ITECH1100: Cryptocurrency's Impact on the Banking Industry

VerifiedAdded on 2023/06/04

|11

|2153

|356

Report

AI Summary

This report, submitted by a student, investigates the potential impact of cryptocurrency on the banking industry. It delves into the core concepts of cryptocurrency, including its cryptographic basis and digital transaction processes, contrasting them with traditional centralized banking systems. The report explores the disruptive effects of cryptocurrency, particularly the shift towards decentralized control and the implications for international trade and financial regulations. It examines the role of blockchain technology, the regulatory landscape, and ethical considerations related to data security. The report also includes a video transcript that further illustrates the contrast between centralized and decentralized transaction systems. Overall, the report provides a comprehensive analysis of how cryptocurrency is reshaping the banking sector, the challenges it presents, and its potential future impact.

Running head: THE POTENTIAL IMPACT OF CRYPTOCURRENCY ON THE BANKING INDUSTRY

The potential impact of Cryptocurrency on the banking industry

Name of the Student

Name of the University

Author Note

The potential impact of Cryptocurrency on the banking industry

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1THE POTENTIAL IMPACT OF CRYPTOCURRENCY ON THE BANKING INDUSTRY

Table of Contents

Research...........................................................................................................................................2

Brainstorming..................................................................................................................................3

Regulation and Ethics......................................................................................................................3

Disruption........................................................................................................................................4

Video transcript...............................................................................................................................7

References........................................................................................................................................9

Table of Contents

Research...........................................................................................................................................2

Brainstorming..................................................................................................................................3

Regulation and Ethics......................................................................................................................3

Disruption........................................................................................................................................4

Video transcript...............................................................................................................................7

References........................................................................................................................................9

2THE POTENTIAL IMPACT OF CRYPTOCURRENCY ON THE BANKING INDUSTRY

Research

The term cryptocurrency has been devised from the mixture of two words that are mainly

cryptography and currency. It is a form of a currency that is encrypted digitally to produce

economical assets (Böhme et al., 2015). The money generated in the form of cryptocurrencies is

used for digital transactions that are technically secured and verified. They are the digital assets

that are configured in such a way that their exchanges are cryptographically encrypted, additional

units are controlled and the whole transaction process of the assets is verified before initiation

(Iwamura et al., 2014). In the commercial world, they can be classified as a type of digital

currencies, alternative currencies and virtual currencies.

The transactional process of the cryptocurrencies is different to that of the modern

banking system. It is because the banking system is relied upon centralized electronic banking

systems whereas the cryptocurrencies are relied upon a decentralized control of transfer. This

decentralized control of transfer of the cryptocurrencies includes the presence of a blockchain

that is a public transactional database. The blockchain facilitates the transfer of the currencies

using a distributed ledger where the account of all the transactions taking place all across the

world is recorded (Iansiti & Lakhani, 2017). The information about every transaction is

forwarded to every active member of the blockchain so that any sort of discrepancy or falsity can

be avoided. This is the reason for which the system does not require a central authority to

maintain the integrity of the system. According to the protocols of the system, the system decides

whether there is a possibility of introducing a new cryptocurrency unit and if there is a possibility

of such, the system takes the charge of defining the origin of the cryptocurrency and how to

Research

The term cryptocurrency has been devised from the mixture of two words that are mainly

cryptography and currency. It is a form of a currency that is encrypted digitally to produce

economical assets (Böhme et al., 2015). The money generated in the form of cryptocurrencies is

used for digital transactions that are technically secured and verified. They are the digital assets

that are configured in such a way that their exchanges are cryptographically encrypted, additional

units are controlled and the whole transaction process of the assets is verified before initiation

(Iwamura et al., 2014). In the commercial world, they can be classified as a type of digital

currencies, alternative currencies and virtual currencies.

The transactional process of the cryptocurrencies is different to that of the modern

banking system. It is because the banking system is relied upon centralized electronic banking

systems whereas the cryptocurrencies are relied upon a decentralized control of transfer. This

decentralized control of transfer of the cryptocurrencies includes the presence of a blockchain

that is a public transactional database. The blockchain facilitates the transfer of the currencies

using a distributed ledger where the account of all the transactions taking place all across the

world is recorded (Iansiti & Lakhani, 2017). The information about every transaction is

forwarded to every active member of the blockchain so that any sort of discrepancy or falsity can

be avoided. This is the reason for which the system does not require a central authority to

maintain the integrity of the system. According to the protocols of the system, the system decides

whether there is a possibility of introducing a new cryptocurrency unit and if there is a possibility

of such, the system takes the charge of defining the origin of the cryptocurrency and how to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3THE POTENTIAL IMPACT OF CRYPTOCURRENCY ON THE BANKING INDUSTRY

obtain the ownership of that new origin (Ali et al., 2014). The ownership of the newly originated

unit can be proved with the help of several cryptography techniques.

Brainstorming

With the advent of the cryptocurrencies in the process of leading with the transactions,

the banking industry is being disrupted due to the rise of these digital assets through several

ways. The cryptocurrencies uses a decentralized control for the transactions all over the world

for which it is affecting most of the real world currencies. Dollar is one of those currencies that

considered as a primary source of the global economy. It has been able to mark its dominance

through centralized banking in most of the countries. However, with a decentralized control, the

cryptocurrencies have been able to disrupt the centralized banking process (Pilkington, 2016). As

a consequence to this, the international trades, relations with the foreign entities, diplomatic

strategies along with the economic sanction are largely getting impacted.

Although, it is being apprehended that due to its decentralized nature, the

cryptocurrencies are going to play a huge role in the daily life by smoothening the flow of

transactions, several industries such as the payment sectors, governments along with the banking

industry is expected to face severe challenges in adapting to the exchange of economy of the

country (Bech & Garratt, 2017). The cryptocurrency is expected to boost up the economic

growth by allowing merchants to drop in with innovative business ideas and trade points.

Regulation and Ethics

According to Lawrence Lessig there are four regulators that regulate a particular entity.

These four regulators are the law, market, architecture and the norms. The laws are set by the

obtain the ownership of that new origin (Ali et al., 2014). The ownership of the newly originated

unit can be proved with the help of several cryptography techniques.

Brainstorming

With the advent of the cryptocurrencies in the process of leading with the transactions,

the banking industry is being disrupted due to the rise of these digital assets through several

ways. The cryptocurrencies uses a decentralized control for the transactions all over the world

for which it is affecting most of the real world currencies. Dollar is one of those currencies that

considered as a primary source of the global economy. It has been able to mark its dominance

through centralized banking in most of the countries. However, with a decentralized control, the

cryptocurrencies have been able to disrupt the centralized banking process (Pilkington, 2016). As

a consequence to this, the international trades, relations with the foreign entities, diplomatic

strategies along with the economic sanction are largely getting impacted.

Although, it is being apprehended that due to its decentralized nature, the

cryptocurrencies are going to play a huge role in the daily life by smoothening the flow of

transactions, several industries such as the payment sectors, governments along with the banking

industry is expected to face severe challenges in adapting to the exchange of economy of the

country (Bech & Garratt, 2017). The cryptocurrency is expected to boost up the economic

growth by allowing merchants to drop in with innovative business ideas and trade points.

Regulation and Ethics

According to Lawrence Lessig there are four regulators that regulate a particular entity.

These four regulators are the law, market, architecture and the norms. The laws are set by the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4THE POTENTIAL IMPACT OF CRYPTOCURRENCY ON THE BANKING INDUSTRY

governments, the norms are set by the community, the market is set by the economical standards

and the architecture is set by the development and the urge of innovation (Katyal, 2013). The

banking industry uses a centralized system for which the information about the transactions and

the monetary exchanges are kept highly secured under strict supervision. However, the

decentralized transaction process of the digital currencies may lead to an infringement of the

personal accounts since it is not under a strict supervision. Therefore, it is evident from the fact

that there are no governmental laws for the blockchain (MacDonald, Allen & Potts, 2016). The

internal laws of the decentralized system include mandatory cryptocurrency accounts,

maintenance of a ledger and the right to information about all the transactions. An architectural

constraint relating to the technology of the transaction process of cryptocurrencies is the

inclusion of a blockchain, that is a public transactional database used for maintain the records of

all the transactions taking place in a particular period of time. Transactions though a blockchain

is expected to increase the efficiency of all the transactions.

Disruption

Cryptocurrency intends to change the process of transactional workflow in a particular

system of monetary exchanges (De Filippi, 2014). In the centralized form of the system that is in

the banking system the transaction generally takes place through the involvement of several third

parties or the intermediaries. In order to facilitate transaction through a centralized system it is

mandatory to have accounts on both the ends that is the account of the sender and the account of

the recipient. These accounts are in the safe custody of the individual banks on either of the side.

To have an exchange the sender must look into his banking account for his transfer of money and

with the help of a third party he should be able to send money to the account of the recipient. The

governments, the norms are set by the community, the market is set by the economical standards

and the architecture is set by the development and the urge of innovation (Katyal, 2013). The

banking industry uses a centralized system for which the information about the transactions and

the monetary exchanges are kept highly secured under strict supervision. However, the

decentralized transaction process of the digital currencies may lead to an infringement of the

personal accounts since it is not under a strict supervision. Therefore, it is evident from the fact

that there are no governmental laws for the blockchain (MacDonald, Allen & Potts, 2016). The

internal laws of the decentralized system include mandatory cryptocurrency accounts,

maintenance of a ledger and the right to information about all the transactions. An architectural

constraint relating to the technology of the transaction process of cryptocurrencies is the

inclusion of a blockchain, that is a public transactional database used for maintain the records of

all the transactions taking place in a particular period of time. Transactions though a blockchain

is expected to increase the efficiency of all the transactions.

Disruption

Cryptocurrency intends to change the process of transactional workflow in a particular

system of monetary exchanges (De Filippi, 2014). In the centralized form of the system that is in

the banking system the transaction generally takes place through the involvement of several third

parties or the intermediaries. In order to facilitate transaction through a centralized system it is

mandatory to have accounts on both the ends that is the account of the sender and the account of

the recipient. These accounts are in the safe custody of the individual banks on either of the side.

To have an exchange the sender must look into his banking account for his transfer of money and

with the help of a third party he should be able to send money to the account of the recipient. The

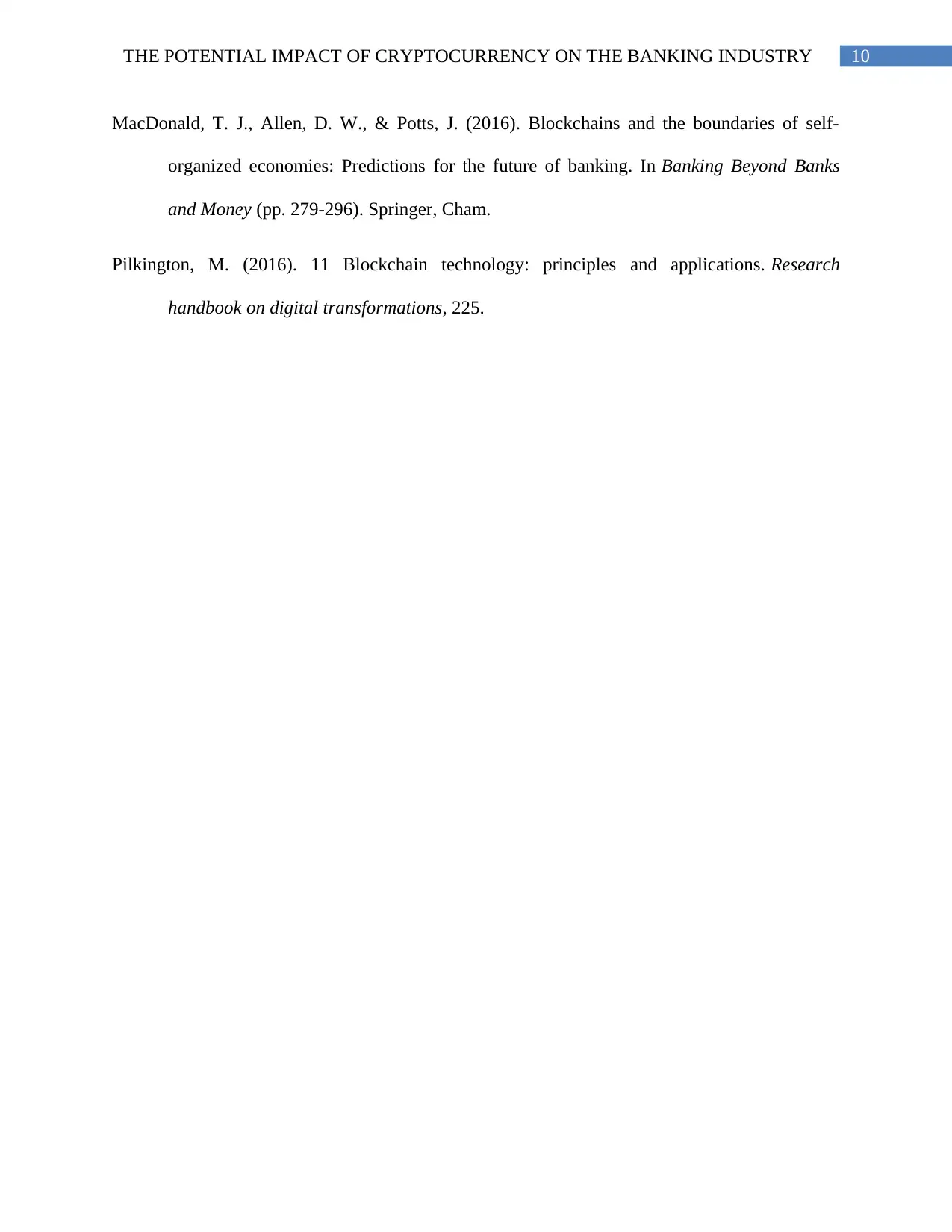

5THE POTENTIAL IMPACT OF CRYPTOCURRENCY ON THE BANKING INDUSTRY

third parties have restrictions at times, are slower, involves extra charges and are closed in nature

(Ally, Gardiner & Lane, 2016).

Figure 1: Transaction through centralized system

(Source: Author)

However, the transactional procedure in case of a decentralized system involving the

transfer of the cryptocurrencies is a bit different to that of the transaction in the centralized

process (Fanning & Centers, 2016). The transaction of the cryptocurrencies takes place through

the help of a blockchain and a public network. The blockchain is a public transaction database

while the network is an open network. Being decentralized in nature, the transactions of the

cryptocurrencies does not involve any third parties. In order to send digital currencies, a sender

must have an encrypted account where the cryptocurrencies are stored and he can directly send

the assets to the recipient’s account through the help of the open network (Décourt, Chohan &

Perugini, (2017). This network is a peer to peer network that is much secured than the existing

bank accounts and supports instant transfer unlike the centralized networks. The involvement of

third parties have restrictions at times, are slower, involves extra charges and are closed in nature

(Ally, Gardiner & Lane, 2016).

Figure 1: Transaction through centralized system

(Source: Author)

However, the transactional procedure in case of a decentralized system involving the

transfer of the cryptocurrencies is a bit different to that of the transaction in the centralized

process (Fanning & Centers, 2016). The transaction of the cryptocurrencies takes place through

the help of a blockchain and a public network. The blockchain is a public transaction database

while the network is an open network. Being decentralized in nature, the transactions of the

cryptocurrencies does not involve any third parties. In order to send digital currencies, a sender

must have an encrypted account where the cryptocurrencies are stored and he can directly send

the assets to the recipient’s account through the help of the open network (Décourt, Chohan &

Perugini, (2017). This network is a peer to peer network that is much secured than the existing

bank accounts and supports instant transfer unlike the centralized networks. The involvement of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6THE POTENTIAL IMPACT OF CRYPTOCURRENCY ON THE BANKING INDUSTRY

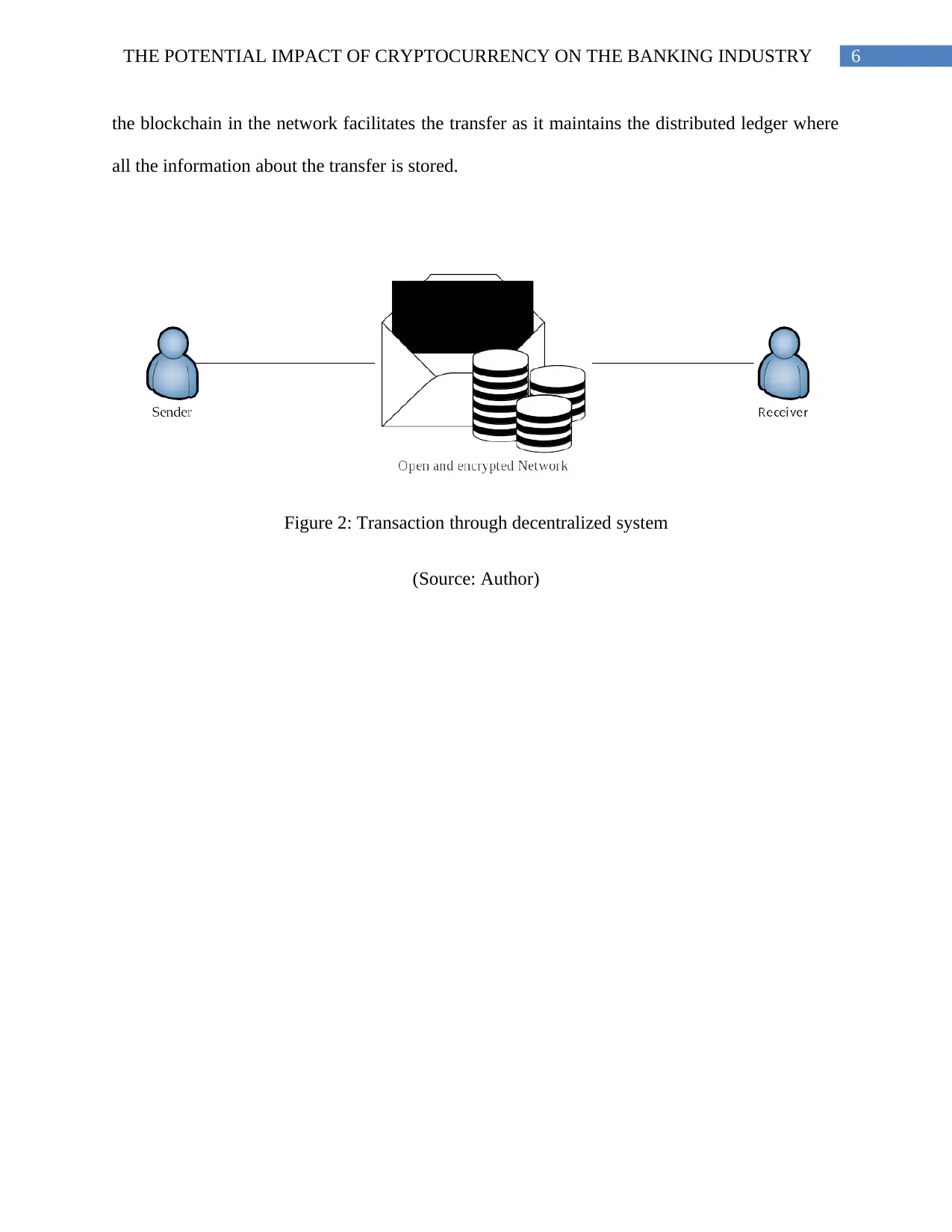

the blockchain in the network facilitates the transfer as it maintains the distributed ledger where

all the information about the transfer is stored.

Figure 2: Transaction through decentralized system

(Source: Author)

the blockchain in the network facilitates the transfer as it maintains the distributed ledger where

all the information about the transfer is stored.

Figure 2: Transaction through decentralized system

(Source: Author)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7THE POTENTIAL IMPACT OF CRYPTOCURRENCY ON THE BANKING INDUSTRY

Video transcript

00:00 – 00:15: In the centralized form of the system [pause] that is in the banking system [pause]

the transaction generally takes place through the involvement of several third parties or the

intermediaries.

00:15 – 00:30: [pause] In order to facilitate transaction through a centralized system [pause] it is

mandatory to have accounts on both the ends that is the account of the sender and the account of

the recipient.

00:30 – 00:40: [pause] These accounts are in the safe custody of the individual banks on either of

the sides that is for both the receiver and the sender.

00:40 – 00:55: [pause] To have an exchange [pause] the sender must look into his banking

account for his transfer of money [pause] and with the help of a third party [pause] he should be

able to send money to the account of the recipient.

00:55 – 01:05: [pause] The third parties have restrictions at times, are slower, involves extra

charges and are closed in nature.

01:05 – 01:20: [pause] However, [pause] the transactional procedure in case of a decentralized

system involving the transfer of the cryptocurrencies [pause] is a bit different to that of the

transaction in the centralized process.

01:20 – 01:30: [pause] The transaction of the cryptocurrencies takes place through the help of a

blockchain and a public network. [pause] The blockchain is a public transaction database while

the network is an open network.

Video transcript

00:00 – 00:15: In the centralized form of the system [pause] that is in the banking system [pause]

the transaction generally takes place through the involvement of several third parties or the

intermediaries.

00:15 – 00:30: [pause] In order to facilitate transaction through a centralized system [pause] it is

mandatory to have accounts on both the ends that is the account of the sender and the account of

the recipient.

00:30 – 00:40: [pause] These accounts are in the safe custody of the individual banks on either of

the sides that is for both the receiver and the sender.

00:40 – 00:55: [pause] To have an exchange [pause] the sender must look into his banking

account for his transfer of money [pause] and with the help of a third party [pause] he should be

able to send money to the account of the recipient.

00:55 – 01:05: [pause] The third parties have restrictions at times, are slower, involves extra

charges and are closed in nature.

01:05 – 01:20: [pause] However, [pause] the transactional procedure in case of a decentralized

system involving the transfer of the cryptocurrencies [pause] is a bit different to that of the

transaction in the centralized process.

01:20 – 01:30: [pause] The transaction of the cryptocurrencies takes place through the help of a

blockchain and a public network. [pause] The blockchain is a public transaction database while

the network is an open network.

8THE POTENTIAL IMPACT OF CRYPTOCURRENCY ON THE BANKING INDUSTRY

01:30 – 01:40: [paused] Being decentralized in nature, [pause] the transactions of the

cryptocurrencies does not involve any third parties.

01:40 – 01:50: [pause] In order to send digital currencies, [pause] a sender must have an

encrypted account where the cryptocurrencies are stored [pause] and he can directly send the

assets to the recipient’s account through the help of the open network.

01:50 – 02:00: [pause] This network is a peer to peer network [pause] that is much secured than

the existing bank accounts and supports instant transfer unlike the centralized networks.

01:30 – 01:40: [paused] Being decentralized in nature, [pause] the transactions of the

cryptocurrencies does not involve any third parties.

01:40 – 01:50: [pause] In order to send digital currencies, [pause] a sender must have an

encrypted account where the cryptocurrencies are stored [pause] and he can directly send the

assets to the recipient’s account through the help of the open network.

01:50 – 02:00: [pause] This network is a peer to peer network [pause] that is much secured than

the existing bank accounts and supports instant transfer unlike the centralized networks.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9THE POTENTIAL IMPACT OF CRYPTOCURRENCY ON THE BANKING INDUSTRY

References

Ali, R., Barrdear, J., Clews, R., & Southgate, J. (2014). Innovations in payment technologies and

the emergence of digital currencies.

Ally, M., Gardiner, M., & Lane, M. (2016). The potential impact of digital currencies on the

Australian economy. arXiv preprint arXiv:1606.02462.

Bech, M. L., & Garratt, R. (2017). Central bank cryptocurrencies.

Böhme, R., Christin, N., Edelman, B., & Moore, T. (2015). Bitcoin: Economics, technology, and

governance. Journal of Economic Perspectives, 29(2), 213-38.

De Filippi, P. (2014). Bitcoin: a regulatory nightmare to a libertarian dream.

Décourt, R. F., Chohan, U. W., & Perugini, M. L. (2017). BITCOIN RETURNS AND THE

MONDAY EFFECT. Horizontes Empresariales, 16(2).

Fanning, K., & Centers, D. P. (2016). Blockchain and its coming impact on financial

services. Journal of Corporate Accounting & Finance, 27(5), 53-57.

Iansiti, M., & Lakhani, K. R. (2017). The truth about blockchain. Harvard Business

Review, 95(1), 118-127.

Iwamura, M., Kitamura, Y., Matsumoto, T., & Saito, K. (2014). Can we stabilize the price of a

Cryptocurrency?: Understanding the design of Bitcoin and its potential to compete with

Central Bank money.

Katyal, N. (2013). Disruptive Technologies and the Law. Geo. LJ, 102, 1685.

References

Ali, R., Barrdear, J., Clews, R., & Southgate, J. (2014). Innovations in payment technologies and

the emergence of digital currencies.

Ally, M., Gardiner, M., & Lane, M. (2016). The potential impact of digital currencies on the

Australian economy. arXiv preprint arXiv:1606.02462.

Bech, M. L., & Garratt, R. (2017). Central bank cryptocurrencies.

Böhme, R., Christin, N., Edelman, B., & Moore, T. (2015). Bitcoin: Economics, technology, and

governance. Journal of Economic Perspectives, 29(2), 213-38.

De Filippi, P. (2014). Bitcoin: a regulatory nightmare to a libertarian dream.

Décourt, R. F., Chohan, U. W., & Perugini, M. L. (2017). BITCOIN RETURNS AND THE

MONDAY EFFECT. Horizontes Empresariales, 16(2).

Fanning, K., & Centers, D. P. (2016). Blockchain and its coming impact on financial

services. Journal of Corporate Accounting & Finance, 27(5), 53-57.

Iansiti, M., & Lakhani, K. R. (2017). The truth about blockchain. Harvard Business

Review, 95(1), 118-127.

Iwamura, M., Kitamura, Y., Matsumoto, T., & Saito, K. (2014). Can we stabilize the price of a

Cryptocurrency?: Understanding the design of Bitcoin and its potential to compete with

Central Bank money.

Katyal, N. (2013). Disruptive Technologies and the Law. Geo. LJ, 102, 1685.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10THE POTENTIAL IMPACT OF CRYPTOCURRENCY ON THE BANKING INDUSTRY

MacDonald, T. J., Allen, D. W., & Potts, J. (2016). Blockchains and the boundaries of self-

organized economies: Predictions for the future of banking. In Banking Beyond Banks

and Money (pp. 279-296). Springer, Cham.

Pilkington, M. (2016). 11 Blockchain technology: principles and applications. Research

handbook on digital transformations, 225.

MacDonald, T. J., Allen, D. W., & Potts, J. (2016). Blockchains and the boundaries of self-

organized economies: Predictions for the future of banking. In Banking Beyond Banks

and Money (pp. 279-296). Springer, Cham.

Pilkington, M. (2016). 11 Blockchain technology: principles and applications. Research

handbook on digital transformations, 225.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.