Taxation Fundamentals: Income Tax, NICs, Policies, and HMRC Assessment

VerifiedAdded on 2023/06/15

|9

|2226

|228

Report

AI Summary

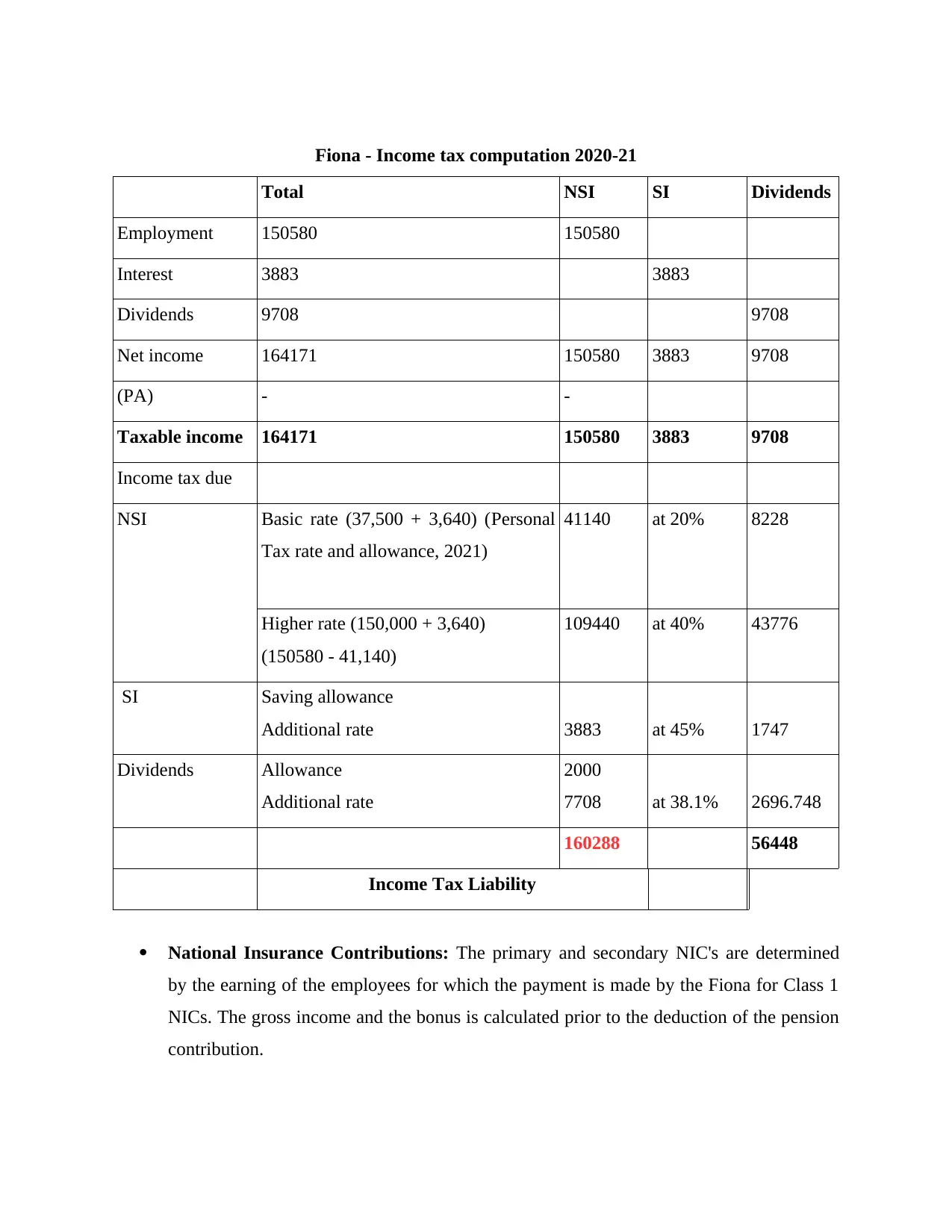

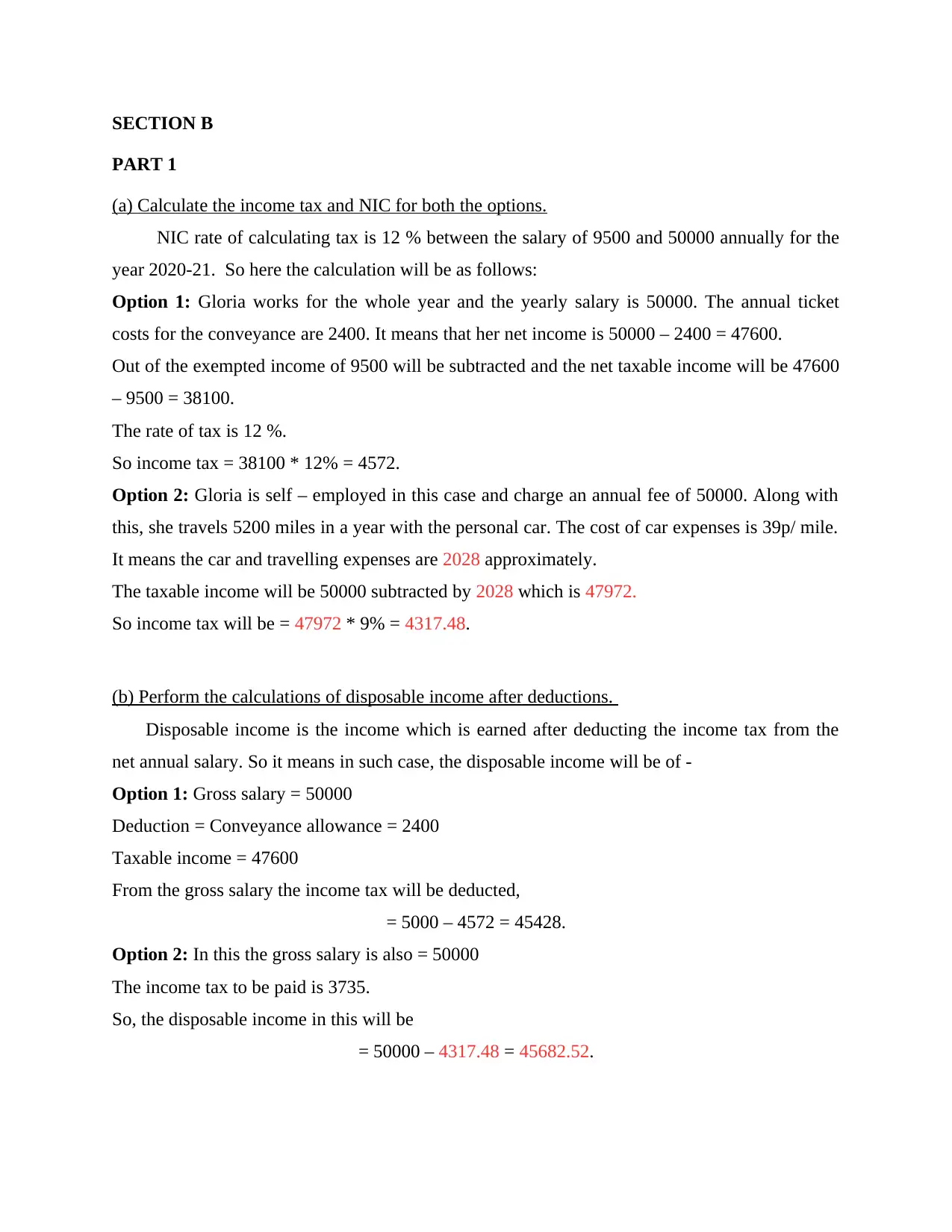

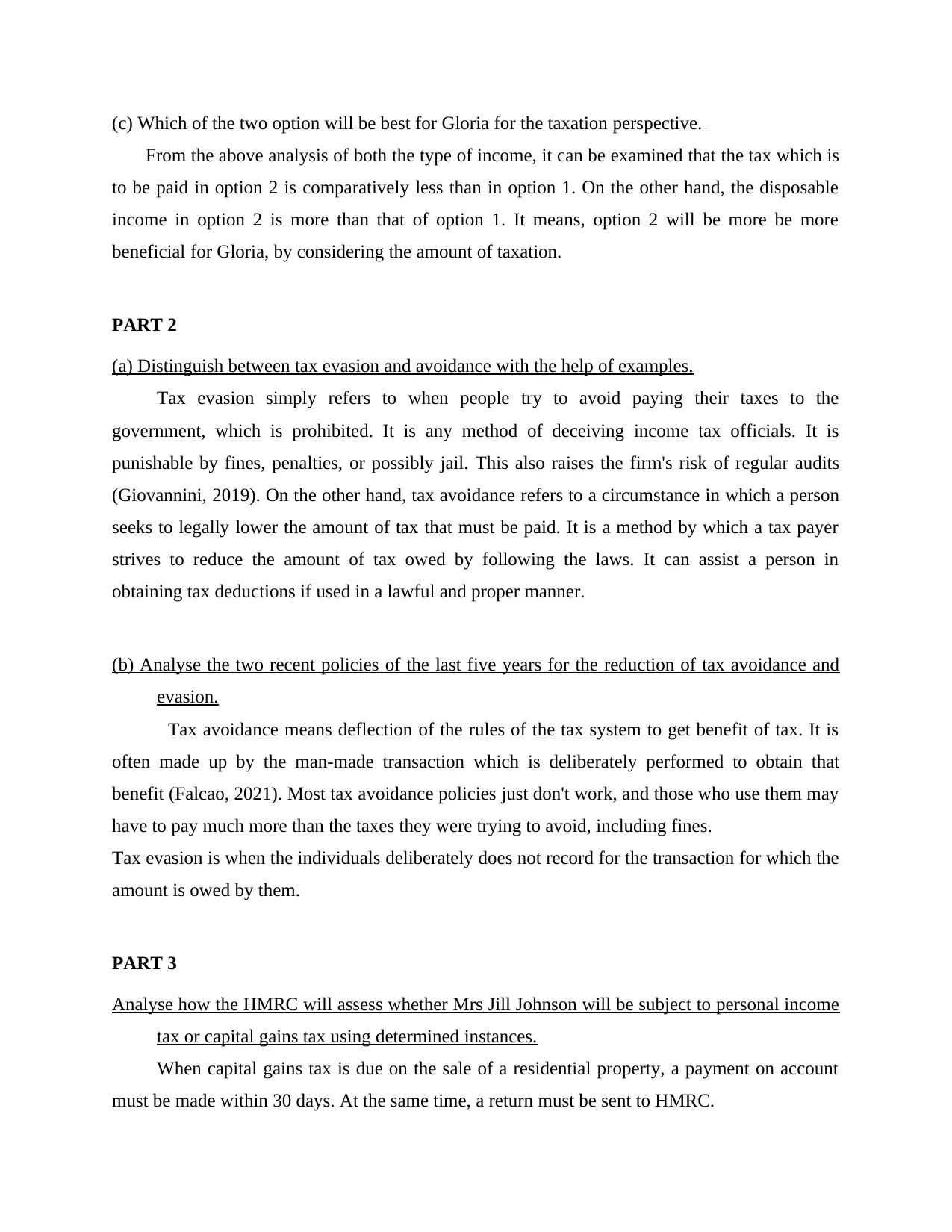

This report provides a detailed explanation of income tax and National Insurance Contributions (NICs), including calculations for various scenarios and an analysis of tax evasion and avoidance. It covers the assessment of income tax for the year 2020-2021, considering factors such as salary, bonuses, pension contributions, personal allowances, gift aid, and other benefits like company accommodation, car benefits, and music systems. The report also includes calculations for income tax and NICs under different employment options, disposable income after deductions, and a distinction between tax evasion and tax avoidance with relevant examples. Furthermore, it analyzes recent policies aimed at reducing tax avoidance and evasion and discusses how HMRC assesses personal income tax versus capital gains tax in specific instances. This document is available on Desklib, a platform offering a wide range of study tools and resources for students.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.