Financial Management Report: Statements, Ratios, and Performance

VerifiedAdded on 2022/12/26

|16

|3353

|41

Report

AI Summary

This report provides a comprehensive overview of financial management, beginning with its core concepts and relevance within an organization. It explores the use of financial statements, including income statements, balance sheets, and cash flow statements, explaining their purpose and components. The report also delves into ratio analysis, covering profitability and efficiency ratios, and demonstrating their application in assessing a company's financial health and performance. Furthermore, the report discusses how organizations can improve their financial performance through effective financial planning, capital structure decisions, and cost control measures. The report uses financial data to illustrate key concepts and calculations, providing a practical understanding of financial management principles and their application in real-world scenarios. The report includes the formulation of financial statements, calculation of financial ratios and explanation of their relevance in decision making.

IMPORTANCE OF

FINANCIAL MANAGEMENT

FINANCIAL MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................3

SECTION 1......................................................................................................................................3

Concept and relevance of financial management. ......................................................................3

SECTION 2......................................................................................................................................4

Brief explanation regarding different types of financial statement & use of ratio in financial

management. ...............................................................................................................................4

SECTION 3......................................................................................................................................7

Formulation of income statement................................................................................................7

Clarification Formulation of balance sheet..................................................................................8

Calculation of ratios. ...................................................................................................................9

SECTION 4....................................................................................................................................11

Process business organization use to improve their financial performance. ............................11

CONCLUSION .............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION ..........................................................................................................................3

SECTION 1......................................................................................................................................3

Concept and relevance of financial management. ......................................................................3

SECTION 2......................................................................................................................................4

Brief explanation regarding different types of financial statement & use of ratio in financial

management. ...............................................................................................................................4

SECTION 3......................................................................................................................................7

Formulation of income statement................................................................................................7

Clarification Formulation of balance sheet..................................................................................8

Calculation of ratios. ...................................................................................................................9

SECTION 4....................................................................................................................................11

Process business organization use to improve their financial performance. ............................11

CONCLUSION .............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

The term financial management is related with managing monetary resource of

organization by implementing effective planning sand controlling strategy related with capital of

finance. This report is formulated to define relevance of financial management by defining use of

tools and technique this approach as well as importance of ratio analysis and use of financial

statement. It is also includes process or strategies use by management department to enhance

financial performance of their business organization.

SECTION 1

Concept and relevance of financial management.

Financial management: The term financial management is combination of 2 words, first is

finance and other is management. Finance is consider as blood of business organization and it

provide money to fulfill requirement of running business activities. On the other side,

management is the process of properly plan, organize, coordinate and control resource of finance

for successfully run operations of business. In other words, financial management is the

procedure of managing financial resource in such a manner which help in increase profitability

rate and performance of business organization. It is consider as an application of planning &

controlling essential function of finance. Following are the importance of this application within

the organization:

Financial planning: Manager use financial management approach for the purpose of

formulate strategies and plan on the basis of analysing market condition. For this purpose

relevant business data is collected which useful in prepare future business policies in

order to attain m long term goal of ABC Limited (Barclay, Fu and Smith, 2020).

Determination of capital structure: Success of the organization depend on how

effective manager take decision regarding formulation of capital structure. As it is

combination of equity, debt, bond securities thus which manager need to invest in

resource help in maintain monetary cycle of cash flow activities within the business.

Manager of ABC Limited use tools of financial management which includes capital

budgeting on the basis of that they decide to format their capital structure in effective

manner.

The term financial management is related with managing monetary resource of

organization by implementing effective planning sand controlling strategy related with capital of

finance. This report is formulated to define relevance of financial management by defining use of

tools and technique this approach as well as importance of ratio analysis and use of financial

statement. It is also includes process or strategies use by management department to enhance

financial performance of their business organization.

SECTION 1

Concept and relevance of financial management.

Financial management: The term financial management is combination of 2 words, first is

finance and other is management. Finance is consider as blood of business organization and it

provide money to fulfill requirement of running business activities. On the other side,

management is the process of properly plan, organize, coordinate and control resource of finance

for successfully run operations of business. In other words, financial management is the

procedure of managing financial resource in such a manner which help in increase profitability

rate and performance of business organization. It is consider as an application of planning &

controlling essential function of finance. Following are the importance of this application within

the organization:

Financial planning: Manager use financial management approach for the purpose of

formulate strategies and plan on the basis of analysing market condition. For this purpose

relevant business data is collected which useful in prepare future business policies in

order to attain m long term goal of ABC Limited (Barclay, Fu and Smith, 2020).

Determination of capital structure: Success of the organization depend on how

effective manager take decision regarding formulation of capital structure. As it is

combination of equity, debt, bond securities thus which manager need to invest in

resource help in maintain monetary cycle of cash flow activities within the business.

Manager of ABC Limited use tools of financial management which includes capital

budgeting on the basis of that they decide to format their capital structure in effective

manner.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Allocation of funds: Financial management useful in allocation of necessary funds of

organization. Manager on the basis of finding requirement of each department allocate

money to department, this will help in reduce issue arises related with internal coherence

between different departments.

Monitoring financial activities: By using various tools of financial management,

manager able to measure and monitor each activity related with finance. On the basis of

that level of cash inflow is maintain.

Facilitate cost control: Financial management tools help in measuring cost require to

run any business activity and on the basis of that financial manager formulate policies &

strategies which help in finding out those investment activities which become reason of

generating high rate of cash outflow and incurred high rate of cost. With using effective

tool manager able to control cost activities (Brzozowski, and Visano, 2020).

Forecasting profit: Manager by formulating budget and analysing financial statement

able to predict regarding future rate of cash inflow as well as on the basis of that they

forecast value of profit, which organization may be able to generate in future time

period. On the basis of analysing amount of profit manager mitigate or control risk arise

during the time of execution of project activities.

Help in decision making process: Business organization run their operation on the

basis of decision they take regarding specific projects. Financial management techniques

are useful in order to take decision regarding with investment, financial, as these are

consider as relevant business decision and success of any project depend on the decision

which manager take regarding with running business activities.

SECTION 2

Brief explanation regarding different types of financial statement & use of ratio in financial

management.

Financial statement are consider as combination of different types of documents which are used

to formulate for the purpose of presenting all the relevant business data in effective manner.

Financial statement includes, balance sheet, income statement and cash flow statement . On the

organization. Manager on the basis of finding requirement of each department allocate

money to department, this will help in reduce issue arises related with internal coherence

between different departments.

Monitoring financial activities: By using various tools of financial management,

manager able to measure and monitor each activity related with finance. On the basis of

that level of cash inflow is maintain.

Facilitate cost control: Financial management tools help in measuring cost require to

run any business activity and on the basis of that financial manager formulate policies &

strategies which help in finding out those investment activities which become reason of

generating high rate of cash outflow and incurred high rate of cost. With using effective

tool manager able to control cost activities (Brzozowski, and Visano, 2020).

Forecasting profit: Manager by formulating budget and analysing financial statement

able to predict regarding future rate of cash inflow as well as on the basis of that they

forecast value of profit, which organization may be able to generate in future time

period. On the basis of analysing amount of profit manager mitigate or control risk arise

during the time of execution of project activities.

Help in decision making process: Business organization run their operation on the

basis of decision they take regarding specific projects. Financial management techniques

are useful in order to take decision regarding with investment, financial, as these are

consider as relevant business decision and success of any project depend on the decision

which manager take regarding with running business activities.

SECTION 2

Brief explanation regarding different types of financial statement & use of ratio in financial

management.

Financial statement are consider as combination of different types of documents which are used

to formulate for the purpose of presenting all the relevant business data in effective manner.

Financial statement includes, balance sheet, income statement and cash flow statement . On the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

basis of formulation of theses statement manager able to represent their statement of financial

position in front of internal as well as external shareholders. Theses statement are define below:

Income statement: The term income statement refer as document which represent revenue or

expenditure incurred for given time period. It is also known as earning report or profit and loss

statement. With the modification in norms of GAAP, now trading statement is also covered and

part of income statement.

This statement help in determine cost require to formation of a product and on the basis

of that expenses incurred on selling and advertisement of the product and income generate from

selling of goods and service and through other sources of income all these information are

define in this project in systematic manner. Profit and loss statement help in find out changes

value of profit as compare with previous year income statement and on the basis of formulation

of this statement manager able to understand and compare their performance of generating net

profit with rival organizations.

Balance sheet: It is a statement which showcase value of assets as well as liabilities.

Assets side are includes all those items which help in generate cash inflow activities and they are

the symbol of growth of organization, on the other side all liabilities includes item which

generate obligation to the organization Assets as well as liabilities also dividend into 2

categories which includes current assets and current liabilities as well as long term assets along

term liabilities (Hulikal Muralidhar, Bossen. Mehra, and O'Neill, 2018).

Assets: Items which contain economic value and help in alternate future profit are

consider assets.

Short term assets: Theses includes those assets which can be convertible, or sold or

liquidated within 1 year of time period. These help in determine liquidity position of

organization and includes, trade receivables, cash and cash related equipments, stock, pre-paid

expenses etc.

Fixed assets: Theses includes assets which value is not change with change of time

period and these are not easily convertible in cash. Fixed assets are help in generate long term

benefits. Theses includes, machine, building, long term investment etc.

Liabilities: Theses includes items which generate obligation on organization. These are

legal responsibilities and sacrifice of economic benefit. There are two types of liabilities :

position in front of internal as well as external shareholders. Theses statement are define below:

Income statement: The term income statement refer as document which represent revenue or

expenditure incurred for given time period. It is also known as earning report or profit and loss

statement. With the modification in norms of GAAP, now trading statement is also covered and

part of income statement.

This statement help in determine cost require to formation of a product and on the basis

of that expenses incurred on selling and advertisement of the product and income generate from

selling of goods and service and through other sources of income all these information are

define in this project in systematic manner. Profit and loss statement help in find out changes

value of profit as compare with previous year income statement and on the basis of formulation

of this statement manager able to understand and compare their performance of generating net

profit with rival organizations.

Balance sheet: It is a statement which showcase value of assets as well as liabilities.

Assets side are includes all those items which help in generate cash inflow activities and they are

the symbol of growth of organization, on the other side all liabilities includes item which

generate obligation to the organization Assets as well as liabilities also dividend into 2

categories which includes current assets and current liabilities as well as long term assets along

term liabilities (Hulikal Muralidhar, Bossen. Mehra, and O'Neill, 2018).

Assets: Items which contain economic value and help in alternate future profit are

consider assets.

Short term assets: Theses includes those assets which can be convertible, or sold or

liquidated within 1 year of time period. These help in determine liquidity position of

organization and includes, trade receivables, cash and cash related equipments, stock, pre-paid

expenses etc.

Fixed assets: Theses includes assets which value is not change with change of time

period and these are not easily convertible in cash. Fixed assets are help in generate long term

benefits. Theses includes, machine, building, long term investment etc.

Liabilities: Theses includes items which generate obligation on organization. These are

legal responsibilities and sacrifice of economic benefit. There are two types of liabilities :

Short term liability: obligations which payment organization need to pay within one

year are known as short term business liabilities. Theses are items which become the reason of

generate problems in between cash inflow. And reason of incurring high rate of cash outflow.

Trade payable, short term borrowing etc.

Long term liability: Items or liabilities which are due more then of over 1 year. It also

includes part of equity, reserve, long term loan and securities bond. Generally equity is part of

liabilities however their block is separate from current as well as long term debt liabilities.

Cash flow statement: Report which is formulated for the purpose of showcase inflow

and outflow related with cash in specific time period. This statement is formulated by applying

direct as well as indirect method. Which are define below:

Operating activity: Activity which define how organization generate money from their

running business operations and selling business products of organization. Operating activity

help in determine how effective and efficiency manager able to maintain their cash flow

activities by selling their business products (Khan, Zaman, Usman,Nassani, Aldakhil and Abro,

2019).

Investment activity: This activity help in find out how effectively manager generate

cash from their investment portfolio and requirement of cash outflow of these activities.

Financial activity: By formulation of statement of cash flow this activity help in

determine relevance of financial activities to generate cash inflow from earn interest, and outflow

which is related with distribution of dividend activities.

This statement help in recognize how effective manager able to maintain their cash position

within organization.

Use of ratio in financial management approach:

Decision making:With the help of calculating different types of ratio organization able to

take decision regarding which alternative is best and generate more profit. On the basis of

calculating gearing ratio and debt equity ratio manager find out rate of generating interest and

pay debt liability which help in formulate policies.

Find out efficiency: Manager on the basis of calculating value of current as well as

quick ratio able to find out rate of liquidity On the basis of that they are able to evaluate ability of

year are known as short term business liabilities. Theses are items which become the reason of

generate problems in between cash inflow. And reason of incurring high rate of cash outflow.

Trade payable, short term borrowing etc.

Long term liability: Items or liabilities which are due more then of over 1 year. It also

includes part of equity, reserve, long term loan and securities bond. Generally equity is part of

liabilities however their block is separate from current as well as long term debt liabilities.

Cash flow statement: Report which is formulated for the purpose of showcase inflow

and outflow related with cash in specific time period. This statement is formulated by applying

direct as well as indirect method. Which are define below:

Operating activity: Activity which define how organization generate money from their

running business operations and selling business products of organization. Operating activity

help in determine how effective and efficiency manager able to maintain their cash flow

activities by selling their business products (Khan, Zaman, Usman,Nassani, Aldakhil and Abro,

2019).

Investment activity: This activity help in find out how effectively manager generate

cash from their investment portfolio and requirement of cash outflow of these activities.

Financial activity: By formulation of statement of cash flow this activity help in

determine relevance of financial activities to generate cash inflow from earn interest, and outflow

which is related with distribution of dividend activities.

This statement help in recognize how effective manager able to maintain their cash position

within organization.

Use of ratio in financial management approach:

Decision making:With the help of calculating different types of ratio organization able to

take decision regarding which alternative is best and generate more profit. On the basis of

calculating gearing ratio and debt equity ratio manager find out rate of generating interest and

pay debt liability which help in formulate policies.

Find out efficiency: Manager on the basis of calculating value of current as well as

quick ratio able to find out rate of liquidity On the basis of that they are able to evaluate ability of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

organization to pay their relevant short term liability by using their liquidity assets and cash

availability within the organization.

Future forecasting: Ratio is part of financial management technique, on the basis of

defining value of different ratio which includes, profit and loss and balance sheet ratio, manager

able to forecast regarding their future rate of gearing. On the basis of ratio analysis they are able

to compare their organization's performance with previous year and this will help in prove bas

regarding formulation of budget and predict future rate of earrings (Marqués, García and

Sánchez, J 2020).

SECTION 3

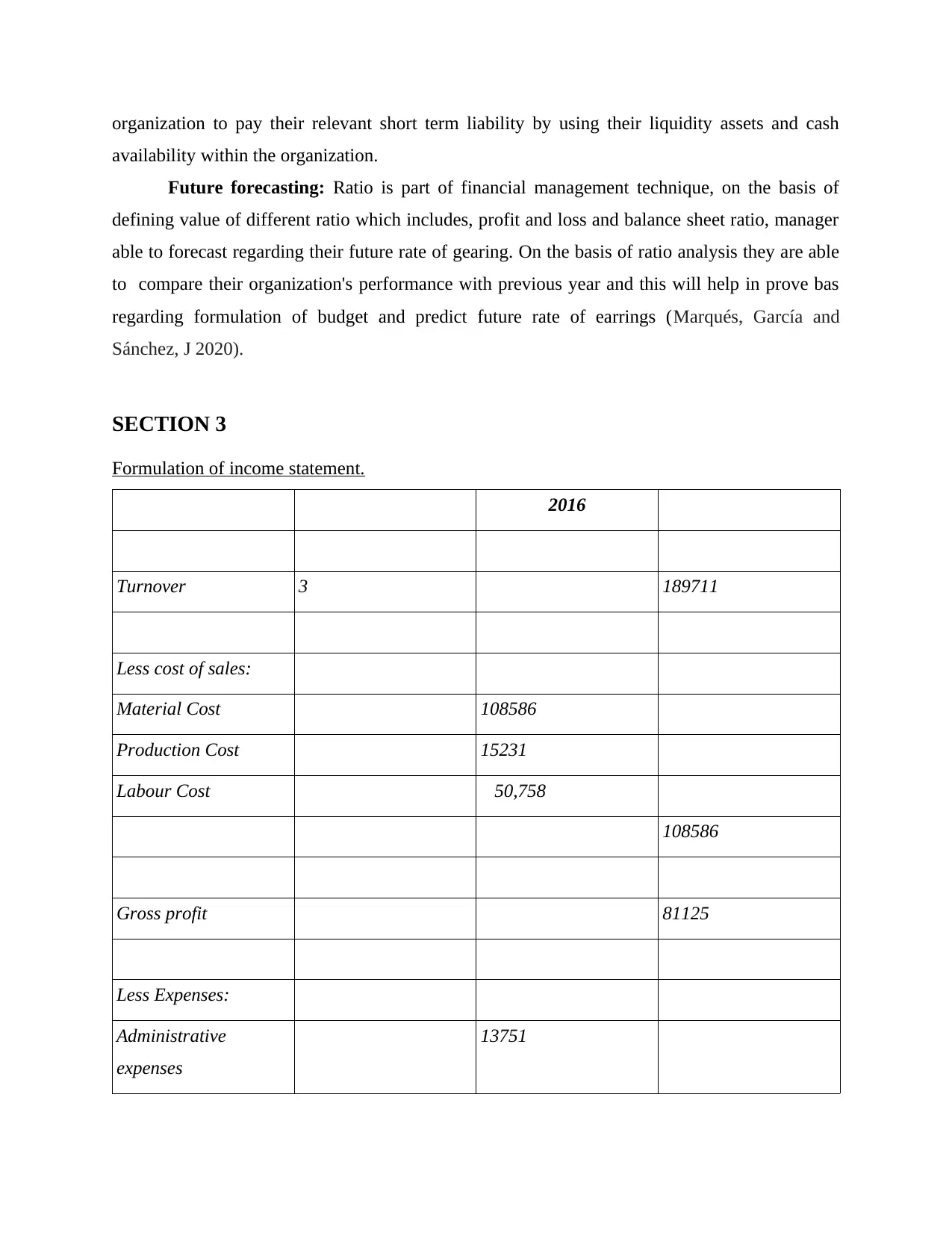

Formulation of income statement.

2016

Turnover 3 189711

Less cost of sales:

Material Cost 108586

Production Cost 15231

Labour Cost 50,758

108586

Gross profit 81125

Less Expenses:

Administrative

expenses

13751

availability within the organization.

Future forecasting: Ratio is part of financial management technique, on the basis of

defining value of different ratio which includes, profit and loss and balance sheet ratio, manager

able to forecast regarding their future rate of gearing. On the basis of ratio analysis they are able

to compare their organization's performance with previous year and this will help in prove bas

regarding formulation of budget and predict future rate of earrings (Marqués, García and

Sánchez, J 2020).

SECTION 3

Formulation of income statement.

2016

Turnover 3 189711

Less cost of sales:

Material Cost 108586

Production Cost 15231

Labour Cost 50,758

108586

Gross profit 81125

Less Expenses:

Administrative

expenses

13751

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

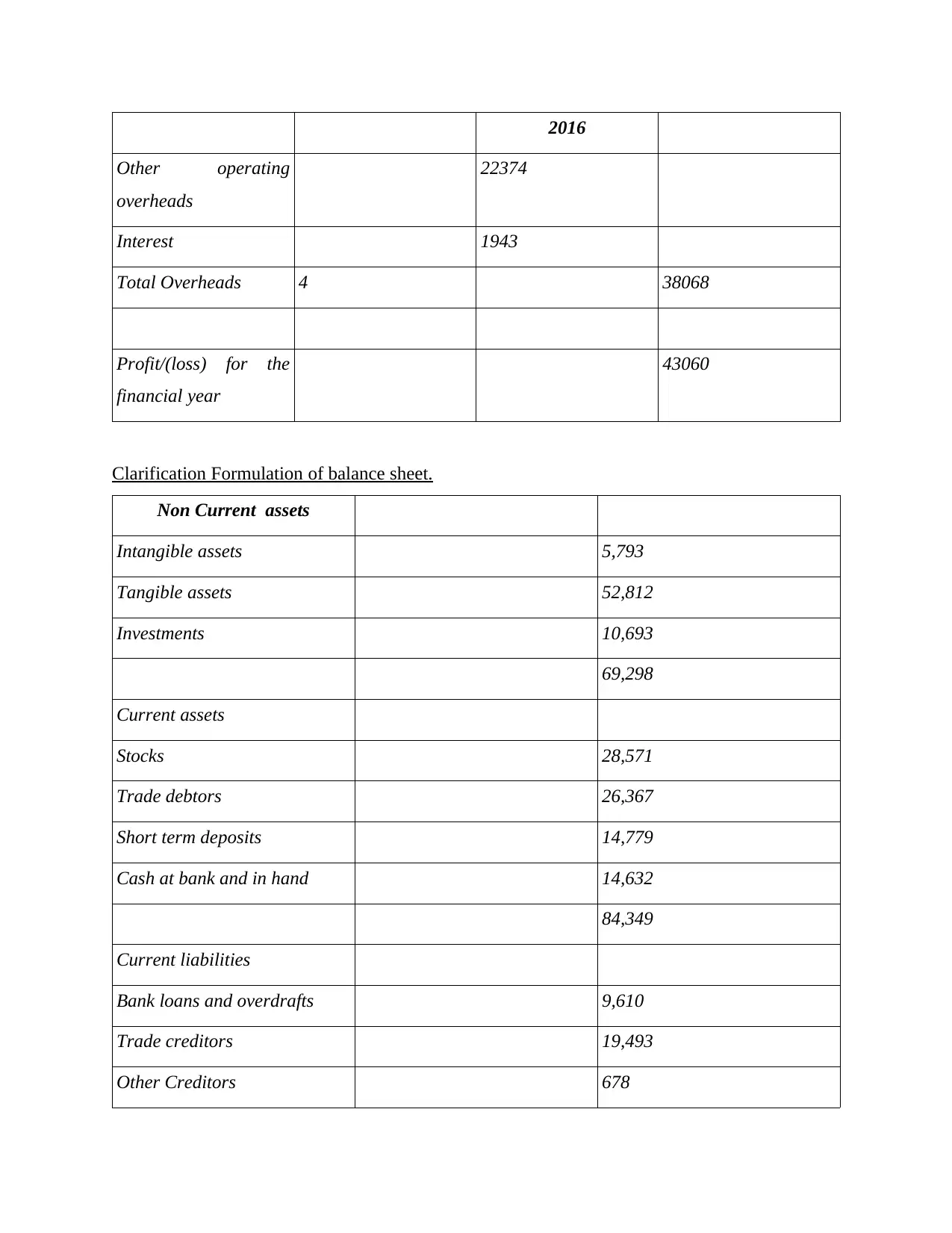

2016

Other operating

overheads

22374

Interest 1943

Total Overheads 4 38068

Profit/(loss) for the

financial year

43060

Clarification Formulation of balance sheet.

Non Current assets

Intangible assets 5,793

Tangible assets 52,812

Investments 10,693

69,298

Current assets

Stocks 28,571

Trade debtors 26,367

Short term deposits 14,779

Cash at bank and in hand 14,632

84,349

Current liabilities

Bank loans and overdrafts 9,610

Trade creditors 19,493

Other Creditors 678

Other operating

overheads

22374

Interest 1943

Total Overheads 4 38068

Profit/(loss) for the

financial year

43060

Clarification Formulation of balance sheet.

Non Current assets

Intangible assets 5,793

Tangible assets 52,812

Investments 10,693

69,298

Current assets

Stocks 28,571

Trade debtors 26,367

Short term deposits 14,779

Cash at bank and in hand 14,632

84,349

Current liabilities

Bank loans and overdrafts 9,610

Trade creditors 19,493

Other Creditors 678

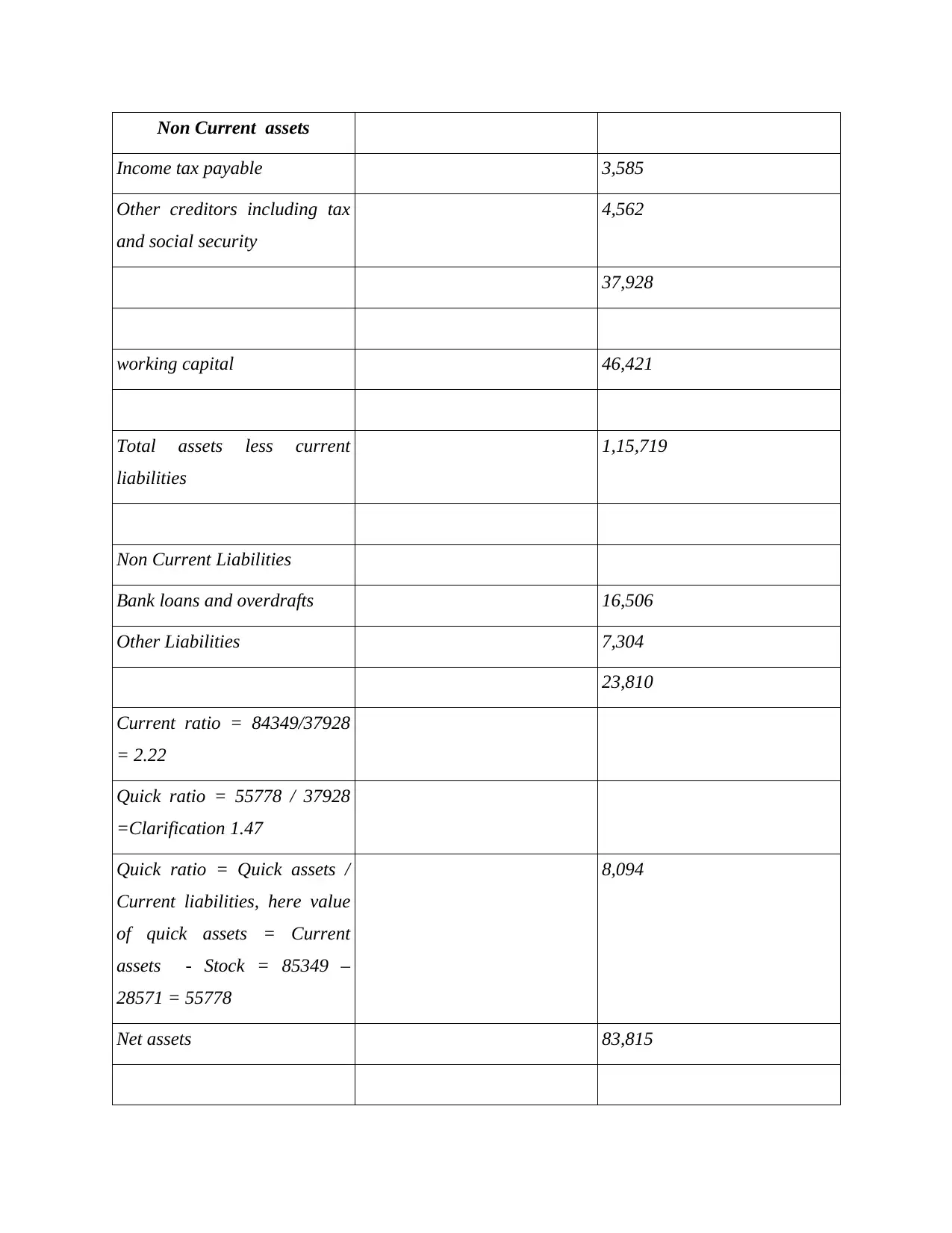

Non Current assets

Income tax payable 3,585

Other creditors including tax

and social security

4,562

37,928

working capital 46,421

Total assets less current

liabilities

1,15,719

Non Current Liabilities

Bank loans and overdrafts 16,506

Other Liabilities 7,304

23,810

Current ratio = 84349/37928

= 2.22

Quick ratio = 55778 / 37928

=Clarification 1.47

Quick ratio = Quick assets /

Current liabilities, here value

of quick assets = Current

assets - Stock = 85349 –

28571 = 55778

8,094

Net assets 83,815

Income tax payable 3,585

Other creditors including tax

and social security

4,562

37,928

working capital 46,421

Total assets less current

liabilities

1,15,719

Non Current Liabilities

Bank loans and overdrafts 16,506

Other Liabilities 7,304

23,810

Current ratio = 84349/37928

= 2.22

Quick ratio = 55778 / 37928

=Clarification 1.47

Quick ratio = Quick assets /

Current liabilities, here value

of quick assets = Current

assets - Stock = 85349 –

28571 = 55778

8,094

Net assets 83,815

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

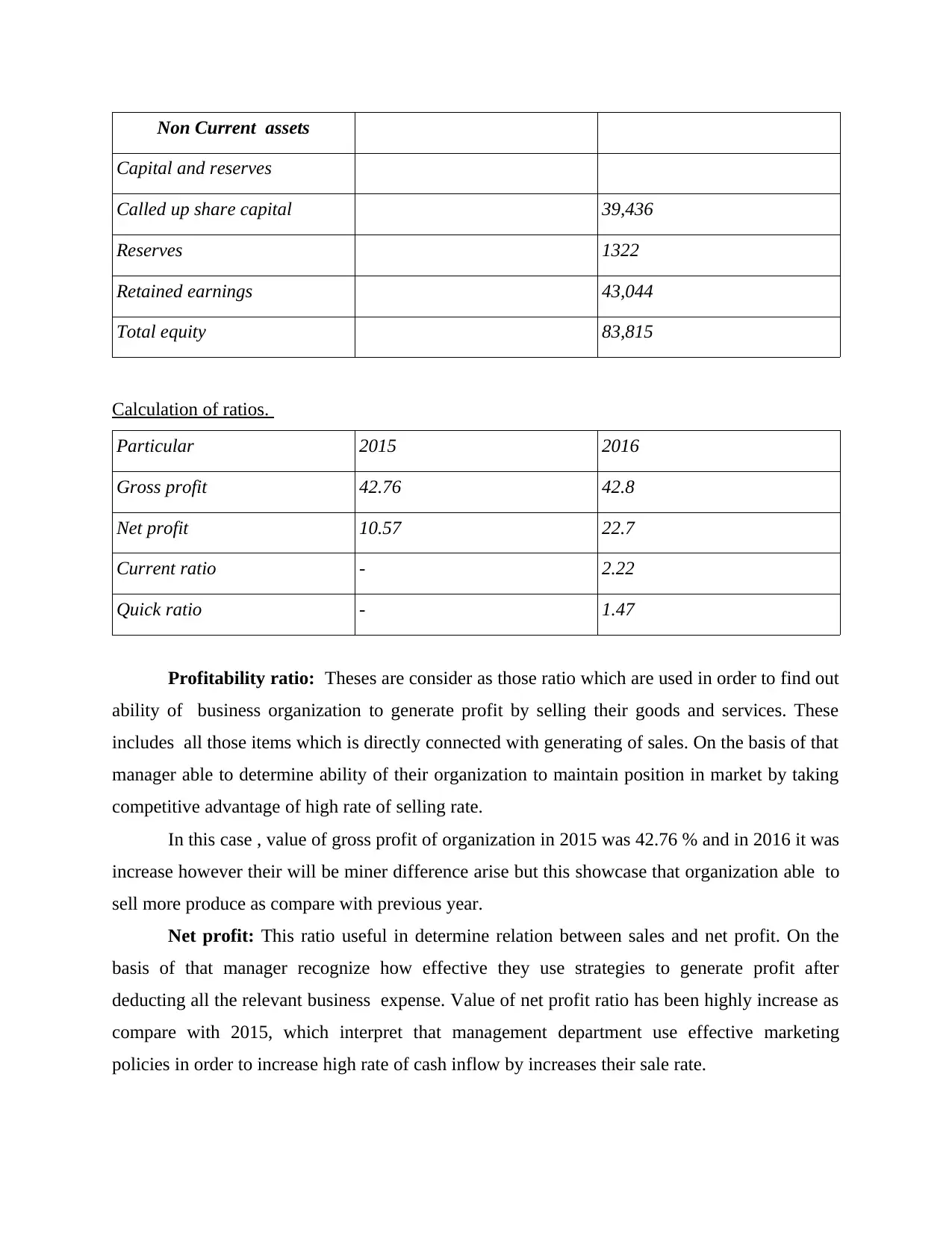

Non Current assets

Capital and reserves

Called up share capital 39,436

Reserves 1322

Retained earnings 43,044

Total equity 83,815

Calculation of ratios.

Particular 2015 2016

Gross profit 42.76 42.8

Net profit 10.57 22.7

Current ratio - 2.22

Quick ratio - 1.47

Profitability ratio: Theses are consider as those ratio which are used in order to find out

ability of business organization to generate profit by selling their goods and services. These

includes all those items which is directly connected with generating of sales. On the basis of that

manager able to determine ability of their organization to maintain position in market by taking

competitive advantage of high rate of selling rate.

In this case , value of gross profit of organization in 2015 was 42.76 % and in 2016 it was

increase however their will be miner difference arise but this showcase that organization able to

sell more produce as compare with previous year.

Net profit: This ratio useful in determine relation between sales and net profit. On the

basis of that manager recognize how effective they use strategies to generate profit after

deducting all the relevant business expense. Value of net profit ratio has been highly increase as

compare with 2015, which interpret that management department use effective marketing

policies in order to increase high rate of cash inflow by increases their sale rate.

Capital and reserves

Called up share capital 39,436

Reserves 1322

Retained earnings 43,044

Total equity 83,815

Calculation of ratios.

Particular 2015 2016

Gross profit 42.76 42.8

Net profit 10.57 22.7

Current ratio - 2.22

Quick ratio - 1.47

Profitability ratio: Theses are consider as those ratio which are used in order to find out

ability of business organization to generate profit by selling their goods and services. These

includes all those items which is directly connected with generating of sales. On the basis of that

manager able to determine ability of their organization to maintain position in market by taking

competitive advantage of high rate of selling rate.

In this case , value of gross profit of organization in 2015 was 42.76 % and in 2016 it was

increase however their will be miner difference arise but this showcase that organization able to

sell more produce as compare with previous year.

Net profit: This ratio useful in determine relation between sales and net profit. On the

basis of that manager recognize how effective they use strategies to generate profit after

deducting all the relevant business expense. Value of net profit ratio has been highly increase as

compare with 2015, which interpret that management department use effective marketing

policies in order to increase high rate of cash inflow by increases their sale rate.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Efficiency ratio: This ratio help in determine efficiency level of organization. On the

basis of that manager able to find out how effective department work in order to achieve goals.

This ratio includes, stock turn over , debtor turn over ratio. On the basis of calculating value of

these ratio ability of paying debt liability and collection of funds from debtors can be define in

systematic manner. High time of payable ratio showcase that organization require more time in

order to collect their funds and on the other side short time period of payment of funds showcase

that organization use effective creditor management policy thus on the basis of that they easily

collect money from their debtor and pay short term liability to creditors.

Liquidity ratio: This ratio is useful in order to find out liquidity rate of organization on

the basis of that manager able to determine liquidity portion of business organization to pay their

short term debt liability. For this purpose current as well as quick ratio is calculated on the basis

of that manager able to find out how much cash and related assets organization have to easily pay

their short term business liability (Vasvári, 2020.).

Current ratio: This ratio is calculated for the purpose of determine relation between

current assets as well as with current liabilities. On the basis of that manager able to evaluate

whether they have ability to maintain ideal current ratio or not. In this case value of current ratio

has been change from 3.44 to 2.22 which means that in 2016 organization maintain their current

assets ineffective manner even though their vale of asst has been decile but it will help in

managing these assets for relevant purpose of business.

Quick ratio: This ratio is part of liquidity ratio which help in finding out time availability

of assets for the purpose of paying and fulfil debt liability by using only cash and cash relevant

assets. Value of quick assets is determine by deducing stock value from theses assets. Value of

quick ratio as determine at 1.47 which is more then ideal ratio however thus mean that

organization have access of cash assets to pay their short term debt ability by using cash capital

of organization.

Shareholder's equity: This ratio useful in determine relation between debt and equity,

on the basis of that ratio and level of of these item in organization can be determine. This ratio

useful in interpret ratio of capital structure in debt as compare with equities. Value of

shareholders equity has been changes from 63,057 to 83815 which means that management

department use effective strategies in order to increase their share capital which is

showcase symbol of of growth of organization as compare with previous year.

basis of that manager able to find out how effective department work in order to achieve goals.

This ratio includes, stock turn over , debtor turn over ratio. On the basis of calculating value of

these ratio ability of paying debt liability and collection of funds from debtors can be define in

systematic manner. High time of payable ratio showcase that organization require more time in

order to collect their funds and on the other side short time period of payment of funds showcase

that organization use effective creditor management policy thus on the basis of that they easily

collect money from their debtor and pay short term liability to creditors.

Liquidity ratio: This ratio is useful in order to find out liquidity rate of organization on

the basis of that manager able to determine liquidity portion of business organization to pay their

short term debt liability. For this purpose current as well as quick ratio is calculated on the basis

of that manager able to find out how much cash and related assets organization have to easily pay

their short term business liability (Vasvári, 2020.).

Current ratio: This ratio is calculated for the purpose of determine relation between

current assets as well as with current liabilities. On the basis of that manager able to evaluate

whether they have ability to maintain ideal current ratio or not. In this case value of current ratio

has been change from 3.44 to 2.22 which means that in 2016 organization maintain their current

assets ineffective manner even though their vale of asst has been decile but it will help in

managing these assets for relevant purpose of business.

Quick ratio: This ratio is part of liquidity ratio which help in finding out time availability

of assets for the purpose of paying and fulfil debt liability by using only cash and cash relevant

assets. Value of quick assets is determine by deducing stock value from theses assets. Value of

quick ratio as determine at 1.47 which is more then ideal ratio however thus mean that

organization have access of cash assets to pay their short term debt ability by using cash capital

of organization.

Shareholder's equity: This ratio useful in determine relation between debt and equity,

on the basis of that ratio and level of of these item in organization can be determine. This ratio

useful in interpret ratio of capital structure in debt as compare with equities. Value of

shareholders equity has been changes from 63,057 to 83815 which means that management

department use effective strategies in order to increase their share capital which is

showcase symbol of of growth of organization as compare with previous year.

SECTION 4

Process business organization use to improve their financial performance.

There are various strategies which manager use in order to enhance financial performance

of organization. Management department on the basis of analysing marketing condition able to

formulate those strategies through which they enhance perforce of organization, some of these

are define below:

Marketing strategies: Manger on the basis of formulating effective marketing strategies

able to attract their target market customers, which help in enhance brand image of business

organization as well as increase sales rate which directly impact on the cash inflow activities.

This'll useful in increase rate of profitability and which beneficial in order to proved growth of

business organization (Young, and Legister, 2018).

Manager on the basis of analysing and evaluating performance of organization able to

generate policies and strategies which useful in enhance rate of profitability of business

organization.

Other strategies: Other then marketing strategies in which by increasing sales rate

manager able to increase their financial performance, organization by minimizing their cost and

cut throat additional expenditure incurred activities able maintain their level of financial

performance and build strong structure of financial capital which is the symbol of growth of

organization.

By using different types of inventory management technique , cost statement , through

applying standard costing method and relevant to of measurement of financial

performance, ,management department of organization able to control or mitigate extra cost

which useful in proved strong base for run future business activities, thus will help in maintain

cash inflow of organization and improve in the performance of organization.

CONCLUSION

From the above analysis it has been concluded that financial management play vital role

ih managing position of organization. As with the use of different technique and tools of

financial management organization able to manage their capital. Manager use this approach for

take relevant or essential business decision as well as understand changes of future business

Process business organization use to improve their financial performance.

There are various strategies which manager use in order to enhance financial performance

of organization. Management department on the basis of analysing marketing condition able to

formulate those strategies through which they enhance perforce of organization, some of these

are define below:

Marketing strategies: Manger on the basis of formulating effective marketing strategies

able to attract their target market customers, which help in enhance brand image of business

organization as well as increase sales rate which directly impact on the cash inflow activities.

This'll useful in increase rate of profitability and which beneficial in order to proved growth of

business organization (Young, and Legister, 2018).

Manager on the basis of analysing and evaluating performance of organization able to

generate policies and strategies which useful in enhance rate of profitability of business

organization.

Other strategies: Other then marketing strategies in which by increasing sales rate

manager able to increase their financial performance, organization by minimizing their cost and

cut throat additional expenditure incurred activities able maintain their level of financial

performance and build strong structure of financial capital which is the symbol of growth of

organization.

By using different types of inventory management technique , cost statement , through

applying standard costing method and relevant to of measurement of financial

performance, ,management department of organization able to control or mitigate extra cost

which useful in proved strong base for run future business activities, thus will help in maintain

cash inflow of organization and improve in the performance of organization.

CONCLUSION

From the above analysis it has been concluded that financial management play vital role

ih managing position of organization. As with the use of different technique and tools of

financial management organization able to manage their capital. Manager use this approach for

take relevant or essential business decision as well as understand changes of future business

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.