Taxation Assignment: Income Tax Liability Calculation and Analysis

VerifiedAdded on 2020/03/23

|11

|2024

|46

Homework Assignment

AI Summary

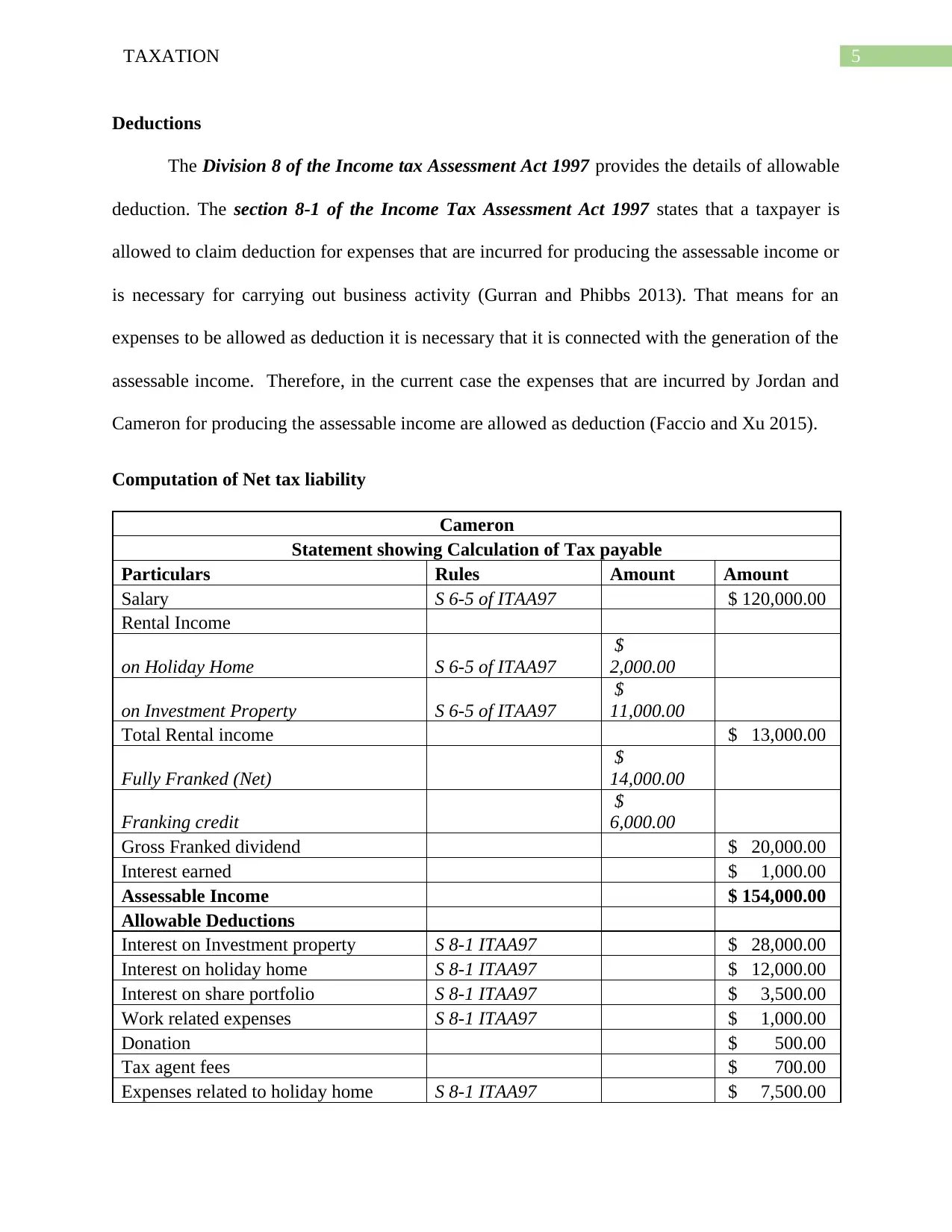

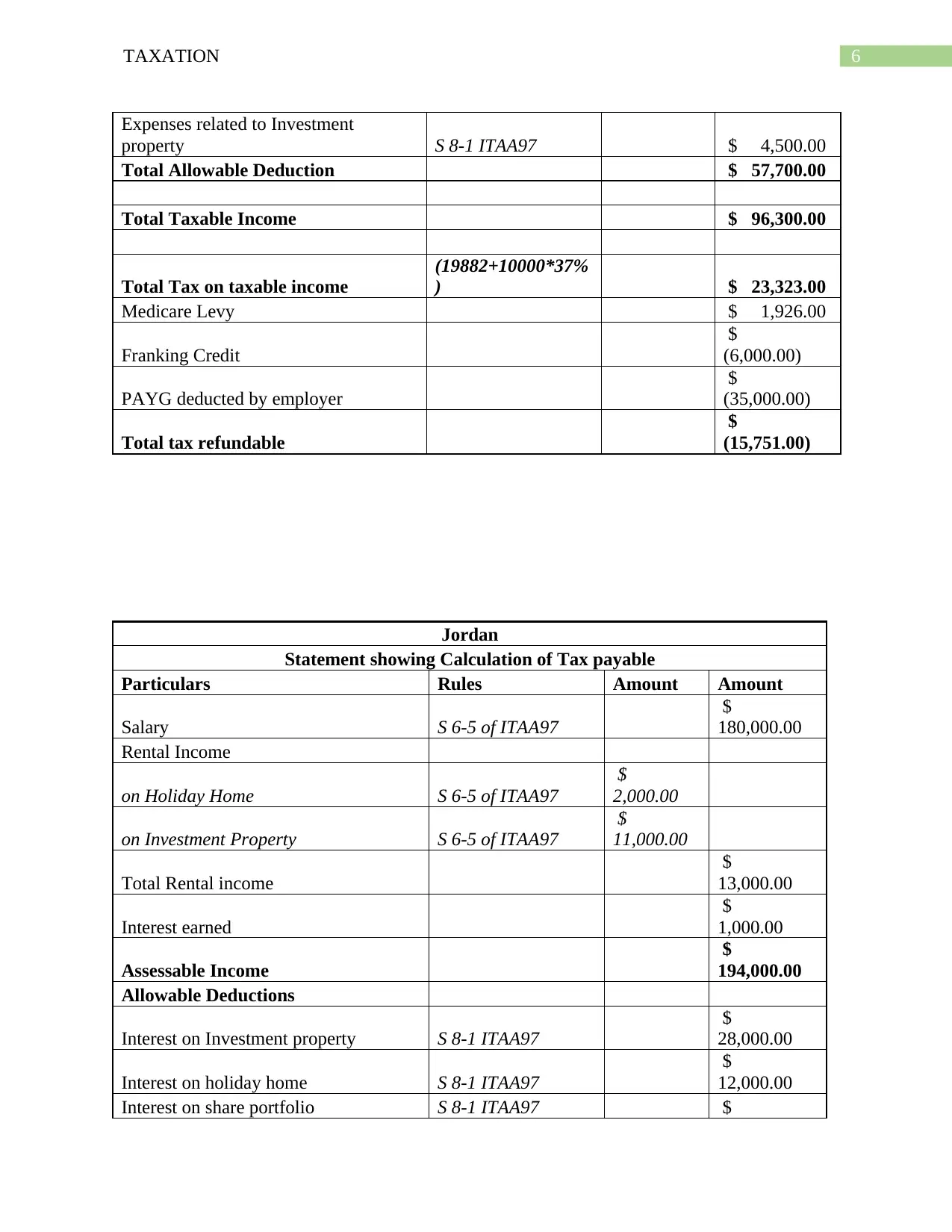

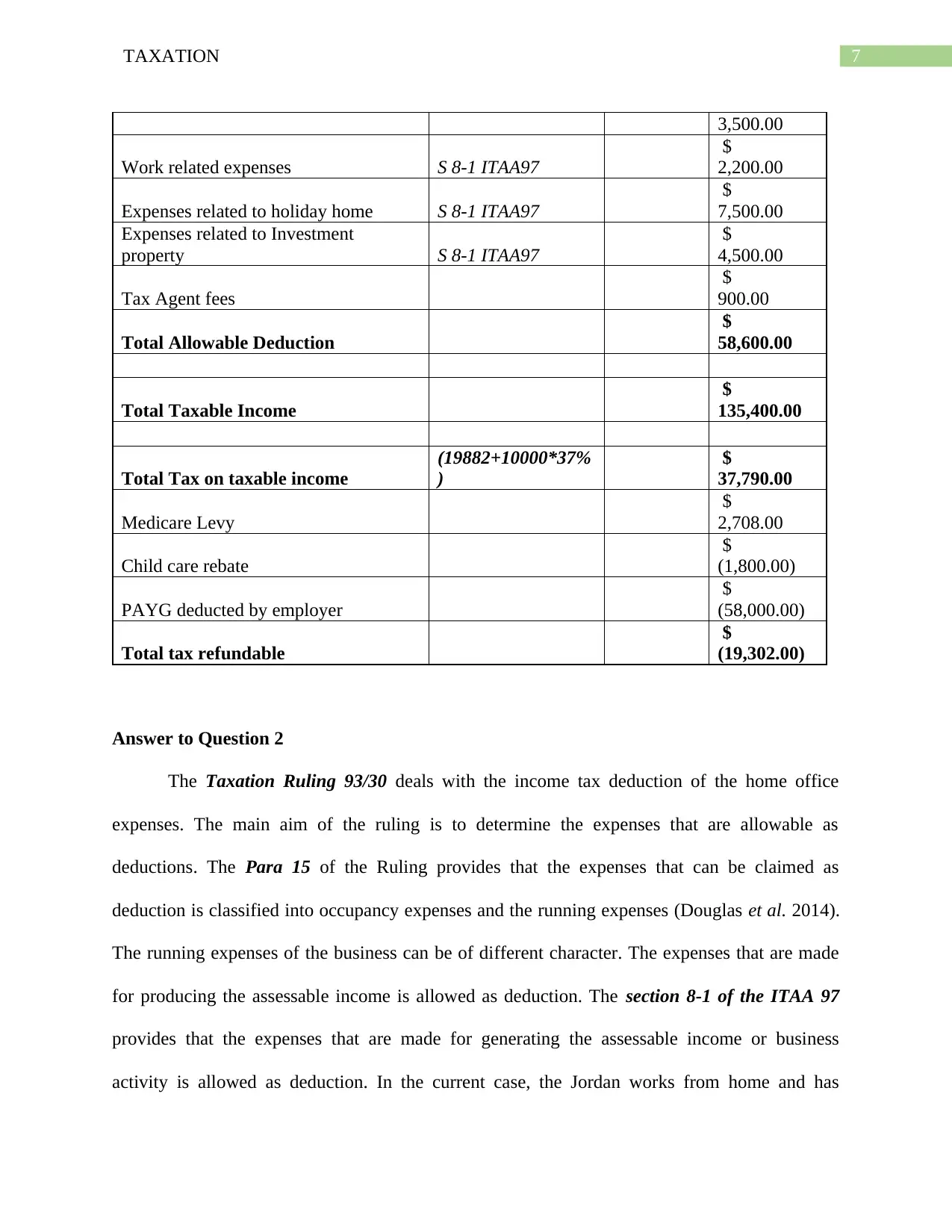

This assignment focuses on calculating the income tax liability of two individuals, Jordan and Cameron, detailing the process of determining assessable income, allowable deductions, and the final net tax payable. It begins with a case introduction outlining the scenario, followed by a review of relevant laws and regulations governing income tax assessment, including the Income Tax Assessment Acts of 1936 and 1997. The analysis section meticulously examines assessable income, specifying which income sources (salary, rental income, interest, dividends) are included and excluded, and why, according to the tax laws. It then delves into allowable deductions, referencing the relevant sections of the ITAA97. The assignment provides detailed calculations for both Jordan and Cameron, demonstrating how to compute their respective tax liabilities, incorporating various income sources, deductions, and tax offsets. Finally, the assignment addresses the deductibility of home office expenses, referencing Taxation Ruling 93/30 and providing advice on allowable deductions for Jordan, who works from home and employs her daughter. The assignment demonstrates a thorough understanding of income tax principles and their practical application.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.