Management Accounting Report: MA Principles and Imperial Brands

VerifiedAdded on 2023/01/19

|19

|5230

|38

Report

AI Summary

This report provides a comprehensive overview of management accounting (MA) and its application within the context of Imperial Brands, a UK-based tobacco company. It begins with an introduction to MA, defining its role in analyzing and collecting financial and non-financial information for internal reporting. The report then delves into the core of MA, examining its role in planning, controlling, and decision-making within organizations. Task 1 explores the types of Management Accounting Systems (MAS), including inventory management, price optimization, and cost accounting systems, along with a comparison of MA and financial accounting. The report also details various MA reports, such as accounts receivable aging reports, cost accounting reports, performance reports, and stock reports, highlighting their benefits. Task 2 focuses on the preparation of income statements using absorption and marginal costing methods, and cost volume profit analysis. The report further investigates the integration of MAS and MA reports with organizational processes, demonstrating how these systems and reports align with departmental functions within Imperial Brands. The conclusion summarizes the key findings and emphasizes the importance of MA in providing valuable insights for effective business management and financial decision-making. References and an appendix with additional data are included to support the analysis.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

TASK 1............................................................................................................................................3

TASK 2............................................................................................................................................7

TASK 3..........................................................................................................................................10

TASK 4..........................................................................................................................................12

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

APPENDIX....................................................................................................................................17

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

TASK 1............................................................................................................................................3

TASK 2............................................................................................................................................7

TASK 3..........................................................................................................................................10

TASK 4..........................................................................................................................................12

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

APPENDIX....................................................................................................................................17

INTRODUCTION

The term MA is an accounting process that is linked with a systematic way of analysing

and collecting information regards to monetary & non monetary aspects (Weygandt, Kimmel and

Kieso, 2015). The main purpose of this accounting is to produce internal reports by utilising

gathered information. The key aim of this project report is to describing information regards to

MA and its role in companies operations. The project report is based on a UK based company

that is “Imperial brands”. The company is involved in process of manufacturing of tobacco

products and its headquarter is at Bristol, United Kingdom. The project report covers about

different kind of MAS, MA reports as well as about vital range of planning tools. The further

part of project report includes about role of MA in order to sort out monetary issues of

companies.

MAIN BODY

TASK 1

Role of MA and types of MAS.

MA- As above stated, this can be defined as a kind of accounting system that is aligned with a

process of controlling companies qualitative and quantitative aspects by help of internal reports.

The purpose of applying this accounting system is to manage internal aspects of business

entities. Below some role of MA are mentioned that are as follows :

Beneficial in planning- The MA is useful for companies in order to make effective

planning of various kind of activities (Derchi, Burkert and Oyon, 2013). It becomes

possible because under this accounting estimation of futuristic income and expenditures

is done that helps in better planning. Like in above company, their manager makes

planning of their manufacturing activities by help of this accounting.

Beneficial in controlling- It is essential for companies to control their different kind of

activities specially to financial activities. It is so because in the absence of control over

financial activities, this may lead to many issues. In above Imperial brands company,

their managers control and allocate financial resources by help of this accounting.

Benefits in decision making- In addition, the MA is useful for companies in order to take

corrective actions and decisions so that higher growth can be achieved. Such as the

The term MA is an accounting process that is linked with a systematic way of analysing

and collecting information regards to monetary & non monetary aspects (Weygandt, Kimmel and

Kieso, 2015). The main purpose of this accounting is to produce internal reports by utilising

gathered information. The key aim of this project report is to describing information regards to

MA and its role in companies operations. The project report is based on a UK based company

that is “Imperial brands”. The company is involved in process of manufacturing of tobacco

products and its headquarter is at Bristol, United Kingdom. The project report covers about

different kind of MAS, MA reports as well as about vital range of planning tools. The further

part of project report includes about role of MA in order to sort out monetary issues of

companies.

MAIN BODY

TASK 1

Role of MA and types of MAS.

MA- As above stated, this can be defined as a kind of accounting system that is aligned with a

process of controlling companies qualitative and quantitative aspects by help of internal reports.

The purpose of applying this accounting system is to manage internal aspects of business

entities. Below some role of MA are mentioned that are as follows :

Beneficial in planning- The MA is useful for companies in order to make effective

planning of various kind of activities (Derchi, Burkert and Oyon, 2013). It becomes

possible because under this accounting estimation of futuristic income and expenditures

is done that helps in better planning. Like in above company, their manager makes

planning of their manufacturing activities by help of this accounting.

Beneficial in controlling- It is essential for companies to control their different kind of

activities specially to financial activities. It is so because in the absence of control over

financial activities, this may lead to many issues. In above Imperial brands company,

their managers control and allocate financial resources by help of this accounting.

Benefits in decision making- In addition, the MA is useful for companies in order to take

corrective actions and decisions so that higher growth can be achieved. Such as the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

manager of above Imperial brands company, takes suitable decisions by help of this

accounting regards to monetary and non monetary aspects.

Comparison of MA and financial accounting :

Basis MA Financial accounting

Covered aspects Under this accounting both financial

and non financial aspects are focused.

While under this accounting only

financial aspects are covered.

Time period of

preparation of

reports

In this accounting, the reports are

prepared as accordance of need of

business entities. There is no specific

time to produce these reports.

On the other hand, in this accounting

the financial reports are prepared as

per the set rules and regulations bye

IFRS.

Compulsory Implementation of this accounting is

not necessary for companies.

While, this is essential for companies

to apply this accounting in order to

manage financial transactions.

Types of MAS :

Inventory management system – It can be defined as a type of accounting system that is

linked with systematic process of focusing of those activities which are linked with

buying and selling of stock (Trucco, 2015). This accounting system is based on the

valuation of inventories by help of different kind of techniques such as LIFO (last in first

out), FIFO (first in first out) and many more. This is essential for manufacturing entities

in order to manage cost of various kind of activities such as ordering cost, carrying cost

and many more. Under LIFO method, goods that are bring in last are used first for

production. While under FIFO method, good that bought first are utilised first for

manufacturing. In the above Imperial brands company, their production department

manages qualitative aspects of material.

Price optimisation system- This is a type of accounting system in which different types of

systematic activities are done in order to set prices of products and services. In broad

manner, under this accounting companies focus on gathering information of customers

perception on different price levels and their consideration about companies products. On

accounting regards to monetary and non monetary aspects.

Comparison of MA and financial accounting :

Basis MA Financial accounting

Covered aspects Under this accounting both financial

and non financial aspects are focused.

While under this accounting only

financial aspects are covered.

Time period of

preparation of

reports

In this accounting, the reports are

prepared as accordance of need of

business entities. There is no specific

time to produce these reports.

On the other hand, in this accounting

the financial reports are prepared as

per the set rules and regulations bye

IFRS.

Compulsory Implementation of this accounting is

not necessary for companies.

While, this is essential for companies

to apply this accounting in order to

manage financial transactions.

Types of MAS :

Inventory management system – It can be defined as a type of accounting system that is

linked with systematic process of focusing of those activities which are linked with

buying and selling of stock (Trucco, 2015). This accounting system is based on the

valuation of inventories by help of different kind of techniques such as LIFO (last in first

out), FIFO (first in first out) and many more. This is essential for manufacturing entities

in order to manage cost of various kind of activities such as ordering cost, carrying cost

and many more. Under LIFO method, goods that are bring in last are used first for

production. While under FIFO method, good that bought first are utilised first for

manufacturing. In the above Imperial brands company, their production department

manages qualitative aspects of material.

Price optimisation system- This is a type of accounting system in which different types of

systematic activities are done in order to set prices of products and services. In broad

manner, under this accounting companies focus on gathering information of customers

perception on different price levels and their consideration about companies products. On

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the basis of this information, the sales department of business entities set the prices of

their manufactured products. It is required by companies in order to revise and set the

prices of various kind of products in an effective manner. In this accounting, different

kind of pricing strategies are being used such as price skimming, penetration strategy and

many more. Under the price skimming strategy, the price of products and services are

kept higher by business entities to get higher amount of market share. In the penetration

strategy, prices of products and services are kept lower to establish in new market. In

above Imperial brands company, their sales department is using this accounting in order

to revise the prices of their tobacco products.

Cost accounting system- It can be defined as a kind of accounting system under which

different kind of expenditures of all activities and operations are controlled in an effective

manner (Fiondella, Maffei and Spanò, 2016). This accounting system is essentially

required by companies in order to control overall expenditures of various kind of

operations. The purpose of this accounting system is to focusing on those aspects that are

causing as higher cost of operations. In this accounting mainly two types of costs are

managed that are :

* Job costing- It is a kind of cost that occurs in order to assigning a particular individual in

process of completing any task or activity. By help of cost accounting system, the managers of

companies keep an effective control over job cost of various kind of tasks.

* Process costing- This is a type of cost that is calculated by companies in order to compute cost

of each process. Such as in above Imperial brands company, the cost of each process of

manufacturing activities is calculated by help of cost accounting system.

MA reports:

The management accounting reports can be defined as a kind of reports that are being

prepared by companies in order to make control over financial and non financial activities. There

are different types of MA reports and some of them are produced by Imperial brands company:

Account receivable ageing report- Under this report information regards to different kind

of debtors and their debt amount is included (Kastberg and Siverbo, 2013). The purpose

of preparing this report is to helping finance department of companies in order to provide

information regards to total due amount by their debtors. This report is beneficial for

their manufactured products. It is required by companies in order to revise and set the

prices of various kind of products in an effective manner. In this accounting, different

kind of pricing strategies are being used such as price skimming, penetration strategy and

many more. Under the price skimming strategy, the price of products and services are

kept higher by business entities to get higher amount of market share. In the penetration

strategy, prices of products and services are kept lower to establish in new market. In

above Imperial brands company, their sales department is using this accounting in order

to revise the prices of their tobacco products.

Cost accounting system- It can be defined as a kind of accounting system under which

different kind of expenditures of all activities and operations are controlled in an effective

manner (Fiondella, Maffei and Spanò, 2016). This accounting system is essentially

required by companies in order to control overall expenditures of various kind of

operations. The purpose of this accounting system is to focusing on those aspects that are

causing as higher cost of operations. In this accounting mainly two types of costs are

managed that are :

* Job costing- It is a kind of cost that occurs in order to assigning a particular individual in

process of completing any task or activity. By help of cost accounting system, the managers of

companies keep an effective control over job cost of various kind of tasks.

* Process costing- This is a type of cost that is calculated by companies in order to compute cost

of each process. Such as in above Imperial brands company, the cost of each process of

manufacturing activities is calculated by help of cost accounting system.

MA reports:

The management accounting reports can be defined as a kind of reports that are being

prepared by companies in order to make control over financial and non financial activities. There

are different types of MA reports and some of them are produced by Imperial brands company:

Account receivable ageing report- Under this report information regards to different kind

of debtors and their debt amount is included (Kastberg and Siverbo, 2013). The purpose

of preparing this report is to helping finance department of companies in order to provide

information regards to total due amount by their debtors. This report is beneficial for

business entities in order to make planning regards to financial resources. It is so because

on the basis of this managers get information about how much amount of fund is needed

to be collect. Such as in above Imperial brands company, their finance manager utilise

key information through this report and make strategy in order to collect debt amount.

Cost accounting report- This report is prepared by utilisation of key information through

cost accounting system. Under this report information regards to each and every activity

is included. By help of this information companies make prediction of futuristic

expenditures and make plan accordingly. This report helps to companies' managers in

providing complete information regards to total expected and actual expenditures. On the

basis of it, finance managers take corrective steps to control total cost of operations. The

manager of above Imperial brands company gather crucial financial information by help

of this report regards to each elements' cost. This benefits them in controlling cost of

different kind of activities and operations regards to production of tobacco products.

Performance report- It can be defined as a kind of report in which information about

actual outcome and estimated outcome is presented along with variation between these

two. By help of this report, managers can focus on those growth and promotion of each

employee separately. As well as this report beneficial to employees to get reward on the

basis of their skills and acts which they perform for a particular business entity. In the

aspect of above Imperial brands company, their managers take decision about promotion

of their staff members as accordance of information derived through this report.

Stock report- Similar as to cost accounting report, this report is being prepared by

integration of inventory management system. The report consists information about how

much quantity of material is being stored in warehouses as well as how much quantity is

used in the aspect of production (Hirsch, Nitzl and Schauß, 2015). On the basis of it,

production department of business entities inform to managers about how much quantity

of raw material is needed by them in order to complete target production. Basically, this

report is prepared as accordance of valuation method of inventory. Such as in the LIFO

method, inventory report is prepared that consists information regards to stock that comes

in last and used first for production. As well as the report that is prepared under FIFO

method, consists information about stock that comes first and used on priority basis for

production. Like in the aspect of above Imperial brands, their production department

on the basis of this managers get information about how much amount of fund is needed

to be collect. Such as in above Imperial brands company, their finance manager utilise

key information through this report and make strategy in order to collect debt amount.

Cost accounting report- This report is prepared by utilisation of key information through

cost accounting system. Under this report information regards to each and every activity

is included. By help of this information companies make prediction of futuristic

expenditures and make plan accordingly. This report helps to companies' managers in

providing complete information regards to total expected and actual expenditures. On the

basis of it, finance managers take corrective steps to control total cost of operations. The

manager of above Imperial brands company gather crucial financial information by help

of this report regards to each elements' cost. This benefits them in controlling cost of

different kind of activities and operations regards to production of tobacco products.

Performance report- It can be defined as a kind of report in which information about

actual outcome and estimated outcome is presented along with variation between these

two. By help of this report, managers can focus on those growth and promotion of each

employee separately. As well as this report beneficial to employees to get reward on the

basis of their skills and acts which they perform for a particular business entity. In the

aspect of above Imperial brands company, their managers take decision about promotion

of their staff members as accordance of information derived through this report.

Stock report- Similar as to cost accounting report, this report is being prepared by

integration of inventory management system. The report consists information about how

much quantity of material is being stored in warehouses as well as how much quantity is

used in the aspect of production (Hirsch, Nitzl and Schauß, 2015). On the basis of it,

production department of business entities inform to managers about how much quantity

of raw material is needed by them in order to complete target production. Basically, this

report is prepared as accordance of valuation method of inventory. Such as in the LIFO

method, inventory report is prepared that consists information regards to stock that comes

in last and used first for production. As well as the report that is prepared under FIFO

method, consists information about stock that comes first and used on priority basis for

production. Like in the aspect of above Imperial brands, their production department

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

gather key information by help of this report in order to take decision regards to

purchasing of new material. The information which is derived in this report is gathered

by help of various kind stock valuation methods such as LIFO, FIFO and many more. In

addition the chosen company is involved in manufacturing process of tobacco products

hence, this is essential for them to keep an extra sight of eye over stock purchasing and

consumptions.

Thus, these are the main accounting reports that are being prepared by above Imperial brands

company.

Benefit of MAS :

Name of MAS Benefits

Inventory management

system

As above stated, this accounting system is linked with process of

controlling quantity and cost of different kind of materials that are

used by companies. In the Imperial brands company, the are getting

benefit from this accounting system in order to make the

production process of tobacco cost effectively.

Price optimisation system This accounting system is useful for business entities in order to

revise the pricing strategies as accordance of need of customers.

The Imperial brands company revise the prices of their tobacco

products as accordance of need and demand of their customers.

Cost accounting system Under this accounting system, overall expenditures of different

aspects are controlled in an effective manner. Such as in the

Imperial brands company, their finance department utilise key

information through this accounting system for keeping control

over cost.

Evaluation of integration of MAS and MA reports with organisational process.

Under MAS a vital range of accounting systems are included and each of them is aligned

with companies process and objectives. Like in the above chosen respective company Imperial

brands, their most of the departments are integrated with mentioned accounting systems. Such as

purchasing of new material. The information which is derived in this report is gathered

by help of various kind stock valuation methods such as LIFO, FIFO and many more. In

addition the chosen company is involved in manufacturing process of tobacco products

hence, this is essential for them to keep an extra sight of eye over stock purchasing and

consumptions.

Thus, these are the main accounting reports that are being prepared by above Imperial brands

company.

Benefit of MAS :

Name of MAS Benefits

Inventory management

system

As above stated, this accounting system is linked with process of

controlling quantity and cost of different kind of materials that are

used by companies. In the Imperial brands company, the are getting

benefit from this accounting system in order to make the

production process of tobacco cost effectively.

Price optimisation system This accounting system is useful for business entities in order to

revise the pricing strategies as accordance of need of customers.

The Imperial brands company revise the prices of their tobacco

products as accordance of need and demand of their customers.

Cost accounting system Under this accounting system, overall expenditures of different

aspects are controlled in an effective manner. Such as in the

Imperial brands company, their finance department utilise key

information through this accounting system for keeping control

over cost.

Evaluation of integration of MAS and MA reports with organisational process.

Under MAS a vital range of accounting systems are included and each of them is aligned

with companies process and objectives. Like in the above chosen respective company Imperial

brands, their most of the departments are integrated with mentioned accounting systems. Such as

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

cost accounting and price optimisation systems are linked with finance & sales department.

Similar as accounting systems, the MA reports are also aligned with different aspects of

companies. For example in above company, their reports like stock report, cost accounting report

are linked with above mentioned departments.

TASK 2

Preparation of income statement as per the absorption and marginal costing method.

There are different kind of techniques in order to produce income statements and some of

them are mentioned below :

Absorption costing – It can be defined as a kind of technique in that fixed and non fixed

costs are absorbed in order to preparation of income statements.

Marginal costing – In this costing technique, fixed costs are considered as period cost as

well as non fixed cost as cost of unit (Kalkhouran, Sofian and Nedaei, 2015).

Cost volume profit analysis – The term cost volume profit analysis can be defined as kind

of analysis technique in which impact of cost on operating profit is analysed in an

effective manner.

MA techniques in order to produce reports regards to chosen organisation.

Companies produce and publish income statements on regular time period by help of

different kind of techniques. The main objective of preparation of these reports to provide

information to internal and external stakeholders. In order to produce financial statements

different kind of techniques are used such as absorption costing, marginal costing and many

more. The above chosen company Imperial brand is preparing their income statements by help of

both absorption and marginal costing.

Except from above described techniques, there are some other methods too for

preparation of financial statements such as standard costing, activity based costing etc. Basically,

it is essential for business entities to produce financial reports by help of these techniques

because it provides an essential framework.

Similar as accounting systems, the MA reports are also aligned with different aspects of

companies. For example in above company, their reports like stock report, cost accounting report

are linked with above mentioned departments.

TASK 2

Preparation of income statement as per the absorption and marginal costing method.

There are different kind of techniques in order to produce income statements and some of

them are mentioned below :

Absorption costing – It can be defined as a kind of technique in that fixed and non fixed

costs are absorbed in order to preparation of income statements.

Marginal costing – In this costing technique, fixed costs are considered as period cost as

well as non fixed cost as cost of unit (Kalkhouran, Sofian and Nedaei, 2015).

Cost volume profit analysis – The term cost volume profit analysis can be defined as kind

of analysis technique in which impact of cost on operating profit is analysed in an

effective manner.

MA techniques in order to produce reports regards to chosen organisation.

Companies produce and publish income statements on regular time period by help of

different kind of techniques. The main objective of preparation of these reports to provide

information to internal and external stakeholders. In order to produce financial statements

different kind of techniques are used such as absorption costing, marginal costing and many

more. The above chosen company Imperial brand is preparing their income statements by help of

both absorption and marginal costing.

Except from above described techniques, there are some other methods too for

preparation of financial statements such as standard costing, activity based costing etc. Basically,

it is essential for business entities to produce financial reports by help of these techniques

because it provides an essential framework.

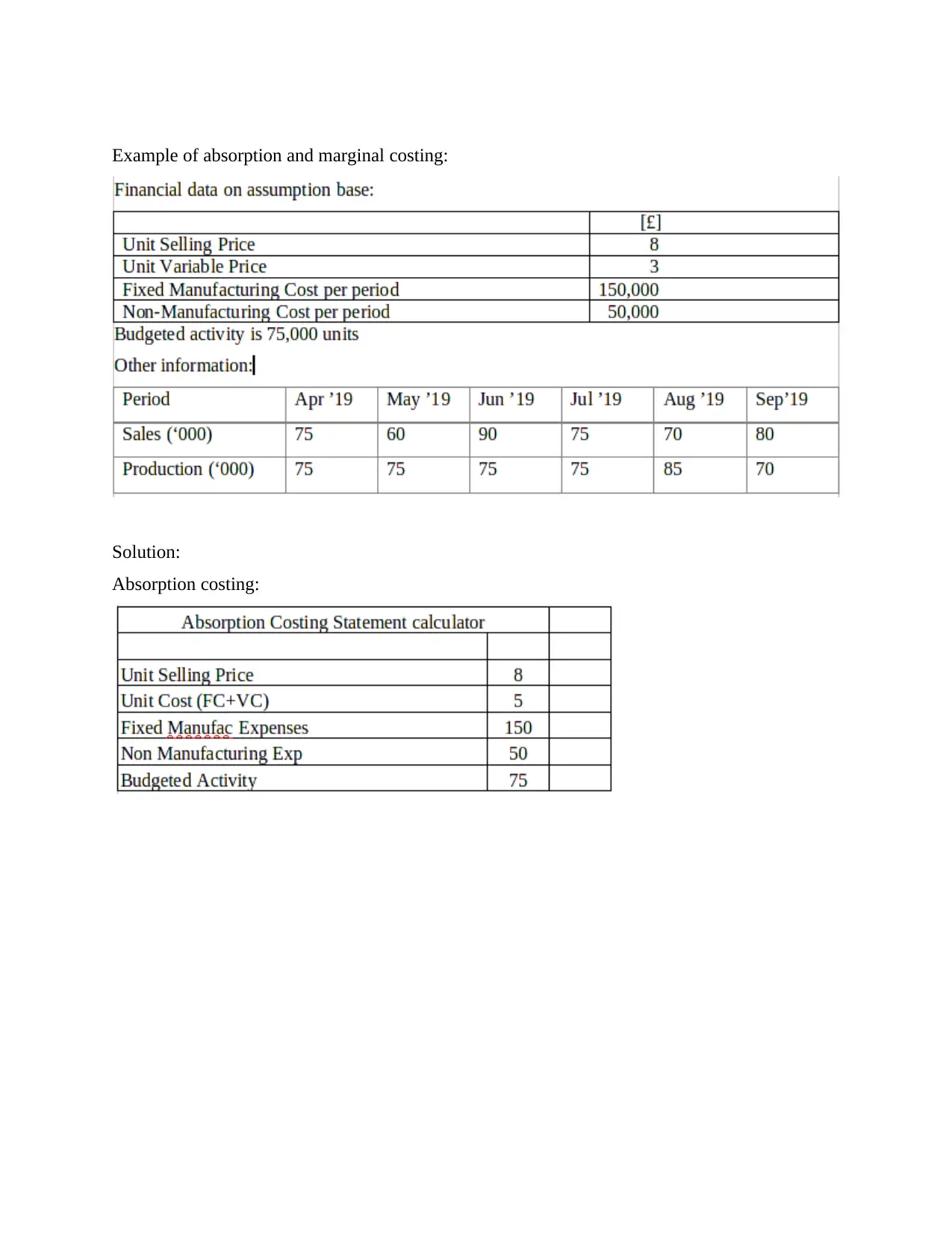

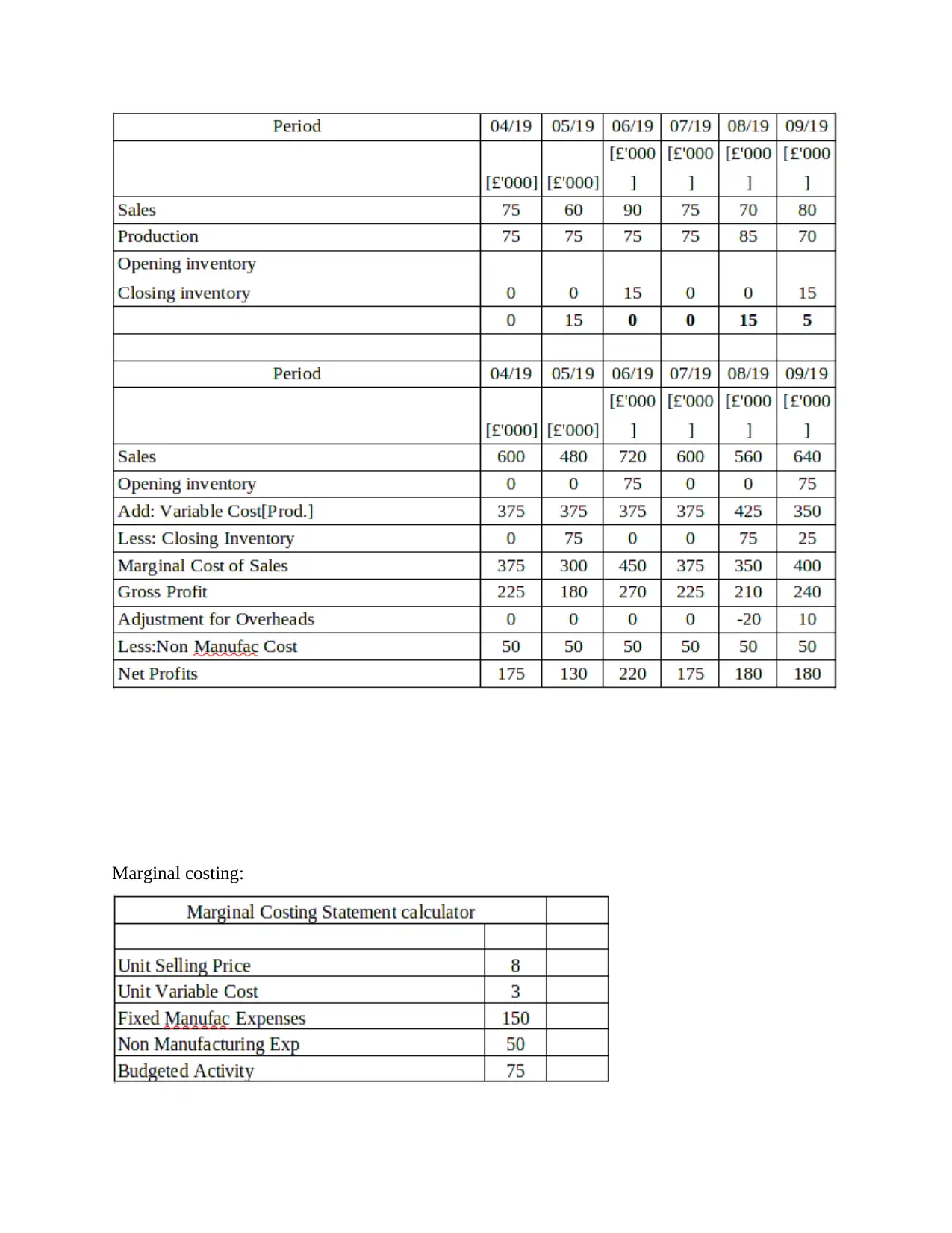

Example of absorption and marginal costing:

Solution:

Absorption costing:

Solution:

Absorption costing:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

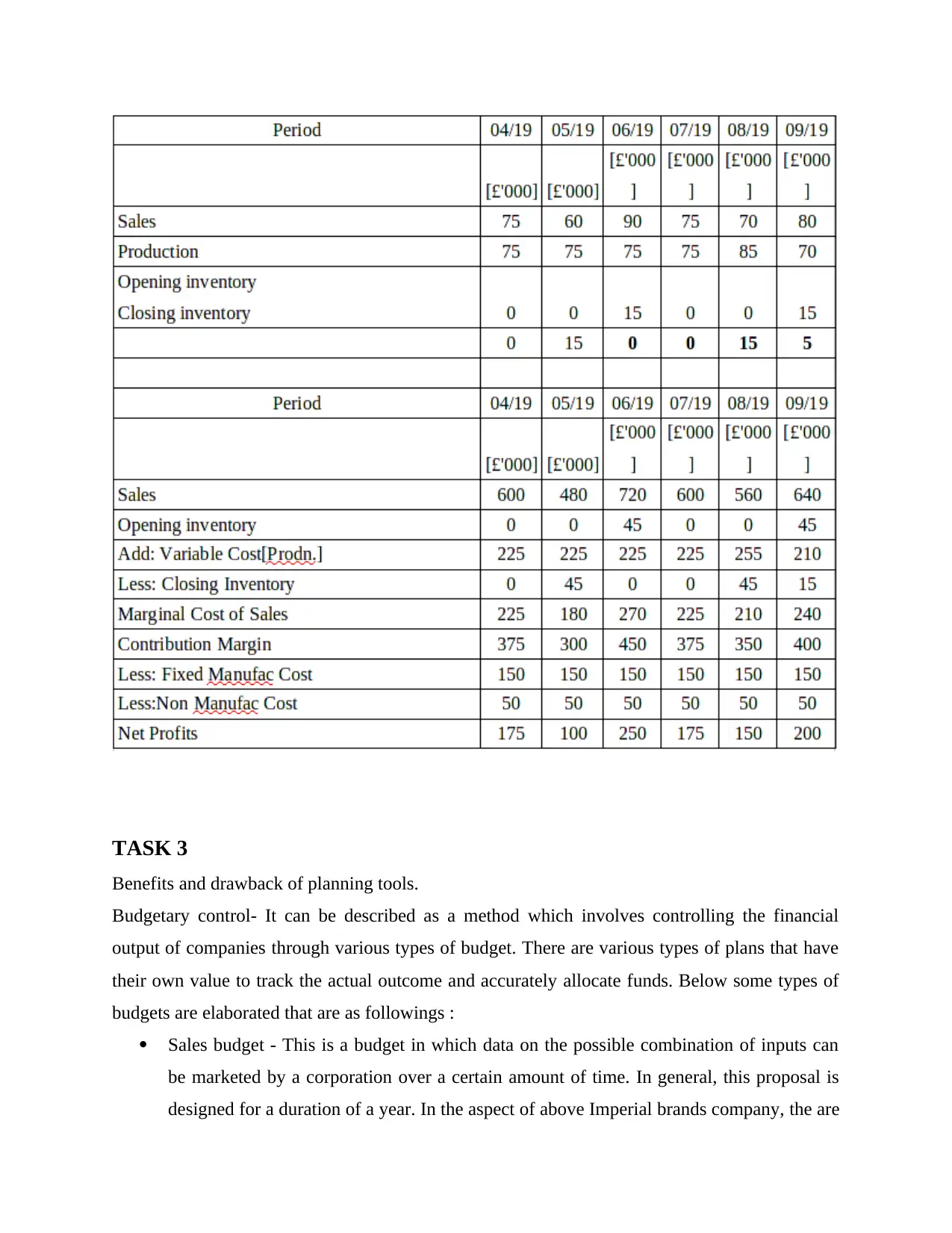

Marginal costing:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 3

Benefits and drawback of planning tools.

Budgetary control- It can be described as a method which involves controlling the financial

output of companies through various types of budget. There are various types of plans that have

their own value to track the actual outcome and accurately allocate funds. Below some types of

budgets are elaborated that are as followings :

Sales budget - This is a budget in which data on the possible combination of inputs can

be marketed by a corporation over a certain amount of time. In general, this proposal is

designed for a duration of a year. In the aspect of above Imperial brands company, the are

Benefits and drawback of planning tools.

Budgetary control- It can be described as a method which involves controlling the financial

output of companies through various types of budget. There are various types of plans that have

their own value to track the actual outcome and accurately allocate funds. Below some types of

budgets are elaborated that are as followings :

Sales budget - This is a budget in which data on the possible combination of inputs can

be marketed by a corporation over a certain amount of time. In general, this proposal is

designed for a duration of a year. In the aspect of above Imperial brands company, the are

preparation of this plan and provide their supervisors with data on the estimated number

of items to be marketed for a specific time period. Below its limitations and benefits are

described which are as followings :

Advantage - This budget is useful for meeting a specific time sector's sales target. It is because

the division of sales plans their tactics and strategies as visionary goals by help of this budget.

Along with companies can become able to beat their competitors in an effective manner if they

follow the activities of this budget.

Disadvantage - Preparing this budget takes too long time because it requires different activities

including editing, adjustment, budget review process. As well as it needs higher range of cost

which can not be affordable by small business entities.

Purchase budget – This can be defined as a kind of budget which is prepared by

companies in order to manage their activities regards to purchasing of different kind of

items. In this budget information about futuristic items that are needed to be buy in order

to manage the production process (Schaltegge and Zvezdov, 2015). The above company

is using this budget in order to control their manufacturing activity of tobacco products. It

has some advantages and disadvantages which are as follows :

Advantages – This budget is beneficial for companies in making financial plan about how much

will be needed in order to acquire raw materials. Unwanted expenditures can be managed easily

with the aid of this budget because the managers make purchasing decisions in accordance with

it.

Disadvantage – The main drawback of this budget, that it does not provide accurate estimation

that may lead to loss for companies. Along with, businesses are unable to relay the operations of

this program because their estimate does not always yield accurate results.

Zero based budget – This is a budgeting system where all expenditures of each new phase

must be explained. The zero-based budget process begins from a "zero basis," as well as

the requirements and expenses of each role in an entity are evaluated. It has some

advantages and disadvantages that are as :

of items to be marketed for a specific time period. Below its limitations and benefits are

described which are as followings :

Advantage - This budget is useful for meeting a specific time sector's sales target. It is because

the division of sales plans their tactics and strategies as visionary goals by help of this budget.

Along with companies can become able to beat their competitors in an effective manner if they

follow the activities of this budget.

Disadvantage - Preparing this budget takes too long time because it requires different activities

including editing, adjustment, budget review process. As well as it needs higher range of cost

which can not be affordable by small business entities.

Purchase budget – This can be defined as a kind of budget which is prepared by

companies in order to manage their activities regards to purchasing of different kind of

items. In this budget information about futuristic items that are needed to be buy in order

to manage the production process (Schaltegge and Zvezdov, 2015). The above company

is using this budget in order to control their manufacturing activity of tobacco products. It

has some advantages and disadvantages which are as follows :

Advantages – This budget is beneficial for companies in making financial plan about how much

will be needed in order to acquire raw materials. Unwanted expenditures can be managed easily

with the aid of this budget because the managers make purchasing decisions in accordance with

it.

Disadvantage – The main drawback of this budget, that it does not provide accurate estimation

that may lead to loss for companies. Along with, businesses are unable to relay the operations of

this program because their estimate does not always yield accurate results.

Zero based budget – This is a budgeting system where all expenditures of each new phase

must be explained. The zero-based budget process begins from a "zero basis," as well as

the requirements and expenses of each role in an entity are evaluated. It has some

advantages and disadvantages that are as :

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.