Deferred Tax Assets & Liabilities: Importance in Financial Statements

VerifiedAdded on 2020/03/16

|8

|1456

|185

Report

AI Summary

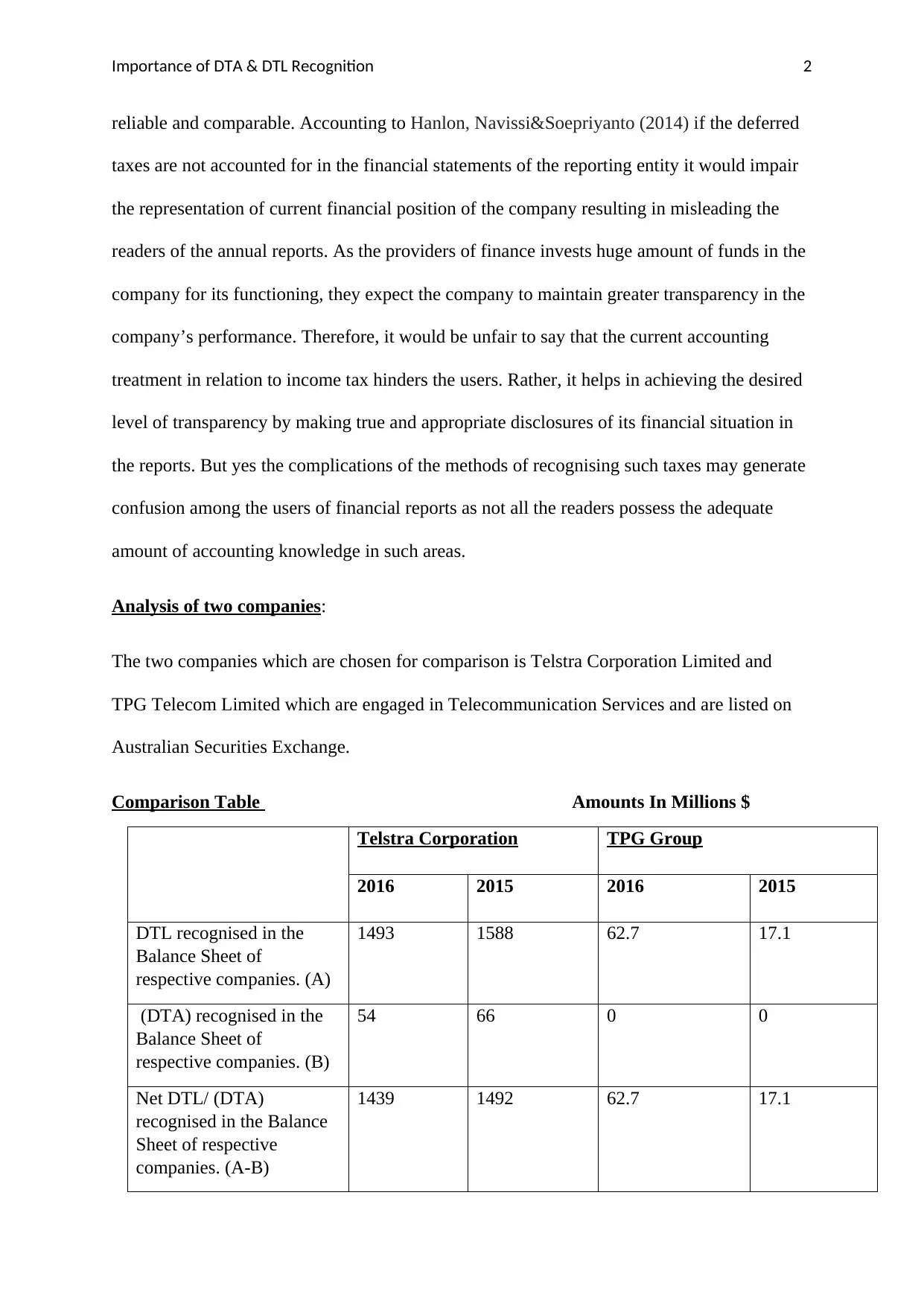

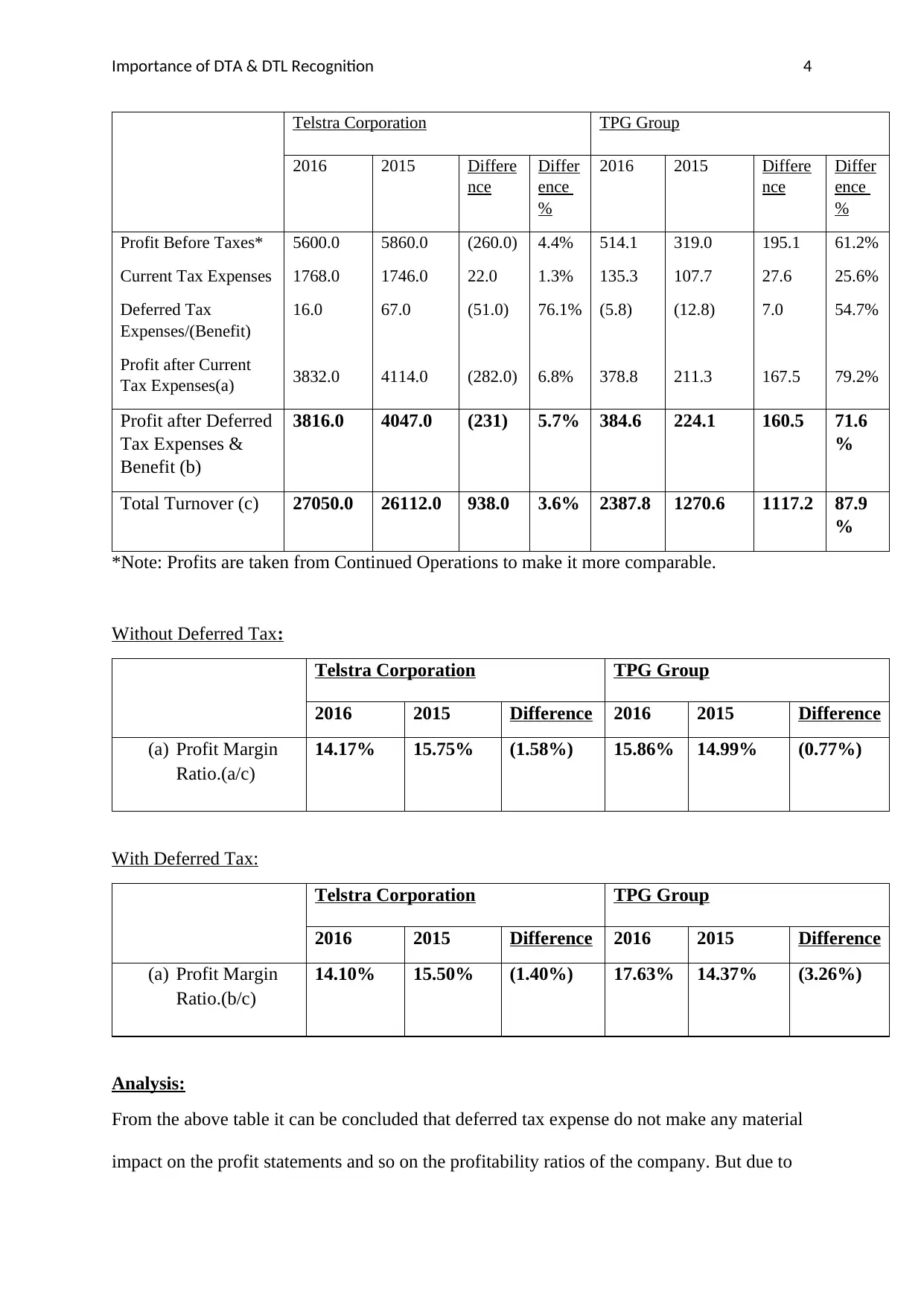

This report examines the importance of recognizing Deferred Tax Assets (DTA) and Liabilities (DTL) in financial accounting, focusing on AASB 112 (Income Taxes) and its alignment with IAS 12. The report discusses the nature of temporary differences, the creation of DTA and DTL, and their impact on financial statements, emphasizing the role of DTA and DTL in providing a true and fair view of a company's financial position. It analyzes the financial statements of Telstra Corporation Limited and TPG Telecom Limited, comparing their DTA and DTL recognition and the impact on their financial ratios. The analysis highlights how changes in effective tax rates and profit margins affect investor understanding and the overall financial performance of the companies. The report concludes with a discussion on the importance of understanding the impact of DTA and DTL on future tax obligations and the transparency of financial reporting, supported by references to relevant literature and annual reports.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.