Banking System Analysis: India and New Zealand, FINC123, Semester 2

VerifiedAdded on 2023/06/07

|24

|5972

|65

Report

AI Summary

This report provides a comprehensive comparison of the banking systems in India and New Zealand. It begins with an executive summary, followed by an introduction to banking and its significance in economic growth. The report then compares the legal frameworks, regulatory authorities, and liquidity standards of both countries, highlighting the roles of the Reserve Bank of India and the Reserve Bank of New Zealand. A qualitative and quantitative analysis is conducted on ICICI Bank and ANZ Bank, examining their services, customer relationship management, and financial data from the perspective of a depositor. The analysis includes a discussion of strengths, weaknesses, opportunities, and threats to the banks in both countries, as well as a detailed look at their products and services. The report concludes with a summary of the key findings and references to the sources used.

Running head: A REPORT ON BANKING SYSTEM

A Report on Banking System

Name of the Student:

Name of the University:

Author Note:

A Report on Banking System

Name of the Student:

Name of the University:

Author Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1A REPORT ON BANKING SYSTEM

Executive Summary:

Banking sector is the most important element of the monetary system and it plays the essential

role in the growth and of an economy. The report is being designed to briefly discuss the banking

system. In this report comparison between the Indian Banking and New Zealand Banking system

is done on the basis of its regulatory body and other criteria. To conclude a clear picture on the

banking system of two countries the two leading banks of both the countries are taken for a

qualitative and quantitative analysis. The analysis is done on the financial data and on its

business.

Introduction:

Banking started at ancient times, when model type merchants use to give loans to the

framers and to the exporters who carried the products to different cities. This event was named as

barter system. The beginning of contemporary banking started from the medieval times. In the

17th century banking notes were emerged. In the traditional sense banking means a trend of

taking deposits of money from the citizen. These deposits are used as lending and investment by

the banks for the growth of economy. These deposits are done according to the distinct and

appropriate features of withdrawable by a slip called cheque. This is a unique system that no

other financial institution offers. An economy reflects the minor mirror of banking.( Acharya et

al. 2013). It is the most essential component of the world for its growth in the economy. The key

of success is banking for any country moving towards development. Bank and economy is

unified to each other. Banks are the important financial institution as they support economy in

creating and channelizing the flow of money. Banking is the helping hand for the citizen who are

Executive Summary:

Banking sector is the most important element of the monetary system and it plays the essential

role in the growth and of an economy. The report is being designed to briefly discuss the banking

system. In this report comparison between the Indian Banking and New Zealand Banking system

is done on the basis of its regulatory body and other criteria. To conclude a clear picture on the

banking system of two countries the two leading banks of both the countries are taken for a

qualitative and quantitative analysis. The analysis is done on the financial data and on its

business.

Introduction:

Banking started at ancient times, when model type merchants use to give loans to the

framers and to the exporters who carried the products to different cities. This event was named as

barter system. The beginning of contemporary banking started from the medieval times. In the

17th century banking notes were emerged. In the traditional sense banking means a trend of

taking deposits of money from the citizen. These deposits are used as lending and investment by

the banks for the growth of economy. These deposits are done according to the distinct and

appropriate features of withdrawable by a slip called cheque. This is a unique system that no

other financial institution offers. An economy reflects the minor mirror of banking.( Acharya et

al. 2013). It is the most essential component of the world for its growth in the economy. The key

of success is banking for any country moving towards development. Bank and economy is

unified to each other. Banks are the important financial institution as they support economy in

creating and channelizing the flow of money. Banking is the helping hand for the citizen who are

2A REPORT ON BANKING SYSTEM

depositors for banks to secure their money. The deposited money acts as a supply chain of

capital for the citizens establishing business in the economy and enhancing employment. Banks

are regulated worldwide.

In the nation to get it support and make stability in the monetary institution there is

banking structure nationally and internationally. The monetary institution that supports the

economy in being stabilized now days. In the globe of banking and investment nothi ng

stands still. The chief revolutionize of everyone is in the, range of the trade of banking.

Banking in its customary form is concerned with the approval of money deposited by the citizen

in their respective accounts, as deposits are lender to seekers. Apart from customary trade, banks

in today`s time offer a ample series of services to p l e a s e t h e c u s t o m e r s ’ n e e d s t h o u g h

t h e n e e d i t b e m o n e t a r y o r n o n - m o n e t a r y . The series of military accessible depends

on bank type and size. (Lee and Choi 2013).

Discussion:

Comparison between the Indian and New Zealand Banking System

Indian Banking System

Legal Framework:

Business related to banking and fiscal services are monitored by the Banking Regulation Act

1949. The act gives power to Reserve Bank of India regarding the issues of regulations,

guidelines, rules and direction on a broad variety of problems related to monetary and banking

sector. RBI is the primary and central bank of India.

depositors for banks to secure their money. The deposited money acts as a supply chain of

capital for the citizens establishing business in the economy and enhancing employment. Banks

are regulated worldwide.

In the nation to get it support and make stability in the monetary institution there is

banking structure nationally and internationally. The monetary institution that supports the

economy in being stabilized now days. In the globe of banking and investment nothi ng

stands still. The chief revolutionize of everyone is in the, range of the trade of banking.

Banking in its customary form is concerned with the approval of money deposited by the citizen

in their respective accounts, as deposits are lender to seekers. Apart from customary trade, banks

in today`s time offer a ample series of services to p l e a s e t h e c u s t o m e r s ’ n e e d s t h o u g h

t h e n e e d i t b e m o n e t a r y o r n o n - m o n e t a r y . The series of military accessible depends

on bank type and size. (Lee and Choi 2013).

Discussion:

Comparison between the Indian and New Zealand Banking System

Indian Banking System

Legal Framework:

Business related to banking and fiscal services are monitored by the Banking Regulation Act

1949. The act gives power to Reserve Bank of India regarding the issues of regulations,

guidelines, rules and direction on a broad variety of problems related to monetary and banking

sector. RBI is the primary and central bank of India.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3A REPORT ON BANKING SYSTEM

Regulatory authorities

Regulatory authority sets norms, give license and guidelines for banks even for those branches

that are out of India. They even set norms for the products and services given by the bank. They

also look after the debt management for the government and currencies are also managed by the

authority.

Other authorities

There sub divisions for regulating the different monetary sector in India. These are:

Insolvency and Bankruptcy Board of India (IBBI) that regulates the development

connecting to conduct bankruptcy procedures under the Insolvency and Bankruptcy Code

(IBC).

Securities Exchange Board of India (SEBI) that is the regulatory power for the securities

market in India.

Insurance Regulatory and Development Authority of India (IRDAI) that regulates the

insurance sector.

Others

The Ministry of Finance deals in legislating and supervising upon the functions of banks and

financial institutions. Acting all the way through its Department of Financial Services, it:

Monitoring the operations that is related in banking.

Lay down the guidelines of sound operating system and functions of public sector banks.

Regulatory authorities

Regulatory authority sets norms, give license and guidelines for banks even for those branches

that are out of India. They even set norms for the products and services given by the bank. They

also look after the debt management for the government and currencies are also managed by the

authority.

Other authorities

There sub divisions for regulating the different monetary sector in India. These are:

Insolvency and Bankruptcy Board of India (IBBI) that regulates the development

connecting to conduct bankruptcy procedures under the Insolvency and Bankruptcy Code

(IBC).

Securities Exchange Board of India (SEBI) that is the regulatory power for the securities

market in India.

Insurance Regulatory and Development Authority of India (IRDAI) that regulates the

insurance sector.

Others

The Ministry of Finance deals in legislating and supervising upon the functions of banks and

financial institutions. Acting all the way through its Department of Financial Services, it:

Monitoring the operations that is related in banking.

Lay down the guidelines of sound operating system and functions of public sector banks.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4A REPORT ON BANKING SYSTEM

Liquidity and capital adequacy

Role of international standards

It is mandatory from April 2013 to implement Basel III capital regulations. This is to ensure

sound transactions to meet the minimum requirement of Basel III capital ratios. The RBI has

previously unconfined guidelines on preservation and calculation of liquidity ratio, the RBI has

in recent times issued strategy on Net Stable Funding Ratio (NSFR) which is based on

concluding rules on NSFR available by the Basel Committee. The NSFR should be equivalent to

at least 100% on a continuing basis. Though, the NSFR would be supplemented by decision-

making appraisal of the steady financial support and liquidity risk figure of a bank. On the basis

of such assessment, the RBI may require a person bank to accept more rigorous standards. The

obligation to preserve 100% NSFR would be compulsory on banks with effect from a date which

will be communicated by the RBI in due route.

Main liquidity

The cash reserve ratio (CRR) is utmost important for every bank to maintain with RBI. It is

average day to day balance that every bank maintains as a part of the total demand and time

liabilities deposits (NDTL). Current rate is 4% the statutory liquidity ratio (SLR) is also

important for every bank to maintain in order to safeguard itself from the crisis impact. It should

also maintain liquid assets in way of gold, cash and government securities. SLR rate is 19.5% at

present.

Liquidity and capital adequacy

Role of international standards

It is mandatory from April 2013 to implement Basel III capital regulations. This is to ensure

sound transactions to meet the minimum requirement of Basel III capital ratios. The RBI has

previously unconfined guidelines on preservation and calculation of liquidity ratio, the RBI has

in recent times issued strategy on Net Stable Funding Ratio (NSFR) which is based on

concluding rules on NSFR available by the Basel Committee. The NSFR should be equivalent to

at least 100% on a continuing basis. Though, the NSFR would be supplemented by decision-

making appraisal of the steady financial support and liquidity risk figure of a bank. On the basis

of such assessment, the RBI may require a person bank to accept more rigorous standards. The

obligation to preserve 100% NSFR would be compulsory on banks with effect from a date which

will be communicated by the RBI in due route.

Main liquidity

The cash reserve ratio (CRR) is utmost important for every bank to maintain with RBI. It is

average day to day balance that every bank maintains as a part of the total demand and time

liabilities deposits (NDTL). Current rate is 4% the statutory liquidity ratio (SLR) is also

important for every bank to maintain in order to safeguard itself from the crisis impact. It should

also maintain liquid assets in way of gold, cash and government securities. SLR rate is 19.5% at

present.

5A REPORT ON BANKING SYSTEM

New Zealand Banking System

Legal framework

New Zealand has a two way approach towards banking regulations with a different prudential

and conduct regulator. The Reserve Bank of New Zealand Act 1989 (RBNZ Act) is the type

portion of legislation surroundings out the powers of Reserve Bank of New Zealand (RBNZ) as

New Zealand's canny regulator. The RBNZ Act regulates with bank registration and enables the

RBNZ to:

Lay conditions for process of registration

Outsourcing facts from the banks

Managing bank failure

The Financial Markets Conduct Act 2013 (FMCA) has the rules for conducting financial and in

fastidious of giving licensing for issuing derivatives, one who is operating in market and

different investment schemes managers.

Regulatory authorities

Lead bank regulators

Reserve Bank of New Zealand (RBNZ) is the primary regulators of banks in New Zealand that

got established by the Reserve Bank of New Zealand Act 1989. In New Zealand RBNZ act as a

canny regulator and regulates all aspects that come under the bank’s commerce. RBNZ does not

have a statutory objective to protect its depositors rather its statutory objective is managing

banking business. In New Zealand the Financial Market Authority (FMA) deals in all the

financial matters of the country. (Ball et al.2013).

New Zealand Banking System

Legal framework

New Zealand has a two way approach towards banking regulations with a different prudential

and conduct regulator. The Reserve Bank of New Zealand Act 1989 (RBNZ Act) is the type

portion of legislation surroundings out the powers of Reserve Bank of New Zealand (RBNZ) as

New Zealand's canny regulator. The RBNZ Act regulates with bank registration and enables the

RBNZ to:

Lay conditions for process of registration

Outsourcing facts from the banks

Managing bank failure

The Financial Markets Conduct Act 2013 (FMCA) has the rules for conducting financial and in

fastidious of giving licensing for issuing derivatives, one who is operating in market and

different investment schemes managers.

Regulatory authorities

Lead bank regulators

Reserve Bank of New Zealand (RBNZ) is the primary regulators of banks in New Zealand that

got established by the Reserve Bank of New Zealand Act 1989. In New Zealand RBNZ act as a

canny regulator and regulates all aspects that come under the bank’s commerce. RBNZ does not

have a statutory objective to protect its depositors rather its statutory objective is managing

banking business. In New Zealand the Financial Market Authority (FMA) deals in all the

financial matters of the country. (Ball et al.2013).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6A REPORT ON BANKING SYSTEM

Others

The council of Financial Regulators consists of:

Financial Markets Authority (FMA)

Ministry of Business, Innovation and Employment

New Zealand Treasury.

Reserve Bank of New Zealand (RBNZ).

Liquidity

Role of international standards

The Reserve Bank of New Zealand (RBNZ) has incorporated the major components of the Basel

Committee on Banking Supervision Basel III Capital Accords (Basel III) in New Zealand by

updating its capital adequacy and liquidity standards in the Banking Supervision Handbook to

replicate the Basel III necessities. Locally incorporated banks have been compulsory to comply

with the least amount capital ratios from January 2013. The capital conservation cushion came

into effect in New Zealand on January 2014, as did the Reserve Bank's power to locate a

countercyclical shock absorber.

Main liquidity

The Reserve Bank of New Zealand's (RBNZ) Liquidity Policy comprising BS13 and BS13A of

the Banking Supervision Handbook introduced in April 2010 in response to the global financial

crisis. The Liquidity Policy has four main apparatus:

Publicly disclosing the requirement of some information about liquidity risk and about

their management by the banks.

Standing orders on risk management.

Others

The council of Financial Regulators consists of:

Financial Markets Authority (FMA)

Ministry of Business, Innovation and Employment

New Zealand Treasury.

Reserve Bank of New Zealand (RBNZ).

Liquidity

Role of international standards

The Reserve Bank of New Zealand (RBNZ) has incorporated the major components of the Basel

Committee on Banking Supervision Basel III Capital Accords (Basel III) in New Zealand by

updating its capital adequacy and liquidity standards in the Banking Supervision Handbook to

replicate the Basel III necessities. Locally incorporated banks have been compulsory to comply

with the least amount capital ratios from January 2013. The capital conservation cushion came

into effect in New Zealand on January 2014, as did the Reserve Bank's power to locate a

countercyclical shock absorber.

Main liquidity

The Reserve Bank of New Zealand's (RBNZ) Liquidity Policy comprising BS13 and BS13A of

the Banking Supervision Handbook introduced in April 2010 in response to the global financial

crisis. The Liquidity Policy has four main apparatus:

Publicly disclosing the requirement of some information about liquidity risk and about

their management by the banks.

Standing orders on risk management.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7A REPORT ON BANKING SYSTEM

Regular updating of the liquidity position of the banks

Qualitative and Quantitative Analysis of ICICI Bank and ANZ bank of New Zealand:

Qualitative Analysis:

ANZ Bank:

In Australia ANZ is among the largest company who has attended the majority of hold in

international banking sector and monetary team. This is known amongst the big four banks of

Australia. In 1970 ANZ bank was established leading a merger with English, Scottish and

Australian Bank Limited (ES&A). After this merger Australia and New Zealand Banking Group

Limited was established. The team sustained to cultivate, regardless of the pay for the first and

foremost Indian-based Grind lays Bank, which submit an evidence of a not as much of ideal

commerce robust and the cluster deprived itself in year 1999. 16088 people were employees of

ANZ Bank and it had 807 branches in Australia by the end of 1999. In the year 1970 among the

lead the way banks of Australia it combined with the networks of SWIFT. The idea of electronic

services of banking started in 1997 but Internet banking was launched in April 1999.

Subsequently, it had a joint venture agreement with ERG and Telstra. This joint venture was

done to form a smart card association that followed an additional planned association with

E*Trade Australia. This association was to develop a foremost online stock market trading. From

the tactical perspective, it can be seen that ANZ has been taking a very practical move toward,

with cooperative ventures, association, and ventures into online banking for trading to linger

cutthroat. It has also incorporated its army, to tender the buyer a ‘one stop’ atmosphere.

Customer Relationship Management (CRM) -nearly everyone touted ready for action tool of

banks in attendance. At present, ANZ is contribution a variety of armed forces counting, account

Regular updating of the liquidity position of the banks

Qualitative and Quantitative Analysis of ICICI Bank and ANZ bank of New Zealand:

Qualitative Analysis:

ANZ Bank:

In Australia ANZ is among the largest company who has attended the majority of hold in

international banking sector and monetary team. This is known amongst the big four banks of

Australia. In 1970 ANZ bank was established leading a merger with English, Scottish and

Australian Bank Limited (ES&A). After this merger Australia and New Zealand Banking Group

Limited was established. The team sustained to cultivate, regardless of the pay for the first and

foremost Indian-based Grind lays Bank, which submit an evidence of a not as much of ideal

commerce robust and the cluster deprived itself in year 1999. 16088 people were employees of

ANZ Bank and it had 807 branches in Australia by the end of 1999. In the year 1970 among the

lead the way banks of Australia it combined with the networks of SWIFT. The idea of electronic

services of banking started in 1997 but Internet banking was launched in April 1999.

Subsequently, it had a joint venture agreement with ERG and Telstra. This joint venture was

done to form a smart card association that followed an additional planned association with

E*Trade Australia. This association was to develop a foremost online stock market trading. From

the tactical perspective, it can be seen that ANZ has been taking a very practical move toward,

with cooperative ventures, association, and ventures into online banking for trading to linger

cutthroat. It has also incorporated its army, to tender the buyer a ‘one stop’ atmosphere.

Customer Relationship Management (CRM) -nearly everyone touted ready for action tool of

banks in attendance. At present, ANZ is contribution a variety of armed forces counting, account

8A REPORT ON BANKING SYSTEM

administration, credit cards managing payments, payments of bills, trading shares, fund transfer

and investment administration. The reimburse anybody trait allows the client to shift finances to

the bank account of any individual with a participating fiscal organization. The bank was

performing upon buyer hassle to power. The result of internet banking is updated in the website

through monthly survey with a motive of improving and developing the new facilities. This has

helped the depositors to accept the internet based banking. The bank had achieved a great

success in transforming ATM, phone and branch customers to Internet form of banking. The

maximum exchange rate of 8.6 percent amongst its client is marked of achievement in internet

business by ANZ. (Adge et al. 2014).

ICICI Bank:

A clandestine assembly in India set ICICI bank under commercial banking head. In January 1994

it was registered and got the licensed by RBI for its operations. At the end of 1999, it had 64

branches at all over India that was featured by state of the art technology and systems.

Networking is done through V-SAT technology. At the end of the year 2000 it had more than

100 branches, 200 ATMs that were spread over the country. ICICI bank gives a wide variety of

banking services domestically and internationally. This done for facilitating the trade cross-

borders businesses and investment also the treasury and services provided in foreign exchanges.

ICICI bank was the first one to launch the Internet Banking named as Infinity. It also offer free

phone banking. The phone-banking offer services for transferring of funds, payments of bill and

payment of e-bills and e shopping. (Altman 2013).

Strategically, at the time when deregulation was at peak ICICI had a benefit of a first

mover advantage as it started it operations at the rising time of technologies that was lacking

administration, credit cards managing payments, payments of bills, trading shares, fund transfer

and investment administration. The reimburse anybody trait allows the client to shift finances to

the bank account of any individual with a participating fiscal organization. The bank was

performing upon buyer hassle to power. The result of internet banking is updated in the website

through monthly survey with a motive of improving and developing the new facilities. This has

helped the depositors to accept the internet based banking. The bank had achieved a great

success in transforming ATM, phone and branch customers to Internet form of banking. The

maximum exchange rate of 8.6 percent amongst its client is marked of achievement in internet

business by ANZ. (Adge et al. 2014).

ICICI Bank:

A clandestine assembly in India set ICICI bank under commercial banking head. In January 1994

it was registered and got the licensed by RBI for its operations. At the end of 1999, it had 64

branches at all over India that was featured by state of the art technology and systems.

Networking is done through V-SAT technology. At the end of the year 2000 it had more than

100 branches, 200 ATMs that were spread over the country. ICICI bank gives a wide variety of

banking services domestically and internationally. This done for facilitating the trade cross-

borders businesses and investment also the treasury and services provided in foreign exchanges.

ICICI bank was the first one to launch the Internet Banking named as Infinity. It also offer free

phone banking. The phone-banking offer services for transferring of funds, payments of bill and

payment of e-bills and e shopping. (Altman 2013).

Strategically, at the time when deregulation was at peak ICICI had a benefit of a first

mover advantage as it started it operations at the rising time of technologies that was lacking

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9A REPORT ON BANKING SYSTEM

with older banks. A tie- up was made with the technology providers such as software trainers

like NIIT, ISP Satyam Online and Compaq to spread it reach. These types of alliances are

growing more than 50% every year. (Ball et al. 2013). The expansion of its own share prices is

analytic of the organization’s success. Pay seal was launched in July 2000 that was a payment

gateway ensuring the safety and security for the transactions done. It interfaces along the web

merchant, banking system and internet shopper to facilitate online payments in a safe

environment. On September 22, 1999 subsidiary of ICICI got listed on the NYSE. ICICI was a

commercial bank who was first from India to be listed on NYSE and second Asian bank. Since it

was listed the share price was constant any movements was seen due to the effect of US

elections. The growth trend shows overall a good health. The bank target young professionals

who belonged to urban areas to maintain its tag line. It strategy was based on services that were

on demand like payments of bills loans- car, home, education, products for investment. ICICI

planned for branching out from getting support of professionals and being amalgamated with

other private sector banks for enabling its growth in the rural sector. The continuous momentum

of internet development is estimated to assist its expansion. However, strategically in spite of

regulations and issues regarding infrastructure it had been able to make profit on the path of

technical growth. For boosting its competitive benefit it gives offers in a wide variety in online

banking. ( Laudon and Laudon 2016).

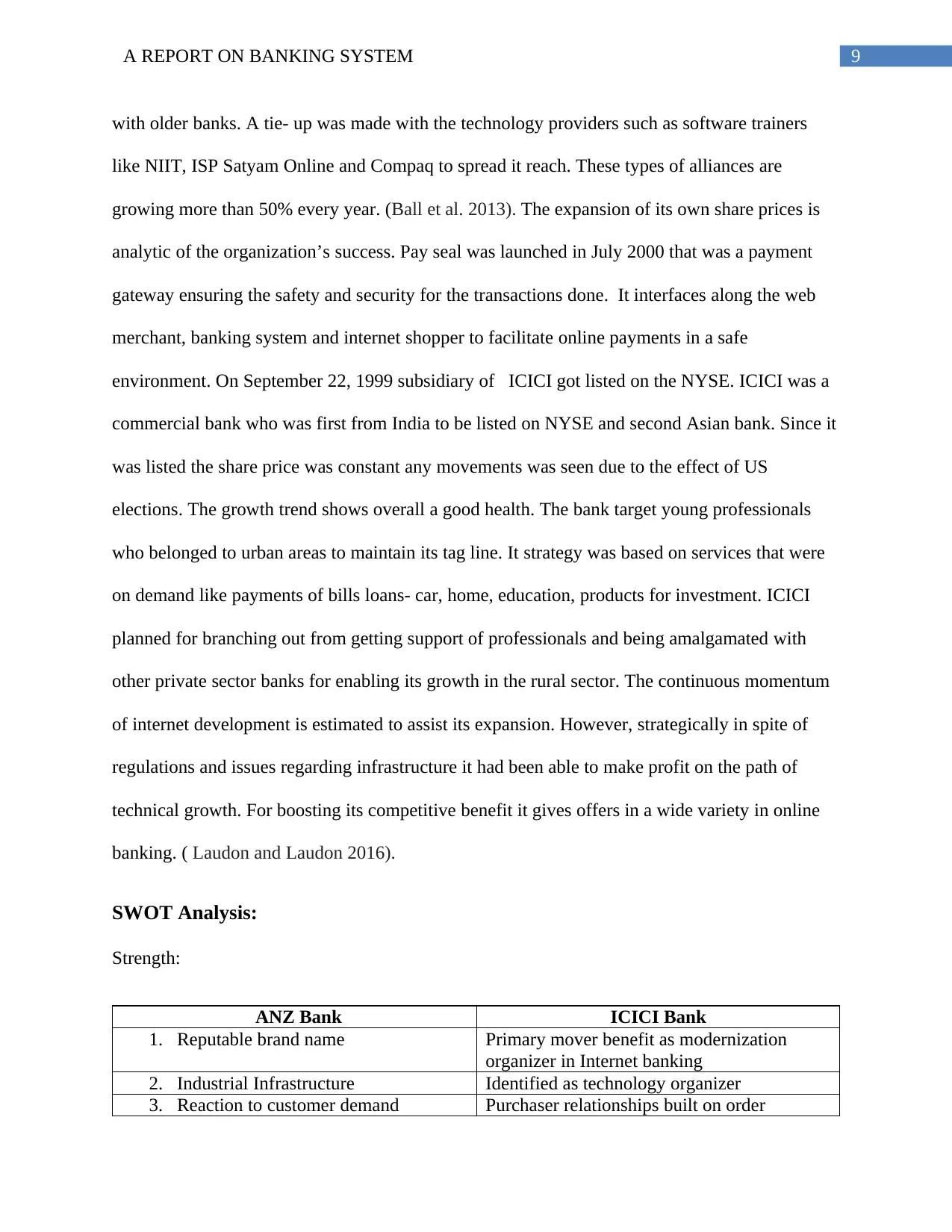

SWOT Analysis:

Strength:

ANZ Bank ICICI Bank

1. Reputable brand name Primary mover benefit as modernization

organizer in Internet banking

2. Industrial Infrastructure Identified as technology organizer

3. Reaction to customer demand Purchaser relationships built on order

with older banks. A tie- up was made with the technology providers such as software trainers

like NIIT, ISP Satyam Online and Compaq to spread it reach. These types of alliances are

growing more than 50% every year. (Ball et al. 2013). The expansion of its own share prices is

analytic of the organization’s success. Pay seal was launched in July 2000 that was a payment

gateway ensuring the safety and security for the transactions done. It interfaces along the web

merchant, banking system and internet shopper to facilitate online payments in a safe

environment. On September 22, 1999 subsidiary of ICICI got listed on the NYSE. ICICI was a

commercial bank who was first from India to be listed on NYSE and second Asian bank. Since it

was listed the share price was constant any movements was seen due to the effect of US

elections. The growth trend shows overall a good health. The bank target young professionals

who belonged to urban areas to maintain its tag line. It strategy was based on services that were

on demand like payments of bills loans- car, home, education, products for investment. ICICI

planned for branching out from getting support of professionals and being amalgamated with

other private sector banks for enabling its growth in the rural sector. The continuous momentum

of internet development is estimated to assist its expansion. However, strategically in spite of

regulations and issues regarding infrastructure it had been able to make profit on the path of

technical growth. For boosting its competitive benefit it gives offers in a wide variety in online

banking. ( Laudon and Laudon 2016).

SWOT Analysis:

Strength:

ANZ Bank ICICI Bank

1. Reputable brand name Primary mover benefit as modernization

organizer in Internet banking

2. Industrial Infrastructure Identified as technology organizer

3. Reaction to customer demand Purchaser relationships built on order

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10A REPORT ON BANKING SYSTEM

4. Growing customer adaptation rate of

internet banking

Online banking enlargement motivated by

buyer Perce

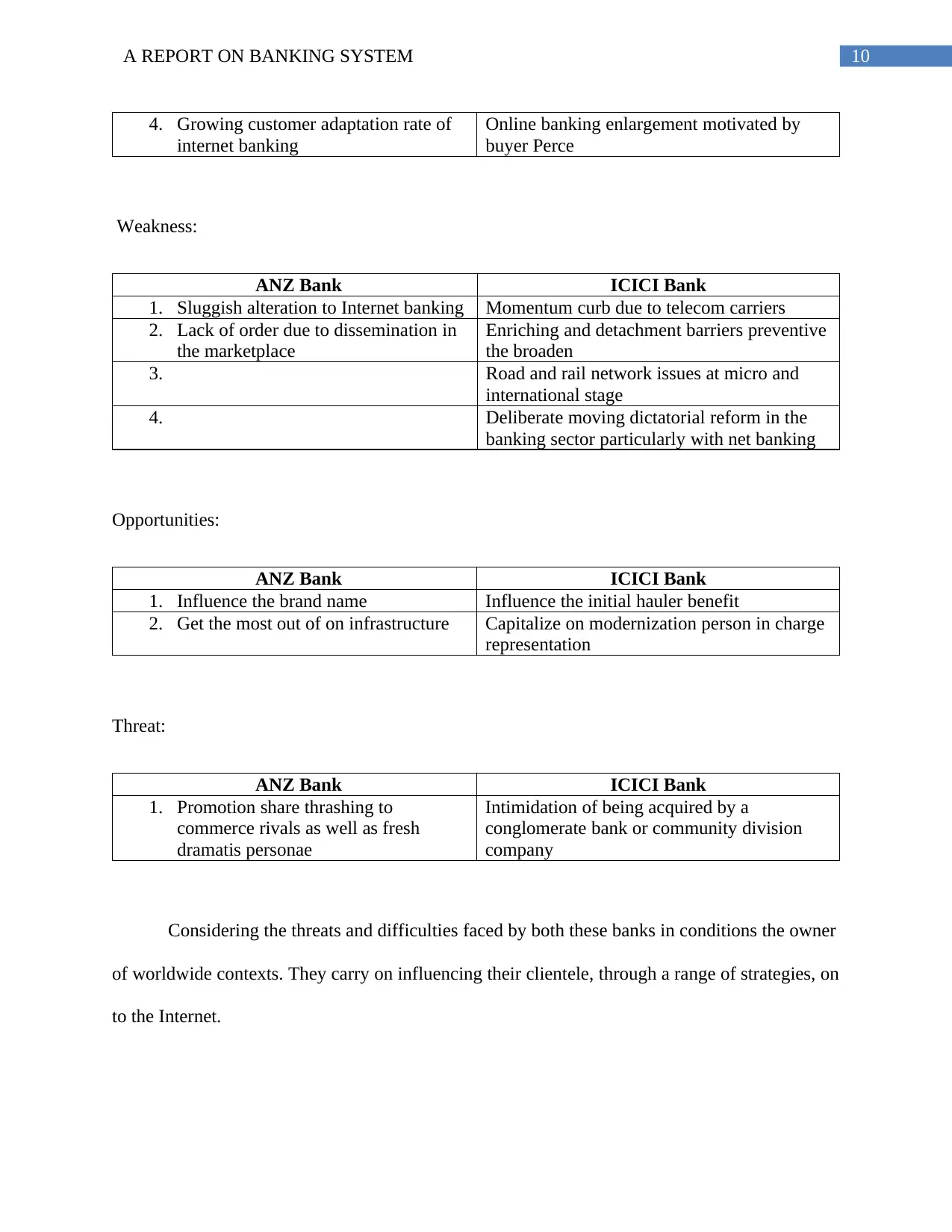

Weakness:

ANZ Bank ICICI Bank

1. Sluggish alteration to Internet banking Momentum curb due to telecom carriers

2. Lack of order due to dissemination in

the marketplace

Enriching and detachment barriers preventive

the broaden

3. Road and rail network issues at micro and

international stage

4. Deliberate moving dictatorial reform in the

banking sector particularly with net banking

Opportunities:

ANZ Bank ICICI Bank

1. Influence the brand name Influence the initial hauler benefit

2. Get the most out of on infrastructure Capitalize on modernization person in charge

representation

Threat:

ANZ Bank ICICI Bank

1. Promotion share thrashing to

commerce rivals as well as fresh

dramatis personae

Intimidation of being acquired by a

conglomerate bank or community division

company

Considering the threats and difficulties faced by both these banks in conditions the owner

of worldwide contexts. They carry on influencing their clientele, through a range of strategies, on

to the Internet.

4. Growing customer adaptation rate of

internet banking

Online banking enlargement motivated by

buyer Perce

Weakness:

ANZ Bank ICICI Bank

1. Sluggish alteration to Internet banking Momentum curb due to telecom carriers

2. Lack of order due to dissemination in

the marketplace

Enriching and detachment barriers preventive

the broaden

3. Road and rail network issues at micro and

international stage

4. Deliberate moving dictatorial reform in the

banking sector particularly with net banking

Opportunities:

ANZ Bank ICICI Bank

1. Influence the brand name Influence the initial hauler benefit

2. Get the most out of on infrastructure Capitalize on modernization person in charge

representation

Threat:

ANZ Bank ICICI Bank

1. Promotion share thrashing to

commerce rivals as well as fresh

dramatis personae

Intimidation of being acquired by a

conglomerate bank or community division

company

Considering the threats and difficulties faced by both these banks in conditions the owner

of worldwide contexts. They carry on influencing their clientele, through a range of strategies, on

to the Internet.

11A REPORT ON BANKING SYSTEM

As these banks are adapting internet banks and participating in their chain value in the internet

services that are helping them to cut down their transaction cost so that they can elevate their

picture as pioneer and innovative bankers. Acharya (2013) states that attractive the principal

agent role in banking delivers one’s participants with the chance to trail, with an improved-

intended or more urbane service. There is rising request for operational banking services, as the

involvements of these two innovator administrations have revealed.

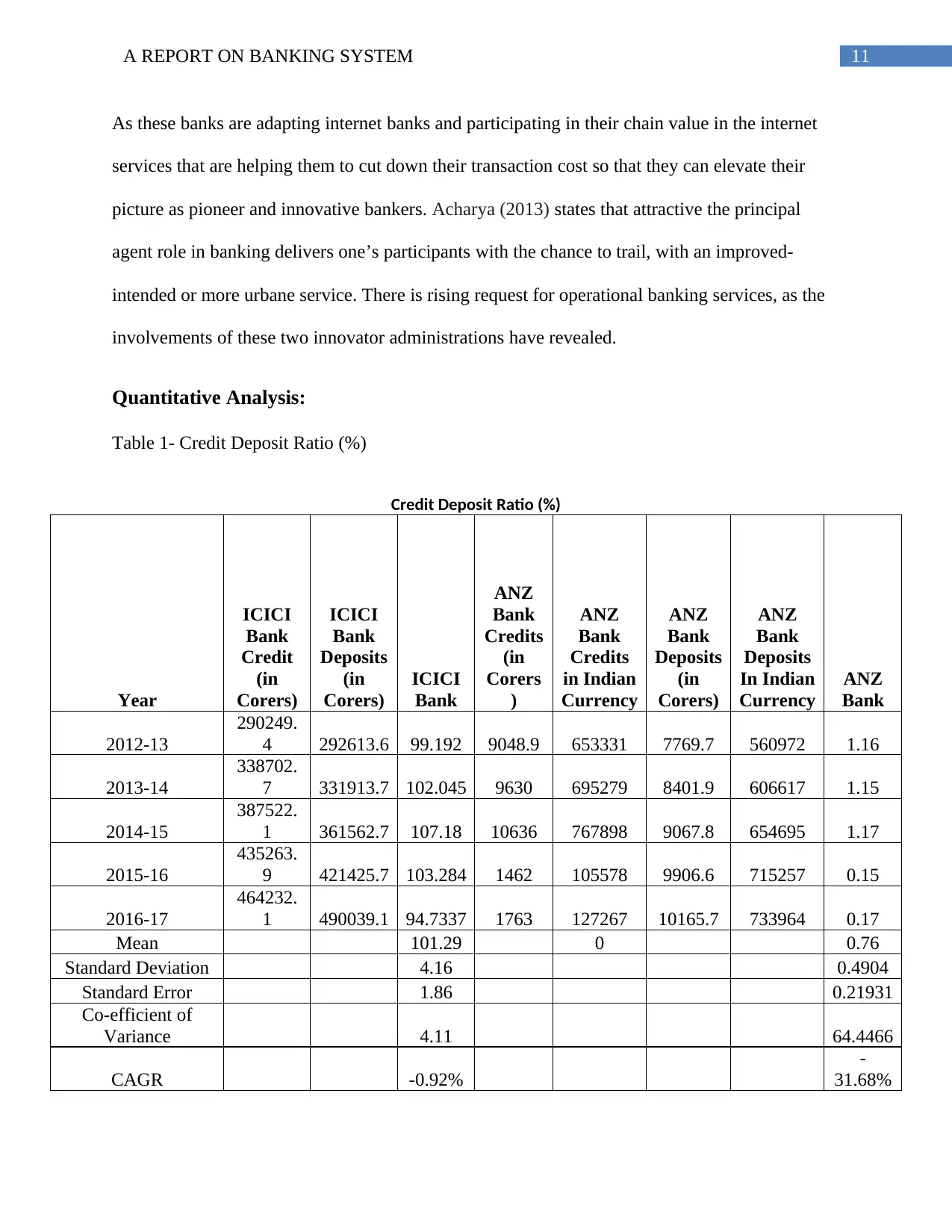

Quantitative Analysis:

Table 1- Credit Deposit Ratio (%)

Credit Deposit Ratio (%)

Year

ICICI

Bank

Credit

(in

Corers)

ICICI

Bank

Deposits

(in

Corers)

ICICI

Bank

ANZ

Bank

Credits

(in

Corers

)

ANZ

Bank

Credits

in Indian

Currency

ANZ

Bank

Deposits

(in

Corers)

ANZ

Bank

Deposits

In Indian

Currency

ANZ

Bank

2012-13

290249.

4 292613.6 99.192 9048.9 653331 7769.7 560972 1.16

2013-14

338702.

7 331913.7 102.045 9630 695279 8401.9 606617 1.15

2014-15

387522.

1 361562.7 107.18 10636 767898 9067.8 654695 1.17

2015-16

435263.

9 421425.7 103.284 1462 105578 9906.6 715257 0.15

2016-17

464232.

1 490039.1 94.7337 1763 127267 10165.7 733964 0.17

Mean 101.29 0 0.76

Standard Deviation 4.16 0.4904

Standard Error 1.86 0.21931

Co-efficient of

Variance 4.11 64.4466

CAGR -0.92%

-

31.68%

As these banks are adapting internet banks and participating in their chain value in the internet

services that are helping them to cut down their transaction cost so that they can elevate their

picture as pioneer and innovative bankers. Acharya (2013) states that attractive the principal

agent role in banking delivers one’s participants with the chance to trail, with an improved-

intended or more urbane service. There is rising request for operational banking services, as the

involvements of these two innovator administrations have revealed.

Quantitative Analysis:

Table 1- Credit Deposit Ratio (%)

Credit Deposit Ratio (%)

Year

ICICI

Bank

Credit

(in

Corers)

ICICI

Bank

Deposits

(in

Corers)

ICICI

Bank

ANZ

Bank

Credits

(in

Corers

)

ANZ

Bank

Credits

in Indian

Currency

ANZ

Bank

Deposits

(in

Corers)

ANZ

Bank

Deposits

In Indian

Currency

ANZ

Bank

2012-13

290249.

4 292613.6 99.192 9048.9 653331 7769.7 560972 1.16

2013-14

338702.

7 331913.7 102.045 9630 695279 8401.9 606617 1.15

2014-15

387522.

1 361562.7 107.18 10636 767898 9067.8 654695 1.17

2015-16

435263.

9 421425.7 103.284 1462 105578 9906.6 715257 0.15

2016-17

464232.

1 490039.1 94.7337 1763 127267 10165.7 733964 0.17

Mean 101.29 0 0.76

Standard Deviation 4.16 0.4904

Standard Error 1.86 0.21931

Co-efficient of

Variance 4.11 64.4466

CAGR -0.92%

-

31.68%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.