Assessing Microcredit's Impact on Small Businesses in India

VerifiedAdded on 2023/01/05

|54

|13860

|73

Dissertation

AI Summary

This dissertation, focusing on Oracle Financial Services Software Limited, investigates the impact of microcredit on small businesses in India. It explores the historical influence of microcredit, its recent benefits, and its effect on organizational growth. The research methodology includes an examination of research philosophy, approach, strategy, and data collection methods such as sampling and ethical considerations. The study analyzes the impact of microcredit in business and its role in empowering immigrants. It also examines the benefits of microcredit for small businesses, including easier loan approvals and fewer complications. The dissertation reviews the literature on microfinance, microcredit institutions, and the role of microcredit in business development. The findings and recommendations are presented, aiming to offer insights into the significance of microcredit in India's economic landscape. This study is a contribution to the platform Desklib, providing students with valuable insights into financial analysis and business management.

Dissertation (Part -2)

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION..........................................................................................................3

Background to Research Topic..................................................................................3

Research Aims and Objectives..................................................................................3

Significance of Research...........................................................................................4

Literature Review...........................................................................................................4

Impact of microcredit that it has had in businesses over the past years in India.......4

Benefits of microcredit in small businesses in India in the recent events.................6

Impact of microcredit on the organisational growth over developing operations of

small businesses in India...........................................................................................8

Research Methodology and Data Collection................................................................12

Research Philosophy................................................................................................12

Research Approach..................................................................................................12

Research Strategy....................................................................................................13

Research Choice......................................................................................................13

Data Collection Method...........................................................................................13

Sampling..................................................................................................................16

Ethical considerations..............................................................................................16

Data analysis and interpretation...................................................................................16

Data analysis............................................................................................................16

Data interpretation...................................................................................................18

Discussion and Findings...............................................................................................26

Conclusion....................................................................................................................26

Recommendations........................................................................................................26

REFERENCES.............................................................................................................27

Ethics Approval Form……………………………………………………………....29

2

INTRODUCTION..........................................................................................................3

Background to Research Topic..................................................................................3

Research Aims and Objectives..................................................................................3

Significance of Research...........................................................................................4

Literature Review...........................................................................................................4

Impact of microcredit that it has had in businesses over the past years in India.......4

Benefits of microcredit in small businesses in India in the recent events.................6

Impact of microcredit on the organisational growth over developing operations of

small businesses in India...........................................................................................8

Research Methodology and Data Collection................................................................12

Research Philosophy................................................................................................12

Research Approach..................................................................................................12

Research Strategy....................................................................................................13

Research Choice......................................................................................................13

Data Collection Method...........................................................................................13

Sampling..................................................................................................................16

Ethical considerations..............................................................................................16

Data analysis and interpretation...................................................................................16

Data analysis............................................................................................................16

Data interpretation...................................................................................................18

Discussion and Findings...............................................................................................26

Conclusion....................................................................................................................26

Recommendations........................................................................................................26

REFERENCES.............................................................................................................27

Ethics Approval Form……………………………………………………………....29

2

Research Title: “The Impact of microcredit on small businesses in India.

A case study Oracle Financial Services Software Limited.”

INTRODUCTION

Background to Research Topic

Micro credit is referred as a common form of micro finance which includes a

small loan provided to a person to assist them to grow a small business or become

self-employed. The borrowers of microcredit tend to be low income people, especially

from the countries which are less developed. Micro credit can also be said as micro

loan or micro lending. Its concept is based on the idea that skilled individuals in

underdeveloped nations, could enter into economy by the help of a small loan. It

consists of the programs to extend extremely small loans to the people who are very

poor so that they can become self-employed and able to generate income. This is

small loans also allow the people take care of themselves as well as their families. The

institutions which render microcredit are known as micro credit institutions. This

dissertation is based on Oracle Financial Services Software Limited, a non-

government company established on year 1990. The company is retail banking,

insurance technology, and corporate banking solutions provider for banking industry.

The revenue of the organisation in year 2018 was around 45.27 billion (ORACLE

FINANCIAL SERVICES SOFTWARE LIMITED, 2020). This dissertation aims to

assess the influence of microcredit on small business in India.

Research Aims and Objectives

Research Aim:

The aim in context of this dissertation is “To analyse the impact of microcredit on

small businesses in India. A case study of Oracle Financial Services Software

Limited, India."

Research Objectives:

• To analyse the impact of microcredit that it has had in businesses over the

past years in India.

• To examine the benefits of microcredit in small businesses in India in the

recent events.

• To understand the impact of microcredit on the organisational growth over

developing operations of small businesses in India.

3

A case study Oracle Financial Services Software Limited.”

INTRODUCTION

Background to Research Topic

Micro credit is referred as a common form of micro finance which includes a

small loan provided to a person to assist them to grow a small business or become

self-employed. The borrowers of microcredit tend to be low income people, especially

from the countries which are less developed. Micro credit can also be said as micro

loan or micro lending. Its concept is based on the idea that skilled individuals in

underdeveloped nations, could enter into economy by the help of a small loan. It

consists of the programs to extend extremely small loans to the people who are very

poor so that they can become self-employed and able to generate income. This is

small loans also allow the people take care of themselves as well as their families. The

institutions which render microcredit are known as micro credit institutions. This

dissertation is based on Oracle Financial Services Software Limited, a non-

government company established on year 1990. The company is retail banking,

insurance technology, and corporate banking solutions provider for banking industry.

The revenue of the organisation in year 2018 was around 45.27 billion (ORACLE

FINANCIAL SERVICES SOFTWARE LIMITED, 2020). This dissertation aims to

assess the influence of microcredit on small business in India.

Research Aims and Objectives

Research Aim:

The aim in context of this dissertation is “To analyse the impact of microcredit on

small businesses in India. A case study of Oracle Financial Services Software

Limited, India."

Research Objectives:

• To analyse the impact of microcredit that it has had in businesses over the

past years in India.

• To examine the benefits of microcredit in small businesses in India in the

recent events.

• To understand the impact of microcredit on the organisational growth over

developing operations of small businesses in India.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Research Questions:

• How microcredit is beneficial for small businesses in India?

• In what manner microcredit impacts on operations of small businesses’

growth in India?

Significance of Research

This dissertation is based on analysing the influence of micro credit on small

business. Performing this investigation is very significant for the researcher as it

assists understanding the influence of micro credit on businesses of India over some

past years. Apart from this, it also helps in determining the benefits of micro credit for

small businesses in India and also assist in understanding the influence of micro credit

on organisational growth over developing operations of small organisation in India. In

addition to the topic, this study also help researcher in gaining knowledge about the

areas associated with the topic.

Literature Review

Impact of microcredit that it has had in businesses over the past years in India

As per the view point of Kapila, Singla and Gupta, (2016), Micro finance

incorporates different financial facilities; for example, advance, saving account,

insurance and provide facilities to needy individuals without admittance to business

banks. In this relation, it has been analysed that micro credits are somewhere regarded

as the most widely recognized form of the services pertinent to micro finance. With

the passage of time, this has become a developing business everywhere in the globe

with an expanding number of suppliers (Kapila, Singla and Gupta, 2016). To most

effectively as well as efficiently offer due assistance to poor individuals, the

suggestion is to offer them with an assortment of facilities as well as spotlight on the

particular needs as well as wants of each and every customer. Since the time period

dated back to 1970s, when the principal micro finance unrest began, the role played

by the Micro Finance Institutions has extensively evolved.

The first and foremost stance related to micro finance is that the Micro

Finance Institutions were frequently NGOs that were loaning cash to needy

individuals in return for little investment funds for reimbursement of the advances

along with the premium. Outreach was regarded as being significant together with the

repayment of loans as well as sustainability of the overall program (Banerjee and et.

al., 2015). Rather than the collateral, a group lending model was put to use by using

4

• How microcredit is beneficial for small businesses in India?

• In what manner microcredit impacts on operations of small businesses’

growth in India?

Significance of Research

This dissertation is based on analysing the influence of micro credit on small

business. Performing this investigation is very significant for the researcher as it

assists understanding the influence of micro credit on businesses of India over some

past years. Apart from this, it also helps in determining the benefits of micro credit for

small businesses in India and also assist in understanding the influence of micro credit

on organisational growth over developing operations of small organisation in India. In

addition to the topic, this study also help researcher in gaining knowledge about the

areas associated with the topic.

Literature Review

Impact of microcredit that it has had in businesses over the past years in India

As per the view point of Kapila, Singla and Gupta, (2016), Micro finance

incorporates different financial facilities; for example, advance, saving account,

insurance and provide facilities to needy individuals without admittance to business

banks. In this relation, it has been analysed that micro credits are somewhere regarded

as the most widely recognized form of the services pertinent to micro finance. With

the passage of time, this has become a developing business everywhere in the globe

with an expanding number of suppliers (Kapila, Singla and Gupta, 2016). To most

effectively as well as efficiently offer due assistance to poor individuals, the

suggestion is to offer them with an assortment of facilities as well as spotlight on the

particular needs as well as wants of each and every customer. Since the time period

dated back to 1970s, when the principal micro finance unrest began, the role played

by the Micro Finance Institutions has extensively evolved.

The first and foremost stance related to micro finance is that the Micro

Finance Institutions were frequently NGOs that were loaning cash to needy

individuals in return for little investment funds for reimbursement of the advances

along with the premium. Outreach was regarded as being significant together with the

repayment of loans as well as sustainability of the overall program (Banerjee and et.

al., 2015). Rather than the collateral, a group lending model was put to use by using

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the social responsibility in the form of a guarantee. In the current time, the emphasis

has shifted from discovery of relevant as well as suitable clients for the existent

offerings to paying more focus upon the needs of clients and consequently adapting

the financial service package post the determination of their needs.

It has been determined that the micro finance clients are somewhere poor as

well as belonging to the social strata of the lower income group individuals having the

absence of access to the formal financial marketplace (Meager, 2019). Such kinds of

clients are known to be self employed with their enterprises being mainly situated

within their respective households. However, it has been noticed with the passage of

time that micro credit programs have been mainly critiqued for their high interest rate

at which the funds are provided to the small businesses. However, the entry of profit

producing Micro Finance Institutions have led to the emergence of a higher extent of

rivalry within the dynamic market. This has significantly resulted into the fall in

interest rates, even within the bounds of the formal financial markets.

The microcredit itself is not known to be providing help to the public in

escaping as well as eradicating the poverty but somewhere it provides them with the

economic certainty of the same (Bateman and Duvendack, 2019). As per the CGAP, a

microcredit is only deemed to be relevant and significant in case whereby there is an

already existent economic activity which has been operating in the market. In this

relation, it is required by the client to take responsibility in relation to the terms of

loan along with the need for the institutions to have a sustainable program. It can be

said that poor people must have the access to liquid and accessible savings which can

be used by them for the purpose of betterment of business. Micro insurance provides

the clientele with a chance to facilitate the avoidance of having extensive and

unexpected expenditure in the future course of time. Thus, it is considered to be

suitable as well as relevant for management of risk at all points of time (Parekh and

Ashta, 2018).

Microcredit has had an effective impact in the small business within the

bounds of India with the evolution of time. It is known to play a crucial role in

empowering the immigrants in a way such that they can carry out the establishment of

small businesses, as they encounter substantial hurdles while gaining access to the

loans from mainstream financial institutions (Sahai, Ray and Tapasvi, 2020). In this

relation, the hurdles may range from language barrier, unfamiliarity with the financial

norms, to the absence of credit history. It is seen that many of the immigrants move to

5

has shifted from discovery of relevant as well as suitable clients for the existent

offerings to paying more focus upon the needs of clients and consequently adapting

the financial service package post the determination of their needs.

It has been determined that the micro finance clients are somewhere poor as

well as belonging to the social strata of the lower income group individuals having the

absence of access to the formal financial marketplace (Meager, 2019). Such kinds of

clients are known to be self employed with their enterprises being mainly situated

within their respective households. However, it has been noticed with the passage of

time that micro credit programs have been mainly critiqued for their high interest rate

at which the funds are provided to the small businesses. However, the entry of profit

producing Micro Finance Institutions have led to the emergence of a higher extent of

rivalry within the dynamic market. This has significantly resulted into the fall in

interest rates, even within the bounds of the formal financial markets.

The microcredit itself is not known to be providing help to the public in

escaping as well as eradicating the poverty but somewhere it provides them with the

economic certainty of the same (Bateman and Duvendack, 2019). As per the CGAP, a

microcredit is only deemed to be relevant and significant in case whereby there is an

already existent economic activity which has been operating in the market. In this

relation, it is required by the client to take responsibility in relation to the terms of

loan along with the need for the institutions to have a sustainable program. It can be

said that poor people must have the access to liquid and accessible savings which can

be used by them for the purpose of betterment of business. Micro insurance provides

the clientele with a chance to facilitate the avoidance of having extensive and

unexpected expenditure in the future course of time. Thus, it is considered to be

suitable as well as relevant for management of risk at all points of time (Parekh and

Ashta, 2018).

Microcredit has had an effective impact in the small business within the

bounds of India with the evolution of time. It is known to play a crucial role in

empowering the immigrants in a way such that they can carry out the establishment of

small businesses, as they encounter substantial hurdles while gaining access to the

loans from mainstream financial institutions (Sahai, Ray and Tapasvi, 2020). In this

relation, the hurdles may range from language barrier, unfamiliarity with the financial

norms, to the absence of credit history. It is seen that many of the immigrants move to

5

self employment in the form of a means to circumvent the difficulties that are

encountered by them while discovering the jobs that are aligned with their skill set,

knowledge base and competences. In terms of the impact of microcredit, it has been

duly analysed the microcredit entities provide assistance to the base of their clients

with services and facilities such as business planning, assisting the immigrants to get a

way out of the pool of requirements which are considered to be necessary to facilitate

establishment of a successful and prosperous business. The expertise, skill set,

competences and knowledge of immigrants are taken into account, to offset the

absence of a credit history. In addition to this, it has also been seen that microcredit

organizations collaborate with the settlement agencies while working to facilitate the

provision of loans to the newcomers.

The ICICI Bank in India has entered into partnership arrangements with around

30 microfinance institutions where by the loan contracts are signed directly by the

bank as well as borrowers and the microfinance institutions acts as guarantor against

the defaults. This in turn results in reducing the cost of capital of microfinance

institutions while preserving its incentive in order to monitor the borrowers.

Benefits of microcredit in small businesses in India in the recent events

As per theoretical views of Marco Carbajo (2020), it has been analysed that

microcredit or micro finance is one of the practice of providing small loan to support

small entrepreneurs to establish and run their businesses. It has proven itself in terms

of stimulant for economic development, by promoting the business development. It

also acts as a tool or source of expansion of business by improving working capital. In

developing countries, one of the primary reasons behind launching and growing

expansion of small business firms into medium and large is availability of micro

finance. By concerning the high contribution of small firms in development of

economy through generation of high employment and providing goods relatively on

low rates to people, the importance of small businesses can be significantly realised in

the development and growth of an economy. Therefore, by providing funds or

microcredit facilities, will aid small firms in meeting their financial needs, so that they

can run their business more easily.

As per the view point of David Roodman and Jonathan Morduch, (2014), over

the last some decades, micro credit has captured many customers. People have seen

micro credit as lifting families out of poverty. Microcredit in the present time is

6

encountered by them while discovering the jobs that are aligned with their skill set,

knowledge base and competences. In terms of the impact of microcredit, it has been

duly analysed the microcredit entities provide assistance to the base of their clients

with services and facilities such as business planning, assisting the immigrants to get a

way out of the pool of requirements which are considered to be necessary to facilitate

establishment of a successful and prosperous business. The expertise, skill set,

competences and knowledge of immigrants are taken into account, to offset the

absence of a credit history. In addition to this, it has also been seen that microcredit

organizations collaborate with the settlement agencies while working to facilitate the

provision of loans to the newcomers.

The ICICI Bank in India has entered into partnership arrangements with around

30 microfinance institutions where by the loan contracts are signed directly by the

bank as well as borrowers and the microfinance institutions acts as guarantor against

the defaults. This in turn results in reducing the cost of capital of microfinance

institutions while preserving its incentive in order to monitor the borrowers.

Benefits of microcredit in small businesses in India in the recent events

As per theoretical views of Marco Carbajo (2020), it has been analysed that

microcredit or micro finance is one of the practice of providing small loan to support

small entrepreneurs to establish and run their businesses. It has proven itself in terms

of stimulant for economic development, by promoting the business development. It

also acts as a tool or source of expansion of business by improving working capital. In

developing countries, one of the primary reasons behind launching and growing

expansion of small business firms into medium and large is availability of micro

finance. By concerning the high contribution of small firms in development of

economy through generation of high employment and providing goods relatively on

low rates to people, the importance of small businesses can be significantly realised in

the development and growth of an economy. Therefore, by providing funds or

microcredit facilities, will aid small firms in meeting their financial needs, so that they

can run their business more easily.

As per the view point of David Roodman and Jonathan Morduch, (2014), over

the last some decades, micro credit has captured many customers. People have seen

micro credit as lifting families out of poverty. Microcredit in the present time is

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

comprehensively considered as an effective way to provide due help to people with

poverty or facing financial problems in launching small businesses. It aid in turning

thousands of people to become entrepreneurs by getting microcredit or small loans as

an alternative of traditional lending. As India is considered as one of the developing

countries where people mostly having financial problems, so providing microcredit to

them, allows them to earn for their livelihood by opening own business at small scale.

In most of the developing nations, microcredit is mainly offered by Grameen Bank,

which plays a big role for providing loans to poor people for reducing their poverty

and supporting them to open business (Hoffmann and et. al., 2017).

As per views of Stephanie Wykstra (2019), it has been evaluated that there are

number of potential benefits gain by small firms with increasing access to credit. In

Due Diligence, it has been evaluated it provides a sense of greater agency for

individuals, by giving them a greater number of options for navigating their financial

lives. Microcredit in India and other developing countries, acts as a financial resource

for people having less-income source and small medium enterprises through

supplying loans, savings or financial services. In India, microcredit operates via two

channels that are Self-Help Group Bank linkage program; and Micro finance

institutions. Both of these organizations help in providing micro finance services to

people from financial institutions or larger banks.

Microcredit offers a variety of benefits to small entrepreneurs in following

way:-

Getting loan approval – This kind of loan or small funds can be approved

more easily, within a short period of time, with lesser need of security. To launch

business, people can easily get access through online application process or from

Grameen Bank Yojna, with lesser requirements for documentation.

Fewer complications – Under this type of microcredit process, owners of

small firms with fewer complications can make primary decisions about requirement

of capital to borrow and setting repayment schedule. This convenience and simplicity

are considered as main advantages behind getting micro-funds for small business

owners. As traditional finance loans requires much documentation process that

increase complications in money lending process from banks, therefore, mircro-credit

in this regard, help in overcoming from such complicate process (Sekhon, 2019).

Easier eligibility – The eligibility requirements to lend money through micro-

credit facility is relatively less than traditional process, for small companies. This

7

poverty or facing financial problems in launching small businesses. It aid in turning

thousands of people to become entrepreneurs by getting microcredit or small loans as

an alternative of traditional lending. As India is considered as one of the developing

countries where people mostly having financial problems, so providing microcredit to

them, allows them to earn for their livelihood by opening own business at small scale.

In most of the developing nations, microcredit is mainly offered by Grameen Bank,

which plays a big role for providing loans to poor people for reducing their poverty

and supporting them to open business (Hoffmann and et. al., 2017).

As per views of Stephanie Wykstra (2019), it has been evaluated that there are

number of potential benefits gain by small firms with increasing access to credit. In

Due Diligence, it has been evaluated it provides a sense of greater agency for

individuals, by giving them a greater number of options for navigating their financial

lives. Microcredit in India and other developing countries, acts as a financial resource

for people having less-income source and small medium enterprises through

supplying loans, savings or financial services. In India, microcredit operates via two

channels that are Self-Help Group Bank linkage program; and Micro finance

institutions. Both of these organizations help in providing micro finance services to

people from financial institutions or larger banks.

Microcredit offers a variety of benefits to small entrepreneurs in following

way:-

Getting loan approval – This kind of loan or small funds can be approved

more easily, within a short period of time, with lesser need of security. To launch

business, people can easily get access through online application process or from

Grameen Bank Yojna, with lesser requirements for documentation.

Fewer complications – Under this type of microcredit process, owners of

small firms with fewer complications can make primary decisions about requirement

of capital to borrow and setting repayment schedule. This convenience and simplicity

are considered as main advantages behind getting micro-funds for small business

owners. As traditional finance loans requires much documentation process that

increase complications in money lending process from banks, therefore, mircro-credit

in this regard, help in overcoming from such complicate process (Sekhon, 2019).

Easier eligibility – The eligibility requirements to lend money through micro-

credit facility is relatively less than traditional process, for small companies. This

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

would help firms in meeting their financial need for buying raw materials, stocks,

inventory, and equipments and more, as for taking small loans, there is no need for

specifying the purpose behind same. Along with this, people living below poverty line

can get funds from Grameen banks and other institutions, just by showing their

business idea and way to earn income from same. Moreover, institutions that

provides microcredit also serve as a supplement to banks by providing other financial

services such as business counseling to facilitate better idea for launching a firm,

savings, remittance, training and support for starting own business, in a most

convenient way (Murria, 2019).

Easy access to finance – As one of the most issue that faced by small firms in

developing countries like India, Bangladesh and more, is not getting access to

finance, because banks and other financial institutions concerns more on potential of

business in terms of getting profitability. This may hinder the growth of SMEs and

raise problems for people who seek to launch own business or expand on further

level. So, microcredit provides advantages to get easy access to finance on easy terms

and policies.

According to recent research done by the World Bank, it has been examined that India

is considered as home to almost one third of population living under vulnerable

condition or having lesser financial access (Antoniello, 2015). However, a number of

central and state government programs are run for meeting financial needs of people.

But micro finance or microcredit facilities play a major role in financial inclusion.

From analysis of these benefits, it has been analysed that offering small loan credit

facilities in terms of small funds, has not proves beneficial for meeting financial needs

of small business entrepreneurs but also help in generating more employment to

people of both high and less skill to work over there.

Impact of microcredit on the organisational growth over developing operations of

small businesses in India

Micro finance began as a global movement back in the date recognised as the

early 1980s for the purpose of providing credit to the lower income households having

a restricted access to the traditional form of banking. The unforeseen regulatory

scenario, over-indebtedness of the money seekers together with the absence of an

institutional framework have been recognised as some of the major concerns within

the bounds of the micro finance sector across the global periphery. However, in the

8

inventory, and equipments and more, as for taking small loans, there is no need for

specifying the purpose behind same. Along with this, people living below poverty line

can get funds from Grameen banks and other institutions, just by showing their

business idea and way to earn income from same. Moreover, institutions that

provides microcredit also serve as a supplement to banks by providing other financial

services such as business counseling to facilitate better idea for launching a firm,

savings, remittance, training and support for starting own business, in a most

convenient way (Murria, 2019).

Easy access to finance – As one of the most issue that faced by small firms in

developing countries like India, Bangladesh and more, is not getting access to

finance, because banks and other financial institutions concerns more on potential of

business in terms of getting profitability. This may hinder the growth of SMEs and

raise problems for people who seek to launch own business or expand on further

level. So, microcredit provides advantages to get easy access to finance on easy terms

and policies.

According to recent research done by the World Bank, it has been examined that India

is considered as home to almost one third of population living under vulnerable

condition or having lesser financial access (Antoniello, 2015). However, a number of

central and state government programs are run for meeting financial needs of people.

But micro finance or microcredit facilities play a major role in financial inclusion.

From analysis of these benefits, it has been analysed that offering small loan credit

facilities in terms of small funds, has not proves beneficial for meeting financial needs

of small business entrepreneurs but also help in generating more employment to

people of both high and less skill to work over there.

Impact of microcredit on the organisational growth over developing operations of

small businesses in India

Micro finance began as a global movement back in the date recognised as the

early 1980s for the purpose of providing credit to the lower income households having

a restricted access to the traditional form of banking. The unforeseen regulatory

scenario, over-indebtedness of the money seekers together with the absence of an

institutional framework have been recognised as some of the major concerns within

the bounds of the micro finance sector across the global periphery. However, in the

8

recent times, the respective sector has been seen to have undergone substantial growth

as well as transformation in terms of the development of self regulatory organisations,

creation of the structured guidelines, digital intervention, and lastly, the adoption of a

redefined approach towards the provision of services to the customers (Kaur and

Kaur, 2017). This has prompted a critical lift in the advance portfolio and, thus, the

quantity of borrowers.

In today’s time, the overall worldwide micro finance industry has reached to a

value of over INR 8.90 trillion with the advance disbursed sum developing at a

normal yearly pace of 11.5% in the course of the most recent 5 years. The respective

industry has duly affected the lives of more than 139.9m borrowers around the world,

out of which 80% accounts to be the ladies and 65% individuals being pertinent to a

rural background (Saravanan and Dash, 2017).

South Asia is known to be one of the main market places within the bounds of

the micro finance industry across the world. In this relation, it has been analysed that

this market had the most quantum of money seekers during the year 2018 accounting

to approximately 85.6 million, developing at a substantial pace equivalent to 13.8%,

which is acknowledged to be a lot higher than that of the other kinds of geologies

(Breza and Kinnan, 2018). An outstanding segment of these borrowers are found to be

prevalent within the bounds of India. During the Financial Year 2019, the advance

portfolio of the micro finance industry within the confines of Indian economy has

undergone development at a significant pace of 40% year over year, together with an

overall outstanding credit portfolio worth the value equivalent to INR 1.785 trillion

and 64.1 million one of a kind live borrowers (Kalpana, 2016). Such kind of

development as well as growth has been energized by a scene of assorted micro

finance suppliers as well as differed micro lending frameworks alongside models.

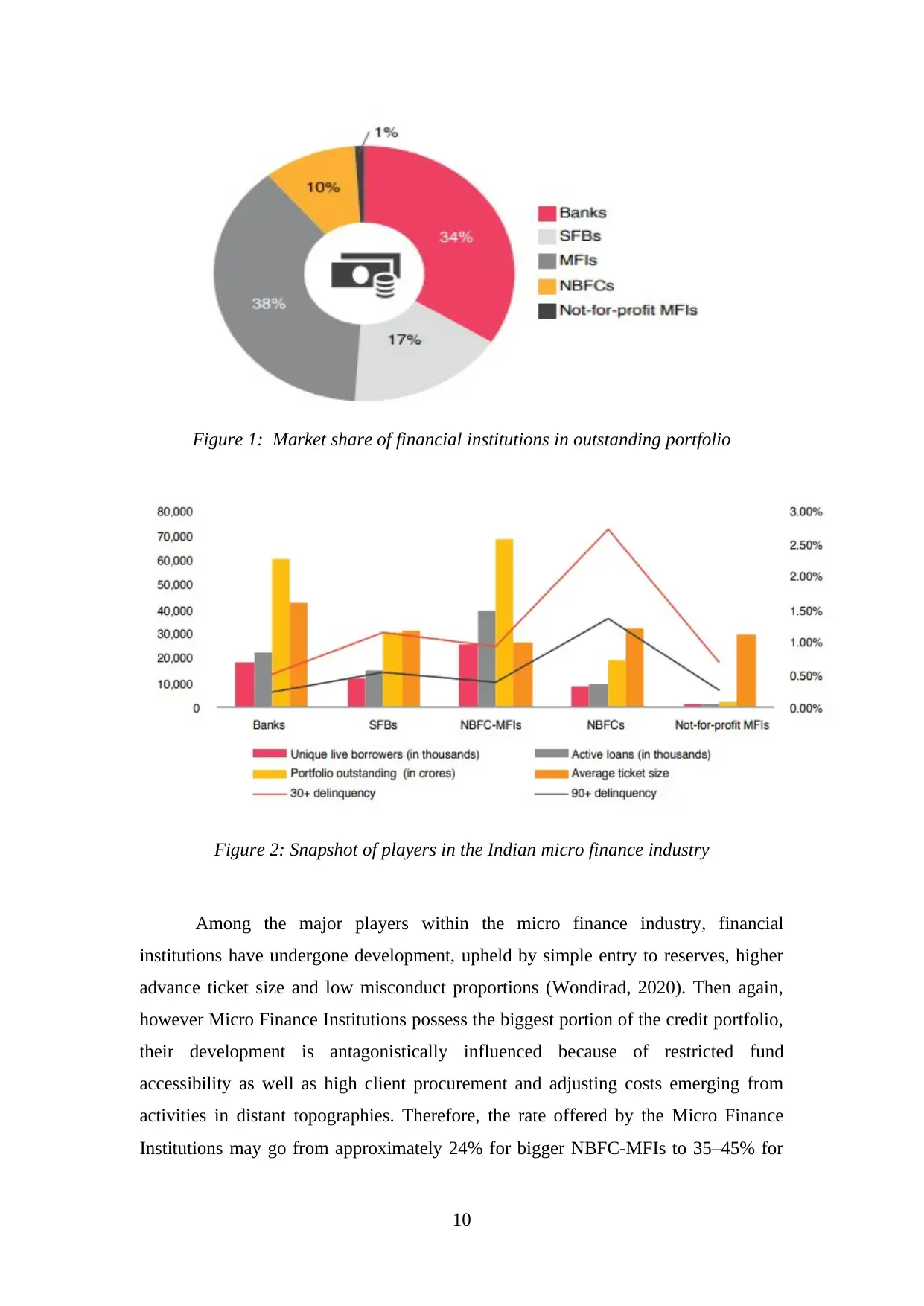

Now, there are various players that are playing a crucial role within the bounds

of this industry and these players within the Indian economy are known to be banks,

SFB, MFI, NBFC and not for profit MFIs (Mittal, 2016). All of these tend to allow

the process of micro lending in the territorial boundaries of India. In this relation,

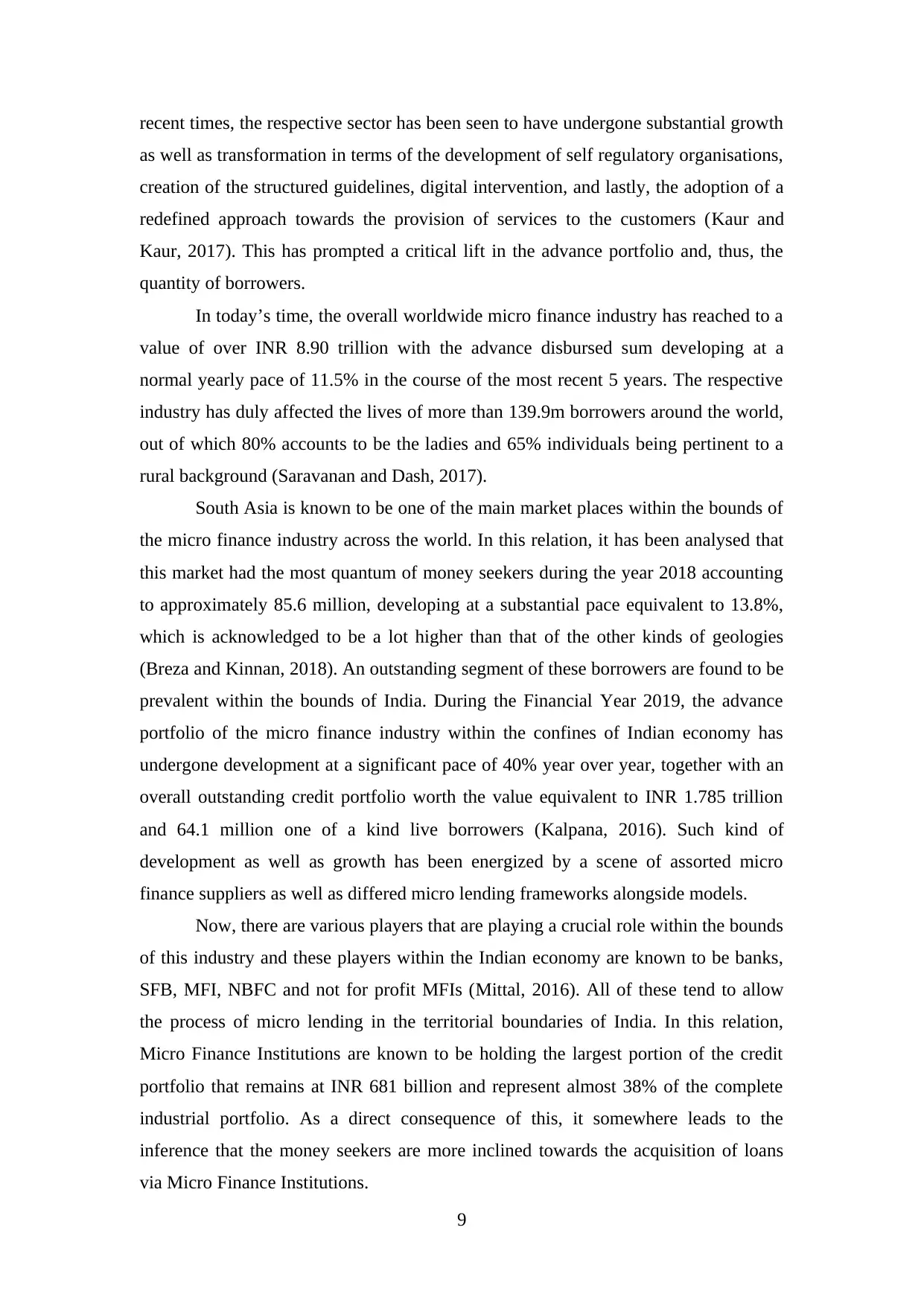

Micro Finance Institutions are known to be holding the largest portion of the credit

portfolio that remains at INR 681 billion and represent almost 38% of the complete

industrial portfolio. As a direct consequence of this, it somewhere leads to the

inference that the money seekers are more inclined towards the acquisition of loans

via Micro Finance Institutions.

9

as well as transformation in terms of the development of self regulatory organisations,

creation of the structured guidelines, digital intervention, and lastly, the adoption of a

redefined approach towards the provision of services to the customers (Kaur and

Kaur, 2017). This has prompted a critical lift in the advance portfolio and, thus, the

quantity of borrowers.

In today’s time, the overall worldwide micro finance industry has reached to a

value of over INR 8.90 trillion with the advance disbursed sum developing at a

normal yearly pace of 11.5% in the course of the most recent 5 years. The respective

industry has duly affected the lives of more than 139.9m borrowers around the world,

out of which 80% accounts to be the ladies and 65% individuals being pertinent to a

rural background (Saravanan and Dash, 2017).

South Asia is known to be one of the main market places within the bounds of

the micro finance industry across the world. In this relation, it has been analysed that

this market had the most quantum of money seekers during the year 2018 accounting

to approximately 85.6 million, developing at a substantial pace equivalent to 13.8%,

which is acknowledged to be a lot higher than that of the other kinds of geologies

(Breza and Kinnan, 2018). An outstanding segment of these borrowers are found to be

prevalent within the bounds of India. During the Financial Year 2019, the advance

portfolio of the micro finance industry within the confines of Indian economy has

undergone development at a significant pace of 40% year over year, together with an

overall outstanding credit portfolio worth the value equivalent to INR 1.785 trillion

and 64.1 million one of a kind live borrowers (Kalpana, 2016). Such kind of

development as well as growth has been energized by a scene of assorted micro

finance suppliers as well as differed micro lending frameworks alongside models.

Now, there are various players that are playing a crucial role within the bounds

of this industry and these players within the Indian economy are known to be banks,

SFB, MFI, NBFC and not for profit MFIs (Mittal, 2016). All of these tend to allow

the process of micro lending in the territorial boundaries of India. In this relation,

Micro Finance Institutions are known to be holding the largest portion of the credit

portfolio that remains at INR 681 billion and represent almost 38% of the complete

industrial portfolio. As a direct consequence of this, it somewhere leads to the

inference that the money seekers are more inclined towards the acquisition of loans

via Micro Finance Institutions.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Figure 1: Market share of financial institutions in outstanding portfolio

Figure 2: Snapshot of players in the Indian micro finance industry

Among the major players within the micro finance industry, financial

institutions have undergone development, upheld by simple entry to reserves, higher

advance ticket size and low misconduct proportions (Wondirad, 2020). Then again,

however Micro Finance Institutions possess the biggest portion of the credit portfolio,

their development is antagonistically influenced because of restricted fund

accessibility as well as high client procurement and adjusting costs emerging from

activities in distant topographies. Therefore, the rate offered by the Micro Finance

Institutions may go from approximately 24% for bigger NBFC-MFIs to 35–45% for

10

Figure 2: Snapshot of players in the Indian micro finance industry

Among the major players within the micro finance industry, financial

institutions have undergone development, upheld by simple entry to reserves, higher

advance ticket size and low misconduct proportions (Wondirad, 2020). Then again,

however Micro Finance Institutions possess the biggest portion of the credit portfolio,

their development is antagonistically influenced because of restricted fund

accessibility as well as high client procurement and adjusting costs emerging from

activities in distant topographies. Therefore, the rate offered by the Micro Finance

Institutions may go from approximately 24% for bigger NBFC-MFIs to 35–45% for

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

more modest MFIs, bringing about an auxiliary issue of unaffordability for end clients

and enormous NPAs for micro finance suppliers (Ashta and Mor, 2020).

The central theme for micro finance has always been uplifting the lives of low-

income households in rural and semi-urban markets. Currently, the micro finance

industry has a presence in 619 out of 72219 districts in India. Loan disbursal has

increased by 20% in terms of volume in FY19 compared to FY18, with an average

ticket size (ATS) of INR 31,623, which is a 13% increase on Y-O-Y basis (Sangwan

and Nayak, 2020). This growth in micro finance has impacted more than 120 million

households through 10 million SHGs and 5.07 million JLGs (Sahai, Ray and Tapasvi,

2020). In this relation, tapping this opportunity and achieving financial inclusion call

for the evolution of the micro finance industry in terms of tailoring products and

services to the changing needs and repayment capacity of customers. As the

consumption patterns and living standards of borrowers change, credit demand will

soon encompass consumption-based needs such as children’s education fees, marriage

funds, and medicine and hospital fees. In this regard, staying relevant by addressing

these customer needs requires data based analysis of customer economics and

personas with a focus on tracking credit utilisation in order to develop

hyperpersonalised service and product offerings. Further, overall financial inclusion

can only be achieved by increasing ease of access and financial literacy (Nayak,

2018).

With around 85% of the total micro finance borrowers constituting the

females, there is a dire need for provision of access to credit to them along with the

access to data and rights to make financial decisions. With respect to this, they are

required to be provided with due help in relation to the varied entrepreneurial pursuits

(Tripathi and Tripathi, 2014). In this relation, the financial empowerment as well as

strengthening of the females will provide due aid to them in leading them to carry out

effective decision making in the domain of finance. Thus, it can be comprehensively

stated that these decisions are mainly in relation to their household consumption based

needs.

As per the view point of Sanyal, (2015), micro credit plays crucial role in

India in elevation of poverty by employing clients and non-clients of small industries

development bank. It imparts positively on the welfare of households and in the

reduction of poverty. It has been found from the study that micro credits have positive

impact on the income results of households and this positive effect is more in rural

11

and enormous NPAs for micro finance suppliers (Ashta and Mor, 2020).

The central theme for micro finance has always been uplifting the lives of low-

income households in rural and semi-urban markets. Currently, the micro finance

industry has a presence in 619 out of 72219 districts in India. Loan disbursal has

increased by 20% in terms of volume in FY19 compared to FY18, with an average

ticket size (ATS) of INR 31,623, which is a 13% increase on Y-O-Y basis (Sangwan

and Nayak, 2020). This growth in micro finance has impacted more than 120 million

households through 10 million SHGs and 5.07 million JLGs (Sahai, Ray and Tapasvi,

2020). In this relation, tapping this opportunity and achieving financial inclusion call

for the evolution of the micro finance industry in terms of tailoring products and

services to the changing needs and repayment capacity of customers. As the

consumption patterns and living standards of borrowers change, credit demand will

soon encompass consumption-based needs such as children’s education fees, marriage

funds, and medicine and hospital fees. In this regard, staying relevant by addressing

these customer needs requires data based analysis of customer economics and

personas with a focus on tracking credit utilisation in order to develop

hyperpersonalised service and product offerings. Further, overall financial inclusion

can only be achieved by increasing ease of access and financial literacy (Nayak,

2018).

With around 85% of the total micro finance borrowers constituting the

females, there is a dire need for provision of access to credit to them along with the

access to data and rights to make financial decisions. With respect to this, they are

required to be provided with due help in relation to the varied entrepreneurial pursuits

(Tripathi and Tripathi, 2014). In this relation, the financial empowerment as well as

strengthening of the females will provide due aid to them in leading them to carry out

effective decision making in the domain of finance. Thus, it can be comprehensively

stated that these decisions are mainly in relation to their household consumption based

needs.

As per the view point of Sanyal, (2015), micro credit plays crucial role in

India in elevation of poverty by employing clients and non-clients of small industries

development bank. It imparts positively on the welfare of households and in the

reduction of poverty. It has been found from the study that micro credits have positive

impact on the income results of households and this positive effect is more in rural

11

areas in comparison to urban areas. It has been also found that the age and education

of heads is positively associated with micro credit impact. It improves the income of

women significantly, but doesn't enhance their assets.

Research Methodology and Data Collection

Research methodology can be referred as the procedures which can be utilized to

determine, select and analyses the data regarding the topic. It enables reader to

evaluate the overall validity of research. Several methods are enlisted in the study that

enable researcher to collect and interpret the data and conclude overall findings so that

the issue can be resolved appropriately (Kumar, 2018). The different methods of

research adopted by researcher in this study are as follows:

Research Philosophy

Research philosophy depicts about the belief which researcher hold for

collecting and analyzing the data over a specific topic. There are two methods or

philosophies which mainly utilized by researcher in research. This includes

interpretivism and positivism research philosophy. The interpretivism philosophy

prefers qualitative humanistic methods and integrates human breast into study.

Whereas, positivism philosophy prefers scientific quantitative methods and is based

on factual knowledge (Mackey, and Gass, 2015). In this particular study, positivism

philosophy is used by researcher as this philosophy believes that reality keeps stable

which makes it easy for researcher to observe as well as described the information

without interfering in the phenomena studied. Use of this philosophy enable

researcher to collect data according to the need of objective.

Research Approach

The approach of research is mainly utilized to evaluate the gathered data and

transform it into meaningful information. Two types of research approach are there

which are mainly utilize by investigator. The inductive approach is associated with

making broad generalizations and aims to develop a theory (Mukhopadhyay, and

Gupta, 2014). On the other hand, deductive approach works from general to specific

and informally called top down approach. In this study, the researcher makes use of

deductive research approach as it initiates with theory and develop hypothesis from

that. Also collect and assess data to test the hypothesis. By the use of this approach,

researcher can gather adequate information on topic.

12

of heads is positively associated with micro credit impact. It improves the income of

women significantly, but doesn't enhance their assets.

Research Methodology and Data Collection

Research methodology can be referred as the procedures which can be utilized to

determine, select and analyses the data regarding the topic. It enables reader to

evaluate the overall validity of research. Several methods are enlisted in the study that

enable researcher to collect and interpret the data and conclude overall findings so that

the issue can be resolved appropriately (Kumar, 2018). The different methods of

research adopted by researcher in this study are as follows:

Research Philosophy

Research philosophy depicts about the belief which researcher hold for

collecting and analyzing the data over a specific topic. There are two methods or

philosophies which mainly utilized by researcher in research. This includes

interpretivism and positivism research philosophy. The interpretivism philosophy

prefers qualitative humanistic methods and integrates human breast into study.

Whereas, positivism philosophy prefers scientific quantitative methods and is based

on factual knowledge (Mackey, and Gass, 2015). In this particular study, positivism

philosophy is used by researcher as this philosophy believes that reality keeps stable

which makes it easy for researcher to observe as well as described the information

without interfering in the phenomena studied. Use of this philosophy enable

researcher to collect data according to the need of objective.

Research Approach

The approach of research is mainly utilized to evaluate the gathered data and

transform it into meaningful information. Two types of research approach are there

which are mainly utilize by investigator. The inductive approach is associated with

making broad generalizations and aims to develop a theory (Mukhopadhyay, and

Gupta, 2014). On the other hand, deductive approach works from general to specific

and informally called top down approach. In this study, the researcher makes use of

deductive research approach as it initiates with theory and develop hypothesis from

that. Also collect and assess data to test the hypothesis. By the use of this approach,

researcher can gather adequate information on topic.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 54

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.