Taxation Assignment 6004 LBSAF: Income and National Insurance

VerifiedAdded on 2023/04/19

|15

|2397

|179

Homework Assignment

AI Summary

This assignment presents a comprehensive taxation analysis for Rebekah Oliver, a client of Harrison & Hawes LLP, a firm of Chartered Accountants. The assignment explores two work opportunities: employment and self-employment, along with her property and investment income. It calculates the total income tax and National Insurance contributions for both scenarios, considering various income sources like employment income, property income, bank interest, and dividends. Detailed explanations are provided for the tax treatment of each item, including deductions for pension, car and fuel benefits, and loans from the employer. The analysis also covers capital allowances for self-employment, and a memorandum to Rebekah summarizing the tax calculations and relevant regulations. The document includes detailed workings and a bibliography for reference. The assignment provides a clear understanding of the financial implications of each employment choice, aiding Rebekah in making informed decisions regarding her tax obligations and overall financial planning.

TAXATION

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

SECTION A: Option 1 – Employment............................................................................................3

SECTION A: Option 2 – Self Employment....................................................................................5

SECTION B.....................................................................................................................................7

Bibliography..................................................................................................................................10

Workings........................................................................................................................................11

SECTION A: Option 1 – Employment............................................................................................3

SECTION A: Option 2 – Self Employment....................................................................................5

SECTION B.....................................................................................................................................7

Bibliography..................................................................................................................................10

Workings........................................................................................................................................11

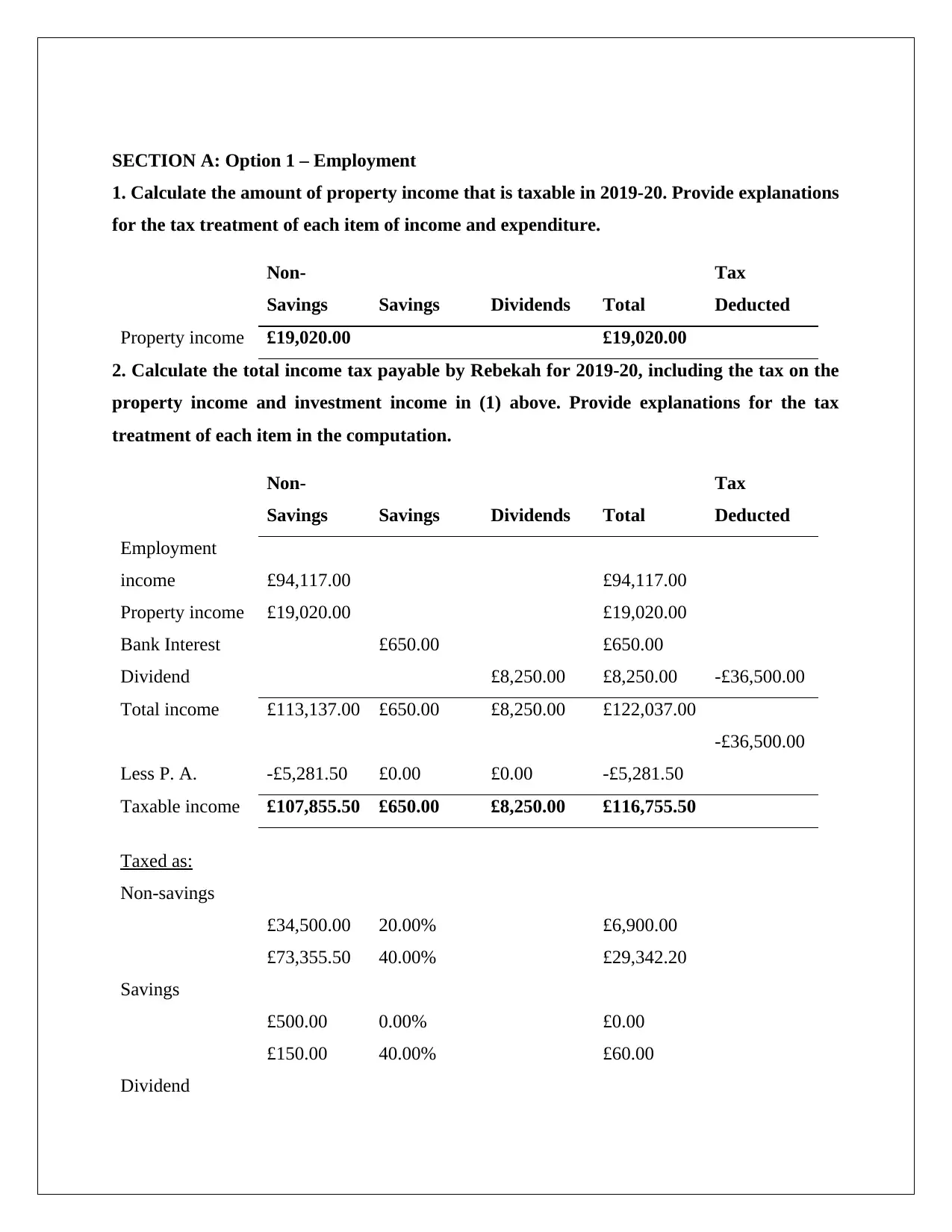

SECTION A: Option 1 – Employment

1. Calculate the amount of property income that is taxable in 2019-20. Provide explanations

for the tax treatment of each item of income and expenditure.

Non-

Savings Savings Dividends Total

Tax

Deducted

Property income £19,020.00 £19,020.00

2. Calculate the total income tax payable by Rebekah for 2019-20, including the tax on the

property income and investment income in (1) above. Provide explanations for the tax

treatment of each item in the computation.

Non-

Savings Savings Dividends Total

Tax

Deducted

Employment

income £94,117.00 £94,117.00

Property income £19,020.00 £19,020.00

Bank Interest £650.00 £650.00

Dividend £8,250.00 £8,250.00 -£36,500.00

Total income £113,137.00 £650.00 £8,250.00 £122,037.00

-£36,500.00

Less P. A. -£5,281.50 £0.00 £0.00 -£5,281.50

Taxable income £107,855.50 £650.00 £8,250.00 £116,755.50

Taxed as:

Non-savings

£34,500.00 20.00% £6,900.00

£73,355.50 40.00% £29,342.20

Savings

£500.00 0.00% £0.00

£150.00 40.00% £60.00

Dividend

1. Calculate the amount of property income that is taxable in 2019-20. Provide explanations

for the tax treatment of each item of income and expenditure.

Non-

Savings Savings Dividends Total

Tax

Deducted

Property income £19,020.00 £19,020.00

2. Calculate the total income tax payable by Rebekah for 2019-20, including the tax on the

property income and investment income in (1) above. Provide explanations for the tax

treatment of each item in the computation.

Non-

Savings Savings Dividends Total

Tax

Deducted

Employment

income £94,117.00 £94,117.00

Property income £19,020.00 £19,020.00

Bank Interest £650.00 £650.00

Dividend £8,250.00 £8,250.00 -£36,500.00

Total income £113,137.00 £650.00 £8,250.00 £122,037.00

-£36,500.00

Less P. A. -£5,281.50 £0.00 £0.00 -£5,281.50

Taxable income £107,855.50 £650.00 £8,250.00 £116,755.50

Taxed as:

Non-savings

£34,500.00 20.00% £6,900.00

£73,355.50 40.00% £29,342.20

Savings

£500.00 0.00% £0.00

£150.00 40.00% £60.00

Dividend

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

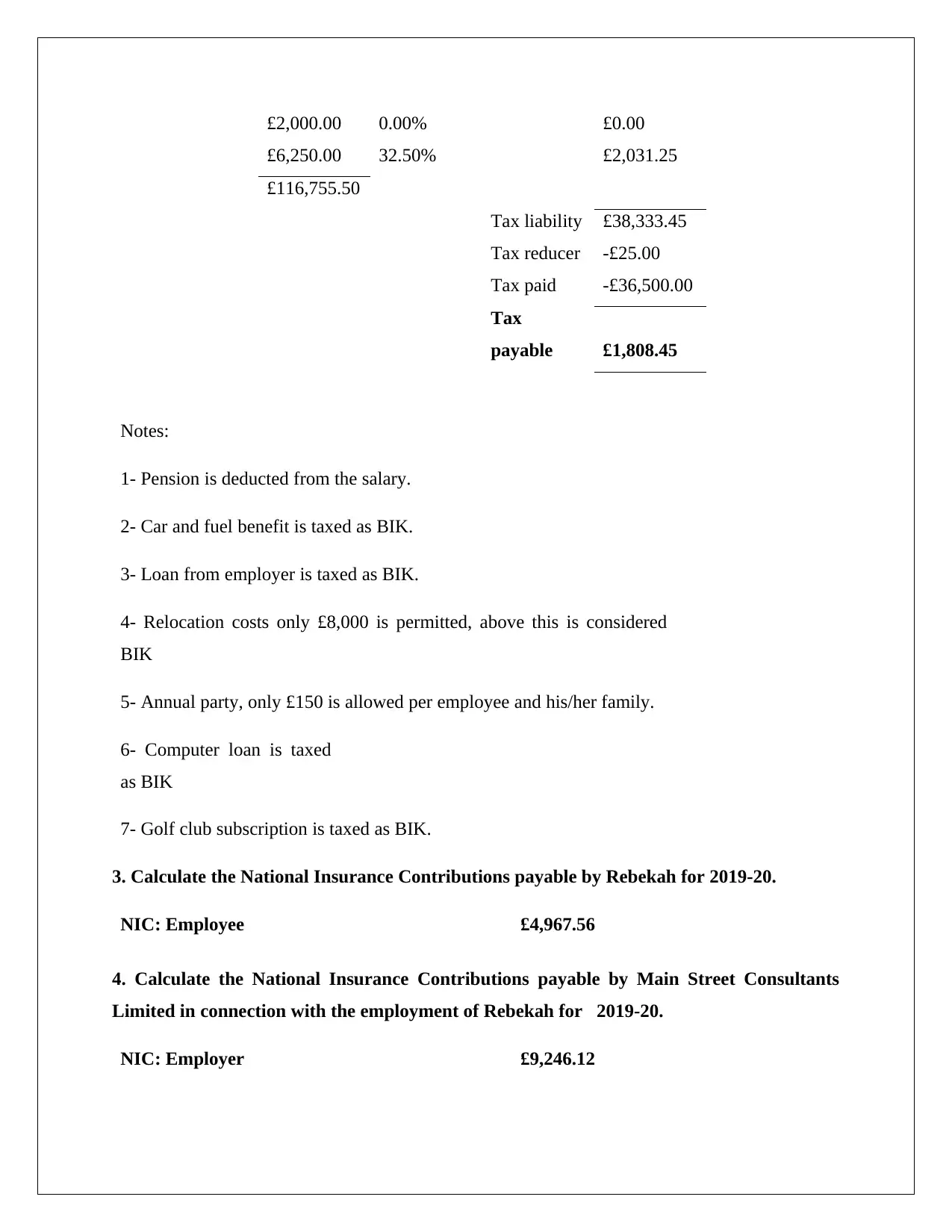

£2,000.00 0.00% £0.00

£6,250.00 32.50% £2,031.25

£116,755.50

Tax liability £38,333.45

Tax reducer -£25.00

Tax paid -£36,500.00

Tax

payable £1,808.45

Notes:

1- Pension is deducted from the salary.

2- Car and fuel benefit is taxed as BIK.

3- Loan from employer is taxed as BIK.

4- Relocation costs only £8,000 is permitted, above this is considered

BIK

5- Annual party, only £150 is allowed per employee and his/her family.

6- Computer loan is taxed

as BIK

7- Golf club subscription is taxed as BIK.

3. Calculate the National Insurance Contributions payable by Rebekah for 2019-20.

NIC: Employee £4,967.56

4. Calculate the National Insurance Contributions payable by Main Street Consultants

Limited in connection with the employment of Rebekah for 2019-20.

NIC: Employer £9,246.12

£6,250.00 32.50% £2,031.25

£116,755.50

Tax liability £38,333.45

Tax reducer -£25.00

Tax paid -£36,500.00

Tax

payable £1,808.45

Notes:

1- Pension is deducted from the salary.

2- Car and fuel benefit is taxed as BIK.

3- Loan from employer is taxed as BIK.

4- Relocation costs only £8,000 is permitted, above this is considered

BIK

5- Annual party, only £150 is allowed per employee and his/her family.

6- Computer loan is taxed

as BIK

7- Golf club subscription is taxed as BIK.

3. Calculate the National Insurance Contributions payable by Rebekah for 2019-20.

NIC: Employee £4,967.56

4. Calculate the National Insurance Contributions payable by Main Street Consultants

Limited in connection with the employment of Rebekah for 2019-20.

NIC: Employer £9,246.12

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

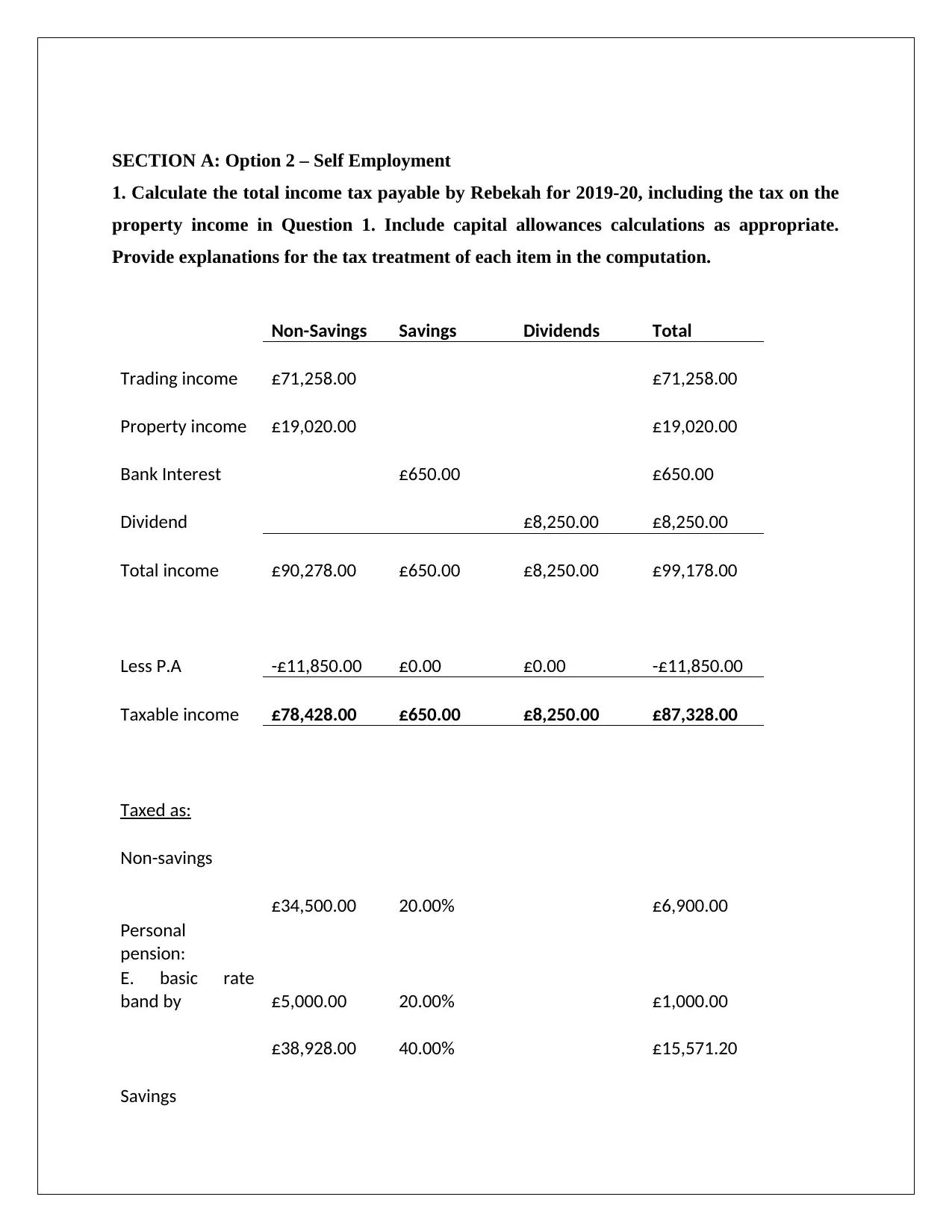

SECTION A: Option 2 – Self Employment

1. Calculate the total income tax payable by Rebekah for 2019-20, including the tax on the

property income in Question 1. Include capital allowances calculations as appropriate.

Provide explanations for the tax treatment of each item in the computation.

Non-Savings Savings Dividends Total

Trading income £71,258.00 £71,258.00

Property income £19,020.00 £19,020.00

Bank Interest £650.00 £650.00

Dividend £8,250.00 £8,250.00

Total income £90,278.00 £650.00 £8,250.00 £99,178.00

Less P.A -£11,850.00 £0.00 £0.00 -£11,850.00

Taxable income £78,428.00 £650.00 £8,250.00 £87,328.00

Taxed as:

Non-savings

£34,500.00 20.00% £6,900.00

Personal

pension:

E. basic rate

band by £5,000.00 20.00% £1,000.00

£38,928.00 40.00% £15,571.20

Savings

1. Calculate the total income tax payable by Rebekah for 2019-20, including the tax on the

property income in Question 1. Include capital allowances calculations as appropriate.

Provide explanations for the tax treatment of each item in the computation.

Non-Savings Savings Dividends Total

Trading income £71,258.00 £71,258.00

Property income £19,020.00 £19,020.00

Bank Interest £650.00 £650.00

Dividend £8,250.00 £8,250.00

Total income £90,278.00 £650.00 £8,250.00 £99,178.00

Less P.A -£11,850.00 £0.00 £0.00 -£11,850.00

Taxable income £78,428.00 £650.00 £8,250.00 £87,328.00

Taxed as:

Non-savings

£34,500.00 20.00% £6,900.00

Personal

pension:

E. basic rate

band by £5,000.00 20.00% £1,000.00

£38,928.00 40.00% £15,571.20

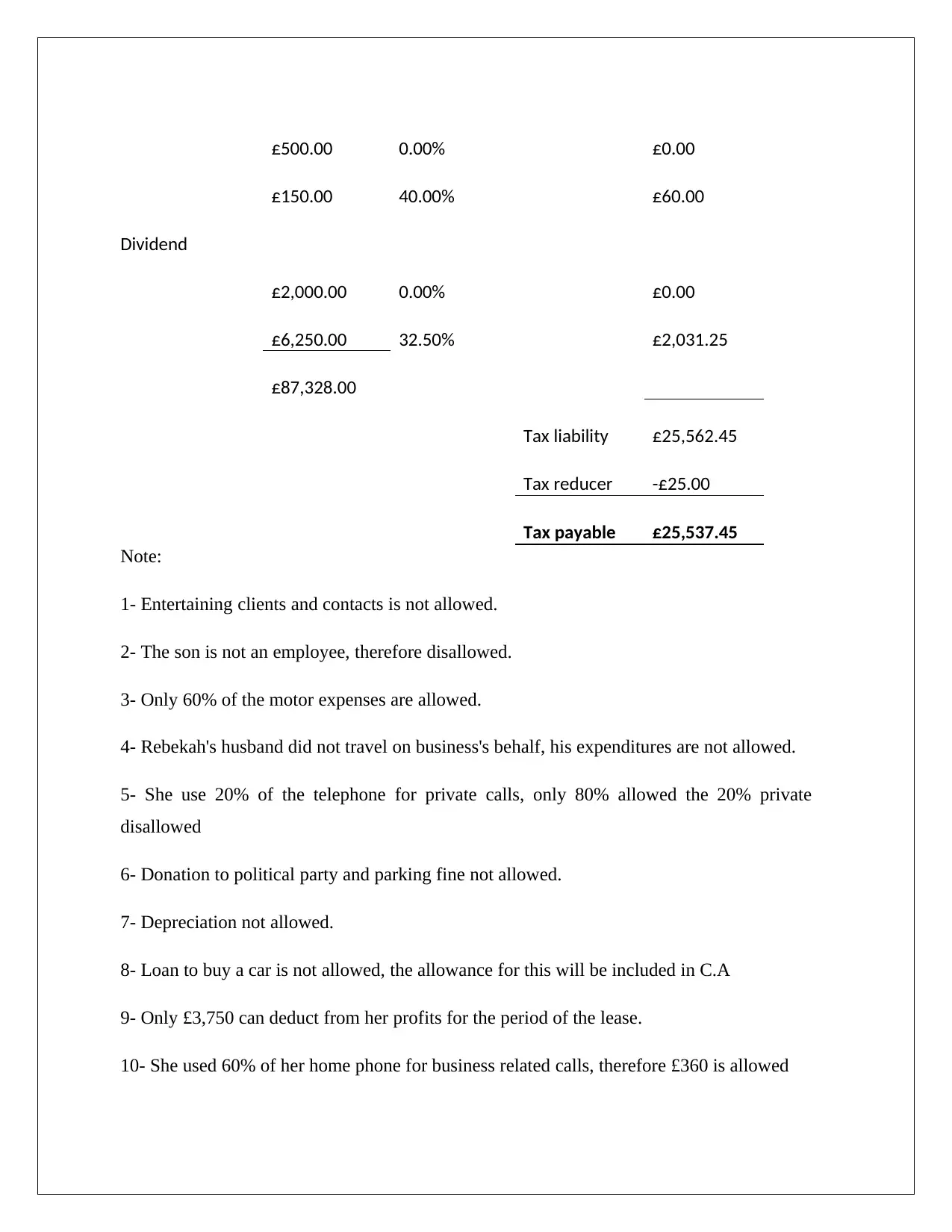

Savings

£500.00 0.00% £0.00

£150.00 40.00% £60.00

Dividend

£2,000.00 0.00% £0.00

£6,250.00 32.50% £2,031.25

£87,328.00

Tax liability £25,562.45

Tax reducer -£25.00

Tax payable £25,537.45

Note:

1- Entertaining clients and contacts is not allowed.

2- The son is not an employee, therefore disallowed.

3- Only 60% of the motor expenses are allowed.

4- Rebekah's husband did not travel on business's behalf, his expenditures are not allowed.

5- She use 20% of the telephone for private calls, only 80% allowed the 20% private

disallowed

6- Donation to political party and parking fine not allowed.

7- Depreciation not allowed.

8- Loan to buy a car is not allowed, the allowance for this will be included in C.A

9- Only £3,750 can deduct from her profits for the period of the lease.

10- She used 60% of her home phone for business related calls, therefore £360 is allowed

£150.00 40.00% £60.00

Dividend

£2,000.00 0.00% £0.00

£6,250.00 32.50% £2,031.25

£87,328.00

Tax liability £25,562.45

Tax reducer -£25.00

Tax payable £25,537.45

Note:

1- Entertaining clients and contacts is not allowed.

2- The son is not an employee, therefore disallowed.

3- Only 60% of the motor expenses are allowed.

4- Rebekah's husband did not travel on business's behalf, his expenditures are not allowed.

5- She use 20% of the telephone for private calls, only 80% allowed the 20% private

disallowed

6- Donation to political party and parking fine not allowed.

7- Depreciation not allowed.

8- Loan to buy a car is not allowed, the allowance for this will be included in C.A

9- Only £3,750 can deduct from her profits for the period of the lease.

10- She used 60% of her home phone for business related calls, therefore £360 is allowed

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

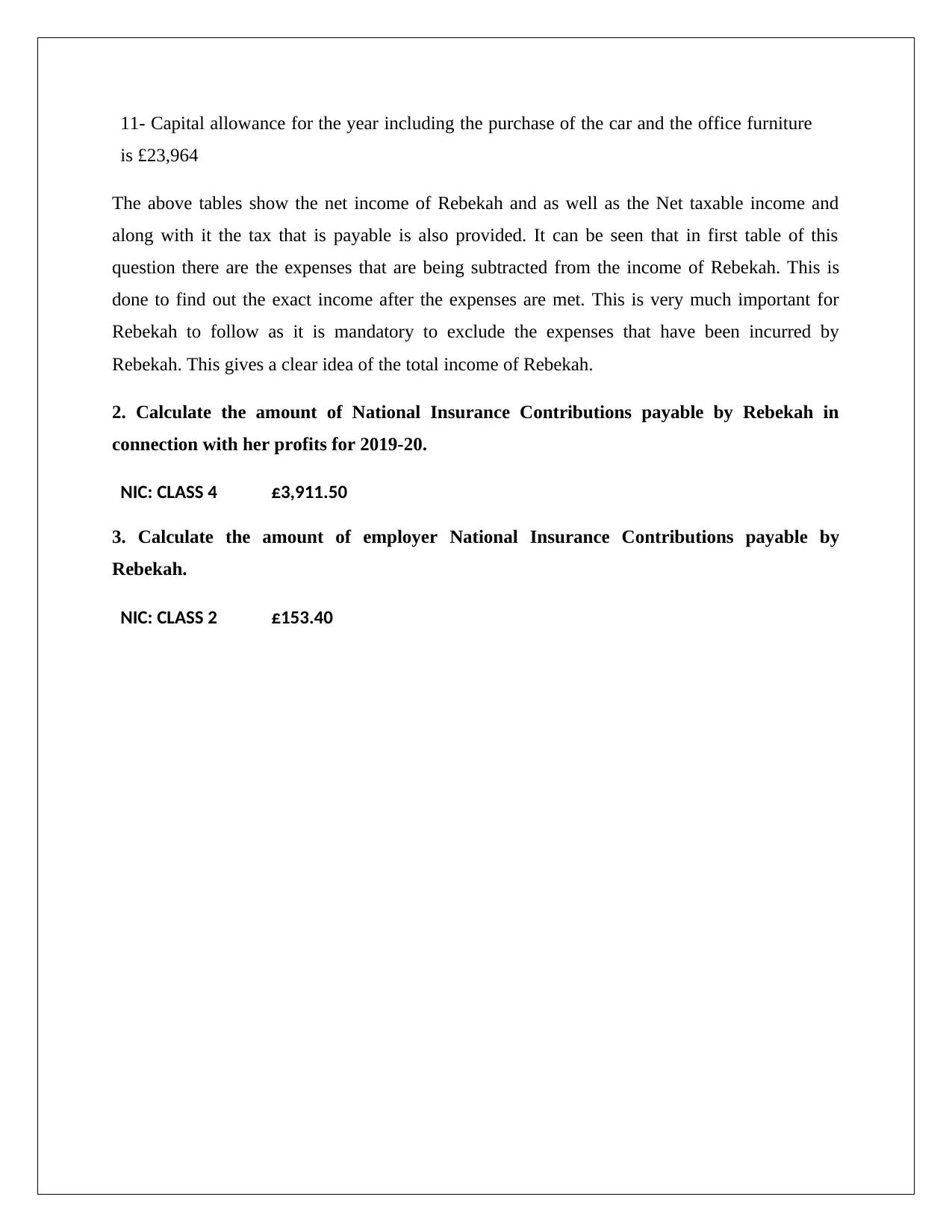

11- Capital allowance for the year including the purchase of the car and the office furniture

is £23,964

The above tables show the net income of Rebekah and as well as the Net taxable income and

along with it the tax that is payable is also provided. It can be seen that in first table of this

question there are the expenses that are being subtracted from the income of Rebekah. This is

done to find out the exact income after the expenses are met. This is very much important for

Rebekah to follow as it is mandatory to exclude the expenses that have been incurred by

Rebekah. This gives a clear idea of the total income of Rebekah.

2. Calculate the amount of National Insurance Contributions payable by Rebekah in

connection with her profits for 2019-20.

NIC: CLASS 4 £3,911.50

3. Calculate the amount of employer National Insurance Contributions payable by

Rebekah.

NIC: CLASS 2 £153.40

is £23,964

The above tables show the net income of Rebekah and as well as the Net taxable income and

along with it the tax that is payable is also provided. It can be seen that in first table of this

question there are the expenses that are being subtracted from the income of Rebekah. This is

done to find out the exact income after the expenses are met. This is very much important for

Rebekah to follow as it is mandatory to exclude the expenses that have been incurred by

Rebekah. This gives a clear idea of the total income of Rebekah.

2. Calculate the amount of National Insurance Contributions payable by Rebekah in

connection with her profits for 2019-20.

NIC: CLASS 4 £3,911.50

3. Calculate the amount of employer National Insurance Contributions payable by

Rebekah.

NIC: CLASS 2 £153.40

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

SECTION B

To Rebekah

From Advisor

Date: February 8, 2019

Subject: Memorandum of Business

This is hereby to inform you that the calculations of the income tax are done according to the

rules set by the office of the income tax. There are a number of tables that are attached for you to

have a look at the taxable income and the amount that is needed to be paid by you. As per the

conversation with you, it can be seen that there are a number of expenses that have been incurred

and all are taken into consideration for the income tax calculation. In addition to this, it can be

also inferred that there are various considerations which are considered. All deductions are done

based on rules and regulations. After considering all the deductions, capital gains tax payable has

been calculated. In the given case study, as per taxation acts, individuals cannot claim income

tax deductions for the costs of property as it generate rental income. However, few costs may

reduce the CGT (Capital Gains Tax liability) for an individual. Due to this reason while

calculating income tax payable, property income has been considered for the given case. In

addition to this, it can be inferred that PAYG has been deducted from Annual salary. In UK if the

income slab is between $37,001 – $90,000, then, total tax payable will be $3572 plus 32.5c for

each $1 above $37000. From the above analysis, it can be inferred that the total income tax

payable is $9399.14. This can be considered to be higher. However, some amount of rebate can

be claimed by Rebekah in order to minimize the total amount of CGT for the financial year

2019. It can be seen that in first table of this question there are the expenses that are being

subtracted from the income of Rebekah. This is done to find out the exact income after the

expenses are met. This is very much important for Rebekah to follow as it is mandatory to

exclude the expenses that have been incurred by Rebekah.

In addition to this, there are various items are not included while assessing taxable income.

These are as follows:-

To Rebekah

From Advisor

Date: February 8, 2019

Subject: Memorandum of Business

This is hereby to inform you that the calculations of the income tax are done according to the

rules set by the office of the income tax. There are a number of tables that are attached for you to

have a look at the taxable income and the amount that is needed to be paid by you. As per the

conversation with you, it can be seen that there are a number of expenses that have been incurred

and all are taken into consideration for the income tax calculation. In addition to this, it can be

also inferred that there are various considerations which are considered. All deductions are done

based on rules and regulations. After considering all the deductions, capital gains tax payable has

been calculated. In the given case study, as per taxation acts, individuals cannot claim income

tax deductions for the costs of property as it generate rental income. However, few costs may

reduce the CGT (Capital Gains Tax liability) for an individual. Due to this reason while

calculating income tax payable, property income has been considered for the given case. In

addition to this, it can be inferred that PAYG has been deducted from Annual salary. In UK if the

income slab is between $37,001 – $90,000, then, total tax payable will be $3572 plus 32.5c for

each $1 above $37000. From the above analysis, it can be inferred that the total income tax

payable is $9399.14. This can be considered to be higher. However, some amount of rebate can

be claimed by Rebekah in order to minimize the total amount of CGT for the financial year

2019. It can be seen that in first table of this question there are the expenses that are being

subtracted from the income of Rebekah. This is done to find out the exact income after the

expenses are met. This is very much important for Rebekah to follow as it is mandatory to

exclude the expenses that have been incurred by Rebekah.

In addition to this, there are various items are not included while assessing taxable income.

These are as follows:-

child care receipts underneath indicated cutoff points courage grants – annuities and extra

benefits paid to holders of the Victoria Cross, George Cross and most other valiance decorations

are non-assessable holocaust exploited people – remuneration, home enhancement stipends from

your Local Authority, emergency clinic patients' voyaging costs under the Hospital Travel

Scheme, lodging stipends from your Local Authority ,pay or harms granted for individual

wounds whether got in one single amount or over a period and whether granted by a court or out

of court settlement enthusiasm up to the season of judgment granted by a court on pay or harms

for individual wounds legal hearers' budgetary misfortune stipend, if the member of the jury is a

representative life confirmation strategies – certain rewards and benefits long administration

grants to representatives following 20 years of administration, where the blessing does not

surpass £50 for every time of administration and where the blessing is substantial, for instance a

check or offers in an organization. A money grant is normally assessable except if it is an erratic

installment which is excluded in your agreement of work upkeep installments got from a life

partner or common accomplice excavators' free coal or money in lieu of coal certain annuities.

Intentional benefits which are not associated with a past activity and to which you contribute

yearly are tax-exempt. Incapacity annuities of individuals from the military are tax-exempt. Any

annuity granted to you as a worker on retirement in view of damage at work is tax-exempt

German and Austrian annuities and benefits for casualties of Nazi mistreatment single amount

benefits installments (greatest 25% of the capital incentive up to a specific point of confinement

remuneration and enthusiasm for mis-sold individual annuities taken out between 29 April 1988

and 30 June 1994 comprehensive protection benefits paid to you on the off chance that you are

debilitated, incapacitated or jobless to meet your budgetary responsibilities, for instance, benefits

paid under home loan security protection, changeless medical coverage, installment assurance

(leaser) protection and long haul care protection strike pay and joblessness pay from worker's

guilds ,premium bond prizes, rewards from the National Lottery and football pools, and from

wagering for instance, horse hustling ,property pay - the first £1,000 of salary from leasing some

portion of your property is tax-exempt, for instance leasing a parking spot on your drive (this is

isolated to the Rent a Room plot) ,acquired annuities – capital component of the sum you get the

first £30,000 of instalments which are pay for loss of a vocation, including statutory and legally

binding repetition instalments and, in specific cases, a single amount instalment in lieu of notice.

benefits paid to holders of the Victoria Cross, George Cross and most other valiance decorations

are non-assessable holocaust exploited people – remuneration, home enhancement stipends from

your Local Authority, emergency clinic patients' voyaging costs under the Hospital Travel

Scheme, lodging stipends from your Local Authority ,pay or harms granted for individual

wounds whether got in one single amount or over a period and whether granted by a court or out

of court settlement enthusiasm up to the season of judgment granted by a court on pay or harms

for individual wounds legal hearers' budgetary misfortune stipend, if the member of the jury is a

representative life confirmation strategies – certain rewards and benefits long administration

grants to representatives following 20 years of administration, where the blessing does not

surpass £50 for every time of administration and where the blessing is substantial, for instance a

check or offers in an organization. A money grant is normally assessable except if it is an erratic

installment which is excluded in your agreement of work upkeep installments got from a life

partner or common accomplice excavators' free coal or money in lieu of coal certain annuities.

Intentional benefits which are not associated with a past activity and to which you contribute

yearly are tax-exempt. Incapacity annuities of individuals from the military are tax-exempt. Any

annuity granted to you as a worker on retirement in view of damage at work is tax-exempt

German and Austrian annuities and benefits for casualties of Nazi mistreatment single amount

benefits installments (greatest 25% of the capital incentive up to a specific point of confinement

remuneration and enthusiasm for mis-sold individual annuities taken out between 29 April 1988

and 30 June 1994 comprehensive protection benefits paid to you on the off chance that you are

debilitated, incapacitated or jobless to meet your budgetary responsibilities, for instance, benefits

paid under home loan security protection, changeless medical coverage, installment assurance

(leaser) protection and long haul care protection strike pay and joblessness pay from worker's

guilds ,premium bond prizes, rewards from the National Lottery and football pools, and from

wagering for instance, horse hustling ,property pay - the first £1,000 of salary from leasing some

portion of your property is tax-exempt, for instance leasing a parking spot on your drive (this is

isolated to the Rent a Room plot) ,acquired annuities – capital component of the sum you get the

first £30,000 of instalments which are pay for loss of a vocation, including statutory and legally

binding repetition instalments and, in specific cases, a single amount instalment in lieu of notice.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

There are two processes through which the income tax is calculated. The better advantage of

finance for you is the self-employment where there is more income left after the tax is paid than

the other part. This is very much important for you to check. This is because as per our

conversation, it is only the profitable one that you will follow. The calculations are done

according to the rules and regulations of the taxation office of England and Wales. This is very

much important for you to have a look into everything and decide accordingly. These are the

different rules and regulations that needs to be followed.

Hope you will like the work that we have done for you and please feel free to give us the

feedback and if you want to know more feel free to contact us by our mail-id. If you have any

kind of queries send us a mail and the explanation will be given. In addition to this, if you have

any suggestions, please let us know. We will be highly obliged if you post us your valuable

suggestions. We are waiting for your positive response regarding this memorandum.

Thanks and Regards.

finance for you is the self-employment where there is more income left after the tax is paid than

the other part. This is very much important for you to check. This is because as per our

conversation, it is only the profitable one that you will follow. The calculations are done

according to the rules and regulations of the taxation office of England and Wales. This is very

much important for you to have a look into everything and decide accordingly. These are the

different rules and regulations that needs to be followed.

Hope you will like the work that we have done for you and please feel free to give us the

feedback and if you want to know more feel free to contact us by our mail-id. If you have any

kind of queries send us a mail and the explanation will be given. In addition to this, if you have

any suggestions, please let us know. We will be highly obliged if you post us your valuable

suggestions. We are waiting for your positive response regarding this memorandum.

Thanks and Regards.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Bibliography

Bankman, J., Shaviro, D.N., Stark, K.J. and Kleinbard, E.D., 2018. Federal Income Taxation.

Aspen Casebook.

Blomquist, S. and Simula, L., 2018. Marginal deadweight loss when the income tax is

nonlinear. Journal of Econometrics.

Leroy, F. and Muller-Plathe, F., 2016. Calculation of the Work of Adhesion of Solid-Liquid

Interfaces by Molecular Dynamics Simulations. In NIC Symp.

Tateishi, N., Kouge, K., Tokoda, K., Kotani, I., Ohta, S., Nakazawa, T., Matsuda, S., Li, H.,

Kandani, K., Nakamura, S. and Miyagawa, Y., 2016. Load calculation method, load calculation

program, and load calculation apparatus. U.S. Patent Application 14/987,804.

Bankman, J., Shaviro, D.N., Stark, K.J. and Kleinbard, E.D., 2018. Federal Income Taxation.

Aspen Casebook.

Blomquist, S. and Simula, L., 2018. Marginal deadweight loss when the income tax is

nonlinear. Journal of Econometrics.

Leroy, F. and Muller-Plathe, F., 2016. Calculation of the Work of Adhesion of Solid-Liquid

Interfaces by Molecular Dynamics Simulations. In NIC Symp.

Tateishi, N., Kouge, K., Tokoda, K., Kotani, I., Ohta, S., Nakazawa, T., Matsuda, S., Li, H.,

Kandani, K., Nakamura, S. and Miyagawa, Y., 2016. Load calculation method, load calculation

program, and load calculation apparatus. U.S. Patent Application 14/987,804.

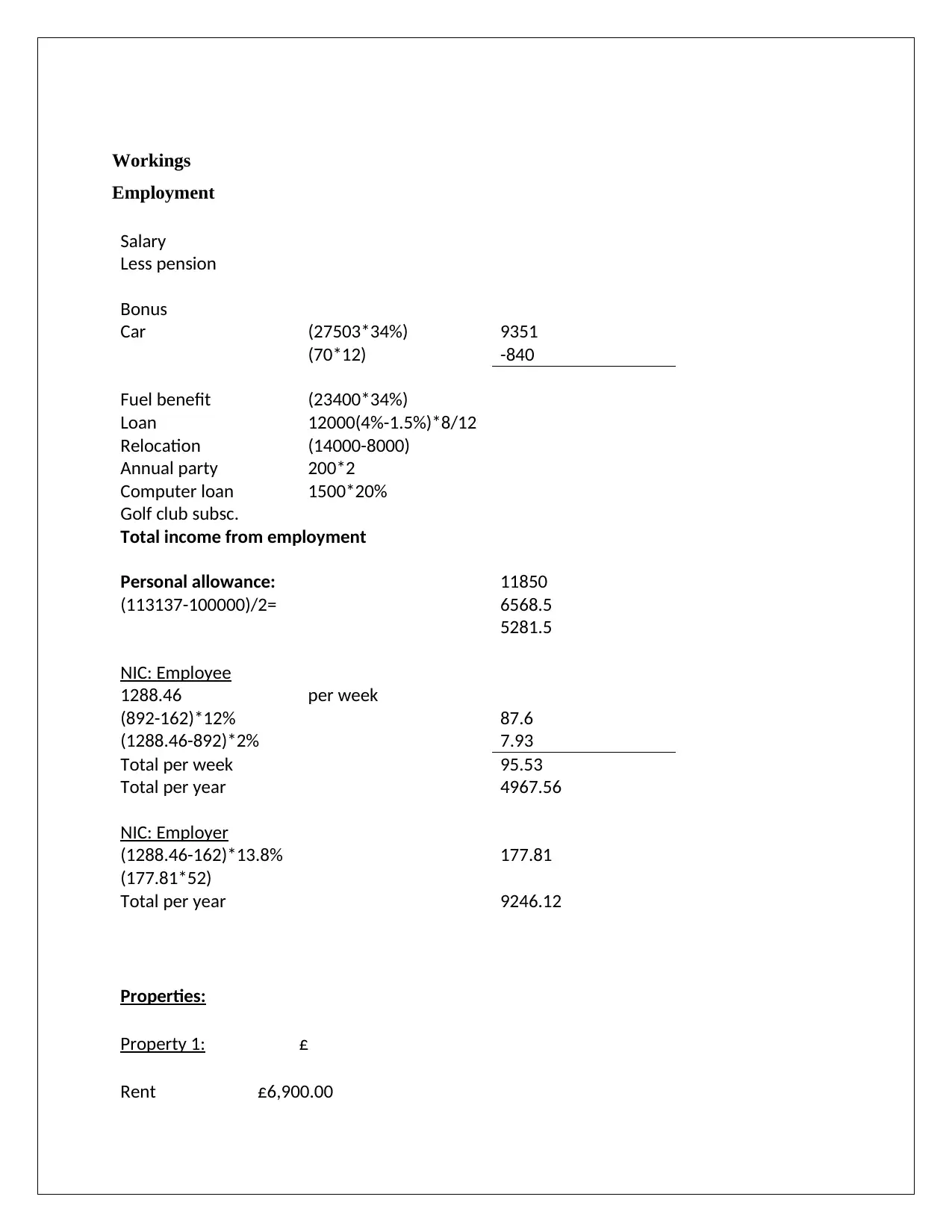

Workings

Employment

Salary

Less pension

Bonus

Car (27503*34%) 9351

(70*12) -840

Fuel benefit (23400*34%)

Loan 12000(4%-1.5%)*8/12

Relocation (14000-8000)

Annual party 200*2

Computer loan 1500*20%

Golf club subsc.

Total income from employment

Personal allowance: 11850

(113137-100000)/2= 6568.5

5281.5

NIC: Employee

1288.46 per week

(892-162)*12% 87.6

(1288.46-892)*2% 7.93

Total per week 95.53

Total per year 4967.56

NIC: Employer

(1288.46-162)*13.8% 177.81

(177.81*52)

Total per year 9246.12

Properties:

Property 1: £

Rent £6,900.00

Employment

Salary

Less pension

Bonus

Car (27503*34%) 9351

(70*12) -840

Fuel benefit (23400*34%)

Loan 12000(4%-1.5%)*8/12

Relocation (14000-8000)

Annual party 200*2

Computer loan 1500*20%

Golf club subsc.

Total income from employment

Personal allowance: 11850

(113137-100000)/2= 6568.5

5281.5

NIC: Employee

1288.46 per week

(892-162)*12% 87.6

(1288.46-892)*2% 7.93

Total per week 95.53

Total per year 4967.56

NIC: Employer

(1288.46-162)*13.8% 177.81

(177.81*52)

Total per year 9246.12

Properties:

Property 1: £

Rent £6,900.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.