Analysis of Income Tax, Corporate Tax, and VAT - Tax Law-II

VerifiedAdded on 2023/04/22

|4

|1147

|379

Homework Assignment

AI Summary

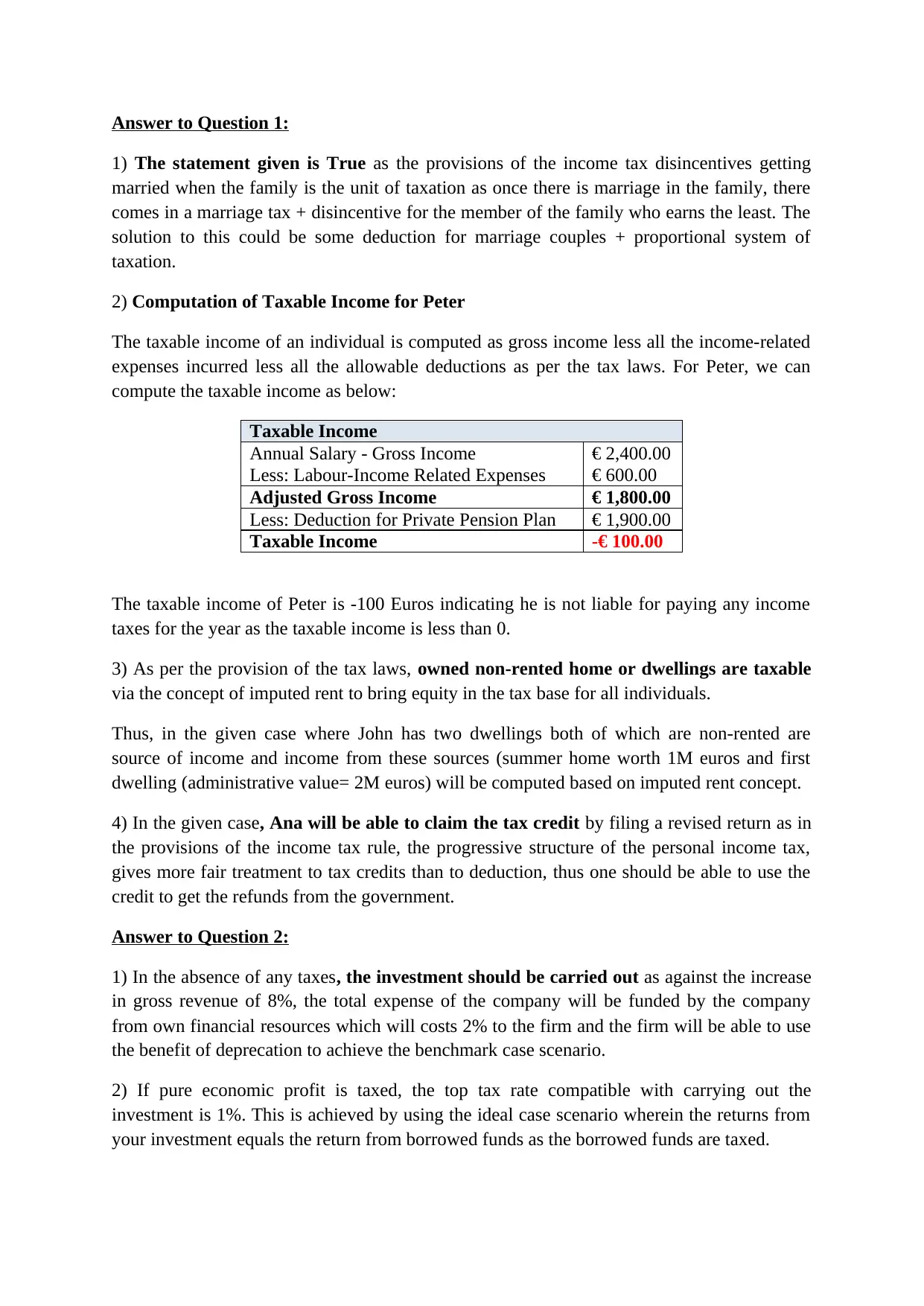

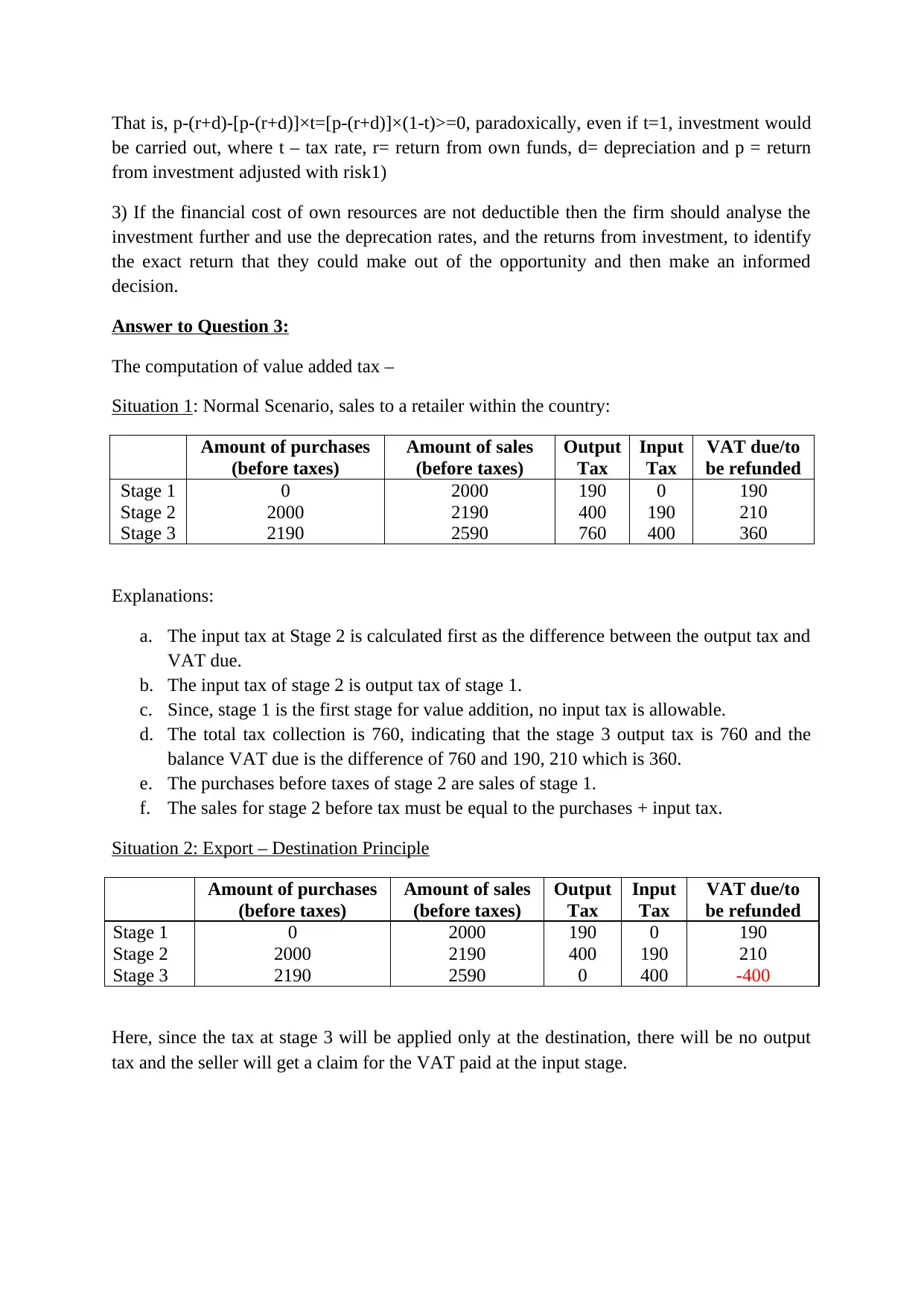

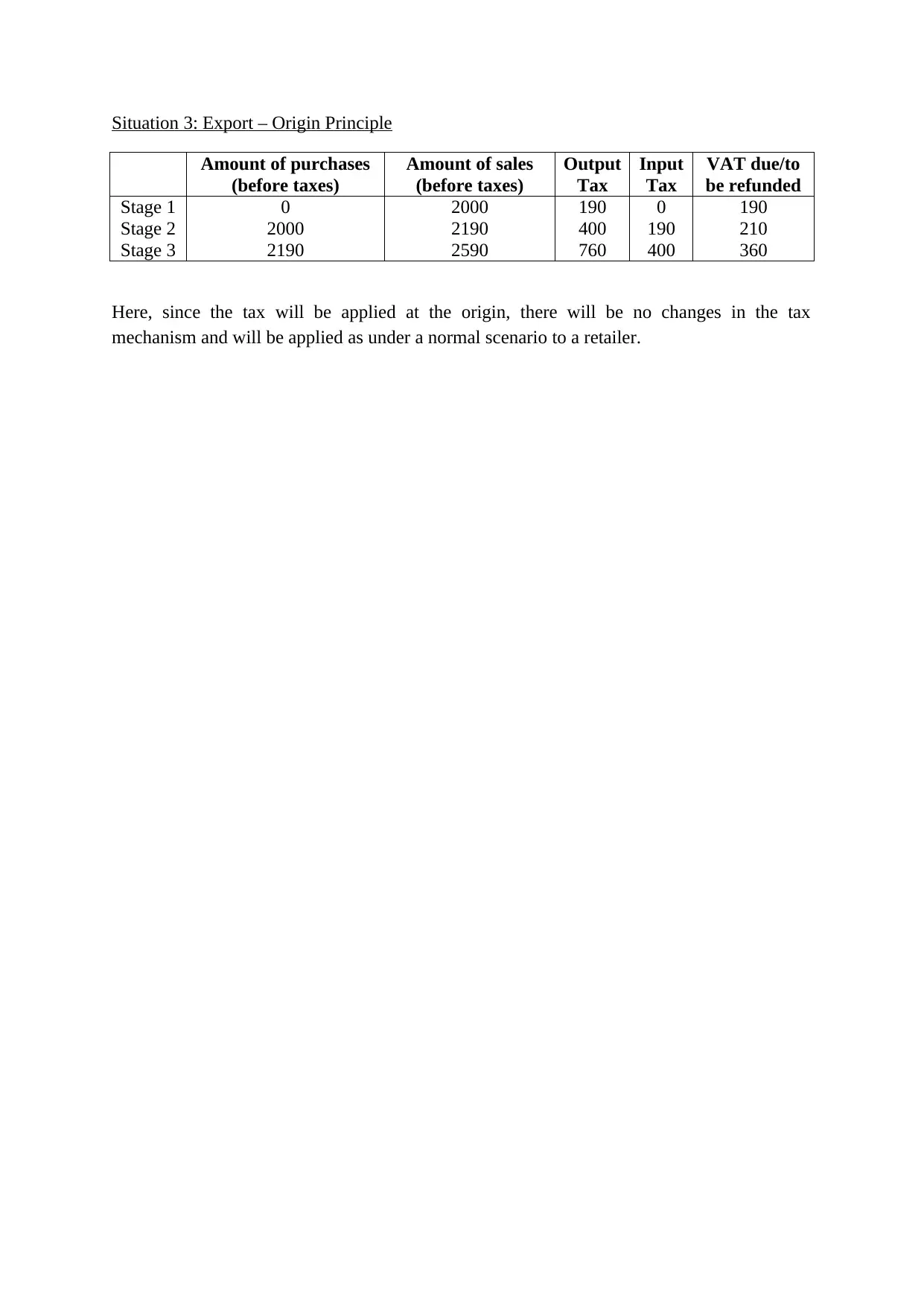

This assignment provides solutions to questions related to personal income tax, corporate income tax, and value-added tax (VAT). It addresses the disincentives of marriage under a proportional income tax system, calculates taxable income for an individual considering deductions and expenses, discusses the taxability of owned non-rented homes through imputed rent, and explains how tax credits can lead to refunds. Furthermore, it analyzes corporate investment decisions in the presence of taxes, including scenarios where economic profit is taxed and where the financial cost of own resources is not deductible. The assignment also includes a detailed computation of VAT under different situations, such as normal sales, exports under the destination principle, and exports under the origin principle. Finally, it summarizes an article discussing why only a small percentage of the Chinese population pays income tax, highlighting potential reforms and issues with government transparency.

1 out of 4

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.