Financial Accounting Project: Impairment Loss Analysis & CGUs

VerifiedAdded on 2020/11/23

|7

|1638

|258

Project

AI Summary

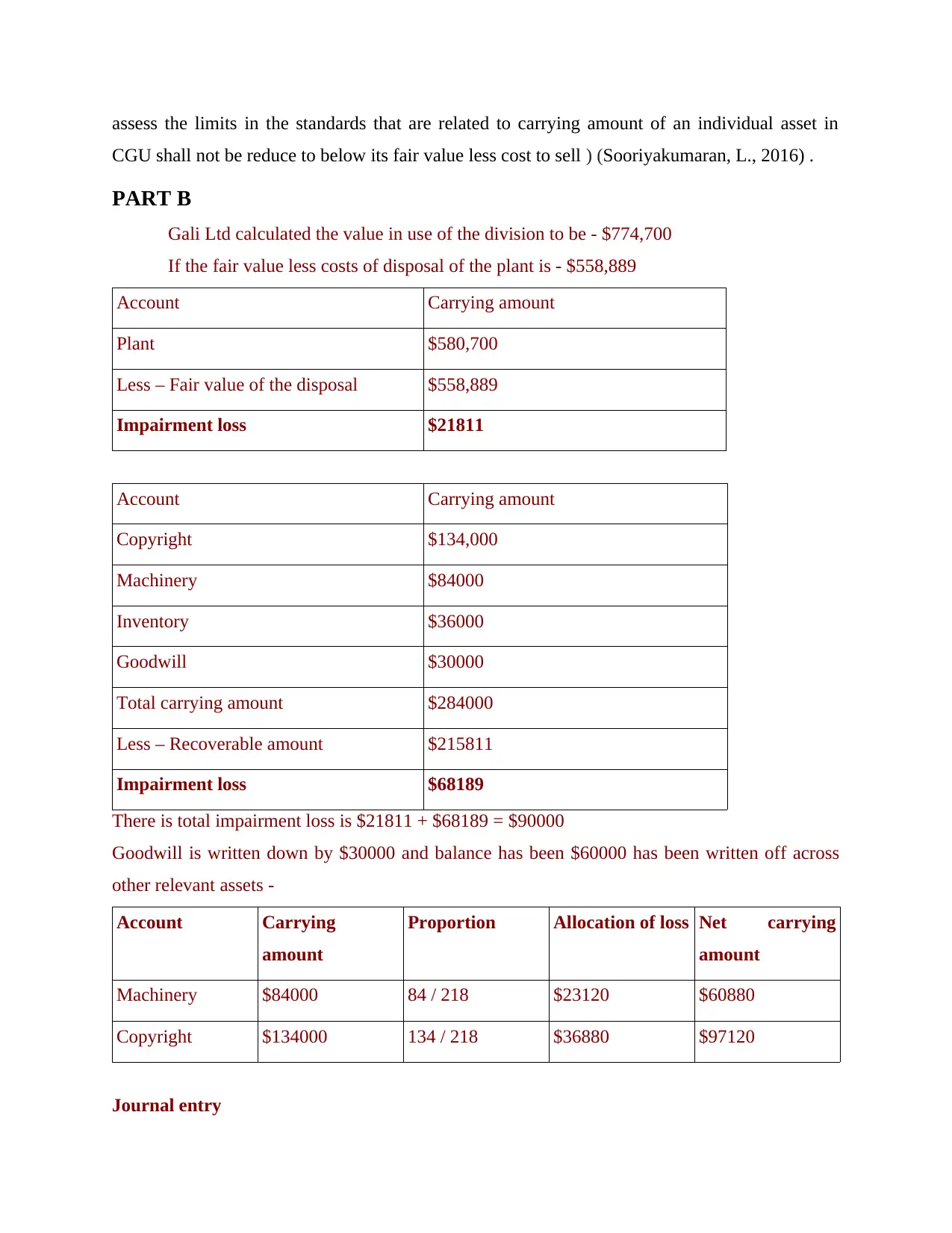

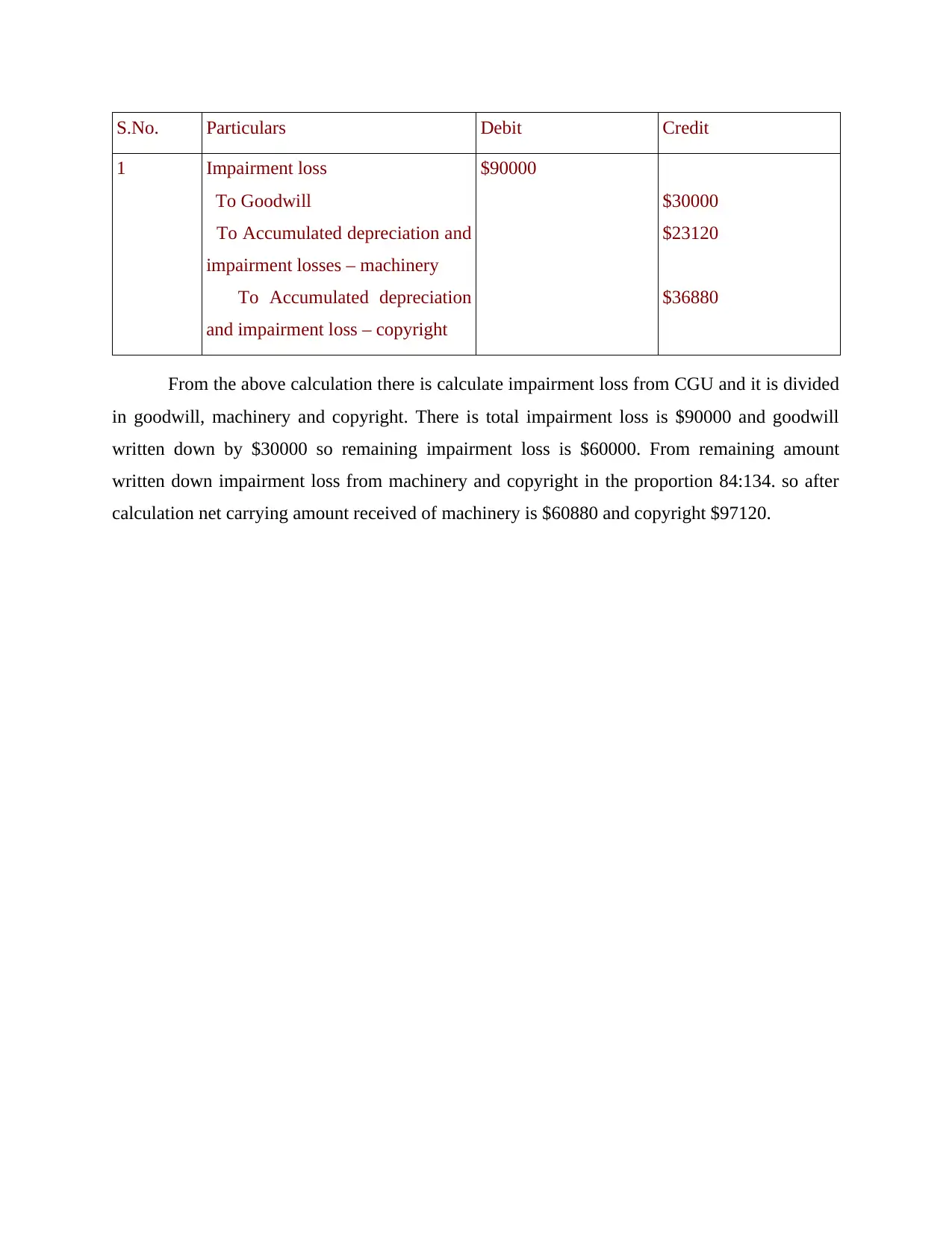

This project focuses on impairment loss for cash-generating units (CGUs) excluding goodwill. It defines impairment loss as the reduction in an asset's value when its recoverable amount is less than its carrying value, explaining the calculation using net carrying value and fair market value. The project outlines the process of identifying impairment factors, estimating fair market value, and comparing it to the carrying value. It emphasizes the importance of testing assets for impairment, especially within CGUs, which are the smallest identifiable groups of assets generating independent cash inflows. The project details the calculation of impairment loss, including the allocation of loss within a CGU, and the assessment of assets based on IAS 36. It also includes a case study with calculations, focusing on determining impairment loss, the allocation of loss to different assets (goodwill, machinery, copyright), and the corresponding journal entries. The project concludes with a list of relevant references.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.