Analyzing the Impacts of COVID-19 on Audit Procedures and Practices

VerifiedAdded on 2021/06/22

|16

|830

|136

Report

AI Summary

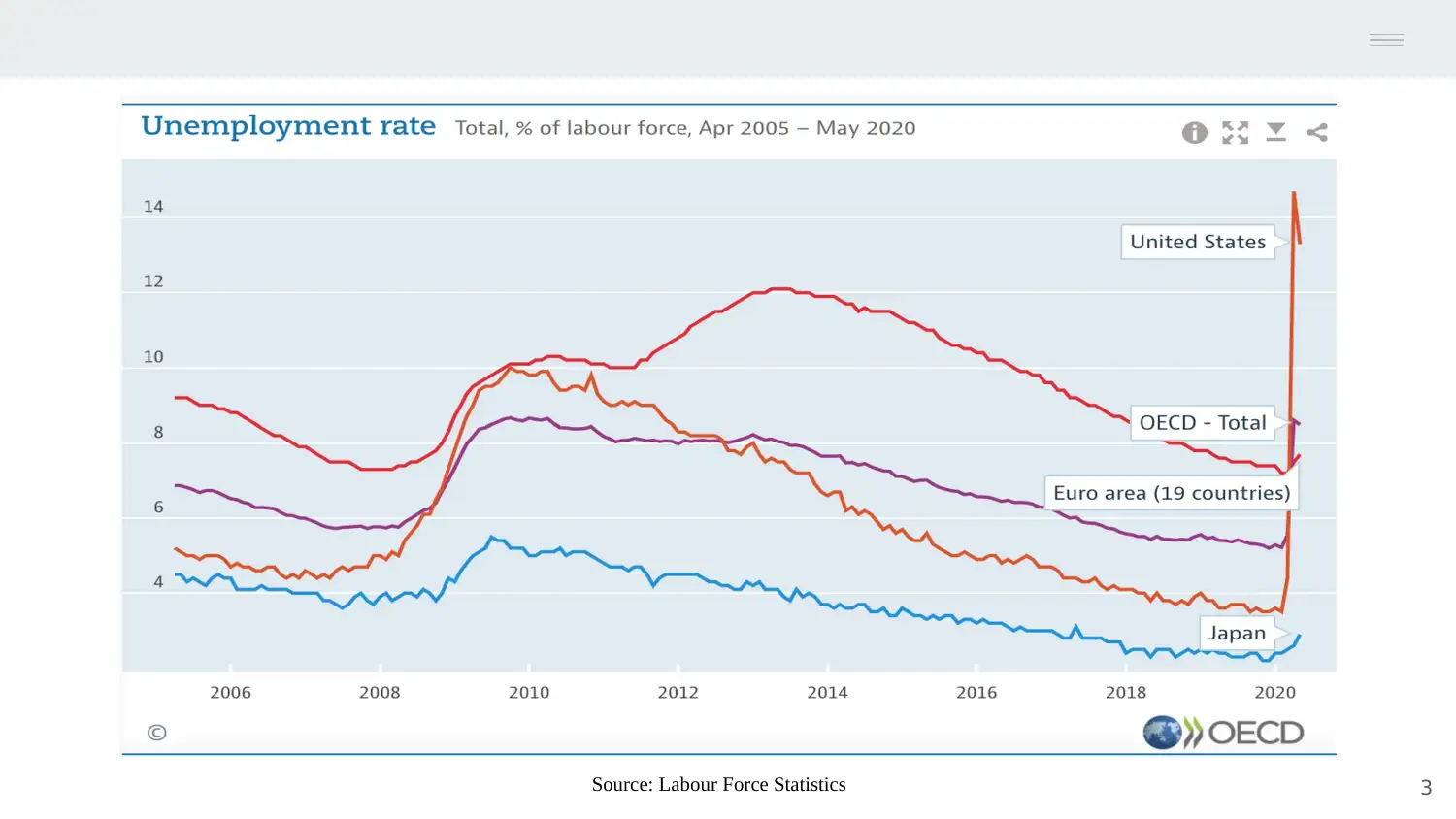

This report, prepared for Lorem Ipsum LLC, analyzes the impacts of the COVID-19 pandemic on auditing practices and procedures. It covers key areas such as determining materiality, ethical considerations, risk assessment, audit evidence gathering, and the handling of subsequent events. The report highlights changes in entity strategies, organizational structures, and business models due to the pandemic, and discusses increased risks of fraud, lack of expertise, and financial instability. It provides insights into auditors' responses, including ongoing communication, understanding of changes, and evaluating altered risks. The report also addresses going concern risks, the impact on materiality, and the implications for audit evidence, including inspections of physical inventories and documents. It offers practical solutions for auditors to adapt to the challenges of the pandemic, such as using technology for remote inspections and communication. References to relevant guidelines and publications from IFAC, ICAEW, CAANZ, and ASIC are included. This report serves as a valuable resource for auditors navigating the complexities of auditing during the COVID-19 era.

1 out of 16

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.