Corporate Accounting: Goodwill Impairment Loss and Reversal

VerifiedAdded on 2023/06/14

|8

|1878

|403

Report

AI Summary

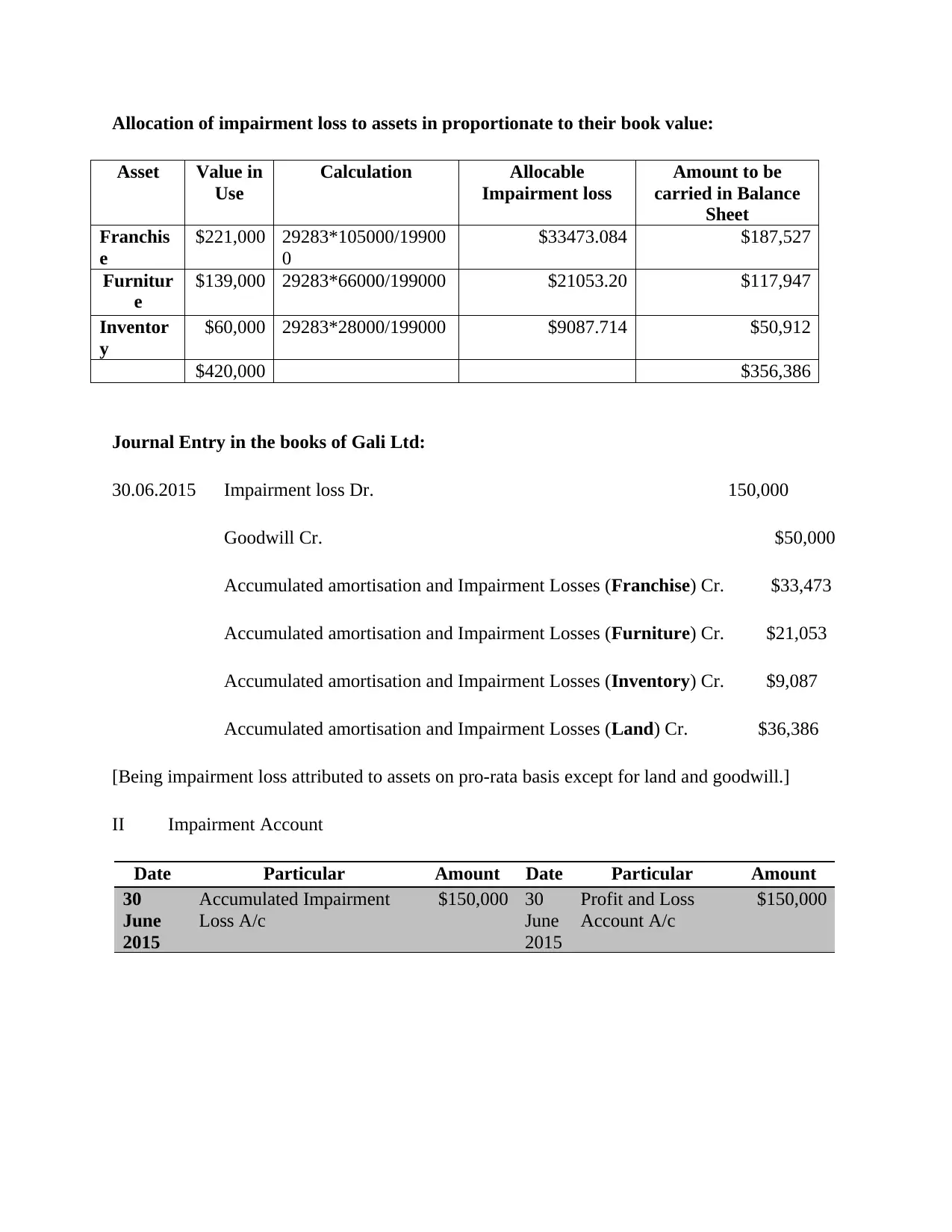

This report provides a comprehensive analysis of goodwill impairment in corporate accounting, focusing on the conditions for reversal, calculation of impairment loss, and relevant journal entries. It examines the accounting standards related to goodwill, particularly IAS 36, which prohibits the reversal of impairment losses on goodwill. The report details how to calculate and allocate impairment losses to various assets within a cash-generating unit (CGU), emphasizing the importance of not reducing an asset's carrying amount below its recoverable value. Furthermore, it includes a practical example with journal entries to illustrate the accounting treatment of impairment losses, providing a clear understanding of the financial implications and reporting requirements. Desklib offers a wealth of similar solved assignments and study resources for students.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.