Corporate Accounting & Reporting Assignment - Finance Module Report

VerifiedAdded on 2020/04/01

|9

|1655

|32

Report

AI Summary

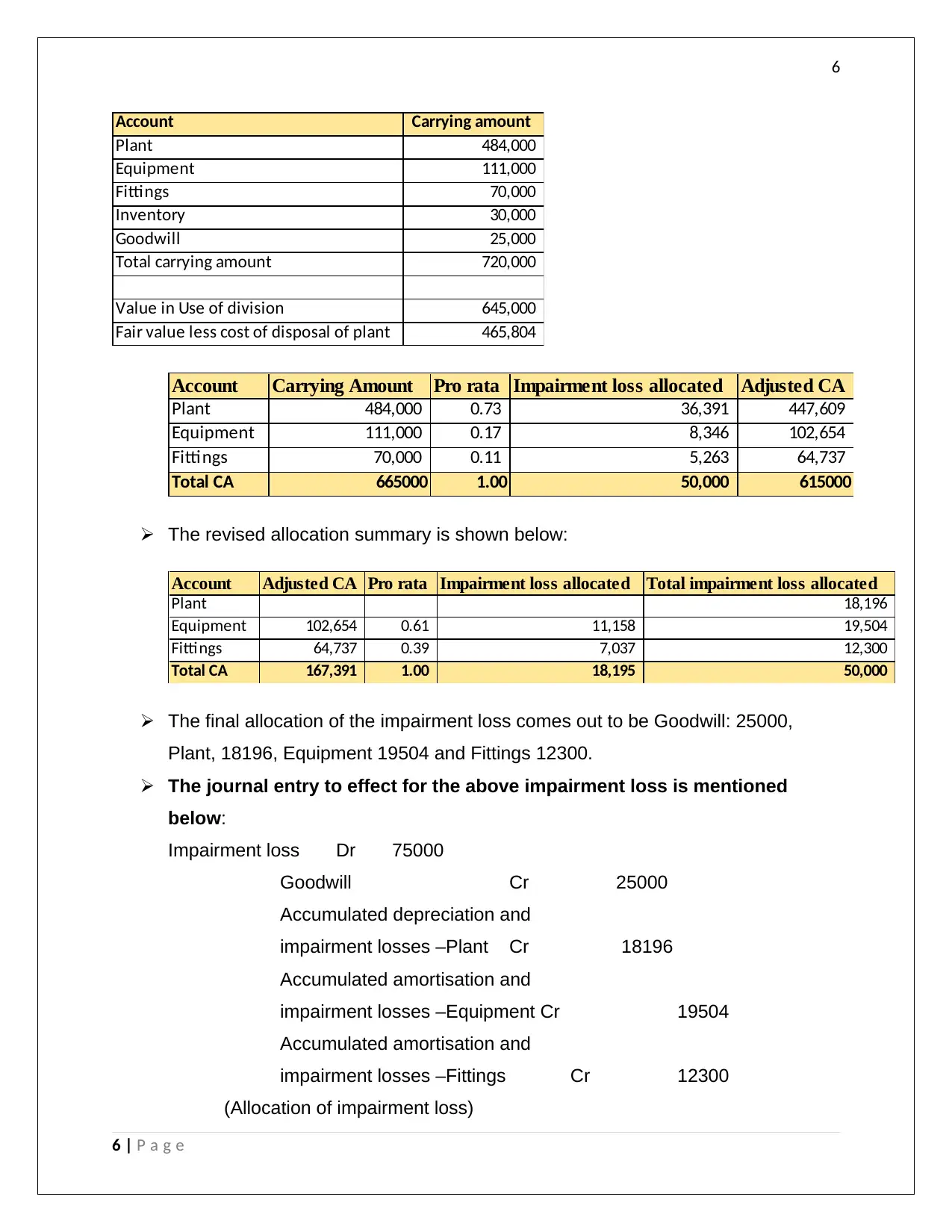

This report delves into the intricacies of corporate accounting, specifically focusing on the recognition and measurement of goodwill impairment losses. It begins with an introduction to goodwill as an intangible asset acquired through business acquisitions and clarifies that in-house goodwill is not recognized. The report outlines the concept of impairment loss, defined as the difference between the carrying amount of an asset and its recoverable amount, and emphasizes the prohibition of goodwill amortization under IFRS 3. It explains the annual impairment testing of goodwill, the allocation of goodwill to cash-generating units, and the determination of recoverable amounts. The report also contrasts the current standards with previous practices regarding the reversal of impairment losses. The report then presents a practical example of impairment assessment for Gali Limited, providing the carrying amounts, allocation summary, and the journal entry to effect the impairment loss. The conclusion highlights the complexity of goodwill impairment accounting and the need for adherence to relevant standards. References from various academic journals and publications are included.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.