Applied Business Finance: Financial Analysis and Improvement

VerifiedAdded on 2023/06/13

|12

|2718

|76

Report

AI Summary

This report provides a comprehensive financial analysis of a sample organization, focusing on key aspects of financial management, including financial statement analysis and performance improvement. It begins with an introduction to financial management, highlighting its importance in planning, organizing, and controlling financial activities. The report then discusses the main financial statements—balance sheet, income statement, and cash flow statement—and explains the use of ratios in financial management to assess a company's performance relative to its competitors. A business review template is completed, including an income statement and balance sheet for the sample organization. The analysis covers profitability, liquidity, and efficiency, using ratios such as gross profit margin, net profit margin, current ratio, quick ratio, and asset turnover ratio. The report concludes by discussing processes that businesses can use to improve their financial performance, such as reducing overhead costs and improving accounts receivable collection.

APPLIED BUSINESS

FINANCE

FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Section 1...........................................................................................................................................3

Introduction to the concept of financial management..................................................................3

Importance of financial management...........................................................................................3

Section 2...........................................................................................................................................4

Discussion of main financial statements......................................................................................4

Explanation of the use of ratios in financial management...........................................................5

Section 3...........................................................................................................................................5

I. Completing Business Review Template...................................................................................5

ii. Income Statement for the Sample Organization......................................................................6

iii. Balance sheet..........................................................................................................................7

iv. Description of Profitability, Liquidity and Efficiency of the company..................................8

Section 4...........................................................................................................................................9

Discussion of processes used by business to improve their financial performance....................9

REFERENCES................................................................................................................................1

Section 1...........................................................................................................................................3

Introduction to the concept of financial management..................................................................3

Importance of financial management...........................................................................................3

Section 2...........................................................................................................................................4

Discussion of main financial statements......................................................................................4

Explanation of the use of ratios in financial management...........................................................5

Section 3...........................................................................................................................................5

I. Completing Business Review Template...................................................................................5

ii. Income Statement for the Sample Organization......................................................................6

iii. Balance sheet..........................................................................................................................7

iv. Description of Profitability, Liquidity and Efficiency of the company..................................8

Section 4...........................................................................................................................................9

Discussion of processes used by business to improve their financial performance....................9

REFERENCES................................................................................................................................1

Section 1

Introduction to the concept of financial management

Financial Management (FM) is a process of planning, organizing, directing and controlling the

financial activities of the organization (Enríquez-Díaz, Castro-Santos and Puime-Guillén, 2021).

The financial activities involve procurement of funds and the utilization of funds in the most

appropriate manner so that cost of capital is reduces and return on investment increases. There

are basically three elements of the financial management which are as follows:

Investment decision: This involve the decision regarding the investment in the fixed assets as

well as other investment projects in order to increase the return on investment and cash inflows.

The project with higher return percentage is selected by company for investment purpose.

Basically company can also use the capital budgeting to make the decision regarding the

investment in current assets which is also known as working capital decision (Al Breiki and

Nobanee, 2019).

Financing decision: This is another element of financial management which state the source of

finance from where company can acquire funds from the market. The sources of finance include

debenture, equity, retained earnings and bank loan. The source of finance having lowest cost of

capital are selected for the fulfilling capital requirement.

Dividend decision: This is one of the significant part of financial management in which

company’s manager need to make the decision regarding whether to distribute earnings available

for shareholders to shareholders or retained it within the organization for future development.

The net profit is divided into either dividend or retained profit or both.

Importance of financial management

Managing finance is considered to be an art and the ability of managers in doing so is very

necessary for the success of the business organization due to the following importance of

financial management:

It aids in financial planning, fund acquisition from different sources and investing the

same in appropriate manner (Ginting, 2021).

Financial management ensures incurring of minimum cost along with earning maximum

profits by reducing production delays, enhancing organizational efficiency, lowering the

cost of fund by acquiring and investing it in an appropriate manner.

Introduction to the concept of financial management

Financial Management (FM) is a process of planning, organizing, directing and controlling the

financial activities of the organization (Enríquez-Díaz, Castro-Santos and Puime-Guillén, 2021).

The financial activities involve procurement of funds and the utilization of funds in the most

appropriate manner so that cost of capital is reduces and return on investment increases. There

are basically three elements of the financial management which are as follows:

Investment decision: This involve the decision regarding the investment in the fixed assets as

well as other investment projects in order to increase the return on investment and cash inflows.

The project with higher return percentage is selected by company for investment purpose.

Basically company can also use the capital budgeting to make the decision regarding the

investment in current assets which is also known as working capital decision (Al Breiki and

Nobanee, 2019).

Financing decision: This is another element of financial management which state the source of

finance from where company can acquire funds from the market. The sources of finance include

debenture, equity, retained earnings and bank loan. The source of finance having lowest cost of

capital are selected for the fulfilling capital requirement.

Dividend decision: This is one of the significant part of financial management in which

company’s manager need to make the decision regarding whether to distribute earnings available

for shareholders to shareholders or retained it within the organization for future development.

The net profit is divided into either dividend or retained profit or both.

Importance of financial management

Managing finance is considered to be an art and the ability of managers in doing so is very

necessary for the success of the business organization due to the following importance of

financial management:

It aids in financial planning, fund acquisition from different sources and investing the

same in appropriate manner (Ginting, 2021).

Financial management ensures incurring of minimum cost along with earning maximum

profits by reducing production delays, enhancing organizational efficiency, lowering the

cost of fund by acquiring and investing it in an appropriate manner.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

By having appropriate financial management in place, businesses are able to take

financial decisions accurately which leads to increased shareholder's wealth. This is

because financial management helps in controlling various aspects of business related to

finance and also generates relevant information through ensuring financial reporting from

time to time which make managers aware of how efficiently they need to utilize funds.

Section 2

Discussion of main financial statements

Financial statements can be defined as the reports that businesses prepared in order to

display their financial activities with reference to a particular accounting period. Accordingly, a

clear view of how a business is carrying out its activities and able to maintain its liquidity,

solvency and efficiency (Osadchy and et.al., 2018). Also, how well a firm is doing can be

determined through financial statements only. There are majorly three types of financial

statements that almost all businesses used to prepare, such as the following:

Balance sheet: It is also known as the statement of financial position. It provides information

regarding book value of company's equity, assets and liabilities. Investors usually look at the

balance sheet of the company in order to evaluate the financial position of business. A snapshot

of what a business owes and owns can be obtained through balance sheet as on the reporting

date. There are five sections that one can find within the balance sheet that is, current assets, non-

current assets, current liabilities, non-current liabilities and equity held by a business at a

particular point of time. It is necessary as per the accounting equation that total balance of assets

must be equals to the equity and liabilities within the business.

Income statement: This financial statement gives a list of income earned and expenditures

incurred by business during a particular accounting period for which the statement has been

prepared (Hasanaj and Kuqi, 2019). It can be determined through this statement that whether a

business is incurring losses or making profit which helps in knowing the financial performance

of a concern. Investor uses this statement to determine business's profitability to understand that

whether they would be able to get their desired return by investing in it or not.

Cash flow statement: From this statement, activities involving cash exchanging are shown which

gives overall view of the liquidity of business. All the outflows and inflows of cash over the

period for which the statement has been prepared are reported here. The statement is broken

down into three sections that is, investing, operating and financing activities. After compiling

financial decisions accurately which leads to increased shareholder's wealth. This is

because financial management helps in controlling various aspects of business related to

finance and also generates relevant information through ensuring financial reporting from

time to time which make managers aware of how efficiently they need to utilize funds.

Section 2

Discussion of main financial statements

Financial statements can be defined as the reports that businesses prepared in order to

display their financial activities with reference to a particular accounting period. Accordingly, a

clear view of how a business is carrying out its activities and able to maintain its liquidity,

solvency and efficiency (Osadchy and et.al., 2018). Also, how well a firm is doing can be

determined through financial statements only. There are majorly three types of financial

statements that almost all businesses used to prepare, such as the following:

Balance sheet: It is also known as the statement of financial position. It provides information

regarding book value of company's equity, assets and liabilities. Investors usually look at the

balance sheet of the company in order to evaluate the financial position of business. A snapshot

of what a business owes and owns can be obtained through balance sheet as on the reporting

date. There are five sections that one can find within the balance sheet that is, current assets, non-

current assets, current liabilities, non-current liabilities and equity held by a business at a

particular point of time. It is necessary as per the accounting equation that total balance of assets

must be equals to the equity and liabilities within the business.

Income statement: This financial statement gives a list of income earned and expenditures

incurred by business during a particular accounting period for which the statement has been

prepared (Hasanaj and Kuqi, 2019). It can be determined through this statement that whether a

business is incurring losses or making profit which helps in knowing the financial performance

of a concern. Investor uses this statement to determine business's profitability to understand that

whether they would be able to get their desired return by investing in it or not.

Cash flow statement: From this statement, activities involving cash exchanging are shown which

gives overall view of the liquidity of business. All the outflows and inflows of cash over the

period for which the statement has been prepared are reported here. The statement is broken

down into three sections that is, investing, operating and financing activities. After compiling

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

cash from generated or used within these activities, net increase or decrease in cash balance is

shown (Yang, Uy and Huang, 2020). At the end of this statement, cash balance held by the

business at the end of reporting period is stated which depicts current liquidity position of the

business.

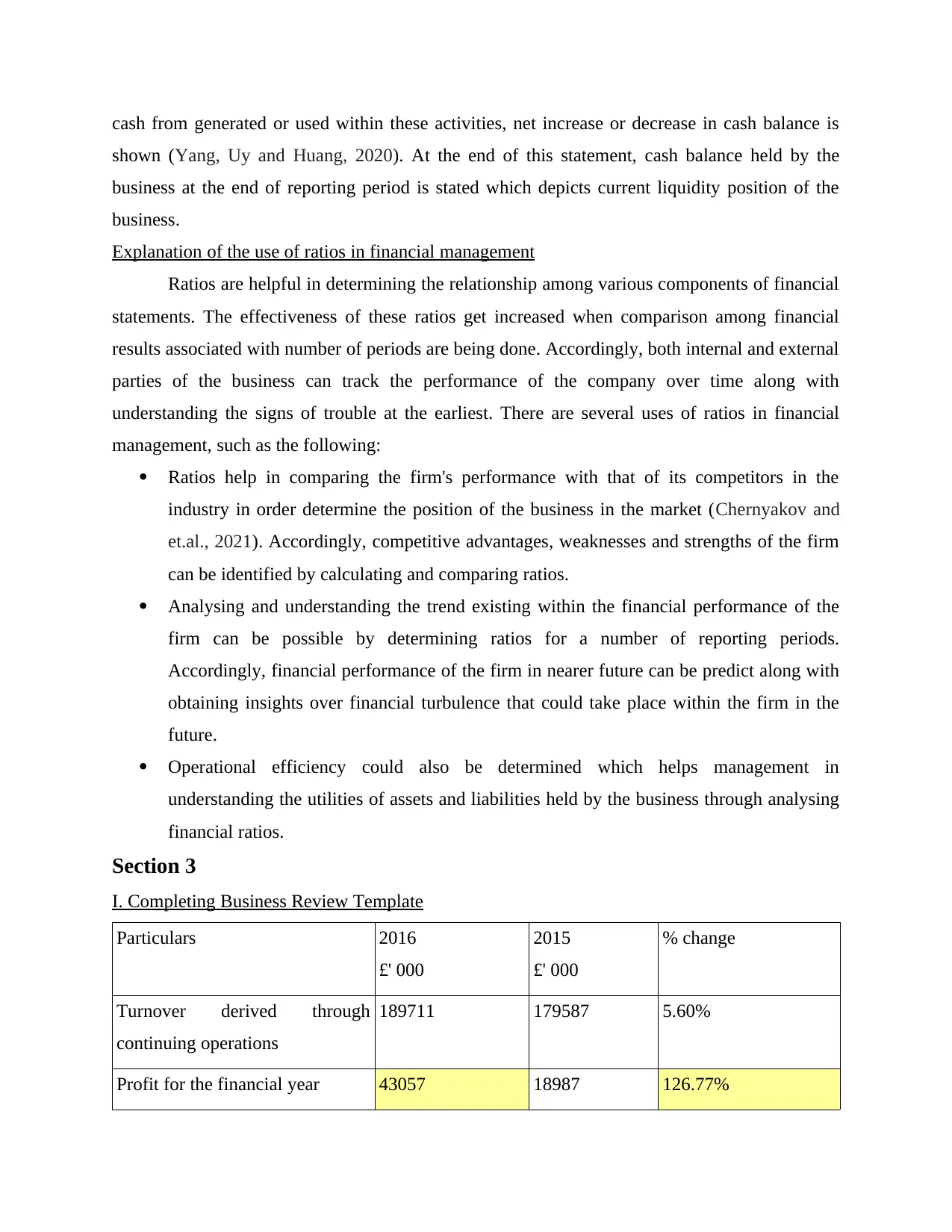

Explanation of the use of ratios in financial management

Ratios are helpful in determining the relationship among various components of financial

statements. The effectiveness of these ratios get increased when comparison among financial

results associated with number of periods are being done. Accordingly, both internal and external

parties of the business can track the performance of the company over time along with

understanding the signs of trouble at the earliest. There are several uses of ratios in financial

management, such as the following:

Ratios help in comparing the firm's performance with that of its competitors in the

industry in order determine the position of the business in the market (Chernyakov and

et.al., 2021). Accordingly, competitive advantages, weaknesses and strengths of the firm

can be identified by calculating and comparing ratios.

Analysing and understanding the trend existing within the financial performance of the

firm can be possible by determining ratios for a number of reporting periods.

Accordingly, financial performance of the firm in nearer future can be predict along with

obtaining insights over financial turbulence that could take place within the firm in the

future.

Operational efficiency could also be determined which helps management in

understanding the utilities of assets and liabilities held by the business through analysing

financial ratios.

Section 3

I. Completing Business Review Template

Particulars 2016

£' 000

2015

£' 000

% change

Turnover derived through

continuing operations

189711 179587 5.60%

Profit for the financial year 43057 18987 126.77%

shown (Yang, Uy and Huang, 2020). At the end of this statement, cash balance held by the

business at the end of reporting period is stated which depicts current liquidity position of the

business.

Explanation of the use of ratios in financial management

Ratios are helpful in determining the relationship among various components of financial

statements. The effectiveness of these ratios get increased when comparison among financial

results associated with number of periods are being done. Accordingly, both internal and external

parties of the business can track the performance of the company over time along with

understanding the signs of trouble at the earliest. There are several uses of ratios in financial

management, such as the following:

Ratios help in comparing the firm's performance with that of its competitors in the

industry in order determine the position of the business in the market (Chernyakov and

et.al., 2021). Accordingly, competitive advantages, weaknesses and strengths of the firm

can be identified by calculating and comparing ratios.

Analysing and understanding the trend existing within the financial performance of the

firm can be possible by determining ratios for a number of reporting periods.

Accordingly, financial performance of the firm in nearer future can be predict along with

obtaining insights over financial turbulence that could take place within the firm in the

future.

Operational efficiency could also be determined which helps management in

understanding the utilities of assets and liabilities held by the business through analysing

financial ratios.

Section 3

I. Completing Business Review Template

Particulars 2016

£' 000

2015

£' 000

% change

Turnover derived through

continuing operations

189711 179587 5.60%

Profit for the financial year 43057 18987 126.77%

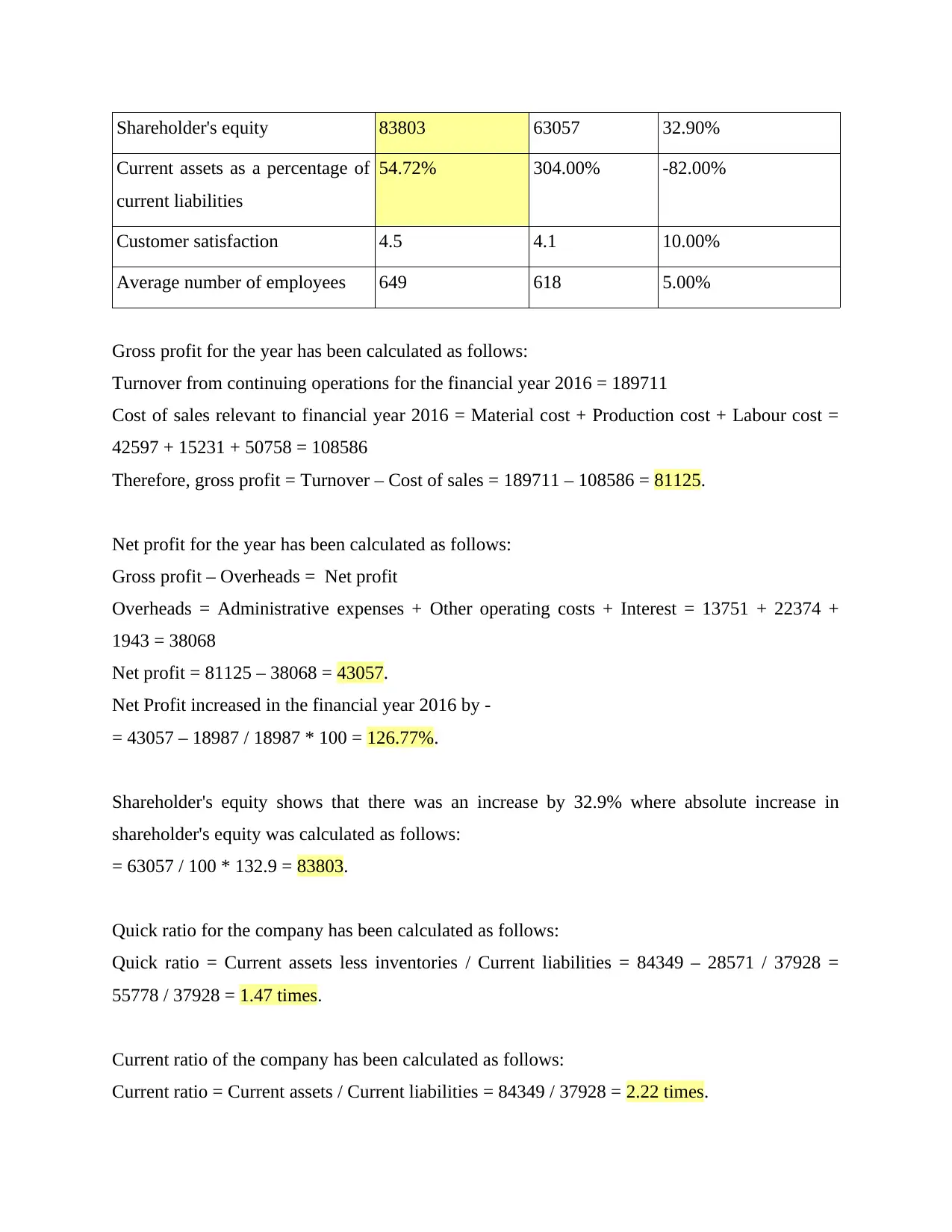

Shareholder's equity 83803 63057 32.90%

Current assets as a percentage of

current liabilities

54.72% 304.00% -82.00%

Customer satisfaction 4.5 4.1 10.00%

Average number of employees 649 618 5.00%

Gross profit for the year has been calculated as follows:

Turnover from continuing operations for the financial year 2016 = 189711

Cost of sales relevant to financial year 2016 = Material cost + Production cost + Labour cost =

42597 + 15231 + 50758 = 108586

Therefore, gross profit = Turnover – Cost of sales = 189711 – 108586 = 81125.

Net profit for the year has been calculated as follows:

Gross profit – Overheads = Net profit

Overheads = Administrative expenses + Other operating costs + Interest = 13751 + 22374 +

1943 = 38068

Net profit = 81125 – 38068 = 43057.

Net Profit increased in the financial year 2016 by -

= 43057 – 18987 / 18987 * 100 = 126.77%.

Shareholder's equity shows that there was an increase by 32.9% where absolute increase in

shareholder's equity was calculated as follows:

= 63057 / 100 * 132.9 = 83803.

Quick ratio for the company has been calculated as follows:

Quick ratio = Current assets less inventories / Current liabilities = 84349 – 28571 / 37928 =

55778 / 37928 = 1.47 times.

Current ratio of the company has been calculated as follows:

Current ratio = Current assets / Current liabilities = 84349 / 37928 = 2.22 times.

Current assets as a percentage of

current liabilities

54.72% 304.00% -82.00%

Customer satisfaction 4.5 4.1 10.00%

Average number of employees 649 618 5.00%

Gross profit for the year has been calculated as follows:

Turnover from continuing operations for the financial year 2016 = 189711

Cost of sales relevant to financial year 2016 = Material cost + Production cost + Labour cost =

42597 + 15231 + 50758 = 108586

Therefore, gross profit = Turnover – Cost of sales = 189711 – 108586 = 81125.

Net profit for the year has been calculated as follows:

Gross profit – Overheads = Net profit

Overheads = Administrative expenses + Other operating costs + Interest = 13751 + 22374 +

1943 = 38068

Net profit = 81125 – 38068 = 43057.

Net Profit increased in the financial year 2016 by -

= 43057 – 18987 / 18987 * 100 = 126.77%.

Shareholder's equity shows that there was an increase by 32.9% where absolute increase in

shareholder's equity was calculated as follows:

= 63057 / 100 * 132.9 = 83803.

Quick ratio for the company has been calculated as follows:

Quick ratio = Current assets less inventories / Current liabilities = 84349 – 28571 / 37928 =

55778 / 37928 = 1.47 times.

Current ratio of the company has been calculated as follows:

Current ratio = Current assets / Current liabilities = 84349 / 37928 = 2.22 times.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ii. Income Statement for the Sample Organization

Attached in Appendix

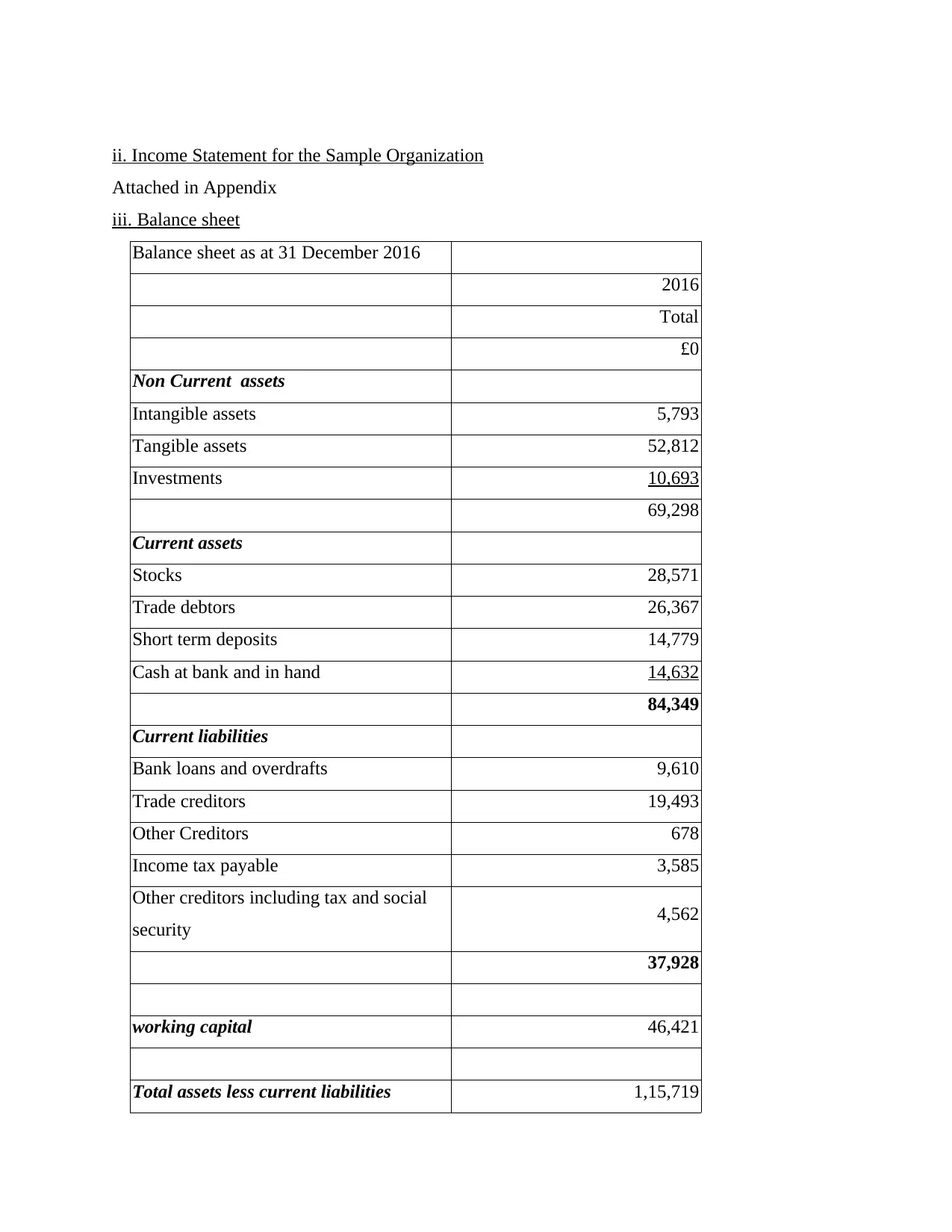

iii. Balance sheet

Balance sheet as at 31 December 2016

2016

Total

£0

Non Current assets

Intangible assets 5,793

Tangible assets 52,812

Investments 10,693

69,298

Current assets

Stocks 28,571

Trade debtors 26,367

Short term deposits 14,779

Cash at bank and in hand 14,632

84,349

Current liabilities

Bank loans and overdrafts 9,610

Trade creditors 19,493

Other Creditors 678

Income tax payable 3,585

Other creditors including tax and social

security 4,562

37,928

working capital 46,421

Total assets less current liabilities 1,15,719

Attached in Appendix

iii. Balance sheet

Balance sheet as at 31 December 2016

2016

Total

£0

Non Current assets

Intangible assets 5,793

Tangible assets 52,812

Investments 10,693

69,298

Current assets

Stocks 28,571

Trade debtors 26,367

Short term deposits 14,779

Cash at bank and in hand 14,632

84,349

Current liabilities

Bank loans and overdrafts 9,610

Trade creditors 19,493

Other Creditors 678

Income tax payable 3,585

Other creditors including tax and social

security 4,562

37,928

working capital 46,421

Total assets less current liabilities 1,15,719

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

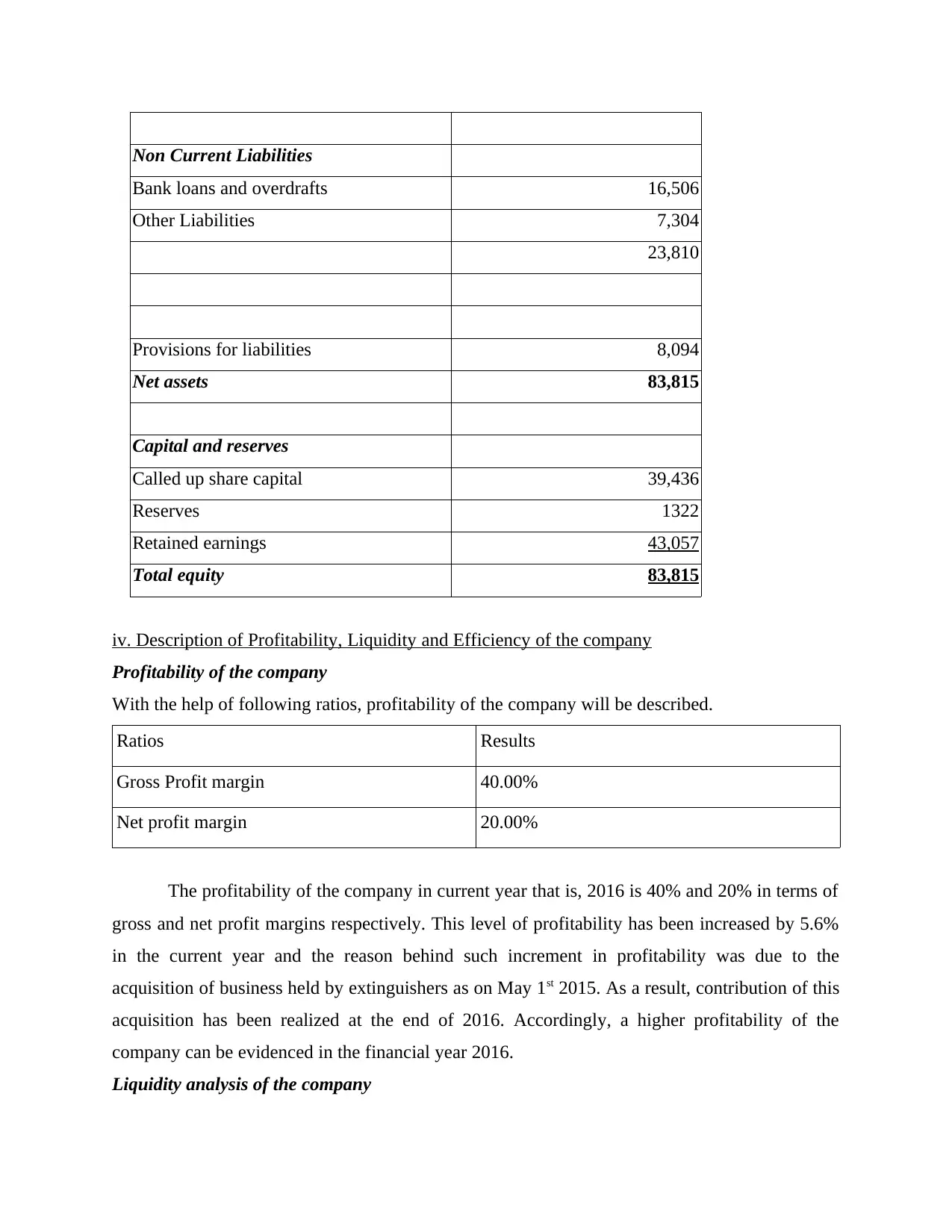

Non Current Liabilities

Bank loans and overdrafts 16,506

Other Liabilities 7,304

23,810

Provisions for liabilities 8,094

Net assets 83,815

Capital and reserves

Called up share capital 39,436

Reserves 1322

Retained earnings 43,057

Total equity 83,815

iv. Description of Profitability, Liquidity and Efficiency of the company

Profitability of the company

With the help of following ratios, profitability of the company will be described.

Ratios Results

Gross Profit margin 40.00%

Net profit margin 20.00%

The profitability of the company in current year that is, 2016 is 40% and 20% in terms of

gross and net profit margins respectively. This level of profitability has been increased by 5.6%

in the current year and the reason behind such increment in profitability was due to the

acquisition of business held by extinguishers as on May 1st 2015. As a result, contribution of this

acquisition has been realized at the end of 2016. Accordingly, a higher profitability of the

company can be evidenced in the financial year 2016.

Liquidity analysis of the company

Bank loans and overdrafts 16,506

Other Liabilities 7,304

23,810

Provisions for liabilities 8,094

Net assets 83,815

Capital and reserves

Called up share capital 39,436

Reserves 1322

Retained earnings 43,057

Total equity 83,815

iv. Description of Profitability, Liquidity and Efficiency of the company

Profitability of the company

With the help of following ratios, profitability of the company will be described.

Ratios Results

Gross Profit margin 40.00%

Net profit margin 20.00%

The profitability of the company in current year that is, 2016 is 40% and 20% in terms of

gross and net profit margins respectively. This level of profitability has been increased by 5.6%

in the current year and the reason behind such increment in profitability was due to the

acquisition of business held by extinguishers as on May 1st 2015. As a result, contribution of this

acquisition has been realized at the end of 2016. Accordingly, a higher profitability of the

company can be evidenced in the financial year 2016.

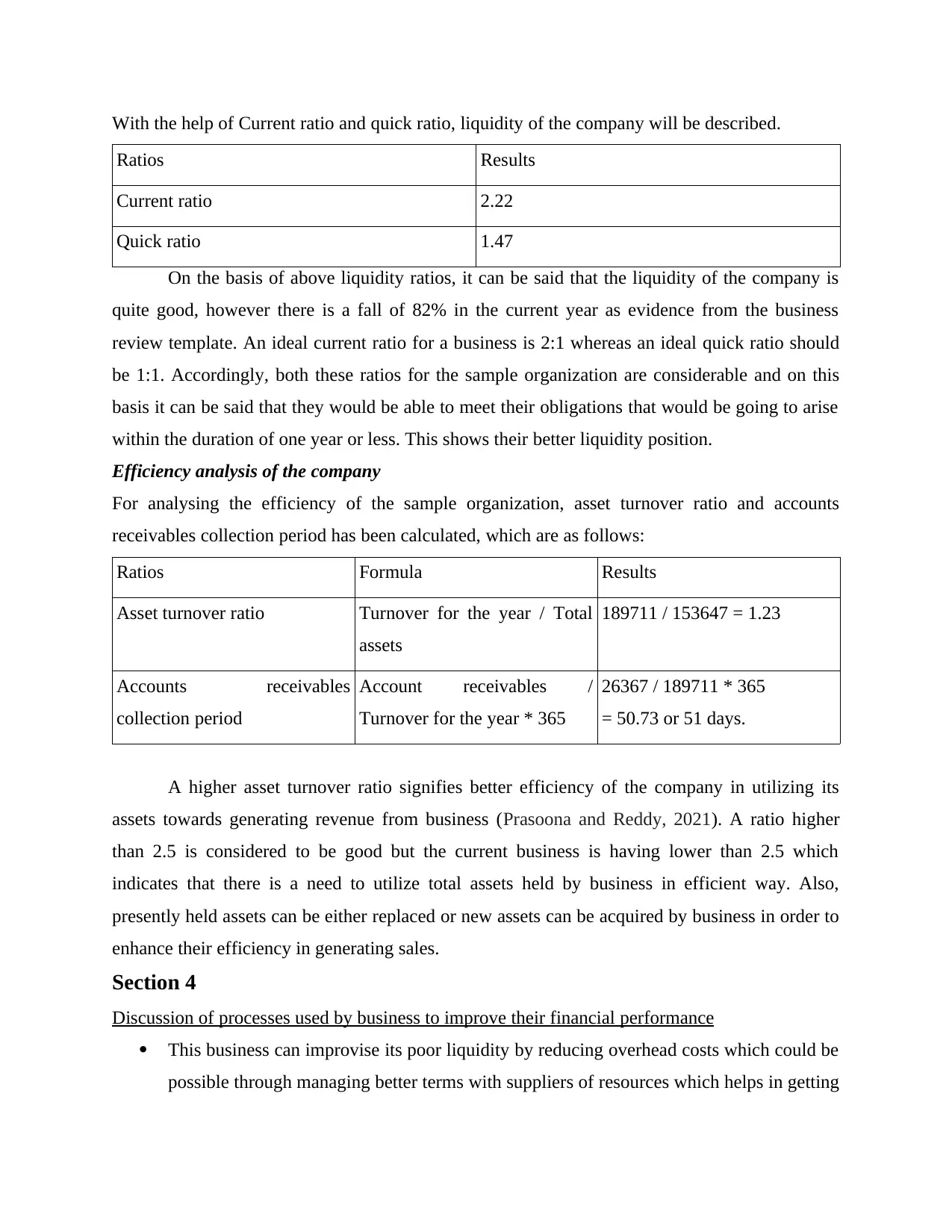

Liquidity analysis of the company

With the help of Current ratio and quick ratio, liquidity of the company will be described.

Ratios Results

Current ratio 2.22

Quick ratio 1.47

On the basis of above liquidity ratios, it can be said that the liquidity of the company is

quite good, however there is a fall of 82% in the current year as evidence from the business

review template. An ideal current ratio for a business is 2:1 whereas an ideal quick ratio should

be 1:1. Accordingly, both these ratios for the sample organization are considerable and on this

basis it can be said that they would be able to meet their obligations that would be going to arise

within the duration of one year or less. This shows their better liquidity position.

Efficiency analysis of the company

For analysing the efficiency of the sample organization, asset turnover ratio and accounts

receivables collection period has been calculated, which are as follows:

Ratios Formula Results

Asset turnover ratio Turnover for the year / Total

assets

189711 / 153647 = 1.23

Accounts receivables

collection period

Account receivables /

Turnover for the year * 365

26367 / 189711 * 365

= 50.73 or 51 days.

A higher asset turnover ratio signifies better efficiency of the company in utilizing its

assets towards generating revenue from business (Prasoona and Reddy, 2021). A ratio higher

than 2.5 is considered to be good but the current business is having lower than 2.5 which

indicates that there is a need to utilize total assets held by business in efficient way. Also,

presently held assets can be either replaced or new assets can be acquired by business in order to

enhance their efficiency in generating sales.

Section 4

Discussion of processes used by business to improve their financial performance

This business can improvise its poor liquidity by reducing overhead costs which could be

possible through managing better terms with suppliers of resources which helps in getting

Ratios Results

Current ratio 2.22

Quick ratio 1.47

On the basis of above liquidity ratios, it can be said that the liquidity of the company is

quite good, however there is a fall of 82% in the current year as evidence from the business

review template. An ideal current ratio for a business is 2:1 whereas an ideal quick ratio should

be 1:1. Accordingly, both these ratios for the sample organization are considerable and on this

basis it can be said that they would be able to meet their obligations that would be going to arise

within the duration of one year or less. This shows their better liquidity position.

Efficiency analysis of the company

For analysing the efficiency of the sample organization, asset turnover ratio and accounts

receivables collection period has been calculated, which are as follows:

Ratios Formula Results

Asset turnover ratio Turnover for the year / Total

assets

189711 / 153647 = 1.23

Accounts receivables

collection period

Account receivables /

Turnover for the year * 365

26367 / 189711 * 365

= 50.73 or 51 days.

A higher asset turnover ratio signifies better efficiency of the company in utilizing its

assets towards generating revenue from business (Prasoona and Reddy, 2021). A ratio higher

than 2.5 is considered to be good but the current business is having lower than 2.5 which

indicates that there is a need to utilize total assets held by business in efficient way. Also,

presently held assets can be either replaced or new assets can be acquired by business in order to

enhance their efficiency in generating sales.

Section 4

Discussion of processes used by business to improve their financial performance

This business can improvise its poor liquidity by reducing overhead costs which could be

possible through managing better terms with suppliers of resources which helps in getting

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

cheaper alternatives. Also, by offering discounts and offers, earlier payment could be

realized from receivables which is helpful in resolving the issue of liquidity crisis

prevailing in the business (Purba and Bimantara, 2020). This leads to lower dependence

on external sources for financing day to day operations of the business and accordingly,

financial costs associated with it can be reduced. All this processes when kept in place, a

higher cash balances with the business can be maintained which would be helpful for the

business in improving their liquidity ratios.

realized from receivables which is helpful in resolving the issue of liquidity crisis

prevailing in the business (Purba and Bimantara, 2020). This leads to lower dependence

on external sources for financing day to day operations of the business and accordingly,

financial costs associated with it can be reduced. All this processes when kept in place, a

higher cash balances with the business can be maintained which would be helpful for the

business in improving their liquidity ratios.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Furthermore, those assets that are no more useful for the business can be sold to make

arrangement for liquidity rather than arranging funds from external sources to finance

asset acquisition. This leads to improvement in efficiency of the business as well due to

acquiring efficient asset by disposing off old one.

Business can also raise or reduce the prices of its product offerings depending upon the

market situation. By doing so, market share can be enhanced which leads to higher

profitability for the business (Bondarenko and et.al., 2018).

At last, using internally generated funds such as equity and retained earnings rather than

funds acquired from external sources would be helpful for the business in eliminating the

additional costs it is incurring towards making payment of interest related expenses and

financial risk as well.

arrangement for liquidity rather than arranging funds from external sources to finance

asset acquisition. This leads to improvement in efficiency of the business as well due to

acquiring efficient asset by disposing off old one.

Business can also raise or reduce the prices of its product offerings depending upon the

market situation. By doing so, market share can be enhanced which leads to higher

profitability for the business (Bondarenko and et.al., 2018).

At last, using internally generated funds such as equity and retained earnings rather than

funds acquired from external sources would be helpful for the business in eliminating the

additional costs it is incurring towards making payment of interest related expenses and

financial risk as well.

REFERENCES

Al Breiki, M. and Nobanee, H., 2019. The role of financial management in promoting

sustainable business practices and development. Available at SSRN 3472404.

Bondarenko, V. A., and et.al., 2018. Financial and marketing monitoring in power selling

sector. European Research Studies, 21, pp.806-813.

Chernyakov, M., and et.al., 2021. The current state of the theory of financial stability. Deutsche

Internationale Zeitschrift für zeitgenössische Wissenschaft, (9-2), pp.16-18.

Enríquez-Díaz, J., Castro-Santos, L. and Puime-Guillén, F. eds., 2021. Financial management

and risk analysis strategies for business sustainability. IGI Global.

Ginting, E. S., 2021. Ratio-Based Financial Performance Analysis of PT. Mustika Ratu,

Tbk. Enrichment: Journal of Management, 11(2), pp.456-462.

Hasanaj, P. and Kuqi, B., 2019. Analysis of financial statements. Humanities and Social Science

Research, 2(2), pp.p17-p17.

Osadchy, E. A., and et.al., 2018. Financial statements of a company as an information base for

decision-making in a transforming economy.

Prasoona, J. and Reddy, R. G., 2021. Analysis of financial statements. Biotica Research

Today, 3(5), pp.373-375.

Purba, J. H. V. and Bimantara, D., 2020, May. The Influence of Asset Management on Financial

Performance, with Panel Data Analysis. In 2nd International Seminar on Business,

Economics, Social Science and Technology (ISBEST 2019) (pp. 150-155). Atlantis

Press.

Yang, Y., Uy, M. C. S. and Huang, A., 2020. Finbert: A pretrained language model for financial

communications. arXiv preprint arXiv:2006.08097.

1

Al Breiki, M. and Nobanee, H., 2019. The role of financial management in promoting

sustainable business practices and development. Available at SSRN 3472404.

Bondarenko, V. A., and et.al., 2018. Financial and marketing monitoring in power selling

sector. European Research Studies, 21, pp.806-813.

Chernyakov, M., and et.al., 2021. The current state of the theory of financial stability. Deutsche

Internationale Zeitschrift für zeitgenössische Wissenschaft, (9-2), pp.16-18.

Enríquez-Díaz, J., Castro-Santos, L. and Puime-Guillén, F. eds., 2021. Financial management

and risk analysis strategies for business sustainability. IGI Global.

Ginting, E. S., 2021. Ratio-Based Financial Performance Analysis of PT. Mustika Ratu,

Tbk. Enrichment: Journal of Management, 11(2), pp.456-462.

Hasanaj, P. and Kuqi, B., 2019. Analysis of financial statements. Humanities and Social Science

Research, 2(2), pp.p17-p17.

Osadchy, E. A., and et.al., 2018. Financial statements of a company as an information base for

decision-making in a transforming economy.

Prasoona, J. and Reddy, R. G., 2021. Analysis of financial statements. Biotica Research

Today, 3(5), pp.373-375.

Purba, J. H. V. and Bimantara, D., 2020, May. The Influence of Asset Management on Financial

Performance, with Panel Data Analysis. In 2nd International Seminar on Business,

Economics, Social Science and Technology (ISBEST 2019) (pp. 150-155). Atlantis

Press.

Yang, Y., Uy, M. C. S. and Huang, A., 2020. Finbert: A pretrained language model for financial

communications. arXiv preprint arXiv:2006.08097.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.