Impairment Accounting Solutions

VerifiedAdded on 2019/11/12

|6

|1275

|225

Homework Assignment

AI Summary

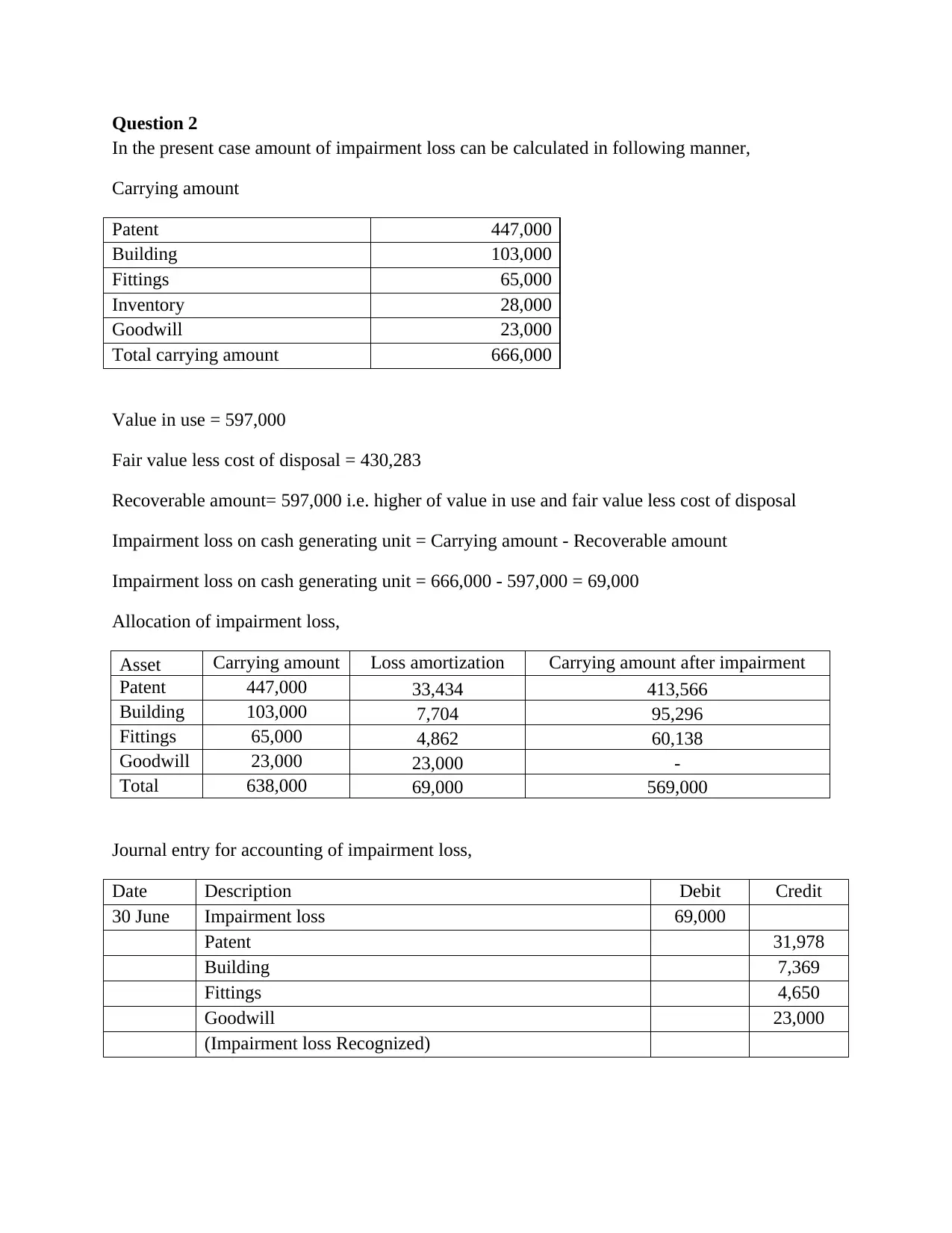

This document presents solutions to two questions related to impairment accounting. The first question explores the concept of impairment reversal on goodwill, explaining that under Australian Accounting Standards (AASB 136) and other international standards (IFRS 3), reversal of impairment loss on goodwill is not permitted. The solution details the reasons behind this prohibition, emphasizing the prevention of internally generated goodwill being recorded. The second question involves a practical calculation of impairment loss on a cash-generating unit. It demonstrates the calculation of impairment loss, its allocation across different assets (patent, building, fittings, goodwill), and the corresponding journal entry. The solution uses specific figures to illustrate the process, showing how to determine the recoverable amount (higher of value in use and fair value less costs of disposal) and allocate the impairment loss proportionally based on carrying amounts. The document includes a bibliography citing relevant accounting standards and academic articles.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.