Analyzing Asset Impairment Under AASB 136 and IFRS Standards

VerifiedAdded on 2020/05/28

|10

|1597

|262

AI Summary

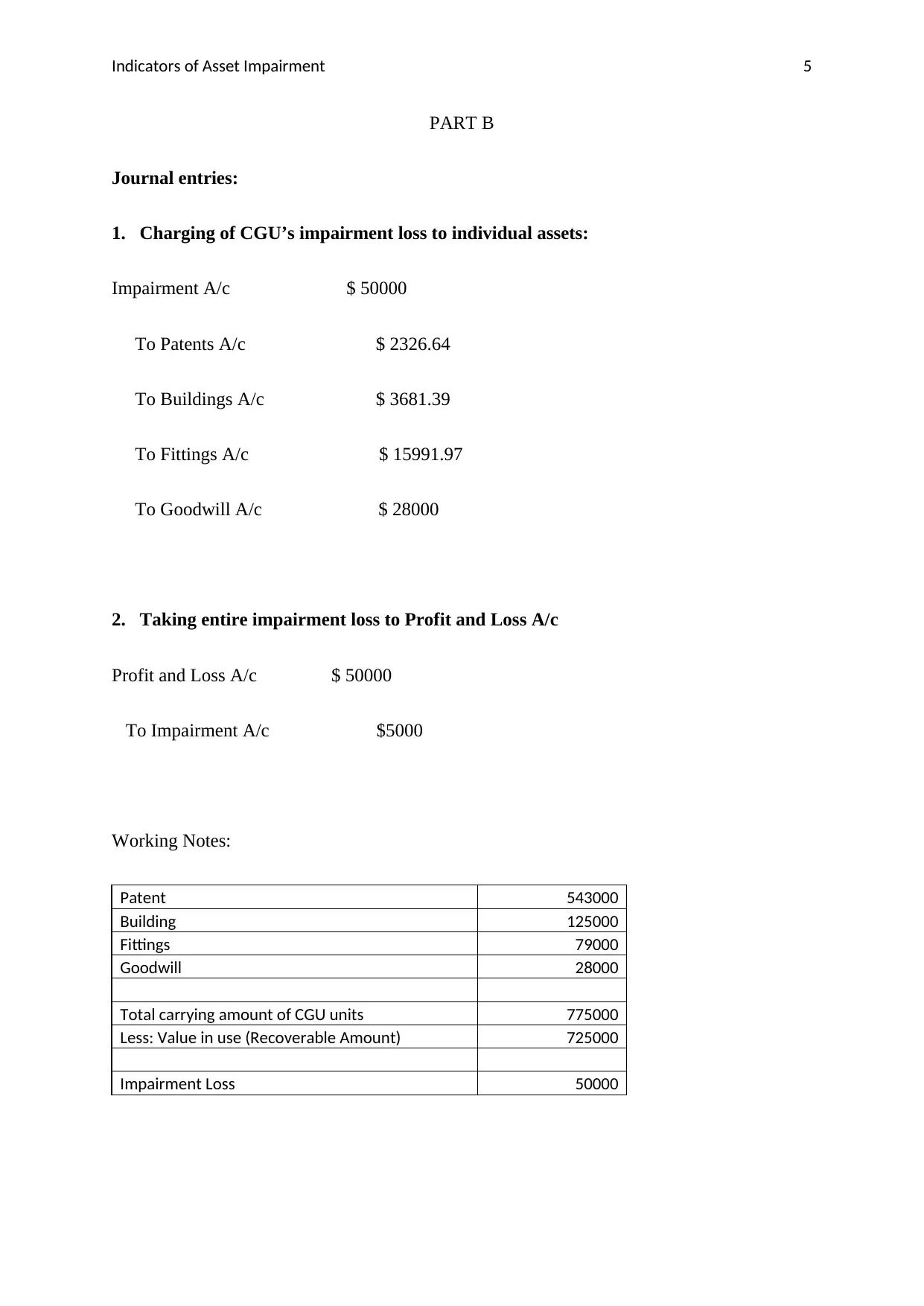

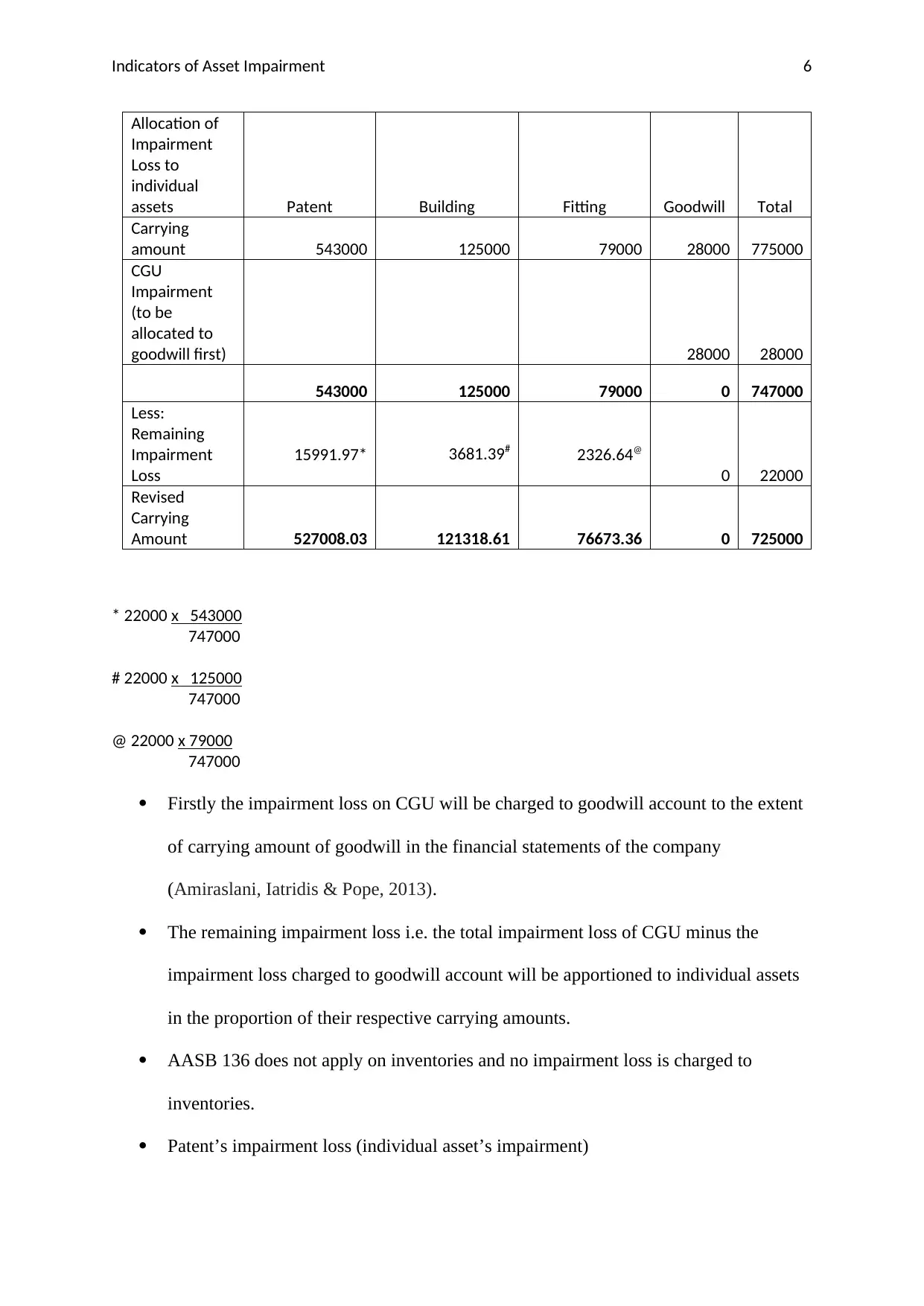

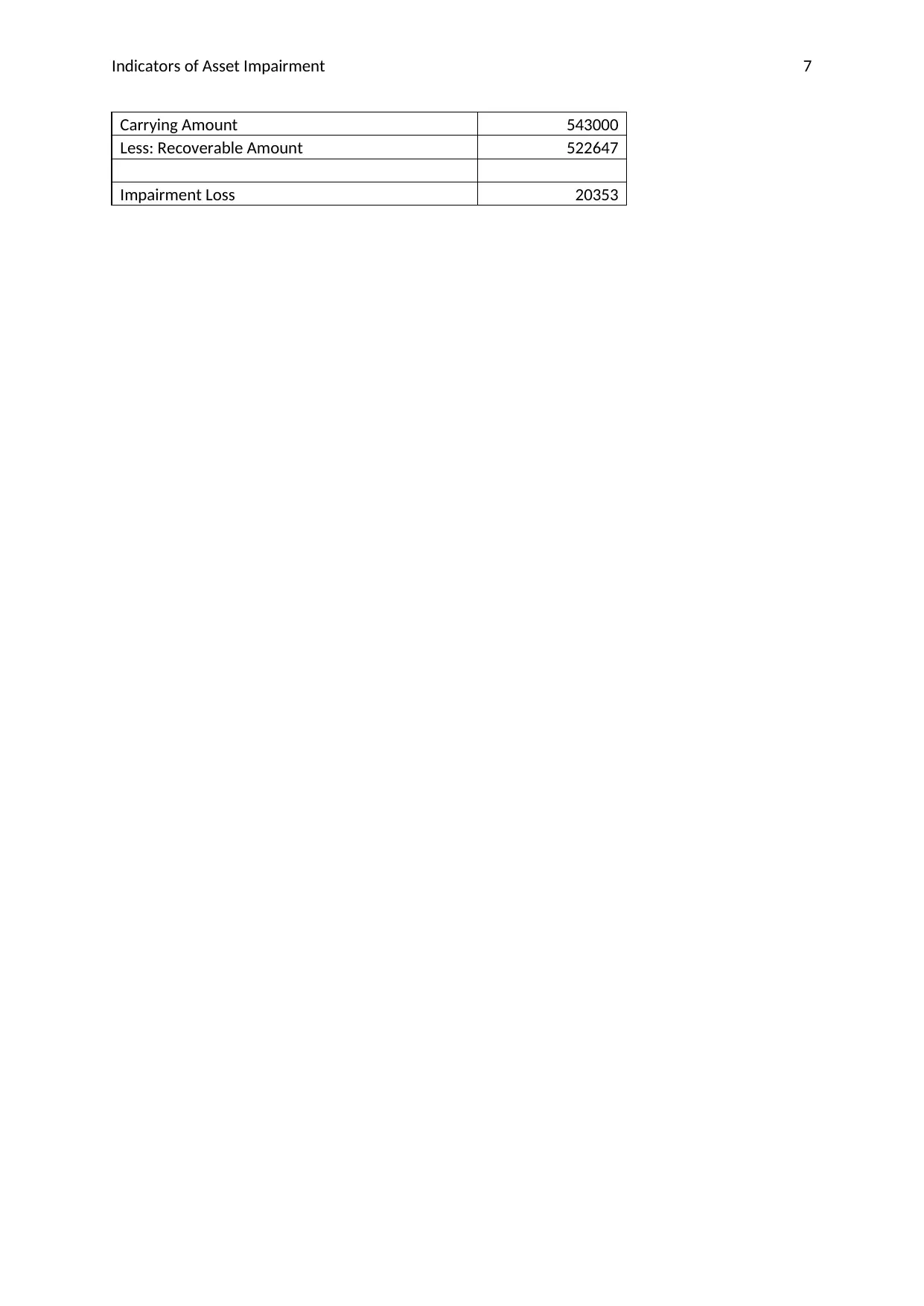

This analysis delves into the principles outlined in AASB 136 concerning the impairment of assets, specifically excluding inventories. The assignment examines how these standards apply to goodwill and other non-inventory assets within a business's financial statements. Key components include assessing the method for determining impairment losses and their subsequent allocation among various asset classes, such as patents, buildings, fittings, and goodwill. A practical example is provided, showcasing how impairment loss on a Cash Generating Unit (CGU) should first be charged to goodwill up to its carrying amount before being proportionally distributed across remaining assets based on their respective values. The analysis also contrasts these procedures with International Financial Reporting Standards (IFRS), highlighting compliance considerations and implications for European accounting practices as per the referenced studies.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.