Implication of Taxation Rules and Regulations on Monash IVF Group Ltd

VerifiedAdded on 2020/05/16

|13

|2367

|69

Report

AI Summary

This report provides an in-depth analysis of the taxation rules and regulations impacting Monash IVF Group Ltd. It examines the company's financial statements, including common stock, contributed capital, accumulated profit, and retained earnings. The report evaluates the company's income tax expenses, deferred tax liabilities, and current tax assets, comparing tax expenses to tax payments. It investigates the differences between accounting and taxation rules, particularly regarding revenue, expenses, and depreciation. The analysis explores the impact of deferred tax liabilities and assets, and how they relate to future tax obligations. Furthermore, the report compares income tax expenses to income tax payable, and income tax expenses in the income statement to income tax paid in the cash flow statement. Finally, it discusses the treatment of tax recording in the company's books, highlighting the interesting and surprising aspects of tax recording, and the difficulties faced. The report refers to AASB-112 and annual reports, including cash flow statements, balance sheets, and income statements to support its findings.

RUNNING HEAD: Implication of taxation rules and regulations on Monash IVF Group Ltd

1

Name of the student-

Topic- Implication of taxation rules and regulations on Monash IVF Group Ltd

University name

1

Name of the student-

Topic- Implication of taxation rules and regulations on Monash IVF Group Ltd

University name

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Implication of taxation rules and regulations on Monash IVF Group Ltd

2

Table of Contents

Answer to question-1.............................................................................................................................3

Answer to question-2.............................................................................................................................5

Answer to question no-3........................................................................................................................5

Answer to question no-4........................................................................................................................7

Answer to question no-5........................................................................................................................8

Answer to question no-6........................................................................................................................9

Answer to question no-7........................................................................................................................9

References...........................................................................................................................................12

.

2

Table of Contents

Answer to question-1.............................................................................................................................3

Answer to question-2.............................................................................................................................5

Answer to question no-3........................................................................................................................5

Answer to question no-4........................................................................................................................7

Answer to question no-5........................................................................................................................8

Answer to question no-6........................................................................................................................9

Answer to question no-7........................................................................................................................9

References...........................................................................................................................................12

.

Implication of taxation rules and regulations on Monash IVF Group Ltd

3

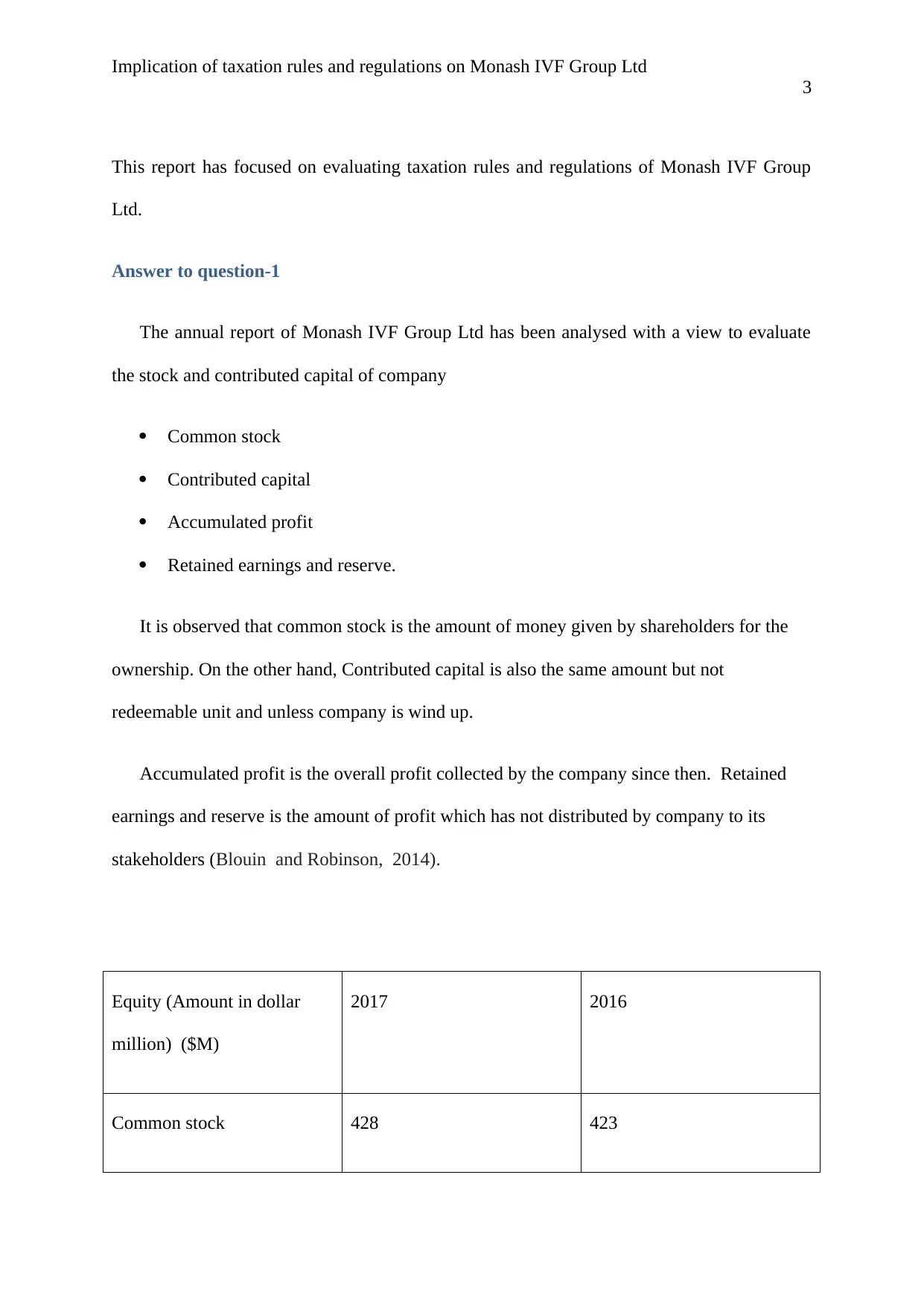

This report has focused on evaluating taxation rules and regulations of Monash IVF Group

Ltd.

Answer to question-1

The annual report of Monash IVF Group Ltd has been analysed with a view to evaluate

the stock and contributed capital of company

Common stock

Contributed capital

Accumulated profit

Retained earnings and reserve.

It is observed that common stock is the amount of money given by shareholders for the

ownership. On the other hand, Contributed capital is also the same amount but not

redeemable unit and unless company is wind up.

Accumulated profit is the overall profit collected by the company since then. Retained

earnings and reserve is the amount of profit which has not distributed by company to its

stakeholders (Blouin and Robinson, 2014).

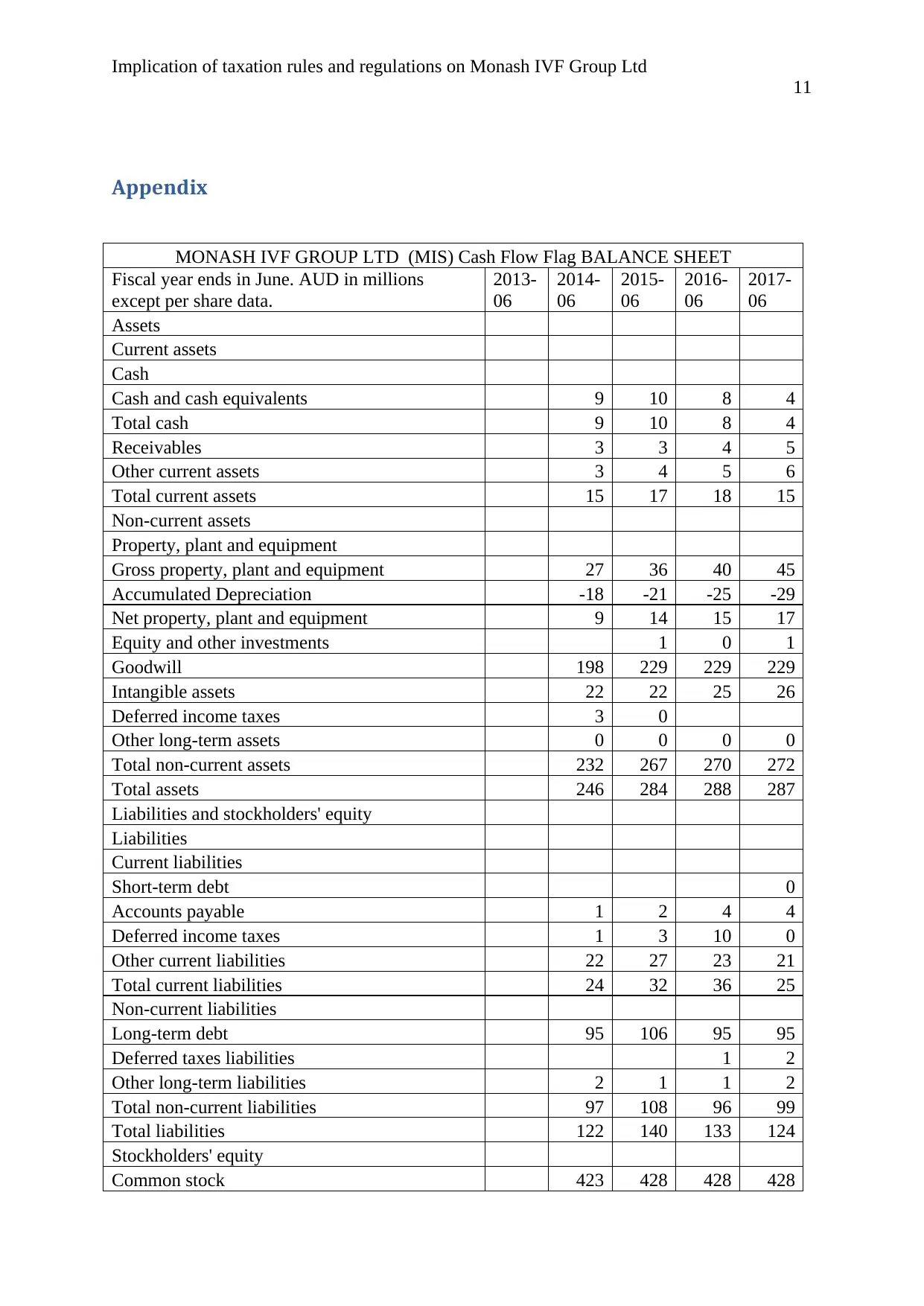

Equity (Amount in dollar

million) ($M)

2017 2016

Common stock 428 423

3

This report has focused on evaluating taxation rules and regulations of Monash IVF Group

Ltd.

Answer to question-1

The annual report of Monash IVF Group Ltd has been analysed with a view to evaluate

the stock and contributed capital of company

Common stock

Contributed capital

Accumulated profit

Retained earnings and reserve.

It is observed that common stock is the amount of money given by shareholders for the

ownership. On the other hand, Contributed capital is also the same amount but not

redeemable unit and unless company is wind up.

Accumulated profit is the overall profit collected by the company since then. Retained

earnings and reserve is the amount of profit which has not distributed by company to its

stakeholders (Blouin and Robinson, 2014).

Equity (Amount in dollar

million) ($M)

2017 2016

Common stock 428 423

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Implication of taxation rules and regulations on Monash IVF Group Ltd

4

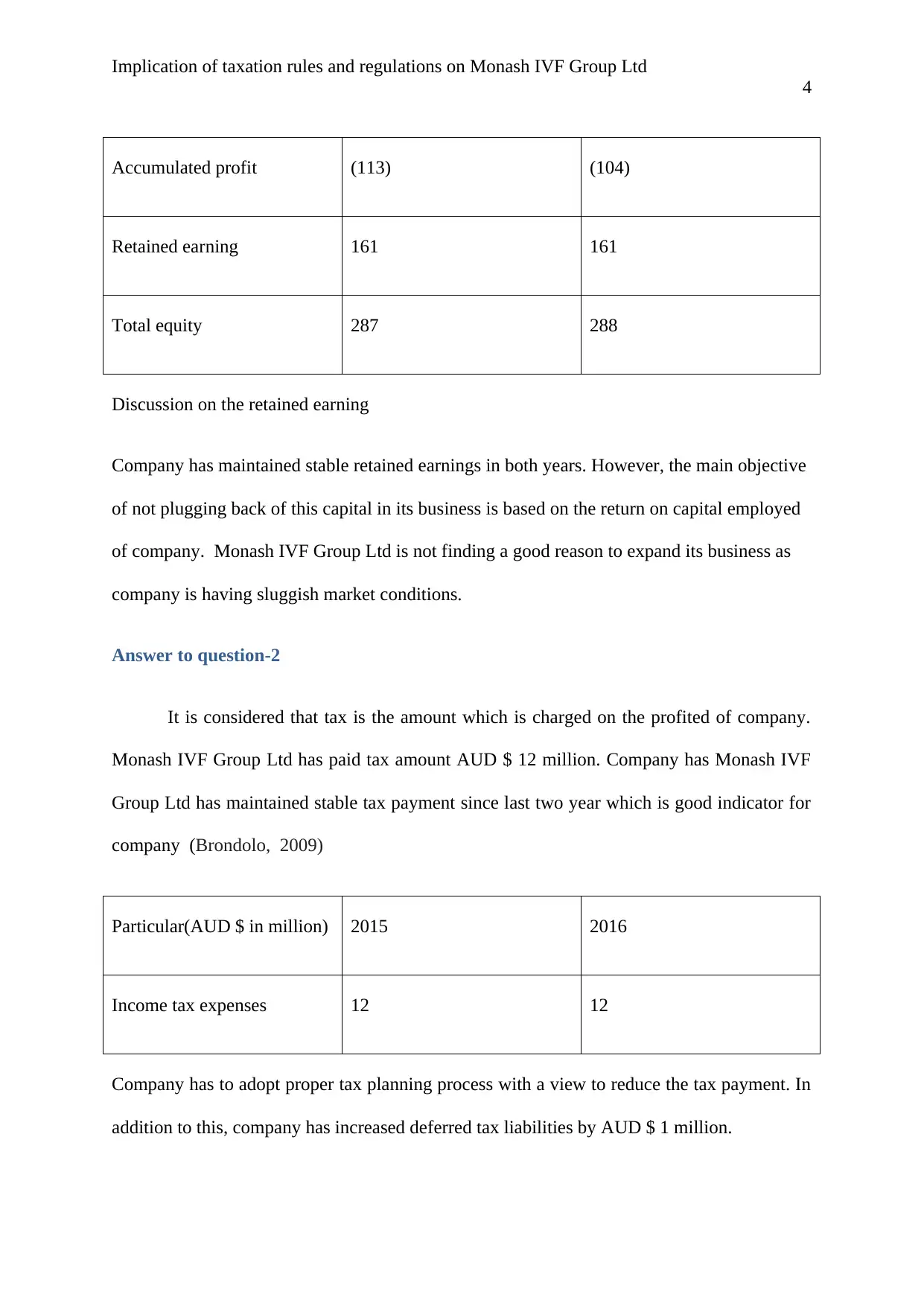

Accumulated profit (113) (104)

Retained earning 161 161

Total equity 287 288

Discussion on the retained earning

Company has maintained stable retained earnings in both years. However, the main objective

of not plugging back of this capital in its business is based on the return on capital employed

of company. Monash IVF Group Ltd is not finding a good reason to expand its business as

company is having sluggish market conditions.

Answer to question-2

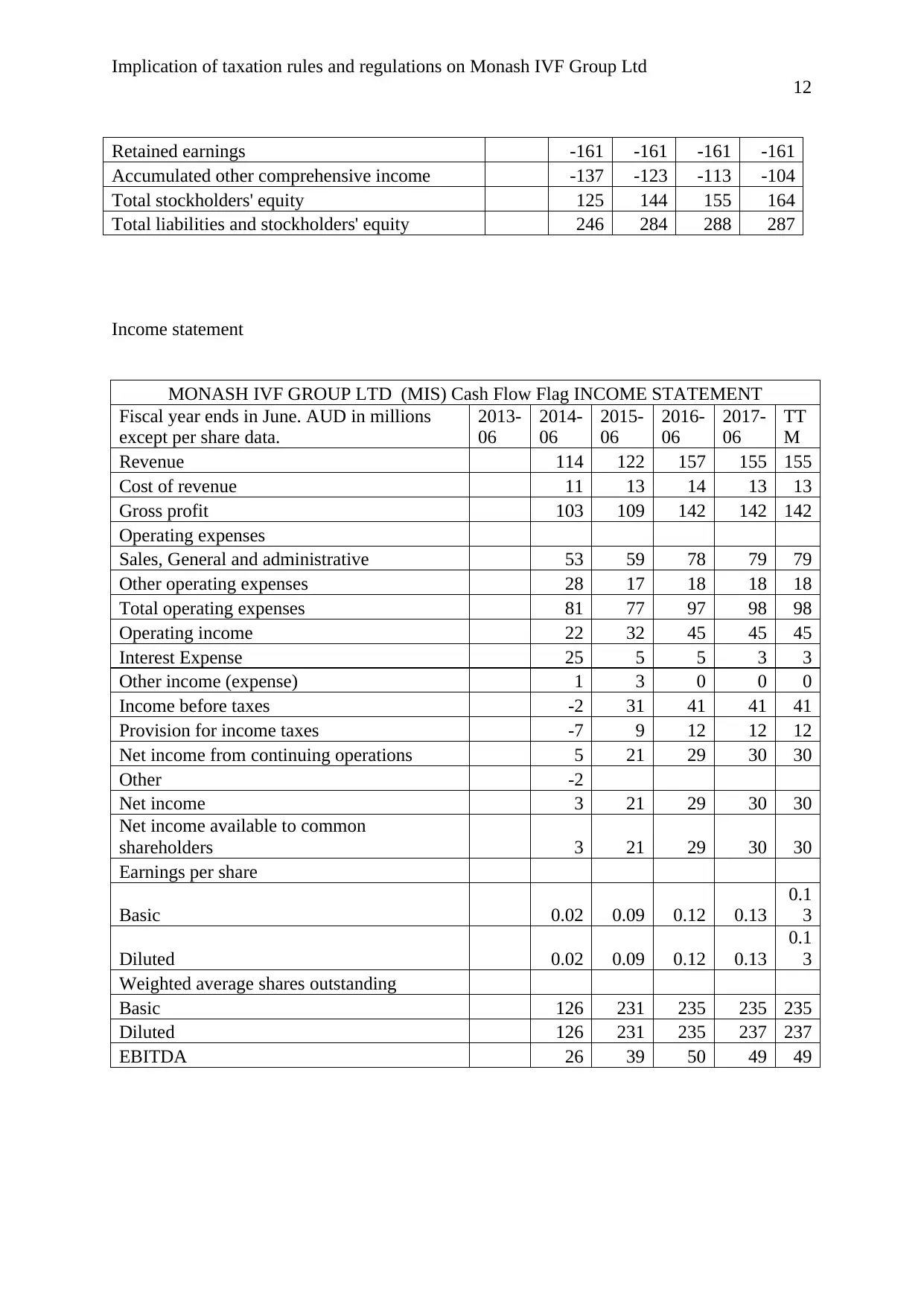

It is considered that tax is the amount which is charged on the profited of company.

Monash IVF Group Ltd has paid tax amount AUD $ 12 million. Company has Monash IVF

Group Ltd has maintained stable tax payment since last two year which is good indicator for

company (Brondolo, 2009)

Particular(AUD $ in million) 2015 2016

Income tax expenses 12 12

Company has to adopt proper tax planning process with a view to reduce the tax payment. In

addition to this, company has increased deferred tax liabilities by AUD $ 1 million.

4

Accumulated profit (113) (104)

Retained earning 161 161

Total equity 287 288

Discussion on the retained earning

Company has maintained stable retained earnings in both years. However, the main objective

of not plugging back of this capital in its business is based on the return on capital employed

of company. Monash IVF Group Ltd is not finding a good reason to expand its business as

company is having sluggish market conditions.

Answer to question-2

It is considered that tax is the amount which is charged on the profited of company.

Monash IVF Group Ltd has paid tax amount AUD $ 12 million. Company has Monash IVF

Group Ltd has maintained stable tax payment since last two year which is good indicator for

company (Brondolo, 2009)

Particular(AUD $ in million) 2015 2016

Income tax expenses 12 12

Company has to adopt proper tax planning process with a view to reduce the tax payment. In

addition to this, company has increased deferred tax liabilities by AUD $ 1 million.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Implication of taxation rules and regulations on Monash IVF Group Ltd

5

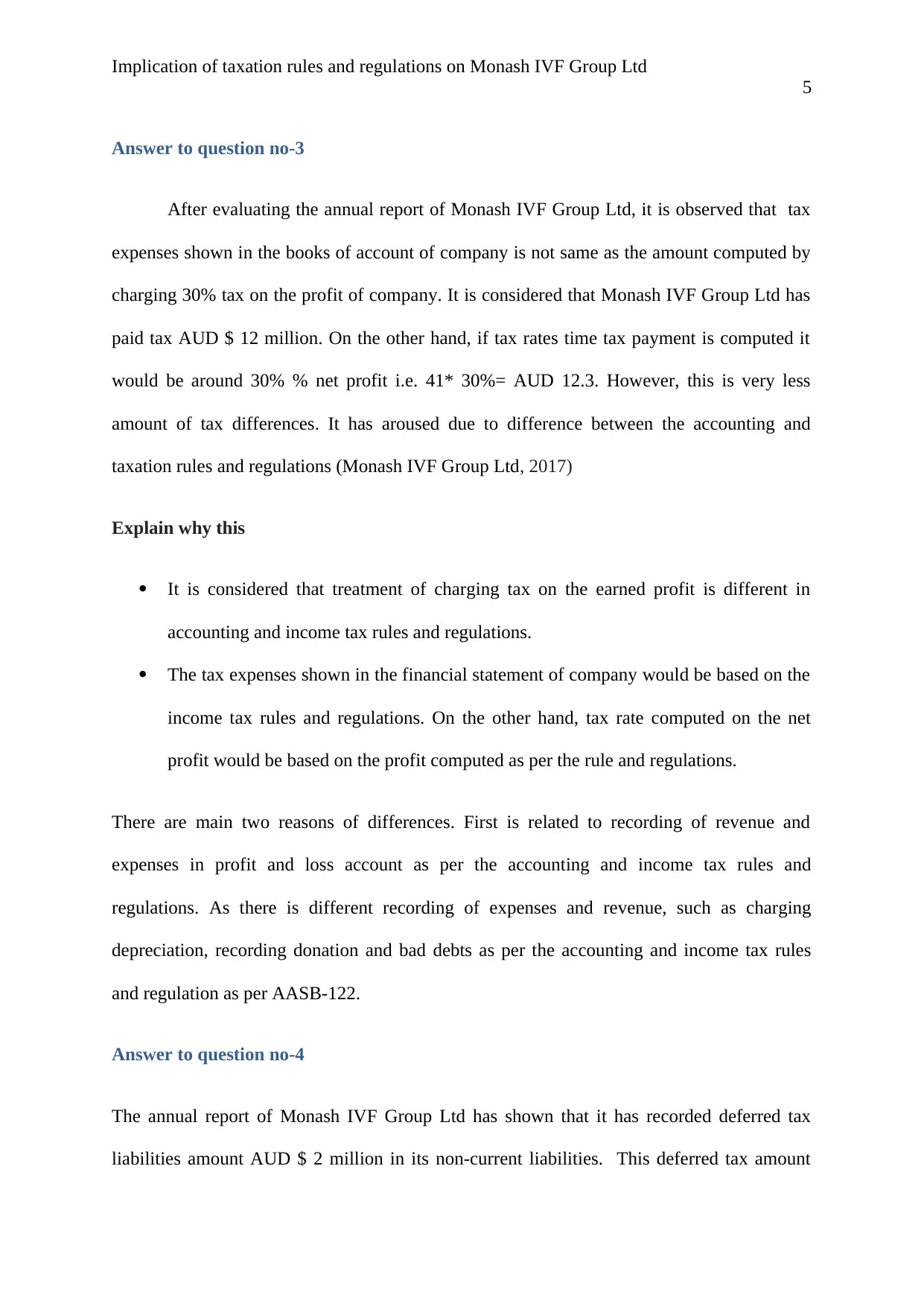

Answer to question no-3

After evaluating the annual report of Monash IVF Group Ltd, it is observed that tax

expenses shown in the books of account of company is not same as the amount computed by

charging 30% tax on the profit of company. It is considered that Monash IVF Group Ltd has

paid tax AUD $ 12 million. On the other hand, if tax rates time tax payment is computed it

would be around 30% % net profit i.e. 41* 30%= AUD 12.3. However, this is very less

amount of tax differences. It has aroused due to difference between the accounting and

taxation rules and regulations (Monash IVF Group Ltd, 2017)

Explain why this

It is considered that treatment of charging tax on the earned profit is different in

accounting and income tax rules and regulations.

The tax expenses shown in the financial statement of company would be based on the

income tax rules and regulations. On the other hand, tax rate computed on the net

profit would be based on the profit computed as per the rule and regulations.

There are main two reasons of differences. First is related to recording of revenue and

expenses in profit and loss account as per the accounting and income tax rules and

regulations. As there is different recording of expenses and revenue, such as charging

depreciation, recording donation and bad debts as per the accounting and income tax rules

and regulation as per AASB-122.

Answer to question no-4

The annual report of Monash IVF Group Ltd has shown that it has recorded deferred tax

liabilities amount AUD $ 2 million in its non-current liabilities. This deferred tax amount

5

Answer to question no-3

After evaluating the annual report of Monash IVF Group Ltd, it is observed that tax

expenses shown in the books of account of company is not same as the amount computed by

charging 30% tax on the profit of company. It is considered that Monash IVF Group Ltd has

paid tax AUD $ 12 million. On the other hand, if tax rates time tax payment is computed it

would be around 30% % net profit i.e. 41* 30%= AUD 12.3. However, this is very less

amount of tax differences. It has aroused due to difference between the accounting and

taxation rules and regulations (Monash IVF Group Ltd, 2017)

Explain why this

It is considered that treatment of charging tax on the earned profit is different in

accounting and income tax rules and regulations.

The tax expenses shown in the financial statement of company would be based on the

income tax rules and regulations. On the other hand, tax rate computed on the net

profit would be based on the profit computed as per the rule and regulations.

There are main two reasons of differences. First is related to recording of revenue and

expenses in profit and loss account as per the accounting and income tax rules and

regulations. As there is different recording of expenses and revenue, such as charging

depreciation, recording donation and bad debts as per the accounting and income tax rules

and regulation as per AASB-122.

Answer to question no-4

The annual report of Monash IVF Group Ltd has shown that it has recorded deferred tax

liabilities amount AUD $ 2 million in its non-current liabilities. This deferred tax amount

Implication of taxation rules and regulations on Monash IVF Group Ltd

6

needs to be recognized and carried forward to the extent that is reasonably sufficient for the

future taxable income. It is analysed that Monash IVF Group Ltd has paid lower tax as per

its income tax rules and regulation as compared to its tax computation based on the

accounting rules. .therefore, payment beyond that has been kept at the deferred tax liabilities.

It reflects that company may need to pay this tax payment in future if taxation rules and

regulations policies changes (Brigham and Ehrhardt, 2013).

On the other hand, if Monash IVF Group Ltd pays higher tax as per the income tax rules as

per the accounting rules and regulations then it needs to charge in its books of account of

company.

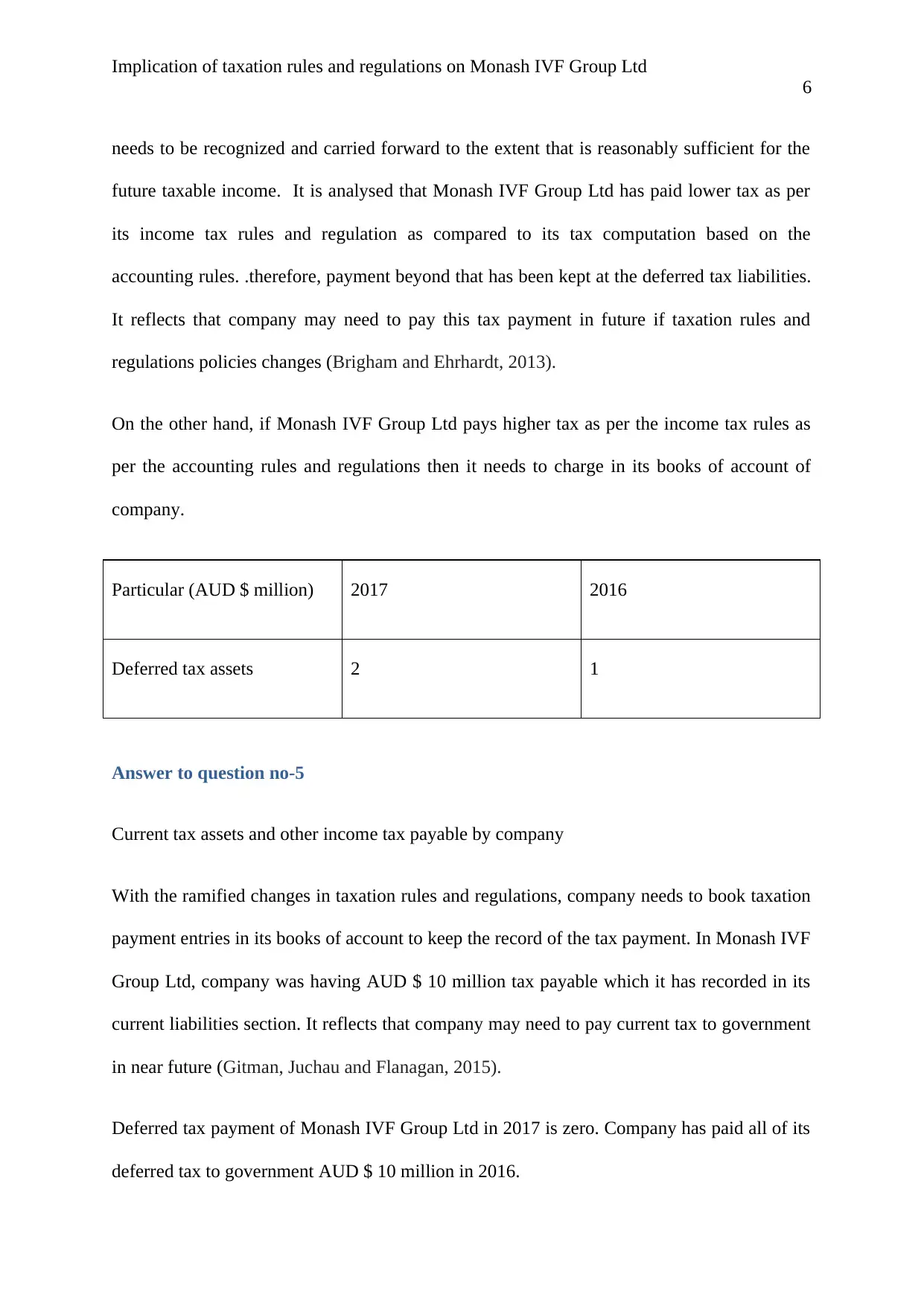

Particular (AUD $ million) 2017 2016

Deferred tax assets 2 1

Answer to question no-5

Current tax assets and other income tax payable by company

With the ramified changes in taxation rules and regulations, company needs to book taxation

payment entries in its books of account to keep the record of the tax payment. In Monash IVF

Group Ltd, company was having AUD $ 10 million tax payable which it has recorded in its

current liabilities section. It reflects that company may need to pay current tax to government

in near future (Gitman, Juchau and Flanagan, 2015).

Deferred tax payment of Monash IVF Group Ltd in 2017 is zero. Company has paid all of its

deferred tax to government AUD $ 10 million in 2016.

6

needs to be recognized and carried forward to the extent that is reasonably sufficient for the

future taxable income. It is analysed that Monash IVF Group Ltd has paid lower tax as per

its income tax rules and regulation as compared to its tax computation based on the

accounting rules. .therefore, payment beyond that has been kept at the deferred tax liabilities.

It reflects that company may need to pay this tax payment in future if taxation rules and

regulations policies changes (Brigham and Ehrhardt, 2013).

On the other hand, if Monash IVF Group Ltd pays higher tax as per the income tax rules as

per the accounting rules and regulations then it needs to charge in its books of account of

company.

Particular (AUD $ million) 2017 2016

Deferred tax assets 2 1

Answer to question no-5

Current tax assets and other income tax payable by company

With the ramified changes in taxation rules and regulations, company needs to book taxation

payment entries in its books of account to keep the record of the tax payment. In Monash IVF

Group Ltd, company was having AUD $ 10 million tax payable which it has recorded in its

current liabilities section. It reflects that company may need to pay current tax to government

in near future (Gitman, Juchau and Flanagan, 2015).

Deferred tax payment of Monash IVF Group Ltd in 2017 is zero. Company has paid all of its

deferred tax to government AUD $ 10 million in 2016.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Implication of taxation rules and regulations on Monash IVF Group Ltd

7

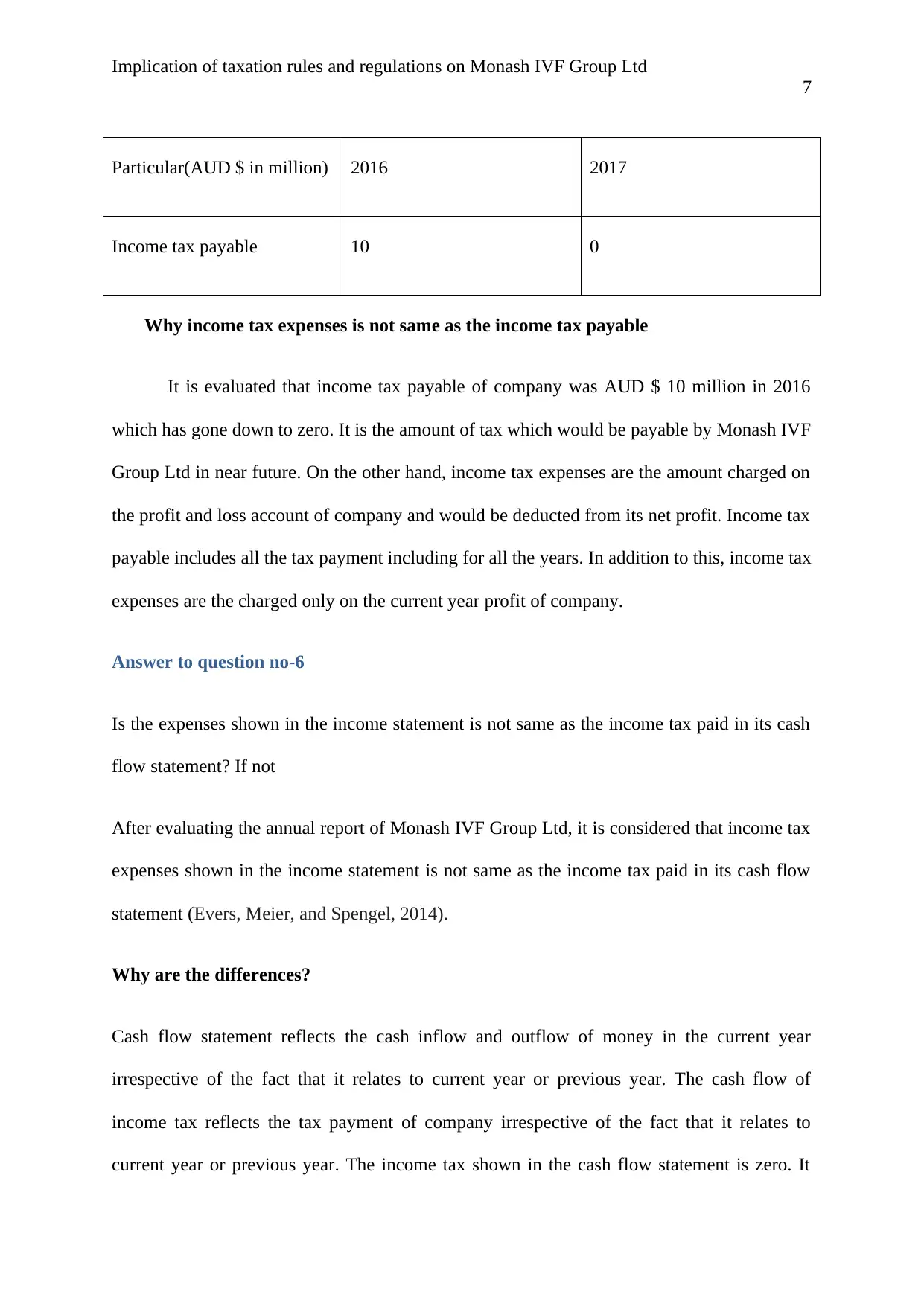

Particular(AUD $ in million) 2016 2017

Income tax payable 10 0

Why income tax expenses is not same as the income tax payable

It is evaluated that income tax payable of company was AUD $ 10 million in 2016

which has gone down to zero. It is the amount of tax which would be payable by Monash IVF

Group Ltd in near future. On the other hand, income tax expenses are the amount charged on

the profit and loss account of company and would be deducted from its net profit. Income tax

payable includes all the tax payment including for all the years. In addition to this, income tax

expenses are the charged only on the current year profit of company.

Answer to question no-6

Is the expenses shown in the income statement is not same as the income tax paid in its cash

flow statement? If not

After evaluating the annual report of Monash IVF Group Ltd, it is considered that income tax

expenses shown in the income statement is not same as the income tax paid in its cash flow

statement (Evers, Meier, and Spengel, 2014).

Why are the differences?

Cash flow statement reflects the cash inflow and outflow of money in the current year

irrespective of the fact that it relates to current year or previous year. The cash flow of

income tax reflects the tax payment of company irrespective of the fact that it relates to

current year or previous year. The income tax shown in the cash flow statement is zero. It

7

Particular(AUD $ in million) 2016 2017

Income tax payable 10 0

Why income tax expenses is not same as the income tax payable

It is evaluated that income tax payable of company was AUD $ 10 million in 2016

which has gone down to zero. It is the amount of tax which would be payable by Monash IVF

Group Ltd in near future. On the other hand, income tax expenses are the amount charged on

the profit and loss account of company and would be deducted from its net profit. Income tax

payable includes all the tax payment including for all the years. In addition to this, income tax

expenses are the charged only on the current year profit of company.

Answer to question no-6

Is the expenses shown in the income statement is not same as the income tax paid in its cash

flow statement? If not

After evaluating the annual report of Monash IVF Group Ltd, it is considered that income tax

expenses shown in the income statement is not same as the income tax paid in its cash flow

statement (Evers, Meier, and Spengel, 2014).

Why are the differences?

Cash flow statement reflects the cash inflow and outflow of money in the current year

irrespective of the fact that it relates to current year or previous year. The cash flow of

income tax reflects the tax payment of company irrespective of the fact that it relates to

current year or previous year. The income tax shown in the cash flow statement is zero. It

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Implication of taxation rules and regulations on Monash IVF Group Ltd

8

reflects that in current year company has paid zero amount of tax. On the other hand, income

tax expenses shown in the profit and loss account is the amount of tax charged on the profit

and loss account. The current tax expenses of Monash IVF Group Ltd is AUD $ 12 million. Now

in the end, it could be inferred that each and every statement of company has its own

recording process and values. These documents serve their own particular objects. There is

zero amount of tax payment in the current year of Monash IVF Group Ltd. Therefore, there is

no amount shown in the cash flow statement of company.

Answer to question no-7

Treatment of recording of tax in the books of account of Monash IVF Group Ltd

Interesting thing about the recorded its entire tax amount

Recording of income tax in the books of account of company is based on the taxation rules

and regulations given under AASB-112. It is considered that entries for tax recording are

done in the profit and loss account, balance sheet and cash flow statement. The main

interesting thing about the recording of tax is related to contradiction of tax computation as

per the accounting rules and regulations and taxation rules and regulations (Monash IVF

Group Ltd, 2017).

Surprising thing about the recorded its entire tax amount

The main surprising thing about recording of tax in the books of Monash IVF Group Ltd is

related to corporate governance recording and income tax rules. Company needs to block

high amount in its deferred tax liabilities in case its tax computation is low as per the

accounting rules while comparing the same with the taxation rules. In addition to this,

8

reflects that in current year company has paid zero amount of tax. On the other hand, income

tax expenses shown in the profit and loss account is the amount of tax charged on the profit

and loss account. The current tax expenses of Monash IVF Group Ltd is AUD $ 12 million. Now

in the end, it could be inferred that each and every statement of company has its own

recording process and values. These documents serve their own particular objects. There is

zero amount of tax payment in the current year of Monash IVF Group Ltd. Therefore, there is

no amount shown in the cash flow statement of company.

Answer to question no-7

Treatment of recording of tax in the books of account of Monash IVF Group Ltd

Interesting thing about the recorded its entire tax amount

Recording of income tax in the books of account of company is based on the taxation rules

and regulations given under AASB-112. It is considered that entries for tax recording are

done in the profit and loss account, balance sheet and cash flow statement. The main

interesting thing about the recording of tax is related to contradiction of tax computation as

per the accounting rules and regulations and taxation rules and regulations (Monash IVF

Group Ltd, 2017).

Surprising thing about the recorded its entire tax amount

The main surprising thing about recording of tax in the books of Monash IVF Group Ltd is

related to corporate governance recording and income tax rules. Company needs to block

high amount in its deferred tax liabilities in case its tax computation is low as per the

accounting rules while comparing the same with the taxation rules. In addition to this,

Implication of taxation rules and regulations on Monash IVF Group Ltd

9

Monash IVF Group Ltd can never have deferred tax assets and deferred tax liabilities at the

same.

Difficulty in recorded the entire tax amount

Monash IVF Group Ltd has complex tax recording structure. The main problem arise when

the income tax expenses is not same as per the tax rate income computation of company.

Monash IVF Group Ltd has found difficult to bifurcate tax payment as per the rule

and regulation given under AASB-112.

New insight about the company account for the income tax

The main insight about the recording of tax in the books of account is related to

changing taxation rules and regulations. Company needs to be ready and alert for the taxation

rules and regulation. Company might face cumbersome and complicated process while

recording of taxation rules and regulation in its books of account.

9

Monash IVF Group Ltd can never have deferred tax assets and deferred tax liabilities at the

same.

Difficulty in recorded the entire tax amount

Monash IVF Group Ltd has complex tax recording structure. The main problem arise when

the income tax expenses is not same as per the tax rate income computation of company.

Monash IVF Group Ltd has found difficult to bifurcate tax payment as per the rule

and regulation given under AASB-112.

New insight about the company account for the income tax

The main insight about the recording of tax in the books of account is related to

changing taxation rules and regulations. Company needs to be ready and alert for the taxation

rules and regulation. Company might face cumbersome and complicated process while

recording of taxation rules and regulation in its books of account.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Implication of taxation rules and regulations on Monash IVF Group Ltd

10

References

Ballas, A.A., Skoutela, D. and Tzovas, C.A., 2010. The relevance of IFRS to an emerging

market: evidence from Greece. Managerial Finance, 36(11), pp.931-948.

Blouin, J.L. and Robinson, L.A., 2014. Insights from academic participation in the FAF's

initial PIR: The PIR of FIN 48. Accounting Horizons, 28(3), pp.479-500.

Brigham, E.F. and Ehrhardt, M.C., 2013. Financial management: Theory & practice.

Cengage Learning.

Brondolo, J., 2009. Collecting taxes during an economic crisis: challenges and policy

options (No. 2009-2017). International Monetary Fund.

Evers, M.T., Meier, I. and Spengel, C., 2014. Transparency in Financial Reporting: Is

Country-by-Country Reporting suitable to combat international profit shifting?.

Gitman, L.J., Juchau, R. and Flanagan, J., 2015. Principles of managerial finance. Pearson

Higher Education AU.

Monash IVF Group Ltd, 2017, annual report, Retrieved on 22st January, 2017 from

http://ir.monashivfgroup.com.au/Investor-Centre/?page=Annual-Reports

10

References

Ballas, A.A., Skoutela, D. and Tzovas, C.A., 2010. The relevance of IFRS to an emerging

market: evidence from Greece. Managerial Finance, 36(11), pp.931-948.

Blouin, J.L. and Robinson, L.A., 2014. Insights from academic participation in the FAF's

initial PIR: The PIR of FIN 48. Accounting Horizons, 28(3), pp.479-500.

Brigham, E.F. and Ehrhardt, M.C., 2013. Financial management: Theory & practice.

Cengage Learning.

Brondolo, J., 2009. Collecting taxes during an economic crisis: challenges and policy

options (No. 2009-2017). International Monetary Fund.

Evers, M.T., Meier, I. and Spengel, C., 2014. Transparency in Financial Reporting: Is

Country-by-Country Reporting suitable to combat international profit shifting?.

Gitman, L.J., Juchau, R. and Flanagan, J., 2015. Principles of managerial finance. Pearson

Higher Education AU.

Monash IVF Group Ltd, 2017, annual report, Retrieved on 22st January, 2017 from

http://ir.monashivfgroup.com.au/Investor-Centre/?page=Annual-Reports

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Implication of taxation rules and regulations on Monash IVF Group Ltd

11

Appendix

MONASH IVF GROUP LTD (MIS) Cash Flow Flag BALANCE SHEET

Fiscal year ends in June. AUD in millions

except per share data.

2013-

06

2014-

06

2015-

06

2016-

06

2017-

06

Assets

Current assets

Cash

Cash and cash equivalents 9 10 8 4

Total cash 9 10 8 4

Receivables 3 3 4 5

Other current assets 3 4 5 6

Total current assets 15 17 18 15

Non-current assets

Property, plant and equipment

Gross property, plant and equipment 27 36 40 45

Accumulated Depreciation -18 -21 -25 -29

Net property, plant and equipment 9 14 15 17

Equity and other investments 1 0 1

Goodwill 198 229 229 229

Intangible assets 22 22 25 26

Deferred income taxes 3 0

Other long-term assets 0 0 0 0

Total non-current assets 232 267 270 272

Total assets 246 284 288 287

Liabilities and stockholders' equity

Liabilities

Current liabilities

Short-term debt 0

Accounts payable 1 2 4 4

Deferred income taxes 1 3 10 0

Other current liabilities 22 27 23 21

Total current liabilities 24 32 36 25

Non-current liabilities

Long-term debt 95 106 95 95

Deferred taxes liabilities 1 2

Other long-term liabilities 2 1 1 2

Total non-current liabilities 97 108 96 99

Total liabilities 122 140 133 124

Stockholders' equity

Common stock 423 428 428 428

11

Appendix

MONASH IVF GROUP LTD (MIS) Cash Flow Flag BALANCE SHEET

Fiscal year ends in June. AUD in millions

except per share data.

2013-

06

2014-

06

2015-

06

2016-

06

2017-

06

Assets

Current assets

Cash

Cash and cash equivalents 9 10 8 4

Total cash 9 10 8 4

Receivables 3 3 4 5

Other current assets 3 4 5 6

Total current assets 15 17 18 15

Non-current assets

Property, plant and equipment

Gross property, plant and equipment 27 36 40 45

Accumulated Depreciation -18 -21 -25 -29

Net property, plant and equipment 9 14 15 17

Equity and other investments 1 0 1

Goodwill 198 229 229 229

Intangible assets 22 22 25 26

Deferred income taxes 3 0

Other long-term assets 0 0 0 0

Total non-current assets 232 267 270 272

Total assets 246 284 288 287

Liabilities and stockholders' equity

Liabilities

Current liabilities

Short-term debt 0

Accounts payable 1 2 4 4

Deferred income taxes 1 3 10 0

Other current liabilities 22 27 23 21

Total current liabilities 24 32 36 25

Non-current liabilities

Long-term debt 95 106 95 95

Deferred taxes liabilities 1 2

Other long-term liabilities 2 1 1 2

Total non-current liabilities 97 108 96 99

Total liabilities 122 140 133 124

Stockholders' equity

Common stock 423 428 428 428

Implication of taxation rules and regulations on Monash IVF Group Ltd

12

Retained earnings -161 -161 -161 -161

Accumulated other comprehensive income -137 -123 -113 -104

Total stockholders' equity 125 144 155 164

Total liabilities and stockholders' equity 246 284 288 287

Income statement

MONASH IVF GROUP LTD (MIS) Cash Flow Flag INCOME STATEMENT

Fiscal year ends in June. AUD in millions

except per share data.

2013-

06

2014-

06

2015-

06

2016-

06

2017-

06

TT

M

Revenue 114 122 157 155 155

Cost of revenue 11 13 14 13 13

Gross profit 103 109 142 142 142

Operating expenses

Sales, General and administrative 53 59 78 79 79

Other operating expenses 28 17 18 18 18

Total operating expenses 81 77 97 98 98

Operating income 22 32 45 45 45

Interest Expense 25 5 5 3 3

Other income (expense) 1 3 0 0 0

Income before taxes -2 31 41 41 41

Provision for income taxes -7 9 12 12 12

Net income from continuing operations 5 21 29 30 30

Other -2

Net income 3 21 29 30 30

Net income available to common

shareholders 3 21 29 30 30

Earnings per share

Basic 0.02 0.09 0.12 0.13

0.1

3

Diluted 0.02 0.09 0.12 0.13

0.1

3

Weighted average shares outstanding

Basic 126 231 235 235 235

Diluted 126 231 235 237 237

EBITDA 26 39 50 49 49

12

Retained earnings -161 -161 -161 -161

Accumulated other comprehensive income -137 -123 -113 -104

Total stockholders' equity 125 144 155 164

Total liabilities and stockholders' equity 246 284 288 287

Income statement

MONASH IVF GROUP LTD (MIS) Cash Flow Flag INCOME STATEMENT

Fiscal year ends in June. AUD in millions

except per share data.

2013-

06

2014-

06

2015-

06

2016-

06

2017-

06

TT

M

Revenue 114 122 157 155 155

Cost of revenue 11 13 14 13 13

Gross profit 103 109 142 142 142

Operating expenses

Sales, General and administrative 53 59 78 79 79

Other operating expenses 28 17 18 18 18

Total operating expenses 81 77 97 98 98

Operating income 22 32 45 45 45

Interest Expense 25 5 5 3 3

Other income (expense) 1 3 0 0 0

Income before taxes -2 31 41 41 41

Provision for income taxes -7 9 12 12 12

Net income from continuing operations 5 21 29 30 30

Other -2

Net income 3 21 29 30 30

Net income available to common

shareholders 3 21 29 30 30

Earnings per share

Basic 0.02 0.09 0.12 0.13

0.1

3

Diluted 0.02 0.09 0.12 0.13

0.1

3

Weighted average shares outstanding

Basic 126 231 235 235 235

Diluted 126 231 235 237 237

EBITDA 26 39 50 49 49

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.