Management Accounting Report: Enhancing Zylla Company Performance

VerifiedAdded on 2020/06/04

|14

|4942

|59

Report

AI Summary

This report, prepared by a management accounting officer, provides a comprehensive analysis of management accounting practices within the Zylla Company. It begins with an introduction to management accounting and its various types, including cost accounting, job costing, and inventory management systems, highlighting their importance in improving firm performance and achieving sustainable development. The report then delves into the diverse methods of reporting systems used by the company, such as performance reporting, operational reporting, and inventory management reports, emphasizing their role in enhancing profitability and transparency. The core of the report explores costing methods, specifically absorption and marginal costing, demonstrating their application in profit analysis through detailed calculations. Furthermore, the report discusses the advantages and disadvantages of different planning tools and how management accounting can respond to financial problems. The report concludes by summarizing the key findings and recommendations for improving the management operations of the Zylla Company, emphasizing the use of management accounting tools for effective decision-making and sustainable growth.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

From: Management account officer.................................................................................................1

To: General Manager.......................................................................................................................1

Subject: For improving the management operations of the Zylla company. ..................................1

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and its types:.............................................................................1

P2 Diverse methods of reporting system used by the Zylla company:..................................2

M1:.........................................................................................................................................3

D1:..........................................................................................................................................4

TASK 2............................................................................................................................................4

P3 Costing methods used for profit analysis:.........................................................................4

M2:.........................................................................................................................................5

D2:..........................................................................................................................................5

TASK 3............................................................................................................................................6

P4 Advantages and disadvantage of different planning tools:...............................................6

M3:.........................................................................................................................................8

D4:..........................................................................................................................................8

P5 Management accounting to respond financial problems:..................................................9

CONCLUSION ............................................................................................................................10

REFERENCES..............................................................................................................................12

From: Management account officer.................................................................................................1

To: General Manager.......................................................................................................................1

Subject: For improving the management operations of the Zylla company. ..................................1

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and its types:.............................................................................1

P2 Diverse methods of reporting system used by the Zylla company:..................................2

M1:.........................................................................................................................................3

D1:..........................................................................................................................................4

TASK 2............................................................................................................................................4

P3 Costing methods used for profit analysis:.........................................................................4

M2:.........................................................................................................................................5

D2:..........................................................................................................................................5

TASK 3............................................................................................................................................6

P4 Advantages and disadvantage of different planning tools:...............................................6

M3:.........................................................................................................................................8

D4:..........................................................................................................................................8

P5 Management accounting to respond financial problems:..................................................9

CONCLUSION ............................................................................................................................10

REFERENCES..............................................................................................................................12

From: Management account officer

To: General Manager

Subject: For improving the management operations of the Zylla company.

INTRODUCTION

Management accounting is the tool which is used by each firm in order to improve the

performance in an effective manner. With the help of management accounting, Zylla company

can gain the sustainable development. Under this report, various management accounting tool is

defined their advantages for getting the firm development are used. But for gaining the

sustainability, firm makes certain management accounting reports. In this assignment, absorption

and marginal costing methods are used by the firm in order to optimise the profits of the firm.

With the help of budgetary tools, company could perform better (Figge and Hahn, 2013). There

are certain tools that can be used by the Zylla company in order to assess the work so effectively.

However, this can be said that the company needs to make certain tools that can be used by the

firm so that this can gain the sustainable development.

TASK 1

P1 Management accounting and its types:

Management accounting is the process which is used by the firm for making management

accounting reports that could helps the firm for making business decisions effectively. This is the

process of assessing, interpreting and demonstrating of accounting information gathered by

taking help of financial accounting system (Management Accounting, 2017). There are certain

tools that can be used by the firm so that the business can be used by the firm in order to assess

the performance of the firm. With the help of management accounting tool, Zylla company can

effectively use the available resources within the firm.

There are some management accounting tools which are explained hereunder:

Cost accounting system: Cost accounting system is the major tool which are used by the

firm on order to renders the cost efficiency in the firm. However, this is the most effective tool

which are used by the firm in order to lower the per unit cost of production. By using this,

company can eliminate the cost. This is also known as the lean accounting system which is used

by the firm in order to improve the performance. This helps the firm to eliminate the cost

1

To: General Manager

Subject: For improving the management operations of the Zylla company.

INTRODUCTION

Management accounting is the tool which is used by each firm in order to improve the

performance in an effective manner. With the help of management accounting, Zylla company

can gain the sustainable development. Under this report, various management accounting tool is

defined their advantages for getting the firm development are used. But for gaining the

sustainability, firm makes certain management accounting reports. In this assignment, absorption

and marginal costing methods are used by the firm in order to optimise the profits of the firm.

With the help of budgetary tools, company could perform better (Figge and Hahn, 2013). There

are certain tools that can be used by the Zylla company in order to assess the work so effectively.

However, this can be said that the company needs to make certain tools that can be used by the

firm so that this can gain the sustainable development.

TASK 1

P1 Management accounting and its types:

Management accounting is the process which is used by the firm for making management

accounting reports that could helps the firm for making business decisions effectively. This is the

process of assessing, interpreting and demonstrating of accounting information gathered by

taking help of financial accounting system (Management Accounting, 2017). There are certain

tools that can be used by the firm so that the business can be used by the firm in order to assess

the performance of the firm. With the help of management accounting tool, Zylla company can

effectively use the available resources within the firm.

There are some management accounting tools which are explained hereunder:

Cost accounting system: Cost accounting system is the major tool which are used by the

firm on order to renders the cost efficiency in the firm. However, this is the most effective tool

which are used by the firm in order to lower the per unit cost of production. By using this,

company can eliminate the cost. This is also known as the lean accounting system which is used

by the firm in order to improve the performance. This helps the firm to eliminate the cost

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

effectively. Cost accounting system is the best way to make the cost of production so that they

could effectively eliminate the wastage cost.

Job costing system: This is the collection of costs of materials, labour and the overhead

costs for a particular job. Such approach is an effective tool which is used for tracking the

particular costs to the individual jobs and assessing them to oversee if the costs could be limited

in a later jobs. Job costing is implemented to gather costs at a small unit level. This is the

procedure of assigning the costs spends to incur to a particular job when the business is covered

with.

Inventory management system: This is the management system which is used by the

firm to keeps track of its stuff (Zimmerman and Yahya-Zadeh, 2011). This is the tool which can

be used by the firm in order to manage the inventory and also helps the firm to effectively

manage the available resources. By using this system, inventory is optimum used and no wastage

of money occurred.

Price optimisation system: This is an effective tool that can be used by the firm in order

to optimize the price of the product. However, for determining the price is a crucial tool, and

price optimisation is the best way to determine the exact price of the firm. This is used by the

Zylla company for determining the price at which customer is willing to purchase the product

and firm can get utmost benefits for the firm.

These are the tools which can helps the firm to gain the sustainable development.

P2 Diverse methods of reporting system used by the Zylla company:

There are various methods of reporting system that can be used by Zylla company in

order enhance the profitability and growth. They needs to have the great organised reporting

systems so that each business transaction can be recorded transparently. However, management

accounting systems are used by taking help of the financial statements of the firm. MA tools

does also assist the firm to gain the profitability by minimising the wastage costs. The

management of Zylla company can take the decisions so effectively only by taking help of

management accounting reporting tools. The performance of the firm can be assessed so

effectively so that the business could lower the wastage of the firm. Management of the firm can

accumulate the data from financial and non- financial sources for making the reports which are

useful for making strategies for the firm so that the firm can get the competitive advantage so

effectively. This is crucial for the firm to maintain reports so that any mistakes and any fraud can

2

could effectively eliminate the wastage cost.

Job costing system: This is the collection of costs of materials, labour and the overhead

costs for a particular job. Such approach is an effective tool which is used for tracking the

particular costs to the individual jobs and assessing them to oversee if the costs could be limited

in a later jobs. Job costing is implemented to gather costs at a small unit level. This is the

procedure of assigning the costs spends to incur to a particular job when the business is covered

with.

Inventory management system: This is the management system which is used by the

firm to keeps track of its stuff (Zimmerman and Yahya-Zadeh, 2011). This is the tool which can

be used by the firm in order to manage the inventory and also helps the firm to effectively

manage the available resources. By using this system, inventory is optimum used and no wastage

of money occurred.

Price optimisation system: This is an effective tool that can be used by the firm in order

to optimize the price of the product. However, for determining the price is a crucial tool, and

price optimisation is the best way to determine the exact price of the firm. This is used by the

Zylla company for determining the price at which customer is willing to purchase the product

and firm can get utmost benefits for the firm.

These are the tools which can helps the firm to gain the sustainable development.

P2 Diverse methods of reporting system used by the Zylla company:

There are various methods of reporting system that can be used by Zylla company in

order enhance the profitability and growth. They needs to have the great organised reporting

systems so that each business transaction can be recorded transparently. However, management

accounting systems are used by taking help of the financial statements of the firm. MA tools

does also assist the firm to gain the profitability by minimising the wastage costs. The

management of Zylla company can take the decisions so effectively only by taking help of

management accounting reporting tools. The performance of the firm can be assessed so

effectively so that the business could lower the wastage of the firm. Management of the firm can

accumulate the data from financial and non- financial sources for making the reports which are

useful for making strategies for the firm so that the firm can get the competitive advantage so

effectively. This is crucial for the firm to maintain reports so that any mistakes and any fraud can

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

not incur. The future investment of the firm is totally relied upon these reporting upon which

goodwill is totally depends. There are so many reporting system which could be implemented by

the Zylla firm. Few of them are as follows:

Performance reporting system: As per this reporting, essential information about firm

previous and current year performances which are recorded. This reporting system is used by the

firm by applying diverse statements. This is essential report as future investment related

decisions are interpreted if the performance of the firm is sound in the past few years.

Operation reporting: This is the information which are connected with the production

process which covers the costs and expenses which covers the over production procedure. This

would assist the firm to identify actual costs spend by the firm during the particular period

(Ward, 2012). However, this can be said that operational reporting system are connected with the

internal reporting system.

Job cost reporting: This is the reporting system which covers of those costs which

charged over material, labour and other production overhead. This is an efficient tool which are

used by the firm to track actual costs levied on an individual jobs and evaluate them critically.

Inventory management report: This is the key decision in production, retail and few

service organisations is at what level of inventory firm needs to have on hand? Stock in the firm

is commonly a firm largest asset. This helps to apply the effective component of supply chain

which demonstrates flow of products from manufacturer to storehouse. This reports is totally

related to chase of products, billing records, supplier information and delivering data.

Account receivable report: This covers of particular lists of debtors. With the help of

this report, firm can get the sustainability so that the business can able to have the effective

policies. The company can attain the pre-set targets by applying account receivable report.

M1:

This has already elaborated that MA is an efficient technique for assessing firm's

performance. This would likewise to assist management of Zylla company to acquire optimistic

outcomes by using available resources. For this aim, they assist the firm to get positive outcomes

with the available resources. For achieving the positive outcome, management of the cited firm

uses diverse management accounting system which could assist them to satiate their aims and

objectives. This is considered as one of the key aspects to firm. Because, optimum profitability

could attained via effective system (van der Steen, 2011). Long term decisions can be formed by

3

goodwill is totally depends. There are so many reporting system which could be implemented by

the Zylla firm. Few of them are as follows:

Performance reporting system: As per this reporting, essential information about firm

previous and current year performances which are recorded. This reporting system is used by the

firm by applying diverse statements. This is essential report as future investment related

decisions are interpreted if the performance of the firm is sound in the past few years.

Operation reporting: This is the information which are connected with the production

process which covers the costs and expenses which covers the over production procedure. This

would assist the firm to identify actual costs spend by the firm during the particular period

(Ward, 2012). However, this can be said that operational reporting system are connected with the

internal reporting system.

Job cost reporting: This is the reporting system which covers of those costs which

charged over material, labour and other production overhead. This is an efficient tool which are

used by the firm to track actual costs levied on an individual jobs and evaluate them critically.

Inventory management report: This is the key decision in production, retail and few

service organisations is at what level of inventory firm needs to have on hand? Stock in the firm

is commonly a firm largest asset. This helps to apply the effective component of supply chain

which demonstrates flow of products from manufacturer to storehouse. This reports is totally

related to chase of products, billing records, supplier information and delivering data.

Account receivable report: This covers of particular lists of debtors. With the help of

this report, firm can get the sustainability so that the business can able to have the effective

policies. The company can attain the pre-set targets by applying account receivable report.

M1:

This has already elaborated that MA is an efficient technique for assessing firm's

performance. This would likewise to assist management of Zylla company to acquire optimistic

outcomes by using available resources. For this aim, they assist the firm to get positive outcomes

with the available resources. For achieving the positive outcome, management of the cited firm

uses diverse management accounting system which could assist them to satiate their aims and

objectives. This is considered as one of the key aspects to firm. Because, optimum profitability

could attained via effective system (van der Steen, 2011). Long term decisions can be formed by

3

using MA techniques. In addition to this, the overall efficiency of the firm can be achieved

under this.

D1:

An accurate outcome can be achieved only by applying adequate financial information which

could assist the firm to plan their future aims. For this aim, reporting is the useful technique on

which decisions of the cited firm are based. Financial report are made by implementing essential

information about the current year and previous year performance. This is implemented by

investors for making capital investment plan in the forthcoming projects. The key source of data

collection is taken from income statement and balance sheet. Job cost reporting and performance

reporting is on the topmost priority as optimum attention of the firm are depends upon these two.

TASK 2

P3 Costing methods used for profit analysis:

Costing is termed as the process by which all the cost related to the manufacturing and

selling of products are covered. These are covered under material, labour and overheads which

implemented at the time of manufacturing. This is normally known as monitory value which

brief with efforts and resources implements for delivering quality products to its customers. This

covers variable costs which change with the vary in the unit. These are known as the direct costs.

In the financial accounting, there are so many costing methods which are implemented for

incurring optimum profits and sustain a great future for the firm. Few of them are as follows:

Absorption costing: This is the costing tool which treats all the costs, whether these are

variable or fixed, are covered. This is assumes to be the best method which allocates particular

part of fixed production costs to each unit and also fixed costs (Tucker and Parker, 2014). This is

also known as the full costing methods as entire manufacturing costs are known as the product

costs.

Marginal costing: This is the cost which vary with the change in the per unit of

production. However, this can not consider the fixed cost while calculating the marginal costing.

However this can be said that the company charge the price of the product for per unit of

products if these are more than the marginal cost of manufacturing goods then this is positive

sign to produce that unit.

Calculation by using marginal costing:

4

under this.

D1:

An accurate outcome can be achieved only by applying adequate financial information which

could assist the firm to plan their future aims. For this aim, reporting is the useful technique on

which decisions of the cited firm are based. Financial report are made by implementing essential

information about the current year and previous year performance. This is implemented by

investors for making capital investment plan in the forthcoming projects. The key source of data

collection is taken from income statement and balance sheet. Job cost reporting and performance

reporting is on the topmost priority as optimum attention of the firm are depends upon these two.

TASK 2

P3 Costing methods used for profit analysis:

Costing is termed as the process by which all the cost related to the manufacturing and

selling of products are covered. These are covered under material, labour and overheads which

implemented at the time of manufacturing. This is normally known as monitory value which

brief with efforts and resources implements for delivering quality products to its customers. This

covers variable costs which change with the vary in the unit. These are known as the direct costs.

In the financial accounting, there are so many costing methods which are implemented for

incurring optimum profits and sustain a great future for the firm. Few of them are as follows:

Absorption costing: This is the costing tool which treats all the costs, whether these are

variable or fixed, are covered. This is assumes to be the best method which allocates particular

part of fixed production costs to each unit and also fixed costs (Tucker and Parker, 2014). This is

also known as the full costing methods as entire manufacturing costs are known as the product

costs.

Marginal costing: This is the cost which vary with the change in the per unit of

production. However, this can not consider the fixed cost while calculating the marginal costing.

However this can be said that the company charge the price of the product for per unit of

products if these are more than the marginal cost of manufacturing goods then this is positive

sign to produce that unit.

Calculation by using marginal costing:

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

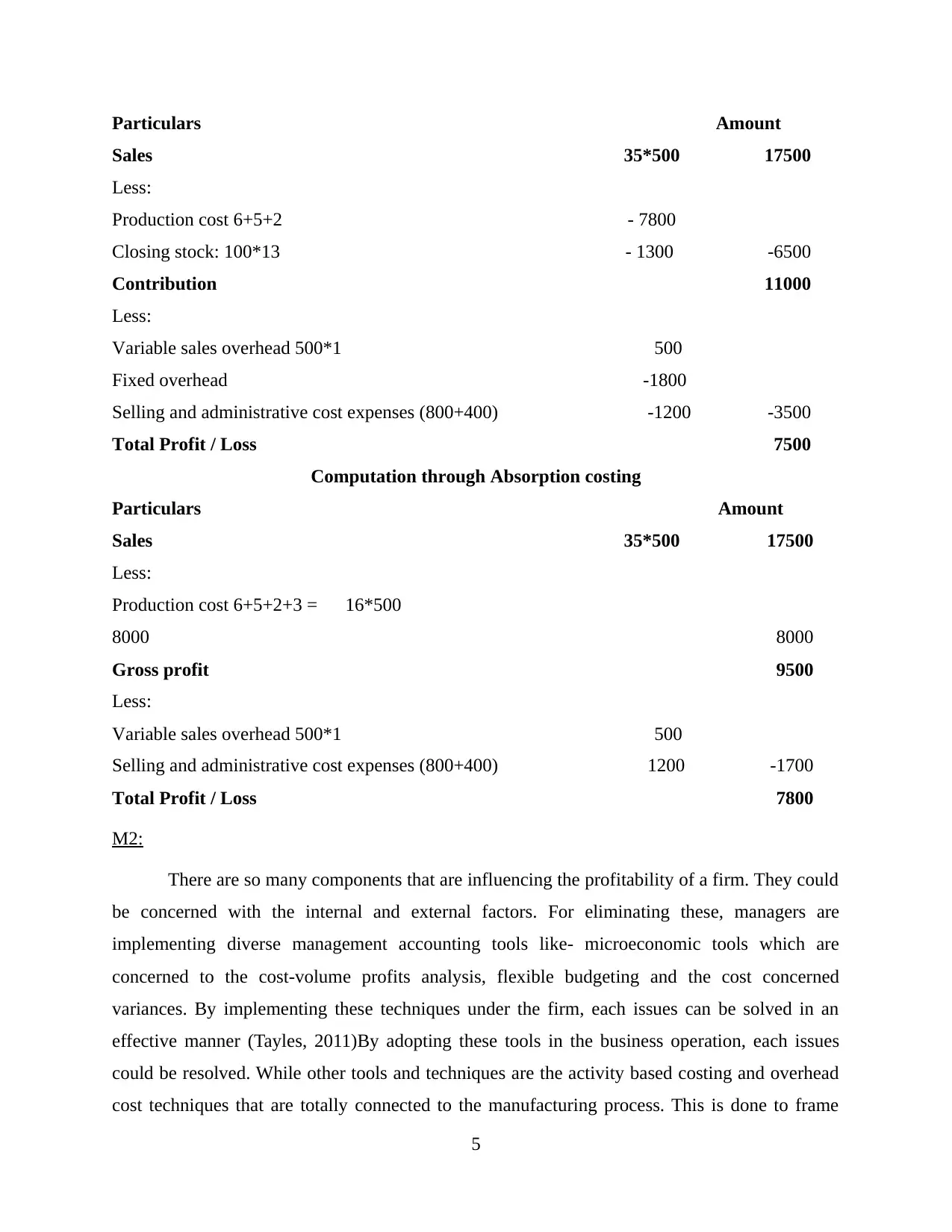

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2 - 7800

Closing stock: 100*13 - 1300 -6500

Contribution 11000

Less:

Variable sales overhead 500*1 500

Fixed overhead -1800

Selling and administrative cost expenses (800+400) -1200 -3500

Total Profit / Loss 7500

Computation through Absorption costing

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2+3 = 16*500

8000 8000

Gross profit 9500

Less:

Variable sales overhead 500*1 500

Selling and administrative cost expenses (800+400) 1200 -1700

Total Profit / Loss 7800

M2:

There are so many components that are influencing the profitability of a firm. They could

be concerned with the internal and external factors. For eliminating these, managers are

implementing diverse management accounting tools like- microeconomic tools which are

concerned to the cost-volume profits analysis, flexible budgeting and the cost concerned

variances. By implementing these techniques under the firm, each issues can be solved in an

effective manner (Tayles, 2011)By adopting these tools in the business operation, each issues

could be resolved. While other tools and techniques are the activity based costing and overhead

cost techniques that are totally connected to the manufacturing process. This is done to frame

5

Sales 35*500 17500

Less:

Production cost 6+5+2 - 7800

Closing stock: 100*13 - 1300 -6500

Contribution 11000

Less:

Variable sales overhead 500*1 500

Fixed overhead -1800

Selling and administrative cost expenses (800+400) -1200 -3500

Total Profit / Loss 7500

Computation through Absorption costing

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2+3 = 16*500

8000 8000

Gross profit 9500

Less:

Variable sales overhead 500*1 500

Selling and administrative cost expenses (800+400) 1200 -1700

Total Profit / Loss 7800

M2:

There are so many components that are influencing the profitability of a firm. They could

be concerned with the internal and external factors. For eliminating these, managers are

implementing diverse management accounting tools like- microeconomic tools which are

concerned to the cost-volume profits analysis, flexible budgeting and the cost concerned

variances. By implementing these techniques under the firm, each issues can be solved in an

effective manner (Tayles, 2011)By adopting these tools in the business operation, each issues

could be resolved. While other tools and techniques are the activity based costing and overhead

cost techniques that are totally connected to the manufacturing process. This is done to frame

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

positive comparison between actual and the standard costs which are implemented by the firm in

order to manage the wastage funds.

D2:

In the above-mentioned table, profits is calculated by using marginal costing method and the

absorption costing methods. Net profits is maximised by using absorption costing method under

the cited case. By using absorption costing the net profit is calculated as 7800. while on the other

hand, by applying marginal costing, the net profits is calculated as 7500. which is 300 less than

the profits calculated as per the absorption costing.

TASK 3

P4 Advantages and disadvantage of different planning tools:

The budget or planning tools are the most crucial tools which are used by the firm in

order to gain the competitive advantages over the rivals. The budget is an estimation of incomes

and expenses for a particular period of time. However these are made on the basis of the previous

financial information. With the help of budget, firm can improve the performance of the business

operations of Zylla company (Types of Budgets for Businesses, 2017). However the company

needs to have certain tools that can be used by their managers in order to make the budget or

planning tools.

There are so many budgets or planning tools which are applied in firms. In this, the below

mentioned planning tools are used:

Static budget: This is the budget which is fixed and does not change with the cost of production.

A static budget is the one which forms forecasting values about inputs and outputs which are

conceived before the period in question started. When compared to actual outcomes which are

gained after the fact, the numbers from static budget are usually totally different from the actual

outcomes.

Advantages:

the main benefits of static budget is that this is easy to implement in the firm. This is not required

to be updated regularly via accounting periods which they are intended to cover. In addition to

this, a static budget could offer deep investigation into the firm's costs and profits at the time of

variance analysis is executed. It enables the firm to overview where it is overestimating or

underestimating its expenses and earnings henceforth, it can make changes accordingly.

6

order to manage the wastage funds.

D2:

In the above-mentioned table, profits is calculated by using marginal costing method and the

absorption costing methods. Net profits is maximised by using absorption costing method under

the cited case. By using absorption costing the net profit is calculated as 7800. while on the other

hand, by applying marginal costing, the net profits is calculated as 7500. which is 300 less than

the profits calculated as per the absorption costing.

TASK 3

P4 Advantages and disadvantage of different planning tools:

The budget or planning tools are the most crucial tools which are used by the firm in

order to gain the competitive advantages over the rivals. The budget is an estimation of incomes

and expenses for a particular period of time. However these are made on the basis of the previous

financial information. With the help of budget, firm can improve the performance of the business

operations of Zylla company (Types of Budgets for Businesses, 2017). However the company

needs to have certain tools that can be used by their managers in order to make the budget or

planning tools.

There are so many budgets or planning tools which are applied in firms. In this, the below

mentioned planning tools are used:

Static budget: This is the budget which is fixed and does not change with the cost of production.

A static budget is the one which forms forecasting values about inputs and outputs which are

conceived before the period in question started. When compared to actual outcomes which are

gained after the fact, the numbers from static budget are usually totally different from the actual

outcomes.

Advantages:

the main benefits of static budget is that this is easy to implement in the firm. This is not required

to be updated regularly via accounting periods which they are intended to cover. In addition to

this, a static budget could offer deep investigation into the firm's costs and profits at the time of

variance analysis is executed. It enables the firm to overview where it is overestimating or

underestimating its expenses and earnings henceforth, it can make changes accordingly.

6

Disadvantages:

The main drawback of the static budget is that it's lack of flexibility. If a firm incorporates a

budget which is based on the particular level of sales quantity and quantity increased. This can

not allocate extra resources to keep up (Contrafatto and Burns, 2013). In addition to this, if a firm

determines underperforming areas of the firm, this can't allocate extra resources to help. This can

adversely influence firm's revenues stream. In addition to this, static budget are based on the

earlier data, newer firms might have more difficulty in incorporating and implementing them.

Henceforth, this is the more useful tool for firms with greatly predictable sales volume and costs.

Flexible budget: This is the budget which vary for changes in the volume of activity. The

flexibility budget is highly sophisticated and helpful than a static budget, which keeps at one

amount regardless of the volume of the activity.

Advantages:

This is the budget which changes during the budget. Flexible budget is the one which enables to

adjust relies on the change in the hypothesis which is required to form the budget at the time of

management planning process. A static budget keeps the same even if there are important

changes from assumptions made at the time of planning. The highest advantages which is

flexible budget which has over a static budget is its adaptability.

Disadvantages:

In each time, all production in a budget could be flexible. For instance, a firm's rent

expense is fixed for the entire year. This is not practical to estimate that to vary each month or at

each quarter. In either a flexible budget or static budget, the rent is fixed (Bodie, 2013).

Sales budget: This is the budget or planning tool which covers estimation of the future

sales for a particular period of time. However, this is assumed to be the best tool which are going

to implement these tools that can be used by the firm so that actual outcome could meet out the

budgeted figure. If the variance or deviation covers then the company's management could

overcome these by applying the best management practises.

Advantages:

This is the tool which helps to determines the sales estimation and makes strategy as well. This

planning tool also helps the firm to eliminate the wastage costs so that the firm can get the

competitive advantages over the other rivals. This the tool that helps the firm to make strategies

which help the firm to maximise the sales values.

7

The main drawback of the static budget is that it's lack of flexibility. If a firm incorporates a

budget which is based on the particular level of sales quantity and quantity increased. This can

not allocate extra resources to keep up (Contrafatto and Burns, 2013). In addition to this, if a firm

determines underperforming areas of the firm, this can't allocate extra resources to help. This can

adversely influence firm's revenues stream. In addition to this, static budget are based on the

earlier data, newer firms might have more difficulty in incorporating and implementing them.

Henceforth, this is the more useful tool for firms with greatly predictable sales volume and costs.

Flexible budget: This is the budget which vary for changes in the volume of activity. The

flexibility budget is highly sophisticated and helpful than a static budget, which keeps at one

amount regardless of the volume of the activity.

Advantages:

This is the budget which changes during the budget. Flexible budget is the one which enables to

adjust relies on the change in the hypothesis which is required to form the budget at the time of

management planning process. A static budget keeps the same even if there are important

changes from assumptions made at the time of planning. The highest advantages which is

flexible budget which has over a static budget is its adaptability.

Disadvantages:

In each time, all production in a budget could be flexible. For instance, a firm's rent

expense is fixed for the entire year. This is not practical to estimate that to vary each month or at

each quarter. In either a flexible budget or static budget, the rent is fixed (Bodie, 2013).

Sales budget: This is the budget or planning tool which covers estimation of the future

sales for a particular period of time. However, this is assumed to be the best tool which are going

to implement these tools that can be used by the firm so that actual outcome could meet out the

budgeted figure. If the variance or deviation covers then the company's management could

overcome these by applying the best management practises.

Advantages:

This is the tool which helps to determines the sales estimation and makes strategy as well. This

planning tool also helps the firm to eliminate the wastage costs so that the firm can get the

competitive advantages over the other rivals. This the tool that helps the firm to make strategies

which help the firm to maximise the sales values.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Disadvantages:

The main drawback of the firm is that the management not always makes an exact

estimation of the firm. That is why, firm estimate inaccurate data that would make the firm

ineffective performance. The management of the cited firm can not make certain prediction for a

particular period of time. Once this is made can not be altered (Baldvinsdottir, Mitchell and

Nørreklit, 2010).

Cash flow budget: This is the most effective tool which is used by the firm in order to

predict the cash inflow and cash outflow for a particular period of time. With the help of cash

flow budget, firm could get the sustainable development.

Advantages:

By using the cash flow budget, firm could make their future spending plans so that the

management save their amount effectively. The company can use their business operations so

effectively by taking cash budget. Management also know about their future earnings which are

going to realised in cash for a particular period of time. This is an effective organised

information about total cash implement by firm during the year is identify easily.

Disadvantages:

The main constraint of cash budget is that it does not estimate an exact cash inflows and

outflows. Henceforth, on believing this planning tool, firm can not attain its pre-set objectives.

M3:

In connection to get more dependable results, organization's utilized to frame budgetary plans.

For this reason, different budgetary plans instruments are used. These all are utilized to make

powerful assessment of organization's execution and to make essential strides for advance up

gradation. With the assistance of this, long term obligations can be paid to accomplish future

purpose. Operating plans or plans are utilized to make investigation of expenses and costs that

are bring about by Zylla organization at the time of production. While, on the other hand, cash

budgets are utilized in order to decide total cash during particular year.

D4:

For assessing the performance analysis, various factors are requires to be analysed which could

affects the performance of the firm. This is linked with management of routine business

operations. This influences the financial and non financial factors which are used by the firm.

This is the main responsibility of the managers of the Zylla company to assess and evaluate those

8

The main drawback of the firm is that the management not always makes an exact

estimation of the firm. That is why, firm estimate inaccurate data that would make the firm

ineffective performance. The management of the cited firm can not make certain prediction for a

particular period of time. Once this is made can not be altered (Baldvinsdottir, Mitchell and

Nørreklit, 2010).

Cash flow budget: This is the most effective tool which is used by the firm in order to

predict the cash inflow and cash outflow for a particular period of time. With the help of cash

flow budget, firm could get the sustainable development.

Advantages:

By using the cash flow budget, firm could make their future spending plans so that the

management save their amount effectively. The company can use their business operations so

effectively by taking cash budget. Management also know about their future earnings which are

going to realised in cash for a particular period of time. This is an effective organised

information about total cash implement by firm during the year is identify easily.

Disadvantages:

The main constraint of cash budget is that it does not estimate an exact cash inflows and

outflows. Henceforth, on believing this planning tool, firm can not attain its pre-set objectives.

M3:

In connection to get more dependable results, organization's utilized to frame budgetary plans.

For this reason, different budgetary plans instruments are used. These all are utilized to make

powerful assessment of organization's execution and to make essential strides for advance up

gradation. With the assistance of this, long term obligations can be paid to accomplish future

purpose. Operating plans or plans are utilized to make investigation of expenses and costs that

are bring about by Zylla organization at the time of production. While, on the other hand, cash

budgets are utilized in order to decide total cash during particular year.

D4:

For assessing the performance analysis, various factors are requires to be analysed which could

affects the performance of the firm. This is linked with management of routine business

operations. This influences the financial and non financial factors which are used by the firm.

This is the main responsibility of the managers of the Zylla company to assess and evaluate those

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

financial related problems or issues so that the company can not adversely influence the firm's

profitability. For resolving these issues, firm implement Key performance indicators,

benchmarking, financial governance and others tools.

P5 Management accounting to respond financial problems:

The financial problems arises due to the lack of practises of the management accounting

system in a firm. However, this can be said that the company needs to adopt various systems

which assist the firm for getting the sustainable development. The financial problems are the key

major constraints which can occurred in the firm (Guest, 2011). This is the reason, company

could not make certain tools. However, there is a need to make overcome these financial

problems in the firm by applying effective management system in the firm. However, there are

certain tools in the management accounting which are used by the firm so that the business can

attain various pre-set objectives of the firm. There are certain tools which can be used by the firm

in order to provides problems in an effective manner. There are certain tools which are as

follows:

Key Performance Indicators: This is the measurable value which demonstrates how efficiently

a firm attains key business objectives. Firms apply this KPIs at various levels in order to assess

their success by attaining the pre-set targets. A optimum level KPIs must concentrates on the

entire performance of the firm, while on the other hand, low level KPIs concentrate on the

processes in the divisions like- sales, marketing or others.

A KPI is the effective tool whci helps the managers of the firm an also to the employees gauge

the efficiency of different functions and processes which are important for attaining the firms

objectives (Ellis, 2010). A firm KPI is linked to the firm's strategic objectives and are

implemented by the firm to help managers to evaluate whether they are on goals as they work

towards these pre-set goals and targets. A customer support team may assess the average on hold

time for customers and the percentage of call which emerge in a more post call survey rating and

overall customer satisfaction.

There is a need to implement key performance indicators. But that must be well developed so

that the consistent review of the firm's processes can be done. Enhancement in the employee

engagement and customer satisfaction assessment must be positive. Which helps the firm to get

the sustainability.

9

profitability. For resolving these issues, firm implement Key performance indicators,

benchmarking, financial governance and others tools.

P5 Management accounting to respond financial problems:

The financial problems arises due to the lack of practises of the management accounting

system in a firm. However, this can be said that the company needs to adopt various systems

which assist the firm for getting the sustainable development. The financial problems are the key

major constraints which can occurred in the firm (Guest, 2011). This is the reason, company

could not make certain tools. However, there is a need to make overcome these financial

problems in the firm by applying effective management system in the firm. However, there are

certain tools in the management accounting which are used by the firm so that the business can

attain various pre-set objectives of the firm. There are certain tools which can be used by the firm

in order to provides problems in an effective manner. There are certain tools which are as

follows:

Key Performance Indicators: This is the measurable value which demonstrates how efficiently

a firm attains key business objectives. Firms apply this KPIs at various levels in order to assess

their success by attaining the pre-set targets. A optimum level KPIs must concentrates on the

entire performance of the firm, while on the other hand, low level KPIs concentrate on the

processes in the divisions like- sales, marketing or others.

A KPI is the effective tool whci helps the managers of the firm an also to the employees gauge

the efficiency of different functions and processes which are important for attaining the firms

objectives (Ellis, 2010). A firm KPI is linked to the firm's strategic objectives and are

implemented by the firm to help managers to evaluate whether they are on goals as they work

towards these pre-set goals and targets. A customer support team may assess the average on hold

time for customers and the percentage of call which emerge in a more post call survey rating and

overall customer satisfaction.

There is a need to implement key performance indicators. But that must be well developed so

that the consistent review of the firm's processes can be done. Enhancement in the employee

engagement and customer satisfaction assessment must be positive. Which helps the firm to get

the sustainability.

9

Benchmarking: It is an effective management tool which is used by the firm in order to

overcome financial problems that can assist the firm to gain the sustainable development.

This tool helps the firm to show whether the firm performance is stronger or weaker than the

competitors. This would provides a clear picture of where improvements are required and how it

requires to enhance profits (DRURY, 2013). This is the regular process of consistent

improvement. Once the changes implemented, then there is a need to benchmark business in

order to feel the results. With the help of this, what is working, and firm can improve their

performance. This is the continuous process under which firms regularly seek the improvement

of their practices.

This is usually used by the firm in order to evaluate the performance of the firm by

concentrating on one or more particular business. These are the indicators which might be the

cost per unit, productivity, defects per unit or others. The measurement of the performance is

then compared to that of the other firms within the similar industry. This is the process which is

usually applied by the strategic management. Firms needs to assess so many aspects of their

processes and compare them to the procedures of the best practice firms.

With the help of benchmarking information gained from such a comparison enables firms to

assess how well they perform in comparison with the best and in turn emerge new and advanced

strategies in order to work towards improving or considering the best practices (Ball, Grubnic

and Birchall, 2014).

Financial governance: This is the most important tool which are used by the firm in order to

effective transparency in the operations of the firm. However, this can be seen that the company

needs to provides effective tools so that the financial governance can be improved. This complies

all the finance related performance of the firm so that the business can be done so effectively.

Corporate scandals like- Enron Debacle and collapse of Bearings Bank, have demonstrates the

requirement for sound and stronger supervisory regulations for those company which are listed

on any exchange. However, each country have their own regulation like- JSOX in Japan,

Turnbull in the UK, and MI52-109 and Bill 198 in Canada. Every regulation effectively

identifies imperative, stricter personal accountability of the corporation's executive management

and inner controls for the adequacy of reported financial statements (Baird, Jia Hu and Reeve,

2011).

10

overcome financial problems that can assist the firm to gain the sustainable development.

This tool helps the firm to show whether the firm performance is stronger or weaker than the

competitors. This would provides a clear picture of where improvements are required and how it

requires to enhance profits (DRURY, 2013). This is the regular process of consistent

improvement. Once the changes implemented, then there is a need to benchmark business in

order to feel the results. With the help of this, what is working, and firm can improve their

performance. This is the continuous process under which firms regularly seek the improvement

of their practices.

This is usually used by the firm in order to evaluate the performance of the firm by

concentrating on one or more particular business. These are the indicators which might be the

cost per unit, productivity, defects per unit or others. The measurement of the performance is

then compared to that of the other firms within the similar industry. This is the process which is

usually applied by the strategic management. Firms needs to assess so many aspects of their

processes and compare them to the procedures of the best practice firms.

With the help of benchmarking information gained from such a comparison enables firms to

assess how well they perform in comparison with the best and in turn emerge new and advanced

strategies in order to work towards improving or considering the best practices (Ball, Grubnic

and Birchall, 2014).

Financial governance: This is the most important tool which are used by the firm in order to

effective transparency in the operations of the firm. However, this can be seen that the company

needs to provides effective tools so that the financial governance can be improved. This complies

all the finance related performance of the firm so that the business can be done so effectively.

Corporate scandals like- Enron Debacle and collapse of Bearings Bank, have demonstrates the

requirement for sound and stronger supervisory regulations for those company which are listed

on any exchange. However, each country have their own regulation like- JSOX in Japan,

Turnbull in the UK, and MI52-109 and Bill 198 in Canada. Every regulation effectively

identifies imperative, stricter personal accountability of the corporation's executive management

and inner controls for the adequacy of reported financial statements (Baird, Jia Hu and Reeve,

2011).

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.