Accounting for Business: Revenue Recognition and Financial Analysis

VerifiedAdded on 2023/06/04

|8

|1319

|53

Report

AI Summary

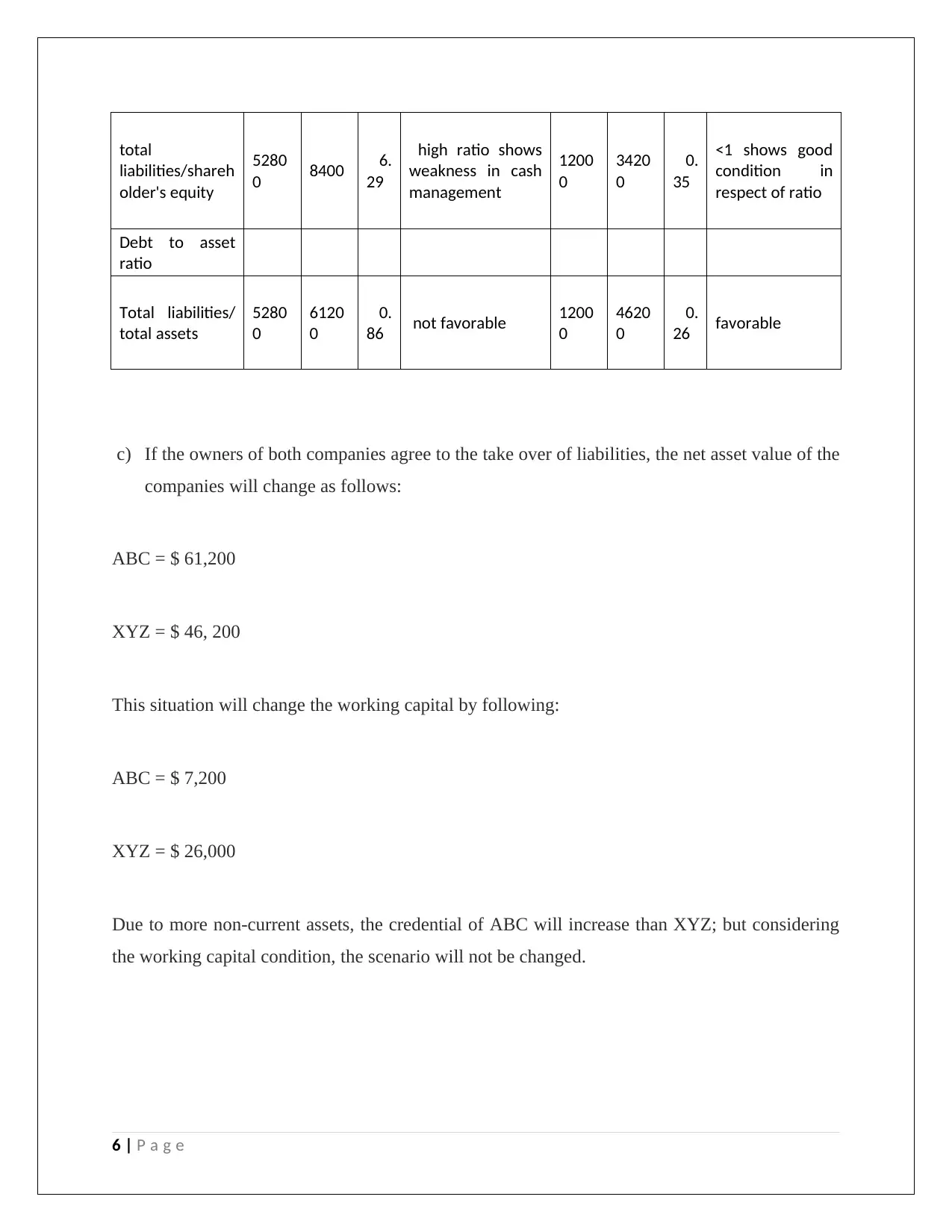

This report provides a detailed analysis of income recognition for an anti-virus software company, applying AASB 15 and other relevant accounting standards to determine which financial items qualify as income. It further evaluates the loan credentials and acquisition factors of two companies, ABC and XYZ, using financial ratios and balance sheet information to assess their financial health and attractiveness for loans or acquisition. The report concludes by examining how changes in liability assumptions would impact acquisition decisions, offering a comprehensive overview of financial analysis in a business context. Desklib offers a wealth of similar solved assignments and past papers to aid students in their studies.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.