Income Tax Assessment: Deduction and Small Business CGT Concession

VerifiedAdded on 2023/06/05

|20

|5871

|144

Report

AI Summary

This report provides a detailed analysis of income tax consequences for individuals and small businesses in Australia, focusing on allowable deductions under Section 8-1 of ITAA 1997 and the Capital Gains Tax (CGT) concessions available to small businesses. It examines the conditions under which taxpayers can claim deductions for various expenses, including bank interest, lease payments, equipment purchases, and employee wages, while also identifying non-deductible expenses such as personal expenditures and certain business start-up costs. The report further explores the complexities and benefits of the small business CGT concessions, highlighting their role in supporting the Australian economy and reducing the tax compliance burden for small enterprises. It references relevant legal cases and statutory provisions to provide a comprehensive understanding of the current tax law system in Australia. Desklib offers a platform to access similar solved assignments and past papers for students.

Running head: TAXATION

Tax

Name of the Student:

Name of the university:

Authors Note:

Tax

Name of the Student:

Name of the university:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION

Table of Contents

Answer To Part A:.....................................................................................................................2

Answer To Part B:......................................................................................................................5

Reference..................................................................................................................................17

Table of Contents

Answer To Part A:.....................................................................................................................2

Answer To Part B:......................................................................................................................5

Reference..................................................................................................................................17

2TAXATION

Answer To Part A:

Issue:

The current issue is regarding the income tax consequence for the financial year

ended 2018 for Anna. In other words, to be exact the issue is, whether the person paying tax

qualifies for deduction under section “8-1 of ITAA 1997”?

Rule:

The provision of “section 8-1 of ITAA 1997” says that, a person paying tax can claim

deduction relating to transaction mentioned under the general deduction clause of the said act.

An expense or loss may be considered as deduction under section 8-1 and under certain

specific provision. A person paying tax can be allowed to claim deduction from the income

that is taxable only if the expense is a consequence of earning that income (Becker et al.,

2015). A taxpayer is not allowed to claim deduction under the negative or non-permissible

limb of section 8-1(2) of ITAA 1997. Expenses in the nature of capital, private or domestic is

not allowed for deduction.

If a person acquires loan for buying equipment and stock, then it is allowed for

deduction under the positive limb of the section 8-1 of ITAA 1997. The reason being, those

expenses are a result of producing assessable income or operating business with the intention

of creating an income that is taxable in nature (Saad, 2014).

The tax commissioner in the case of “Lunney v FCT” decided that the pre-requisite

of deriving income that is taxable should be considered. A person paying tax is allowed to

claim deduction under the general provision of section 8-1 of ITAA 1997, regarding the pre-

commencement of income producing acts. As decided by the court of law in the case of

“Softwood Pulp and paper v FCT”, the commissioner denied the deduction as the expense

Answer To Part A:

Issue:

The current issue is regarding the income tax consequence for the financial year

ended 2018 for Anna. In other words, to be exact the issue is, whether the person paying tax

qualifies for deduction under section “8-1 of ITAA 1997”?

Rule:

The provision of “section 8-1 of ITAA 1997” says that, a person paying tax can claim

deduction relating to transaction mentioned under the general deduction clause of the said act.

An expense or loss may be considered as deduction under section 8-1 and under certain

specific provision. A person paying tax can be allowed to claim deduction from the income

that is taxable only if the expense is a consequence of earning that income (Becker et al.,

2015). A taxpayer is not allowed to claim deduction under the negative or non-permissible

limb of section 8-1(2) of ITAA 1997. Expenses in the nature of capital, private or domestic is

not allowed for deduction.

If a person acquires loan for buying equipment and stock, then it is allowed for

deduction under the positive limb of the section 8-1 of ITAA 1997. The reason being, those

expenses are a result of producing assessable income or operating business with the intention

of creating an income that is taxable in nature (Saad, 2014).

The tax commissioner in the case of “Lunney v FCT” decided that the pre-requisite

of deriving income that is taxable should be considered. A person paying tax is allowed to

claim deduction under the general provision of section 8-1 of ITAA 1997, regarding the pre-

commencement of income producing acts. As decided by the court of law in the case of

“Softwood Pulp and paper v FCT”, the commissioner denied the deduction as the expense

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION

was not incurred for producing taxable income (Lang et al., 2018). It was used to establish

the business and the actual income producing activity. This deduction can be claimed only in

situation where the expense was incurred in earning the actual income. Thus, purchasing any

tool or equipment which assist in earing income will qualify for deduction which can be

claimed for the entire or a part depending on the cost of business and private use of asset

(Richardson et al., 2015).

A person can claim deduction when some of act travelling or employee traveling

result to expense. As said under section 25-100 of ITAA 1997, deduction for the travel

expense can be claimed in situation where the travel places are related income generating

activities. The taxpayer can claim deduction for travel expense when it forms part-performing

duties related to the job or business.

An individual who pays tax is allowed to assert deduction for majority of the expenses

that is incurred in carrying or running the business. The expenses incurred for purchase of

jewellery represents the mercantilism stock expense and it is allowed as deductions. On the

opposite hand, a private person paying tax is allowed to assert for the salaries and wages

that's paid to the worker or staff (Wilkins, 2015). If a person operates because the sole dealer,

or the business owner and not because the worker of the business and thus the owner of the

business cannot pay remuneration to themselves. However, on creating any variety of

nominal payment within the variety of regular payment or wages is usually control because

the profit distribution that does not forms the part of deductions.

Application:

The present case says that Anna has a jewellery business and she incurred a bank

interest of $6000 for acquiring equipment and stocks. She can claim deduction under the

affirmative wing of section 8-1 of ITAA 1997. Anna sustained the expenses in producing the

was not incurred for producing taxable income (Lang et al., 2018). It was used to establish

the business and the actual income producing activity. This deduction can be claimed only in

situation where the expense was incurred in earning the actual income. Thus, purchasing any

tool or equipment which assist in earing income will qualify for deduction which can be

claimed for the entire or a part depending on the cost of business and private use of asset

(Richardson et al., 2015).

A person can claim deduction when some of act travelling or employee traveling

result to expense. As said under section 25-100 of ITAA 1997, deduction for the travel

expense can be claimed in situation where the travel places are related income generating

activities. The taxpayer can claim deduction for travel expense when it forms part-performing

duties related to the job or business.

An individual who pays tax is allowed to assert deduction for majority of the expenses

that is incurred in carrying or running the business. The expenses incurred for purchase of

jewellery represents the mercantilism stock expense and it is allowed as deductions. On the

opposite hand, a private person paying tax is allowed to assert for the salaries and wages

that's paid to the worker or staff (Wilkins, 2015). If a person operates because the sole dealer,

or the business owner and not because the worker of the business and thus the owner of the

business cannot pay remuneration to themselves. However, on creating any variety of

nominal payment within the variety of regular payment or wages is usually control because

the profit distribution that does not forms the part of deductions.

Application:

The present case says that Anna has a jewellery business and she incurred a bank

interest of $6000 for acquiring equipment and stocks. She can claim deduction under the

affirmative wing of section 8-1 of ITAA 1997. Anna sustained the expenses in producing the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION

computable income and in the course of carrying on of her business with the intention of

producing taxable income (James et al., 2015).

She reports of her expense of $2000 for the lease of the shop and after the case of

“Ronpibon Tin NL v FCT”, it was decided that this expense would be considered for

deduction as it relevant and result of creating taxable income. The legal fees of $4,400 that

has occurred by Anna for getting the recommendation for establishing the business could be a

preliminary to the start of financial gain generating activity. By relating “Softwood Pulp &

Paper v FCT” non-deductible underneath general provision of “section 8-1”. Anna reports

associate expenses of $2200 for the acquisition of laptop computer. She used laptop computer

10% of the time for private purpose. Anna will solely claim 90th of the laptop computer price

for deductions as 10% of the laptop computer used comprised of private use.

The expenses of $2,500 incurred for gap party of search with native celebrities are

often classified as personal or domestic expenditure and non-deductible since the expenses

fails to fulfil the positive limbs and non-deductible underneath second negative limb of

“section 8-1 (2) (b)”. A sole dealer is allowed to assert deductions concerning the acquisition

of commerce stock since these expenses forms the part of carrying on of the business in

manufacturing the assessable financial gain (Avi-Yonah, 2015). Similarly, the price incurred

in investigation of shop is additionally deductible underneath the positive limbs of “section 8-

1” since the prices is essentially incurred and relevant within the taxpayer’s financial gain

manufacturing activity.

The traveling expenses for movement with business category that is incurred by Anna

for attending the New York fashion is classified because the personal in nature. Anna will be

denied to assert deductions below “section 8-1”. In addition, she incurred expenses on

accommodation and food that was in relation for the business purpose. Therefore, a deduction

computable income and in the course of carrying on of her business with the intention of

producing taxable income (James et al., 2015).

She reports of her expense of $2000 for the lease of the shop and after the case of

“Ronpibon Tin NL v FCT”, it was decided that this expense would be considered for

deduction as it relevant and result of creating taxable income. The legal fees of $4,400 that

has occurred by Anna for getting the recommendation for establishing the business could be a

preliminary to the start of financial gain generating activity. By relating “Softwood Pulp &

Paper v FCT” non-deductible underneath general provision of “section 8-1”. Anna reports

associate expenses of $2200 for the acquisition of laptop computer. She used laptop computer

10% of the time for private purpose. Anna will solely claim 90th of the laptop computer price

for deductions as 10% of the laptop computer used comprised of private use.

The expenses of $2,500 incurred for gap party of search with native celebrities are

often classified as personal or domestic expenditure and non-deductible since the expenses

fails to fulfil the positive limbs and non-deductible underneath second negative limb of

“section 8-1 (2) (b)”. A sole dealer is allowed to assert deductions concerning the acquisition

of commerce stock since these expenses forms the part of carrying on of the business in

manufacturing the assessable financial gain (Avi-Yonah, 2015). Similarly, the price incurred

in investigation of shop is additionally deductible underneath the positive limbs of “section 8-

1” since the prices is essentially incurred and relevant within the taxpayer’s financial gain

manufacturing activity.

The traveling expenses for movement with business category that is incurred by Anna

for attending the New York fashion is classified because the personal in nature. Anna will be

denied to assert deductions below “section 8-1”. In addition, she incurred expenses on

accommodation and food that was in relation for the business purpose. Therefore, a deduction

5TAXATION

is allowable. Citing the instances of “Lunney v FCT” the price incurred by anna to catch up

along with her friends is personal in nature and non-deductible below positive limbs of

“section 8-1”. Anna will claim deductions for wage and wages paid to staff but the wage paid

to herself is non-deductible since it constitutes nominal payment of remuneration and it'd be

treated as profit distribution (Bankman et al., 2017).

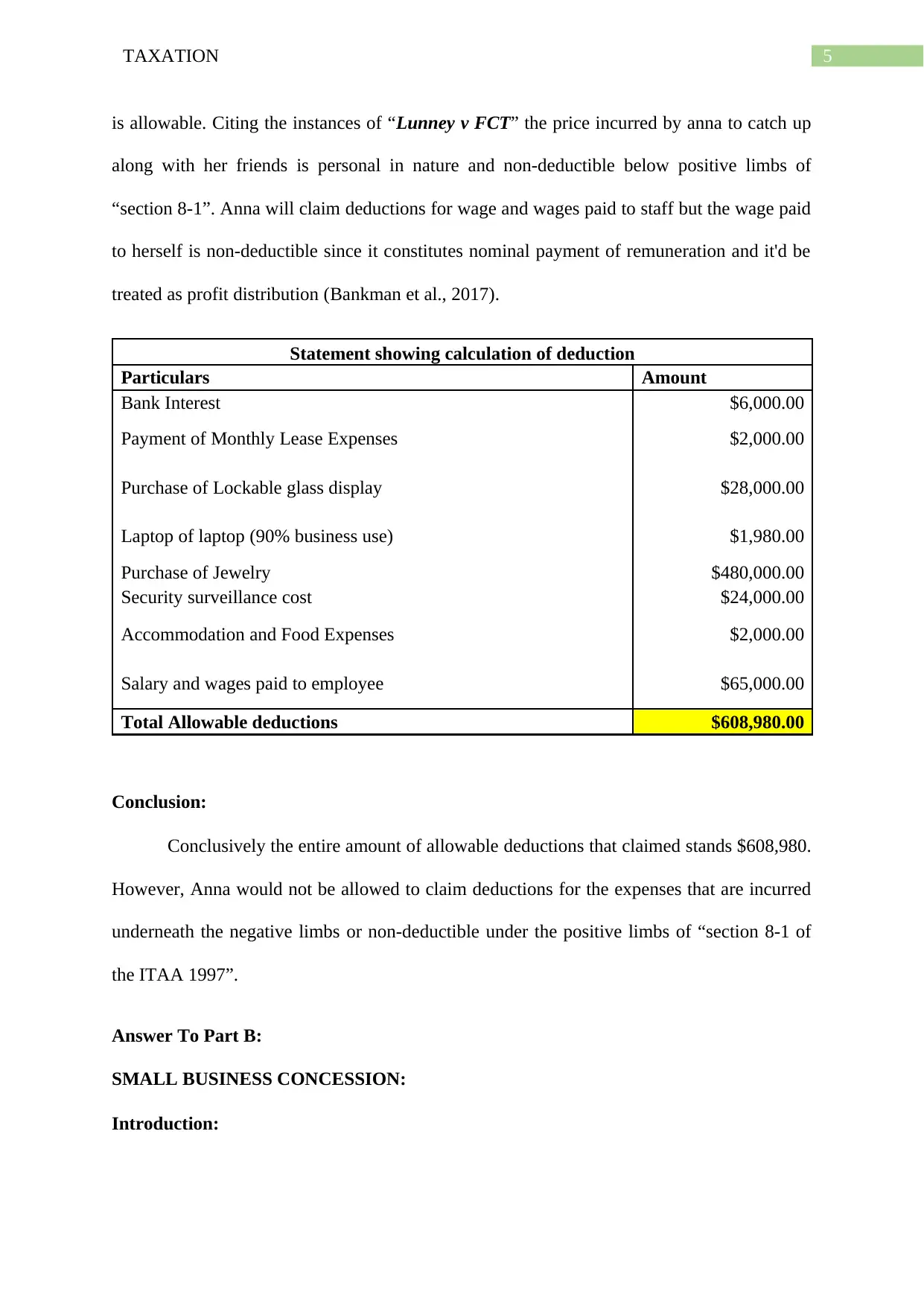

Statement showing calculation of deduction

Particulars Amount

Bank Interest $6,000.00

Payment of Monthly Lease Expenses $2,000.00

Purchase of Lockable glass display $28,000.00

Laptop of laptop (90% business use) $1,980.00

Purchase of Jewelry $480,000.00

Security surveillance cost $24,000.00

Accommodation and Food Expenses $2,000.00

Salary and wages paid to employee $65,000.00

Total Allowable deductions $608,980.00

Conclusion:

Conclusively the entire amount of allowable deductions that claimed stands $608,980.

However, Anna would not be allowed to claim deductions for the expenses that are incurred

underneath the negative limbs or non-deductible under the positive limbs of “section 8-1 of

the ITAA 1997”.

Answer To Part B:

SMALL BUSINESS CONCESSION:

Introduction:

is allowable. Citing the instances of “Lunney v FCT” the price incurred by anna to catch up

along with her friends is personal in nature and non-deductible below positive limbs of

“section 8-1”. Anna will claim deductions for wage and wages paid to staff but the wage paid

to herself is non-deductible since it constitutes nominal payment of remuneration and it'd be

treated as profit distribution (Bankman et al., 2017).

Statement showing calculation of deduction

Particulars Amount

Bank Interest $6,000.00

Payment of Monthly Lease Expenses $2,000.00

Purchase of Lockable glass display $28,000.00

Laptop of laptop (90% business use) $1,980.00

Purchase of Jewelry $480,000.00

Security surveillance cost $24,000.00

Accommodation and Food Expenses $2,000.00

Salary and wages paid to employee $65,000.00

Total Allowable deductions $608,980.00

Conclusion:

Conclusively the entire amount of allowable deductions that claimed stands $608,980.

However, Anna would not be allowed to claim deductions for the expenses that are incurred

underneath the negative limbs or non-deductible under the positive limbs of “section 8-1 of

the ITAA 1997”.

Answer To Part B:

SMALL BUSINESS CONCESSION:

Introduction:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION

In Australia, though big companies come into picture when it comes to shaping the

economy, the small business has an overall strong hold over the economy as well. All small

business together has a huge collective effect on the economy. In this part of the paper, we

will discuss about how small business can claim concession under the current tax law system

of Australia. When it comes to capital gain tax, small business enterprise has been given

more space compared to big companies. Section 152 of ITAA 1997, talks about small

business concession (Geljic et al., 2016). There are various policies under the current tax

regime that grants space to claim concession, thus in this part we will discuss about the

detailed statutory explanation of policies available for concession.

Small Business Concession

The private venture division of Australia has frequently sought after the testing

necessities value, effortlessness and effectiveness under the salary tax administration by

particularly setting centre around the idea of straightforwardness. Throughout the most recent

decade, various endeavours have been made to offer the private venture in Australian with

effortlessness and decrease weight of tax consistence with the assistance of disentangled

arrangement of taxation (Sanderson, 2015). By and by, disregarding making a few revisions

in the course of the most recent decade, the improved tax framework has been broadly

censured by the tax experts.

The small business frames the significant part of Australian economy. The small

business of Australia is around valued at $1.5 trillion. In a report distributed by Australian

Bureau of Statistics these small business with under $2 million turnover for each annum

makes up around 97% of the business in Australia. The small business is regularly named as

the motor for the Australian economy (Festa, 2018). The small business is particularly unfit

to accomplish the economies of expansive scale profits by their more prominent counterparts.

In Australia, though big companies come into picture when it comes to shaping the

economy, the small business has an overall strong hold over the economy as well. All small

business together has a huge collective effect on the economy. In this part of the paper, we

will discuss about how small business can claim concession under the current tax law system

of Australia. When it comes to capital gain tax, small business enterprise has been given

more space compared to big companies. Section 152 of ITAA 1997, talks about small

business concession (Geljic et al., 2016). There are various policies under the current tax

regime that grants space to claim concession, thus in this part we will discuss about the

detailed statutory explanation of policies available for concession.

Small Business Concession

The private venture division of Australia has frequently sought after the testing

necessities value, effortlessness and effectiveness under the salary tax administration by

particularly setting centre around the idea of straightforwardness. Throughout the most recent

decade, various endeavours have been made to offer the private venture in Australian with

effortlessness and decrease weight of tax consistence with the assistance of disentangled

arrangement of taxation (Sanderson, 2015). By and by, disregarding making a few revisions

in the course of the most recent decade, the improved tax framework has been broadly

censured by the tax experts.

The small business frames the significant part of Australian economy. The small

business of Australia is around valued at $1.5 trillion. In a report distributed by Australian

Bureau of Statistics these small business with under $2 million turnover for each annum

makes up around 97% of the business in Australia. The small business is regularly named as

the motor for the Australian economy (Festa, 2018). The small business is particularly unfit

to accomplish the economies of expansive scale profits by their more prominent counterparts.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION

With developing significance of small business, the administration has routinely attempted of

decreasing the tax consistence cost. In the long run, with low acknowledgment rate and

across the board feedback, drove the modernized and rebadged frameworks for concessions

known as SBE administration.

As indicated by the leading body of taxation a well-made tax concessionary

administration and subsidisations is gone for helping the small business that are looked with

particular difficulties. The small business concession can assume an indispensable part in

helping the small businesses at each period of their business life expectancy. This reaches

from essential start up face to development and retirement of business proprietors (Evans et

al., 2014). The present writing would diagram the small business CGT concession in

Australia and would basically evaluate the CGT concession for small business together with

the general targets of policy. The investigation would likewise evaluate whether the

concessionary administration meets the policy goals went with facilitate fundamental

suggestions to the plan.

The Small Business CGT Concession:

Any small business element that fulfils the basic criteria that is sketched out under the

"section 152 of the ITAA 1997" is qualified for a wide assortment of CGT concessions that

are expressed under the "subdivision 152Bto 152E". The imperative effect of the concessions

gave to small business incorporates that the capital gains that starts on influencing the

dynamic asset sale to be brought down by half and 100%. In any case, unique in relation to

the next five concessions that are accessible to small business, the taxpayers of small business

substance barely chooses to execute these necessities (Sadiq and Marsden, 2014). Given that

a small business unit satisfies the basic conditions, the element acquires the CGT alleviation.

Subsequently, the tax consultants would frequently utilize arrangement of small business

With developing significance of small business, the administration has routinely attempted of

decreasing the tax consistence cost. In the long run, with low acknowledgment rate and

across the board feedback, drove the modernized and rebadged frameworks for concessions

known as SBE administration.

As indicated by the leading body of taxation a well-made tax concessionary

administration and subsidisations is gone for helping the small business that are looked with

particular difficulties. The small business concession can assume an indispensable part in

helping the small businesses at each period of their business life expectancy. This reaches

from essential start up face to development and retirement of business proprietors (Evans et

al., 2014). The present writing would diagram the small business CGT concession in

Australia and would basically evaluate the CGT concession for small business together with

the general targets of policy. The investigation would likewise evaluate whether the

concessionary administration meets the policy goals went with facilitate fundamental

suggestions to the plan.

The Small Business CGT Concession:

Any small business element that fulfils the basic criteria that is sketched out under the

"section 152 of the ITAA 1997" is qualified for a wide assortment of CGT concessions that

are expressed under the "subdivision 152Bto 152E". The imperative effect of the concessions

gave to small business incorporates that the capital gains that starts on influencing the

dynamic asset sale to be brought down by half and 100%. In any case, unique in relation to

the next five concessions that are accessible to small business, the taxpayers of small business

substance barely chooses to execute these necessities (Sadiq and Marsden, 2014). Given that

a small business unit satisfies the basic conditions, the element acquires the CGT alleviation.

Subsequently, the tax consultants would frequently utilize arrangement of small business

8TAXATION

CGT concessions that are given under the "Division 152 of the ITAA 1997" when the

customers of small business make the sale of dynamic asset.

By actualizing the specific provisions of concessions, the tax consultants can bring

down tax liability of capital gains beginning from the sale of their customer's business. As

clear, the main boss parts of the tax consultants are to decrease the taxpayer's issues of

diminished tax liability anyway the small business CGT concessions are viewed as one of the

strategy through which the tax specialists can significantly get the concession for the small

business substance (Yuan, 2014).

As per Sadiq and Marsden (2014) the small business CGT concessions is viewed as

one of most troublesome provision under the ITAA. While the taxpayers are anxious to

implement the small business CGT concessions however a few taxpayers have referred to

that the provision is not anything but difficult to implement and regularly devours time to

explore through which at last includes the tax consistence costs (Ma, 2015). There were

remarks that the CGT concessions is certainly well known strategy yet includes broad

measure of exertion. As expressed by a business can cause a cost that would run somewhere

in the range of $5000 and $10,000 for their company to learn whether the business meets all

requirements for the concessions under the small business CGT administration.

In spite of the trouble and higher inalienable costs related with the utilization of small

business CGT concessions, taxpayers see the tax concession administration as the profoundly

refreshing concession. This can be portrayed through the sheer size of tax minimization

advantage which can be acquired through utilizing the small business CGT concession.

Experimental confirmations have proposed that the small business concessions expressed

under Division 152 is exceptionally intricate and in the end results in vital cost of compliance

for the taxpayers (Tran‐Nam et al., 2016). In opposite, the tax specialist's remarks showed up

CGT concessions that are given under the "Division 152 of the ITAA 1997" when the

customers of small business make the sale of dynamic asset.

By actualizing the specific provisions of concessions, the tax consultants can bring

down tax liability of capital gains beginning from the sale of their customer's business. As

clear, the main boss parts of the tax consultants are to decrease the taxpayer's issues of

diminished tax liability anyway the small business CGT concessions are viewed as one of the

strategy through which the tax specialists can significantly get the concession for the small

business substance (Yuan, 2014).

As per Sadiq and Marsden (2014) the small business CGT concessions is viewed as

one of most troublesome provision under the ITAA. While the taxpayers are anxious to

implement the small business CGT concessions however a few taxpayers have referred to

that the provision is not anything but difficult to implement and regularly devours time to

explore through which at last includes the tax consistence costs (Ma, 2015). There were

remarks that the CGT concessions is certainly well known strategy yet includes broad

measure of exertion. As expressed by a business can cause a cost that would run somewhere

in the range of $5000 and $10,000 for their company to learn whether the business meets all

requirements for the concessions under the small business CGT administration.

In spite of the trouble and higher inalienable costs related with the utilization of small

business CGT concessions, taxpayers see the tax concession administration as the profoundly

refreshing concession. This can be portrayed through the sheer size of tax minimization

advantage which can be acquired through utilizing the small business CGT concession.

Experimental confirmations have proposed that the small business concessions expressed

under Division 152 is exceptionally intricate and in the end results in vital cost of compliance

for the taxpayers (Tran‐Nam et al., 2016). In opposite, the tax specialist's remarks showed up

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION

inverse. The tax master saw the CGT concession as the advantage that potentially stream

toward the taxpayers and by implementing this tax concession administration, they can

exceed the cost compliance costs.

Existing writing has seen that the CGT concession for small business upsets the

principle of straightforwardness. As indicated by the taxpayers are all the more regularly

compelled to invest a substantial measure of energy in deciding if their business fulfil the

basic conditions and are from now on qualified for at least one CGT concessions (Chung,

2016). This sort of trouble existent in the eligibility govern drives the customer to confront

increment aggregate of bookkeeping expenses due to the time that is spend by the tax

operator in evaluating every concession and discovering which concessions fits well to the

business.

As an outcome of this, it is plausible where the professionals trust that the attainable

quality of the markdown is marginal with taxpayers may be exhorted that the costs that are

caused in inquiring about the attainable quality of the tax concession and implementing the

same may be high to legitimize. This speaks to that the inalienable cost that are connected

with the tax concessions multifaceted nature, couple of qualified business will most likely be

unable to utilize those regimes of tax concession as they can't bear the cost of the risk of

carrying the costs with no benefits identified with it. Thusly, the regimes of tax concessions

damages the tax principle of equity (Lignier et al., 2014). On a decisive note, the small

business CGT concessions are seen as an instrument of more noteworthy advantage anyway

the trouble in eligibility rules is extremely limiting and costly; maybe require a direct

extensive assessment.

Overall Policy Objective under Present System of Taxation:

inverse. The tax master saw the CGT concession as the advantage that potentially stream

toward the taxpayers and by implementing this tax concession administration, they can

exceed the cost compliance costs.

Existing writing has seen that the CGT concession for small business upsets the

principle of straightforwardness. As indicated by the taxpayers are all the more regularly

compelled to invest a substantial measure of energy in deciding if their business fulfil the

basic conditions and are from now on qualified for at least one CGT concessions (Chung,

2016). This sort of trouble existent in the eligibility govern drives the customer to confront

increment aggregate of bookkeeping expenses due to the time that is spend by the tax

operator in evaluating every concession and discovering which concessions fits well to the

business.

As an outcome of this, it is plausible where the professionals trust that the attainable

quality of the markdown is marginal with taxpayers may be exhorted that the costs that are

caused in inquiring about the attainable quality of the tax concession and implementing the

same may be high to legitimize. This speaks to that the inalienable cost that are connected

with the tax concessions multifaceted nature, couple of qualified business will most likely be

unable to utilize those regimes of tax concession as they can't bear the cost of the risk of

carrying the costs with no benefits identified with it. Thusly, the regimes of tax concessions

damages the tax principle of equity (Lignier et al., 2014). On a decisive note, the small

business CGT concessions are seen as an instrument of more noteworthy advantage anyway

the trouble in eligibility rules is extremely limiting and costly; maybe require a direct

extensive assessment.

Overall Policy Objective under Present System of Taxation:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION

The tax concessions for the taxpayers of small business frames a vital component of

the present system of Australian taxation system. There are various policy targets that

supports the tax concession. Certain policies are gone for decreasing the weight of

compliance while different policies are gone for offering more prominent tax help to elevate

the entrance to business achievement. While different policies are gone for elevating more

extensive access to acquire finance for their retirement and with concessions that are made to

meet the mix of the above expressed goals (Woellner et al., 2015).

The lower company tax rate concession was started amid 2015-16 with decrease the

rate of company tax to 28.5 for business that have a yearly-accumulated turnover of lower

than $2 million. In the next year 2015-17 the rate of company tax rate was additionally

brought down to 27.5% for business that have the yearly turnover of lower than $10 million.

The Capital gains tax concession is another policy where the proprietors of the net assets of

not more noteworthy than $6 million. The yearly sales turnover of lower than $2 million are

qualified for a small business CGT concession on the small business dynamic assets which is

held continually for a time of 15 years or where the taxpayers accomplishes the age of 55 and

resigns (Trad and Freudenberg, 2017).

The small business CGT concession give half decrease of the capital gains that starts

from the sale of dynamic small business assets together with the general CGT discount. The

policy gives the small business the exemption until the lifetime top of $500,000 on the capital

gains beginning from the sale of dynamic small business assets and where the sale continues

of the assets are utilized to finance the retirement (Evans and Krever, 2017). The present

policy gives the small business the CGT rollover helps for the capital gains beginning upon

the sale of the small business dynamic assets given the sales continues are employed in the

buy of dynamic small business assets.

The tax concessions for the taxpayers of small business frames a vital component of

the present system of Australian taxation system. There are various policy targets that

supports the tax concession. Certain policies are gone for decreasing the weight of

compliance while different policies are gone for offering more prominent tax help to elevate

the entrance to business achievement. While different policies are gone for elevating more

extensive access to acquire finance for their retirement and with concessions that are made to

meet the mix of the above expressed goals (Woellner et al., 2015).

The lower company tax rate concession was started amid 2015-16 with decrease the

rate of company tax to 28.5 for business that have a yearly-accumulated turnover of lower

than $2 million. In the next year 2015-17 the rate of company tax rate was additionally

brought down to 27.5% for business that have the yearly turnover of lower than $10 million.

The Capital gains tax concession is another policy where the proprietors of the net assets of

not more noteworthy than $6 million. The yearly sales turnover of lower than $2 million are

qualified for a small business CGT concession on the small business dynamic assets which is

held continually for a time of 15 years or where the taxpayers accomplishes the age of 55 and

resigns (Trad and Freudenberg, 2017).

The small business CGT concession give half decrease of the capital gains that starts

from the sale of dynamic small business assets together with the general CGT discount. The

policy gives the small business the exemption until the lifetime top of $500,000 on the capital

gains beginning from the sale of dynamic small business assets and where the sale continues

of the assets are utilized to finance the retirement (Evans and Krever, 2017). The present

policy gives the small business the CGT rollover helps for the capital gains beginning upon

the sale of the small business dynamic assets given the sales continues are employed in the

buy of dynamic small business assets.

11TAXATION

The present policy gives the small business the moment asset discounting under the

rearranged depreciation rules. The small business elements that have the aggregate turnover

of lower than $10 million can get the entrance of concessional depreciation course of action

for its business assets (Freudenberg et al., 2017). Under such concessions, the business

elements are permitted to promptly assert reasonings for those assets that costs lower than as

far as possible. Policies, for example, rebuild rollover alleviation gives the small business

proprietors of dynamic assets with the CGT and salary tax rollover help identifying with bona

fide business rebuild in view of the conditions that the economic responsibility for assets is

unaltered. The rollover is accessible for the business that have the aggregate turnover of

lower than $10 million.

The present policy objective gives the small business improved tenets of exchanging

stock. Small businesses that have the aggregated yearly sales turnover of lower than $10

million may utilize the disentangled exchanging stock regimes. Under these regimes, the

small business can choose not to represent the adjustments in the stock values for the wage

year finished given the distinction between the opening estimation of the stock close by and

the assessed stock close by toward the year's end would not go past $5000. The policy

objective convincingly conveys that the tax system likewise masterminds positive results to

the section of small business by making it simple to pull in the consideration of financial

specialists (Freebairn, 2016).

Critical Evaluation of SBE Concession:

The customary tax policy needs a tax regime with the goal that it can satisfy certain

number of assorted and as often as possible clashing criteria to be estimated as the great tax

policy. The principles of equity, comfort, sureness and economy is regularly seen as the old-

style gauges where distinctive government and administrative units generally attempt these

criteria in some frame while applying the new provision of tax regimes alongside the general

The present policy gives the small business the moment asset discounting under the

rearranged depreciation rules. The small business elements that have the aggregate turnover

of lower than $10 million can get the entrance of concessional depreciation course of action

for its business assets (Freudenberg et al., 2017). Under such concessions, the business

elements are permitted to promptly assert reasonings for those assets that costs lower than as

far as possible. Policies, for example, rebuild rollover alleviation gives the small business

proprietors of dynamic assets with the CGT and salary tax rollover help identifying with bona

fide business rebuild in view of the conditions that the economic responsibility for assets is

unaltered. The rollover is accessible for the business that have the aggregate turnover of

lower than $10 million.

The present policy objective gives the small business improved tenets of exchanging

stock. Small businesses that have the aggregated yearly sales turnover of lower than $10

million may utilize the disentangled exchanging stock regimes. Under these regimes, the

small business can choose not to represent the adjustments in the stock values for the wage

year finished given the distinction between the opening estimation of the stock close by and

the assessed stock close by toward the year's end would not go past $5000. The policy

objective convincingly conveys that the tax system likewise masterminds positive results to

the section of small business by making it simple to pull in the consideration of financial

specialists (Freebairn, 2016).

Critical Evaluation of SBE Concession:

The customary tax policy needs a tax regime with the goal that it can satisfy certain

number of assorted and as often as possible clashing criteria to be estimated as the great tax

policy. The principles of equity, comfort, sureness and economy is regularly seen as the old-

style gauges where distinctive government and administrative units generally attempt these

criteria in some frame while applying the new provision of tax regimes alongside the general

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.