Detailed Analysis of Indirect Tax, VAT Regulations and Accounting

VerifiedAdded on 2021/01/01

|13

|3776

|427

Report

AI Summary

This report delves into the intricacies of indirect tax, particularly Value Added Tax (VAT), offering a comprehensive overview of its regulations and accounting practices. It begins with an introduction to indirect taxes, highlighting VAT's significance in the UK and its role in revenue generation. The report then explores various facets of VAT, including sources of information, interactions with government agencies like HMRC, VAT registration requirements, and the information that must be included on business documents. It details different VAT schemes such as annual accounting, cash accounting, flat-rate schemes, and standard schemes, along with their implications for businesses. The report further examines the importance of maintaining up-to-date knowledge of changes in legislation and provides practical examples of data extraction, input and output calculations, and the determination of VAT liabilities. It also covers the implications of non-compliance with VAT regulations, adjustments for errors, and the impact of VAT payments on cash flow and financial forecasts, concluding with advice on changes in VAT legislation. The report aims to provide a detailed understanding of VAT and its operational aspects within a business context.

INDIRECT TAX

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Sources of VAT information.................................................................................................1

1.2 The way in which an organisation should interact with the relevant government agency....1

1.3 VAT registration requirements.............................................................................................2

1.4 Information that must be included on business documents of VAT registered businesses. .2

1.5 Requirements and frequency of reporting for VAT schemes...............................................3

1.6 Maintaining an up-to-date knowledge of changes to code of practice, regulation or

legislation....................................................................................................................................4

TASK 2............................................................................................................................................4

2.1 Extract relevant data for a specific period from the accounting system...............................4

2.2 Calculation of inputs and outputs using VAT classifications...............................................5

2.3 Calculation of VAT due to, or from the relevant tax authority.............................................5

2.4 VAT return and associated payment within the statutory time limits...................................6

TASK 3............................................................................................................................................7

3.1 Implications and penalties for an organisation resulting from failure to abide by VAT

regulations...................................................................................................................................7

3.2 Adjustments and declarations for any errors or omission identified in previous VAT

period...........................................................................................................................................8

TASK 4............................................................................................................................................9

4.1 Impact of VAT payment on organisation's cash flow and financial forecasts......................9

4.2 Advise persons regarding changes in VAT legislation which would have an effect on an

organisation recording system to the concerned people ............................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Sources of VAT information.................................................................................................1

1.2 The way in which an organisation should interact with the relevant government agency....1

1.3 VAT registration requirements.............................................................................................2

1.4 Information that must be included on business documents of VAT registered businesses. .2

1.5 Requirements and frequency of reporting for VAT schemes...............................................3

1.6 Maintaining an up-to-date knowledge of changes to code of practice, regulation or

legislation....................................................................................................................................4

TASK 2............................................................................................................................................4

2.1 Extract relevant data for a specific period from the accounting system...............................4

2.2 Calculation of inputs and outputs using VAT classifications...............................................5

2.3 Calculation of VAT due to, or from the relevant tax authority.............................................5

2.4 VAT return and associated payment within the statutory time limits...................................6

TASK 3............................................................................................................................................7

3.1 Implications and penalties for an organisation resulting from failure to abide by VAT

regulations...................................................................................................................................7

3.2 Adjustments and declarations for any errors or omission identified in previous VAT

period...........................................................................................................................................8

TASK 4............................................................................................................................................9

4.1 Impact of VAT payment on organisation's cash flow and financial forecasts......................9

4.2 Advise persons regarding changes in VAT legislation which would have an effect on an

organisation recording system to the concerned people ............................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

An indirect tax is collected by an intermediary from the person who bears the ultimate

economic burden of the tax. Indirect tax is a type of tax where the incidence and impact of

taxation does not fall on the same entity. In this case burden of tax can be shifted by the taxpayer

to someone else. It has the effect to rising the price of the products on which they are imposed.

Indirect tax is collected by one entity in the supply chain and paid to the government but burden

of this tax is passed to ultimate consumer as part of the purchase price of goods and service.

Indirect taxes are sales tax, value added tax (VAT)and goods and service tax (GST). In United

Kingdom value added tax was introduced in the year 1973 and is the third largest source of

revenue for the government (Adema, Fron and Ladaique, 2014). In this project regulations of

VAT, accurate and timely VAT return , VAT penalties and communication of VAT information

is discussed.

TASK 1

1.1 Sources of VAT information

VAT is applied to all the provisions of goods and services. It is collected on the value of

goods or services that have been provided every time when there is a translation of sale and

purchase of goods and services. Information regarding VAT is collected from the sale and

purchase books that are maintained by businesses. As this tax is applied on the sale and purchase

then it information regarding amount of VAT tax that is collected or paid by the company is

calculated by the sale and purchase books. When sales return is received by business entity then

a credit note is issued by the business and amount of VAT collected is reversed. Debit note is

received by the businesses when purchased goods are returned. Both debit and credit note have

effect on the amount of tax that is needed to be paid to the government. So, before settling the

amount of VAT with the government sales and purchase books and debit, credit notes must be

considered. As all these are considered as source of information of VAT amount.

1.2 The way in which an organisation should interact with the relevant government agency

Business organisations operating in the country needs to comply with all the government

rules and regulations prescribed to be followed (Bargain and et.al., 2015). HMRC is the

government institution in UK that deals with various related to tax. Interaction between

businesses and government is done through departments established by HMRC. There are 25

1

An indirect tax is collected by an intermediary from the person who bears the ultimate

economic burden of the tax. Indirect tax is a type of tax where the incidence and impact of

taxation does not fall on the same entity. In this case burden of tax can be shifted by the taxpayer

to someone else. It has the effect to rising the price of the products on which they are imposed.

Indirect tax is collected by one entity in the supply chain and paid to the government but burden

of this tax is passed to ultimate consumer as part of the purchase price of goods and service.

Indirect taxes are sales tax, value added tax (VAT)and goods and service tax (GST). In United

Kingdom value added tax was introduced in the year 1973 and is the third largest source of

revenue for the government (Adema, Fron and Ladaique, 2014). In this project regulations of

VAT, accurate and timely VAT return , VAT penalties and communication of VAT information

is discussed.

TASK 1

1.1 Sources of VAT information

VAT is applied to all the provisions of goods and services. It is collected on the value of

goods or services that have been provided every time when there is a translation of sale and

purchase of goods and services. Information regarding VAT is collected from the sale and

purchase books that are maintained by businesses. As this tax is applied on the sale and purchase

then it information regarding amount of VAT tax that is collected or paid by the company is

calculated by the sale and purchase books. When sales return is received by business entity then

a credit note is issued by the business and amount of VAT collected is reversed. Debit note is

received by the businesses when purchased goods are returned. Both debit and credit note have

effect on the amount of tax that is needed to be paid to the government. So, before settling the

amount of VAT with the government sales and purchase books and debit, credit notes must be

considered. As all these are considered as source of information of VAT amount.

1.2 The way in which an organisation should interact with the relevant government agency

Business organisations operating in the country needs to comply with all the government

rules and regulations prescribed to be followed (Bargain and et.al., 2015). HMRC is the

government institution in UK that deals with various related to tax. Interaction between

businesses and government is done through departments established by HMRC. There are 25

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

departments that are established in the country that have direct interaction with businesses. These

departments can be communicated for any issue physically and online also. Qualified and

experienced persons are available there to provide every possible solution to the issue.

1.3 VAT registration requirements

The compulsory registration threshold for VAT in the UK is £83,000 of non-VAT

exempt income per financial year. The registration threshold for distance-selling into the UK is

£70000. the threshold is based on the VAT taxable turnover that means sales that are not

exempted from VAT (Tagkalakis, 2014). Distance selling means when a registered business of

one European Union country sells goods to other country in European Union. To registration of

business under VAT following documents are required-

National Insurance (NI) number

Tax identifier i.e. Unique Taxpayer's reference (UTR) number

Certificate of incorporation and incorporation details

Business banks accounts details

Information on all associated businesses within last two years

Some businesses are prohibited from registering under VAT if the business tends to sell

goods or services that are exempt from VAT tax such as insurance and education businesses.

Companies that do businesses with the UK but don't have a physical presence within the UK

needs to demonstrate that they are making sales to UK to have VAT registration. When

registration process is complete then registration certificate is provided to the businesses that

includes VAT number and details regarding submission of first return.

1.4 Information that must be included on business documents of VAT registered businesses

Businesses that are registered under VAT while preparing invoices must include

information that specifies that business is registered. Invoices that are issued by businesses are

considered as business documents. While generating a invoice registration number that is

provided to the business by tax department of VAT must be mentioned. This is a unique number

that is possessed by businesses that are registered under VAT. Government of the country

collects and make refund of the tax collected by business entities on the basis of registration

number. Together with this invoice generated for sale or received by businesses must contain

name of the enterprise that is involved in the transaction. In addition to this information legal

form of the business, location of the business must also be present in documents. Corporate

2

departments can be communicated for any issue physically and online also. Qualified and

experienced persons are available there to provide every possible solution to the issue.

1.3 VAT registration requirements

The compulsory registration threshold for VAT in the UK is £83,000 of non-VAT

exempt income per financial year. The registration threshold for distance-selling into the UK is

£70000. the threshold is based on the VAT taxable turnover that means sales that are not

exempted from VAT (Tagkalakis, 2014). Distance selling means when a registered business of

one European Union country sells goods to other country in European Union. To registration of

business under VAT following documents are required-

National Insurance (NI) number

Tax identifier i.e. Unique Taxpayer's reference (UTR) number

Certificate of incorporation and incorporation details

Business banks accounts details

Information on all associated businesses within last two years

Some businesses are prohibited from registering under VAT if the business tends to sell

goods or services that are exempt from VAT tax such as insurance and education businesses.

Companies that do businesses with the UK but don't have a physical presence within the UK

needs to demonstrate that they are making sales to UK to have VAT registration. When

registration process is complete then registration certificate is provided to the businesses that

includes VAT number and details regarding submission of first return.

1.4 Information that must be included on business documents of VAT registered businesses

Businesses that are registered under VAT while preparing invoices must include

information that specifies that business is registered. Invoices that are issued by businesses are

considered as business documents. While generating a invoice registration number that is

provided to the business by tax department of VAT must be mentioned. This is a unique number

that is possessed by businesses that are registered under VAT. Government of the country

collects and make refund of the tax collected by business entities on the basis of registration

number. Together with this invoice generated for sale or received by businesses must contain

name of the enterprise that is involved in the transaction. In addition to this information legal

form of the business, location of the business must also be present in documents. Corporate

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

identification number that is provided to each business must me mentioned in business

documents with VAT number. Agreements that are entered by the businesses are considered as

business documents and different goods and services differs for VAT rate. It will be easy for the

business when rate of VAT is specified in the agreements that are entered by various entities for

business transactions (Pomeranz, 2015).

1.5 Requirements and frequency of reporting for VAT schemes

VAT accounting schemes helps business to make complex processes simpler by

improving cash flows in the business. Introduction of these schemes is done to make

administration and general burden of accounting for tax easier for smaller businesses. Various

VAT schemes that are used by the businesses are as follows-

Annual accounting- The annual accounting scheme helps small businesses by allowing

them to submit only one VAT return annually rather then four returns. During the year

they pay instalments for expected liability for VAT with the balancing payments due with

the return. The scheme is intended to help with budgeting and cash flow and reduce

paperwork.

Cash accounting- This scheme helped small businesses with their finances and to

prevent them having to pay over VAT to revenue and customs without having first

received the proceeds of sale from their consumers. As new and small businesses grants

credit to consumer to gain their trade and realisation of revenue gates delayed. Imposing

taxes before realisation of revenue creates problem of cash in the business. This issue is

resolved by cash accounting scheme (McNabb and LeMay-Boucher, 2014).

Flat-rate scheme- An optional flat rate scheme is available to businesses for

simplification VAT accounting burden on small businesses with taxable turnover of

£150000 (excluding VAT) or less. Adopting this scheme remove burden of detailed

records of purchase and sales. Flat rate percentage varies according to the main business

activity of different organisations.

Standard scheme- The standard VAT accounting scheme is a method of reporting VAT

on the basis when invoices are issued. Businesses under this scheme submits a VAT

return four times a year. Amount of tax is paid quarterly and similarly refunds are also

granted quarterly. Refund is granted when the amount of tax paid is more then payable

amount.

3

documents with VAT number. Agreements that are entered by the businesses are considered as

business documents and different goods and services differs for VAT rate. It will be easy for the

business when rate of VAT is specified in the agreements that are entered by various entities for

business transactions (Pomeranz, 2015).

1.5 Requirements and frequency of reporting for VAT schemes

VAT accounting schemes helps business to make complex processes simpler by

improving cash flows in the business. Introduction of these schemes is done to make

administration and general burden of accounting for tax easier for smaller businesses. Various

VAT schemes that are used by the businesses are as follows-

Annual accounting- The annual accounting scheme helps small businesses by allowing

them to submit only one VAT return annually rather then four returns. During the year

they pay instalments for expected liability for VAT with the balancing payments due with

the return. The scheme is intended to help with budgeting and cash flow and reduce

paperwork.

Cash accounting- This scheme helped small businesses with their finances and to

prevent them having to pay over VAT to revenue and customs without having first

received the proceeds of sale from their consumers. As new and small businesses grants

credit to consumer to gain their trade and realisation of revenue gates delayed. Imposing

taxes before realisation of revenue creates problem of cash in the business. This issue is

resolved by cash accounting scheme (McNabb and LeMay-Boucher, 2014).

Flat-rate scheme- An optional flat rate scheme is available to businesses for

simplification VAT accounting burden on small businesses with taxable turnover of

£150000 (excluding VAT) or less. Adopting this scheme remove burden of detailed

records of purchase and sales. Flat rate percentage varies according to the main business

activity of different organisations.

Standard scheme- The standard VAT accounting scheme is a method of reporting VAT

on the basis when invoices are issued. Businesses under this scheme submits a VAT

return four times a year. Amount of tax is paid quarterly and similarly refunds are also

granted quarterly. Refund is granted when the amount of tax paid is more then payable

amount.

3

1.6 Maintaining an up-to-date knowledge of changes to code of practice, regulation or legislation

Code of practice, regulation or legislation are followed by organisations to have smooth

functioning of operations. It is advisable to have up to date knowledge regarding various

regulations that are provided by the government. As following improved legislation and code of

conduct improved quality of services provided (Mathur and Morris, 2014). This also helps to

maintain all the financial information that belongs to taxes in more appropriate manner. Changes

in the government regulations are made to reduce loop holes that are present in previous law.

Keeping up-to-date knowledge about code of conduct, legislation helps to adopt changes to

become more accurate. Chances of mistakes are minimised and conflict in the organisation

reduces when everyone in the organisation is aware about changes. Calculation of taxes as per

new regulations minimise government intervention in business activities. As all the laws and

standards set by the government are met by the business houses.

TASK 2

2.1 Extract relevant data for a specific period from the accounting system

Example 1- Standard rate of VAT is currently is 20%.

Zoe is in the process of completing her VAT return for the quarter ended 31 march 2018.

the following information is available:

Sales invoices totalling is £128000 were issued in respect of standard rated sales.

Standard rated expenses amounted to £24800.

On 15 February 2013 Gwen purchased machinery at a cost of £24150 inclusive of VAT.

Example 2- Cathy will commence trading in the near future. She operates a small

aeroplane and is considering three alternative types of businesses (Madden, 2015). These are (1)

training, in which case all sales will be standard rated for VAT, (2) transport, in which case all

sales will be Zero rated for VAT and (3) an air ambulance service, in which case all sales will be

exempted for VAT.

For each alternative Cathy sales will be £ 80000 per month(exclusive of VAT) and

standard rated expenses will be £ 15000 per month(inclusive of VAT).

4

Code of practice, regulation or legislation are followed by organisations to have smooth

functioning of operations. It is advisable to have up to date knowledge regarding various

regulations that are provided by the government. As following improved legislation and code of

conduct improved quality of services provided (Mathur and Morris, 2014). This also helps to

maintain all the financial information that belongs to taxes in more appropriate manner. Changes

in the government regulations are made to reduce loop holes that are present in previous law.

Keeping up-to-date knowledge about code of conduct, legislation helps to adopt changes to

become more accurate. Chances of mistakes are minimised and conflict in the organisation

reduces when everyone in the organisation is aware about changes. Calculation of taxes as per

new regulations minimise government intervention in business activities. As all the laws and

standards set by the government are met by the business houses.

TASK 2

2.1 Extract relevant data for a specific period from the accounting system

Example 1- Standard rate of VAT is currently is 20%.

Zoe is in the process of completing her VAT return for the quarter ended 31 march 2018.

the following information is available:

Sales invoices totalling is £128000 were issued in respect of standard rated sales.

Standard rated expenses amounted to £24800.

On 15 February 2013 Gwen purchased machinery at a cost of £24150 inclusive of VAT.

Example 2- Cathy will commence trading in the near future. She operates a small

aeroplane and is considering three alternative types of businesses (Madden, 2015). These are (1)

training, in which case all sales will be standard rated for VAT, (2) transport, in which case all

sales will be Zero rated for VAT and (3) an air ambulance service, in which case all sales will be

exempted for VAT.

For each alternative Cathy sales will be £ 80000 per month(exclusive of VAT) and

standard rated expenses will be £ 15000 per month(inclusive of VAT).

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2.2 Calculation of inputs and outputs using VAT classifications

Standard supplies: Example1

Output VAT

Sales (128000*20%)

£ 25600

Input VAT

Expenses (24800*20%) (£4960)

Machinery (24150*20/120) (£4960)

VAT payable £16615

Example 2

In this example Cathy will be required to register for VAT as taxable supplies are made

by her. Output VAT of £16000 (80000*20%) per month will be due and input tax of £ 2500

(15000*20/120) per month will be receivable.

Exempted supplies: Cathy will not be required or permitted to register for VAT as she

will not be making taxable supplies.

Zero -rated supplies: Cathy can apply for exemption from registration for VAT since

she is making zero-rated supplies, otherwise she should still register as these are taxable

supplies.

Output VAT will not be due but input VAT of £2500 per month will be recoverable.

Exports: VAT is charged on the goods that are used in European Union and if goods that

are exported outside the EU no VAT is charged (Schenk, Thuronyi and Cui, 2015).

Goods exported can be charged with zero-rated so that input credit can be enjoyed by the

businesses.

2.3 Calculation of VAT due to, or from the relevant tax authority

When amount of tax that needs to be paid to other business entity is more then the

amount receivable then it will be termed as amount due to tax department (Kumar, 2014). To

5

Standard supplies: Example1

Output VAT

Sales (128000*20%)

£ 25600

Input VAT

Expenses (24800*20%) (£4960)

Machinery (24150*20/120) (£4960)

VAT payable £16615

Example 2

In this example Cathy will be required to register for VAT as taxable supplies are made

by her. Output VAT of £16000 (80000*20%) per month will be due and input tax of £ 2500

(15000*20/120) per month will be receivable.

Exempted supplies: Cathy will not be required or permitted to register for VAT as she

will not be making taxable supplies.

Zero -rated supplies: Cathy can apply for exemption from registration for VAT since

she is making zero-rated supplies, otherwise she should still register as these are taxable

supplies.

Output VAT will not be due but input VAT of £2500 per month will be recoverable.

Exports: VAT is charged on the goods that are used in European Union and if goods that

are exported outside the EU no VAT is charged (Schenk, Thuronyi and Cui, 2015).

Goods exported can be charged with zero-rated so that input credit can be enjoyed by the

businesses.

2.3 Calculation of VAT due to, or from the relevant tax authority

When amount of tax that needs to be paid to other business entity is more then the

amount receivable then it will be termed as amount due to tax department (Kumar, 2014). To

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

calculate amount of due to or due from the appropriate authority input and output tax

calculations will be done.

Standard supplies- Amount of VAT will be calculated at the general applicable rate of

20%. Zoe will be liable to pay £16615 to the VAT department authorised by HMRC.

In another case Cathy is required to pay an amount of £13500 to the department as net

VAT payable.

Zero-rated supplies: Zero-rated means goods and services are not exempt from tax but

rate of tax charged is zero. This helps to take credit to the business for the amount paid as input

tax. Cathy is exempted from registration and do not required to pay any output tax to the

government. Input tax that must be receivable of £2500 (Raj, 2017).

Exempted supplies: For supply of goods and services that are registered as exempted the

registration is not required. So, output VAT will not be payable and no input tax will be

recoverable.

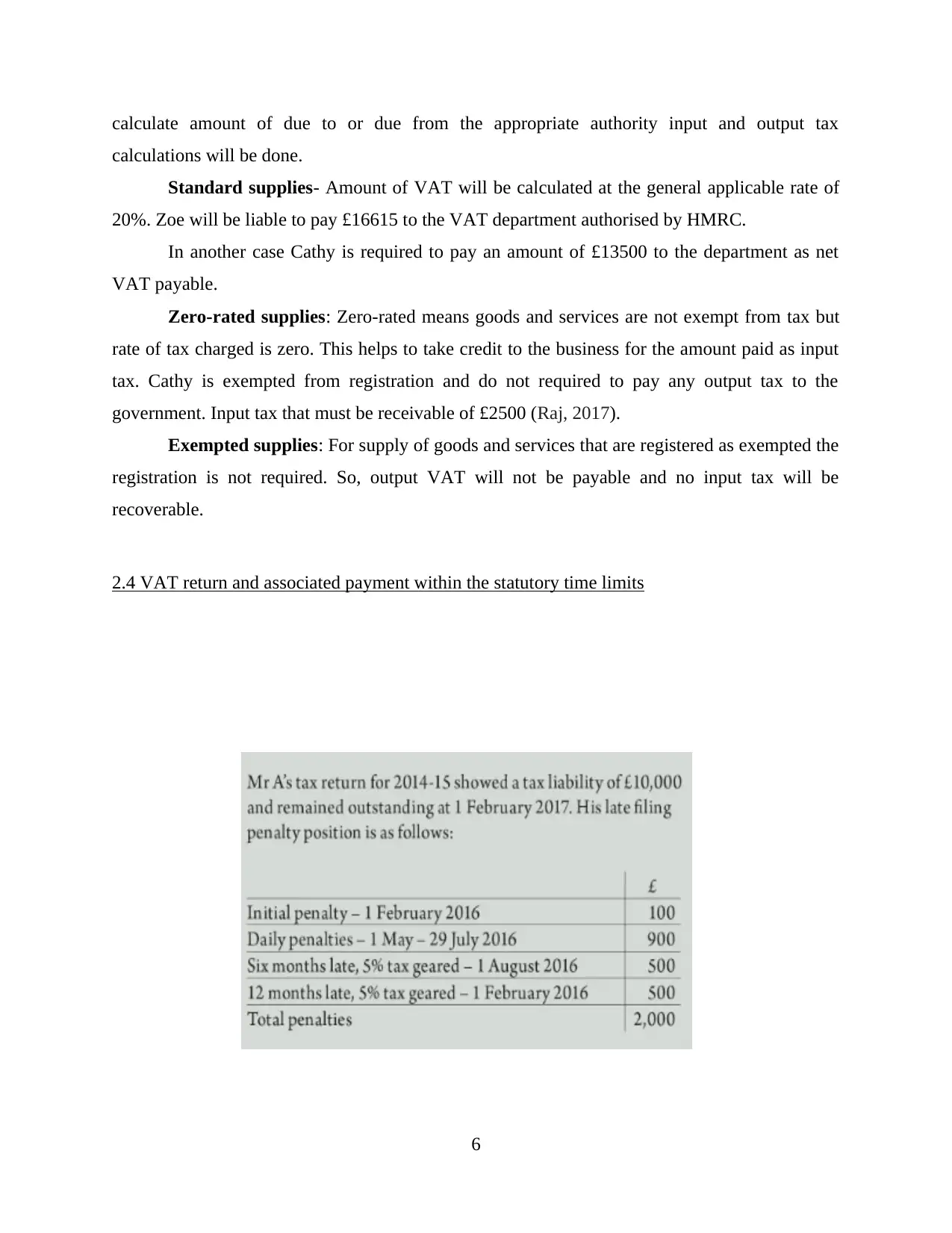

2.4 VAT return and associated payment within the statutory time limits

6

calculations will be done.

Standard supplies- Amount of VAT will be calculated at the general applicable rate of

20%. Zoe will be liable to pay £16615 to the VAT department authorised by HMRC.

In another case Cathy is required to pay an amount of £13500 to the department as net

VAT payable.

Zero-rated supplies: Zero-rated means goods and services are not exempt from tax but

rate of tax charged is zero. This helps to take credit to the business for the amount paid as input

tax. Cathy is exempted from registration and do not required to pay any output tax to the

government. Input tax that must be receivable of £2500 (Raj, 2017).

Exempted supplies: For supply of goods and services that are registered as exempted the

registration is not required. So, output VAT will not be payable and no input tax will be

recoverable.

2.4 VAT return and associated payment within the statutory time limits

6

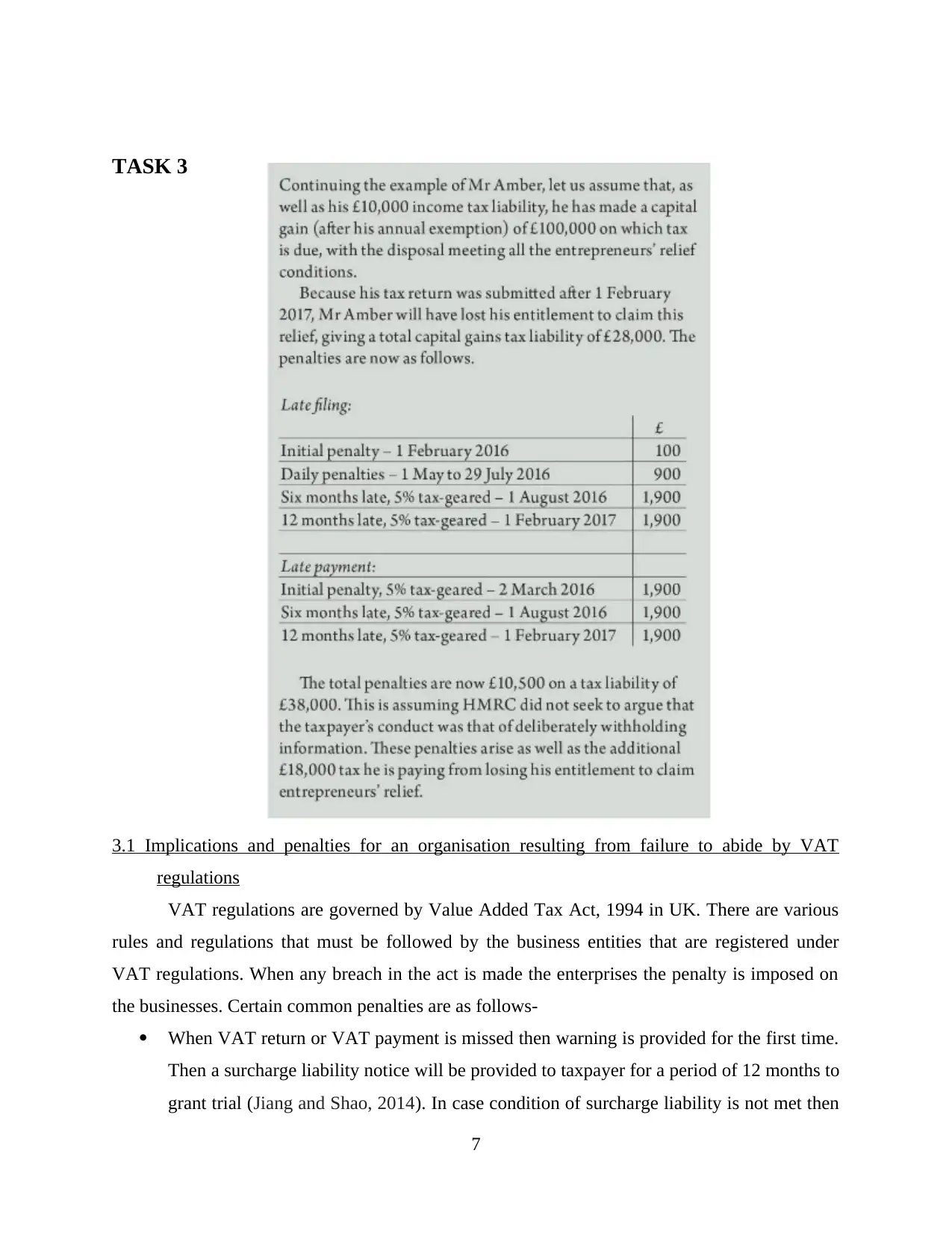

TASK 3

3.1 Implications and penalties for an organisation resulting from failure to abide by VAT

regulations

VAT regulations are governed by Value Added Tax Act, 1994 in UK. There are various

rules and regulations that must be followed by the business entities that are registered under

VAT regulations. When any breach in the act is made the enterprises the penalty is imposed on

the businesses. Certain common penalties are as follows-

When VAT return or VAT payment is missed then warning is provided for the first time.

Then a surcharge liability notice will be provided to taxpayer for a period of 12 months to

grant trial (Jiang and Shao, 2014). In case condition of surcharge liability is not met then

7

3.1 Implications and penalties for an organisation resulting from failure to abide by VAT

regulations

VAT regulations are governed by Value Added Tax Act, 1994 in UK. There are various

rules and regulations that must be followed by the business entities that are registered under

VAT regulations. When any breach in the act is made the enterprises the penalty is imposed on

the businesses. Certain common penalties are as follows-

When VAT return or VAT payment is missed then warning is provided for the first time.

Then a surcharge liability notice will be provided to taxpayer for a period of 12 months to

grant trial (Jiang and Shao, 2014). In case condition of surcharge liability is not met then

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2% surcharge will be applied and penalty will be increased to 5, 10 or 15 percent if error

is repeated again.

Late registration under VAT also attracts penalty, when period of delay is less the 9

months the 5% of the VAT due is termed as penalty. Delay is for 9 to 18 months the

penalty is 10% of the VAT due. For more then 18 months 15% of the VAT due is

considered as penalty.

When VAT regulations are avoided by organisations then it attracts legal action against

the business. When turnover exceeds the basic limit not required to register under VAT then it

become a legal obligation of the businesses to get registered. Otherwise legal actions will be

taken by the government and it will affects image of the company.

3.2 Adjustments and declarations for any errors or omission identified in previous VAT period

Adjustments in the current VAT account can be made to correct errors on past returns if

they are-

below the reporting threshold

not deliberated(mistake made on a purpose)

for an accounting period that ends less then 4 years ago

Reporting threshold means adjustment in next VAT return can be made if the amount of

error is £10000 or less (Errors in VAT records, 2015). Report of error is filled in the form

VAT652 and send to the error correction team. HMRC then send a notice to the organisation

regarding tax or interest owed by businesses. There are two methods of correcting errors such as-

Method 1: If the errors of a net value don not exceed £10000 or net value is between

£10000 and £50000 but do not exceed 1% of the net output of the VAT return period.

Method 2: It is forb the errors of a net value between £10000 and £50000 that can exceed

not more then £5000000.

TASK 4

4.1 Impact of VAT payment on organisation's cash flow and financial forecasts

VAT is an indirect tax collected by the businesses from ultimate consumers and paid to

the government on quarterly basis. Credit is allowed by businesses to expand and survive in

competitive market. Allowing credit to consumers creates a time gape between sales and

realisation of revenue (Fabbri, 2015). When sales are made and quarterly return is filled by

8

is repeated again.

Late registration under VAT also attracts penalty, when period of delay is less the 9

months the 5% of the VAT due is termed as penalty. Delay is for 9 to 18 months the

penalty is 10% of the VAT due. For more then 18 months 15% of the VAT due is

considered as penalty.

When VAT regulations are avoided by organisations then it attracts legal action against

the business. When turnover exceeds the basic limit not required to register under VAT then it

become a legal obligation of the businesses to get registered. Otherwise legal actions will be

taken by the government and it will affects image of the company.

3.2 Adjustments and declarations for any errors or omission identified in previous VAT period

Adjustments in the current VAT account can be made to correct errors on past returns if

they are-

below the reporting threshold

not deliberated(mistake made on a purpose)

for an accounting period that ends less then 4 years ago

Reporting threshold means adjustment in next VAT return can be made if the amount of

error is £10000 or less (Errors in VAT records, 2015). Report of error is filled in the form

VAT652 and send to the error correction team. HMRC then send a notice to the organisation

regarding tax or interest owed by businesses. There are two methods of correcting errors such as-

Method 1: If the errors of a net value don not exceed £10000 or net value is between

£10000 and £50000 but do not exceed 1% of the net output of the VAT return period.

Method 2: It is forb the errors of a net value between £10000 and £50000 that can exceed

not more then £5000000.

TASK 4

4.1 Impact of VAT payment on organisation's cash flow and financial forecasts

VAT is an indirect tax collected by the businesses from ultimate consumers and paid to

the government on quarterly basis. Credit is allowed by businesses to expand and survive in

competitive market. Allowing credit to consumers creates a time gape between sales and

realisation of revenue (Fabbri, 2015). When sales are made and quarterly return is filled by

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

organisation for VAT tax on the sales made is submitted to the government instead of realisation

of revenue from customers. Payment of VAT amount to the government have negative effect on

financial condition of the business. As outflow of cash is more then inflow in form of payment of

taxes to the government. Elasticity of funds helps in quick decision making that involves focus

on the availability of funds. When payment of taxes are made in advance before they are

recovered from the consumers then liquidity of the company gets hampered. When taxes paid to

the government is more then the amount realised then future condition of finances in the business

gets affected and business suffers in long run. Inefficient cash flow of the company affects

organisational planning for future and chances of failure of business gets increased.

4.2 Advise persons regarding changes in VAT legislation which would have an effect on an

organisation recording system to the concerned people

Financial statements of the organisation represents calculation of VAT for a specific time

period. Preparation of these statements are based on rules and regulations that are provided by

the taxation department of the country (Duclos, Makdissi and Araar, 2014). Change in VAT

legislation will affects recording system followed by the organisation. For example- When

changes regarding rate of VAT is introduced by the department or variation is introduced with

reporting of transaction by making reporting of all the transaction compulsory. This will have

change in the recording system of the company for the transactions that are related to the

businesses. Affect of change in VAT legislation is taken care by accountants and tax department

in the company. As change in VAT legislation will impact accounting method that is followed

earlier by the businesses. Together with this if the changes that are in regarding to return or rate

then tax department needs to be aware about this change and adequate steps are taken to meet the

required change.

CONCLUSION

From the above report it is concluded that indirect tax is burden to the consumers of

goods and services. Organisation that deals in sale and purchase of goods and services needs to

be registered under VAT. Business entities has to follow all the required regulations of VAT in

preparation of financial statements. VAT returns has to be filled accurately and timely manner to

avoid any legal complications. Default in VAT regulations and return filling attracts various

penalties that are imposed on business houses. Taxes that are paid by organisations as VAT

9

of revenue from customers. Payment of VAT amount to the government have negative effect on

financial condition of the business. As outflow of cash is more then inflow in form of payment of

taxes to the government. Elasticity of funds helps in quick decision making that involves focus

on the availability of funds. When payment of taxes are made in advance before they are

recovered from the consumers then liquidity of the company gets hampered. When taxes paid to

the government is more then the amount realised then future condition of finances in the business

gets affected and business suffers in long run. Inefficient cash flow of the company affects

organisational planning for future and chances of failure of business gets increased.

4.2 Advise persons regarding changes in VAT legislation which would have an effect on an

organisation recording system to the concerned people

Financial statements of the organisation represents calculation of VAT for a specific time

period. Preparation of these statements are based on rules and regulations that are provided by

the taxation department of the country (Duclos, Makdissi and Araar, 2014). Change in VAT

legislation will affects recording system followed by the organisation. For example- When

changes regarding rate of VAT is introduced by the department or variation is introduced with

reporting of transaction by making reporting of all the transaction compulsory. This will have

change in the recording system of the company for the transactions that are related to the

businesses. Affect of change in VAT legislation is taken care by accountants and tax department

in the company. As change in VAT legislation will impact accounting method that is followed

earlier by the businesses. Together with this if the changes that are in regarding to return or rate

then tax department needs to be aware about this change and adequate steps are taken to meet the

required change.

CONCLUSION

From the above report it is concluded that indirect tax is burden to the consumers of

goods and services. Organisation that deals in sale and purchase of goods and services needs to

be registered under VAT. Business entities has to follow all the required regulations of VAT in

preparation of financial statements. VAT returns has to be filled accurately and timely manner to

avoid any legal complications. Default in VAT regulations and return filling attracts various

penalties that are imposed on business houses. Taxes that are paid by organisations as VAT

9

impacts cash flow of the business and must be deal in efficient manner to cope with the

complication involved with the financial position. Together with this change in VAT regulations

must be effectively implemented by company to have positive growth.

10

complication involved with the financial position. Together with this change in VAT regulations

must be effectively implemented by company to have positive growth.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.