Integrated Accounting Projects: Tech Impacts on Financial Reporting

VerifiedAdded on 2023/04/04

|22

|4472

|331

Report

AI Summary

This research proposal examines the impact of technology on financial reporting within the accounting field. The study investigates the relationship between technology systems, including data processing, storage, and retrieval, and the quality of financial reports. The objectives include analyzing technology's contribution to financial reporting quality, assessing how technology improves accounting data systems, and determining if it enhances internal financial reporting controls. The research methodology employs a descriptive research design, utilizing questionnaires for data collection and quantitative analysis. The conceptual framework outlines independent variables (technology systems) and dependent variables (financial quality), with hypotheses addressing the impact of data processing, storage, and retrieval on financial report quality. The proposal also acknowledges limitations related to time, funding, and researcher experience. The study aims to contribute insights into the evolving role of technology in enhancing financial reporting processes and outcomes. The research is a continuation of a previous literature review.

Running Head: INTEGRATED ACCOUNTING PROJECTS 1

Integrated Accounting Projects

Name

Affiliation

Date

Integrated Accounting Projects

Name

Affiliation

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTEGRATED ACCOUNTING PROJECTS2

Table of Contents

Abstract..................................................................................................................................................3

Chapter one............................................................................................................................................4

Introduction...........................................................................................................................................4

1. Background....................................................................................................................................4

1.2. The significance of the study and motivation...........................................................................6

1.3. The purpose/objective of the study...........................................................................................7

1.4. Research Problem and Questions.............................................................................................7

1.4.1. Problem statement.................................................................................................................7

1.4.2. Research question..................................................................................................................8

Chapter two...........................................................................................................................................9

2. Conceptual framework..................................................................................................................9

2.2. Hypotheses..................................................................................................................................9

Chapter three.......................................................................................................................................10

Research methodology........................................................................................................................10

3. Introduction.................................................................................................................................10

3.2. Research design........................................................................................................................10

3.3. Target population....................................................................................................................11

3.4. Sample design...........................................................................................................................11

3.5. Data sources.............................................................................................................................12

3.6. Data collection methods...........................................................................................................13

3.7. Data reliability and Validity....................................................................................................13

3.8. Data analysis............................................................................................................................14

3.9. Ethical declaration...................................................................................................................14

3.10. Limitation of the study........................................................................................................15

References............................................................................................................................................18

Appendix:.............................................................................................................................................22

Table of Contents

Abstract..................................................................................................................................................3

Chapter one............................................................................................................................................4

Introduction...........................................................................................................................................4

1. Background....................................................................................................................................4

1.2. The significance of the study and motivation...........................................................................6

1.3. The purpose/objective of the study...........................................................................................7

1.4. Research Problem and Questions.............................................................................................7

1.4.1. Problem statement.................................................................................................................7

1.4.2. Research question..................................................................................................................8

Chapter two...........................................................................................................................................9

2. Conceptual framework..................................................................................................................9

2.2. Hypotheses..................................................................................................................................9

Chapter three.......................................................................................................................................10

Research methodology........................................................................................................................10

3. Introduction.................................................................................................................................10

3.2. Research design........................................................................................................................10

3.3. Target population....................................................................................................................11

3.4. Sample design...........................................................................................................................11

3.5. Data sources.............................................................................................................................12

3.6. Data collection methods...........................................................................................................13

3.7. Data reliability and Validity....................................................................................................13

3.8. Data analysis............................................................................................................................14

3.9. Ethical declaration...................................................................................................................14

3.10. Limitation of the study........................................................................................................15

References............................................................................................................................................18

Appendix:.............................................................................................................................................22

INTEGRATED ACCOUNTING PROJECTS3

Abstract

The relationship between business and technology is still a major concern by most of the

technological and enterprise or business managers. The increased use of technology in the

financial reporting of business illustrates the major relations that exist between technology

challenges and responses in illustrating the future research so as to enhance the alignment that

exists between organizational performance and the adopted technology. The major objective of

this study was to make an analysis of the impacts created by technology on financial reporting.

The study was also guided by other specific objectives such as (i) to measure the rate at which

technology contributes towards the quality of financial reporting, (ii) how an organization

improves its outputs of accounting data system and if the program improves an organization's

control of internal financial reporting. The study involves the use of "descriptive research

design" in order to evaluate the research variables plus the major tools of collecting data. For this

study, the major tool that was considered for collecting data was questionnaire. Also, the study

indicated that quantitative data will be analyzed with inferential and descriptive analysis. The

study indicated that the research will consider the dependent variables (financial quality) as

relevancy, reliability and understandability and independent variables (technology systems) to be

"account8ing data processing, account8ing data storage, and accounting data retrieval." The

study also indicated that the research will involve various limitations such as time, funds, and

inadequate experience of the researchers to collect data in various organizations.

Keywords: financial reporting, technology data, data quality.

Abstract

The relationship between business and technology is still a major concern by most of the

technological and enterprise or business managers. The increased use of technology in the

financial reporting of business illustrates the major relations that exist between technology

challenges and responses in illustrating the future research so as to enhance the alignment that

exists between organizational performance and the adopted technology. The major objective of

this study was to make an analysis of the impacts created by technology on financial reporting.

The study was also guided by other specific objectives such as (i) to measure the rate at which

technology contributes towards the quality of financial reporting, (ii) how an organization

improves its outputs of accounting data system and if the program improves an organization's

control of internal financial reporting. The study involves the use of "descriptive research

design" in order to evaluate the research variables plus the major tools of collecting data. For this

study, the major tool that was considered for collecting data was questionnaire. Also, the study

indicated that quantitative data will be analyzed with inferential and descriptive analysis. The

study indicated that the research will consider the dependent variables (financial quality) as

relevancy, reliability and understandability and independent variables (technology systems) to be

"account8ing data processing, account8ing data storage, and accounting data retrieval." The

study also indicated that the research will involve various limitations such as time, funds, and

inadequate experience of the researchers to collect data in various organizations.

Keywords: financial reporting, technology data, data quality.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTEGRATED ACCOUNTING PROJECTS4

Chapter one

Introduction

1. Background

Currently, the increased use of technology in financial accounting reporting is a new

system. Most of the studies have tried to illustrate the role played by technology in financial

reporting. In this case, financial reporting plays an important role in the organization operations.

All business are required to monitor their financial data that is in line with the activities of the

business. Financial reporting is also made up of various processes where some are complex,

burdensome and others simple. As a result of increased growth of the business by entering into

new markets, acquiring new customers and also maintain the pace of the continued evolution of

technology, the business is supposed to maintain high levels of accuracy, statuary and inventory

records. As a result of the increased number of financial transactions and exposure of errors in

information as a result of the complexity of various accounting systems, businesses are required

to process and store their accounting information with increased storage, processing capacity,

and speed. As a result of this need, financial accounting software systems were introduced and

developed (Hla, & Teru, 2015).

Today, most of the businesses or organizations integrate and automate their business

activities by implementing technology systems. In this case, technology systems are computer-

based or manual systems that are aimed at increasing the control of an organization by assigning

a quantitative role of the present, future, and past financial events. Technology systems play a

vital role in financial reporting such as data maintenance, data knowledge management,

information generation, security or data control, and data collection (Iskandar, 2015).

Chapter one

Introduction

1. Background

Currently, the increased use of technology in financial accounting reporting is a new

system. Most of the studies have tried to illustrate the role played by technology in financial

reporting. In this case, financial reporting plays an important role in the organization operations.

All business are required to monitor their financial data that is in line with the activities of the

business. Financial reporting is also made up of various processes where some are complex,

burdensome and others simple. As a result of increased growth of the business by entering into

new markets, acquiring new customers and also maintain the pace of the continued evolution of

technology, the business is supposed to maintain high levels of accuracy, statuary and inventory

records. As a result of the increased number of financial transactions and exposure of errors in

information as a result of the complexity of various accounting systems, businesses are required

to process and store their accounting information with increased storage, processing capacity,

and speed. As a result of this need, financial accounting software systems were introduced and

developed (Hla, & Teru, 2015).

Today, most of the businesses or organizations integrate and automate their business

activities by implementing technology systems. In this case, technology systems are computer-

based or manual systems that are aimed at increasing the control of an organization by assigning

a quantitative role of the present, future, and past financial events. Technology systems play a

vital role in financial reporting such as data maintenance, data knowledge management,

information generation, security or data control, and data collection (Iskandar, 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTEGRATED ACCOUNTING PROJECTS5

In financial reporting, technology seeks to take part in improving the quantity and quality

of data in order to enhance the business's delivery of services to users hence meeting their needs.

The use of technology in financial reporting helps in recording the financial reports or

transaction s of the business with the help of software and computer. The system is a database-

based application which involves the data transaction and storage in the organization's database.

The users of the system are required to operate their activities on a database with the help of an

interface. Also, the system is required to take the necessary financial reports by accurately

transforming the stored financial information and data. Therefore, in financial accounting,

technology plays an important role in streamlining, integrating and simplifying all the process of

the business at a reduced cost through helping in the presentation of business activities to its

users inform of financial reports. As a result of increased technological innovation, various

businesses to monitor their financial transactions with the help of computerized systems than

using manual systems that involve "the use of physical ledger." A Because of the increased

technological innovation, "computerized accounting systems" have emerged which assist in

producing faithful and accurate financial reports for the organization and other external users

(Khaled, & Abdulqawi, 2015).

1.2. The significance of the study and motivation

This study's significance is aimed at illustrating the required information concerning the

"Impact of technology on financial reporting." Also, the study aims at explaining the effects and

influence created by technological systems on accounting and financial reporting. As a result of

the continued change in technology across the world, modernization has become a major aspect

of technology. As already indicated previously in the literature review, very many countries

across the world use technology for accounting and financial reporting. This indicates that

In financial reporting, technology seeks to take part in improving the quantity and quality

of data in order to enhance the business's delivery of services to users hence meeting their needs.

The use of technology in financial reporting helps in recording the financial reports or

transaction s of the business with the help of software and computer. The system is a database-

based application which involves the data transaction and storage in the organization's database.

The users of the system are required to operate their activities on a database with the help of an

interface. Also, the system is required to take the necessary financial reports by accurately

transforming the stored financial information and data. Therefore, in financial accounting,

technology plays an important role in streamlining, integrating and simplifying all the process of

the business at a reduced cost through helping in the presentation of business activities to its

users inform of financial reports. As a result of increased technological innovation, various

businesses to monitor their financial transactions with the help of computerized systems than

using manual systems that involve "the use of physical ledger." A Because of the increased

technological innovation, "computerized accounting systems" have emerged which assist in

producing faithful and accurate financial reports for the organization and other external users

(Khaled, & Abdulqawi, 2015).

1.2. The significance of the study and motivation

This study's significance is aimed at illustrating the required information concerning the

"Impact of technology on financial reporting." Also, the study aims at explaining the effects and

influence created by technological systems on accounting and financial reporting. As a result of

the continued change in technology across the world, modernization has become a major aspect

of technology. As already indicated previously in the literature review, very many countries

across the world use technology for accounting and financial reporting. This indicates that

INTEGRATED ACCOUNTING PROJECTS6

technology is greatly increased "capitalism for information technology department and lesser

man force required by the companies" (Marshall, & Paul, 2012).

Technology systems provide organizations data concerning financial obligations,

activities, and resources that are required to be used primarily by creditors, investors and

"external decision makers" of the organization. Therefore, this study aims at providing vital

information regarding credit decisions and investment (Muhindo, et al, 2014).

1.3. The purpose/objective of the study

Technology helps various businesses to obtain the required information to organization

managers at various levels in elaborating their duties in an efficient and effective manner in

various accounting and financial area of performance evaluation, decision making, planning, and

resource control and thereby considered a major important financial system of an organization

(Muhindo, et al, 2014).

For this study, the main objective is to make an analysis of the impacts of technology on

financial reporting. Also, the paper aims at measuring the rate at which technology contributes

towards the quality of financial reporting, how an organization improves its outputs of

accounting data system and if the program improves an organization's control of internal

financial reporting (Muhindo, et al, 2014).

1.4. Research Problem and Questions

1.4.1. Problem statement

Currently, technology plays a vital role in the quality of financial and accounting

reporting by creating a relation between technological responses and challenges. The research is

required to point out the organization's future for improving technology in supporting financial

technology is greatly increased "capitalism for information technology department and lesser

man force required by the companies" (Marshall, & Paul, 2012).

Technology systems provide organizations data concerning financial obligations,

activities, and resources that are required to be used primarily by creditors, investors and

"external decision makers" of the organization. Therefore, this study aims at providing vital

information regarding credit decisions and investment (Muhindo, et al, 2014).

1.3. The purpose/objective of the study

Technology helps various businesses to obtain the required information to organization

managers at various levels in elaborating their duties in an efficient and effective manner in

various accounting and financial area of performance evaluation, decision making, planning, and

resource control and thereby considered a major important financial system of an organization

(Muhindo, et al, 2014).

For this study, the main objective is to make an analysis of the impacts of technology on

financial reporting. Also, the paper aims at measuring the rate at which technology contributes

towards the quality of financial reporting, how an organization improves its outputs of

accounting data system and if the program improves an organization's control of internal

financial reporting (Muhindo, et al, 2014).

1.4. Research Problem and Questions

1.4.1. Problem statement

Currently, technology plays a vital role in the quality of financial and accounting

reporting by creating a relation between technological responses and challenges. The research is

required to point out the organization's future for improving technology in supporting financial

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTEGRATED ACCOUNTING PROJECTS7

reporting. For this case, more research is required to acquire detailed knowledge about the

benefits and potentialities that technology brings to the organization's financial reporting and the

impact they create on the accounting function. An organization's technology can best be

improved by managing user commitment and competence. The implementation of technological

systems contributes a big change towards the accounting and financial reporting of the

organization by using computerized systems which are difficult to be adopted by most users.

Most organizations are finding means of designing perfect data accounting or financial systems

which can be in the position to enhance their performance. The study aims at examining the

impacts created by technology on financial reporting considering different strategic options

(Saeidi, 2014).

Today, technology has become a major driving force of organizations’ performance,

structure, operations, and ownership. These forces cover various industries creating up changes

which in turn result in significant social and economic impacts towards the effectiveness of the

organization. The emerging technology in accounting and financial reporting is made up of

various traditional systems which have continuously increased the need for efficient and reduced

operating costs in an organization. An organization's ability to attain competitive advantages of

improved financial reporting is determined by its capacity to adapt to technological systems so as

to attain effective financial markets and operation (Tazik, & Mohamed, 2014).

As a result of the increased growth of technology, the use of manual systems in financial

reporting has become inadequate for facilitating the organization needs. Consequently, private

and public sectors in both developed and developing economies consider using technological

systems to ensure efficient and effective accounting and financial flow, processing, analysis and

recording. The efficient and effective flow of information enhances the decision making of an

reporting. For this case, more research is required to acquire detailed knowledge about the

benefits and potentialities that technology brings to the organization's financial reporting and the

impact they create on the accounting function. An organization's technology can best be

improved by managing user commitment and competence. The implementation of technological

systems contributes a big change towards the accounting and financial reporting of the

organization by using computerized systems which are difficult to be adopted by most users.

Most organizations are finding means of designing perfect data accounting or financial systems

which can be in the position to enhance their performance. The study aims at examining the

impacts created by technology on financial reporting considering different strategic options

(Saeidi, 2014).

Today, technology has become a major driving force of organizations’ performance,

structure, operations, and ownership. These forces cover various industries creating up changes

which in turn result in significant social and economic impacts towards the effectiveness of the

organization. The emerging technology in accounting and financial reporting is made up of

various traditional systems which have continuously increased the need for efficient and reduced

operating costs in an organization. An organization's ability to attain competitive advantages of

improved financial reporting is determined by its capacity to adapt to technological systems so as

to attain effective financial markets and operation (Tazik, & Mohamed, 2014).

As a result of the increased growth of technology, the use of manual systems in financial

reporting has become inadequate for facilitating the organization needs. Consequently, private

and public sectors in both developed and developing economies consider using technological

systems to ensure efficient and effective accounting and financial flow, processing, analysis and

recording. The efficient and effective flow of information enhances the decision making of an

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTEGRATED ACCOUNTING PROJECTS8

organization thereby increasing its ability to achieving business and corporate strategy objectives

(Saeed, 2016).

1.4.2. Research question

What is the major importance of using technology in financial and accounting reporting?

What problems are in line with using technology systems in financial accounting

reporting?

What procedures are followed to choose a given technology system for financial

reporting?

Chapter two

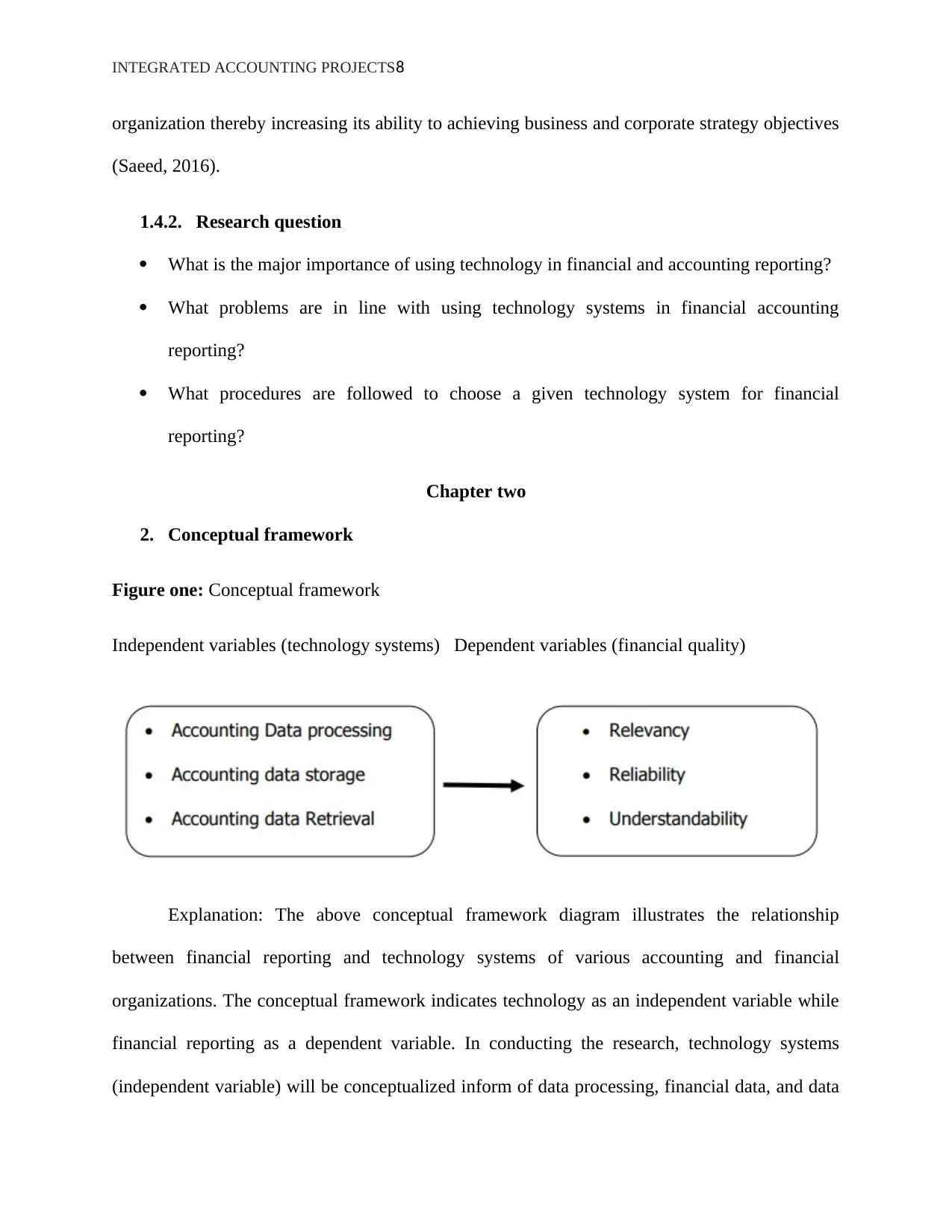

2. Conceptual framework

Figure one: Conceptual framework

Independent variables (technology systems) Dependent variables (financial quality)

Explanation: The above conceptual framework diagram illustrates the relationship

between financial reporting and technology systems of various accounting and financial

organizations. The conceptual framework indicates technology as an independent variable while

financial reporting as a dependent variable. In conducting the research, technology systems

(independent variable) will be conceptualized inform of data processing, financial data, and data

organization thereby increasing its ability to achieving business and corporate strategy objectives

(Saeed, 2016).

1.4.2. Research question

What is the major importance of using technology in financial and accounting reporting?

What problems are in line with using technology systems in financial accounting

reporting?

What procedures are followed to choose a given technology system for financial

reporting?

Chapter two

2. Conceptual framework

Figure one: Conceptual framework

Independent variables (technology systems) Dependent variables (financial quality)

Explanation: The above conceptual framework diagram illustrates the relationship

between financial reporting and technology systems of various accounting and financial

organizations. The conceptual framework indicates technology as an independent variable while

financial reporting as a dependent variable. In conducting the research, technology systems

(independent variable) will be conceptualized inform of data processing, financial data, and data

INTEGRATED ACCOUNTING PROJECTS9

retrieval. On the other hand, financial reports (dependent variable) will be determined by their

understandability, relevancy, and reliability. To effectively perform this study, researchers will

be in the position to carry out a survey concerning medium and small enterprises in Australia.

The researcher will be able to make sure that all financial organizations which haven't

implemented technology systems for accounting and financial reporting incorporate them

(Shiraj, 2015).

2.2. Hypotheses

Accounting Data or information processing lacks major significant impact on the quality

of accounting and financial reports of an organization or commercial bank

Accounting information or data storage lacks significant impacts on the organization's

quality of accounting and financial reports

The Retrieval of accounting data has no major effects on the quality of an organization's

financial report.

Chapter three

Research methodology

3. Introduction

This chapter illustrates the research methodology of the study that will be followed to

help in carrying out the research. This section is comprised of various subheading, that is to say,

research design, sampling and sample design, data collection methods, data reliability and

validity, data collection tools, sampling design, and data analysis

3.2. Research design

retrieval. On the other hand, financial reports (dependent variable) will be determined by their

understandability, relevancy, and reliability. To effectively perform this study, researchers will

be in the position to carry out a survey concerning medium and small enterprises in Australia.

The researcher will be able to make sure that all financial organizations which haven't

implemented technology systems for accounting and financial reporting incorporate them

(Shiraj, 2015).

2.2. Hypotheses

Accounting Data or information processing lacks major significant impact on the quality

of accounting and financial reports of an organization or commercial bank

Accounting information or data storage lacks significant impacts on the organization's

quality of accounting and financial reports

The Retrieval of accounting data has no major effects on the quality of an organization's

financial report.

Chapter three

Research methodology

3. Introduction

This chapter illustrates the research methodology of the study that will be followed to

help in carrying out the research. This section is comprised of various subheading, that is to say,

research design, sampling and sample design, data collection methods, data reliability and

validity, data collection tools, sampling design, and data analysis

3.2. Research design

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTEGRATED ACCOUNTING PROJECTS10

The research will be carried out with the help of a "descriptive research approach" so as

to evaluate the impact created by technology on the "quality of financial reports" of a selected

bank in Australia. The Description research design will be defined as "a scientific method in

which information is collected without changing the environment itincludes surveys and fact-

finding inquiries of different kinds, which seeks to obtain information that discloses existing

phenomenon." This research design will be adopted because it will help in describing the nature

of issues as they appear in the current perspective. The study will also involve a quantitative

approach. This will involve "the collection of numerical data in order to explain, predict and

control phenomena of interest, data analysis being more statistical" It will also involve the

collection of data so as to answer different cautions in regards to the present status of the matter

under investigation and test the hypotheses (SLMOF, 2013).

3.3. Target population

For this study, the target population will be enterprises mostly banks using technology to

make financial reporting. The study will comprise of 10 enterprises. In this case, various

departments in the enterprise will take part in the study, for example, the accounting department,

operational department, and Information Communication Technology department (ICT). At least

a total of 20 members in each department will take part in the study (Turner, & Weickgenannt,

2013).

3.4. Sample design

Selection and sampling are important procedures and principles that are used to choose,

gain and identify necessary sources of data. In simple terms, a sample refers to "a smaller (but

hopefully representative) collection of units from a population used to determine truths about

The research will be carried out with the help of a "descriptive research approach" so as

to evaluate the impact created by technology on the "quality of financial reports" of a selected

bank in Australia. The Description research design will be defined as "a scientific method in

which information is collected without changing the environment itincludes surveys and fact-

finding inquiries of different kinds, which seeks to obtain information that discloses existing

phenomenon." This research design will be adopted because it will help in describing the nature

of issues as they appear in the current perspective. The study will also involve a quantitative

approach. This will involve "the collection of numerical data in order to explain, predict and

control phenomena of interest, data analysis being more statistical" It will also involve the

collection of data so as to answer different cautions in regards to the present status of the matter

under investigation and test the hypotheses (SLMOF, 2013).

3.3. Target population

For this study, the target population will be enterprises mostly banks using technology to

make financial reporting. The study will comprise of 10 enterprises. In this case, various

departments in the enterprise will take part in the study, for example, the accounting department,

operational department, and Information Communication Technology department (ICT). At least

a total of 20 members in each department will take part in the study (Turner, & Weickgenannt,

2013).

3.4. Sample design

Selection and sampling are important procedures and principles that are used to choose,

gain and identify necessary sources of data. In simple terms, a sample refers to "a smaller (but

hopefully representative) collection of units from a population used to determine truths about

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTEGRATED ACCOUNTING PROJECTS11

that population." There are major two types of sampling designs mostly used in by researchers,

that is to say, Non -probability sampling and representative or probability sampling. For

Probability sampling, it is always common with "survey research strategies as each case being

selected from the population is known and is usually equal for all cases." while judgemental or

non-probability sampling is "the probability of each case being selected from the total population

is not known." The sampling design method to be used in the study is non-probability. According

to VanBaren (2017), non-probability sampling "provides a range of alternative techniques to

select samples based on your subjective judgment. In the exploratory stages of some research

projects, a non-probability sample may be the most practical." For this study, the relevant

samples will be selected within an enterprise. Interviews will be carried out on the members in

the organization depending on their departments such as the ICT department, financial

department, and many others. Therefore, the selection will be done on individuals with

significant experience in financial reporting and technology so as to obtain the correct data

required for the study (El- Dalabeeh, 2012).

The study will also involve a purposive sampling design. In this case, purposive is

"based on judgment on possession of specialized accounting experiences and knowledge on

information technology." This sampling design will be chosen because it is helpful in the

selection of people within a given sample with specialized experiences or information regarding

the problem under investigation or study by virtual of their position or specific position in the

organization. For example the head of the ICT department. The method is more considerable

because it provides accurate results for maximum and heterogeneous variation sampling

(Alshebeil, 2010).

3.5. Data sources

that population." There are major two types of sampling designs mostly used in by researchers,

that is to say, Non -probability sampling and representative or probability sampling. For

Probability sampling, it is always common with "survey research strategies as each case being

selected from the population is known and is usually equal for all cases." while judgemental or

non-probability sampling is "the probability of each case being selected from the total population

is not known." The sampling design method to be used in the study is non-probability. According

to VanBaren (2017), non-probability sampling "provides a range of alternative techniques to

select samples based on your subjective judgment. In the exploratory stages of some research

projects, a non-probability sample may be the most practical." For this study, the relevant

samples will be selected within an enterprise. Interviews will be carried out on the members in

the organization depending on their departments such as the ICT department, financial

department, and many others. Therefore, the selection will be done on individuals with

significant experience in financial reporting and technology so as to obtain the correct data

required for the study (El- Dalabeeh, 2012).

The study will also involve a purposive sampling design. In this case, purposive is

"based on judgment on possession of specialized accounting experiences and knowledge on

information technology." This sampling design will be chosen because it is helpful in the

selection of people within a given sample with specialized experiences or information regarding

the problem under investigation or study by virtual of their position or specific position in the

organization. For example the head of the ICT department. The method is more considerable

because it provides accurate results for maximum and heterogeneous variation sampling

(Alshebeil, 2010).

3.5. Data sources

INTEGRATED ACCOUNTING PROJECTS12

Data from the study will be obtained from the primary and secondary sources. In this

case, the study will be performed with the help of raw data from different enterprises. The data

will be collected with the help of questionnaires as the research tools. These will help in the

appropriate collection of data to evaluate the current situation under investigation.The researcher

will also collect data using secondary sources. In this case, the researcher will be required to use

the current data sources that are available publically known as "secondary sources of data." This

kind of data is originally obtained with the intention of fulfilling other roles. Secondary data is

made up of the industry and company-specific websites and also other relevant and previous

research journal articles and papers (Nejad, & Soudani, 2012).

3.6. Data collection methods

In research, data collection is a critical element. For this case, the study will use "a self-

administered questionnaire" which will be required to collect primary data. The researcher will

be required to design a self-administered questionnaire and distribute them to various enterprise

members included in the study. The questionnaires will be categorized into major three sections,

that is to say, Section A which will be dealing with the respondents' Bio-data, section B will also

be concerned with an organization's independent variables, and technology systems and Section

C will be made up of the "dependent variables" of the study. In addition, questionnaires will be

printed in simple and clear language possible so that the respondents can be in the position to

understand them. The respondents will be required to make their rightful choices by ticking the

most right answers (Onaolapo, 2014).

3.7. Data reliability and Validity

Data from the study will be obtained from the primary and secondary sources. In this

case, the study will be performed with the help of raw data from different enterprises. The data

will be collected with the help of questionnaires as the research tools. These will help in the

appropriate collection of data to evaluate the current situation under investigation.The researcher

will also collect data using secondary sources. In this case, the researcher will be required to use

the current data sources that are available publically known as "secondary sources of data." This

kind of data is originally obtained with the intention of fulfilling other roles. Secondary data is

made up of the industry and company-specific websites and also other relevant and previous

research journal articles and papers (Nejad, & Soudani, 2012).

3.6. Data collection methods

In research, data collection is a critical element. For this case, the study will use "a self-

administered questionnaire" which will be required to collect primary data. The researcher will

be required to design a self-administered questionnaire and distribute them to various enterprise

members included in the study. The questionnaires will be categorized into major three sections,

that is to say, Section A which will be dealing with the respondents' Bio-data, section B will also

be concerned with an organization's independent variables, and technology systems and Section

C will be made up of the "dependent variables" of the study. In addition, questionnaires will be

printed in simple and clear language possible so that the respondents can be in the position to

understand them. The respondents will be required to make their rightful choices by ticking the

most right answers (Onaolapo, 2014).

3.7. Data reliability and Validity

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.