Essay: Inappropriate Incentives and the 2007/08 Financial Crisis

VerifiedAdded on 2020/01/07

|9

|2745

|323

Essay

AI Summary

This essay investigates the extent to which inappropriate incentives contributed to the global financial crisis of 2007/08. It explores various factors, including subprime lending, the housing bubble, deregulation, and overleveraging, highlighting how perverse incentives within financial institutions fostered excessive risk-taking and manipulation. The essay references research on banking crises, the impact of short-term compensation systems, and the role of rating agencies. It examines the originate-and-distribute model, the creation of new money by banks, and the subsequent increase in personal debt. The analysis also covers the impact of the financial crisis on the economy, including lending slowdowns, price drops, and recessions. The essay concludes by emphasizing the need for regular evaluation of incentive contracts to prevent future crises and minimize system failures. The essay draws on various sources, including research papers, books, and reports from financial authorities, to support its arguments.

Essay on: “To what extent was the global financial

crisis of 2007/08 caused by inappropriate

incentives?”

crisis of 2007/08 caused by inappropriate

incentives?”

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Topic: “To what extent was the global financial crisis of 2007/08 caused by inappropriate

incentives?”

In the present research emphasize is given on assessing the impact of inappropriate

incentives leading to financial crisis in 2008. There are several banks such as investment and

commercial as well as central banks which controls the money supply and interest rates are

responsible for leading to crises situation in the market. It is because of the fact that, financial

institution were unable to manage the funds which indeed led the huge market slump. Thus,

researcher focusing on understanding how inappropriate incentives cause financial crises.

In 2008, financial crisis happened because of several reasons which consist of subprime

lending, growth of housing bubble, easy credit conditions, deregulations, increased debt burden

and overleveraging, inappropriate incentives etc. Herein, researcher emphasize on assessing the

role of inappropriate incentives in causing financial crisis. According to the study by Pesch

(2011), banking crises can be found throughout history. Herein, author argues that inconsistent

incentives have cause the financial crisis. However, the roots of current financial crisis lie in the

housing bubble due to which banking has suffered from the burst of bubble doe two main

reasons: firstly, banks have been able to place assets in off balance sheet vehicles and does not

have to possess capital buffers against the institutions (Pesch, 2011). While secondly, banks

could lower their regulatory capital requirements by investing in triple “A” rate securities,

mainly mortgage backs or related derivatives.

Similar to this research conducted by Brek (2008) states that, it has been often argued that

the crisis was due to the creation of pertinacious incentives in the management of financial

institution. However, incentives, financial or otherwise are intended to promote certain behavior

that are expected to lead to desired results, but they can also cause unwanted effects, perhaps

because they are poorly designed i.e. improper reward system (Brek, 2008). For instance Bank of

England and the Federal Reserve, reward an increase in the share price in the short term rather

than the achievement of grater value in the long term. It is because they assumed that agents are

only motivated by economic interest, so that the introduction of incentive of this nature crowds

out other possible targets such as the quality of their work or the creation of teams which are

effective in long term.

It is likely that many of the inappropriate behaviors in the recent crisis are related to the

existence of perverse incentives (Malinen, 2016). For instance, the attempt to align the interest of

1 | P a g e

incentives?”

In the present research emphasize is given on assessing the impact of inappropriate

incentives leading to financial crisis in 2008. There are several banks such as investment and

commercial as well as central banks which controls the money supply and interest rates are

responsible for leading to crises situation in the market. It is because of the fact that, financial

institution were unable to manage the funds which indeed led the huge market slump. Thus,

researcher focusing on understanding how inappropriate incentives cause financial crises.

In 2008, financial crisis happened because of several reasons which consist of subprime

lending, growth of housing bubble, easy credit conditions, deregulations, increased debt burden

and overleveraging, inappropriate incentives etc. Herein, researcher emphasize on assessing the

role of inappropriate incentives in causing financial crisis. According to the study by Pesch

(2011), banking crises can be found throughout history. Herein, author argues that inconsistent

incentives have cause the financial crisis. However, the roots of current financial crisis lie in the

housing bubble due to which banking has suffered from the burst of bubble doe two main

reasons: firstly, banks have been able to place assets in off balance sheet vehicles and does not

have to possess capital buffers against the institutions (Pesch, 2011). While secondly, banks

could lower their regulatory capital requirements by investing in triple “A” rate securities,

mainly mortgage backs or related derivatives.

Similar to this research conducted by Brek (2008) states that, it has been often argued that

the crisis was due to the creation of pertinacious incentives in the management of financial

institution. However, incentives, financial or otherwise are intended to promote certain behavior

that are expected to lead to desired results, but they can also cause unwanted effects, perhaps

because they are poorly designed i.e. improper reward system (Brek, 2008). For instance Bank of

England and the Federal Reserve, reward an increase in the share price in the short term rather

than the achievement of grater value in the long term. It is because they assumed that agents are

only motivated by economic interest, so that the introduction of incentive of this nature crowds

out other possible targets such as the quality of their work or the creation of teams which are

effective in long term.

It is likely that many of the inappropriate behaviors in the recent crisis are related to the

existence of perverse incentives (Malinen, 2016). For instance, the attempt to align the interest of

1 | P a g e

managers and analysts with those of shareholder has led to compensation systems that emphasize

short term results, which may have led to undesirable behaviors such as excessive risk taking and

manipulation of financial results. In particular to the case of inappropriate incentives, the major

conflict is regarding interest that have arisen for instance in the rating agencies, whose income

depended in large measure on the valuation of their clients assets. In the banking sector, a US

bank incentivized employees to lend to small business and increased lending by 47%, but

parallel to this defaults also increased sharply (Allen, 2009). However, as per the book published

by Bratton (2015) researcher evaluated that, risky behavior fuelled by inappropriate incentives

has been cited has the cause of financial crisis that began in 2008. Further author criticizing that,

new pay paradigm is based on the ethical deficiencies because the practice increases employee

risk and simultaneously diminishes collective representation in pay system (Bratton, 2015). On

the basis of this, employee risk increases as a larger proportion of pay is contingent on individual

performance which along with the growth of zero hours contracts means that earnings are far less

predictable.

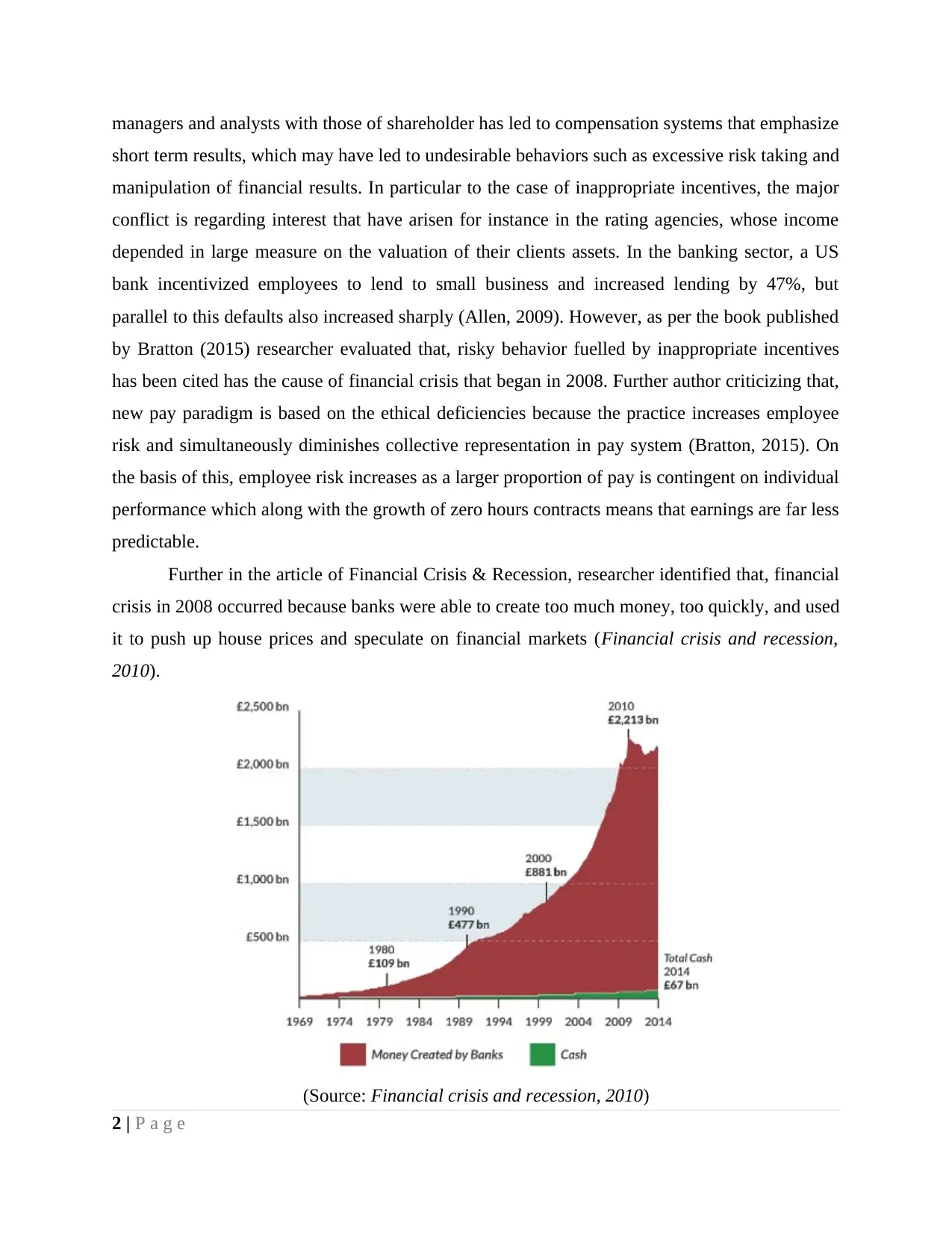

Further in the article of Financial Crisis & Recession, researcher identified that, financial

crisis in 2008 occurred because banks were able to create too much money, too quickly, and used

it to push up house prices and speculate on financial markets (Financial crisis and recession,

2010).

(Source: Financial crisis and recession, 2010)

2 | P a g e

short term results, which may have led to undesirable behaviors such as excessive risk taking and

manipulation of financial results. In particular to the case of inappropriate incentives, the major

conflict is regarding interest that have arisen for instance in the rating agencies, whose income

depended in large measure on the valuation of their clients assets. In the banking sector, a US

bank incentivized employees to lend to small business and increased lending by 47%, but

parallel to this defaults also increased sharply (Allen, 2009). However, as per the book published

by Bratton (2015) researcher evaluated that, risky behavior fuelled by inappropriate incentives

has been cited has the cause of financial crisis that began in 2008. Further author criticizing that,

new pay paradigm is based on the ethical deficiencies because the practice increases employee

risk and simultaneously diminishes collective representation in pay system (Bratton, 2015). On

the basis of this, employee risk increases as a larger proportion of pay is contingent on individual

performance which along with the growth of zero hours contracts means that earnings are far less

predictable.

Further in the article of Financial Crisis & Recession, researcher identified that, financial

crisis in 2008 occurred because banks were able to create too much money, too quickly, and used

it to push up house prices and speculate on financial markets (Financial crisis and recession,

2010).

(Source: Financial crisis and recession, 2010)

2 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

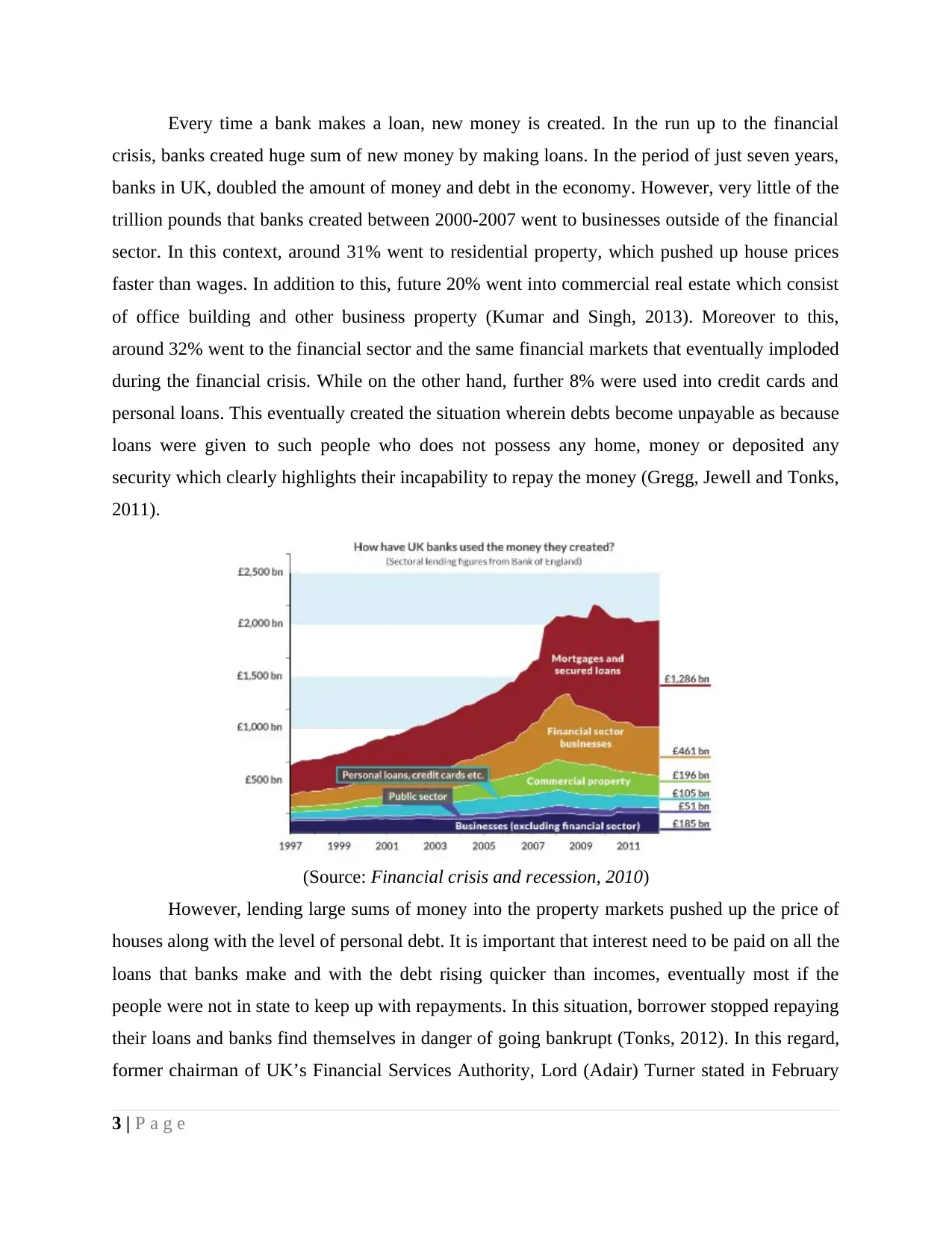

Every time a bank makes a loan, new money is created. In the run up to the financial

crisis, banks created huge sum of new money by making loans. In the period of just seven years,

banks in UK, doubled the amount of money and debt in the economy. However, very little of the

trillion pounds that banks created between 2000-2007 went to businesses outside of the financial

sector. In this context, around 31% went to residential property, which pushed up house prices

faster than wages. In addition to this, future 20% went into commercial real estate which consist

of office building and other business property (Kumar and Singh, 2013). Moreover to this,

around 32% went to the financial sector and the same financial markets that eventually imploded

during the financial crisis. While on the other hand, further 8% were used into credit cards and

personal loans. This eventually created the situation wherein debts become unpayable as because

loans were given to such people who does not possess any home, money or deposited any

security which clearly highlights their incapability to repay the money (Gregg, Jewell and Tonks,

2011).

(Source: Financial crisis and recession, 2010)

However, lending large sums of money into the property markets pushed up the price of

houses along with the level of personal debt. It is important that interest need to be paid on all the

loans that banks make and with the debt rising quicker than incomes, eventually most if the

people were not in state to keep up with repayments. In this situation, borrower stopped repaying

their loans and banks find themselves in danger of going bankrupt (Tonks, 2012). In this regard,

former chairman of UK’s Financial Services Authority, Lord (Adair) Turner stated in February

3 | P a g e

crisis, banks created huge sum of new money by making loans. In the period of just seven years,

banks in UK, doubled the amount of money and debt in the economy. However, very little of the

trillion pounds that banks created between 2000-2007 went to businesses outside of the financial

sector. In this context, around 31% went to residential property, which pushed up house prices

faster than wages. In addition to this, future 20% went into commercial real estate which consist

of office building and other business property (Kumar and Singh, 2013). Moreover to this,

around 32% went to the financial sector and the same financial markets that eventually imploded

during the financial crisis. While on the other hand, further 8% were used into credit cards and

personal loans. This eventually created the situation wherein debts become unpayable as because

loans were given to such people who does not possess any home, money or deposited any

security which clearly highlights their incapability to repay the money (Gregg, Jewell and Tonks,

2011).

(Source: Financial crisis and recession, 2010)

However, lending large sums of money into the property markets pushed up the price of

houses along with the level of personal debt. It is important that interest need to be paid on all the

loans that banks make and with the debt rising quicker than incomes, eventually most if the

people were not in state to keep up with repayments. In this situation, borrower stopped repaying

their loans and banks find themselves in danger of going bankrupt (Tonks, 2012). In this regard,

former chairman of UK’s Financial Services Authority, Lord (Adair) Turner stated in February

3 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2013 that, the financial crisis of 2007 to 2008 occurred because we failed to constrain the

financial system’s creation of private credit and money. However, this process caused the

financial crisis. As the crisis struck, banks limited their new lending to businesses and

households. Further, the slowdown in lending cause prices in these markets to drop and this

means those that have borrowed too much to speculate on rising prices have to sell the assets in

regards to repay their loans (McKibbin and Stoeckel, 2009). Herein, prices of house dropped

down significantly which burst the bubble as a result of which banks panicked and cut lending

event future. A downward spiral thus begins and the economy tips into recession.

During the period of recession, big financial institutions like, Central bank, Bank of

England and the Federal Reserve refuse to lend the money which resulted in shrink of the

economy. Thereafter, banks lend when they feel confident that they will be repaid. So when

economy is doing badly banks prefer to limit their lending (Rajan, Seru and Vig, 2008). During

this period, financial institutions of UK limits their amount of new loans they make but still

public have to keep up repayments on debts they already have. The problem arises when the

money which is used to repay loans are being destroyed or disappeared from the market or

economy. In this regard, Bank of England illustrated that, just as taking out a new loan creates

money, the repayment of bank loans destroy money. However, the banks making loans and

consumers repaying them are the most significant ways in which bank deposits are created and

destroyed in the modern economy (Lo, Repin and Steenbarger, 2010).

In addition to this, the theory of laissez-faire capitalism clearly indicates that financial

institutions would be risk averse because failure would result in liquidation. But in this context,

Federal Reserve’s 1984 rescue of continental Illinois and the 1998 rescue of the long term capital

management hedge fund, among others showed that institutions which failed to exercise due

diligence could reasonably expect to be protected from the consequences of their mistakes

(Financial crisis and recession, 2010). However, when too big to fail syndrome the short term

structure of compensation packages creates perverse incentives for executives to maximize the

short term performance of their companies at the expense of long term. According to the concept

developed by Black (2010), control fraud is defined as executives whop pervert good business

rules to transfer substantial wealth to themselves from shareholders and customers. During a

period of strong global growth, growing capital flows and lengthy stability earlier this decade,

4 | P a g e

financial system’s creation of private credit and money. However, this process caused the

financial crisis. As the crisis struck, banks limited their new lending to businesses and

households. Further, the slowdown in lending cause prices in these markets to drop and this

means those that have borrowed too much to speculate on rising prices have to sell the assets in

regards to repay their loans (McKibbin and Stoeckel, 2009). Herein, prices of house dropped

down significantly which burst the bubble as a result of which banks panicked and cut lending

event future. A downward spiral thus begins and the economy tips into recession.

During the period of recession, big financial institutions like, Central bank, Bank of

England and the Federal Reserve refuse to lend the money which resulted in shrink of the

economy. Thereafter, banks lend when they feel confident that they will be repaid. So when

economy is doing badly banks prefer to limit their lending (Rajan, Seru and Vig, 2008). During

this period, financial institutions of UK limits their amount of new loans they make but still

public have to keep up repayments on debts they already have. The problem arises when the

money which is used to repay loans are being destroyed or disappeared from the market or

economy. In this regard, Bank of England illustrated that, just as taking out a new loan creates

money, the repayment of bank loans destroy money. However, the banks making loans and

consumers repaying them are the most significant ways in which bank deposits are created and

destroyed in the modern economy (Lo, Repin and Steenbarger, 2010).

In addition to this, the theory of laissez-faire capitalism clearly indicates that financial

institutions would be risk averse because failure would result in liquidation. But in this context,

Federal Reserve’s 1984 rescue of continental Illinois and the 1998 rescue of the long term capital

management hedge fund, among others showed that institutions which failed to exercise due

diligence could reasonably expect to be protected from the consequences of their mistakes

(Financial crisis and recession, 2010). However, when too big to fail syndrome the short term

structure of compensation packages creates perverse incentives for executives to maximize the

short term performance of their companies at the expense of long term. According to the concept

developed by Black (2010), control fraud is defined as executives whop pervert good business

rules to transfer substantial wealth to themselves from shareholders and customers. During a

period of strong global growth, growing capital flows and lengthy stability earlier this decade,

4 | P a g e

market participants sought higher yields without an adequate appreciation of the risks and failed

to exercise pro-per due diligence (Gregg, Jewell and Tonks, 2011).

From August 2007 until September 2008, there was fairly wide agreement that poor

incentives in the US Mortgage industry had caused the problem. According to this explanation

what had happened was that the way the mortgage sector worked had changed significantly over

the years (Kumar and Singh, 2013). Traditionally, banks would raise funds, screen borrowers

and then lend out the money to those approved. If the borrower defaulted, the banks would bear

the losses. This system provided good incentives for banks to carefully assess the credit

worthiness of borrowers.

Over the time period, change made in the process and incentives were altered. In which

instead of banks originating mortgages and holding on to them, what happened was that brokers

and also some banks started originating them and selling them to be securitized. This process is

known as originate and distribute model. In addition to this, another major issue with incentive is

concerned with the ratings agencies (Lo, Repin and Steenbarger, 2010). Since the buyers of the

tranches looked at ratings the question arises: are the rating agencies doing a good job? There are

several experts, who argued that the answer was no because the agencies began to receive a large

proportion of their income from undertaking ratings of the securitized products. It is because of

the fact that, agencies started losing their objectivity and to give ratings that weren’t justified.

As per the mortgage incentives view of the crisis, the whole procedure for checking the

quality of the borrowers and the mortgages underlying the securitizations broke down. This

clearly indicated that world suggest it is fairly simple to solve the crisis and stop it from

reoccurring (Financial crisis and recession, 2010). Herein, government needs to regulate the

mortgage industry to make sure that everybody has the correct incentive and this will stop the

issue. However, it seems from the statements provided by Federal Reserve and the Treasury at

the time that initially this was the view that they took. However, as the crisis continued and then

after the default of Lehman the dramatic collapse in the global real economy made this view that

subprime mortgages were to blame less (Malinen, 2016).

In addition to this, Chairman of Financial Services Authority (FSA) Adair Turner in UK

claimed that, inappropriate incentive structure played significant role in encouraging behavior

which contributed to the financial crisis (Kumar and Singh, 2013). While contradicting to the US

Financial Crisis Inquiry Commission stated that, Lehman’s failure resulted in part from

5 | P a g e

to exercise pro-per due diligence (Gregg, Jewell and Tonks, 2011).

From August 2007 until September 2008, there was fairly wide agreement that poor

incentives in the US Mortgage industry had caused the problem. According to this explanation

what had happened was that the way the mortgage sector worked had changed significantly over

the years (Kumar and Singh, 2013). Traditionally, banks would raise funds, screen borrowers

and then lend out the money to those approved. If the borrower defaulted, the banks would bear

the losses. This system provided good incentives for banks to carefully assess the credit

worthiness of borrowers.

Over the time period, change made in the process and incentives were altered. In which

instead of banks originating mortgages and holding on to them, what happened was that brokers

and also some banks started originating them and selling them to be securitized. This process is

known as originate and distribute model. In addition to this, another major issue with incentive is

concerned with the ratings agencies (Lo, Repin and Steenbarger, 2010). Since the buyers of the

tranches looked at ratings the question arises: are the rating agencies doing a good job? There are

several experts, who argued that the answer was no because the agencies began to receive a large

proportion of their income from undertaking ratings of the securitized products. It is because of

the fact that, agencies started losing their objectivity and to give ratings that weren’t justified.

As per the mortgage incentives view of the crisis, the whole procedure for checking the

quality of the borrowers and the mortgages underlying the securitizations broke down. This

clearly indicated that world suggest it is fairly simple to solve the crisis and stop it from

reoccurring (Financial crisis and recession, 2010). Herein, government needs to regulate the

mortgage industry to make sure that everybody has the correct incentive and this will stop the

issue. However, it seems from the statements provided by Federal Reserve and the Treasury at

the time that initially this was the view that they took. However, as the crisis continued and then

after the default of Lehman the dramatic collapse in the global real economy made this view that

subprime mortgages were to blame less (Malinen, 2016).

In addition to this, Chairman of Financial Services Authority (FSA) Adair Turner in UK

claimed that, inappropriate incentive structure played significant role in encouraging behavior

which contributed to the financial crisis (Kumar and Singh, 2013). While contradicting to the US

Financial Crisis Inquiry Commission stated that, Lehman’s failure resulted in part from

5 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

significant problems in its corporate governance. Further, in the recent result conducted by

Gregg and et.al. (2011), investigated that whether bank executives has been incentivized to take

undue risks. Herein, author evaluated that, short term profits in the banking sector meant that

remuneration structure in banks and financial services were to blame for the crisis (Tonks, 2012).

In conclusion to the study it can be stated that, incentive contracts are nearly impossible

to be created in an accurate way. However, to prevent banking systems from crisis due to flawed

incentives the incentives contracts must be evaluated on a more regular basis and have to account

for existing as well as expected risks and uncertainties. By the means of this, government can

minimize the possibility of system failures due to misinterpreted incentives. However, it can be

said that banking crisis occurred due to multiple influencing factors and are expected to happen

again.

6 | P a g e

Gregg and et.al. (2011), investigated that whether bank executives has been incentivized to take

undue risks. Herein, author evaluated that, short term profits in the banking sector meant that

remuneration structure in banks and financial services were to blame for the crisis (Tonks, 2012).

In conclusion to the study it can be stated that, incentive contracts are nearly impossible

to be created in an accurate way. However, to prevent banking systems from crisis due to flawed

incentives the incentives contracts must be evaluated on a more regular basis and have to account

for existing as well as expected risks and uncertainties. By the means of this, government can

minimize the possibility of system failures due to misinterpreted incentives. However, it can be

said that banking crisis occurred due to multiple influencing factors and are expected to happen

again.

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Allen, F., 2009. The Global Financial Crisis: Causes and Consequences. [PDF]. Available

through: <http://www.bm.ust.hk/gmifc/Prof.%20Allen%20&%20Carletti_The%20Global

%20Financial%20Crisis.pdf>. [Accessed on 26th July 2016].

Bratton, J., 2015. Introduction to Work and Organizational Behaviour. Palgrave Macmillan.

Brek, B. J., 2008. Incentives and the Financial Crisis. [Online]. Available through:

<https://www.gsb.stanford.edu/insights/incentives-financial-crisis>. [Accessed on 26th

July 2016].

Financial crisis and recession, 2010. [Online]. Available through:

<http://positivemoney.org/issues/recessions-crisis/>. [Accessed on 26th July 2016].

Gregg, P., Jewell, S. and Tonks, I., 2011. Executive Pay and Performance: Did Bankers’

Bonuses Cause the Crisis?. [PDF]. Available through:

<http://www.bath.ac.uk/management/research/pdf/2011-01.pdf>. [Accessed on 26th July

2016].

Kumar, N. and Singh, P. J., 2013. Global Financial Crisis: Corporate Governance Failures and

Lessons. [Online]. Available through: <http://www.gsmi-ijgb.com/documents/jfam

%20v4%20n1%20p02%20-naveen%20kumar%20-global%20financial%20crisis.pdf/>.

[Accessed on 26th July 2016].

Lo, A., Repin, D. V. and Steenbarger, B. N., 2010. Fear and Greed in Financial Markets: A

Clinical Study of Day-Traders. American Economic Review. 95. pp.352-359.

Malinen, T., 2016. Who Caused the Great Recession?. [Online]. Available through:

<http://www.huffingtonpost.in/entry/who-caused-the-great-rece_b_9805056>. [Accessed

on 26th July 2016].

McKibbin, J. W. and Stoeckel, A., 2009. The Global Financial Crisis: Causes and

Consequences. [PDF]. Available through:

<http://www.lowyinstitute.org/files/pubfiles/McKibbin_and_Stoeckel,_The_global_finan

cial_crisis.pdf>. [Accessed on 26th July 2016].

Pesch, M., 2011. Financial Crisis: Flawed Incentives Cause Banking Crises. [Online]. Available

through: <http://www.grin.com/en/e-book/164361/financial-crisis-flawed-incentives-

cause-banking-crises>. [Accessed on 26th July 2016].

7 | P a g e

Allen, F., 2009. The Global Financial Crisis: Causes and Consequences. [PDF]. Available

through: <http://www.bm.ust.hk/gmifc/Prof.%20Allen%20&%20Carletti_The%20Global

%20Financial%20Crisis.pdf>. [Accessed on 26th July 2016].

Bratton, J., 2015. Introduction to Work and Organizational Behaviour. Palgrave Macmillan.

Brek, B. J., 2008. Incentives and the Financial Crisis. [Online]. Available through:

<https://www.gsb.stanford.edu/insights/incentives-financial-crisis>. [Accessed on 26th

July 2016].

Financial crisis and recession, 2010. [Online]. Available through:

<http://positivemoney.org/issues/recessions-crisis/>. [Accessed on 26th July 2016].

Gregg, P., Jewell, S. and Tonks, I., 2011. Executive Pay and Performance: Did Bankers’

Bonuses Cause the Crisis?. [PDF]. Available through:

<http://www.bath.ac.uk/management/research/pdf/2011-01.pdf>. [Accessed on 26th July

2016].

Kumar, N. and Singh, P. J., 2013. Global Financial Crisis: Corporate Governance Failures and

Lessons. [Online]. Available through: <http://www.gsmi-ijgb.com/documents/jfam

%20v4%20n1%20p02%20-naveen%20kumar%20-global%20financial%20crisis.pdf/>.

[Accessed on 26th July 2016].

Lo, A., Repin, D. V. and Steenbarger, B. N., 2010. Fear and Greed in Financial Markets: A

Clinical Study of Day-Traders. American Economic Review. 95. pp.352-359.

Malinen, T., 2016. Who Caused the Great Recession?. [Online]. Available through:

<http://www.huffingtonpost.in/entry/who-caused-the-great-rece_b_9805056>. [Accessed

on 26th July 2016].

McKibbin, J. W. and Stoeckel, A., 2009. The Global Financial Crisis: Causes and

Consequences. [PDF]. Available through:

<http://www.lowyinstitute.org/files/pubfiles/McKibbin_and_Stoeckel,_The_global_finan

cial_crisis.pdf>. [Accessed on 26th July 2016].

Pesch, M., 2011. Financial Crisis: Flawed Incentives Cause Banking Crises. [Online]. Available

through: <http://www.grin.com/en/e-book/164361/financial-crisis-flawed-incentives-

cause-banking-crises>. [Accessed on 26th July 2016].

7 | P a g e

Rajan, U, Seru, A. and Vig, V., 2008. The Failure of Models that Predict Failure: Distance,

Incentives and Defaults. Chicago GSB Research. pp.08-19.

Tonks, I., 2012. Bankers’ bonuses and the financial crisis. [PDF]. Available through:

<http://voxeu.org/article/bankers-bonuses-and-financial-crisis>. [Accessed on 26th July

2016].

8 | P a g e

Incentives and Defaults. Chicago GSB Research. pp.08-19.

Tonks, I., 2012. Bankers’ bonuses and the financial crisis. [PDF]. Available through:

<http://voxeu.org/article/bankers-bonuses-and-financial-crisis>. [Accessed on 26th July

2016].

8 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.