Taxation Fundamentals Coursework: Income Tax, NIC, and Tax Planning

VerifiedAdded on 2023/06/17

|10

|2151

|78

Report

AI Summary

This report provides a detailed analysis of taxation fundamentals, focusing on the calculation of income tax payable and National Insurance Contributions (NIC). It includes a breakdown of Fiona's income tax and NIC, considering various income sources, deductions, and allowances. The report also evaluates the impact of taxes and tax planning, particularly concerning the Financial Act 2020, using Gloria's financial scenarios. Further, it differentiates between tax evasion and tax avoidance, highlighting recent policies introduced by HMRC to combat these issues. The report also discusses capital gains tax in the context of Mrs. Jill Johnson's property transactions, distinguishing it from income tax. The conclusion emphasizes taxation as a crucial government revenue source, highlighting the importance of adhering to tax regulations and guidelines.

Taxation Fundamental

Coursework

Coursework

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

SECTION A.....................................................................................................................................3

Detailed explanation relating to Fiona’s income tax payable and NIC......................................3

SECTION B.....................................................................................................................................5

PART 1 – Impact of taxes and tax planning - Financial Act 2020.............................................5

PART 2 – Income Tax Administration.......................................................................................6

PART 3 – Income Tax Administration.......................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

APPENDIX....................................................................................................................................10

INTRODUCTION...........................................................................................................................3

SECTION A.....................................................................................................................................3

Detailed explanation relating to Fiona’s income tax payable and NIC......................................3

SECTION B.....................................................................................................................................5

PART 1 – Impact of taxes and tax planning - Financial Act 2020.............................................5

PART 2 – Income Tax Administration.......................................................................................6

PART 3 – Income Tax Administration.......................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

APPENDIX....................................................................................................................................10

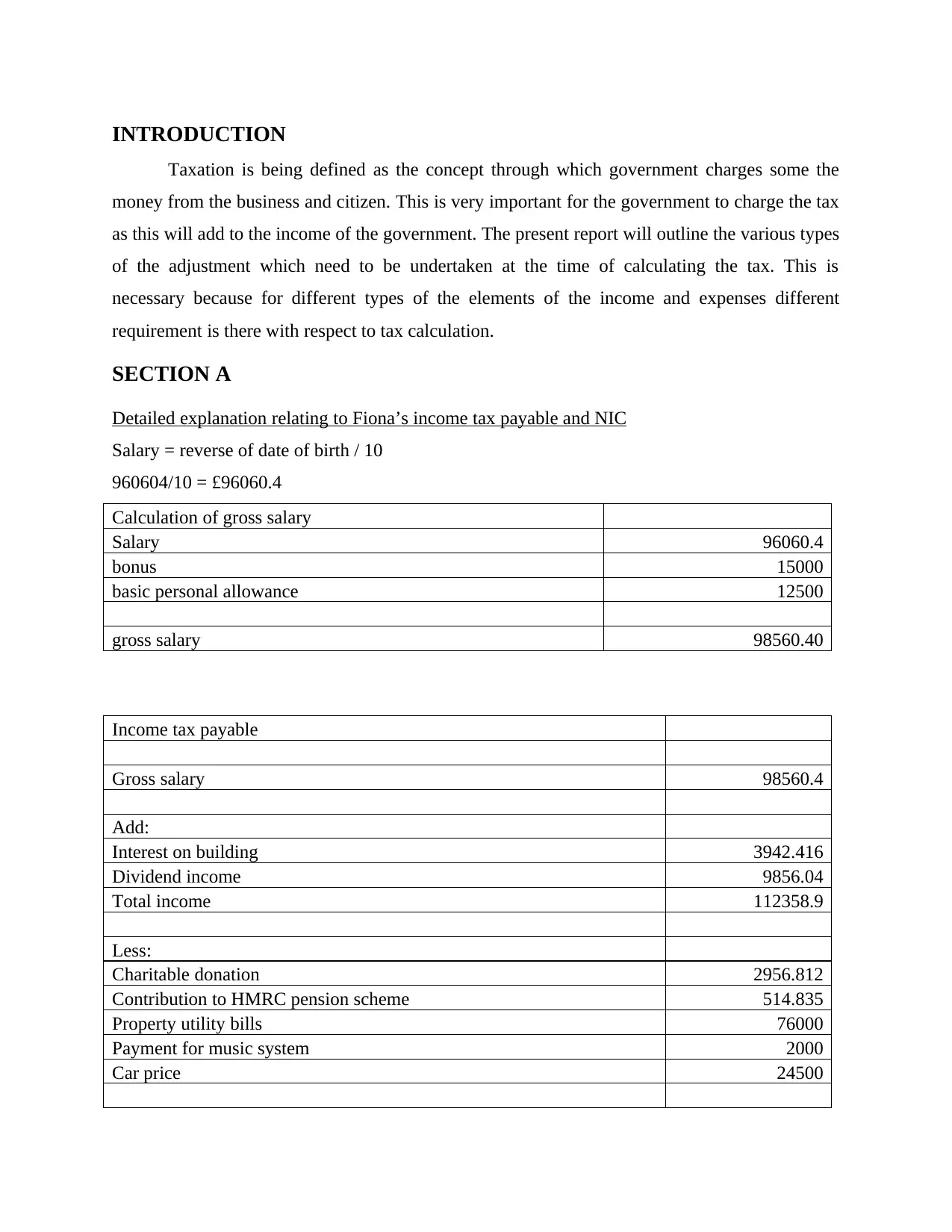

INTRODUCTION

Taxation is being defined as the concept through which government charges some the

money from the business and citizen. This is very important for the government to charge the tax

as this will add to the income of the government. The present report will outline the various types

of the adjustment which need to be undertaken at the time of calculating the tax. This is

necessary because for different types of the elements of the income and expenses different

requirement is there with respect to tax calculation.

SECTION A

Detailed explanation relating to Fiona’s income tax payable and NIC

Salary = reverse of date of birth / 10

960604/10 = £96060.4

Calculation of gross salary

Salary 96060.4

bonus 15000

basic personal allowance 12500

gross salary 98560.40

Income tax payable

Gross salary 98560.4

Add:

Interest on building 3942.416

Dividend income 9856.04

Total income 112358.9

Less:

Charitable donation 2956.812

Contribution to HMRC pension scheme 514.835

Property utility bills 76000

Payment for music system 2000

Car price 24500

Taxation is being defined as the concept through which government charges some the

money from the business and citizen. This is very important for the government to charge the tax

as this will add to the income of the government. The present report will outline the various types

of the adjustment which need to be undertaken at the time of calculating the tax. This is

necessary because for different types of the elements of the income and expenses different

requirement is there with respect to tax calculation.

SECTION A

Detailed explanation relating to Fiona’s income tax payable and NIC

Salary = reverse of date of birth / 10

960604/10 = £96060.4

Calculation of gross salary

Salary 96060.4

bonus 15000

basic personal allowance 12500

gross salary 98560.40

Income tax payable

Gross salary 98560.4

Add:

Interest on building 3942.416

Dividend income 9856.04

Total income 112358.9

Less:

Charitable donation 2956.812

Contribution to HMRC pension scheme 514.835

Property utility bills 76000

Payment for music system 2000

Car price 24500

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

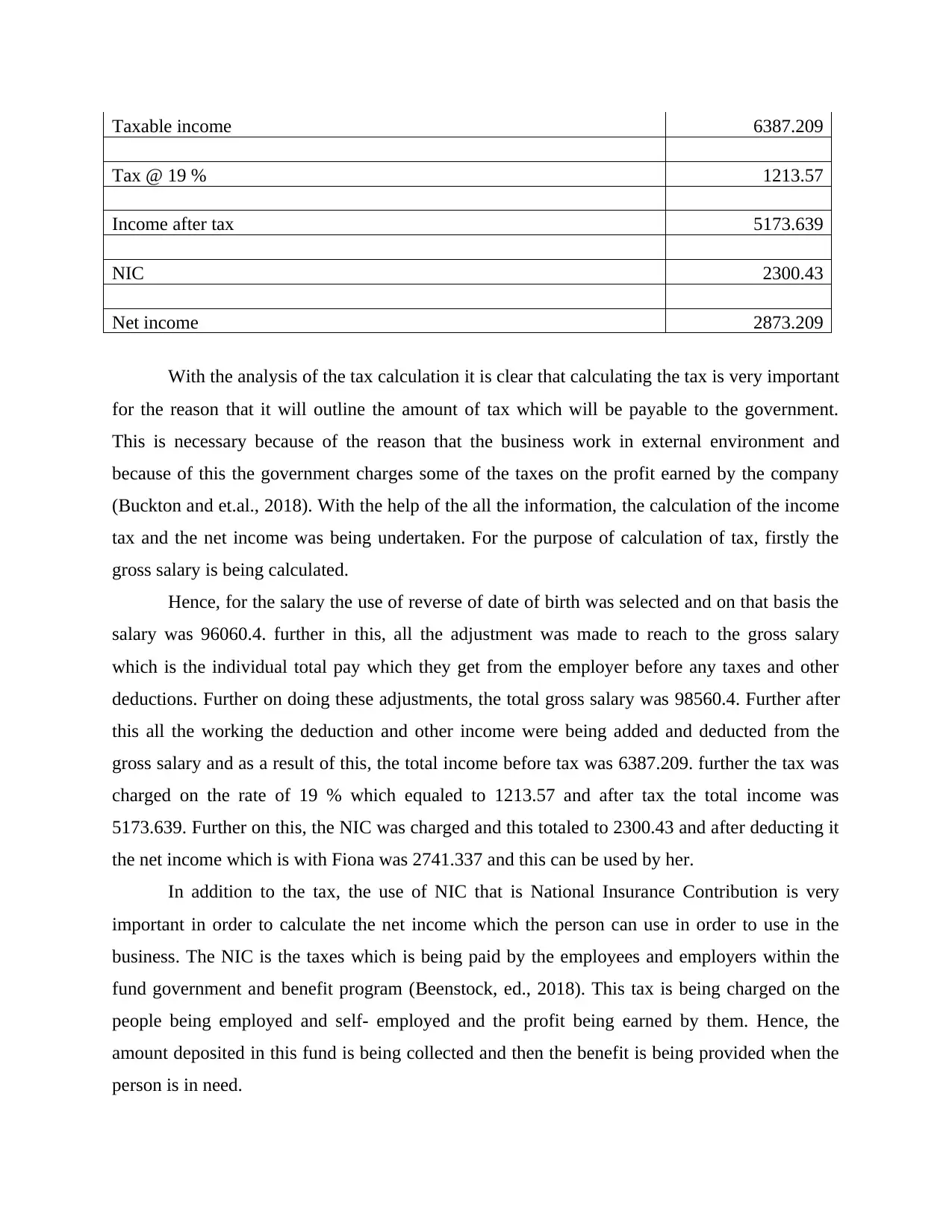

Taxable income 6387.209

Tax @ 19 % 1213.57

Income after tax 5173.639

NIC 2300.43

Net income 2873.209

With the analysis of the tax calculation it is clear that calculating the tax is very important

for the reason that it will outline the amount of tax which will be payable to the government.

This is necessary because of the reason that the business work in external environment and

because of this the government charges some of the taxes on the profit earned by the company

(Buckton and et.al., 2018). With the help of the all the information, the calculation of the income

tax and the net income was being undertaken. For the purpose of calculation of tax, firstly the

gross salary is being calculated.

Hence, for the salary the use of reverse of date of birth was selected and on that basis the

salary was 96060.4. further in this, all the adjustment was made to reach to the gross salary

which is the individual total pay which they get from the employer before any taxes and other

deductions. Further on doing these adjustments, the total gross salary was 98560.4. Further after

this all the working the deduction and other income were being added and deducted from the

gross salary and as a result of this, the total income before tax was 6387.209. further the tax was

charged on the rate of 19 % which equaled to 1213.57 and after tax the total income was

5173.639. Further on this, the NIC was charged and this totaled to 2300.43 and after deducting it

the net income which is with Fiona was 2741.337 and this can be used by her.

In addition to the tax, the use of NIC that is National Insurance Contribution is very

important in order to calculate the net income which the person can use in order to use in the

business. The NIC is the taxes which is being paid by the employees and employers within the

fund government and benefit program (Beenstock, ed., 2018). This tax is being charged on the

people being employed and self- employed and the profit being earned by them. Hence, the

amount deposited in this fund is being collected and then the benefit is being provided when the

person is in need.

Tax @ 19 % 1213.57

Income after tax 5173.639

NIC 2300.43

Net income 2873.209

With the analysis of the tax calculation it is clear that calculating the tax is very important

for the reason that it will outline the amount of tax which will be payable to the government.

This is necessary because of the reason that the business work in external environment and

because of this the government charges some of the taxes on the profit earned by the company

(Buckton and et.al., 2018). With the help of the all the information, the calculation of the income

tax and the net income was being undertaken. For the purpose of calculation of tax, firstly the

gross salary is being calculated.

Hence, for the salary the use of reverse of date of birth was selected and on that basis the

salary was 96060.4. further in this, all the adjustment was made to reach to the gross salary

which is the individual total pay which they get from the employer before any taxes and other

deductions. Further on doing these adjustments, the total gross salary was 98560.4. Further after

this all the working the deduction and other income were being added and deducted from the

gross salary and as a result of this, the total income before tax was 6387.209. further the tax was

charged on the rate of 19 % which equaled to 1213.57 and after tax the total income was

5173.639. Further on this, the NIC was charged and this totaled to 2300.43 and after deducting it

the net income which is with Fiona was 2741.337 and this can be used by her.

In addition to the tax, the use of NIC that is National Insurance Contribution is very

important in order to calculate the net income which the person can use in order to use in the

business. The NIC is the taxes which is being paid by the employees and employers within the

fund government and benefit program (Beenstock, ed., 2018). This tax is being charged on the

people being employed and self- employed and the profit being earned by them. Hence, the

amount deposited in this fund is being collected and then the benefit is being provided when the

person is in need.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

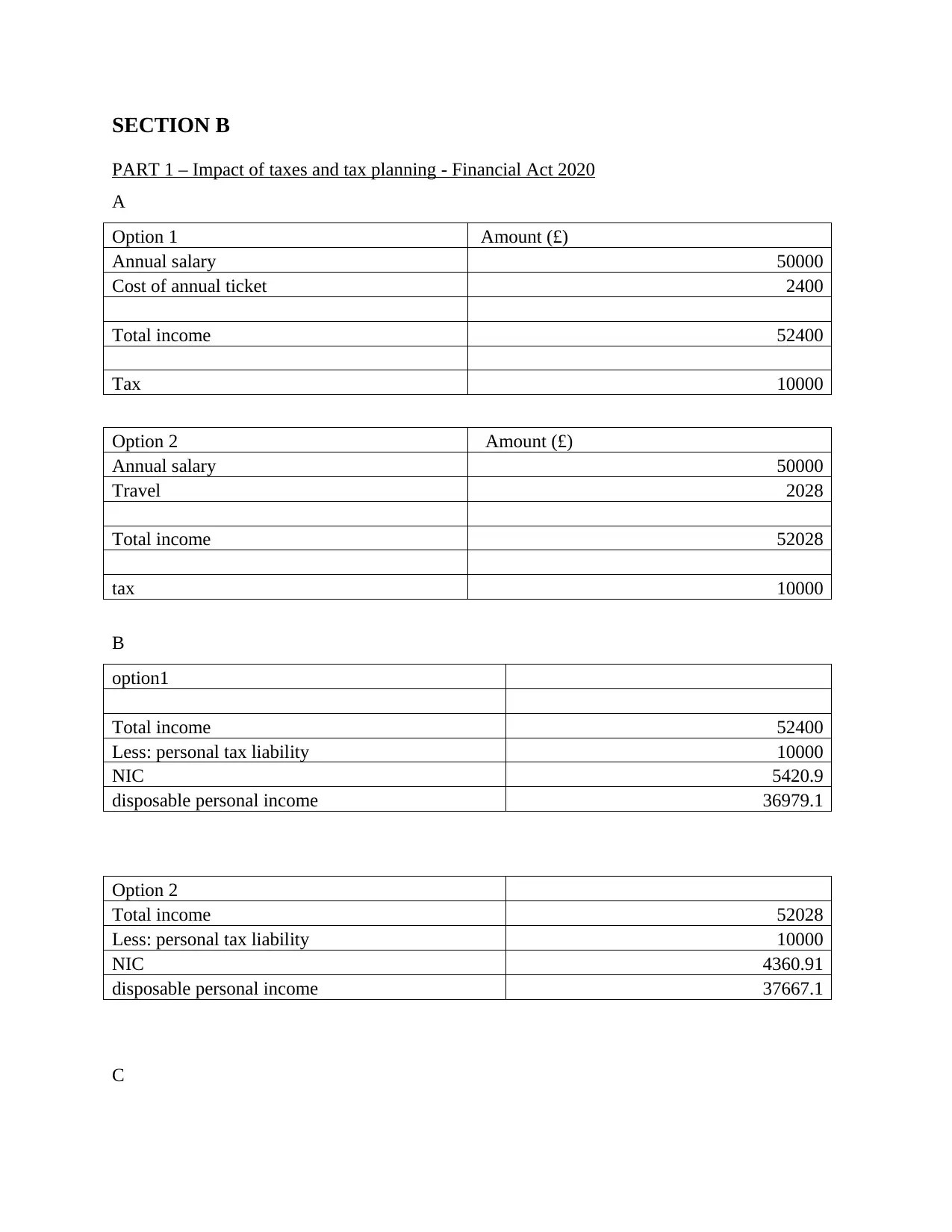

SECTION B

PART 1 – Impact of taxes and tax planning - Financial Act 2020

A

Option 1 Amount (£)

Annual salary 50000

Cost of annual ticket 2400

Total income 52400

Tax 10000

Option 2 Amount (£)

Annual salary 50000

Travel 2028

Total income 52028

tax 10000

B

option1

Total income 52400

Less: personal tax liability 10000

NIC 5420.9

disposable personal income 36979.1

Option 2

Total income 52028

Less: personal tax liability 10000

NIC 4360.91

disposable personal income 37667.1

C

PART 1 – Impact of taxes and tax planning - Financial Act 2020

A

Option 1 Amount (£)

Annual salary 50000

Cost of annual ticket 2400

Total income 52400

Tax 10000

Option 2 Amount (£)

Annual salary 50000

Travel 2028

Total income 52028

tax 10000

B

option1

Total income 52400

Less: personal tax liability 10000

NIC 5420.9

disposable personal income 36979.1

Option 2

Total income 52028

Less: personal tax liability 10000

NIC 4360.91

disposable personal income 37667.1

C

Other than, the factors analysed in A and B there are not any other factors on the basis of

which Gloria can take into consideration the best option. The reason underlying this fact is that

in the above two points the income tax and that disposable income has been calculated. With the

help of the income tax it is evident that the tax for both the option is same that is 10000. This is

pertaining to the fact that the annual salary is same and due to this the tax will also be same that

is 10000 on the basis of 20 %. Further, the decision to be taken for the selection of the best

option will be based on disposable personal income only (Liu, 2018). This is pertaining to the

fact that disposable income is the one which is used by the person and in case the disposable

income will be more, then that option will be suitable to the person. Hence, on this basis the

option 2 will be suitable and selected. The reason pertaining to the fact is that it involves more

disposable income in comparison to the option 1.

PART 2 – Income Tax Administration

Analysing the difference between tax evasion and tax avoidance.

Tax evasion Tax avoidance

The tax evasion is being referred to as the

reduction within the tax liability with the use

of some illegal ways.

On the other hand, the tax avoidance is being

defined as minimising of the liability of tax by

using such methods which do not result in the

violation of any tax rule.

This is also known as the concealment of the

tax

on the contradictory note, tax avoidance is

known as hedging of the tax.

The major attribute which highlight the fact

that there is tax evasion is the use of illegal and

objectionable working

In against of this, the attributing highlighting

tax avoidance is immoral in nature and this

involve making modification within the law

but not breaking the law.

The objectives of undertaking the tax evasion

is to reduce the liability of the tax by

undertaking use of unfair means.

On the other side, the purpose or objective of

using tax avoidance is to have some reduction

within the application of laws (Gardner, 2018).

The tax evasion generally occurs at the time

after the tax liability arises.

In against of this, tax avoidance happens just

before the occurrence of tax liability.

which Gloria can take into consideration the best option. The reason underlying this fact is that

in the above two points the income tax and that disposable income has been calculated. With the

help of the income tax it is evident that the tax for both the option is same that is 10000. This is

pertaining to the fact that the annual salary is same and due to this the tax will also be same that

is 10000 on the basis of 20 %. Further, the decision to be taken for the selection of the best

option will be based on disposable personal income only (Liu, 2018). This is pertaining to the

fact that disposable income is the one which is used by the person and in case the disposable

income will be more, then that option will be suitable to the person. Hence, on this basis the

option 2 will be suitable and selected. The reason pertaining to the fact is that it involves more

disposable income in comparison to the option 1.

PART 2 – Income Tax Administration

Analysing the difference between tax evasion and tax avoidance.

Tax evasion Tax avoidance

The tax evasion is being referred to as the

reduction within the tax liability with the use

of some illegal ways.

On the other hand, the tax avoidance is being

defined as minimising of the liability of tax by

using such methods which do not result in the

violation of any tax rule.

This is also known as the concealment of the

tax

on the contradictory note, tax avoidance is

known as hedging of the tax.

The major attribute which highlight the fact

that there is tax evasion is the use of illegal and

objectionable working

In against of this, the attributing highlighting

tax avoidance is immoral in nature and this

involve making modification within the law

but not breaking the law.

The objectives of undertaking the tax evasion

is to reduce the liability of the tax by

undertaking use of unfair means.

On the other side, the purpose or objective of

using tax avoidance is to have some reduction

within the application of laws (Gardner, 2018).

The tax evasion generally occurs at the time

after the tax liability arises.

In against of this, tax avoidance happens just

before the occurrence of tax liability.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The type of act under which tax evasion is

included is a criminal act.

The type of act through which the tax

avoidance is seen is legal.

The major consequence of tax evasion is either

penalty or imprisonment.

On the other hand, consequence of tax

avoidance is deferment of tax liability.

Two recent policies introduced by HMRC for incidence tax evasion and avoidance

The first and foremost step taken by the HMRC in direction of managing tax evasion and

avoidance is that that they have set more than 60 regional offices across UK since the year 2011.

The aim of all these task force is on the high risk sectors involving tobacco sales, alcohol and

other related product and services (Lenoel, Matsu and Naisbitt, 2018). This is particularly in

these companies the income is very high and in case they will evade tax then it will affect the

earning of the government to a great extent.

In addition to this, HMRC has also organized for some campaigns to persuade the

professional and businessman to pay the taxes on time. This involves using different letters,

advertisement, social media and many other different sources. This campaign will outline the

different types of the actions being taken against the people who are evading or avoiding taxes.

PART 3 – Income Tax Administration

In the resent case Mrs Jill Johnson has purchased two leaseholds and three freehold

housed. During the purchase of these property she paid some legal fees, stamp duty and also

some other charges for the acquiring of the machine. After that she also renovated the building

and thereafter sold for profit. Hence, this is a part of capital gain tax (Capital Gains Tax: What It

Is And How To Avoid It, 2021). This is pertaining to the fact that because of selling of investment

property, the person has gain on selling of capital asset. In addition to this, there were no any

other income being earned by the Mrs Jill and due to this there will not be any of the income tax

being payable. The reason pertaining to the fact is that the income tax is being paid on the profit

or the income earned by the person. Hence, in the present case of Mrs Jill she has purchased the

house and made some expenses on its repair and then sold for profit. Hence, this is a case of

capital gain tax and not the case of income tax.

In case Mrs Jill was working or having business in the field of buying and selling of the

investment then this will be resulting in the inclusion within income tax. Hence, as a result of

this, the selling of the investment will be included within the income of the person and tax will

included is a criminal act.

The type of act through which the tax

avoidance is seen is legal.

The major consequence of tax evasion is either

penalty or imprisonment.

On the other hand, consequence of tax

avoidance is deferment of tax liability.

Two recent policies introduced by HMRC for incidence tax evasion and avoidance

The first and foremost step taken by the HMRC in direction of managing tax evasion and

avoidance is that that they have set more than 60 regional offices across UK since the year 2011.

The aim of all these task force is on the high risk sectors involving tobacco sales, alcohol and

other related product and services (Lenoel, Matsu and Naisbitt, 2018). This is particularly in

these companies the income is very high and in case they will evade tax then it will affect the

earning of the government to a great extent.

In addition to this, HMRC has also organized for some campaigns to persuade the

professional and businessman to pay the taxes on time. This involves using different letters,

advertisement, social media and many other different sources. This campaign will outline the

different types of the actions being taken against the people who are evading or avoiding taxes.

PART 3 – Income Tax Administration

In the resent case Mrs Jill Johnson has purchased two leaseholds and three freehold

housed. During the purchase of these property she paid some legal fees, stamp duty and also

some other charges for the acquiring of the machine. After that she also renovated the building

and thereafter sold for profit. Hence, this is a part of capital gain tax (Capital Gains Tax: What It

Is And How To Avoid It, 2021). This is pertaining to the fact that because of selling of investment

property, the person has gain on selling of capital asset. In addition to this, there were no any

other income being earned by the Mrs Jill and due to this there will not be any of the income tax

being payable. The reason pertaining to the fact is that the income tax is being paid on the profit

or the income earned by the person. Hence, in the present case of Mrs Jill she has purchased the

house and made some expenses on its repair and then sold for profit. Hence, this is a case of

capital gain tax and not the case of income tax.

In case Mrs Jill was working or having business in the field of buying and selling of the

investment then this will be resulting in the inclusion within income tax. Hence, as a result of

this, the selling of the investment will be included within the income of the person and tax will

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

be applied over it (Kerley, 2019). As per the HMRC, the capital gain tax is being defined as the

profit which is being earned by the person in case when something is sold that is asset with the

increased value. For instance, a land is purchased for £5000 but in future it is sold for £20000

the it implies that there is a gain of £15000 which is 20000 – 5000. Further in case any capital

gain is earned by the person then on this gain as well the tax need to be paid. This is particularly

because of the reason that this is an additional income of the person and on this, the tax is being

charged on some other rate as done on some other regular income.

CONCLUSION

The above report concluded the fact that taxation is a source of income for the

government which is being charged by the government from business and citizen of the country.

For the various business the different tax rates and related adjustments are provided within the

guidelines and the companies have to comply with those. Hence, the above report evaluated

different adjustment relating to calculation of taxable income and NIC in the above both the

cases.

profit which is being earned by the person in case when something is sold that is asset with the

increased value. For instance, a land is purchased for £5000 but in future it is sold for £20000

the it implies that there is a gain of £15000 which is 20000 – 5000. Further in case any capital

gain is earned by the person then on this gain as well the tax need to be paid. This is particularly

because of the reason that this is an additional income of the person and on this, the tax is being

charged on some other rate as done on some other regular income.

CONCLUSION

The above report concluded the fact that taxation is a source of income for the

government which is being charged by the government from business and citizen of the country.

For the various business the different tax rates and related adjustments are provided within the

guidelines and the companies have to comply with those. Hence, the above report evaluated

different adjustment relating to calculation of taxable income and NIC in the above both the

cases.

REFERENCES

Books and Journals

Beenstock, M. ed., 2018. Work, welfare and taxation: A study of labour supply incentives in the

UK (Vol. 4). Routledge.

Buckton, C. H., and et.al., 2018. The palatability of sugar-sweetened beverage taxation: A

content analysis of newspaper coverage of the UK sugar debate. Plos one. 13(12).

p.e0207576.

Gardner, L., 2018. TAXATION IN PORTUGUESE AFRICA-Administration and Taxation in

Former Portuguese Africa, 1900–1945. By Philip J. Havik, Alexander Keese, and Maciel

Santos. Cambridge, UK: Cambridge Scholars Publishing, 2015. Pp. 255. $81.95, hardcover

(ISBN 9781443870108). The Journal of African History. 59(1). pp.132-134.

Kerley, R., 2019. Public Spending and Taxation. Story of the Scottish Parliament: The First Two

Decades Explained, p.123.

Lenoel, C., Matsu, J. and Naisbitt, B., 2018. International evidence review on housing

taxation. Final report, UK Collaborative Centre for Housing Evidence. 3.

Liu, M. L., 2018. Where does multinational investment go with territorial taxation? Evidence

from the UK. International Monetary Fund.

Online

Capital Gains Tax: What It Is And How To Avoid It. 2021. [Online]. Available through: <

https://www.rockethq.com/learn/personal-finances/capital-gains-tax >

Books and Journals

Beenstock, M. ed., 2018. Work, welfare and taxation: A study of labour supply incentives in the

UK (Vol. 4). Routledge.

Buckton, C. H., and et.al., 2018. The palatability of sugar-sweetened beverage taxation: A

content analysis of newspaper coverage of the UK sugar debate. Plos one. 13(12).

p.e0207576.

Gardner, L., 2018. TAXATION IN PORTUGUESE AFRICA-Administration and Taxation in

Former Portuguese Africa, 1900–1945. By Philip J. Havik, Alexander Keese, and Maciel

Santos. Cambridge, UK: Cambridge Scholars Publishing, 2015. Pp. 255. $81.95, hardcover

(ISBN 9781443870108). The Journal of African History. 59(1). pp.132-134.

Kerley, R., 2019. Public Spending and Taxation. Story of the Scottish Parliament: The First Two

Decades Explained, p.123.

Lenoel, C., Matsu, J. and Naisbitt, B., 2018. International evidence review on housing

taxation. Final report, UK Collaborative Centre for Housing Evidence. 3.

Liu, M. L., 2018. Where does multinational investment go with territorial taxation? Evidence

from the UK. International Monetary Fund.

Online

Capital Gains Tax: What It Is And How To Avoid It. 2021. [Online]. Available through: <

https://www.rockethq.com/learn/personal-finances/capital-gains-tax >

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

APPENDIX

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.