Report: Financial Analysis of Imperial Brands PLC (2015-2019)

VerifiedAdded on 2023/01/16

|21

|3973

|84

Report

AI Summary

This report provides a comprehensive financial analysis of Imperial Brands PLC, a UK-based tobacco company, from 2015 to 2019. The analysis begins with an executive summary and an overview of the business environment, including industry trends, competitors, and market positioning. The core of the report focuses on a detailed data analysis and discussion, utilizing ratio analysis to evaluate the company's financial performance. Various categories of ratios are calculated, including profitability, liquidity, efficiency, investor, and gearing ratios. The report presents the calculated ratios, along with graphical representations and interpretations of key financial metrics such as gross profit, operating profit, and net profit margins. The study also examines liquidity, efficiency, and investor ratios to assess the company's financial health and operational effectiveness. Finally, the report concludes with findings, recommendations, and interpretations of the financial data, offering insights into Imperial Brands PLC's strengths, weaknesses, and overall financial standing.

Business Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

1. EXECUTIVE SUMMARY.........................................................................................................3

2. BUSINESS ENVIRONMENT....................................................................................................3

2.1 Description of business:.........................................................................................................3

2.2 Industry overview:.................................................................................................................3

2.3 Competitors and market positioning......................................................................................5

3. DATA ANALYSIS AND DISCUSSION...................................................................................5

3.1 Financial analysis:..................................................................................................................5

3.2 Different categories of ratios:................................................................................................6

3.3 Calculation of ratios:..............................................................................................................7

4. FINDINGS AND RECOMMENDATIONS.............................................................................10

CONCLUSION..............................................................................................................................19

REFERENCES..............................................................................................................................20

1. EXECUTIVE SUMMARY.........................................................................................................3

2. BUSINESS ENVIRONMENT....................................................................................................3

2.1 Description of business:.........................................................................................................3

2.2 Industry overview:.................................................................................................................3

2.3 Competitors and market positioning......................................................................................5

3. DATA ANALYSIS AND DISCUSSION...................................................................................5

3.1 Financial analysis:..................................................................................................................5

3.2 Different categories of ratios:................................................................................................6

3.3 Calculation of ratios:..............................................................................................................7

4. FINDINGS AND RECOMMENDATIONS.............................................................................10

CONCLUSION..............................................................................................................................19

REFERENCES..............................................................................................................................20

1. EXECUTIVE SUMMARY

The project report summarise about overall analysis of UK stock market listed company

which is Imperial brand plc. The initial part of abstracts about industrial review of company that

is involved in tobacco sector. In addition, financial analysis is done by help of ratio analysis

technique and a range of ratios are calculated such as profitability ratio, liquidity ratio and many

more.

2. BUSINESS ENVIRONMENT

2.1 Description of business:

Imperial brands plc is a British multinational tobacco company whose headquarter is in

Bristol, United Kingdom. This company was founded in year 1901, almost 119 years ago. The

company sell its products and services in more then 160 countries as well as they sell almost 320

billion cigarettes in a year (About Imperial brand plc, 2019). This company had about 51

factories all around the world. The company is world's fourth biggest international cigarette

company. As well as they are world's largest producer of tobacco products such as cigars, fine

cut tobacco and many more. In current time period there are more then 33000 employees who

are working with this company at global level.

Management and governance- Imperial brands plc delivering different range of products and

services by applying shared growth ambition strategy (Julien, 2018). The framework offers key

basis for promoting higher standards of corporate governance in Imperial brands plc.

The group risk committee is one of the most senior body which is responsible for assessing and

monitoring risk profit of company. This committee reports issues in according to Imperial brand

plc reputation risk control framework.

2.2 Industry overview:

Imperial brands plc is one of the biggest tobacco manufacturer and seller all around of

United Kingdom and world. The tobacco industry in UK employs about 5000 people. Industrial

revenue in year 2019 was of 480 million pounds in entire UK. As well as Imperial brand plc and

British American tobacco plc are two companies which are leading whole tobacco industry of

world.

The project report summarise about overall analysis of UK stock market listed company

which is Imperial brand plc. The initial part of abstracts about industrial review of company that

is involved in tobacco sector. In addition, financial analysis is done by help of ratio analysis

technique and a range of ratios are calculated such as profitability ratio, liquidity ratio and many

more.

2. BUSINESS ENVIRONMENT

2.1 Description of business:

Imperial brands plc is a British multinational tobacco company whose headquarter is in

Bristol, United Kingdom. This company was founded in year 1901, almost 119 years ago. The

company sell its products and services in more then 160 countries as well as they sell almost 320

billion cigarettes in a year (About Imperial brand plc, 2019). This company had about 51

factories all around the world. The company is world's fourth biggest international cigarette

company. As well as they are world's largest producer of tobacco products such as cigars, fine

cut tobacco and many more. In current time period there are more then 33000 employees who

are working with this company at global level.

Management and governance- Imperial brands plc delivering different range of products and

services by applying shared growth ambition strategy (Julien, 2018). The framework offers key

basis for promoting higher standards of corporate governance in Imperial brands plc.

The group risk committee is one of the most senior body which is responsible for assessing and

monitoring risk profit of company. This committee reports issues in according to Imperial brand

plc reputation risk control framework.

2.2 Industry overview:

Imperial brands plc is one of the biggest tobacco manufacturer and seller all around of

United Kingdom and world. The tobacco industry in UK employs about 5000 people. Industrial

revenue in year 2019 was of 480 million pounds in entire UK. As well as Imperial brand plc and

British American tobacco plc are two companies which are leading whole tobacco industry of

world.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

In the context of Barclays plc, SWOT is done below which is as follows:

SWOT analysis- This technique is being used in order to do micro environment analysis. It

assess strength, weakness, opportunities and threats.

Strength- It is related to those positive elements which a company has internally (Charter, 2017).

Imperial brands plc has below mentioned strengths:

Company has an effective cost structure that helps them in keeping overall cost lower

then standards.

Imperial company has a strong financial position which consecutive revenues in last 5

years which is a key strength.

Weakness- It is related to those negative elements which a company has internally. Imperial

brands plc has below mentioned weaknesses:

Above company has a lower current ratio that shows their inability to make payment of

short term debts.

This company has not conducted complete market research in last two years which is a

huge weakness to them.

Opportunities- This is linked with positive aspects of external environment which can benefit to

companies (Owen, Botelho and Anwar, 2016). Imperial brand plc has below mentioned

opportunities:

This company has an opportunity to expand own business on e-commerce which may

lead to higher sales revenue.

They have opportunity to do promotion of products and services through social media

that can be helpful for them to do marketing at lower cost.

Threats- This is linked with negative aspects of external environment which can affect negatively

to companies. Imperial brand plc has below mentioned threats:

Political uncertainties in the UK can affect to this bank because they will not be able to

manage all activities.

Increased level of competition is also a big threat for this enterprise.

SWOT analysis- This technique is being used in order to do micro environment analysis. It

assess strength, weakness, opportunities and threats.

Strength- It is related to those positive elements which a company has internally (Charter, 2017).

Imperial brands plc has below mentioned strengths:

Company has an effective cost structure that helps them in keeping overall cost lower

then standards.

Imperial company has a strong financial position which consecutive revenues in last 5

years which is a key strength.

Weakness- It is related to those negative elements which a company has internally. Imperial

brands plc has below mentioned weaknesses:

Above company has a lower current ratio that shows their inability to make payment of

short term debts.

This company has not conducted complete market research in last two years which is a

huge weakness to them.

Opportunities- This is linked with positive aspects of external environment which can benefit to

companies (Owen, Botelho and Anwar, 2016). Imperial brand plc has below mentioned

opportunities:

This company has an opportunity to expand own business on e-commerce which may

lead to higher sales revenue.

They have opportunity to do promotion of products and services through social media

that can be helpful for them to do marketing at lower cost.

Threats- This is linked with negative aspects of external environment which can affect negatively

to companies. Imperial brand plc has below mentioned threats:

Political uncertainties in the UK can affect to this bank because they will not be able to

manage all activities.

Increased level of competition is also a big threat for this enterprise.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2.3 Competitors and market positioning.

Competitors analysis- This can be defined as a systematic process of analysing number of

competitors which a business entity has in external environment (Mazzucato and Penna, 2015).

Such as Imperial brand plc has below mentioned competitors which are as follows:

Competitors of Barclays plc

S. No. Name of company

1 Altria

2 Reynolds American

3 British American Tobacco Plc

4 Japan Tobacco

5 Philip Morris International Plc

6 Vector Group Plc

7 Alliance one international incorporation

8 Swedish match AB

Market positioning- This can be defined as an ability to influence consumer perception regards to

a product relative to competitors. In other words, it is being used in order to assess market share

of a company in external environment. In the aspect of above company, market share is

fluctuating time to time because of tough competition. The market share of this company was of

7.2% in year 2015 that raised year after year. Such as in year 2017, it was of 8.5% and 9.2% in

year 2018.

3. DATA ANALYSIS AND DISCUSSION

3.1 Financial analysis:

The term financial analysis can be defined as a technique of gathering all sort of

monetary data and making proper analysis in an effective manner. There are different kinds of

Competitors analysis- This can be defined as a systematic process of analysing number of

competitors which a business entity has in external environment (Mazzucato and Penna, 2015).

Such as Imperial brand plc has below mentioned competitors which are as follows:

Competitors of Barclays plc

S. No. Name of company

1 Altria

2 Reynolds American

3 British American Tobacco Plc

4 Japan Tobacco

5 Philip Morris International Plc

6 Vector Group Plc

7 Alliance one international incorporation

8 Swedish match AB

Market positioning- This can be defined as an ability to influence consumer perception regards to

a product relative to competitors. In other words, it is being used in order to assess market share

of a company in external environment. In the aspect of above company, market share is

fluctuating time to time because of tough competition. The market share of this company was of

7.2% in year 2015 that raised year after year. Such as in year 2017, it was of 8.5% and 9.2% in

year 2018.

3. DATA ANALYSIS AND DISCUSSION

3.1 Financial analysis:

The term financial analysis can be defined as a technique of gathering all sort of

monetary data and making proper analysis in an effective manner. There are different kinds of

techniques in order to conduct financial analysis such as ratio analysis, vertical analysis and

many more. In the context of above Imperial brand plc, ratio analysis technique is applied for

making financial analysis.

3.2 Different categories of ratios:

Ratio analysis- It can be defined as a type of technique which is related to computing a range of

ratios with an objective of financial analysis (Grjebine and Tripier, 2016). There are a vital range

of ratios and some of them are mentioned below in such manner:

1. Profitability ratio- This ratio is computed in order to make proper analysis of profitability in an

effective manner. Under it, various kinds of ratios are included which are as follows:

Gross profit ratio

Net profit ratio

Operating profit ratio

2. Liquidity ratio- Under it, different types of ratios are included in order to analyse liquidity

position of companies (Haseeb, 2018). By help of this ratio, business entities become able to

know whether they are able to make short term debts or not. Herein, below some key liquidity

ratios are mentioned that are as follows:

Current ratio

Quick ratio

3. Efficiency ratio- It is defined as a type of ratio which shows the expenses as % of revenues

with some variations (Maxfield, 2019). This is essential for companies to compute amount of

expenses which they spend in order to gain revenues. Herein, below some key efficiency ratios

are mentioned that are as follows:

Inventory turn over ratio

Accounts receivable turnover ratio

Accounts payable turnover ratio

Total assets turnover ratio

Fixed assets turnover ratio

many more. In the context of above Imperial brand plc, ratio analysis technique is applied for

making financial analysis.

3.2 Different categories of ratios:

Ratio analysis- It can be defined as a type of technique which is related to computing a range of

ratios with an objective of financial analysis (Grjebine and Tripier, 2016). There are a vital range

of ratios and some of them are mentioned below in such manner:

1. Profitability ratio- This ratio is computed in order to make proper analysis of profitability in an

effective manner. Under it, various kinds of ratios are included which are as follows:

Gross profit ratio

Net profit ratio

Operating profit ratio

2. Liquidity ratio- Under it, different types of ratios are included in order to analyse liquidity

position of companies (Haseeb, 2018). By help of this ratio, business entities become able to

know whether they are able to make short term debts or not. Herein, below some key liquidity

ratios are mentioned that are as follows:

Current ratio

Quick ratio

3. Efficiency ratio- It is defined as a type of ratio which shows the expenses as % of revenues

with some variations (Maxfield, 2019). This is essential for companies to compute amount of

expenses which they spend in order to gain revenues. Herein, below some key efficiency ratios

are mentioned that are as follows:

Inventory turn over ratio

Accounts receivable turnover ratio

Accounts payable turnover ratio

Total assets turnover ratio

Fixed assets turnover ratio

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

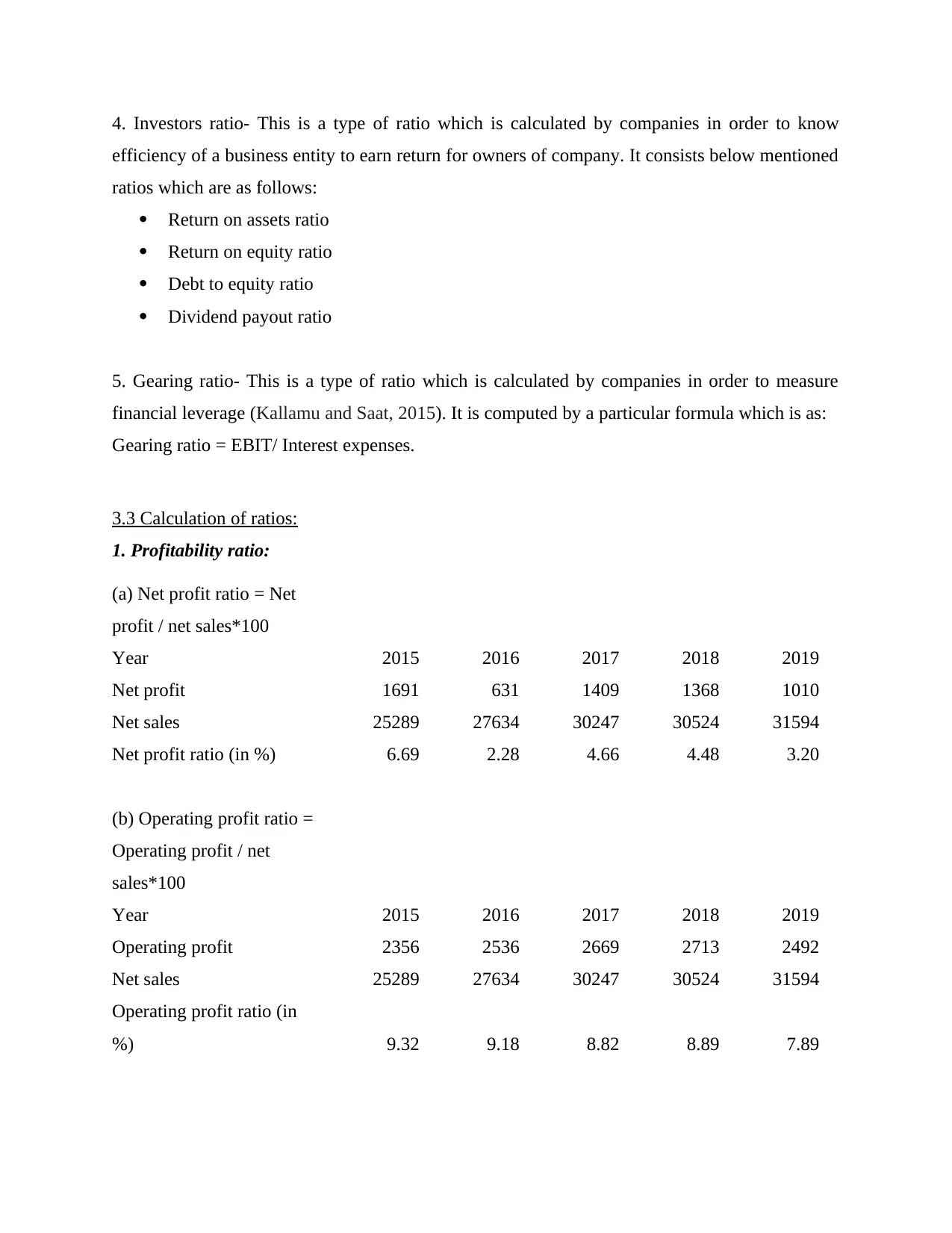

4. Investors ratio- This is a type of ratio which is calculated by companies in order to know

efficiency of a business entity to earn return for owners of company. It consists below mentioned

ratios which are as follows:

Return on assets ratio

Return on equity ratio

Debt to equity ratio

Dividend payout ratio

5. Gearing ratio- This is a type of ratio which is calculated by companies in order to measure

financial leverage (Kallamu and Saat, 2015). It is computed by a particular formula which is as:

Gearing ratio = EBIT/ Interest expenses.

3.3 Calculation of ratios:

1. Profitability ratio:

(a) Net profit ratio = Net

profit / net sales*100

Year 2015 2016 2017 2018 2019

Net profit 1691 631 1409 1368 1010

Net sales 25289 27634 30247 30524 31594

Net profit ratio (in %) 6.69 2.28 4.66 4.48 3.20

(b) Operating profit ratio =

Operating profit / net

sales*100

Year 2015 2016 2017 2018 2019

Operating profit 2356 2536 2669 2713 2492

Net sales 25289 27634 30247 30524 31594

Operating profit ratio (in

%) 9.32 9.18 8.82 8.89 7.89

efficiency of a business entity to earn return for owners of company. It consists below mentioned

ratios which are as follows:

Return on assets ratio

Return on equity ratio

Debt to equity ratio

Dividend payout ratio

5. Gearing ratio- This is a type of ratio which is calculated by companies in order to measure

financial leverage (Kallamu and Saat, 2015). It is computed by a particular formula which is as:

Gearing ratio = EBIT/ Interest expenses.

3.3 Calculation of ratios:

1. Profitability ratio:

(a) Net profit ratio = Net

profit / net sales*100

Year 2015 2016 2017 2018 2019

Net profit 1691 631 1409 1368 1010

Net sales 25289 27634 30247 30524 31594

Net profit ratio (in %) 6.69 2.28 4.66 4.48 3.20

(b) Operating profit ratio =

Operating profit / net

sales*100

Year 2015 2016 2017 2018 2019

Operating profit 2356 2536 2669 2713 2492

Net sales 25289 27634 30247 30524 31594

Operating profit ratio (in

%) 9.32 9.18 8.82 8.89 7.89

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

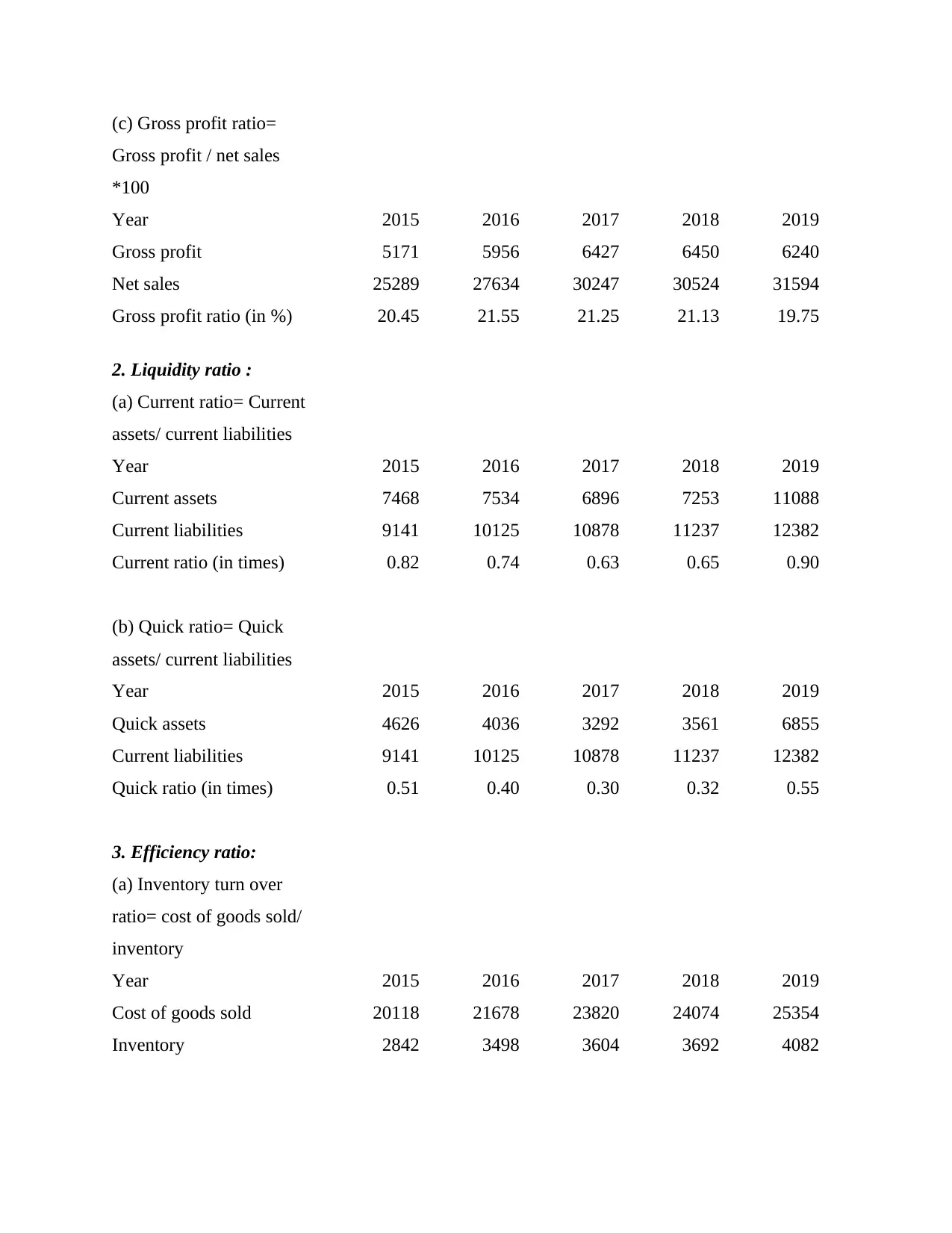

(c) Gross profit ratio=

Gross profit / net sales

*100

Year 2015 2016 2017 2018 2019

Gross profit 5171 5956 6427 6450 6240

Net sales 25289 27634 30247 30524 31594

Gross profit ratio (in %) 20.45 21.55 21.25 21.13 19.75

2. Liquidity ratio :

(a) Current ratio= Current

assets/ current liabilities

Year 2015 2016 2017 2018 2019

Current assets 7468 7534 6896 7253 11088

Current liabilities 9141 10125 10878 11237 12382

Current ratio (in times) 0.82 0.74 0.63 0.65 0.90

(b) Quick ratio= Quick

assets/ current liabilities

Year 2015 2016 2017 2018 2019

Quick assets 4626 4036 3292 3561 6855

Current liabilities 9141 10125 10878 11237 12382

Quick ratio (in times) 0.51 0.40 0.30 0.32 0.55

3. Efficiency ratio:

(a) Inventory turn over

ratio= cost of goods sold/

inventory

Year 2015 2016 2017 2018 2019

Cost of goods sold 20118 21678 23820 24074 25354

Inventory 2842 3498 3604 3692 4082

Gross profit / net sales

*100

Year 2015 2016 2017 2018 2019

Gross profit 5171 5956 6427 6450 6240

Net sales 25289 27634 30247 30524 31594

Gross profit ratio (in %) 20.45 21.55 21.25 21.13 19.75

2. Liquidity ratio :

(a) Current ratio= Current

assets/ current liabilities

Year 2015 2016 2017 2018 2019

Current assets 7468 7534 6896 7253 11088

Current liabilities 9141 10125 10878 11237 12382

Current ratio (in times) 0.82 0.74 0.63 0.65 0.90

(b) Quick ratio= Quick

assets/ current liabilities

Year 2015 2016 2017 2018 2019

Quick assets 4626 4036 3292 3561 6855

Current liabilities 9141 10125 10878 11237 12382

Quick ratio (in times) 0.51 0.40 0.30 0.32 0.55

3. Efficiency ratio:

(a) Inventory turn over

ratio= cost of goods sold/

inventory

Year 2015 2016 2017 2018 2019

Cost of goods sold 20118 21678 23820 24074 25354

Inventory 2842 3498 3604 3692 4082

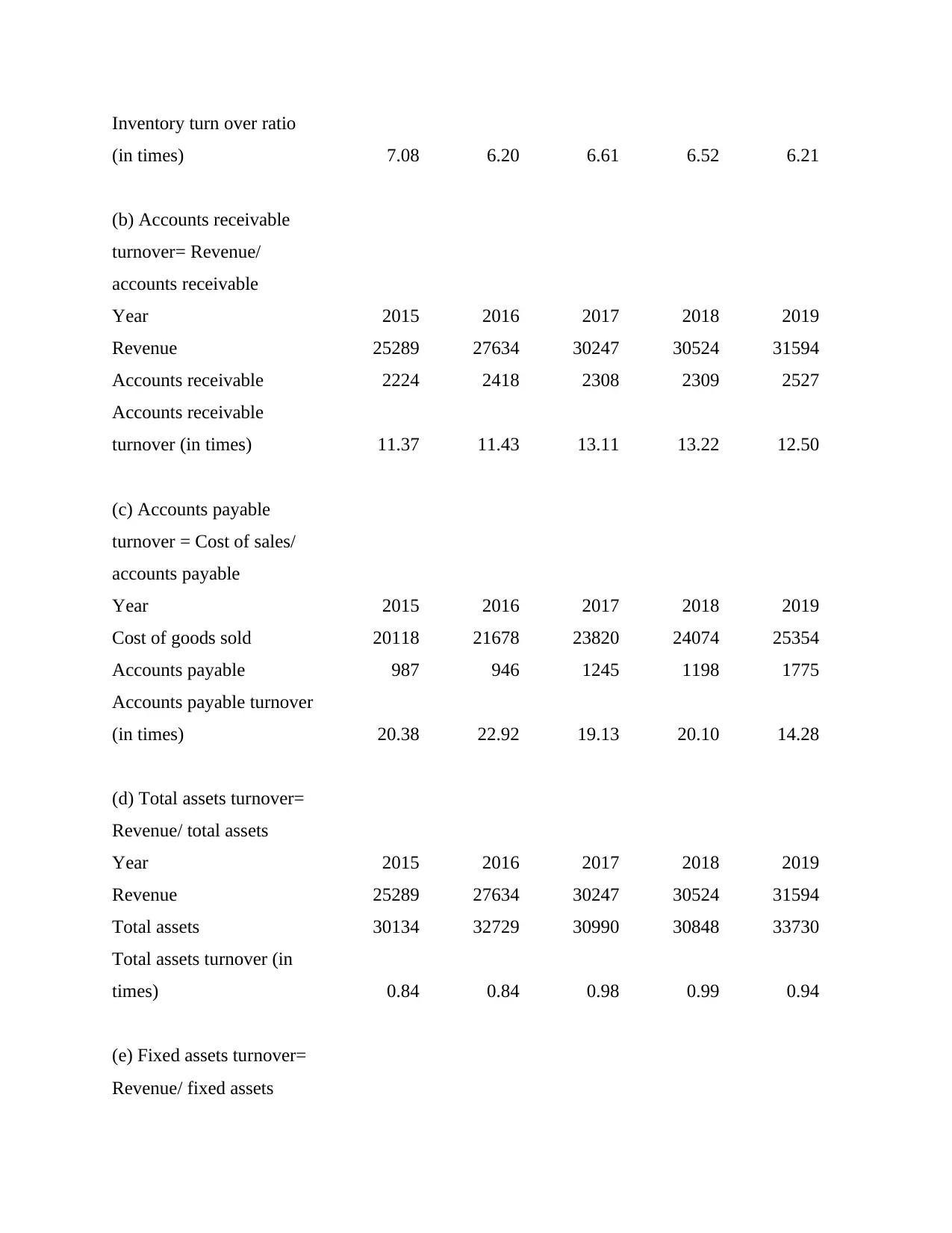

Inventory turn over ratio

(in times) 7.08 6.20 6.61 6.52 6.21

(b) Accounts receivable

turnover= Revenue/

accounts receivable

Year 2015 2016 2017 2018 2019

Revenue 25289 27634 30247 30524 31594

Accounts receivable 2224 2418 2308 2309 2527

Accounts receivable

turnover (in times) 11.37 11.43 13.11 13.22 12.50

(c) Accounts payable

turnover = Cost of sales/

accounts payable

Year 2015 2016 2017 2018 2019

Cost of goods sold 20118 21678 23820 24074 25354

Accounts payable 987 946 1245 1198 1775

Accounts payable turnover

(in times) 20.38 22.92 19.13 20.10 14.28

(d) Total assets turnover=

Revenue/ total assets

Year 2015 2016 2017 2018 2019

Revenue 25289 27634 30247 30524 31594

Total assets 30134 32729 30990 30848 33730

Total assets turnover (in

times) 0.84 0.84 0.98 0.99 0.94

(e) Fixed assets turnover=

Revenue/ fixed assets

(in times) 7.08 6.20 6.61 6.52 6.21

(b) Accounts receivable

turnover= Revenue/

accounts receivable

Year 2015 2016 2017 2018 2019

Revenue 25289 27634 30247 30524 31594

Accounts receivable 2224 2418 2308 2309 2527

Accounts receivable

turnover (in times) 11.37 11.43 13.11 13.22 12.50

(c) Accounts payable

turnover = Cost of sales/

accounts payable

Year 2015 2016 2017 2018 2019

Cost of goods sold 20118 21678 23820 24074 25354

Accounts payable 987 946 1245 1198 1775

Accounts payable turnover

(in times) 20.38 22.92 19.13 20.10 14.28

(d) Total assets turnover=

Revenue/ total assets

Year 2015 2016 2017 2018 2019

Revenue 25289 27634 30247 30524 31594

Total assets 30134 32729 30990 30848 33730

Total assets turnover (in

times) 0.84 0.84 0.98 0.99 0.94

(e) Fixed assets turnover=

Revenue/ fixed assets

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Year 2015 2016 2017 2018 2019

Revenue 25289 27634 30247 30524 31594

Fixed assets 22666 25195 24094 23595 22642

Fixed assets turnover (in

times) 1.12 1.10 1.26 1.29 1.40

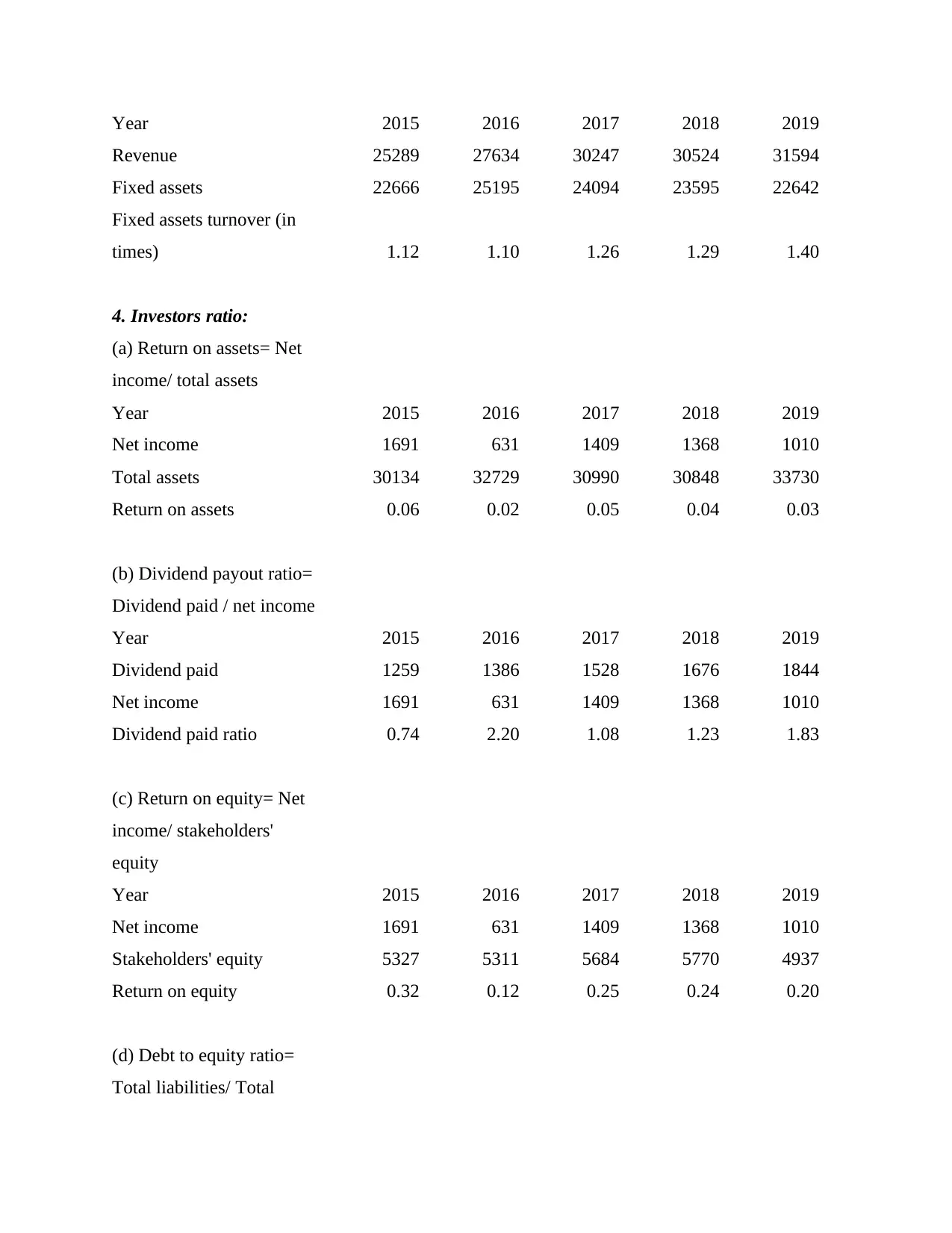

4. Investors ratio:

(a) Return on assets= Net

income/ total assets

Year 2015 2016 2017 2018 2019

Net income 1691 631 1409 1368 1010

Total assets 30134 32729 30990 30848 33730

Return on assets 0.06 0.02 0.05 0.04 0.03

(b) Dividend payout ratio=

Dividend paid / net income

Year 2015 2016 2017 2018 2019

Dividend paid 1259 1386 1528 1676 1844

Net income 1691 631 1409 1368 1010

Dividend paid ratio 0.74 2.20 1.08 1.23 1.83

(c) Return on equity= Net

income/ stakeholders'

equity

Year 2015 2016 2017 2018 2019

Net income 1691 631 1409 1368 1010

Stakeholders' equity 5327 5311 5684 5770 4937

Return on equity 0.32 0.12 0.25 0.24 0.20

(d) Debt to equity ratio=

Total liabilities/ Total

Revenue 25289 27634 30247 30524 31594

Fixed assets 22666 25195 24094 23595 22642

Fixed assets turnover (in

times) 1.12 1.10 1.26 1.29 1.40

4. Investors ratio:

(a) Return on assets= Net

income/ total assets

Year 2015 2016 2017 2018 2019

Net income 1691 631 1409 1368 1010

Total assets 30134 32729 30990 30848 33730

Return on assets 0.06 0.02 0.05 0.04 0.03

(b) Dividend payout ratio=

Dividend paid / net income

Year 2015 2016 2017 2018 2019

Dividend paid 1259 1386 1528 1676 1844

Net income 1691 631 1409 1368 1010

Dividend paid ratio 0.74 2.20 1.08 1.23 1.83

(c) Return on equity= Net

income/ stakeholders'

equity

Year 2015 2016 2017 2018 2019

Net income 1691 631 1409 1368 1010

Stakeholders' equity 5327 5311 5684 5770 4937

Return on equity 0.32 0.12 0.25 0.24 0.20

(d) Debt to equity ratio=

Total liabilities/ Total

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

stakeholders' equity

Year 2015 2016 2017 2018 2019

Total liabilities 24807 27418 25306 25078 28793

Stakeholders' equity 5327 5311 5684 5770 4937

Debt to equity ratio 4.66 5.16 4.45 4.35 5.83

5. Gearing ratio:

Gearing ratio = EBIT/

Interest expenses

Year 2015 2016 2017 2018 2019

EBIT 2356 2536 2669 2713 2492

Interest expenses 630 693 681 639 613

Gearing ratio 3.74 3.66 3.92 4.25 4.07

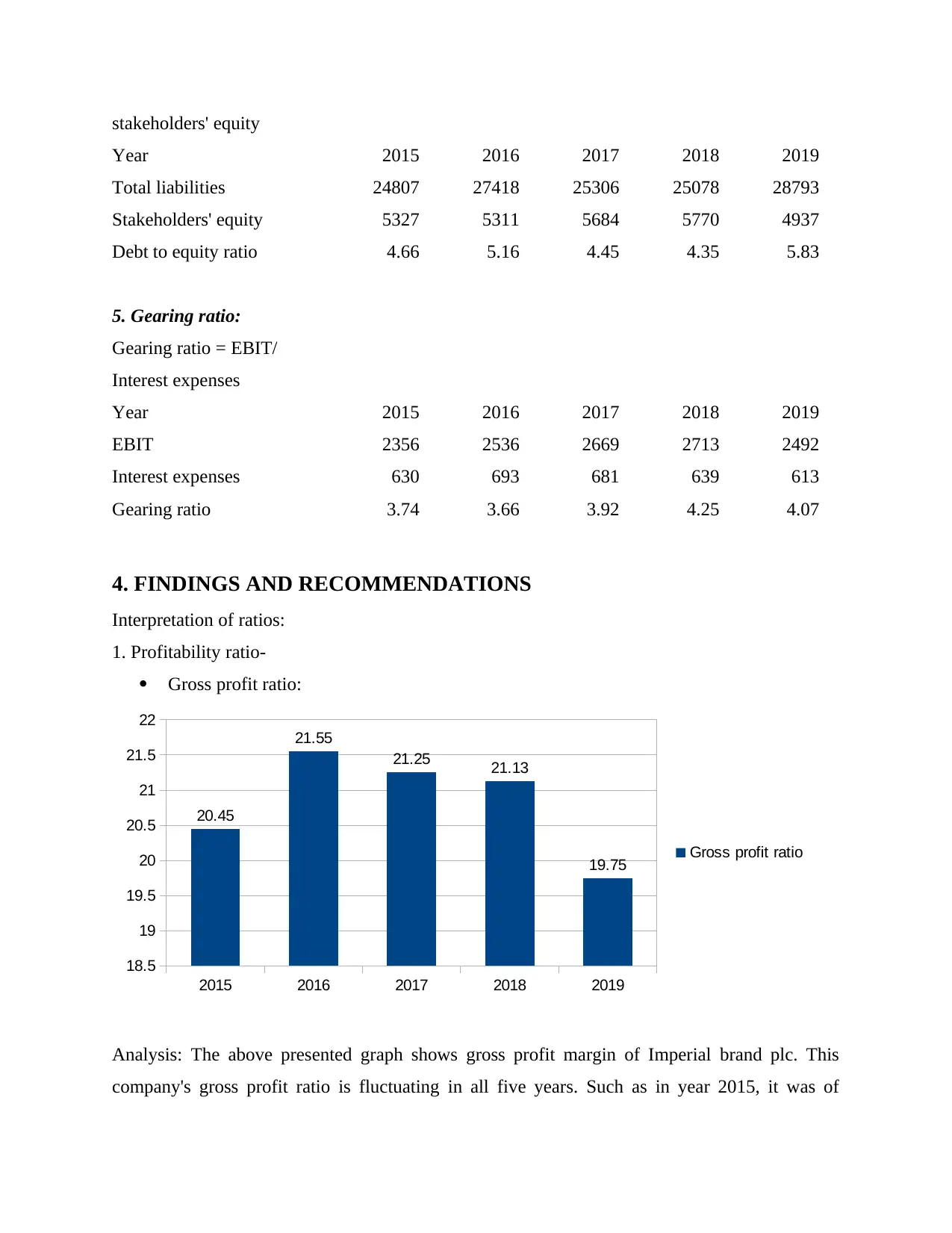

4. FINDINGS AND RECOMMENDATIONS

Interpretation of ratios:

1. Profitability ratio-

Gross profit ratio:

2015 2016 2017 2018 2019

18.5

19

19.5

20

20.5

21

21.5

22

20.45

21.55

21.25 21.13

19.75 Gross profit ratio

Analysis: The above presented graph shows gross profit margin of Imperial brand plc. This

company's gross profit ratio is fluctuating in all five years. Such as in year 2015, it was of

Year 2015 2016 2017 2018 2019

Total liabilities 24807 27418 25306 25078 28793

Stakeholders' equity 5327 5311 5684 5770 4937

Debt to equity ratio 4.66 5.16 4.45 4.35 5.83

5. Gearing ratio:

Gearing ratio = EBIT/

Interest expenses

Year 2015 2016 2017 2018 2019

EBIT 2356 2536 2669 2713 2492

Interest expenses 630 693 681 639 613

Gearing ratio 3.74 3.66 3.92 4.25 4.07

4. FINDINGS AND RECOMMENDATIONS

Interpretation of ratios:

1. Profitability ratio-

Gross profit ratio:

2015 2016 2017 2018 2019

18.5

19

19.5

20

20.5

21

21.5

22

20.45

21.55

21.25 21.13

19.75 Gross profit ratio

Analysis: The above presented graph shows gross profit margin of Imperial brand plc. This

company's gross profit ratio is fluctuating in all five years. Such as in year 2015, it was of

20.45% that raised in next year 2016 till 21.55%. On the other hand, in year 2017, it decreased

and became of 21.25% and in year 2019, this was of 19.75% (About financial data of Imperial

brand plc, 2019).

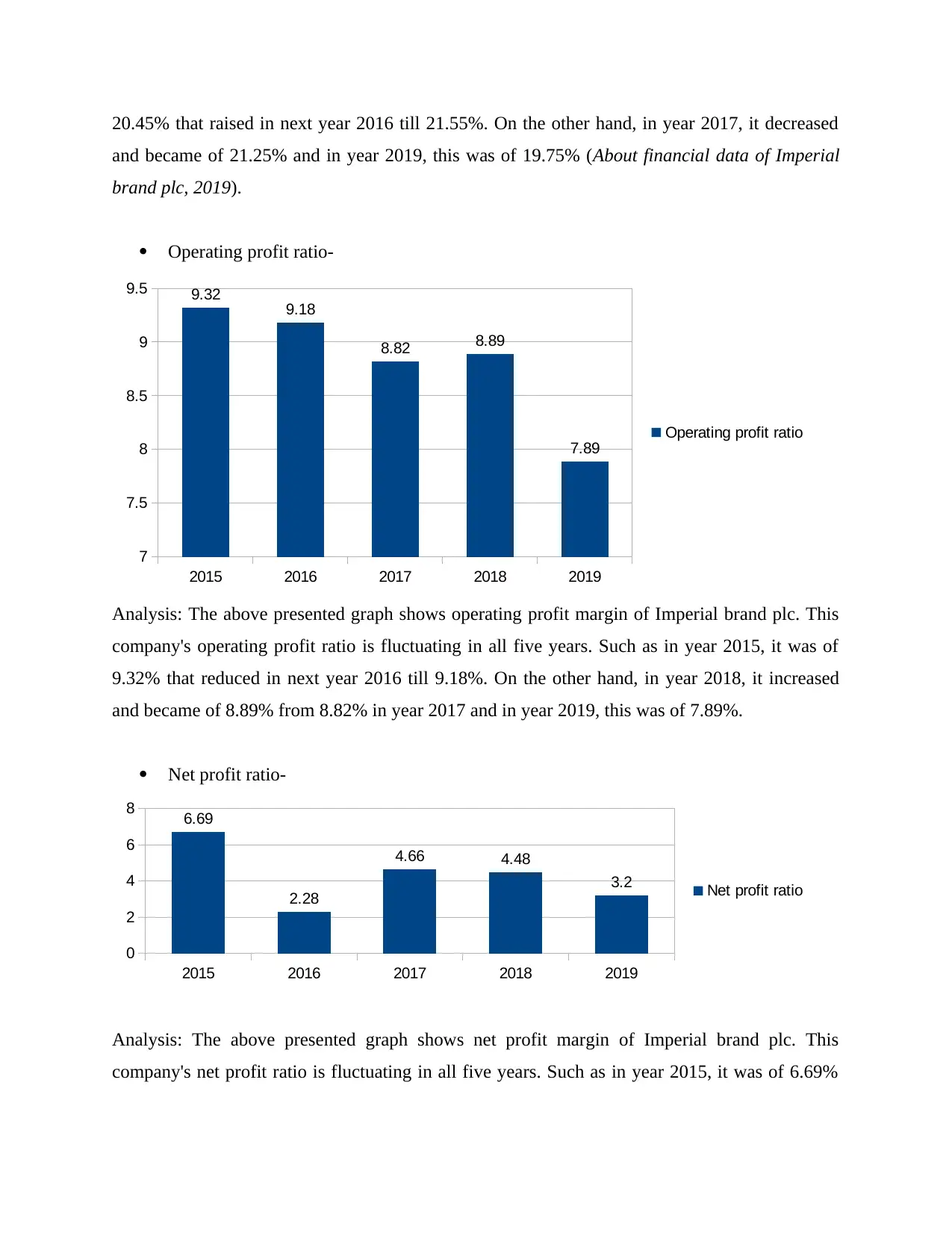

Operating profit ratio-

2015 2016 2017 2018 2019

7

7.5

8

8.5

9

9.5 9.32 9.18

8.82 8.89

7.89

Operating profit ratio

Analysis: The above presented graph shows operating profit margin of Imperial brand plc. This

company's operating profit ratio is fluctuating in all five years. Such as in year 2015, it was of

9.32% that reduced in next year 2016 till 9.18%. On the other hand, in year 2018, it increased

and became of 8.89% from 8.82% in year 2017 and in year 2019, this was of 7.89%.

Net profit ratio-

2015 2016 2017 2018 2019

0

2

4

6

8 6.69

2.28

4.66 4.48

3.2 Net profit ratio

Analysis: The above presented graph shows net profit margin of Imperial brand plc. This

company's net profit ratio is fluctuating in all five years. Such as in year 2015, it was of 6.69%

and became of 21.25% and in year 2019, this was of 19.75% (About financial data of Imperial

brand plc, 2019).

Operating profit ratio-

2015 2016 2017 2018 2019

7

7.5

8

8.5

9

9.5 9.32 9.18

8.82 8.89

7.89

Operating profit ratio

Analysis: The above presented graph shows operating profit margin of Imperial brand plc. This

company's operating profit ratio is fluctuating in all five years. Such as in year 2015, it was of

9.32% that reduced in next year 2016 till 9.18%. On the other hand, in year 2018, it increased

and became of 8.89% from 8.82% in year 2017 and in year 2019, this was of 7.89%.

Net profit ratio-

2015 2016 2017 2018 2019

0

2

4

6

8 6.69

2.28

4.66 4.48

3.2 Net profit ratio

Analysis: The above presented graph shows net profit margin of Imperial brand plc. This

company's net profit ratio is fluctuating in all five years. Such as in year 2015, it was of 6.69%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.