Perpetual Limited: Impairment Testing and Lease Accounting Analysis

VerifiedAdded on 2020/05/28

|10

|3145

|47

Report

AI Summary

This report examines the impairment testing and lease accounting practices of Perpetual Limited, focusing on the application of Australian Accounting Standards (AASB) 136 and 139. It analyzes the company's process of identifying assets subject to impairment, including receivables, property, plant, and equipment, and goodwill, and the methods used to determine recoverable amounts. The report details the identification of cash-generating units, the estimation of future cash flows, and the use of discounting rates. Furthermore, it critiques the subjectivity inherent in the impairment testing process, particularly in relation to the estimation of cash flows and the use of different discounting rates. The report also addresses lease accounting, discussing the impact of the new lease standards and how the balance sheet reflects economic reality. It highlights the changes in accounting treatment, the shift from operating leases to actual liabilities, and the implications for financial statement analysis. The report concludes with a discussion of fair value measurement levels and the interesting aspects of impairment testing, offering a comprehensive overview of the company's financial reporting practices. This report is contributed by a student to Desklib.

ANSWER TO PART A

Part (i)

As per notes to the financial statements of the Company – Perpetual Limited of the year ending

thirtieth of June two thousand and seventeen, following have been identified for which the

company has undergone the test for impairment and accordingly impairment charges or loss have

been recorded:

Receivables – Receivables includes the amount which is due from the sundry debtors and

other receivables.

Noncurrent assets mainly including Property Plant and Equipment which comprises of

Plant and Equipment, Leasehold Improvements and Project Work in Progress.

Intangible asset - Goodwill of the company

Intangibles comprising of customer contracts, capitalized software, and project work in

progress and including those intangibles which acquired by the company during

the acquisition of other companies.

Assets carrying the financial risk.

Part (ii)

The testing of impairment has been done by the company as specified in the annual report of the

company. The company has followed the Australian accounting standard 136 and 139 dealing

with the impairment of assets and the financial instruments – recognition and measurement.

The company has mentioned in the notes to accounts that the assets grouped under the head

property plant and equipment is tested for the impairment when it is required or when it is

probable that the particular asset might have got impaired. The test for the impairment has been

conducted on a yearly basis and generally at the end of the financial year. Like 30th of June 2017

or 31st December 2017. While conducting the impairment test, the two figures of all the assets

within the group – Property plant and equipment are calculated and then compared. These two

1

Part (i)

As per notes to the financial statements of the Company – Perpetual Limited of the year ending

thirtieth of June two thousand and seventeen, following have been identified for which the

company has undergone the test for impairment and accordingly impairment charges or loss have

been recorded:

Receivables – Receivables includes the amount which is due from the sundry debtors and

other receivables.

Noncurrent assets mainly including Property Plant and Equipment which comprises of

Plant and Equipment, Leasehold Improvements and Project Work in Progress.

Intangible asset - Goodwill of the company

Intangibles comprising of customer contracts, capitalized software, and project work in

progress and including those intangibles which acquired by the company during

the acquisition of other companies.

Assets carrying the financial risk.

Part (ii)

The testing of impairment has been done by the company as specified in the annual report of the

company. The company has followed the Australian accounting standard 136 and 139 dealing

with the impairment of assets and the financial instruments – recognition and measurement.

The company has mentioned in the notes to accounts that the assets grouped under the head

property plant and equipment is tested for the impairment when it is required or when it is

probable that the particular asset might have got impaired. The test for the impairment has been

conducted on a yearly basis and generally at the end of the financial year. Like 30th of June 2017

or 31st December 2017. While conducting the impairment test, the two figures of all the assets

within the group – Property plant and equipment are calculated and then compared. These two

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

figures are recoverable amount and the amount at which the assets are being carried on the

balance sheet date. Recoverable amount is defined as the value which is higher of the following:

- Value in Use – Under this amount the present value of all the estimated cash flows is

calculated using the discount rate equivalent to the cost of capital. The estimated cash

flows also include the amount of the residual value of the asset.

- Net Selling Price – It is equivalent to the amount which the company will receive on

selling that particular asset and the amount will be the net off the expenditures.

In case the carrying amount is stated in the financial statements above the recoverable amount,

then the impairment is made and accordingly charged to the statement of profit and loss and

deducted from the value of the particular asset.

For the purpose of the impairment testing of the goodwill, the company has identified three cash

generating units namely:

- Perpetual Private

- Perpetual Corporate Trust

- Australian Equities (Perpetual Investments) (AASB, 2016)

For the purpose of the non financial assets, the company has identified cash generating units for

the purpose of impairment testing.

Part (iii)

As per the annual report of the company for the period ending 30th of June 2017, the company

has charged the impairment to the consolidated profit and loss account. In accordance with the

paragraphs of the accounting standard, in case there is difference between the recoverable

amount and carrying amount then the impairment is charged to the profit and loss account and

the assets account has been deducted with the value of the impairment so charged. The amount

which has been recorded as the impairment for the year in the financial statements is mentioned

below:

2

balance sheet date. Recoverable amount is defined as the value which is higher of the following:

- Value in Use – Under this amount the present value of all the estimated cash flows is

calculated using the discount rate equivalent to the cost of capital. The estimated cash

flows also include the amount of the residual value of the asset.

- Net Selling Price – It is equivalent to the amount which the company will receive on

selling that particular asset and the amount will be the net off the expenditures.

In case the carrying amount is stated in the financial statements above the recoverable amount,

then the impairment is made and accordingly charged to the statement of profit and loss and

deducted from the value of the particular asset.

For the purpose of the impairment testing of the goodwill, the company has identified three cash

generating units namely:

- Perpetual Private

- Perpetual Corporate Trust

- Australian Equities (Perpetual Investments) (AASB, 2016)

For the purpose of the non financial assets, the company has identified cash generating units for

the purpose of impairment testing.

Part (iii)

As per the annual report of the company for the period ending 30th of June 2017, the company

has charged the impairment to the consolidated profit and loss account. In accordance with the

paragraphs of the accounting standard, in case there is difference between the recoverable

amount and carrying amount then the impairment is charged to the profit and loss account and

the assets account has been deducted with the value of the impairment so charged. The amount

which has been recorded as the impairment for the year in the financial statements is mentioned

below:

2

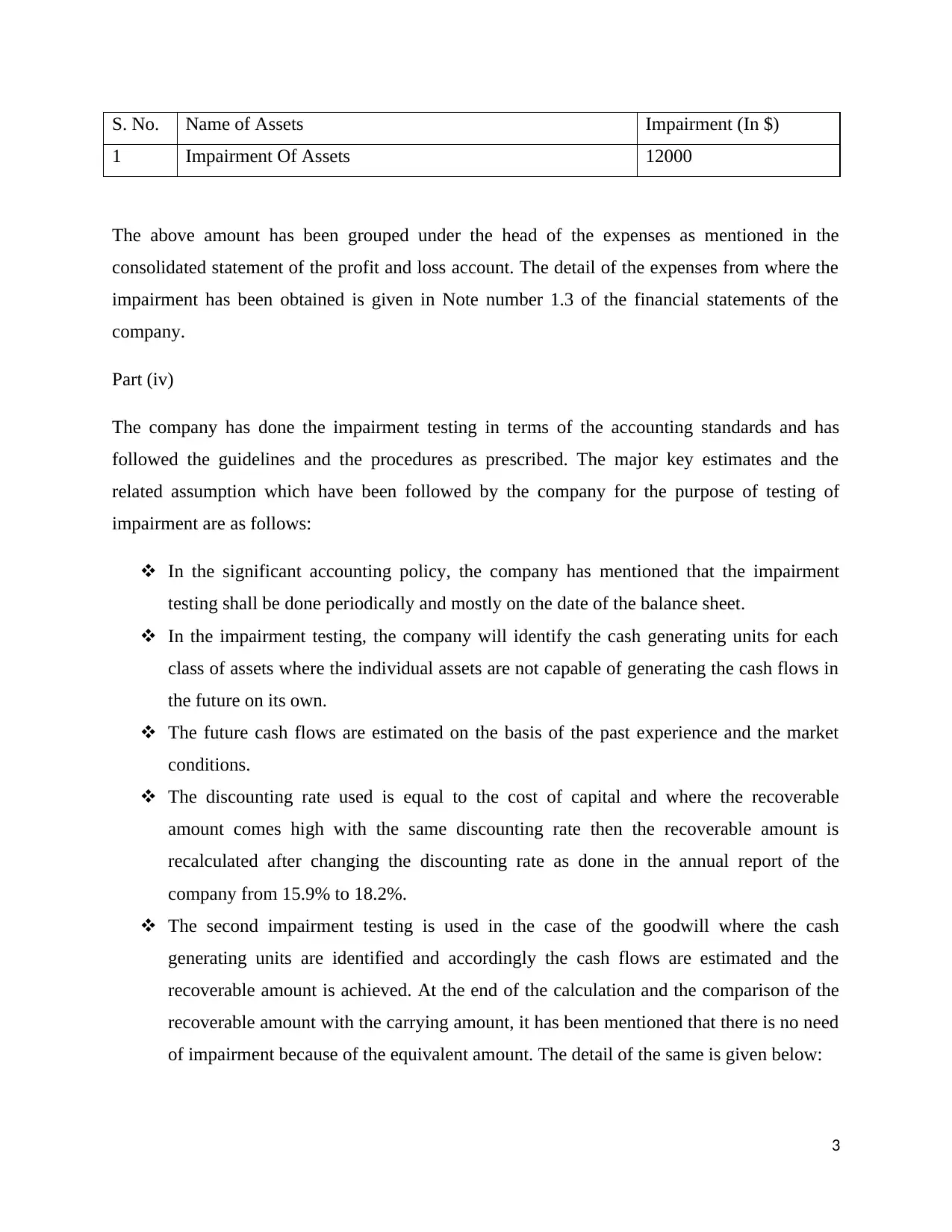

S. No. Name of Assets Impairment (In $)

1 Impairment Of Assets 12000

The above amount has been grouped under the head of the expenses as mentioned in the

consolidated statement of the profit and loss account. The detail of the expenses from where the

impairment has been obtained is given in Note number 1.3 of the financial statements of the

company.

Part (iv)

The company has done the impairment testing in terms of the accounting standards and has

followed the guidelines and the procedures as prescribed. The major key estimates and the

related assumption which have been followed by the company for the purpose of testing of

impairment are as follows:

In the significant accounting policy, the company has mentioned that the impairment

testing shall be done periodically and mostly on the date of the balance sheet.

In the impairment testing, the company will identify the cash generating units for each

class of assets where the individual assets are not capable of generating the cash flows in

the future on its own.

The future cash flows are estimated on the basis of the past experience and the market

conditions.

The discounting rate used is equal to the cost of capital and where the recoverable

amount comes high with the same discounting rate then the recoverable amount is

recalculated after changing the discounting rate as done in the annual report of the

company from 15.9% to 18.2%.

The second impairment testing is used in the case of the goodwill where the cash

generating units are identified and accordingly the cash flows are estimated and the

recoverable amount is achieved. At the end of the calculation and the comparison of the

recoverable amount with the carrying amount, it has been mentioned that there is no need

of impairment because of the equivalent amount. The detail of the same is given below:

3

1 Impairment Of Assets 12000

The above amount has been grouped under the head of the expenses as mentioned in the

consolidated statement of the profit and loss account. The detail of the expenses from where the

impairment has been obtained is given in Note number 1.3 of the financial statements of the

company.

Part (iv)

The company has done the impairment testing in terms of the accounting standards and has

followed the guidelines and the procedures as prescribed. The major key estimates and the

related assumption which have been followed by the company for the purpose of testing of

impairment are as follows:

In the significant accounting policy, the company has mentioned that the impairment

testing shall be done periodically and mostly on the date of the balance sheet.

In the impairment testing, the company will identify the cash generating units for each

class of assets where the individual assets are not capable of generating the cash flows in

the future on its own.

The future cash flows are estimated on the basis of the past experience and the market

conditions.

The discounting rate used is equal to the cost of capital and where the recoverable

amount comes high with the same discounting rate then the recoverable amount is

recalculated after changing the discounting rate as done in the annual report of the

company from 15.9% to 18.2%.

The second impairment testing is used in the case of the goodwill where the cash

generating units are identified and accordingly the cash flows are estimated and the

recoverable amount is achieved. At the end of the calculation and the comparison of the

recoverable amount with the carrying amount, it has been mentioned that there is no need

of impairment because of the equivalent amount. The detail of the same is given below:

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

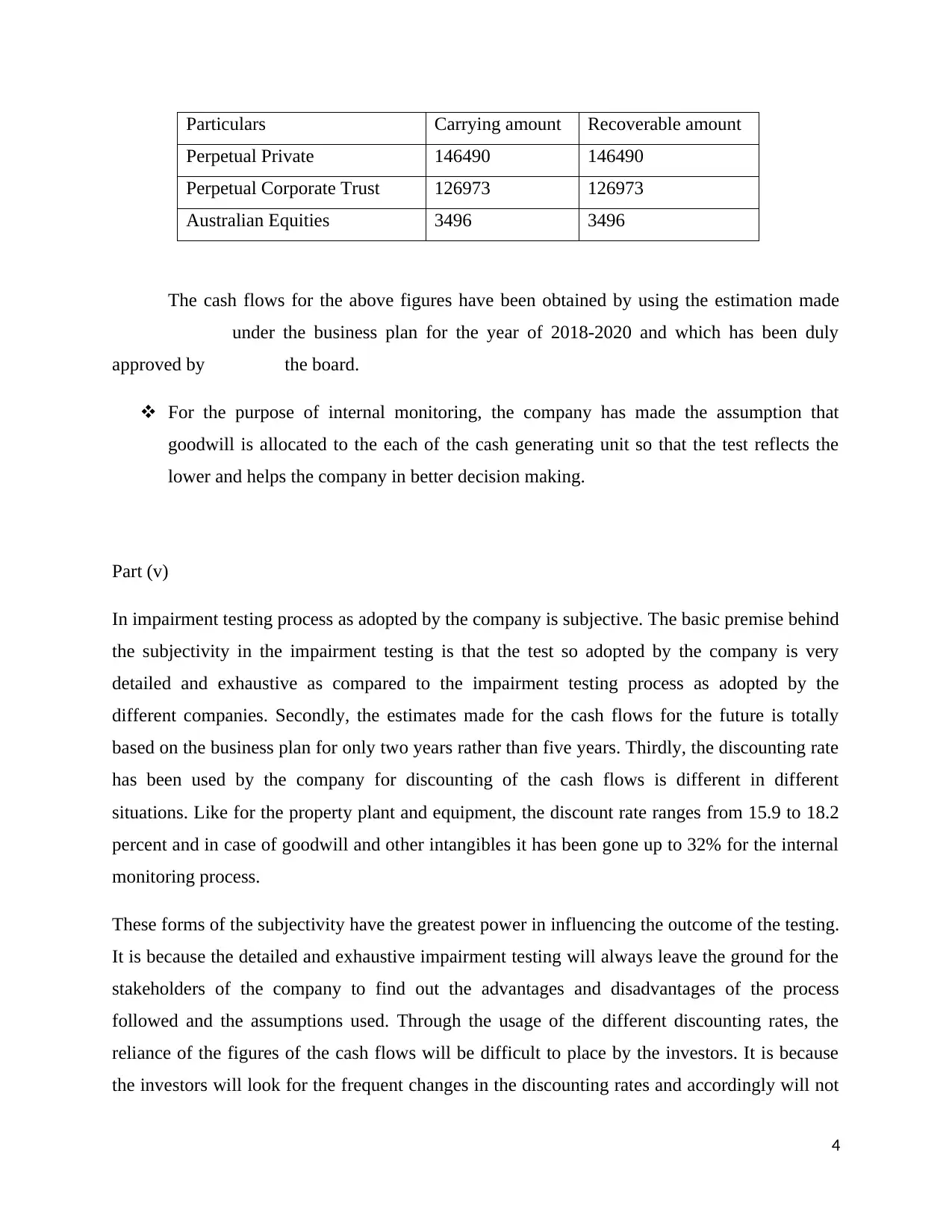

Particulars Carrying amount Recoverable amount

Perpetual Private 146490 146490

Perpetual Corporate Trust 126973 126973

Australian Equities 3496 3496

The cash flows for the above figures have been obtained by using the estimation made

under the business plan for the year of 2018-2020 and which has been duly

approved by the board.

For the purpose of internal monitoring, the company has made the assumption that

goodwill is allocated to the each of the cash generating unit so that the test reflects the

lower and helps the company in better decision making.

Part (v)

In impairment testing process as adopted by the company is subjective. The basic premise behind

the subjectivity in the impairment testing is that the test so adopted by the company is very

detailed and exhaustive as compared to the impairment testing process as adopted by the

different companies. Secondly, the estimates made for the cash flows for the future is totally

based on the business plan for only two years rather than five years. Thirdly, the discounting rate

has been used by the company for discounting of the cash flows is different in different

situations. Like for the property plant and equipment, the discount rate ranges from 15.9 to 18.2

percent and in case of goodwill and other intangibles it has been gone up to 32% for the internal

monitoring process.

These forms of the subjectivity have the greatest power in influencing the outcome of the testing.

It is because the detailed and exhaustive impairment testing will always leave the ground for the

stakeholders of the company to find out the advantages and disadvantages of the process

followed and the assumptions used. Through the usage of the different discounting rates, the

reliance of the figures of the cash flows will be difficult to place by the investors. It is because

the investors will look for the frequent changes in the discounting rates and accordingly will not

4

Perpetual Private 146490 146490

Perpetual Corporate Trust 126973 126973

Australian Equities 3496 3496

The cash flows for the above figures have been obtained by using the estimation made

under the business plan for the year of 2018-2020 and which has been duly

approved by the board.

For the purpose of internal monitoring, the company has made the assumption that

goodwill is allocated to the each of the cash generating unit so that the test reflects the

lower and helps the company in better decision making.

Part (v)

In impairment testing process as adopted by the company is subjective. The basic premise behind

the subjectivity in the impairment testing is that the test so adopted by the company is very

detailed and exhaustive as compared to the impairment testing process as adopted by the

different companies. Secondly, the estimates made for the cash flows for the future is totally

based on the business plan for only two years rather than five years. Thirdly, the discounting rate

has been used by the company for discounting of the cash flows is different in different

situations. Like for the property plant and equipment, the discount rate ranges from 15.9 to 18.2

percent and in case of goodwill and other intangibles it has been gone up to 32% for the internal

monitoring process.

These forms of the subjectivity have the greatest power in influencing the outcome of the testing.

It is because the detailed and exhaustive impairment testing will always leave the ground for the

stakeholders of the company to find out the advantages and disadvantages of the process

followed and the assumptions used. Through the usage of the different discounting rates, the

reliance of the figures of the cash flows will be difficult to place by the investors. It is because

the investors will look for the frequent changes in the discounting rates and accordingly will not

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

have faith in the figure of the net profit after tax. At last, the management of the company is

identifying the cash generating units on the personal basis for the purpose of the internal

monitoring which again will affect the reliance of the stakeholders of the company.

Part (vi)

In my opinion, the impairment testing is really interesting as already mentioned, the detailed note

and the explanation has been given by the company on the impairment wherever it becomes

necessary for the company to do so. The main interesting part is the identification of cash

generating units of the goodwill and the related carrying value and the recoverable value.

Part (vii)

The new thing that has been found in the company impairment testing is that the different

discounting rate has been used by the company and the through this discounting rate the cash

flows have been estimated and accordingly the impairment has been charged. Secondly the most

important thing that has happened is that the company has recalculated the present values with

the new discounting rate so as to keep the impairment at the lower level and accordingly the less

impairment has been booked.

Part (viii)

Note number 4 of the notes forming part of the financial statements of the company, the

company has identified the three levels for the measurement of the fair value of the assets and

liabilities of the company. Level one defines the quoted prices in active markets for the similar

assets and the liabilities. Level two defines the values other than quoted market prices either

directly or indirectly and level three defines those assets and liabilities which are not made

observable in an orderly or in orderly market. Apart from these identified levels, the company

has also defined the measurement of fair value as the market value of the particular asset and

then those are recorded at the fair value less amortization expense if any.

5

identifying the cash generating units on the personal basis for the purpose of the internal

monitoring which again will affect the reliance of the stakeholders of the company.

Part (vi)

In my opinion, the impairment testing is really interesting as already mentioned, the detailed note

and the explanation has been given by the company on the impairment wherever it becomes

necessary for the company to do so. The main interesting part is the identification of cash

generating units of the goodwill and the related carrying value and the recoverable value.

Part (vii)

The new thing that has been found in the company impairment testing is that the different

discounting rate has been used by the company and the through this discounting rate the cash

flows have been estimated and accordingly the impairment has been charged. Secondly the most

important thing that has happened is that the company has recalculated the present values with

the new discounting rate so as to keep the impairment at the lower level and accordingly the less

impairment has been booked.

Part (viii)

Note number 4 of the notes forming part of the financial statements of the company, the

company has identified the three levels for the measurement of the fair value of the assets and

liabilities of the company. Level one defines the quoted prices in active markets for the similar

assets and the liabilities. Level two defines the values other than quoted market prices either

directly or indirectly and level three defines those assets and liabilities which are not made

observable in an orderly or in orderly market. Apart from these identified levels, the company

has also defined the measurement of fair value as the market value of the particular asset and

then those are recorded at the fair value less amortization expense if any.

5

ANSWER TO PART B

i. As refer by the Chairperson of IASB, economic reality in relation to Leases standard

means that the Balance sheet of any company should show its real economic value or

financial value. As per the previous lease standard, leases are bifurcated on the basis of

Operating and Financial Lease which in turn involves the accounting treatment of

showing operating leases as Contingent Liability in place of actual liability (Ely, 2015).

This treatment creates unreal picture of assets and obligations of the company which is

way beyond the reality in economic terms. Also, it misleads the different persons who

wish to put money into the company by overstating the net worth of the company as real

liability were showing a contingent liability which was not considered in calculation of

net worth (Day and Stuart,2013).

ii. The statement which has presented in the question about the debts which are showing

into the balance sheet and outside the balance sheet is because of the reason of the

accounting treatment of the leases in the previous standard. In the pre change standard

leases are bifurcated into two parts which are financial lease and other is operating lease.

The leases are recorded as liability only if the risk and rewards relating to lease contact

has been transferred. In case of operating lease risk and rewards are never transferred or

transferred after the end of contract so this type of lease will not find the place in the

balance sheet but shown as contingent liability off the balance sheet of the company

(Singh, 2011). Before the new standard, this practice has been followed by airlines

companies and their continent liability become so huge that it becomes 3 times the

liabilities shown in the balance sheet as actual liability. Thus, the statement of 66 times

the off the balance sheet liability in comparison to in the balance sheet lease become true

(Ma, 2011).

iii. Previously that in the era of the old accounting standard on leases, most of the airlines

companies enter into a leasing contract which were generally in the form of Operating

leases meaning they are showing their lease liabilities as contingent liability and not

record the same in the balance sheet as actual liability (Singer, 2017). They were able to

play and manage their financial obligations away from financial statements which help

6

i. As refer by the Chairperson of IASB, economic reality in relation to Leases standard

means that the Balance sheet of any company should show its real economic value or

financial value. As per the previous lease standard, leases are bifurcated on the basis of

Operating and Financial Lease which in turn involves the accounting treatment of

showing operating leases as Contingent Liability in place of actual liability (Ely, 2015).

This treatment creates unreal picture of assets and obligations of the company which is

way beyond the reality in economic terms. Also, it misleads the different persons who

wish to put money into the company by overstating the net worth of the company as real

liability were showing a contingent liability which was not considered in calculation of

net worth (Day and Stuart,2013).

ii. The statement which has presented in the question about the debts which are showing

into the balance sheet and outside the balance sheet is because of the reason of the

accounting treatment of the leases in the previous standard. In the pre change standard

leases are bifurcated into two parts which are financial lease and other is operating lease.

The leases are recorded as liability only if the risk and rewards relating to lease contact

has been transferred. In case of operating lease risk and rewards are never transferred or

transferred after the end of contract so this type of lease will not find the place in the

balance sheet but shown as contingent liability off the balance sheet of the company

(Singh, 2011). Before the new standard, this practice has been followed by airlines

companies and their continent liability become so huge that it becomes 3 times the

liabilities shown in the balance sheet as actual liability. Thus, the statement of 66 times

the off the balance sheet liability in comparison to in the balance sheet lease become true

(Ma, 2011).

iii. Previously that in the era of the old accounting standard on leases, most of the airlines

companies enter into a leasing contract which were generally in the form of Operating

leases meaning they are showing their lease liabilities as contingent liability and not

record the same in the balance sheet as actual liability (Singer, 2017). They were able to

play and manage their financial obligations away from financial statements which help

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

them in showing high asset base or high net worth of the company. But after the

introduction of the new accounting standard on leases, the airline companies will have to

show operating leases as their actual liabilities. And the new contracts or new airlines

companies will have the advantage of not showing operating leases as their actual

liabilities resulting in correct net worth which is not higher as in previous cases. Airlines

Company both in term of intra and inter comparison is difficult as data of comparison is

not available. That is why the Chairperson of IASB has mentioned that there will not any

playing fields for airline companies after the introduction of new standard and has very

positively mention that there was no playing field available for airline companies (Gross,

2014).

iv. The Chairperson firmly mentioned that the new accounting standard on leases will not

find its actual place in the market as the it will not entertained by businesses so much

because of the following reasons:

o The first major reason is that the former accounting standard has given the

company very loop holes through which they have penetrated the major benefits

from the rules and regulations and the prescribed accounting standards due to

which they have been in the exercise of the booking the major amount of

liabilities off the balance sheet which otherwise would have come under the

liabilities head on the first view of the balance sheet.

o The second and major decision which the company will have to take is the putting

of the extra cost and the efforts including the time in the implementation of the

new accounting standard. The major cost will be incurred in the implementation

of the accounting standard as the new professionals will have to be hired and the

disclosure requirements will be increased accordingly. The assets and liabilities

which were not recorded earlier will now be mandatorily required to be entered

and disclosed in the same manner as in case of other assets and liabilities and

accordingly the disclosures needs to be made in respect of the accounting standard

followed by the company.

7

introduction of the new accounting standard on leases, the airline companies will have to

show operating leases as their actual liabilities. And the new contracts or new airlines

companies will have the advantage of not showing operating leases as their actual

liabilities resulting in correct net worth which is not higher as in previous cases. Airlines

Company both in term of intra and inter comparison is difficult as data of comparison is

not available. That is why the Chairperson of IASB has mentioned that there will not any

playing fields for airline companies after the introduction of new standard and has very

positively mention that there was no playing field available for airline companies (Gross,

2014).

iv. The Chairperson firmly mentioned that the new accounting standard on leases will not

find its actual place in the market as the it will not entertained by businesses so much

because of the following reasons:

o The first major reason is that the former accounting standard has given the

company very loop holes through which they have penetrated the major benefits

from the rules and regulations and the prescribed accounting standards due to

which they have been in the exercise of the booking the major amount of

liabilities off the balance sheet which otherwise would have come under the

liabilities head on the first view of the balance sheet.

o The second and major decision which the company will have to take is the putting

of the extra cost and the efforts including the time in the implementation of the

new accounting standard. The major cost will be incurred in the implementation

of the accounting standard as the new professionals will have to be hired and the

disclosure requirements will be increased accordingly. The assets and liabilities

which were not recorded earlier will now be mandatorily required to be entered

and disclosed in the same manner as in case of other assets and liabilities and

accordingly the disclosures needs to be made in respect of the accounting standard

followed by the company.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

o The third major reason why the new lease standard will become ineffective is that

the companies will resort to other means of financing instead of leasing (Lim,

2014). It is because there will be less requirement of disclosures and

implementation of the accounting standard provisions rather than other means of

financing. Secondly, their financial statements will become weak if new

accounting standard is adopted as the disclosure of the 66% of the liabilities

which are currently off the balance sheet. Thus, the net worth of the company will

automatically get decreased (Knubley, 2010; Moore and Nagy, 2013).

o The last reason is that mostly listed companies fall under the category of lease and

in case the new accounting standard is adopted then the company will feel

reluctant to adopt as their share price in the Australian stock exchange will get

deteriorated on real time and it will adversely affect the market globally.

Thus, the statement that the new leasing standard will not be popular with everyone is

quite significant and important.

v. There are many reasons behind the statement made by the chairperson. One of the major

reasons is the transparency that all the listed companies will have to follow. The

transparency will provide the management of the company and also the stakeholders of

the company to understand the financial statements of the company in the better manner

and thereby makes an efficient and an effective decision. The adoption of the new

accounting standard will help in eradicating the items like contingent liabilities which in

the current scenario represents the 66% of the total debt of the company FASB, (2016).

Thus, in this manner the new accounting standard has come up with the new methods of

transparency and will boost the confidence of the investors and other stakeholders of the

company.

8

the companies will resort to other means of financing instead of leasing (Lim,

2014). It is because there will be less requirement of disclosures and

implementation of the accounting standard provisions rather than other means of

financing. Secondly, their financial statements will become weak if new

accounting standard is adopted as the disclosure of the 66% of the liabilities

which are currently off the balance sheet. Thus, the net worth of the company will

automatically get decreased (Knubley, 2010; Moore and Nagy, 2013).

o The last reason is that mostly listed companies fall under the category of lease and

in case the new accounting standard is adopted then the company will feel

reluctant to adopt as their share price in the Australian stock exchange will get

deteriorated on real time and it will adversely affect the market globally.

Thus, the statement that the new leasing standard will not be popular with everyone is

quite significant and important.

v. There are many reasons behind the statement made by the chairperson. One of the major

reasons is the transparency that all the listed companies will have to follow. The

transparency will provide the management of the company and also the stakeholders of

the company to understand the financial statements of the company in the better manner

and thereby makes an efficient and an effective decision. The adoption of the new

accounting standard will help in eradicating the items like contingent liabilities which in

the current scenario represents the 66% of the total debt of the company FASB, (2016).

Thus, in this manner the new accounting standard has come up with the new methods of

transparency and will boost the confidence of the investors and other stakeholders of the

company.

8

REFERENCES

AASB, (2016), “Impairment of Assets” available at

http://www.aasb.gov.au/admin/file/content105/c9/AASB136_07-04_COMPjun09_01-10.pdf

accessed on {23-01-2018}.

AASB, (2016), “Financial Instruments: Recognition and Measurement” available at

http://www.aasb.gov.au/admin/file/content105/c9/AASB139_07-04_COMPoct10_01-11.pdf

accessed on {23-01-2018}.

Company Official Website, (2017), “Annual Report 2016”, available on

http://www.perpetuallimited.com.au accessed on {23/01/2018}.

Day, R. and Stuart, R., (2013), “New lease accounting proposal: what it means and what

companies can do to prepare.” Financial Executive, 29(6), pp.11-13.

FASB, (2016), “New Guidance on Lease Accounting” available at

http://www.fasb.org/jsp/FASB/FASBContent_C/NewsPage&cid=1176167901466 accessed on

{23/01/2018}.

Ely, K.M., (2015), “Operating lease accounting and the market's assessment of equity

risk”. Journal of Accounting Research, pp.397-415

Gross, A.D, (2014). “The path of lease resistance: How changes to lease accounting treatment

may impact your business”. Business Horizons, 57(6), pp.759-765.

Knubley, R., (2010). “Proposed changes to lease accounting”. Journal of Property Investment &

Finance, 28(5), pp.322-327

Lim, S.C., (2014), “Market Recognition of the Accounting Disclosure and Economic Benefits of

Operating Leases: Evidence from Borrowing Costs and Credit Ratings”.

9

AASB, (2016), “Impairment of Assets” available at

http://www.aasb.gov.au/admin/file/content105/c9/AASB136_07-04_COMPjun09_01-10.pdf

accessed on {23-01-2018}.

AASB, (2016), “Financial Instruments: Recognition and Measurement” available at

http://www.aasb.gov.au/admin/file/content105/c9/AASB139_07-04_COMPoct10_01-11.pdf

accessed on {23-01-2018}.

Company Official Website, (2017), “Annual Report 2016”, available on

http://www.perpetuallimited.com.au accessed on {23/01/2018}.

Day, R. and Stuart, R., (2013), “New lease accounting proposal: what it means and what

companies can do to prepare.” Financial Executive, 29(6), pp.11-13.

FASB, (2016), “New Guidance on Lease Accounting” available at

http://www.fasb.org/jsp/FASB/FASBContent_C/NewsPage&cid=1176167901466 accessed on

{23/01/2018}.

Ely, K.M., (2015), “Operating lease accounting and the market's assessment of equity

risk”. Journal of Accounting Research, pp.397-415

Gross, A.D, (2014). “The path of lease resistance: How changes to lease accounting treatment

may impact your business”. Business Horizons, 57(6), pp.759-765.

Knubley, R., (2010). “Proposed changes to lease accounting”. Journal of Property Investment &

Finance, 28(5), pp.322-327

Lim, S.C., (2014), “Market Recognition of the Accounting Disclosure and Economic Benefits of

Operating Leases: Evidence from Borrowing Costs and Credit Ratings”.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Ma W, (2011), “Impact on Financial Statements of New Accounting model for leases” available

at http://digitalcommons.uconn.edu/cgi/viewcontent.cgi?article=1194&context=srhonors_theses

accessed on {23/01/2018}

Moore, S. and Nagy, A., (2013), “CONTRACT STRUCTURING UNDER THE NEW LEASE

ACCOUNTING RULES: THE CASE OF CUSTOM DESIGN RETAIL, INC.” Global Perspectives

on Accounting Education, 10, p.81

Singer, R, ( 2017), “Accountinq for Leases Under the New Standard, Part 1: Definition and

Classification of Leases and Lessee Accounting”. CPA Journal, 87(8).

Singh, A.,( 2011). “A restaurant case study of lease accounting impacts of proposed changes in

lease accounting rules”. International Journal of Contemporary Hospitality Management, 23(6),

pp.820-839.

10

at http://digitalcommons.uconn.edu/cgi/viewcontent.cgi?article=1194&context=srhonors_theses

accessed on {23/01/2018}

Moore, S. and Nagy, A., (2013), “CONTRACT STRUCTURING UNDER THE NEW LEASE

ACCOUNTING RULES: THE CASE OF CUSTOM DESIGN RETAIL, INC.” Global Perspectives

on Accounting Education, 10, p.81

Singer, R, ( 2017), “Accountinq for Leases Under the New Standard, Part 1: Definition and

Classification of Leases and Lessee Accounting”. CPA Journal, 87(8).

Singh, A.,( 2011). “A restaurant case study of lease accounting impacts of proposed changes in

lease accounting rules”. International Journal of Contemporary Hospitality Management, 23(6),

pp.820-839.

10

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.