University Assignment: Impairment Testing of JB Hi-Fi Limited

VerifiedAdded on 2022/12/16

|10

|2472

|67

Report

AI Summary

This report provides an in-depth analysis of the application of professional judgment in impairment testing, focusing on the case of JB Hi-Fi Limited. It begins with an overview of the importance of professional judgment in accounting, including its role in ensuring the quality of financial information and ethical practices. The report then examines the impaired assets of JB Hi-Fi, the estimations used for impairment write-downs, and the relevant disclosures in the 2018 annual report. It assesses the suitability of the professional judgments made by the organization, considering aspects like cash flow assumptions and compliance with ASIC regulations. The analysis concludes by evaluating the alignment of these judgments with the objectives of general purpose financial reporting, highlighting areas where improvements could be made to enhance the quality and transparency of financial reporting. The report emphasizes the critical role of professional judgment in financial reporting and offers recommendations for better adherence to accounting standards and regulations.

Running head: APPLICATION OF PROFESSIONAL JUDGEMENT ON IMPAIRMENT

TESTING

Application of Professional Judgment on Impairment Testing

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

ACCG224 S1 2019 SID

TESTING

Application of Professional Judgment on Impairment Testing

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

ACCG224 S1 2019 SID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

APPLICATION OF PROFESSIONAL JUDGEMENT ON IMPAIRMENT TESTING

Executive Summary:

The initial section of the report has emphasised on the value of professional judgement in the

accounting profession. The second part analyses the impairment testing of JB Hi-Fi Limited

based on its disclosures made in the 2018 annual report. The next section has laid stress on

the suitability of the used professional judgements of the organisation. Finally, the report has

shed light on investigating whether the applied professional judgements of the organisation

are in line with the objectives of general purpose financial reporting.

ACCG224 S1 2019 SID Page 1

Executive Summary:

The initial section of the report has emphasised on the value of professional judgement in the

accounting profession. The second part analyses the impairment testing of JB Hi-Fi Limited

based on its disclosures made in the 2018 annual report. The next section has laid stress on

the suitability of the used professional judgements of the organisation. Finally, the report has

shed light on investigating whether the applied professional judgements of the organisation

are in line with the objectives of general purpose financial reporting.

ACCG224 S1 2019 SID Page 1

APPLICATION OF PROFESSIONAL JUDGEMENT ON IMPAIRMENT TESTING

Table of Contents

Introduction:...............................................................................................................................3

Requirement a:...........................................................................................................................3

Role played by professional judgement in accounting:.........................................................3

Two implications on the accounting information users in case of inappropriate professional

judgement:..............................................................................................................................3

Requirement b:...........................................................................................................................4

Impaired assets of JB Hi-Fi Limited:.....................................................................................4

Estimations needed for writing impairment:..........................................................................4

Amount of write-down of impairment:..................................................................................4

Relevant disclosures in the latest financial report with respect to impairment testing:.........5

Requirement c:...........................................................................................................................5

Requirement d:...........................................................................................................................6

Conclusion and recommendation:..............................................................................................6

References:.................................................................................................................................8

ACCG224 S1 2019 SID Page 2

Table of Contents

Introduction:...............................................................................................................................3

Requirement a:...........................................................................................................................3

Role played by professional judgement in accounting:.........................................................3

Two implications on the accounting information users in case of inappropriate professional

judgement:..............................................................................................................................3

Requirement b:...........................................................................................................................4

Impaired assets of JB Hi-Fi Limited:.....................................................................................4

Estimations needed for writing impairment:..........................................................................4

Amount of write-down of impairment:..................................................................................4

Relevant disclosures in the latest financial report with respect to impairment testing:.........5

Requirement c:...........................................................................................................................5

Requirement d:...........................................................................................................................6

Conclusion and recommendation:..............................................................................................6

References:.................................................................................................................................8

ACCG224 S1 2019 SID Page 2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

APPLICATION OF PROFESSIONAL JUDGEMENT ON IMPAIRMENT TESTING

Introduction:

The financial reports provide useful information to the users regarding the financial

health of a particular organisation in order to assist them in making investment decisions

(Rennekamp, Rupar and Seybert 2014). The higher-level management of the organisation

uses a number of accounting models, projections and professional judgement before the

financial reports are presented to the users. The current report is focused on evaluating the

various aspects related to impairment testing of JB Hi-Fi Limited, which is the biggest home

entertainment retailer in Australia (Jbhifi.com.au 2019).

Requirement a:

Role played by professional judgement in accounting:

Professional judgement includes accounting expertise and knowledge as two

significant elements and they have immense value in the accounting field as well. The

accurate application of accounting expertise and knowledge coupled with practical training

assists in ascertaining the quality of reported financial information (Banker, Basu and

Byzalov 2016). Therefore, professional judgement plays a pivotal role in undertaking

accurate decisions. One of the significant concerns confronting the accounting profession in

the current era is ethics, since the professional does not have the same credibility owing to

various accounting scandals that have taken place globally in the past. With the help of sound

professional judgement, ethics could be maintained within the profession necessary to ensure

professional success. Thus, the role of professional judgement is crucial in terms of

disclosure of quality financial information to the financial statement users (Carvalho,

Rodrigues and Ferreira 2016).

Two implications on the accounting information users in case of inappropriate

professional judgement:

When professional judgement is not appropriate, there are two possible implications

on the users of accounting information, which are discussed as follows:

Firstly, it is not possible to gain an understanding of the actual financial health of an

organisation due to lack of relevant or proper professional judgement. In this manner,

the financial statement users would be misguided regarding the financial standing of

the organisation in its operating markets (Coste, Tudor and Pali-Pista 2014).

ACCG224 S1 2019 SID Page 3

Introduction:

The financial reports provide useful information to the users regarding the financial

health of a particular organisation in order to assist them in making investment decisions

(Rennekamp, Rupar and Seybert 2014). The higher-level management of the organisation

uses a number of accounting models, projections and professional judgement before the

financial reports are presented to the users. The current report is focused on evaluating the

various aspects related to impairment testing of JB Hi-Fi Limited, which is the biggest home

entertainment retailer in Australia (Jbhifi.com.au 2019).

Requirement a:

Role played by professional judgement in accounting:

Professional judgement includes accounting expertise and knowledge as two

significant elements and they have immense value in the accounting field as well. The

accurate application of accounting expertise and knowledge coupled with practical training

assists in ascertaining the quality of reported financial information (Banker, Basu and

Byzalov 2016). Therefore, professional judgement plays a pivotal role in undertaking

accurate decisions. One of the significant concerns confronting the accounting profession in

the current era is ethics, since the professional does not have the same credibility owing to

various accounting scandals that have taken place globally in the past. With the help of sound

professional judgement, ethics could be maintained within the profession necessary to ensure

professional success. Thus, the role of professional judgement is crucial in terms of

disclosure of quality financial information to the financial statement users (Carvalho,

Rodrigues and Ferreira 2016).

Two implications on the accounting information users in case of inappropriate

professional judgement:

When professional judgement is not appropriate, there are two possible implications

on the users of accounting information, which are discussed as follows:

Firstly, it is not possible to gain an understanding of the actual financial health of an

organisation due to lack of relevant or proper professional judgement. In this manner,

the financial statement users would be misguided regarding the financial standing of

the organisation in its operating markets (Coste, Tudor and Pali-Pista 2014).

ACCG224 S1 2019 SID Page 3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

APPLICATION OF PROFESSIONAL JUDGEMENT ON IMPAIRMENT TESTING

Secondly, due to the use of inappropriate professional judgement resulting in

inaccurate financial information, it is likely that the users would undertake wrong

investment decisions that would minimise their overall return on investment (Paugam

and Ramond 2015).

Requirement b:

Impaired assets of JB Hi-Fi Limited:

From the annual report of JB Hi-Fi Limited in 2018, it has been identified that the

assets impaired include leasehold improvements, intangible assets having indefinite economic

lives and plant and equipment. Impairment has been recorded by the organisation for its plant

and equipment in 2018; however, there has been no impairment recognition for intangible

assets (Member.afraccess.com 2019).

Estimations needed for writing impairment:

Based on the latest annual report of JB Hi-Fi Limited, it is necessary to use a number

of significant estimations for impairment write-downs. These estimations include cost of

conducting business, growth in revenue, gross margin and discount rate. These estimations

are generally made from previous experience along with projected financial and operating

performance of the organisation for each cash-generating unit (CGU) (André, Dionysiou and

Tsalavoutas 2018). The discount rate is obtained from cost of capital, after which adjustment

is made for different risk profiles (Member.afraccess.com 2019).

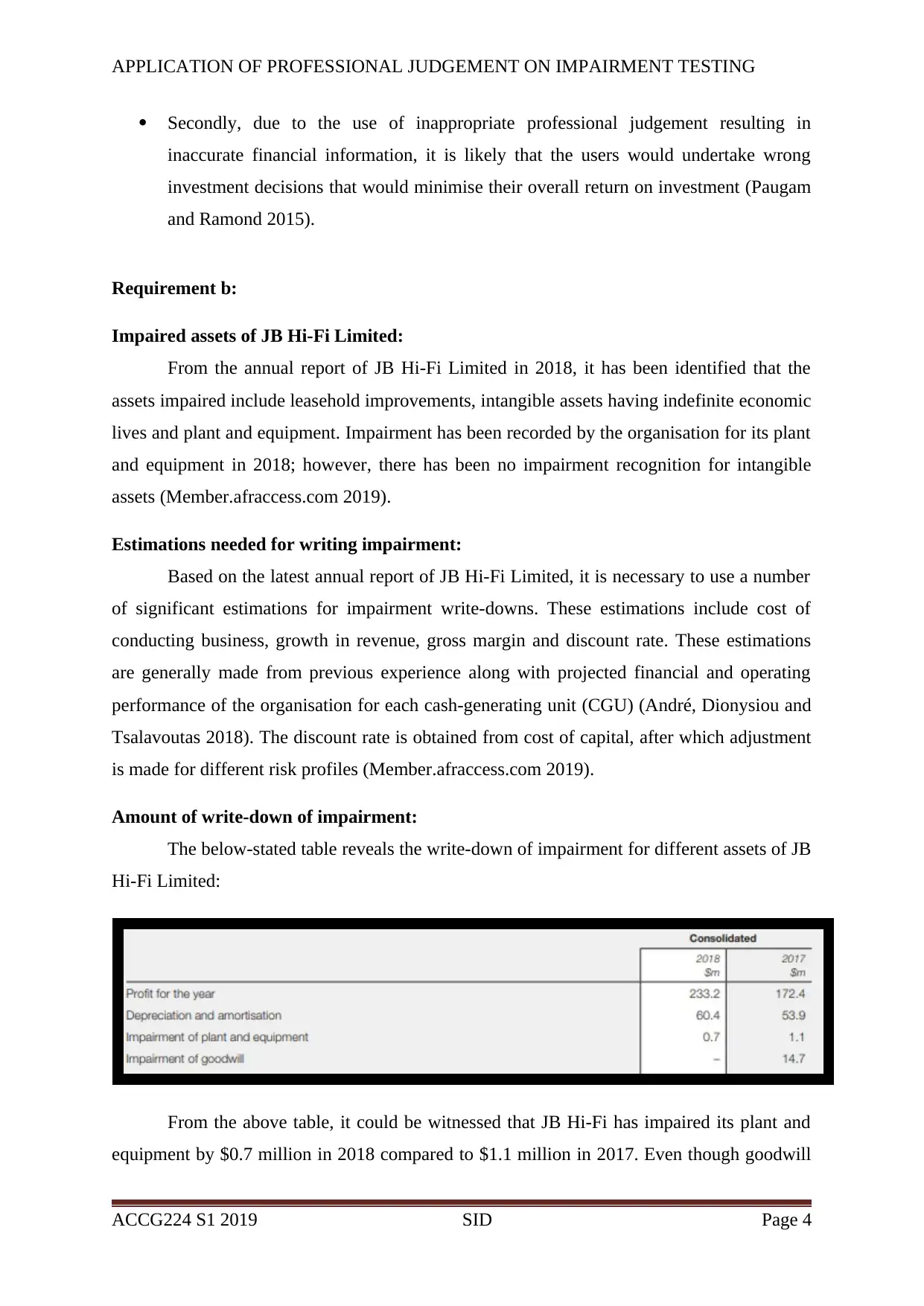

Amount of write-down of impairment:

The below-stated table reveals the write-down of impairment for different assets of JB

Hi-Fi Limited:

From the above table, it could be witnessed that JB Hi-Fi has impaired its plant and

equipment by $0.7 million in 2018 compared to $1.1 million in 2017. Even though goodwill

ACCG224 S1 2019 SID Page 4

Secondly, due to the use of inappropriate professional judgement resulting in

inaccurate financial information, it is likely that the users would undertake wrong

investment decisions that would minimise their overall return on investment (Paugam

and Ramond 2015).

Requirement b:

Impaired assets of JB Hi-Fi Limited:

From the annual report of JB Hi-Fi Limited in 2018, it has been identified that the

assets impaired include leasehold improvements, intangible assets having indefinite economic

lives and plant and equipment. Impairment has been recorded by the organisation for its plant

and equipment in 2018; however, there has been no impairment recognition for intangible

assets (Member.afraccess.com 2019).

Estimations needed for writing impairment:

Based on the latest annual report of JB Hi-Fi Limited, it is necessary to use a number

of significant estimations for impairment write-downs. These estimations include cost of

conducting business, growth in revenue, gross margin and discount rate. These estimations

are generally made from previous experience along with projected financial and operating

performance of the organisation for each cash-generating unit (CGU) (André, Dionysiou and

Tsalavoutas 2018). The discount rate is obtained from cost of capital, after which adjustment

is made for different risk profiles (Member.afraccess.com 2019).

Amount of write-down of impairment:

The below-stated table reveals the write-down of impairment for different assets of JB

Hi-Fi Limited:

From the above table, it could be witnessed that JB Hi-Fi has impaired its plant and

equipment by $0.7 million in 2018 compared to $1.1 million in 2017. Even though goodwill

ACCG224 S1 2019 SID Page 4

APPLICATION OF PROFESSIONAL JUDGEMENT ON IMPAIRMENT TESTING

has been impaired by $14.7 million in 2017, there has been no impairment of the same in

2018.

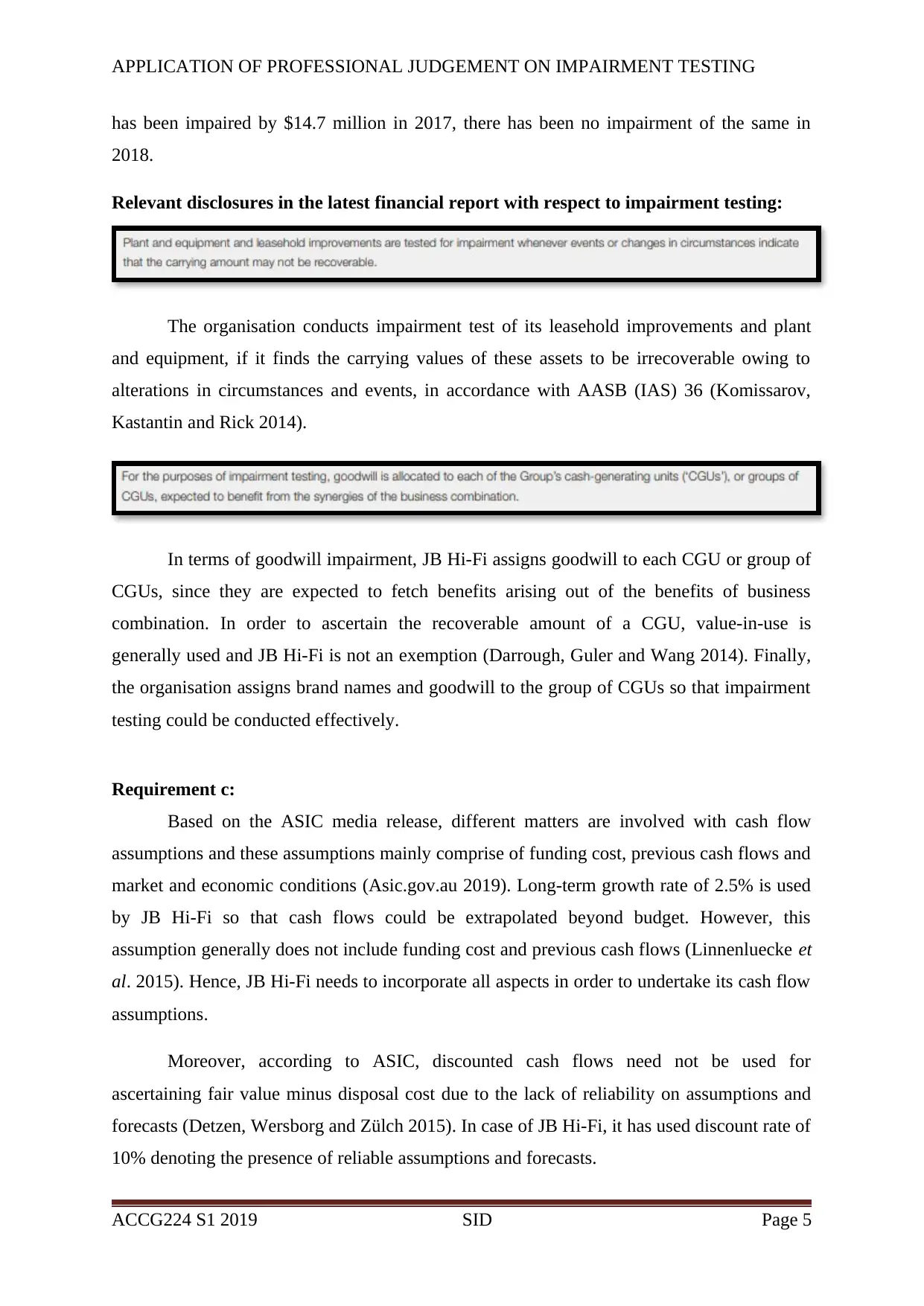

Relevant disclosures in the latest financial report with respect to impairment testing:

The organisation conducts impairment test of its leasehold improvements and plant

and equipment, if it finds the carrying values of these assets to be irrecoverable owing to

alterations in circumstances and events, in accordance with AASB (IAS) 36 (Komissarov,

Kastantin and Rick 2014).

In terms of goodwill impairment, JB Hi-Fi assigns goodwill to each CGU or group of

CGUs, since they are expected to fetch benefits arising out of the benefits of business

combination. In order to ascertain the recoverable amount of a CGU, value-in-use is

generally used and JB Hi-Fi is not an exemption (Darrough, Guler and Wang 2014). Finally,

the organisation assigns brand names and goodwill to the group of CGUs so that impairment

testing could be conducted effectively.

Requirement c:

Based on the ASIC media release, different matters are involved with cash flow

assumptions and these assumptions mainly comprise of funding cost, previous cash flows and

market and economic conditions (Asic.gov.au 2019). Long-term growth rate of 2.5% is used

by JB Hi-Fi so that cash flows could be extrapolated beyond budget. However, this

assumption generally does not include funding cost and previous cash flows (Linnenluecke et

al. 2015). Hence, JB Hi-Fi needs to incorporate all aspects in order to undertake its cash flow

assumptions.

Moreover, according to ASIC, discounted cash flows need not be used for

ascertaining fair value minus disposal cost due to the lack of reliability on assumptions and

forecasts (Detzen, Wersborg and Zülch 2015). In case of JB Hi-Fi, it has used discount rate of

10% denoting the presence of reliable assumptions and forecasts.

ACCG224 S1 2019 SID Page 5

has been impaired by $14.7 million in 2017, there has been no impairment of the same in

2018.

Relevant disclosures in the latest financial report with respect to impairment testing:

The organisation conducts impairment test of its leasehold improvements and plant

and equipment, if it finds the carrying values of these assets to be irrecoverable owing to

alterations in circumstances and events, in accordance with AASB (IAS) 36 (Komissarov,

Kastantin and Rick 2014).

In terms of goodwill impairment, JB Hi-Fi assigns goodwill to each CGU or group of

CGUs, since they are expected to fetch benefits arising out of the benefits of business

combination. In order to ascertain the recoverable amount of a CGU, value-in-use is

generally used and JB Hi-Fi is not an exemption (Darrough, Guler and Wang 2014). Finally,

the organisation assigns brand names and goodwill to the group of CGUs so that impairment

testing could be conducted effectively.

Requirement c:

Based on the ASIC media release, different matters are involved with cash flow

assumptions and these assumptions mainly comprise of funding cost, previous cash flows and

market and economic conditions (Asic.gov.au 2019). Long-term growth rate of 2.5% is used

by JB Hi-Fi so that cash flows could be extrapolated beyond budget. However, this

assumption generally does not include funding cost and previous cash flows (Linnenluecke et

al. 2015). Hence, JB Hi-Fi needs to incorporate all aspects in order to undertake its cash flow

assumptions.

Moreover, according to ASIC, discounted cash flows need not be used for

ascertaining fair value minus disposal cost due to the lack of reliability on assumptions and

forecasts (Detzen, Wersborg and Zülch 2015). In case of JB Hi-Fi, it has used discount rate of

10% denoting the presence of reliable assumptions and forecasts.

ACCG224 S1 2019 SID Page 5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

APPLICATION OF PROFESSIONAL JUDGEMENT ON IMPAIRMENT TESTING

The organisations are obliged by ASIC of not using increasing cash flows after five

years without taking into account the offsetting effect on discount rate (Kabir and Rahman

2016). Due to this, JB H-Fi has used extrapolation method in order to take into account the

impact of cash flows above five years. Moreover, ASIC restricts the organisations in

identifying CGUs at excessively high levels, in which cash flows of an individual asset are

dependent (Sinclair and Keller 2014). By taking into consideration this aspect, JB Hi-Fi has

grouped its CGUs at lower level where there are distinct identifiable and considerably

independent cash flows.

Corporate assets and costs are required to be allocated to the CGUs suitably, in which

reasonableness regarding allocation could be identified (Chen, Krishnan and Sami 2014).

However, these judgements and estimations are found to be missing in the financial reports of

JB Hi-Fi and hence, it is advised to take into account these aspects. Finally, according to

ASIC, organisations are required using fair value effectively in order to conduct exploration

testing. No such disclosure could be found from the latest annual report of JB Hi-Fi, which it

has to consider for enhancing the quality of financial reporting.

Requirement d:

In accordance with general purpose financial reporting (GPFR), organisations have

the obligation to report about their financial position in the market (Su and Wells 2015). The

second objective needs the organisations to reveal their financial performance and the final

objective is to provide cash flow information to the users for decision-making. In addition,

the financial reports presented have to be relevant and represented faithfully. JB Hi-Fi has

applied necessary professional judgements in relation to impairment that carry relevance to

the users. However, it has failed to include certain aspects discussed in the earlier sections in

its financial reports that lack professional judgement and faithful representation (Yallwe and

Buscemi 2014). Therefore, it could be stated that the applied professional judgement are not

aligned completely to the GPFR objectives.

Conclusion and recommendation:

From the above analysis, it is apparent that the role of professional judgement is

crucial, as it possesses the ability of affecting the financial information quality and decision-

making process of the users. The analysis clearly reveals the fact that JB Hi-Fi has reported

the required information of asset impairment in its latest annual report and majority of them

ACCG224 S1 2019 SID Page 6

The organisations are obliged by ASIC of not using increasing cash flows after five

years without taking into account the offsetting effect on discount rate (Kabir and Rahman

2016). Due to this, JB H-Fi has used extrapolation method in order to take into account the

impact of cash flows above five years. Moreover, ASIC restricts the organisations in

identifying CGUs at excessively high levels, in which cash flows of an individual asset are

dependent (Sinclair and Keller 2014). By taking into consideration this aspect, JB Hi-Fi has

grouped its CGUs at lower level where there are distinct identifiable and considerably

independent cash flows.

Corporate assets and costs are required to be allocated to the CGUs suitably, in which

reasonableness regarding allocation could be identified (Chen, Krishnan and Sami 2014).

However, these judgements and estimations are found to be missing in the financial reports of

JB Hi-Fi and hence, it is advised to take into account these aspects. Finally, according to

ASIC, organisations are required using fair value effectively in order to conduct exploration

testing. No such disclosure could be found from the latest annual report of JB Hi-Fi, which it

has to consider for enhancing the quality of financial reporting.

Requirement d:

In accordance with general purpose financial reporting (GPFR), organisations have

the obligation to report about their financial position in the market (Su and Wells 2015). The

second objective needs the organisations to reveal their financial performance and the final

objective is to provide cash flow information to the users for decision-making. In addition,

the financial reports presented have to be relevant and represented faithfully. JB Hi-Fi has

applied necessary professional judgements in relation to impairment that carry relevance to

the users. However, it has failed to include certain aspects discussed in the earlier sections in

its financial reports that lack professional judgement and faithful representation (Yallwe and

Buscemi 2014). Therefore, it could be stated that the applied professional judgement are not

aligned completely to the GPFR objectives.

Conclusion and recommendation:

From the above analysis, it is apparent that the role of professional judgement is

crucial, as it possesses the ability of affecting the financial information quality and decision-

making process of the users. The analysis clearly reveals the fact that JB Hi-Fi has reported

the required information of asset impairment in its latest annual report and majority of them

ACCG224 S1 2019 SID Page 6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

APPLICATION OF PROFESSIONAL JUDGEMENT ON IMPAIRMENT TESTING

adhere to the prevailing standards. However, the organisation has to take into account the

ASIC regulations for enhanced impairment testing and reporting of assets.

ACCG224 S1 2019 SID Page 7

adhere to the prevailing standards. However, the organisation has to take into account the

ASIC regulations for enhanced impairment testing and reporting of assets.

ACCG224 S1 2019 SID Page 7

APPLICATION OF PROFESSIONAL JUDGEMENT ON IMPAIRMENT TESTING

References:

André, P., Dionysiou, D. and Tsalavoutas, I., 2018. Mandated disclosures under IAS 36

Impairment of Assets and IAS 38 Intangible Assets: value relevance and impact on analysts’

forecasts. Applied Economics, 50(7), pp.707-725.

Asic.gov.au., 2019. 18-159MR Major changes affecting reported net assets and profit, and

other focuses for 30 June 2018 reporting | ASIC - Australian Securities and Investments

Commission. [online] Available at: https://asic.gov.au/about-asic/news-centre/find-a-media-

release/2018-releases/18-159mr-major-changes-affecting-reported-net-assets-and-profit-and-

other-focuses-for-30-june-2018-reporting [Accessed 28 Apr. 2019].

Banker, R.D., Basu, S. and Byzalov, D., 2016. Implications of Impairment Decisions and

Assets' Cash-Flow Horizons for Conservatism Research. The Accounting Review, 92(2),

pp.41-67.

Carvalho, C., Rodrigues, A.M. and Ferreira, C., 2016. The recognition of goodwill and other

intangible assets in business combinations–The Portuguese case. Australian Accounting

Review, 26(1), pp.4-20.

Chen, L.H., Krishnan, J. and Sami, H., 2014. Goodwill impairment charges and analyst

forecast properties. Accounting Horizons, 29(1), pp.141-169.

Coste, A.I., Tudor, A.T. and Pali-Pista, S.F., 2014. Compliance of Non-current Assets with

IFRS Requirements Concerning the Information Disclosure–Case Study. Procedia

Economics and Finance, 15, pp.1391-1395.

Darrough, M.N., Guler, L. and Wang, P., 2014. Goodwill impairment losses and CEO

compensation. Journal of Accounting, Auditing & Finance, 29(4), pp.435-463.

Detzen, D., Wersborg, T.S.G. and Zülch, H., 2015. Bleak weather for sun-shine AG: A case

study of impairment of assets. Issues in Accounting Education, 30(2), pp.18-39.

Jbhifi.com.au., 2019. JB Hi-Fi | JB Hi-Fi - Australia's Largest Home Entertainment Retailer.

[online] Available at: https://www.jbhifi.com.au/ [Accessed 28 Apr. 2019].

ACCG224 S1 2019 SID Page 8

References:

André, P., Dionysiou, D. and Tsalavoutas, I., 2018. Mandated disclosures under IAS 36

Impairment of Assets and IAS 38 Intangible Assets: value relevance and impact on analysts’

forecasts. Applied Economics, 50(7), pp.707-725.

Asic.gov.au., 2019. 18-159MR Major changes affecting reported net assets and profit, and

other focuses for 30 June 2018 reporting | ASIC - Australian Securities and Investments

Commission. [online] Available at: https://asic.gov.au/about-asic/news-centre/find-a-media-

release/2018-releases/18-159mr-major-changes-affecting-reported-net-assets-and-profit-and-

other-focuses-for-30-june-2018-reporting [Accessed 28 Apr. 2019].

Banker, R.D., Basu, S. and Byzalov, D., 2016. Implications of Impairment Decisions and

Assets' Cash-Flow Horizons for Conservatism Research. The Accounting Review, 92(2),

pp.41-67.

Carvalho, C., Rodrigues, A.M. and Ferreira, C., 2016. The recognition of goodwill and other

intangible assets in business combinations–The Portuguese case. Australian Accounting

Review, 26(1), pp.4-20.

Chen, L.H., Krishnan, J. and Sami, H., 2014. Goodwill impairment charges and analyst

forecast properties. Accounting Horizons, 29(1), pp.141-169.

Coste, A.I., Tudor, A.T. and Pali-Pista, S.F., 2014. Compliance of Non-current Assets with

IFRS Requirements Concerning the Information Disclosure–Case Study. Procedia

Economics and Finance, 15, pp.1391-1395.

Darrough, M.N., Guler, L. and Wang, P., 2014. Goodwill impairment losses and CEO

compensation. Journal of Accounting, Auditing & Finance, 29(4), pp.435-463.

Detzen, D., Wersborg, T.S.G. and Zülch, H., 2015. Bleak weather for sun-shine AG: A case

study of impairment of assets. Issues in Accounting Education, 30(2), pp.18-39.

Jbhifi.com.au., 2019. JB Hi-Fi | JB Hi-Fi - Australia's Largest Home Entertainment Retailer.

[online] Available at: https://www.jbhifi.com.au/ [Accessed 28 Apr. 2019].

ACCG224 S1 2019 SID Page 8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

APPLICATION OF PROFESSIONAL JUDGEMENT ON IMPAIRMENT TESTING

Kabir, H. and Rahman, A., 2016. The role of corporate governance in accounting discretion

under IFRS: Goodwill impairment in Australia. Journal of Contemporary Accounting &

Economics, 12(3), pp.290-308.

Komissarov, S., Kastantin, J.T. and Rick, K., 2014. Impairment of Long-Lived Assets: A

Comparison under the ASC and IFRS. The CPA Journal, 84(5), p.28.

Linnenluecke, M.K., Birt, J., Lyon, J. and Sidhu, B.K., 2015. Planetary boundaries:

implications for asset impairment. Accounting & Finance, 55(4), pp.911-929.

Member.afraccess.com., 2019. [online] Available at: http://member.afraccess.com/media?

id=CMN://3A498121&filename=20180813/JBH_02008547.pdf [Accessed 28 Apr. 2019].

Paugam, L. and Ramond, O., 2015. Effect of impairment‐testing disclosures on the cost of

equity capital. Journal of Business Finance & Accounting, 42(5-6), pp.583-618.

Rennekamp, K., Rupar, K.K. and Seybert, N., 2014. Impaired judgment: The effects of asset

impairment reversibility and cognitive dissonance on future investment. The Accounting

Review, 90(2), pp.739-759.

Sinclair, R.N. and Keller, K.L., 2014. A case for brands as assets: Acquired and internally

developed. Journal of Brand Management, 21(4), pp.286-302.

Su, W.H. and Wells, P., 2015. The association of identifiable intangible assets acquired and

recognised in business acquisitions with postacquisition firm performance. Accounting &

Finance, 55(4), pp.1171-1199.

Yallwe, A.H. and Buscemi, A., 2014. An era of intangible assets. Journal of Applied Finance

and Banking, 4(5), p.17.

ACCG224 S1 2019 SID Page 9

Kabir, H. and Rahman, A., 2016. The role of corporate governance in accounting discretion

under IFRS: Goodwill impairment in Australia. Journal of Contemporary Accounting &

Economics, 12(3), pp.290-308.

Komissarov, S., Kastantin, J.T. and Rick, K., 2014. Impairment of Long-Lived Assets: A

Comparison under the ASC and IFRS. The CPA Journal, 84(5), p.28.

Linnenluecke, M.K., Birt, J., Lyon, J. and Sidhu, B.K., 2015. Planetary boundaries:

implications for asset impairment. Accounting & Finance, 55(4), pp.911-929.

Member.afraccess.com., 2019. [online] Available at: http://member.afraccess.com/media?

id=CMN://3A498121&filename=20180813/JBH_02008547.pdf [Accessed 28 Apr. 2019].

Paugam, L. and Ramond, O., 2015. Effect of impairment‐testing disclosures on the cost of

equity capital. Journal of Business Finance & Accounting, 42(5-6), pp.583-618.

Rennekamp, K., Rupar, K.K. and Seybert, N., 2014. Impaired judgment: The effects of asset

impairment reversibility and cognitive dissonance on future investment. The Accounting

Review, 90(2), pp.739-759.

Sinclair, R.N. and Keller, K.L., 2014. A case for brands as assets: Acquired and internally

developed. Journal of Brand Management, 21(4), pp.286-302.

Su, W.H. and Wells, P., 2015. The association of identifiable intangible assets acquired and

recognised in business acquisitions with postacquisition firm performance. Accounting &

Finance, 55(4), pp.1171-1199.

Yallwe, A.H. and Buscemi, A., 2014. An era of intangible assets. Journal of Applied Finance

and Banking, 4(5), p.17.

ACCG224 S1 2019 SID Page 9

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.