Critical Analysis: Key Audit Matters in Independent Audit Reports

VerifiedAdded on 2023/03/23

|15

|3445

|52

Essay

AI Summary

This essay provides a comprehensive analysis of key audit matters (KAM) in independent audit reports, focusing on the implications of ISA 701 following the global financial crisis triggered by the collapse of Lehman Brothers. It explores the rationale behind the new auditing standard ASA 701, addressing shareholder demands for greater transparency and earlier warnings of potential issues. The essay evaluates the efficiency of reporting KAM, the process of determining key matters in auditing, and provides examples such as Nearmap Limited and the Bank of Queensland. It further discusses the benefits of implementing KAM, emphasizing its role in improving the understanding and reliability of audit reports. The document also touches on the failure of other big companies due to unethical accounting behaviours and provide a solution by addressing key audit matters.

Analyze and evaluate key audit matters in audit reports

Abstract

In this paper, we explore the new international standard auditing regulation ISA 701 known as

the key audit matters (KAM) and its inclusion in independent audit reports. The explains in detail

what key audit matters are and how their inclusion in reports will affect audit reports, companies,

investors, and the public. The auditor has the mandate to liaise with key players in the company

and engaging external sources concerning financial misstatements which occur through error or

fraud. The paper highlights the case of the demise of Lehman Company limited widely known as

Lehman brothers which caused a global financial crisis when the company filed for bankruptcy.

It also touches on failure of other big companies due to unethical accounting behaviours and

provide a solution by addressing key audit matters.

Contents

Abstract............................................................................................................................................1

Introduction......................................................................................................................................2

The collapse of Lehman firm.......................................................................................................3

What is ISA 701...........................................................................................................................4

The Scope of ISA.........................................................................................................................5

Evaluate the efficiency of reporting KAM...............................................................................5

Determining the key matters in auditing..................................................................................6

Abstract

In this paper, we explore the new international standard auditing regulation ISA 701 known as

the key audit matters (KAM) and its inclusion in independent audit reports. The explains in detail

what key audit matters are and how their inclusion in reports will affect audit reports, companies,

investors, and the public. The auditor has the mandate to liaise with key players in the company

and engaging external sources concerning financial misstatements which occur through error or

fraud. The paper highlights the case of the demise of Lehman Company limited widely known as

Lehman brothers which caused a global financial crisis when the company filed for bankruptcy.

It also touches on failure of other big companies due to unethical accounting behaviours and

provide a solution by addressing key audit matters.

Contents

Abstract............................................................................................................................................1

Introduction......................................................................................................................................2

The collapse of Lehman firm.......................................................................................................3

What is ISA 701...........................................................................................................................4

The Scope of ISA.........................................................................................................................5

Evaluate the efficiency of reporting KAM...............................................................................5

Determining the key matters in auditing..................................................................................6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

KAM report in Nearmap limited..................................................................................................8

Key audit matters identified in Nearmap limited.....................................................................9

Conclusion.....................................................................................................................................12

References......................................................................................................................................13

Introduction

There have been numerous discussions to improve the auditor's reports to allow the investors to

understand financial statements in audit reports. The collapse of big companies like WorldCom,

Enron, and Lehman's company raised a red flag in the financial markets after their fall caused a

financial crisis in the stock exchange security. The crisis spurred the regulators and the users to

address the role of auditors and come up with a way that will detect and deter fraud from

preventing high profile companies filing for bankruptcy or collapsing. Regulatory bodies like the

international auditing and assurance standard board (IAASB), the public company accounting

oversight board (PCAOB) among others have come up with regulations to improve audit reports.

After the collapse of some big companies in the world due to accounting irregularities, stake

holders were alarmed and asked for a growing concern in entities. This led to the introduction of

a new Auditing standard ISA 701 known as the Key Audit Matters. These matters are supposed

to be identified by auditors by communicating with those charged with governance then included

in audit reports.

Key audit matters identified in Nearmap limited.....................................................................9

Conclusion.....................................................................................................................................12

References......................................................................................................................................13

Introduction

There have been numerous discussions to improve the auditor's reports to allow the investors to

understand financial statements in audit reports. The collapse of big companies like WorldCom,

Enron, and Lehman's company raised a red flag in the financial markets after their fall caused a

financial crisis in the stock exchange security. The crisis spurred the regulators and the users to

address the role of auditors and come up with a way that will detect and deter fraud from

preventing high profile companies filing for bankruptcy or collapsing. Regulatory bodies like the

international auditing and assurance standard board (IAASB), the public company accounting

oversight board (PCAOB) among others have come up with regulations to improve audit reports.

After the collapse of some big companies in the world due to accounting irregularities, stake

holders were alarmed and asked for a growing concern in entities. This led to the introduction of

a new Auditing standard ISA 701 known as the Key Audit Matters. These matters are supposed

to be identified by auditors by communicating with those charged with governance then included

in audit reports.

The collapse of Lehman firm

In the year 1850, three brothers Henry, Emmanuel and Mayer Lehman founded the Lehman's

company. This company rose to become among the most significant investment companies in the

United States of America (USA) with over 25,000 employees across the world. Unfortunately,

the company closed down in the year 2008 due to bankruptcy, causing a global financial crisis.

This filing was the most talked about in history compared to other companies that filed for

bankruptcy before Lehman. At the time of filing, the company had $619 billion in debts and

$639 billion in total assets. The collapse of Lehman was a huge blow to global markets because

it contributed to a loss of close to $10 trillion in market capitalization (Wiggins, Piontek, and

Metrick, 2019)

Being a major player not only In the Us but also across the globe, its collapse affected the global

financial markets as well as the US government. What triggered the fall of the Lehman brothers

was losses in the mortgage, dramatic increase in mortgage defaults and severe tightening

liquidity (Fitzpatrick and Thomson, 2016).

Ernst & young accountancy firm was criticized for contributing to the fall of Lehman by failing

to point out a financial misstatement found in the entities financial statement. Ernst & young was

not the first auditing firm to be implicated in an entities failure. Andersen was also implicated in

the WorldCom bank case. This called for the need to revise the regulations governing auditors to

ensure they are guided by regulations in their line of work. ISA 701clearly outline the

responsibilities of auditors while they are doing an audit report.

In the year 1850, three brothers Henry, Emmanuel and Mayer Lehman founded the Lehman's

company. This company rose to become among the most significant investment companies in the

United States of America (USA) with over 25,000 employees across the world. Unfortunately,

the company closed down in the year 2008 due to bankruptcy, causing a global financial crisis.

This filing was the most talked about in history compared to other companies that filed for

bankruptcy before Lehman. At the time of filing, the company had $619 billion in debts and

$639 billion in total assets. The collapse of Lehman was a huge blow to global markets because

it contributed to a loss of close to $10 trillion in market capitalization (Wiggins, Piontek, and

Metrick, 2019)

Being a major player not only In the Us but also across the globe, its collapse affected the global

financial markets as well as the US government. What triggered the fall of the Lehman brothers

was losses in the mortgage, dramatic increase in mortgage defaults and severe tightening

liquidity (Fitzpatrick and Thomson, 2016).

Ernst & young accountancy firm was criticized for contributing to the fall of Lehman by failing

to point out a financial misstatement found in the entities financial statement. Ernst & young was

not the first auditing firm to be implicated in an entities failure. Andersen was also implicated in

the WorldCom bank case. This called for the need to revise the regulations governing auditors to

ensure they are guided by regulations in their line of work. ISA 701clearly outline the

responsibilities of auditors while they are doing an audit report.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

What is ISA 701

ISA 701 is a new international standard of auditing called Key audit matters (KAM). This

regulation is about the inclusion of key matters in the audit reports done by independent auditors

in an organization. This is one of the most significant changes in the auditing world because it

changes how the auditing reports are delivered. This move is meant to increase transparency and

accountability in auditing reports as well as assist the investors to clearly understand the audited

financial reports. The report should disclose confidential information that may cause a risk in

financial statements (Cordos and Fulop, 2015)

The Scope of ISA

According to Segal (2017), ISA has a responsibility of making sure auditors communicate

important issues in their reports for users to understand the financial statement prepared. When

these important matters are communicated, users can freely engage with those in leadership as

well as those charged with governance about issues that relate with financial statements of the

organization.

Evaluate the efficiency of reporting KAM

Below are the most frequently reported types of KAM

Goodwill and intangibles

Acquisitions and disposals

Exploration and evaluation assets

ISA 701 is a new international standard of auditing called Key audit matters (KAM). This

regulation is about the inclusion of key matters in the audit reports done by independent auditors

in an organization. This is one of the most significant changes in the auditing world because it

changes how the auditing reports are delivered. This move is meant to increase transparency and

accountability in auditing reports as well as assist the investors to clearly understand the audited

financial reports. The report should disclose confidential information that may cause a risk in

financial statements (Cordos and Fulop, 2015)

The Scope of ISA

According to Segal (2017), ISA has a responsibility of making sure auditors communicate

important issues in their reports for users to understand the financial statement prepared. When

these important matters are communicated, users can freely engage with those in leadership as

well as those charged with governance about issues that relate with financial statements of the

organization.

Evaluate the efficiency of reporting KAM

Below are the most frequently reported types of KAM

Goodwill and intangibles

Acquisitions and disposals

Exploration and evaluation assets

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Noncurrent assets

Revenue and going concern

Most auditing firms use a risk-based approach whereby main areas of risk in the firms are

identified and evaluated on how they may affect the annual financial report. The identified risks

are categorized as key audit matters (KAM).

ISA 701:8 define key audit matters as matters that are significant in the audit of the

organization's financial statements. The inclusion of KAM in audit reports is aimed at closing the

information gaps in firms by ensuring every concerned party understands what is written in the

report (Segal, 2017)

Determining the key matters in auditing

These matters should be determined by following;

Identification of risks in areas of material misstatement and other risks that are significant,

according to ISA 315. The assessment of these risks should be done through an understanding of

the organization and the environment of the organization.

Auditor judgments, especially on areas in financial statements that significant management

judgment was involved that include areas in accounting where there is a huge estimation of

uncertainty. According to Adu-Gyamfi (2016)

Revenue and going concern

Most auditing firms use a risk-based approach whereby main areas of risk in the firms are

identified and evaluated on how they may affect the annual financial report. The identified risks

are categorized as key audit matters (KAM).

ISA 701:8 define key audit matters as matters that are significant in the audit of the

organization's financial statements. The inclusion of KAM in audit reports is aimed at closing the

information gaps in firms by ensuring every concerned party understands what is written in the

report (Segal, 2017)

Determining the key matters in auditing

These matters should be determined by following;

Identification of risks in areas of material misstatement and other risks that are significant,

according to ISA 315. The assessment of these risks should be done through an understanding of

the organization and the environment of the organization.

Auditor judgments, especially on areas in financial statements that significant management

judgment was involved that include areas in accounting where there is a huge estimation of

uncertainty. According to Adu-Gyamfi (2016)

The effects of transactions in the audit report as well as other related events that occurred during

the period of the audit. Every crucial matter identified in the report must include references to

related disclosures in the organization's financial statements and describe well. There should also

be an explanation of how and why the listed key matters qualify as crucial in the audit report to

make it a KAM. There should also be a description of how the matter was addressed in the

report.

While writing the key audit matters in the report, the users of the report should be put in mind by

considering their understanding of KAM and their knowledge about the same. The objective of

the KAM in the report must also be relevant and insightful. There should be a timely engagement

with those charged with governance (TCWG) to allow them to consider how the KAM may be

addressed in the disclosures or elsewhere in the annual report (Gimbar, Hansen, and Ozlanski,

2015)

Auditors must be able to give feedback to the team that engaged in the filing of the report as they

clearly outline matters that must be communicated to those charged with governance on time to

ensure they are updated on the findings for them to verify if the matters listed qualify as key

matters KAM. Auditors should put in mind that relaying such information is not a personal

opinion of any individual neither is it separate in the financial statement being prepared. All this

require the input of the management for the report to be complete and for it to have a fair

presentation. The crucial matters addressed in the report must relate with the work done and

supported by documentation (Endaya and Hanefah, 2016)

the period of the audit. Every crucial matter identified in the report must include references to

related disclosures in the organization's financial statements and describe well. There should also

be an explanation of how and why the listed key matters qualify as crucial in the audit report to

make it a KAM. There should also be a description of how the matter was addressed in the

report.

While writing the key audit matters in the report, the users of the report should be put in mind by

considering their understanding of KAM and their knowledge about the same. The objective of

the KAM in the report must also be relevant and insightful. There should be a timely engagement

with those charged with governance (TCWG) to allow them to consider how the KAM may be

addressed in the disclosures or elsewhere in the annual report (Gimbar, Hansen, and Ozlanski,

2015)

Auditors must be able to give feedback to the team that engaged in the filing of the report as they

clearly outline matters that must be communicated to those charged with governance on time to

ensure they are updated on the findings for them to verify if the matters listed qualify as key

matters KAM. Auditors should put in mind that relaying such information is not a personal

opinion of any individual neither is it separate in the financial statement being prepared. All this

require the input of the management for the report to be complete and for it to have a fair

presentation. The crucial matters addressed in the report must relate with the work done and

supported by documentation (Endaya and Hanefah, 2016)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

According to Alzeban and Sawan (2015), the auditor has a responsibility to choose and

determine which matters qualify as crucial in the report for them to be listed as key audit matters

(KAM)the auditor has a task to determine which of the matters communicated qualify as key

audit matters (KAM).

The size of the organization, its nature and its complexity is the deciding factor of how many key

audit matters will be included in the report. Key matters that were Identified and listed in the

previous year report could be listed again in the current year if circumstances remain unchanged.

The auditor has also a right to interview and consult people outside the organization and within

the organization in relation to matters that are significant and could pass for key audit matters

and be included in the report.

Matters that have been identified as a risk and linked to fraud don’t necessarily mean they

automatically become key audit matters, issues that are identified as significant risks might not

be included in the report as KAM. According to the proposed ISA 260, auditors are required to

communicate effectively with those charged with governance about his views on the

organization accounting practices like estimates, organizational polices and financial statement

disclosures because these areas can be identified as risks and considered as key audit matters.

The auditor must communicate everything with those charged with governance as outlined in the

proposed ISA 260 paragraph two.

In the event where the auditor has problems or is finding it difficult to obtain information from

the organization, he should immediately report the defiance to those charged with governance for

him to get the information needed to complete the report. Party transactions that limit the auditor

determine which matters qualify as crucial in the report for them to be listed as key audit matters

(KAM)the auditor has a task to determine which of the matters communicated qualify as key

audit matters (KAM).

The size of the organization, its nature and its complexity is the deciding factor of how many key

audit matters will be included in the report. Key matters that were Identified and listed in the

previous year report could be listed again in the current year if circumstances remain unchanged.

The auditor has also a right to interview and consult people outside the organization and within

the organization in relation to matters that are significant and could pass for key audit matters

and be included in the report.

Matters that have been identified as a risk and linked to fraud don’t necessarily mean they

automatically become key audit matters, issues that are identified as significant risks might not

be included in the report as KAM. According to the proposed ISA 260, auditors are required to

communicate effectively with those charged with governance about his views on the

organization accounting practices like estimates, organizational polices and financial statement

disclosures because these areas can be identified as risks and considered as key audit matters.

The auditor must communicate everything with those charged with governance as outlined in the

proposed ISA 260 paragraph two.

In the event where the auditor has problems or is finding it difficult to obtain information from

the organization, he should immediately report the defiance to those charged with governance for

him to get the information needed to complete the report. Party transactions that limit the auditor

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

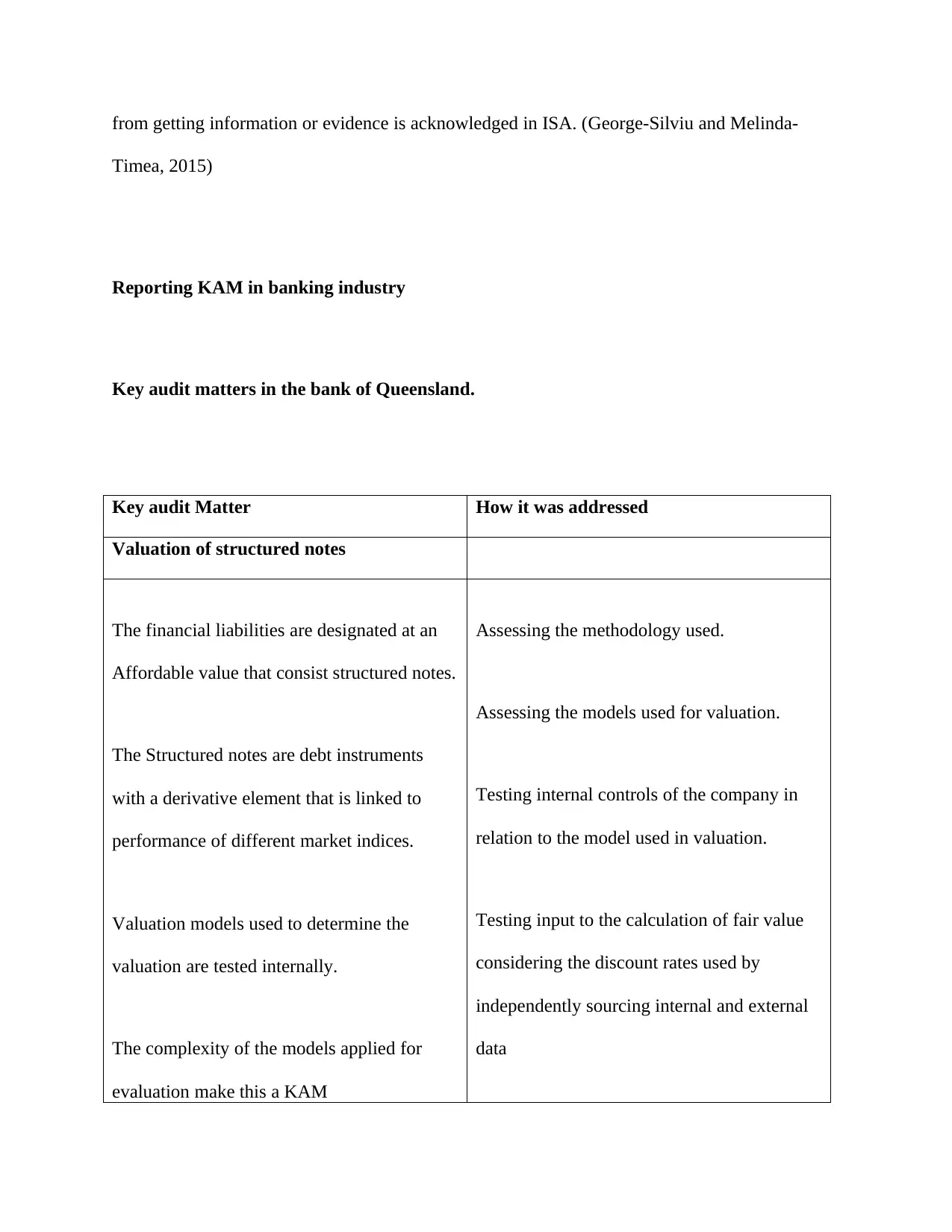

from getting information or evidence is acknowledged in ISA. (George-Silviu and Melinda-

Timea, 2015)

Reporting KAM in banking industry

Key audit matters in the bank of Queensland.

Key audit Matter How it was addressed

Valuation of structured notes

The financial liabilities are designated at an

Affordable value that consist structured notes.

The Structured notes are debt instruments

with a derivative element that is linked to

performance of different market indices.

Valuation models used to determine the

valuation are tested internally.

The complexity of the models applied for

evaluation make this a KAM

Assessing the methodology used.

Assessing the models used for valuation.

Testing internal controls of the company in

relation to the model used in valuation.

Testing input to the calculation of fair value

considering the discount rates used by

independently sourcing internal and external

data

Timea, 2015)

Reporting KAM in banking industry

Key audit matters in the bank of Queensland.

Key audit Matter How it was addressed

Valuation of structured notes

The financial liabilities are designated at an

Affordable value that consist structured notes.

The Structured notes are debt instruments

with a derivative element that is linked to

performance of different market indices.

Valuation models used to determine the

valuation are tested internally.

The complexity of the models applied for

evaluation make this a KAM

Assessing the methodology used.

Assessing the models used for valuation.

Testing internal controls of the company in

relation to the model used in valuation.

Testing input to the calculation of fair value

considering the discount rates used by

independently sourcing internal and external

data

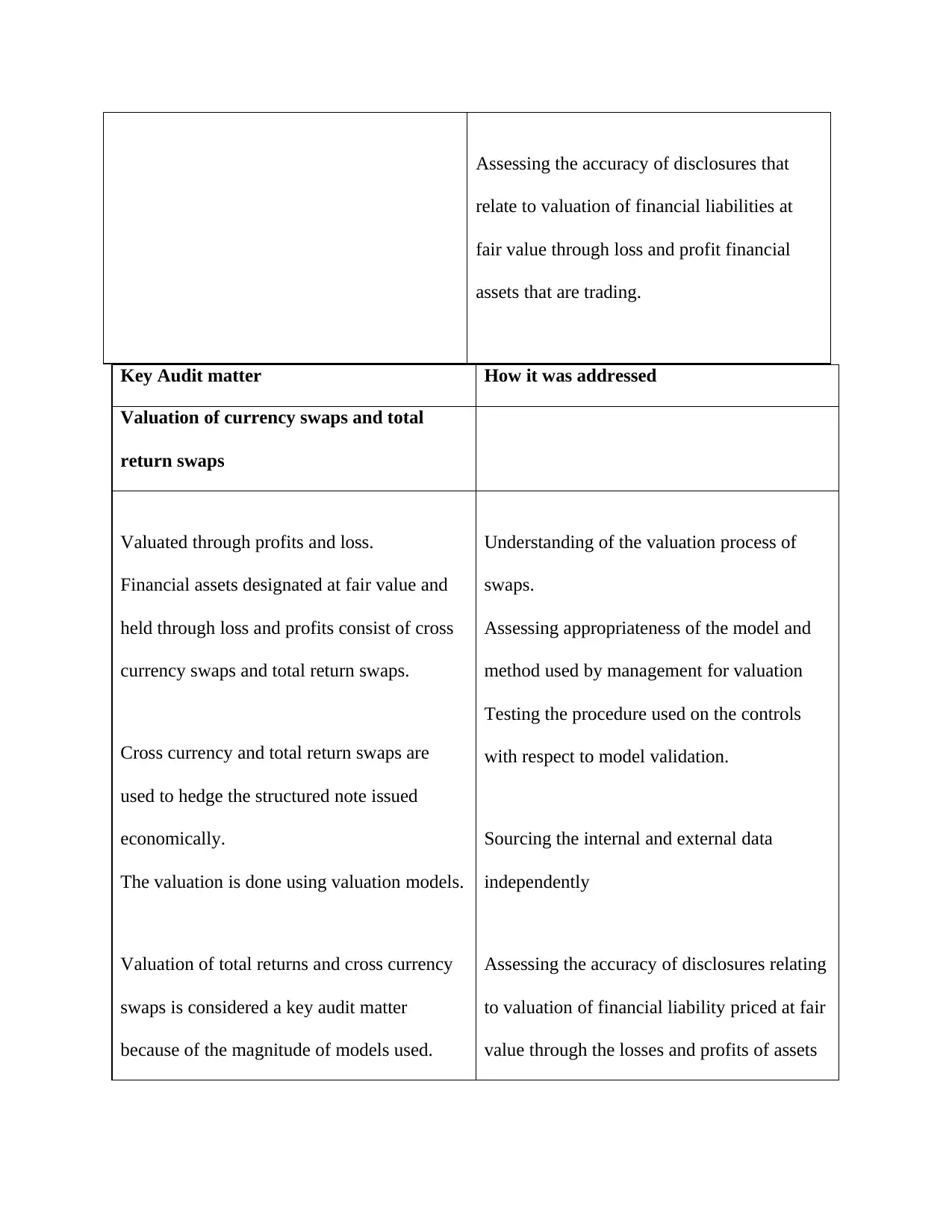

Assessing the accuracy of disclosures that

relate to valuation of financial liabilities at

fair value through loss and profit financial

assets that are trading.

Key Audit matter How it was addressed

Valuation of currency swaps and total

return swaps

Valuated through profits and loss.

Financial assets designated at fair value and

held through loss and profits consist of cross

currency swaps and total return swaps.

Cross currency and total return swaps are

used to hedge the structured note issued

economically.

The valuation is done using valuation models.

Valuation of total returns and cross currency

swaps is considered a key audit matter

because of the magnitude of models used.

Understanding of the valuation process of

swaps.

Assessing appropriateness of the model and

method used by management for valuation

Testing the procedure used on the controls

with respect to model validation.

Sourcing the internal and external data

independently

Assessing the accuracy of disclosures relating

to valuation of financial liability priced at fair

value through the losses and profits of assets

relate to valuation of financial liabilities at

fair value through loss and profit financial

assets that are trading.

Key Audit matter How it was addressed

Valuation of currency swaps and total

return swaps

Valuated through profits and loss.

Financial assets designated at fair value and

held through loss and profits consist of cross

currency swaps and total return swaps.

Cross currency and total return swaps are

used to hedge the structured note issued

economically.

The valuation is done using valuation models.

Valuation of total returns and cross currency

swaps is considered a key audit matter

because of the magnitude of models used.

Understanding of the valuation process of

swaps.

Assessing appropriateness of the model and

method used by management for valuation

Testing the procedure used on the controls

with respect to model validation.

Sourcing the internal and external data

independently

Assessing the accuracy of disclosures relating

to valuation of financial liability priced at fair

value through the losses and profits of assets

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

held.

Benefits of implementing KAM

With many companies implementing the ISA 701, there are different reactions from the

stakeholders concerning the communication of key matters in independent audit reports. Those

who support KAM argue that they make the report easy to understand as auditors don’t leave

communication of crucial issues hanging or difficult to understand. The auditors are able to

define risks in entities while focusing their attention on important matters. Users’ attention is

directed to certain areas of the report related to financial statements. Auditors are encouraged to

highlight crucial issues in the entity and to give an indication of the outcome of the audit

procedure. Disclosing key matters in reports help improve the market response to entities. The

quality of the work done by auditors is also improved since auditors are accountable for the

matters included as KAM therefore they put a lot of effort in their work while determining ad

analysing key audit matters (Gani, Wijeweera, and Eddie, 2017)

Those who have not embrace the inclusion of KAM in audit reports argue that communicating or

disclosure of key audit matters in the reports can lead to confusion if the matters communicated

Benefits of implementing KAM

With many companies implementing the ISA 701, there are different reactions from the

stakeholders concerning the communication of key matters in independent audit reports. Those

who support KAM argue that they make the report easy to understand as auditors don’t leave

communication of crucial issues hanging or difficult to understand. The auditors are able to

define risks in entities while focusing their attention on important matters. Users’ attention is

directed to certain areas of the report related to financial statements. Auditors are encouraged to

highlight crucial issues in the entity and to give an indication of the outcome of the audit

procedure. Disclosing key matters in reports help improve the market response to entities. The

quality of the work done by auditors is also improved since auditors are accountable for the

matters included as KAM therefore they put a lot of effort in their work while determining ad

analysing key audit matters (Gani, Wijeweera, and Eddie, 2017)

Those who have not embrace the inclusion of KAM in audit reports argue that communicating or

disclosure of key audit matters in the reports can lead to confusion if the matters communicated

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

are misunderstood by the user. They also insist that the auditors unmodified opinion concluding

lack of material misstatement is not needed.

Key Audit Matters and the Auditors opinion

According Dodo, (2017) Issues that require the auditor to give an unmodified opinion are by

nature crucial or important and thus qualify to be key audit matters. When an auditor gives a

qualified opinion, a discussion of any other KAM will still be relevant to help the users to

understand the audit report. According to ISA 705, an auditor is not allowed to communicate

Key audit matters when he disclaims an opinion on the financial statements.

Auditing is risk based since it focuses on sensitive matters in misstatement that include

significant risks and areas of complexity. These areas affect the allocation of resources, extend of

the audit effort in relation to involvement of entity executives. While determining key matters,

the auditor might be required to outsource information by engaging people outside the entity. In

some cases, it may be necessary to also involve expertise in auditing or accounting employed or

engaged by the firm to address the key audit matters

Article 13 of the ISA 200 gives requirements for the engagement partner relating to having

appropriate consultation on significant issues. The engagement partner has to discuss with the

engagement quality control reviewer significant issues arising during the audit engagement.

Matters that require consultation should be discussed with the engagement quality control

reviewer.

Going concern

lack of material misstatement is not needed.

Key Audit Matters and the Auditors opinion

According Dodo, (2017) Issues that require the auditor to give an unmodified opinion are by

nature crucial or important and thus qualify to be key audit matters. When an auditor gives a

qualified opinion, a discussion of any other KAM will still be relevant to help the users to

understand the audit report. According to ISA 705, an auditor is not allowed to communicate

Key audit matters when he disclaims an opinion on the financial statements.

Auditing is risk based since it focuses on sensitive matters in misstatement that include

significant risks and areas of complexity. These areas affect the allocation of resources, extend of

the audit effort in relation to involvement of entity executives. While determining key matters,

the auditor might be required to outsource information by engaging people outside the entity. In

some cases, it may be necessary to also involve expertise in auditing or accounting employed or

engaged by the firm to address the key audit matters

Article 13 of the ISA 200 gives requirements for the engagement partner relating to having

appropriate consultation on significant issues. The engagement partner has to discuss with the

engagement quality control reviewer significant issues arising during the audit engagement.

Matters that require consultation should be discussed with the engagement quality control

reviewer.

Going concern

Auditing standards allow an auditor to report about the going concern as a key audit matter in his

report. This applies when the going concern basis has been used inappropriately or when

applicable. Appropriate Disclosures about material uncertainty are not included in financial

statements of entities especially if the material uncertainty relates to circumstances that may cast

doubt on the ability of the entity to continue as a going concern.

Material uncertainty that has been disclosed in the financial report should be reported separately

as material uncertainty related to going concern. There is a new requirement in the auditing

standards for any identified condition or event that could cast doubt on the ability of the entity to

continue as a growing concern without the existence of uncertainty (Bedard et al., 2016)

Conclusion

New audit standard ISA 701 that has been introduced in auditor's reports communicates

crucial/essential matters that are most significant in audit reports. Important matters that are

termed to be most significant should be analysed and evaluated to determine whether they pass

to be key matters or not. It is the responsibility of the auditor to decide which of the

communicated matters by those charged with governance are key matters. Since the introduction

of this new auditing standard ISA701, many entities have embraced the inclusion of key matters

in their reports with few still objecting with varied reasons. The auditing act has laid down rules

and responsibilities that should be carried out while writing the audit report. These

responsibilities include identifying the risk of misstatement in the financial reports, liaising with

parties concerned to get information, making an unmodified opinion among other

responsibilities. For integrity to be upheld, critical issues in entities must be addressed and those

report. This applies when the going concern basis has been used inappropriately or when

applicable. Appropriate Disclosures about material uncertainty are not included in financial

statements of entities especially if the material uncertainty relates to circumstances that may cast

doubt on the ability of the entity to continue as a going concern.

Material uncertainty that has been disclosed in the financial report should be reported separately

as material uncertainty related to going concern. There is a new requirement in the auditing

standards for any identified condition or event that could cast doubt on the ability of the entity to

continue as a growing concern without the existence of uncertainty (Bedard et al., 2016)

Conclusion

New audit standard ISA 701 that has been introduced in auditor's reports communicates

crucial/essential matters that are most significant in audit reports. Important matters that are

termed to be most significant should be analysed and evaluated to determine whether they pass

to be key matters or not. It is the responsibility of the auditor to decide which of the

communicated matters by those charged with governance are key matters. Since the introduction

of this new auditing standard ISA701, many entities have embraced the inclusion of key matters

in their reports with few still objecting with varied reasons. The auditing act has laid down rules

and responsibilities that should be carried out while writing the audit report. These

responsibilities include identifying the risk of misstatement in the financial reports, liaising with

parties concerned to get information, making an unmodified opinion among other

responsibilities. For integrity to be upheld, critical issues in entities must be addressed and those

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.