Essay on Impairment Loss for Cash Generating Units (Finance)

VerifiedAdded on 2019/11/19

|5

|1383

|230

Essay

AI Summary

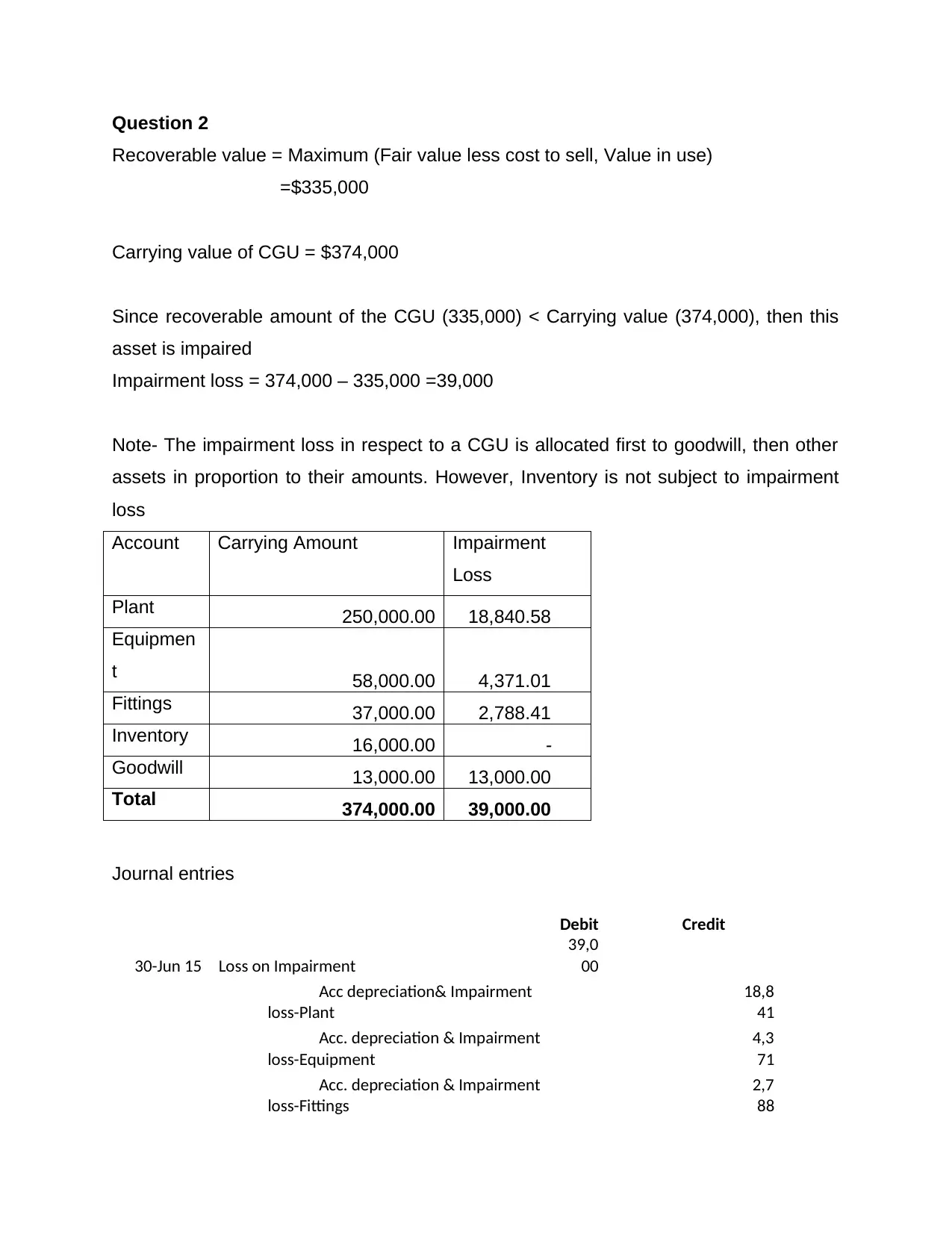

This essay provides a comprehensive overview of impairment losses for cash generating units (CGUs), excluding goodwill, within the framework of Australian Accounting Standards Board 136 (AASB 136). It defines impairment losses and CGUs, emphasizing the importance of these concepts for accurate financial reporting. The essay details the measurement process, including the calculation of recoverable amounts (fair value less costs to sell and value in use) and carrying values. It explains how impairment losses are recognized and allocated, with a specific focus on the order of allocation (first to goodwill, then to other assets). Furthermore, the essay discusses the reversal of impairment losses and the conditions under which this can occur. The essay concludes by highlighting the significance of regularly assessing CGUs for impairment indicators to avoid overvaluation of assets and ensure financial statements reflect a company's true value. It includes a practical example of impairment loss calculation and the related journal entries.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.