Assessment 2: Audited Financial Report and Statements Analysis

VerifiedAdded on 2020/06/04

|9

|1456

|50

Report

AI Summary

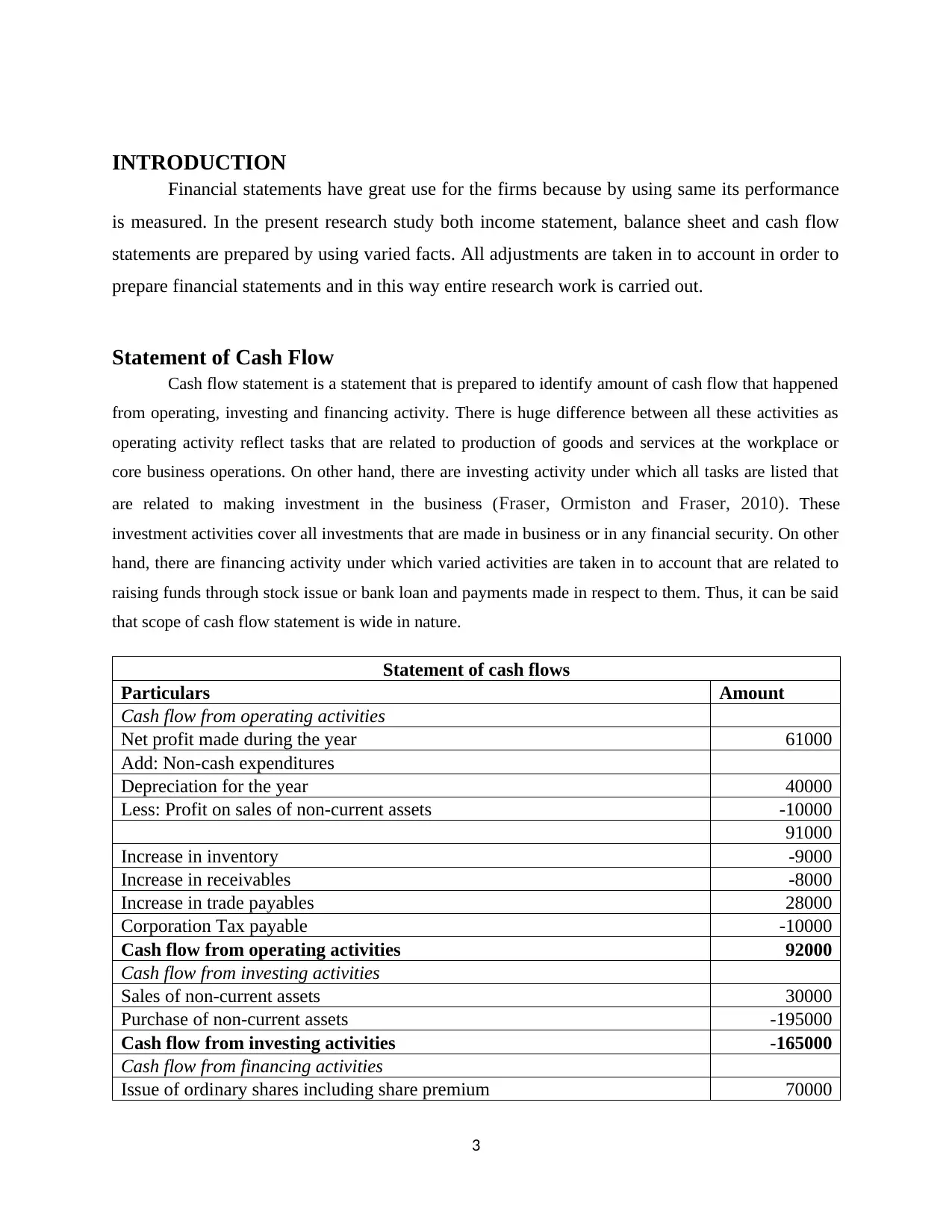

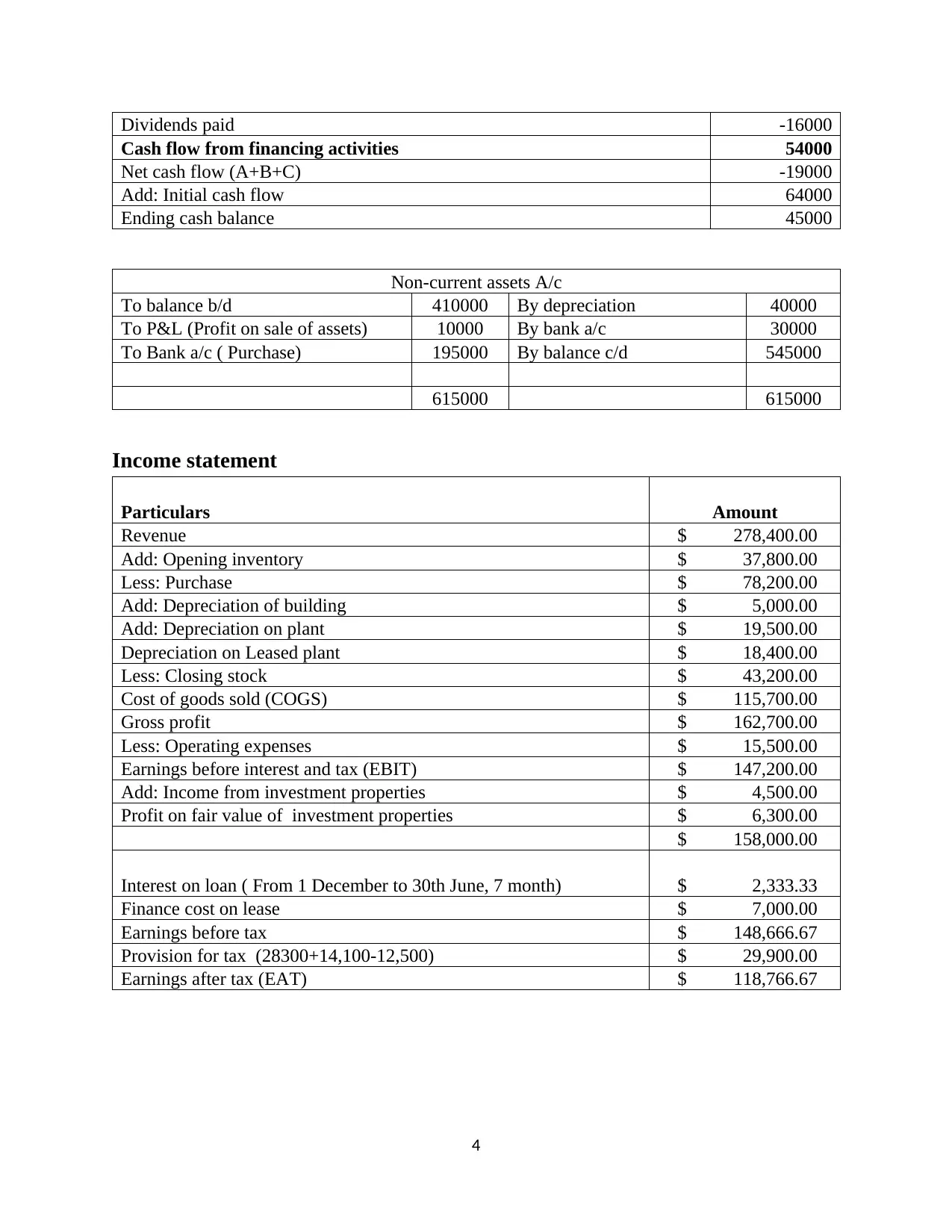

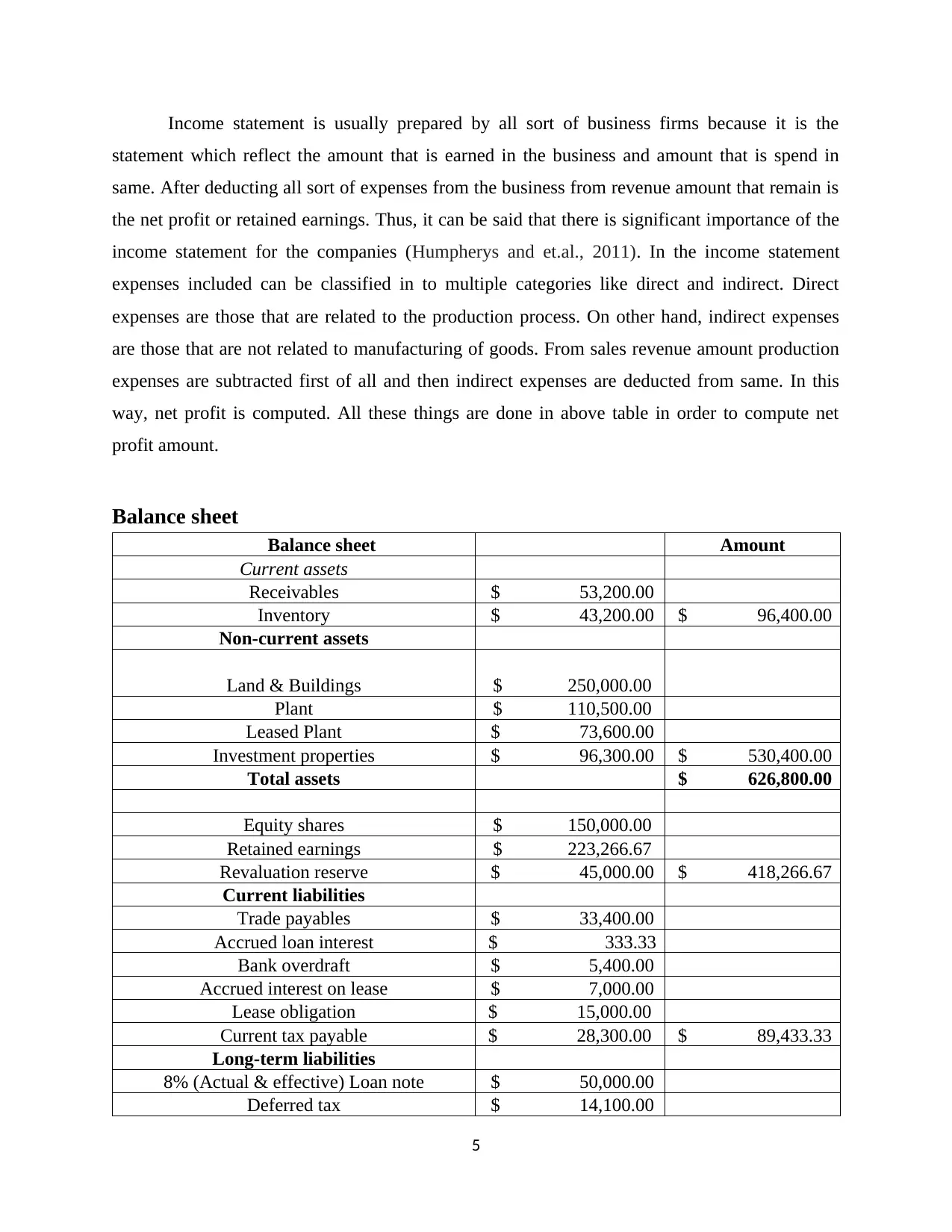

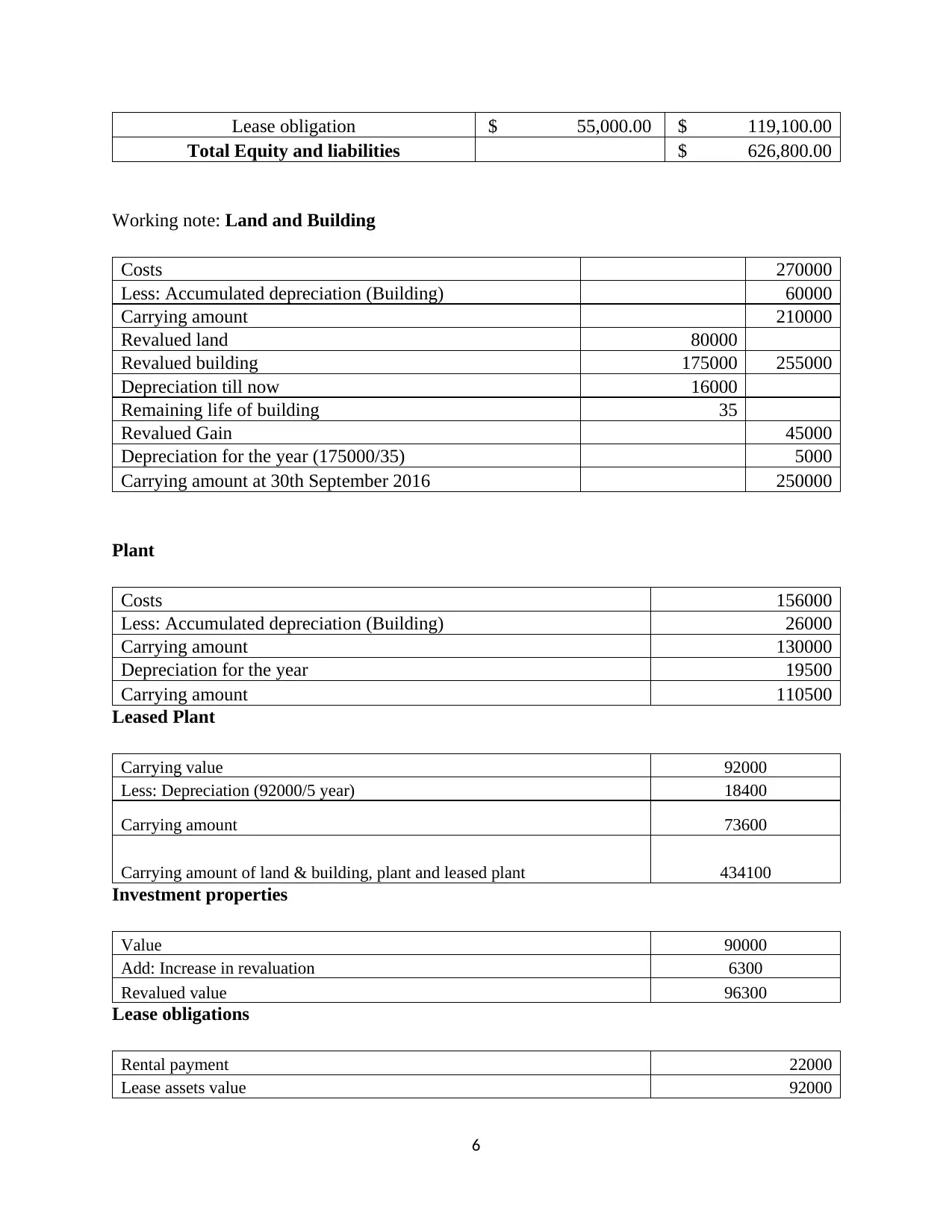

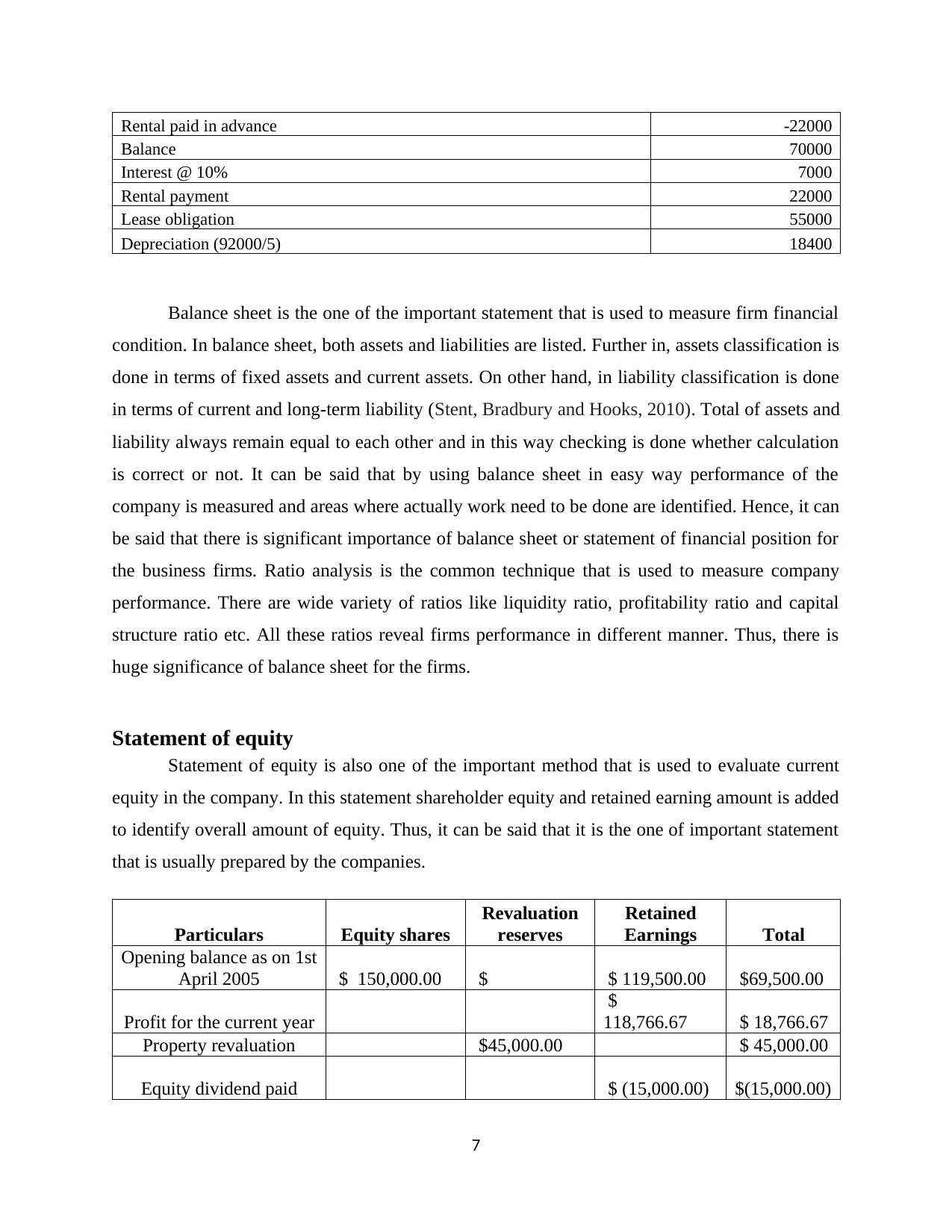

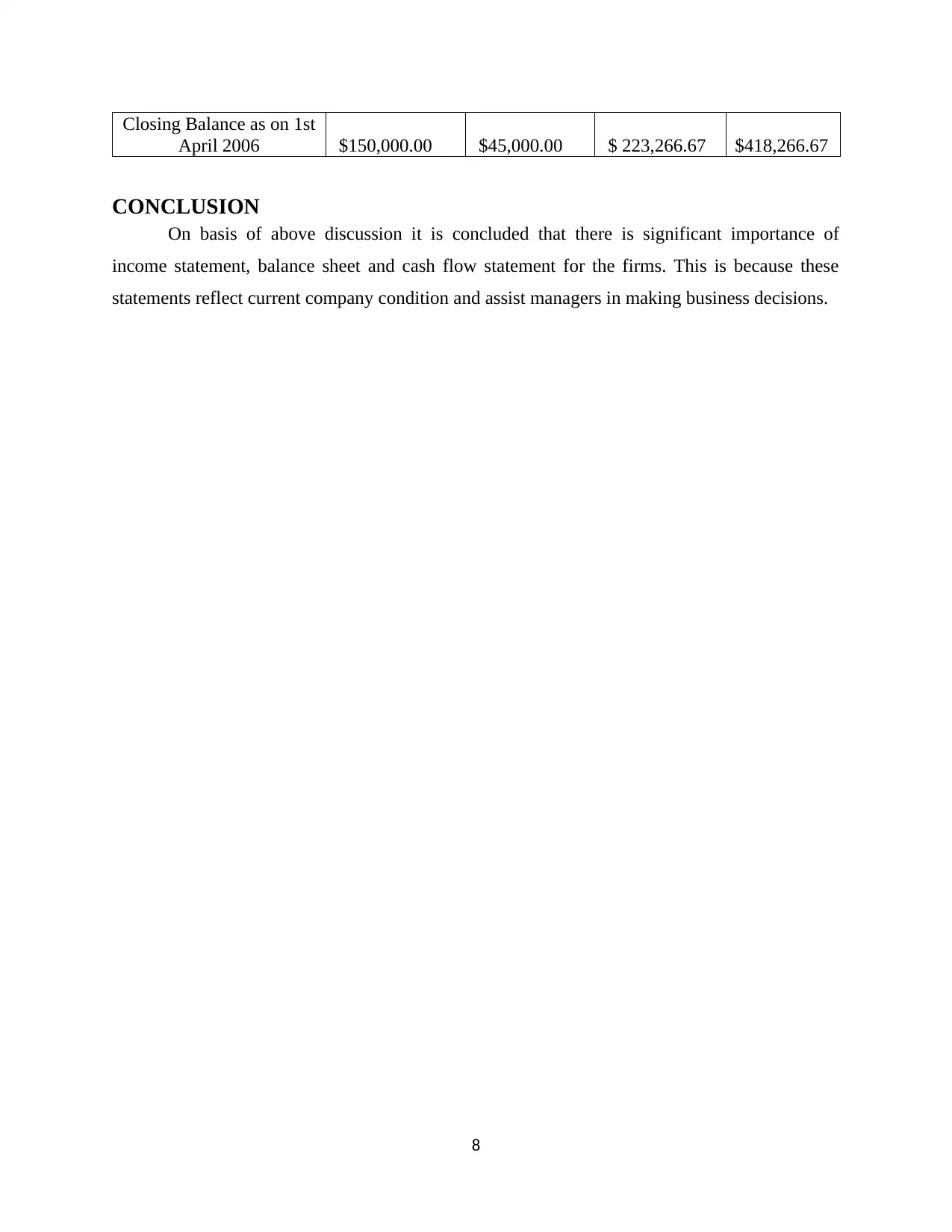

This report provides a detailed analysis of audited financial statements, encompassing the income statement, balance sheet, and cash flow statement. The income statement reveals the revenue, cost of goods sold, and expenses, culminating in the calculation of net profit. The balance sheet presents a snapshot of the company's assets, liabilities, and equity, providing insights into its financial position. The cash flow statement details the movement of cash through operating, investing, and financing activities. The report includes calculations, adjustments, and working notes to support the presented financial data. The analysis highlights the significance of these financial statements for measuring a firm's performance and supporting informed business decisions. The report covers key financial metrics, including profitability, liquidity, and solvency ratios, to provide a comprehensive overview of the company's financial health.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.