use various types of accounting system to analysed their

financial position. The IMDA Tech Ltd has using cost accounting, and Price optimising system,

in their business to manage its retail outlet in UK (Parker, 2012). It helps to identified various

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

investment and cost which are incurred during the year. The internal and external department of

company can be more affective by this accounting system. Cash flows are being analysed by

mangers and according to its need they able to use accounting system (Granlund, 2011).

Types of accounting system:

Cost accounting system: It is said to be costing system that use a framework which firm

make use to calculated cost of their product for profitability analysis and cost control. It includes

normal historical costing which is based on absorption costing as stock valuation and cost

accumulated method. It is also an internal reporting system used by organisation to make

appropriate decision (Weißenberger and Angelkort, 2011).

Normal costing is used to evaluate manufacturing products by using actual material cost,

labour cost and material overhead cost.

Standard costing values its manufacturing products with predetermine costs of material,

labour and overhead.

Actual costing is recording of product cost based on actual cost of material, labour and

overhead by using actual quantity during the year.

Inventory management system : It is the administration of non-capitalized assets. As it

based on managing stocks of the company in their business operation. There are various

techniques to control inventory system which is categorised by three categories like A<B<C.

These grading are given on the basis of its durability.

Job costing system : Job order is a system for assignment production cost to an

individual good or bunch of goods. These are mainly used when there is sufficiently differenced

among each products. It also a method of recording cost of production job rather than processing.

It help to keep track record of cost used during the period of manufacturing.

Price optimising system : It refers to make use of statistical analysis of company to

determine how people will respond to various price for its product that are set for different

distribution channel. It also used by company to determine price which is set to achieve its aim

and objectives such as to increase operating profit for the company. Price optimization utilized

analysis of huge data to estimate the behaviour of buyer to different prices (Bisbe and

Malagueño, 2012).

3

company can be more affective by this accounting system. Cash flows are being analysed by

mangers and according to its need they able to use accounting system (Granlund, 2011).

Types of accounting system:

Cost accounting system: It is said to be costing system that use a framework which firm

make use to calculated cost of their product for profitability analysis and cost control. It includes

normal historical costing which is based on absorption costing as stock valuation and cost

accumulated method. It is also an internal reporting system used by organisation to make

appropriate decision (Weißenberger and Angelkort, 2011).

Normal costing is used to evaluate manufacturing products by using actual material cost,

labour cost and material overhead cost.

Standard costing values its manufacturing products with predetermine costs of material,

labour and overhead.

Actual costing is recording of product cost based on actual cost of material, labour and

overhead by using actual quantity during the year.

Inventory management system : It is the administration of non-capitalized assets. As it

based on managing stocks of the company in their business operation. There are various

techniques to control inventory system which is categorised by three categories like A<B<C.

These grading are given on the basis of its durability.

Job costing system : Job order is a system for assignment production cost to an

individual good or bunch of goods. These are mainly used when there is sufficiently differenced

among each products. It also a method of recording cost of production job rather than processing.

It help to keep track record of cost used during the period of manufacturing.

Price optimising system : It refers to make use of statistical analysis of company to

determine how people will respond to various price for its product that are set for different

distribution channel. It also used by company to determine price which is set to achieve its aim

and objectives such as to increase operating profit for the company. Price optimization utilized

analysis of huge data to estimate the behaviour of buyer to different prices (Bisbe and

Malagueño, 2012).

3

M.1 Benefits of Management accounting

As from above Management accounting system used by the IMDA Tech Ltd in their

business operation how they beneficial for the existence in near future is decided through

evaluating them in proper ways like : The actual performance should be measured with budgets

of the company (Coad, Jack and Kholeif, 2015). The business activities are managed through

using application of both budgeting and planning techniques. To build harmonious relation

between management and labour so that they can motivated with their performance in achieving

objectives. It also help to pre pare future plan by taking support of past outcome generated by the

company.

D.1 Critical evaluation about management accounting and reporting system

According to Vakalfotis, Ballantine and Wall, 2013, major question is being asked that

how to adopt strategies , and practices that are related to the social and organisational demand

while preparing financial profit to their shareholders. The choice of integration is fulfilled

through hold and retain its customer by providing proper requirement of product with minimum

costing. In the words of Scapens, 2011, performance and evaluation of financial statement are

done just to create synergy among firm and individual as they play a vital role in management

decision. Costing techniques can be very useful for managing financial resources of the

company.

TASK 2

P.3 Costing method used by company

Absorption Costing : It refers as all those manufacturing cost which are absorbed by

units produced. In other hand , cost of finished unit in stock will sum up by including direct

material, direct labour and both variable and fixed production overhead. It is often highlight of

variable or direct costing (Quinn, 2011). The fixed overhead cost are not allowed which are

associated to manufacturing process.

Marginal Costing : It is said to be accounting system under which variable cost are

imposed to cost unit and fixed cost of time are written off against the multiple contribution. In

other words we can say that the cost of extra unit or additional unit of quantity or output.

By using above two costing method IMDA Tech Ltd can identified its net loss or gain from

manufacturing of product.

4

As from above Management accounting system used by the IMDA Tech Ltd in their

business operation how they beneficial for the existence in near future is decided through

evaluating them in proper ways like : The actual performance should be measured with budgets

of the company (Coad, Jack and Kholeif, 2015). The business activities are managed through

using application of both budgeting and planning techniques. To build harmonious relation

between management and labour so that they can motivated with their performance in achieving

objectives. It also help to pre pare future plan by taking support of past outcome generated by the

company.

D.1 Critical evaluation about management accounting and reporting system

According to Vakalfotis, Ballantine and Wall, 2013, major question is being asked that

how to adopt strategies , and practices that are related to the social and organisational demand

while preparing financial profit to their shareholders. The choice of integration is fulfilled

through hold and retain its customer by providing proper requirement of product with minimum

costing. In the words of Scapens, 2011, performance and evaluation of financial statement are

done just to create synergy among firm and individual as they play a vital role in management

decision. Costing techniques can be very useful for managing financial resources of the

company.

TASK 2

P.3 Costing method used by company

Absorption Costing : It refers as all those manufacturing cost which are absorbed by

units produced. In other hand , cost of finished unit in stock will sum up by including direct

material, direct labour and both variable and fixed production overhead. It is often highlight of

variable or direct costing (Quinn, 2011). The fixed overhead cost are not allowed which are

associated to manufacturing process.

Marginal Costing : It is said to be accounting system under which variable cost are

imposed to cost unit and fixed cost of time are written off against the multiple contribution. In

other words we can say that the cost of extra unit or additional unit of quantity or output.

By using above two costing method IMDA Tech Ltd can identified its net loss or gain from

manufacturing of product.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

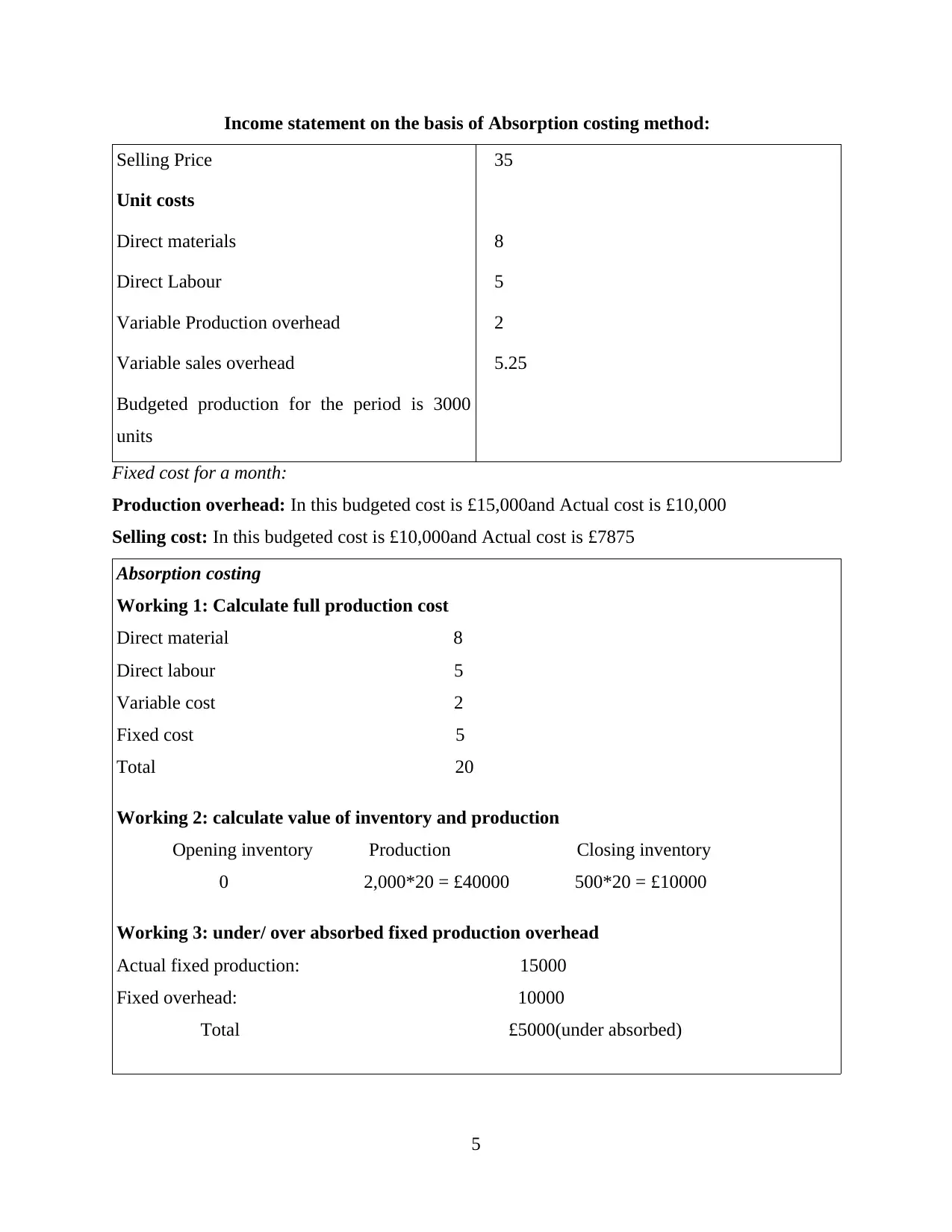

Income statement on the basis of Absorption costing method:

Selling Price £35

Unit costs

Direct materials £8

Direct Labour £5

Variable Production overhead £2

Variable sales overhead £5.25

Budgeted production for the period is 3000

units

Fixed cost for a month:

Production overhead: In this budgeted cost is £15,000and Actual cost is £10,000

Selling cost: In this budgeted cost is £10,000and Actual cost is £7875

Absorption costing

Working 1: Calculate full production cost

Direct material £8

Direct labour £5

Variable cost £2

Fixed cost £5

Total £20

Working 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 2,000*20 = £40000 500*20 = £10000

Working 3: under/ over absorbed fixed production overhead

Actual fixed production: £15000

Fixed overhead: £10000

Total £5000(under absorbed)

5

Selling Price £35

Unit costs

Direct materials £8

Direct Labour £5

Variable Production overhead £2

Variable sales overhead £5.25

Budgeted production for the period is 3000

units

Fixed cost for a month:

Production overhead: In this budgeted cost is £15,000and Actual cost is £10,000

Selling cost: In this budgeted cost is £10,000and Actual cost is £7875

Absorption costing

Working 1: Calculate full production cost

Direct material £8

Direct labour £5

Variable cost £2

Fixed cost £5

Total £20

Working 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 2,000*20 = £40000 500*20 = £10000

Working 3: under/ over absorbed fixed production overhead

Actual fixed production: £15000

Fixed overhead: £10000

Total £5000(under absorbed)

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

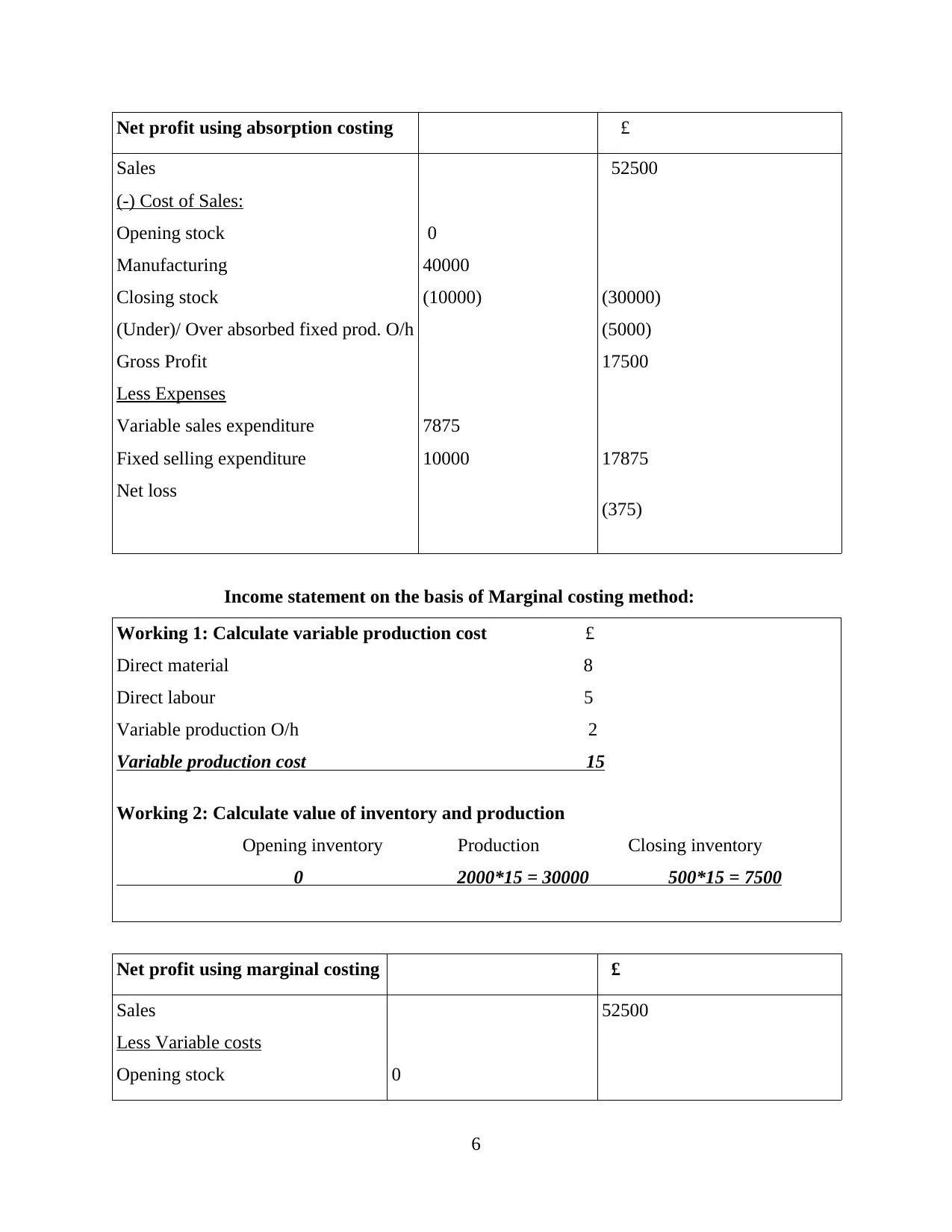

Net profit using absorption costing £ £

Sales

(-) Cost of Sales:

Opening stock

Manufacturing

Closing stock

(Under)/ Over absorbed fixed prod. O/h

Gross Profit

Less Expenses

Variable sales expenditure

Fixed selling expenditure

Net loss

0

40000

(10000)

7875

10000

52500

(30000)

(5000)

17500

17875

(375)

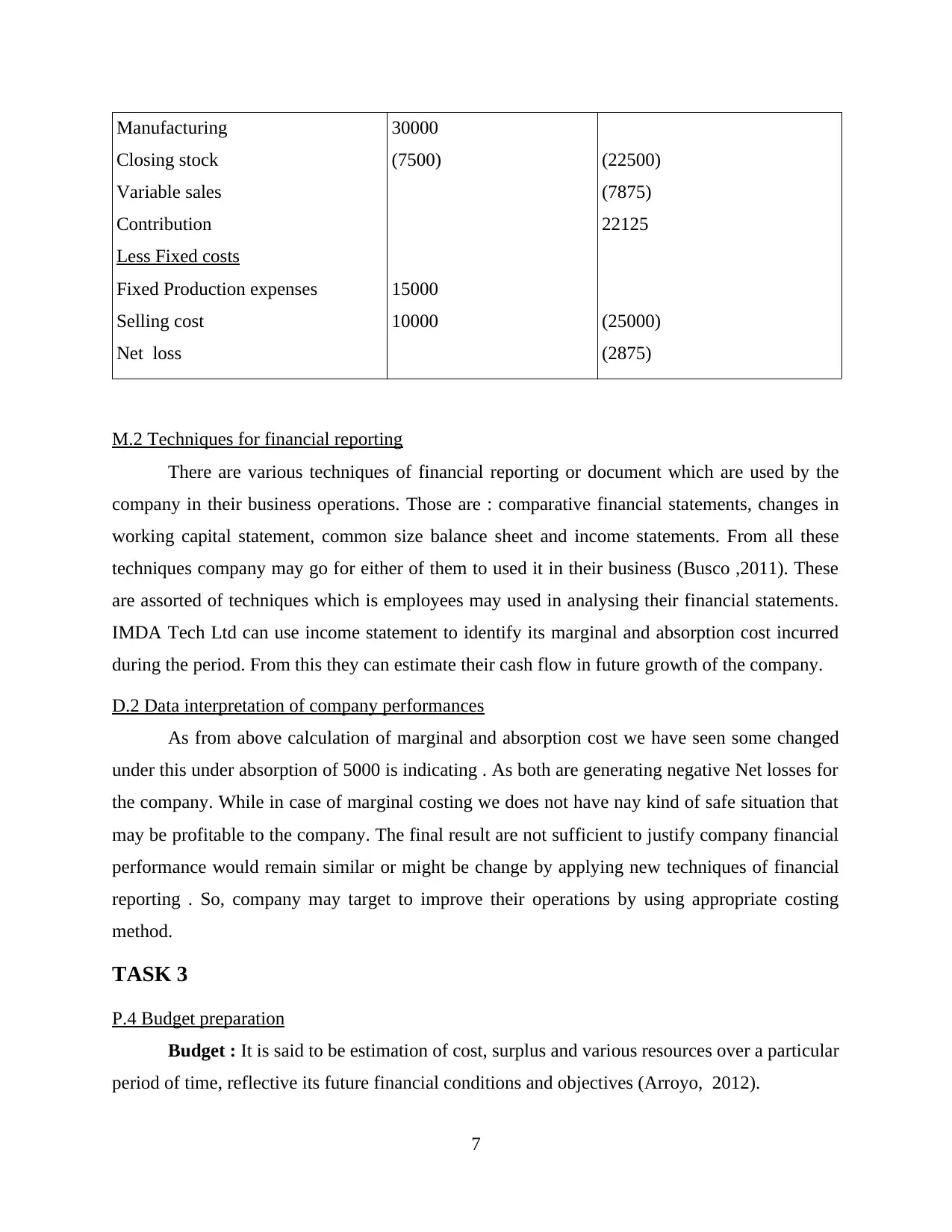

Income statement on the basis of Marginal costing method:

Working 1: Calculate variable production cost £

Direct material 8

Direct labour 5

Variable production O/h 2

Variable production cost 15

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 2000*15 = 30000 500*15 = 7500

Net profit using marginal costing £ £

Sales

Less Variable costs

Opening stock 0

52500

6

Sales

(-) Cost of Sales:

Opening stock

Manufacturing

Closing stock

(Under)/ Over absorbed fixed prod. O/h

Gross Profit

Less Expenses

Variable sales expenditure

Fixed selling expenditure

Net loss

0

40000

(10000)

7875

10000

52500

(30000)

(5000)

17500

17875

(375)

Income statement on the basis of Marginal costing method:

Working 1: Calculate variable production cost £

Direct material 8

Direct labour 5

Variable production O/h 2

Variable production cost 15

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 2000*15 = 30000 500*15 = 7500

Net profit using marginal costing £ £

Sales

Less Variable costs

Opening stock 0

52500

6

Manufacturing

Closing stock

Variable sales

Contribution

Less Fixed costs

Fixed Production expenses

Selling cost

Net loss

30000

(7500)

15000

10000

(22500)

(7875)

22125

(25000)

(2875)

M.2 Techniques for financial reporting

There are various techniques of financial reporting or document which are used by the

company in their business operations. Those are : comparative financial statements, changes in

working capital statement, common size balance sheet and income statements. From all these

techniques company may go for either of them to used it in their business (Busco ,2011). These

are assorted of techniques which is employees may used in analysing their financial statements.

IMDA Tech Ltd can use income statement to identify its marginal and absorption cost incurred

during the period. From this they can estimate their cash flow in future growth of the company.

D.2 Data interpretation of company performances

As from above calculation of marginal and absorption cost we have seen some changed

under this under absorption of 5000 is indicating . As both are generating negative Net losses for

the company. While in case of marginal costing we does not have nay kind of safe situation that

may be profitable to the company. The final result are not sufficient to justify company financial

performance would remain similar or might be change by applying new techniques of financial

reporting . So, company may target to improve their operations by using appropriate costing

method.

TASK 3

P.4 Budget preparation

Budget : It is said to be estimation of cost, surplus and various resources over a particular

period of time, reflective its future financial conditions and objectives (Arroyo, 2012).

7

Closing stock

Variable sales

Contribution

Less Fixed costs

Fixed Production expenses

Selling cost

Net loss

30000

(7500)

15000

10000

(22500)

(7875)

22125

(25000)

(2875)

M.2 Techniques for financial reporting

There are various techniques of financial reporting or document which are used by the

company in their business operations. Those are : comparative financial statements, changes in

working capital statement, common size balance sheet and income statements. From all these

techniques company may go for either of them to used it in their business (Busco ,2011). These

are assorted of techniques which is employees may used in analysing their financial statements.

IMDA Tech Ltd can use income statement to identify its marginal and absorption cost incurred

during the period. From this they can estimate their cash flow in future growth of the company.

D.2 Data interpretation of company performances

As from above calculation of marginal and absorption cost we have seen some changed

under this under absorption of 5000 is indicating . As both are generating negative Net losses for

the company. While in case of marginal costing we does not have nay kind of safe situation that

may be profitable to the company. The final result are not sufficient to justify company financial

performance would remain similar or might be change by applying new techniques of financial

reporting . So, company may target to improve their operations by using appropriate costing

method.

TASK 3

P.4 Budget preparation

Budget : It is said to be estimation of cost, surplus and various resources over a particular

period of time, reflective its future financial conditions and objectives (Arroyo, 2012).

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Types of budget :

Master budget : It is total aggregation of company individual budget prepared to bring

image of financial activity. It combines various factors like sales,operating expenses,assets and

income statements that company help to establish goals and objectives of the company. These

are prepared by large manufacturing companies.

Advantages

It explain all the aspect of financial statements of company performances at in one

statements.

It is said to overall business budgets.

Disadvantages

Lack of specificity.

Difficult to read and update financial statements under master budgets.

Operational budgets : It refers to the forecast and analysis of estimated income and

expenses over a specific time duration (Hiebl, 2014). All the direct cost of material, labour and

overheads are to be analysed and recorded under the operational budgets. These are mostly

created on weakly , monthly or yearly basis.

Advantages

Estimation of total number of extra expenses those are incurred during a project process.

Managing current expenses for operating budget.

Disadvantages

misuse and extra cost can not be control and managed by the company.

Individual managers are no comfortable with the budget as they co-operate badly.

Cash flow budget : It is kind of budget which provide information about cash in and

flows out of a business within a specific duration time. It is very much helpful for company as to

determine they are managing is cash transaction properly. These are based on three activities like

operating activities , investing activity and financing activity.

Advantages

Only cash transactions is being recorded under this budget.

Overall business estimation of cost that are required to complete a particular project can

be identified.

Disadvantages

8

Master budget : It is total aggregation of company individual budget prepared to bring

image of financial activity. It combines various factors like sales,operating expenses,assets and

income statements that company help to establish goals and objectives of the company. These

are prepared by large manufacturing companies.

Advantages

It explain all the aspect of financial statements of company performances at in one

statements.

It is said to overall business budgets.

Disadvantages

Lack of specificity.

Difficult to read and update financial statements under master budgets.

Operational budgets : It refers to the forecast and analysis of estimated income and

expenses over a specific time duration (Hiebl, 2014). All the direct cost of material, labour and

overheads are to be analysed and recorded under the operational budgets. These are mostly

created on weakly , monthly or yearly basis.

Advantages

Estimation of total number of extra expenses those are incurred during a project process.

Managing current expenses for operating budget.

Disadvantages

misuse and extra cost can not be control and managed by the company.

Individual managers are no comfortable with the budget as they co-operate badly.

Cash flow budget : It is kind of budget which provide information about cash in and

flows out of a business within a specific duration time. It is very much helpful for company as to

determine they are managing is cash transaction properly. These are based on three activities like

operating activities , investing activity and financing activity.

Advantages

Only cash transactions is being recorded under this budget.

Overall business estimation of cost that are required to complete a particular project can

be identified.

Disadvantages

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It may cause distortion. Cash inflows doesn't equate to gain.

Cash budget are susceptible to manipulation in day to day transactions.

Process of budget formulation

1. Update budget assumption : About the business environment reviews.

2. Review choke point: Determine capacity level of primary outcome .

3. Available funding : Estimation of mostly amount from different sources.

4. Obtain revenue forecast : obtain sale forecast from the managers.

5. Collect budget from different department : check error and step costing constrain and

make adjustment accordingly (Ossadnik and Kaspar, 2013).

6. Review the budget : meet the senior authority to review the budget.

7. Issues budget : create a wide vision of budget and distribute to recipients.

8. Load the budget : load information into the financial software.

Pricing strategies : A business concern various pricing strategies while selling a goods

or services. The price can be fixed to maximise profitability of each unit sold by the company in

market. To increase market share or planning to enter into new market.

M.3 Analysis of planning and application of budget

As business is operational we first target to plan and toughly manage its financial

performance. When you are operating a business it is get slow down in day to day issues those

are arises in companies. The budget based on growth and dependability which will help to

estimated total value of company that will create value in near future. Application of forecasting

budget are based on estimating accuracy of forecast and cost benefit analysis. It is also depend

on total number of time forecasting as crucial factor in budgeting.

D.3 Evaluate planning tool for overcome financial issues

The initial stage to overcome financial issues to known implicit problems that are

impacting business performance. The other things are by creating budget which is best way for

combating financial issues. Next to determine financial priorities which might be clear. As per

the above used tools and techniques used in accounting systems for current year. It is based on

setting benchmarking tool of other competitors by keeping other aspects of accounting which are

used in budget preparation.

9

Cash budget are susceptible to manipulation in day to day transactions.

Process of budget formulation

1. Update budget assumption : About the business environment reviews.

2. Review choke point: Determine capacity level of primary outcome .

3. Available funding : Estimation of mostly amount from different sources.

4. Obtain revenue forecast : obtain sale forecast from the managers.

5. Collect budget from different department : check error and step costing constrain and

make adjustment accordingly (Ossadnik and Kaspar, 2013).

6. Review the budget : meet the senior authority to review the budget.

7. Issues budget : create a wide vision of budget and distribute to recipients.

8. Load the budget : load information into the financial software.

Pricing strategies : A business concern various pricing strategies while selling a goods

or services. The price can be fixed to maximise profitability of each unit sold by the company in

market. To increase market share or planning to enter into new market.

M.3 Analysis of planning and application of budget

As business is operational we first target to plan and toughly manage its financial

performance. When you are operating a business it is get slow down in day to day issues those

are arises in companies. The budget based on growth and dependability which will help to

estimated total value of company that will create value in near future. Application of forecasting

budget are based on estimating accuracy of forecast and cost benefit analysis. It is also depend

on total number of time forecasting as crucial factor in budgeting.

D.3 Evaluate planning tool for overcome financial issues

The initial stage to overcome financial issues to known implicit problems that are

impacting business performance. The other things are by creating budget which is best way for

combating financial issues. Next to determine financial priorities which might be clear. As per

the above used tools and techniques used in accounting systems for current year. It is based on

setting benchmarking tool of other competitors by keeping other aspects of accounting which are

used in budget preparation.

9

TASK 4

P.5 Balance scorecard and its respond to financial issues.

I):

Balance scorecard : It is said to be strategic design and structure system which is used to

line up business activity to the vision and strategies of management by observing performance

against strategic goal. It was traditional performances that are measure only external accounting

data which are obsolete in nature (Jakobsen, 2012). This will help to provide balance to financial

situations.

Use of balance Scorecard:

It will help to improve organisational performance by evaluating matters.

Maximise concentration on strategies and desire outcome.

Combine institution strategies with individual on every day basis.

Focus on established communication of company vision and mission.

Measurement of Balance scorecard

Financial: These are based on how much return on capital employed , economic value

added ,sales prediction and available cash flows.

Customer: It refers to customer satisfaction, retention strategies and market share or

increasing profitability.

Internal business: it includes measurement as internal value like innovation, operation

and post sale services offer to customer.

Learning and growth : It includes people, and system which measure critical original

time.

Non-financial measures are mostly used to evaluated performance through using central

concepts which is balance score card. These can be helpful because any combination of cost less

performance can reduce risk. It also measures customer satisfaction, product quality etc. to

increase market performance.

Some of the financial issues which are arises in the organisation are:

Inventory management issues: The record of stock items are not maintain in proper

manner which leads to the lot of wastages to the company resources.

10

P.5 Balance scorecard and its respond to financial issues.

I):

Balance scorecard : It is said to be strategic design and structure system which is used to

line up business activity to the vision and strategies of management by observing performance

against strategic goal. It was traditional performances that are measure only external accounting

data which are obsolete in nature (Jakobsen, 2012). This will help to provide balance to financial

situations.

Use of balance Scorecard:

It will help to improve organisational performance by evaluating matters.

Maximise concentration on strategies and desire outcome.

Combine institution strategies with individual on every day basis.

Focus on established communication of company vision and mission.

Measurement of Balance scorecard

Financial: These are based on how much return on capital employed , economic value

added ,sales prediction and available cash flows.

Customer: It refers to customer satisfaction, retention strategies and market share or

increasing profitability.

Internal business: it includes measurement as internal value like innovation, operation

and post sale services offer to customer.

Learning and growth : It includes people, and system which measure critical original

time.

Non-financial measures are mostly used to evaluated performance through using central

concepts which is balance score card. These can be helpful because any combination of cost less

performance can reduce risk. It also measures customer satisfaction, product quality etc. to

increase market performance.

Some of the financial issues which are arises in the organisation are:

Inventory management issues: The record of stock items are not maintain in proper

manner which leads to the lot of wastages to the company resources.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.