Deakin University MAA262 Assignment: Managerial Costing Analysis

VerifiedAdded on 2023/06/09

|14

|2414

|479

Homework Assignment

AI Summary

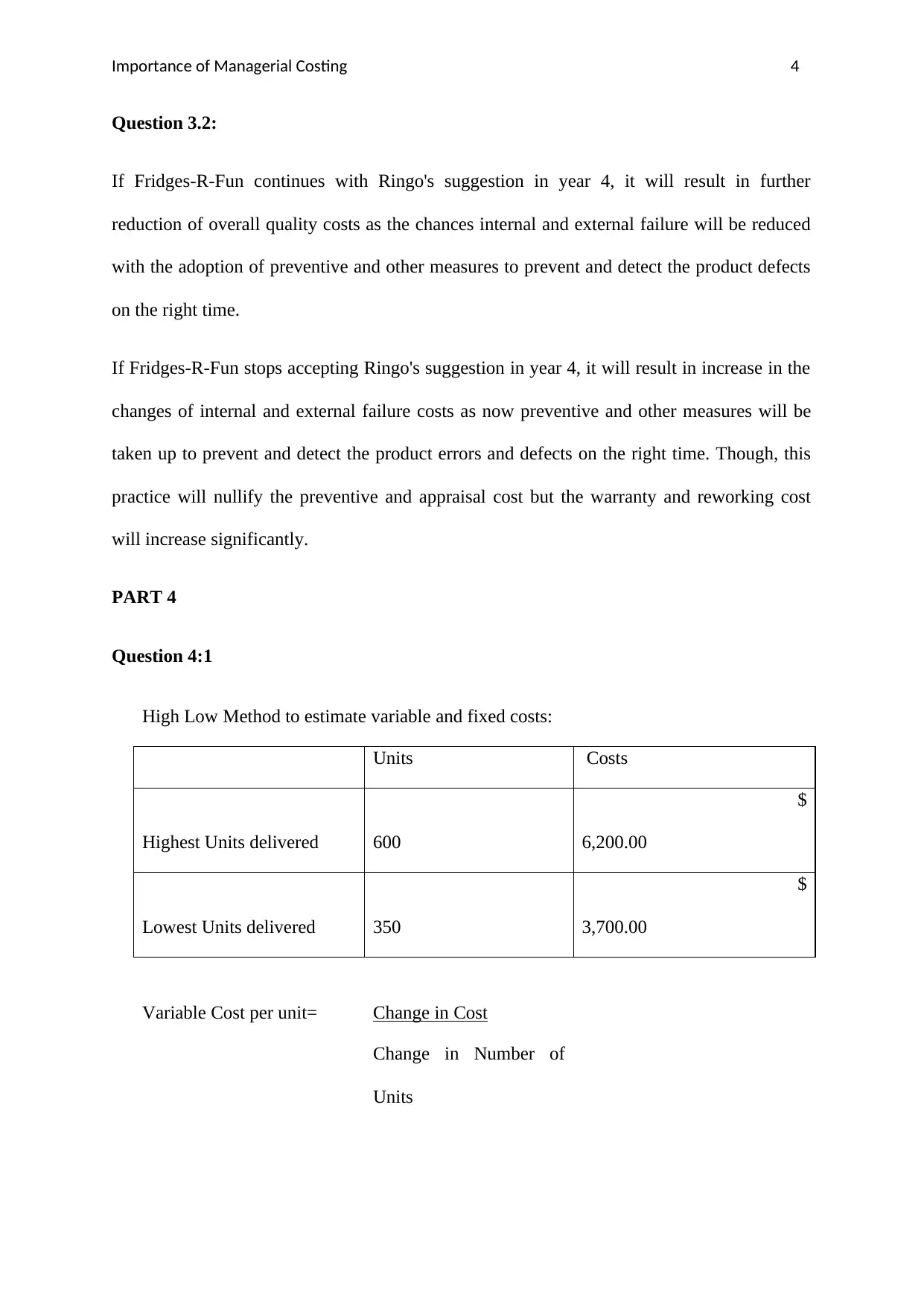

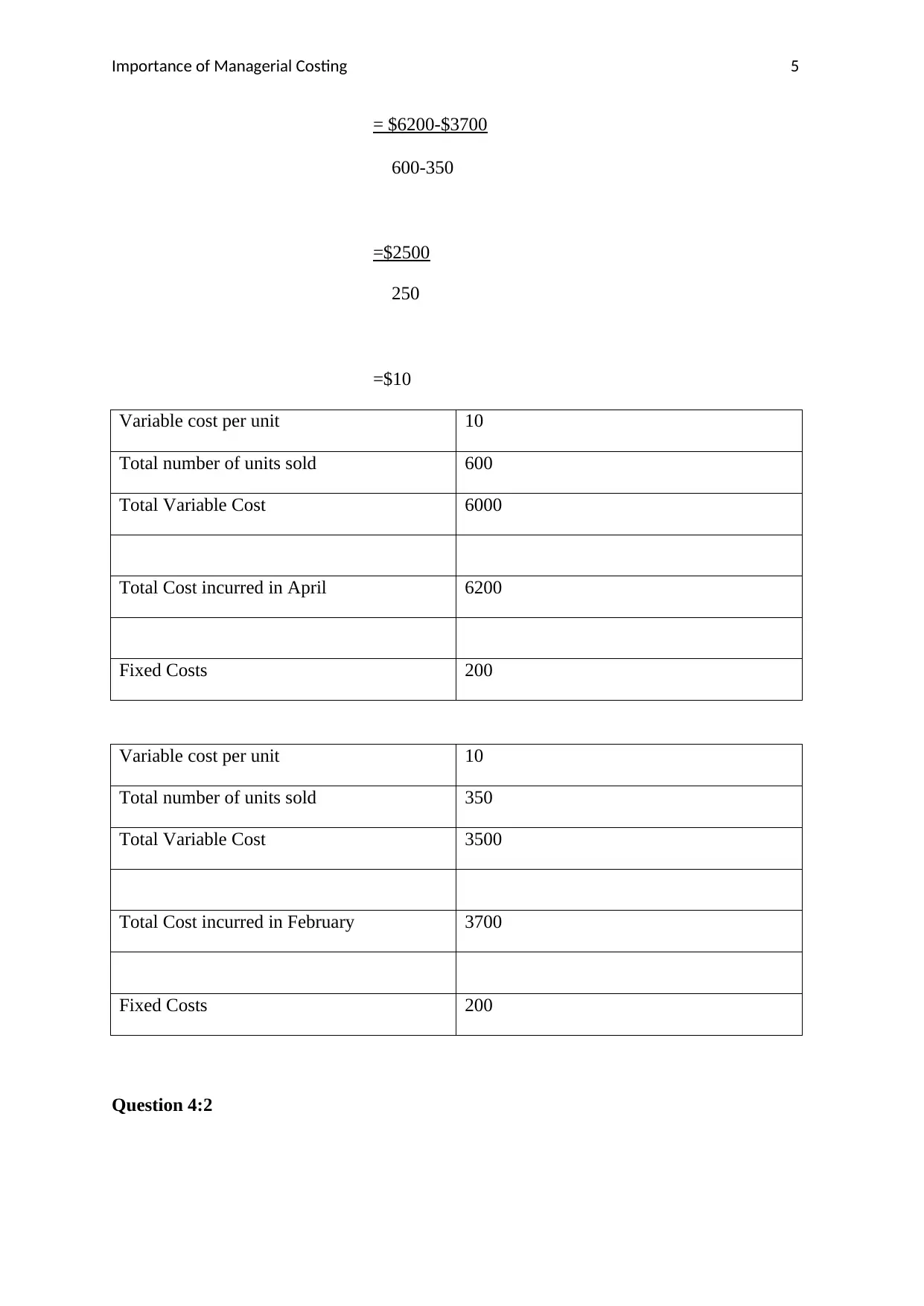

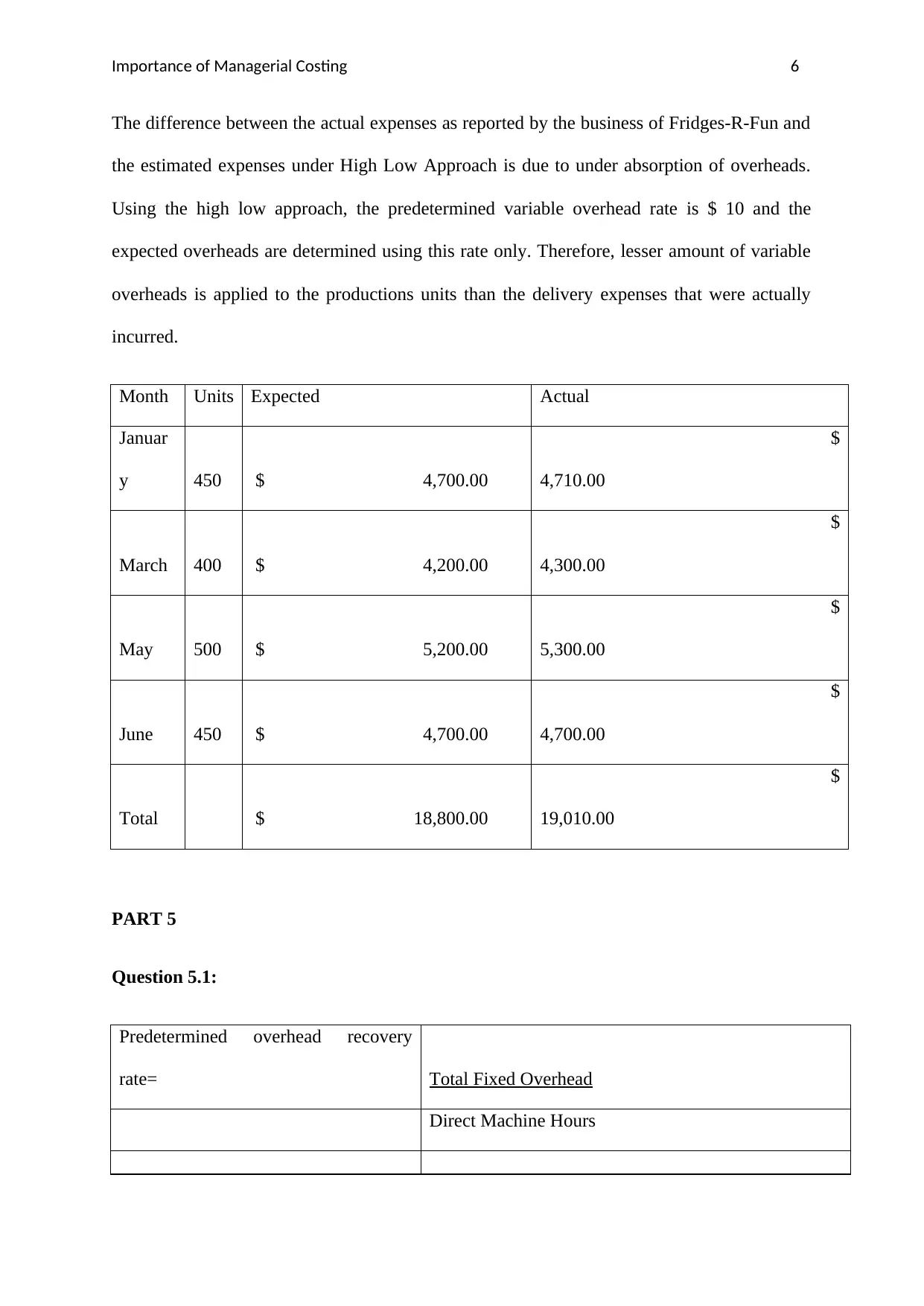

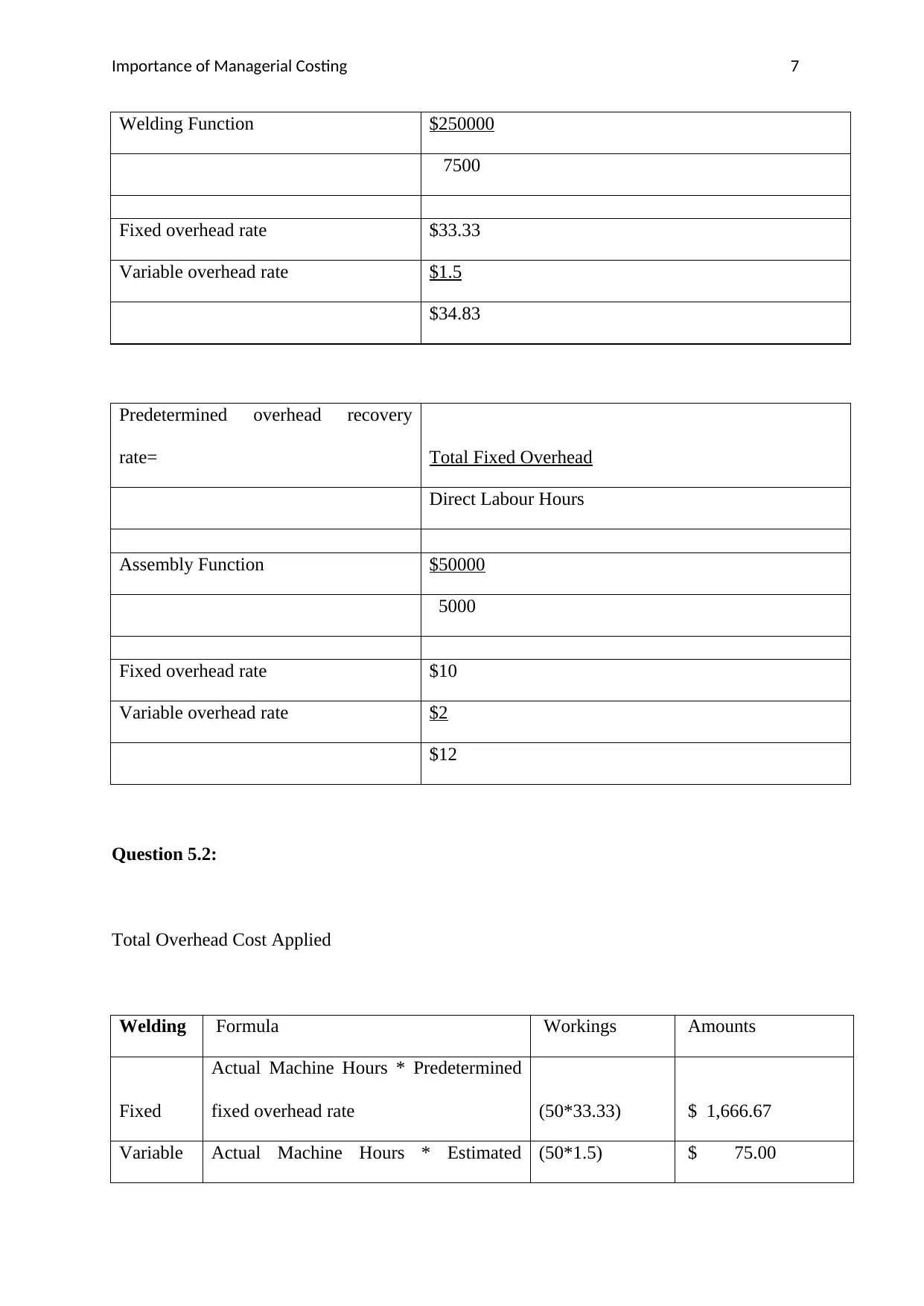

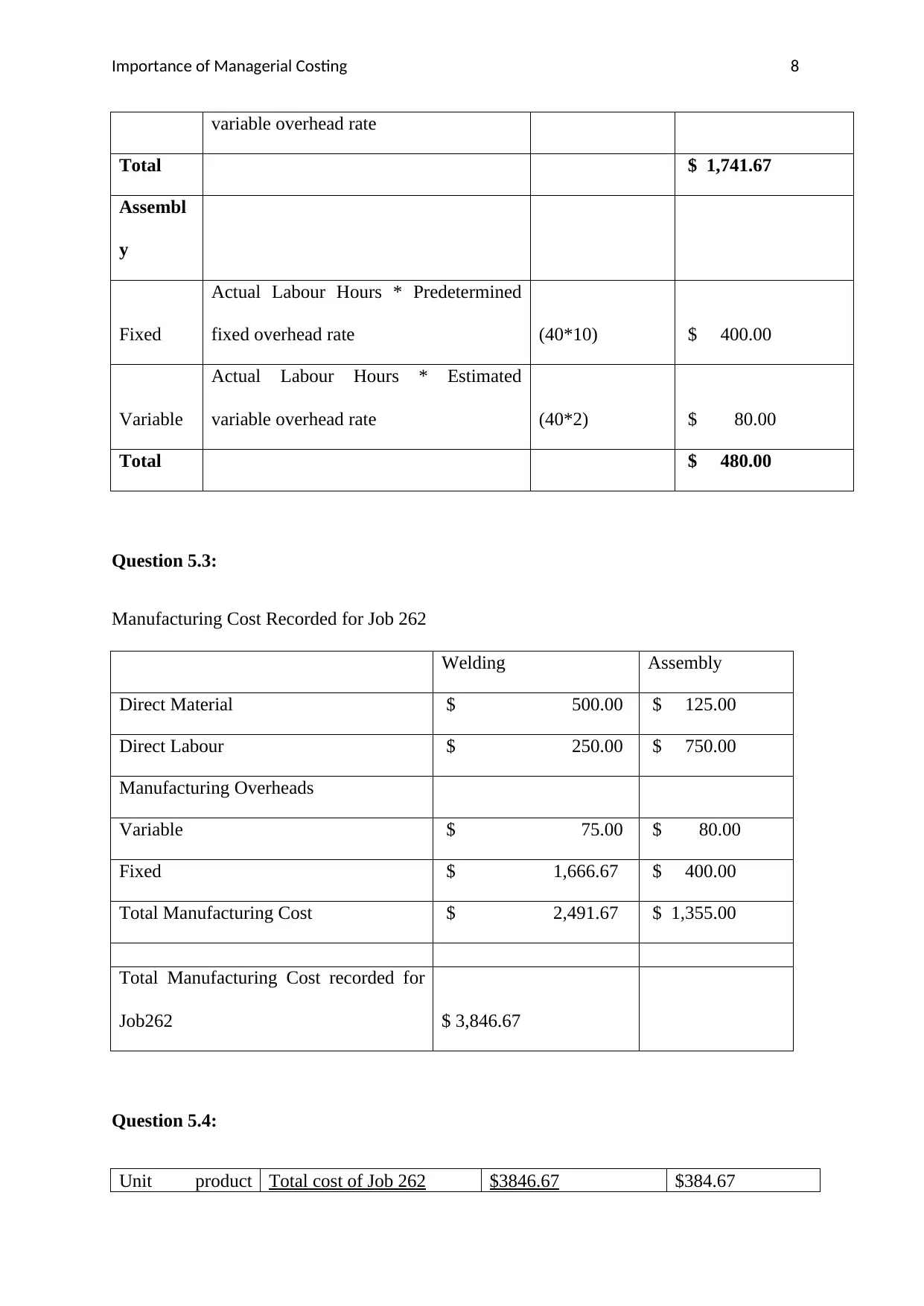

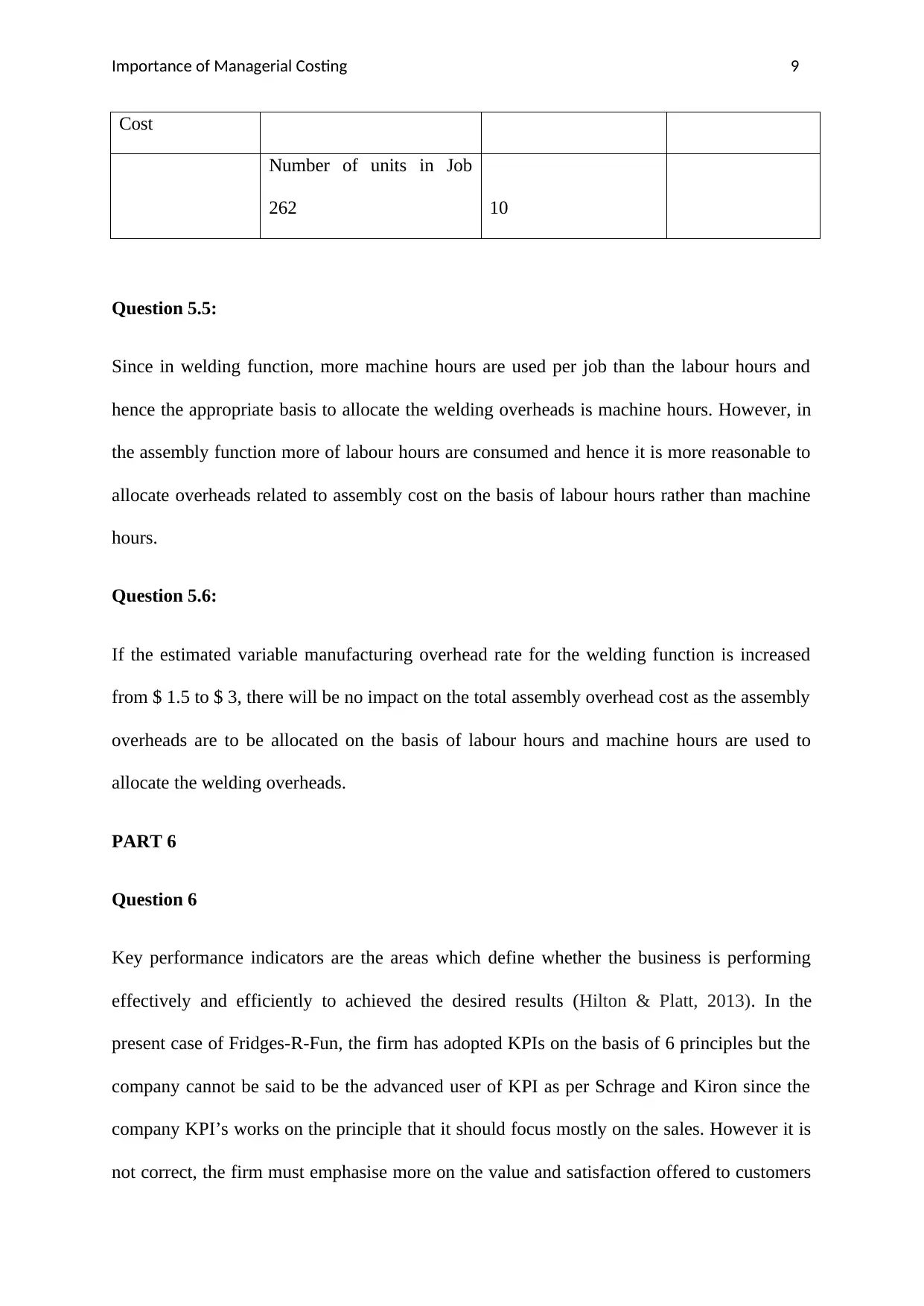

This assignment delves into various aspects of managerial accounting, beginning with ethical considerations for management accountants, specifically addressing competence, confidentiality, integrity, and credibility. It then analyzes quality costs, differentiating between prevention, appraisal, internal failure, and external failure costs, and evaluates the impact of preventive measures on reducing overall quality costs. The assignment explores the High-Low method for estimating fixed and variable costs, followed by an examination of overhead allocation using predetermined rates for both welding and assembly functions. It then assesses key performance indicators (KPIs) and their alignment with business objectives, contrasting cost-plus and value-based pricing strategies. The solution offers detailed calculations, interpretations, and recommendations based on the provided case study of Fridges-R-Fun, including discussions on ethical dilemmas, cost analysis, and strategic decision-making.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.