A Comprehensive Report on Taxation Fundamentals: Income Tax & NICs

VerifiedAdded on 2023/06/15

|9

|2236

|153

Report

AI Summary

This report provides a detailed explanation of income tax and National Insurance Contributions (NICs), including the assessment of income tax based on various sources such as salary, bonus, and benefits. It covers topics like personal allowance, gift aid, company accommodation, and car/fuel benefits, along with calculations for income tax liability and NICs. The report also analyzes the difference between tax evasion and tax avoidance, examines HMRC policies aimed at reducing tax evasion, and determines whether income is subject to personal income tax or capital gains tax. Furthermore, it calculates disposable income under different scenarios, offering a comparative analysis to determine the most financially advantageous option. This comprehensive overview is valuable for understanding the complexities of taxation and financial planning.

Taxation

Fundamentals

Fundamentals

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Prepare a report providing detailed explanation for the income tax payment and its NICs........3

Section B..........................................................................................................................................6

Part 1................................................................................................................................................6

(a) Calculate the income tax and NIC for both the options.........................................................6

(b) Calculate the disposable income after performing deductions..............................................6

From the two options which option is best..................................................................................7

Part 2................................................................................................................................................7

Analyse the difference between tax evasion and tax avoidance..................................................7

Analyse two different policies introduced by HMRC in last five years with a view to reduce

tax evasion and avoidance...........................................................................................................7

Part 3................................................................................................................................................7

Analyse the way in which HMRC will ascertain that whether Mrs Jill Jonson will be subjected

to personal income tax or capital gains tax..................................................................................7

REFERENCES................................................................................................................................9

Prepare a report providing detailed explanation for the income tax payment and its NICs........3

Section B..........................................................................................................................................6

Part 1................................................................................................................................................6

(a) Calculate the income tax and NIC for both the options.........................................................6

(b) Calculate the disposable income after performing deductions..............................................6

From the two options which option is best..................................................................................7

Part 2................................................................................................................................................7

Analyse the difference between tax evasion and tax avoidance..................................................7

Analyse two different policies introduced by HMRC in last five years with a view to reduce

tax evasion and avoidance...........................................................................................................7

Part 3................................................................................................................................................7

Analyse the way in which HMRC will ascertain that whether Mrs Jill Jonson will be subjected

to personal income tax or capital gains tax..................................................................................7

REFERENCES................................................................................................................................9

Section A

Prepare a report providing detailed explanation for the income tax payment and its NICs.

Assessment of income tax on the basis of income earned from all sources.

Salary and Bonus- Fiona is earning a salary of £ 95081 which is calculated from the date

of birth 10.08.95 and then it is divided by 10. On reversing the data, it comes out to be

958010 and on dividing it by 10 the resulting value is 95081. Also, it received a bonus of

£ 15000 on 12 may 2020 which was entitled on 22 March 2020. this amount will be

taxable in current year.

Contribution- Fiona is contributing 5 % of its gross salary to HMRC registered

occupational pension scheme which is calculated as

95081 * 5% = £ 4754

This amount will be available for tax deduction and would not increase the limit of tax.

Personal Allowance- This benefit is tax free and can be reduced in case the adjusted net

income is more than £ 100000 by the extent of half of the amount. For instance a person

earned an amount of £ 125000, then personal allowance of that being is zero.

Christian, husband of Fiona transfers its Marriage allowance to Fiona as it is unemployed. This

amount usually equal to the 10 % of basic personal allowance. But in case one of the two

spouses is a heavy tax payer then the transfer is not done. Fiona is not entitled to personal

allowance as the amount of marriage allowance cannot to be transferred to it.

Gift aid- Fiona made a charitable donation of £ 2852, which is equal to the 3 % of the

total gross salary . This needs to be adjusted up up grossing up the value.

2852 *100 / 80 = £ 3565

This amount of £ 3565 will be added to higher and basic relief limit for Fiona.

Other income- Fiona received an interest of 4 % on the gross salary which amounts to £

3803. In addition to this, it is also receiving an income of £ 9508 which is equal to 10%

of its gross salary.

Other benefits

Company accommodation- The property used by Fiona was purchased before more than

six years thus the value of providing accommodation will be equal to £ 250000 which

was the value of house on the date it shifter over their. In addition to this, the

improvement cost of £ 31000 is also made but this is before the start of taxation year.

Prepare a report providing detailed explanation for the income tax payment and its NICs.

Assessment of income tax on the basis of income earned from all sources.

Salary and Bonus- Fiona is earning a salary of £ 95081 which is calculated from the date

of birth 10.08.95 and then it is divided by 10. On reversing the data, it comes out to be

958010 and on dividing it by 10 the resulting value is 95081. Also, it received a bonus of

£ 15000 on 12 may 2020 which was entitled on 22 March 2020. this amount will be

taxable in current year.

Contribution- Fiona is contributing 5 % of its gross salary to HMRC registered

occupational pension scheme which is calculated as

95081 * 5% = £ 4754

This amount will be available for tax deduction and would not increase the limit of tax.

Personal Allowance- This benefit is tax free and can be reduced in case the adjusted net

income is more than £ 100000 by the extent of half of the amount. For instance a person

earned an amount of £ 125000, then personal allowance of that being is zero.

Christian, husband of Fiona transfers its Marriage allowance to Fiona as it is unemployed. This

amount usually equal to the 10 % of basic personal allowance. But in case one of the two

spouses is a heavy tax payer then the transfer is not done. Fiona is not entitled to personal

allowance as the amount of marriage allowance cannot to be transferred to it.

Gift aid- Fiona made a charitable donation of £ 2852, which is equal to the 3 % of the

total gross salary . This needs to be adjusted up up grossing up the value.

2852 *100 / 80 = £ 3565

This amount of £ 3565 will be added to higher and basic relief limit for Fiona.

Other income- Fiona received an interest of 4 % on the gross salary which amounts to £

3803. In addition to this, it is also receiving an income of £ 9508 which is equal to 10%

of its gross salary.

Other benefits

Company accommodation- The property used by Fiona was purchased before more than

six years thus the value of providing accommodation will be equal to £ 250000 which

was the value of house on the date it shifter over their. In addition to this, the

improvement cost of £ 31000 is also made but this is before the start of taxation year.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The annual value if accommodation is £ 11600.

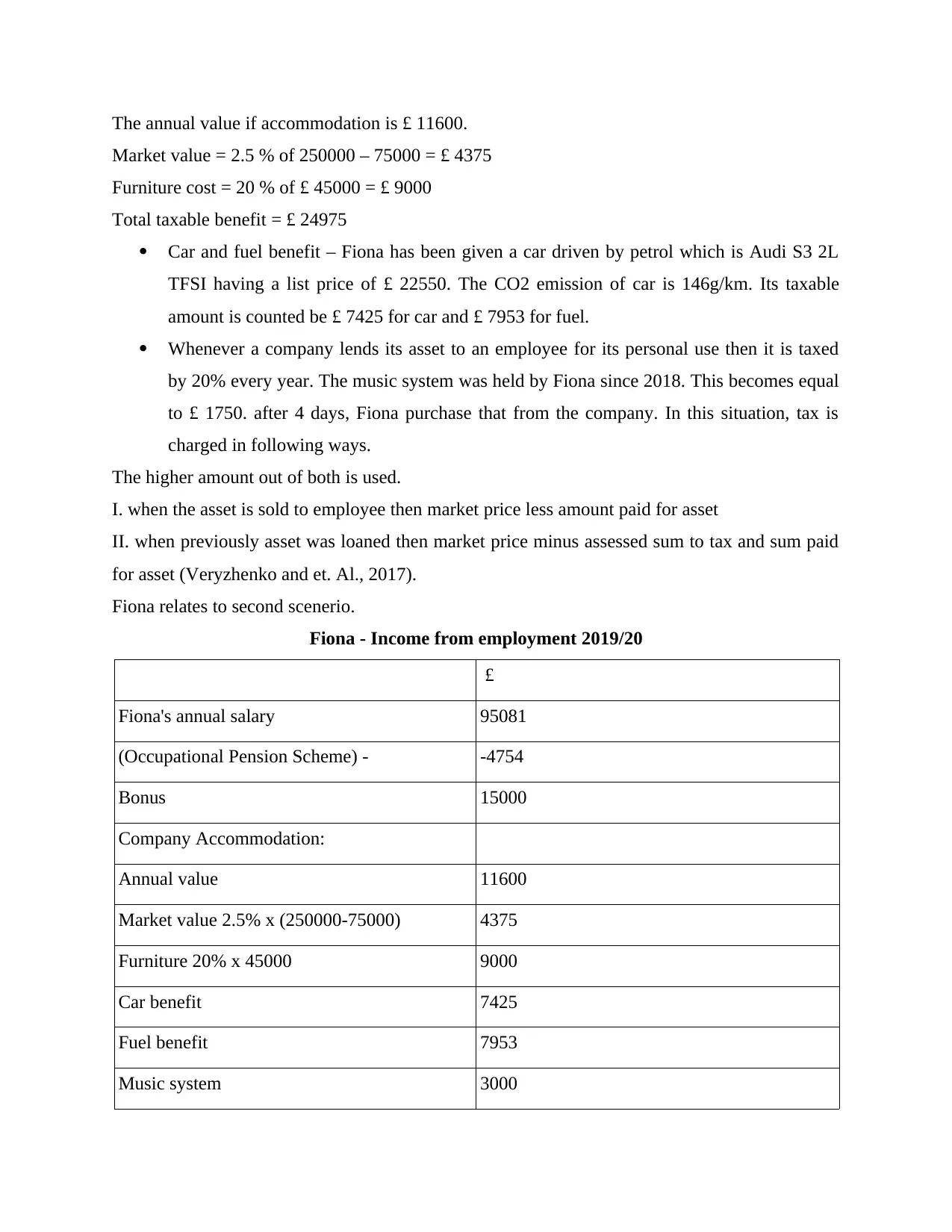

Market value = 2.5 % of 250000 – 75000 = £ 4375

Furniture cost = 20 % of £ 45000 = £ 9000

Total taxable benefit = £ 24975

Car and fuel benefit – Fiona has been given a car driven by petrol which is Audi S3 2L

TFSI having a list price of £ 22550. The CO2 emission of car is 146g/km. Its taxable

amount is counted be £ 7425 for car and £ 7953 for fuel.

Whenever a company lends its asset to an employee for its personal use then it is taxed

by 20% every year. The music system was held by Fiona since 2018. This becomes equal

to £ 1750. after 4 days, Fiona purchase that from the company. In this situation, tax is

charged in following ways.

The higher amount out of both is used.

I. when the asset is sold to employee then market price less amount paid for asset

II. when previously asset was loaned then market price minus assessed sum to tax and sum paid

for asset (Veryzhenko and et. Al., 2017).

Fiona relates to second scenerio.

Fiona - Income from employment 2019/20

£

Fiona's annual salary 95081

(Occupational Pension Scheme) - -4754

Bonus 15000

Company Accommodation:

Annual value 11600

Market value 2.5% x (250000-75000) 4375

Furniture 20% x 45000 9000

Car benefit 7425

Fuel benefit 7953

Music system 3000

Market value = 2.5 % of 250000 – 75000 = £ 4375

Furniture cost = 20 % of £ 45000 = £ 9000

Total taxable benefit = £ 24975

Car and fuel benefit – Fiona has been given a car driven by petrol which is Audi S3 2L

TFSI having a list price of £ 22550. The CO2 emission of car is 146g/km. Its taxable

amount is counted be £ 7425 for car and £ 7953 for fuel.

Whenever a company lends its asset to an employee for its personal use then it is taxed

by 20% every year. The music system was held by Fiona since 2018. This becomes equal

to £ 1750. after 4 days, Fiona purchase that from the company. In this situation, tax is

charged in following ways.

The higher amount out of both is used.

I. when the asset is sold to employee then market price less amount paid for asset

II. when previously asset was loaned then market price minus assessed sum to tax and sum paid

for asset (Veryzhenko and et. Al., 2017).

Fiona relates to second scenerio.

Fiona - Income from employment 2019/20

£

Fiona's annual salary 95081

(Occupational Pension Scheme) - -4754

Bonus 15000

Company Accommodation:

Annual value 11600

Market value 2.5% x (250000-75000) 4375

Furniture 20% x 45000 9000

Car benefit 7425

Fuel benefit 7953

Music system 3000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

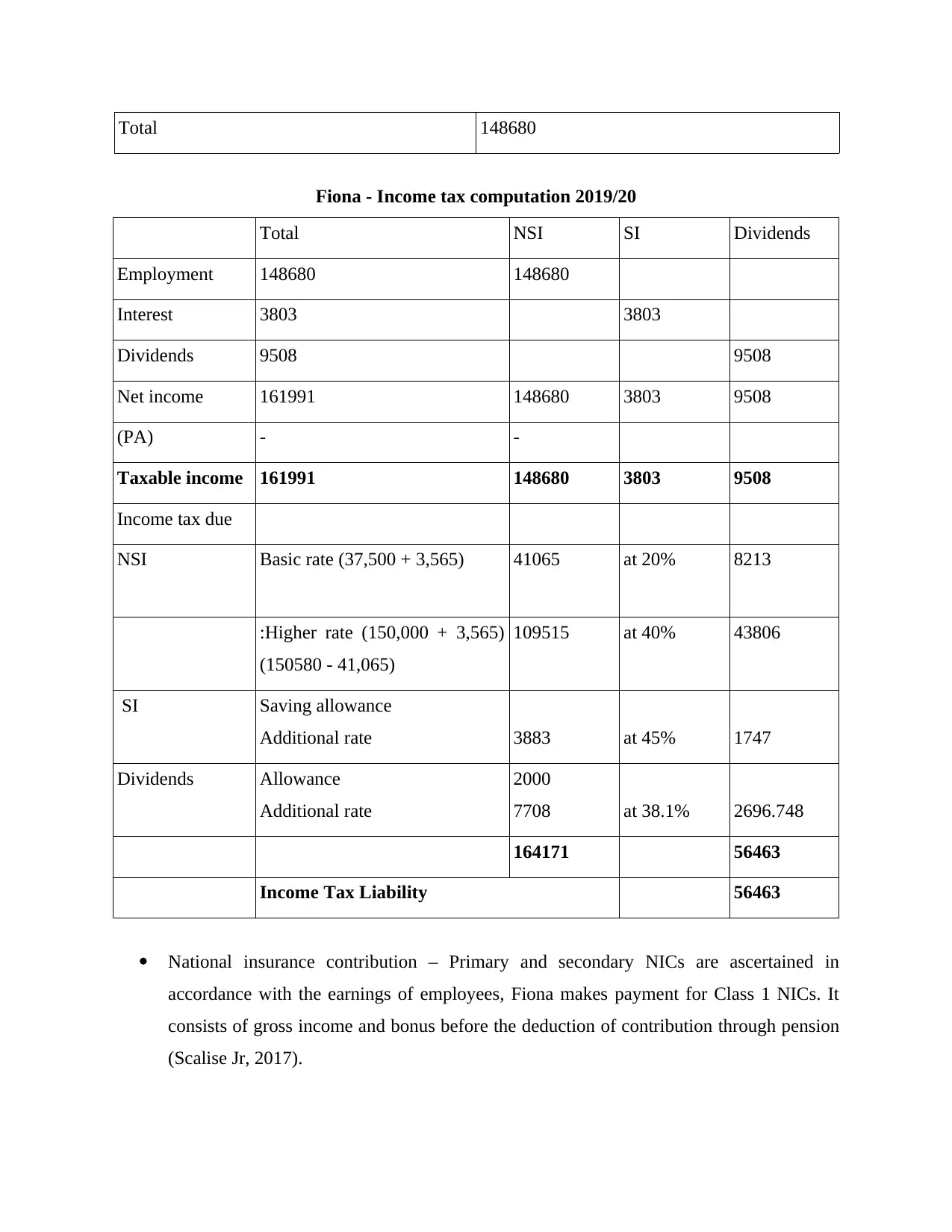

Total 148680

Fiona - Income tax computation 2019/20

Total NSI SI Dividends

Employment 148680 148680

Interest 3803 3803

Dividends 9508 9508

Net income 161991 148680 3803 9508

(PA) - -

Taxable income 161991 148680 3803 9508

Income tax due

NSI Basic rate (37,500 + 3,565) 41065 at 20% 8213

:Higher rate (150,000 + 3,565)

(150580 - 41,065)

109515 at 40% 43806

SI Saving allowance

Additional rate 3883 at 45% 1747

Dividends Allowance

Additional rate

2000

7708 at 38.1% 2696.748

164171 56463

Income Tax Liability 56463

National insurance contribution – Primary and secondary NICs are ascertained in

accordance with the earnings of employees, Fiona makes payment for Class 1 NICs. It

consists of gross income and bonus before the deduction of contribution through pension

(Scalise Jr, 2017).

Fiona - Income tax computation 2019/20

Total NSI SI Dividends

Employment 148680 148680

Interest 3803 3803

Dividends 9508 9508

Net income 161991 148680 3803 9508

(PA) - -

Taxable income 161991 148680 3803 9508

Income tax due

NSI Basic rate (37,500 + 3,565) 41065 at 20% 8213

:Higher rate (150,000 + 3,565)

(150580 - 41,065)

109515 at 40% 43806

SI Saving allowance

Additional rate 3883 at 45% 1747

Dividends Allowance

Additional rate

2000

7708 at 38.1% 2696.748

164171 56463

Income Tax Liability 56463

National insurance contribution – Primary and secondary NICs are ascertained in

accordance with the earnings of employees, Fiona makes payment for Class 1 NICs. It

consists of gross income and bonus before the deduction of contribution through pension

(Scalise Jr, 2017).

Section B

Part 1

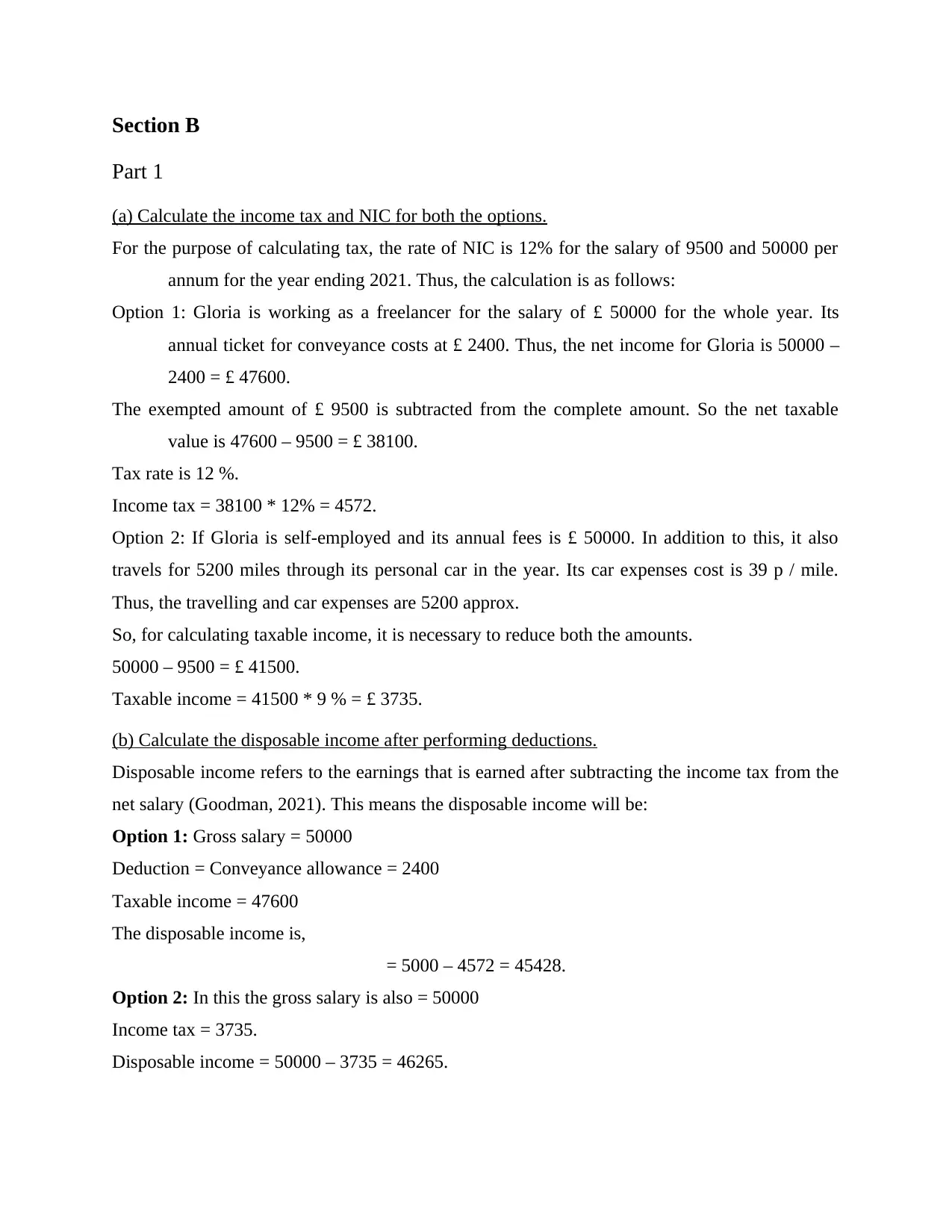

(a) Calculate the income tax and NIC for both the options.

For the purpose of calculating tax, the rate of NIC is 12% for the salary of 9500 and 50000 per

annum for the year ending 2021. Thus, the calculation is as follows:

Option 1: Gloria is working as a freelancer for the salary of £ 50000 for the whole year. Its

annual ticket for conveyance costs at £ 2400. Thus, the net income for Gloria is 50000 –

2400 = £ 47600.

The exempted amount of £ 9500 is subtracted from the complete amount. So the net taxable

value is 47600 – 9500 = £ 38100.

Tax rate is 12 %.

Income tax = 38100 * 12% = 4572.

Option 2: If Gloria is self-employed and its annual fees is £ 50000. In addition to this, it also

travels for 5200 miles through its personal car in the year. Its car expenses cost is 39 p / mile.

Thus, the travelling and car expenses are 5200 approx.

So, for calculating taxable income, it is necessary to reduce both the amounts.

50000 – 9500 = £ 41500.

Taxable income = 41500 * 9 % = £ 3735.

(b) Calculate the disposable income after performing deductions.

Disposable income refers to the earnings that is earned after subtracting the income tax from the

net salary (Goodman, 2021). This means the disposable income will be:

Option 1: Gross salary = 50000

Deduction = Conveyance allowance = 2400

Taxable income = 47600

The disposable income is,

= 5000 – 4572 = 45428.

Option 2: In this the gross salary is also = 50000

Income tax = 3735.

Disposable income = 50000 – 3735 = 46265.

Part 1

(a) Calculate the income tax and NIC for both the options.

For the purpose of calculating tax, the rate of NIC is 12% for the salary of 9500 and 50000 per

annum for the year ending 2021. Thus, the calculation is as follows:

Option 1: Gloria is working as a freelancer for the salary of £ 50000 for the whole year. Its

annual ticket for conveyance costs at £ 2400. Thus, the net income for Gloria is 50000 –

2400 = £ 47600.

The exempted amount of £ 9500 is subtracted from the complete amount. So the net taxable

value is 47600 – 9500 = £ 38100.

Tax rate is 12 %.

Income tax = 38100 * 12% = 4572.

Option 2: If Gloria is self-employed and its annual fees is £ 50000. In addition to this, it also

travels for 5200 miles through its personal car in the year. Its car expenses cost is 39 p / mile.

Thus, the travelling and car expenses are 5200 approx.

So, for calculating taxable income, it is necessary to reduce both the amounts.

50000 – 9500 = £ 41500.

Taxable income = 41500 * 9 % = £ 3735.

(b) Calculate the disposable income after performing deductions.

Disposable income refers to the earnings that is earned after subtracting the income tax from the

net salary (Goodman, 2021). This means the disposable income will be:

Option 1: Gross salary = 50000

Deduction = Conveyance allowance = 2400

Taxable income = 47600

The disposable income is,

= 5000 – 4572 = 45428.

Option 2: In this the gross salary is also = 50000

Income tax = 3735.

Disposable income = 50000 – 3735 = 46265.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

From the two options which option is best

It is clear from above discussion that option 2 is good as the tax payment in this option is

less as compared to Option1.

Part 2

Analyse the difference between tax evasion and tax avoidance.

Tax evasion simply refers to the situation when persons try to hide their tax from the

authorities which is illegal (Ironside, 2017). It is a means of lying to income tax authorities in

any form. It can lead to punishment, penalties, fines or even to imprisonment. This also increases

the risk of regular audits to the firm. On the other had tax avoidance means the situation when a

person tries to reduce the amount of payment of tax in legal manner. It is a structured manner in

which the tax payer attempts to minimise the amount of tax obligation according to the rules

provided for that. If used is legal and appropriate manner, it can help the person in claiming tax

deductions.

Analyse two different policies introduced by HMRC in last five years with a view to reduce tax

evasion and avoidance.

Tax avoidance can be defined as a usage of rules and regulations of taxation system for getting

the benefit of tax. This is made through human transactions and is performed in a view to earn

benefits. Most of the tax avoidance policies do not perform as per their need and many times

make the people to pay more than the tax they try to avoid (Ouazad, 2021). Tax evasion is when

the individuals deliberately does not record for the transaction for which the amount is owed by

them.

Part 3

Analyse the way in which HMRC will ascertain that whether Mrs Jill Jonson will be subjected to

personal income tax or capital gains tax.

For ascertaining that the properly being sold, is a capital gain or a personal income tax,

HMRC would have to look at the daily transactions of the business. Whenever a stock or

building is purchased for business purpose as a stock, then the person always tries to sell its

product at some profit. While on the other hand, the sales of capital asset is not necessary to be

sold on credit. The buildings have been sold by Jill on no profit basis, which shows that it was

It is clear from above discussion that option 2 is good as the tax payment in this option is

less as compared to Option1.

Part 2

Analyse the difference between tax evasion and tax avoidance.

Tax evasion simply refers to the situation when persons try to hide their tax from the

authorities which is illegal (Ironside, 2017). It is a means of lying to income tax authorities in

any form. It can lead to punishment, penalties, fines or even to imprisonment. This also increases

the risk of regular audits to the firm. On the other had tax avoidance means the situation when a

person tries to reduce the amount of payment of tax in legal manner. It is a structured manner in

which the tax payer attempts to minimise the amount of tax obligation according to the rules

provided for that. If used is legal and appropriate manner, it can help the person in claiming tax

deductions.

Analyse two different policies introduced by HMRC in last five years with a view to reduce tax

evasion and avoidance.

Tax avoidance can be defined as a usage of rules and regulations of taxation system for getting

the benefit of tax. This is made through human transactions and is performed in a view to earn

benefits. Most of the tax avoidance policies do not perform as per their need and many times

make the people to pay more than the tax they try to avoid (Ouazad, 2021). Tax evasion is when

the individuals deliberately does not record for the transaction for which the amount is owed by

them.

Part 3

Analyse the way in which HMRC will ascertain that whether Mrs Jill Jonson will be subjected to

personal income tax or capital gains tax.

For ascertaining that the properly being sold, is a capital gain or a personal income tax,

HMRC would have to look at the daily transactions of the business. Whenever a stock or

building is purchased for business purpose as a stock, then the person always tries to sell its

product at some profit. While on the other hand, the sales of capital asset is not necessary to be

sold on credit. The buildings have been sold by Jill on no profit basis, which shows that it was

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

not a profit earning sale. This shows that the earnings on sale of houses will be taken as capital

gain and will be taxed under this system only.

Also, whenever a residential property is sold, the taxable capital gain is required to be paid

within the time period of 30 days and is required to be send to HMRC. All the other capital

losses experienced in this year can be adjusted against this capital income (Özen and Ersoy,

2019). But if there is any capital loss that has arisen after the sale of this residential property is

ignored and not allowed to be adjusted against the capital gain. At the end of taxation year, the

property gain on the sale of asset is included in the self-assessment capital gain for the

computation of the taxable income. Payment for the capital tax gains is different in regular tax

assessment with regards to 31 January of the tax year and 31 July of the coming year. But it does

not examine the calculation of payments in a situation when more than single residential property

is sold in a whole tax year. Thus, it can be said that Jill Johnson is required to be paid according

to capital tax gain (Rupitsch, 2018).

gain and will be taxed under this system only.

Also, whenever a residential property is sold, the taxable capital gain is required to be paid

within the time period of 30 days and is required to be send to HMRC. All the other capital

losses experienced in this year can be adjusted against this capital income (Özen and Ersoy,

2019). But if there is any capital loss that has arisen after the sale of this residential property is

ignored and not allowed to be adjusted against the capital gain. At the end of taxation year, the

property gain on the sale of asset is included in the self-assessment capital gain for the

computation of the taxable income. Payment for the capital tax gains is different in regular tax

assessment with regards to 31 January of the tax year and 31 July of the coming year. But it does

not examine the calculation of payments in a situation when more than single residential property

is sold in a whole tax year. Thus, it can be said that Jill Johnson is required to be paid according

to capital tax gain (Rupitsch, 2018).

REFERENCES

Books and Journals

Goodman, D., 2021. loosened these linear structures somewhat in the past twenty years but the

fundamentals remain un flanged. ese established input-output relations and

locational specificities of the food system are now threatened by modern biote

nologies. Inputs for the food industry potentially can be derived from a mu wider

range of materials: food and non-food crops and even non. Towards A New Political

Economy Of Agriculture.

Ironside, K., 2017. Between Fiscal, Ideological, and Social Dilemmas: The Soviet ‘Bachelor

Tax’and Post-war Tax Reform, 1941–1962. Europe-Asia Studies. 69(6). pp.855-878.

Ouazad, A., 2021. Resilient Urban Housing Markets: Shocks Versus Fundamentals. In COVID-

19: Systemic Risk and Resilience (pp. 299-331). Springer, Cham.

Özen, E. and Ersoy, G., 2019. The impact of financial literacy on cognitive biases of individual

investors. In Contemporary Issues in Behavioral Finance. Emerald Publishing Limited.

Rupitsch, S.J., 2018. Piezoelectric sensors and actuators: Fundamentals and applications.

Springer.

Scalise Jr, R.J., 2017. Some Fundamentals of Trusts: Ownership or Equity in Louisiana. Tul. L.

Rev.. 92. p.53.

Veryzhenko, I. and et. Al., 2017. Time to slow down for high‐frequency trading? Lessons from

artificial markets. Intelligent Systems in Accounting, Finance and Management. 24(2-3).

pp.73-79.

Books and Journals

Goodman, D., 2021. loosened these linear structures somewhat in the past twenty years but the

fundamentals remain un flanged. ese established input-output relations and

locational specificities of the food system are now threatened by modern biote

nologies. Inputs for the food industry potentially can be derived from a mu wider

range of materials: food and non-food crops and even non. Towards A New Political

Economy Of Agriculture.

Ironside, K., 2017. Between Fiscal, Ideological, and Social Dilemmas: The Soviet ‘Bachelor

Tax’and Post-war Tax Reform, 1941–1962. Europe-Asia Studies. 69(6). pp.855-878.

Ouazad, A., 2021. Resilient Urban Housing Markets: Shocks Versus Fundamentals. In COVID-

19: Systemic Risk and Resilience (pp. 299-331). Springer, Cham.

Özen, E. and Ersoy, G., 2019. The impact of financial literacy on cognitive biases of individual

investors. In Contemporary Issues in Behavioral Finance. Emerald Publishing Limited.

Rupitsch, S.J., 2018. Piezoelectric sensors and actuators: Fundamentals and applications.

Springer.

Scalise Jr, R.J., 2017. Some Fundamentals of Trusts: Ownership or Equity in Louisiana. Tul. L.

Rev.. 92. p.53.

Veryzhenko, I. and et. Al., 2017. Time to slow down for high‐frequency trading? Lessons from

artificial markets. Intelligent Systems in Accounting, Finance and Management. 24(2-3).

pp.73-79.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.