Analysis of Impairment Loss, Goodwill Reversal in Financial Accounting

VerifiedAdded on 2023/04/24

|9

|1395

|381

Homework Assignment

AI Summary

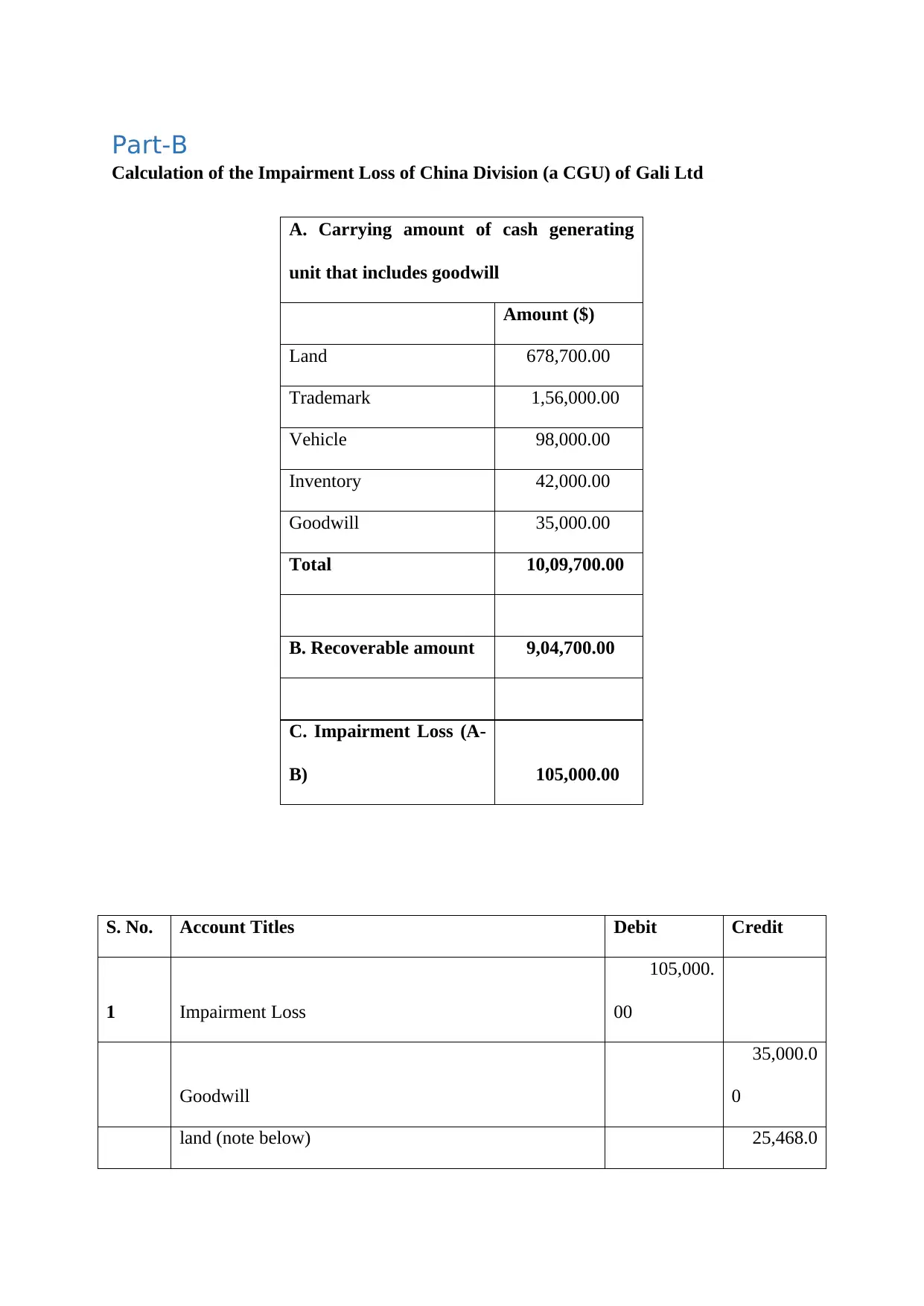

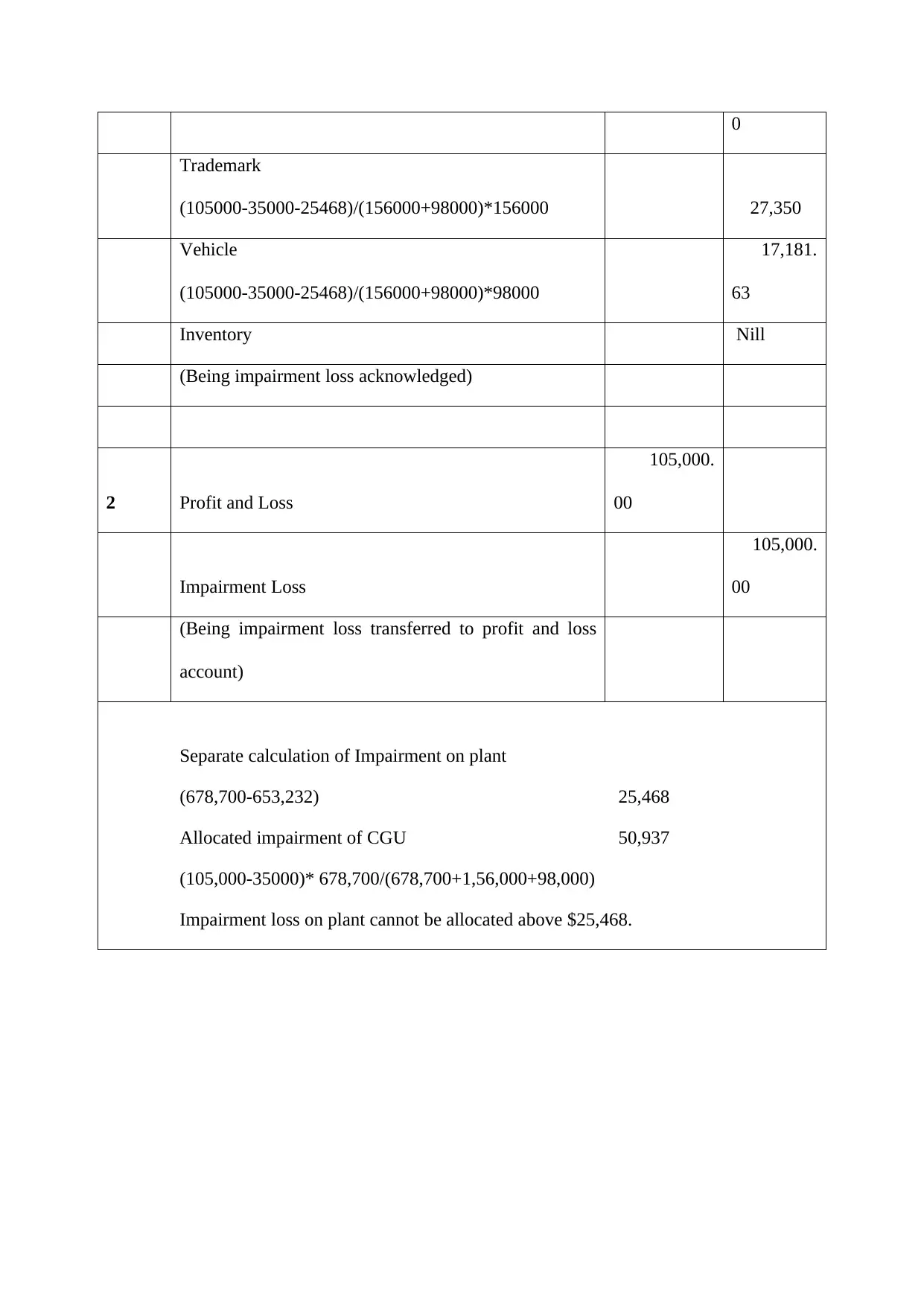

This assignment solution addresses the topic of impairment loss and goodwill reversal in financial accounting. Part A provides a theoretical essay discussing the principles of impairment loss, the role of cash-generating units (CGUs), and the specific treatment of goodwill according to accounting standards like AASB 136. It covers the calculation of impairment loss, allocation to assets, and the reversal of impairment. Part B presents a practical application, including the calculation of impairment loss for a CGU (China Division of Gali Ltd), determination of recoverable amount, and related journal entries. The solution demonstrates the allocation of impairment loss to goodwill and other assets, reflecting the decrease in carrying amounts. The assignment emphasizes the importance of accurate financial reporting and the proper application of accounting standards.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.