Comprehensive Indirect Tax Report: VAT, Calculations, and Compliance

VerifiedAdded on 2021/01/01

|12

|3863

|46

Report

AI Summary

This report comprehensively examines indirect taxes, particularly Value Added Tax (VAT) in the UK. It begins with an introduction to indirect taxes and VAT, explaining their nature and importance. The report then delves into various aspects of VAT, starting with sources of information and how organizations should interact with government agencies like HMRC. It covers VAT registration requirements, the information needed on business documentation, and the frequency of reporting for different VAT schemes, including annual accounting, cash accounting, and flat-rate schemes. The report emphasizes the importance of staying updated on changes to VAT regulations and provides practical examples of VAT calculations, including output tax, input tax, and VAT payable. It also discusses the implications and penalties for non-compliance with VAT regulations and the handling of errors or omissions. Furthermore, the report addresses the impact of VAT payments on an organization's cash flow and financial forecasts, and the need to advise relevant personnel of changes in VAT legislation. The report concludes with a summary of the key points and references.

INDIRECT

TAX

Table of Contents

TAX

Table of Contents

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION...........................................................................................................................3

TASK 1 ...........................................................................................................................................4

1.1 Sources of Information on VAT...........................................................................................4

1.2 Explain how an organization should interact with the relevant government agency............4

1.3 Explain VAT registration requirements................................................................................5

1.4 Identify the information that must be included on business documentation of VAT

registered businesses...................................................................................................................6

1.5 Requirements and the frequency of reporting for various VAT schemes.............................6

1.6 Maintain an up-to-date knowledge of changes to codes of practice, regulation or

legislation....................................................................................................................................7

TASK 2............................................................................................................................................7

2.1 Extract relevant data for a specified data for a specific period from the accounting system.

.....................................................................................................................................................7

2.2 Calculations of VAT.............................................................................................................8

2.3 Calculate the VAT due to, or from, the relevant tax authority.............................................9

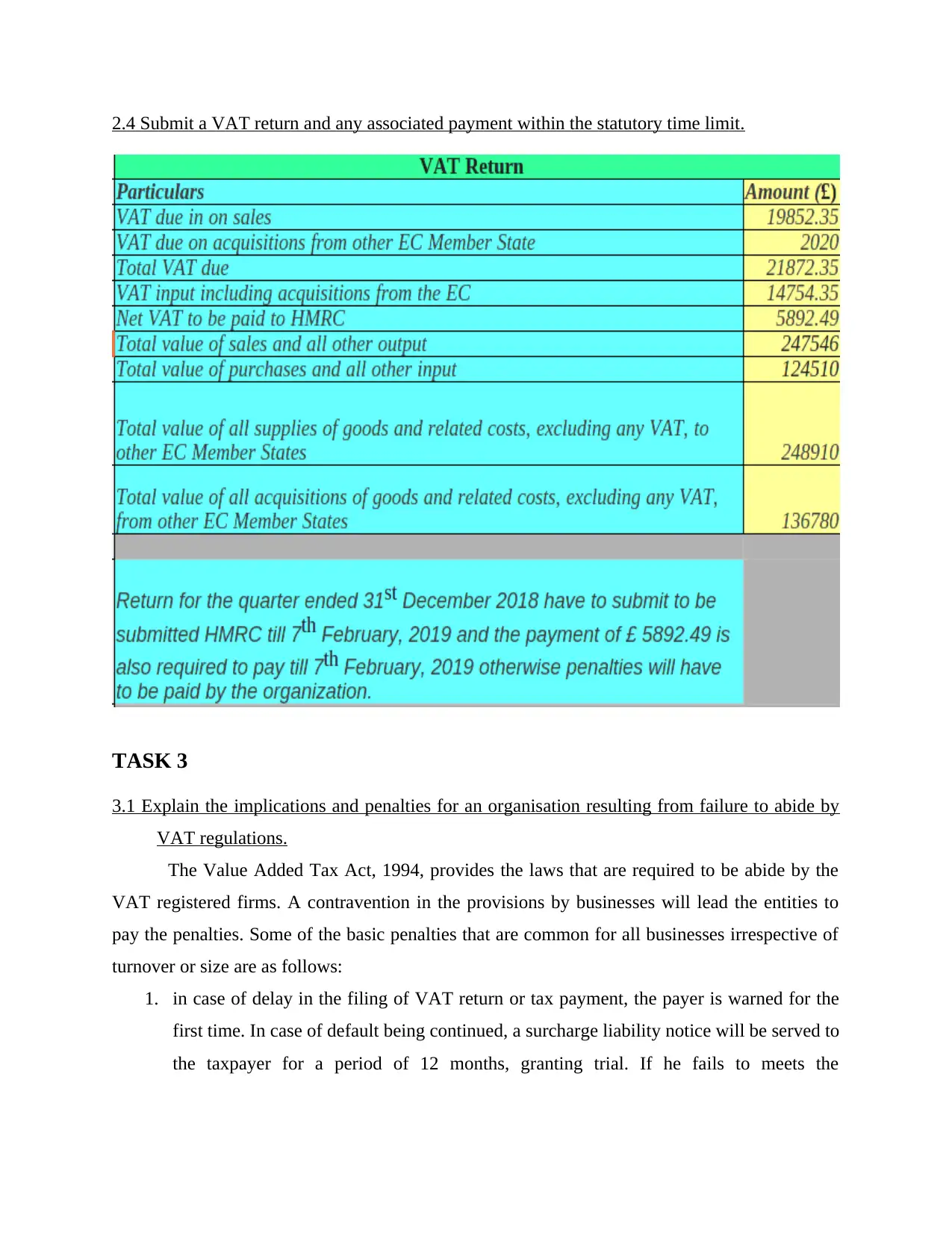

2.4 Submit a VAT return and any associated payment within the statutory time limit............10

TASK 3 .........................................................................................................................................10

3.1 Explain the implications and penalties for an organisation resulting from failure to abide

by VAT regulations...................................................................................................................10

3.2 Adjustments and declarations for any errors or omissions identified in previous VAT

periods.......................................................................................................................................11

TASK 4 .........................................................................................................................................11

4.1 Impact of VAT payment on organization's cash flow and financial forecasts....................11

4.2 Advise relevant people of changes in VAT legislation which would have an effect on an

organization's recording systems...............................................................................................12

CONCLUSION..............................................................................................................................12

................................................................................................................................................12

REFERENCES..............................................................................................................................12

INTRODUCTION

Indirect taxes are imposed on producers or suppliers by UK government. Under this

system, the burden of tax can be shifted to another person (consumer). Unlike, direct tax, it is

TASK 1 ...........................................................................................................................................4

1.1 Sources of Information on VAT...........................................................................................4

1.2 Explain how an organization should interact with the relevant government agency............4

1.3 Explain VAT registration requirements................................................................................5

1.4 Identify the information that must be included on business documentation of VAT

registered businesses...................................................................................................................6

1.5 Requirements and the frequency of reporting for various VAT schemes.............................6

1.6 Maintain an up-to-date knowledge of changes to codes of practice, regulation or

legislation....................................................................................................................................7

TASK 2............................................................................................................................................7

2.1 Extract relevant data for a specified data for a specific period from the accounting system.

.....................................................................................................................................................7

2.2 Calculations of VAT.............................................................................................................8

2.3 Calculate the VAT due to, or from, the relevant tax authority.............................................9

2.4 Submit a VAT return and any associated payment within the statutory time limit............10

TASK 3 .........................................................................................................................................10

3.1 Explain the implications and penalties for an organisation resulting from failure to abide

by VAT regulations...................................................................................................................10

3.2 Adjustments and declarations for any errors or omissions identified in previous VAT

periods.......................................................................................................................................11

TASK 4 .........................................................................................................................................11

4.1 Impact of VAT payment on organization's cash flow and financial forecasts....................11

4.2 Advise relevant people of changes in VAT legislation which would have an effect on an

organization's recording systems...............................................................................................12

CONCLUSION..............................................................................................................................12

................................................................................................................................................12

REFERENCES..............................................................................................................................12

INTRODUCTION

Indirect taxes are imposed on producers or suppliers by UK government. Under this

system, the burden of tax can be shifted to another person (consumer). Unlike, direct tax, it is

charged on incomes of households and firms. It is also called “expenditure taxes”. Value Added

Tax or VAT is an indirect tax, charged on sale of goods and services in the UK. It is a kind of

“consumption tax” due it's being levied on the products that people buy. It is collected by

business on behalf of the government, hence called “indirect tax”. In

UK, it is the third largest source of government revenue after income tax and National insurance.

The report covers, VAT regulations by describing its sources, registration requirements, various

schemes, calculation, penalties for failure or breaching the regulations, adjustments and

declarations for errors assessed in previous VAT return (Acosta‐Ormaechea and et. al., 2012).

TASK 1

1.1 Sources of Information on VAT

The business that are dealing in goods and services should know everything about the

taxes that are levied. The necessary information range from registration to rates to calculations

and basis of charging. It becomes imperative to gather and apply complete detail about the VAT,

for carrying out the activities smoothly. The best source to obtain information in Value Added

Tax Act, 1994 and rules. it contains meaning, definitions, provisions, items covered, criteria for

firms that will be covered by this Act, amendments, penalties for contravention and many more.

Further, online guide has been provided by the UK government in order to enable the entities to

have the every possible knowledge about VAT before starting the business or expansion by

entering into a new segment of service or goods.

1.2 Explain how an organization should interact with the relevant government agency.

VAT is levied and administered by the UK government. It is the ultimate authority for

implementing and changing the provisions of the ACT. All the data from registration to paying

this tax is saved in the database of HM Revenue and Customs (HMRC) department. It has

established its departments to assist the taxpayer regarding the payment. Further, tax

representatives have been appointed by HMRC who will control VAT regulations applicable on

the firms operating in their assigned areas. This department has introduced digital record keeping

system for VAT-registered businesses (Overview of digitalization of tax under HMRC (, 2018).

The firms can file their return physically by visiting the office of the representative or can also

file online by accessing the government official site. Further, any query will be resolved by such

officials for better interaction.

Tax or VAT is an indirect tax, charged on sale of goods and services in the UK. It is a kind of

“consumption tax” due it's being levied on the products that people buy. It is collected by

business on behalf of the government, hence called “indirect tax”. In

UK, it is the third largest source of government revenue after income tax and National insurance.

The report covers, VAT regulations by describing its sources, registration requirements, various

schemes, calculation, penalties for failure or breaching the regulations, adjustments and

declarations for errors assessed in previous VAT return (Acosta‐Ormaechea and et. al., 2012).

TASK 1

1.1 Sources of Information on VAT

The business that are dealing in goods and services should know everything about the

taxes that are levied. The necessary information range from registration to rates to calculations

and basis of charging. It becomes imperative to gather and apply complete detail about the VAT,

for carrying out the activities smoothly. The best source to obtain information in Value Added

Tax Act, 1994 and rules. it contains meaning, definitions, provisions, items covered, criteria for

firms that will be covered by this Act, amendments, penalties for contravention and many more.

Further, online guide has been provided by the UK government in order to enable the entities to

have the every possible knowledge about VAT before starting the business or expansion by

entering into a new segment of service or goods.

1.2 Explain how an organization should interact with the relevant government agency.

VAT is levied and administered by the UK government. It is the ultimate authority for

implementing and changing the provisions of the ACT. All the data from registration to paying

this tax is saved in the database of HM Revenue and Customs (HMRC) department. It has

established its departments to assist the taxpayer regarding the payment. Further, tax

representatives have been appointed by HMRC who will control VAT regulations applicable on

the firms operating in their assigned areas. This department has introduced digital record keeping

system for VAT-registered businesses (Overview of digitalization of tax under HMRC (, 2018).

The firms can file their return physically by visiting the office of the representative or can also

file online by accessing the government official site. Further, any query will be resolved by such

officials for better interaction.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1.3 Explain VAT registration requirements.

A business must be registered to avail the benefits of VAT. Every firm, providing

services or dealing in goods must get registered with HMRC, if its VAT taxable turnover is more

than £85,000 (Keen, 2013). On the completion of the process, a registration certificate will be

provided by quoting the VAT number, details about the first return to filed and payment to be

made together with effective date. There are two types of registrations.

1. Compulsory registration- One must register if:

if VAT taxable turnover is expected to be more than £85,000 in the next 30-day period.

In this case, one must get registered by the end of that 30-day period and the effective

date will the date firm realised, not when the turnover exceeded the threshold limit.

If business had a VAT taxable turnover of more than £85,000 over the last 12 months.

The registration has to be done within 30 days of the end of the month when the limited

went over the specified turnover. Effective date in this case will the first day of the

succeeding month when the limit was exceeded (Alm,2012).

Further, a person can register voluntarily even if the turnover is less than above

mentioned limit, provided the goods that are being sold in not “exempted”. A firm can get

registered online, an account will be created. Also, registration can be done through post using:

Form VAT1 if :

1. for registration exception

2. Agricultural Flat Rate Scheme

3. Registering business units or divisions of a body corporate under separate VAT numbers.

There are separate forms available to be sent through post other than the businesses

mentioned above. These are:

1. VAT1A for EU business distance selling to UK

2. VAT2B importing goods having value of more than £85,000 from another EU state.

3. VAT1C on disposing of assets on which 8th or 13th Directive refunds have been claimed.

No registration is required in case, a firm deals only in those goods or services that are

exempt from VAT, provided, the goods worth more than £85,000 must be bought from EU-VAT

registered suppliers only. Also, one may have to get registered for VAT if he take over a VAT

registered business.

A business must be registered to avail the benefits of VAT. Every firm, providing

services or dealing in goods must get registered with HMRC, if its VAT taxable turnover is more

than £85,000 (Keen, 2013). On the completion of the process, a registration certificate will be

provided by quoting the VAT number, details about the first return to filed and payment to be

made together with effective date. There are two types of registrations.

1. Compulsory registration- One must register if:

if VAT taxable turnover is expected to be more than £85,000 in the next 30-day period.

In this case, one must get registered by the end of that 30-day period and the effective

date will the date firm realised, not when the turnover exceeded the threshold limit.

If business had a VAT taxable turnover of more than £85,000 over the last 12 months.

The registration has to be done within 30 days of the end of the month when the limited

went over the specified turnover. Effective date in this case will the first day of the

succeeding month when the limit was exceeded (Alm,2012).

Further, a person can register voluntarily even if the turnover is less than above

mentioned limit, provided the goods that are being sold in not “exempted”. A firm can get

registered online, an account will be created. Also, registration can be done through post using:

Form VAT1 if :

1. for registration exception

2. Agricultural Flat Rate Scheme

3. Registering business units or divisions of a body corporate under separate VAT numbers.

There are separate forms available to be sent through post other than the businesses

mentioned above. These are:

1. VAT1A for EU business distance selling to UK

2. VAT2B importing goods having value of more than £85,000 from another EU state.

3. VAT1C on disposing of assets on which 8th or 13th Directive refunds have been claimed.

No registration is required in case, a firm deals only in those goods or services that are

exempt from VAT, provided, the goods worth more than £85,000 must be bought from EU-VAT

registered suppliers only. Also, one may have to get registered for VAT if he take over a VAT

registered business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1.4 Identify the information that must be included on business documentation of VAT registered

businesses.

According to VAT Act, 1994, a business registered under this Act must keep the records

of sales and purchases, separate summary of VAT called a VAT account and invoices. The

invoice must have VAT registration number and the amount on which tax will be calculated.

Apart from the this, it must contain the name of the party involved in the transaction. Further,

legal structure and address of the firm should also be mentioned along with the Corporate

Identification Number (CIN). These records must be kept for at least 6 years. Further, these can

be maintained on paper, electronically or as a part of software program. These must be accurate,

complete and illegible (Amir and et. al., 2013). In case, a VAT invoice is lost or damaged or no

longer readable, then a duplicate copy can be requested from the supplier on which the word

“duplicate” will be mentioned. The VAT account is maintained for returns. Invoices must be

issued within 30 days of the date of making supply. It is the primary evidence on the basis of

which VAT amount can be claimed.

1.5 Requirements and the frequency of reporting for various VAT schemes.

VAT Act provides various accounting schemes for business in UK. These are for making

the complex system easier to understand and implement. Also, it improves the cash flows of a

business by saving time and money. Basically, these for small retail firms to make accounting for

tax simple. Types of VAT schemes are as follows:

Annual accounting- Under this scheme, businesses are required to file the return

and make payment on annual basis. There is no need to file quarterly returns. This

method enables the firms to prepared budget with more attention. It minimize the

paperwork and it easy to manage the cash flow. Since, it is to be annually, there

may arise circumstances of over-paying or under-paying of tax, therefore, entities

may required to make a payment or apply for refund (Mathur and Morris, 2014).

Cash accounting- While using this scheme, VAT is to be calculated from the

date when the firm is being paid in contrast to the date of issuing the invoice. It is

useful in those case, where there is delay in payments. It is suitable for the

business buying huge quantity goods on credit. One condition under this scheme,

is that VAT can be claimed only when the company has been paid completely. It

businesses.

According to VAT Act, 1994, a business registered under this Act must keep the records

of sales and purchases, separate summary of VAT called a VAT account and invoices. The

invoice must have VAT registration number and the amount on which tax will be calculated.

Apart from the this, it must contain the name of the party involved in the transaction. Further,

legal structure and address of the firm should also be mentioned along with the Corporate

Identification Number (CIN). These records must be kept for at least 6 years. Further, these can

be maintained on paper, electronically or as a part of software program. These must be accurate,

complete and illegible (Amir and et. al., 2013). In case, a VAT invoice is lost or damaged or no

longer readable, then a duplicate copy can be requested from the supplier on which the word

“duplicate” will be mentioned. The VAT account is maintained for returns. Invoices must be

issued within 30 days of the date of making supply. It is the primary evidence on the basis of

which VAT amount can be claimed.

1.5 Requirements and the frequency of reporting for various VAT schemes.

VAT Act provides various accounting schemes for business in UK. These are for making

the complex system easier to understand and implement. Also, it improves the cash flows of a

business by saving time and money. Basically, these for small retail firms to make accounting for

tax simple. Types of VAT schemes are as follows:

Annual accounting- Under this scheme, businesses are required to file the return

and make payment on annual basis. There is no need to file quarterly returns. This

method enables the firms to prepared budget with more attention. It minimize the

paperwork and it easy to manage the cash flow. Since, it is to be annually, there

may arise circumstances of over-paying or under-paying of tax, therefore, entities

may required to make a payment or apply for refund (Mathur and Morris, 2014).

Cash accounting- While using this scheme, VAT is to be calculated from the

date when the firm is being paid in contrast to the date of issuing the invoice. It is

useful in those case, where there is delay in payments. It is suitable for the

business buying huge quantity goods on credit. One condition under this scheme,

is that VAT can be claimed only when the company has been paid completely. It

can be used by only if the turnover of the business is not expected to go beyond

the specified limit i.e. £1.35million (Schenk and et. al., 2015).

Flat-rate scheme- This accounting scheme can be opted by the businesses having

turnover less than £150,000. Under this, the VAT amount calculated and to be

paid is a percentage of the total turnover. There are different flat rates for different

sectors. However, there is no need to keep VAT record on every purchase or sale.

It is suitable for small firms.

Standard scheme- The VAT return is to be filed in the quarter in which the

invoice is received or issued irrespective of the whether the payment has been

made or received, respectively in individual and different quarter. In nutshell,

firms are required to file quarterly returns and the amounts are claimed in the

respective quarter. However, it is granted only when tax paid is more than the

payable amount.

1.6 Maintain an up-to-date knowledge of changes to codes of practice, regulation or legislation.

Government form Act, rules, code of conduct, legislation for the betterment of firms. A

business must abide by these for carrying its activities without any hindrance. Also, the laws and

rules are amended to have better control and improve the VAT system in the country. Entities

must be aware of such amendments (Collins, 2013). Keeping up to date information of code of

conduct and various applicable legislation provides great efficiency in business dealings.

Further, the intervention of government is reduced, if a business follow the exiting laws and code

of practice along with changes made. Adhering to the updated data will not only help the

businesses regarding taxation part but also it will impact other departments. For example, the

entity will maintain all the accounting records in proper way to claim and avoid any penalties.

TASK 2

2.1 Extract relevant data for a specified data for a specific period from the accounting system.

Example 1- Moon Realty, a VAT registered company, is leasing its 20-door residential

commercial apartment in the following manner:

The 1st 10 units are being used by commercial establishments and being rented for

£13,200 per month while at the back is another 10-door apartment being used as residential and

being rented for £8,000 per month per door. The company for the last month incurred expenses

the specified limit i.e. £1.35million (Schenk and et. al., 2015).

Flat-rate scheme- This accounting scheme can be opted by the businesses having

turnover less than £150,000. Under this, the VAT amount calculated and to be

paid is a percentage of the total turnover. There are different flat rates for different

sectors. However, there is no need to keep VAT record on every purchase or sale.

It is suitable for small firms.

Standard scheme- The VAT return is to be filed in the quarter in which the

invoice is received or issued irrespective of the whether the payment has been

made or received, respectively in individual and different quarter. In nutshell,

firms are required to file quarterly returns and the amounts are claimed in the

respective quarter. However, it is granted only when tax paid is more than the

payable amount.

1.6 Maintain an up-to-date knowledge of changes to codes of practice, regulation or legislation.

Government form Act, rules, code of conduct, legislation for the betterment of firms. A

business must abide by these for carrying its activities without any hindrance. Also, the laws and

rules are amended to have better control and improve the VAT system in the country. Entities

must be aware of such amendments (Collins, 2013). Keeping up to date information of code of

conduct and various applicable legislation provides great efficiency in business dealings.

Further, the intervention of government is reduced, if a business follow the exiting laws and code

of practice along with changes made. Adhering to the updated data will not only help the

businesses regarding taxation part but also it will impact other departments. For example, the

entity will maintain all the accounting records in proper way to claim and avoid any penalties.

TASK 2

2.1 Extract relevant data for a specified data for a specific period from the accounting system.

Example 1- Moon Realty, a VAT registered company, is leasing its 20-door residential

commercial apartment in the following manner:

The 1st 10 units are being used by commercial establishments and being rented for

£13,200 per month while at the back is another 10-door apartment being used as residential and

being rented for £8,000 per month per door. The company for the last month incurred expenses

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

based on actual receipts in the amount £60,000 of which £49,000 comes from VAT registered

suppliers. Based on the above data compute the following: (5%)

a. Output tax for last month

b. Input tax for last month

c. VAT payable for the last month

Example 2- John will start trading in the coming months. He has SUV car and is

considering three alternative types of business. These are; (a) training, in which all sales will be

standard rated for VAT, (b) transport, the sales will be charged at zero rate for VAT and (c) as an

ambulance, in which all sales will be exempt.

For each alternative, the sales will be £70,000 per month (exclusive of VAT), and

standard rated expenses will be £10,000 per month (inclusive of VAT).

2.2 Calculations of VAT

Solution 1-

a. Output tax for the month

10* £13,200

Output tax = --------------------* 12% = £14,142.86

112% or 1.12

b. Input tax

£49,000

Input tax = -----------------------* 12% = £5,250.00

112% or 1.12%

c. Vat payable = £14,142.86 - £5,250 = £8,892.86

Solution 2- Standard rated supplies

It is mandatory for John to get registered for as he is making taxable supplies.

Output tax of will be

= £ 80,000*20% = £14,000

Input tax :

= £10,000*20/120 = £1667

Zero rated supplies:

John is eligible to claim exemption from VAT registration because he is making zero-

rated supplies, otherwise, he should still register as these fall under taxable category.

suppliers. Based on the above data compute the following: (5%)

a. Output tax for last month

b. Input tax for last month

c. VAT payable for the last month

Example 2- John will start trading in the coming months. He has SUV car and is

considering three alternative types of business. These are; (a) training, in which all sales will be

standard rated for VAT, (b) transport, the sales will be charged at zero rate for VAT and (c) as an

ambulance, in which all sales will be exempt.

For each alternative, the sales will be £70,000 per month (exclusive of VAT), and

standard rated expenses will be £10,000 per month (inclusive of VAT).

2.2 Calculations of VAT

Solution 1-

a. Output tax for the month

10* £13,200

Output tax = --------------------* 12% = £14,142.86

112% or 1.12

b. Input tax

£49,000

Input tax = -----------------------* 12% = £5,250.00

112% or 1.12%

c. Vat payable = £14,142.86 - £5,250 = £8,892.86

Solution 2- Standard rated supplies

It is mandatory for John to get registered for as he is making taxable supplies.

Output tax of will be

= £ 80,000*20% = £14,000

Input tax :

= £10,000*20/120 = £1667

Zero rated supplies:

John is eligible to claim exemption from VAT registration because he is making zero-

rated supplies, otherwise, he should still register as these fall under taxable category.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Output tax will not be due, but input tax is recoverable.

Exempt supplies:

Since, John is not dealing in taxable items, VAT registration is not required.

Output VAT will not be due and input VAT will not be recoverable.

Exports:

If goods are exported outside EU, then no VAT will be charged. VAT is for goods dealt

in European Union. It can be imposed with zero rate to enable firms to claim refunds.

2.3 Calculate the VAT due to, or from, the relevant tax authority.

Amount due is the difference between the tax amount paid is more than the payment

previously made. By taking the above examples, amount due to or from the relevant government

will done in this way:

Standard supplies- The HMRC provides a standard rate which is used in general and the

rate is 20%. In example 1, the VAT payable to government is £8,892 and in 2nd example, it is

£1,667.

Zero-rated supplies: It includes goods that are charged at zero rate. Only John will have

to pay £1,667 to the HMRC department.

Exempt supplies: No tax is required to be paid as goods are exempt. Also, no benefit of

refund will be provided.

Exempt supplies:

Since, John is not dealing in taxable items, VAT registration is not required.

Output VAT will not be due and input VAT will not be recoverable.

Exports:

If goods are exported outside EU, then no VAT will be charged. VAT is for goods dealt

in European Union. It can be imposed with zero rate to enable firms to claim refunds.

2.3 Calculate the VAT due to, or from, the relevant tax authority.

Amount due is the difference between the tax amount paid is more than the payment

previously made. By taking the above examples, amount due to or from the relevant government

will done in this way:

Standard supplies- The HMRC provides a standard rate which is used in general and the

rate is 20%. In example 1, the VAT payable to government is £8,892 and in 2nd example, it is

£1,667.

Zero-rated supplies: It includes goods that are charged at zero rate. Only John will have

to pay £1,667 to the HMRC department.

Exempt supplies: No tax is required to be paid as goods are exempt. Also, no benefit of

refund will be provided.

2.4 Submit a VAT return and any associated payment within the statutory time limit.

TASK 3

3.1 Explain the implications and penalties for an organisation resulting from failure to abide by

VAT regulations.

The Value Added Tax Act, 1994, provides the laws that are required to be abide by the

VAT registered firms. A contravention in the provisions by businesses will lead the entities to

pay the penalties. Some of the basic penalties that are common for all businesses irrespective of

turnover or size are as follows:

1. in case of delay in the filing of VAT return or tax payment, the payer is warned for the

first time. In case of default being continued, a surcharge liability notice will be served to

the taxpayer for a period of 12 months, granting trial. If he fails to meets the

TASK 3

3.1 Explain the implications and penalties for an organisation resulting from failure to abide by

VAT regulations.

The Value Added Tax Act, 1994, provides the laws that are required to be abide by the

VAT registered firms. A contravention in the provisions by businesses will lead the entities to

pay the penalties. Some of the basic penalties that are common for all businesses irrespective of

turnover or size are as follows:

1. in case of delay in the filing of VAT return or tax payment, the payer is warned for the

first time. In case of default being continued, a surcharge liability notice will be served to

the taxpayer for a period of 12 months, granting trial. If he fails to meets the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

requirements of the served notice, a surcharge @2% will be charged, which will be

increased to 5%, 10% or 15% if the mistake subsist.

2. Timely registration is important to avoid the penalty. The penalty in such case will be

@5% if registration is delayed by 9 months. 10% will be charged, in case of delay for 9

to 18 months and beyond 18 months, 15% will be charged as penalty. This will be

calculated on the VAT due (Kalotay, 2012).

The circumstances where, a firm attracts penalty can range from not getting registered

even when threshold limit has been exceeded or when it breaches rules or laws. It is compulsory

for every business to comply the legislation for saving the costs being incurred in the legal

consequences. Also, it increases the creditworthiness of the company.

3.2 Adjustments and declarations for any errors or omissions identified in previous VAT periods.

Errors or omissions can be avoided by recoding the details carefully. VAT Act and rules

provide the adjustments in which these can be corrected if made in the previous VAT returns.

However, it can be made right only if they are:

1. below the prescribed reporting threshold limit

2. the errors or mistakes were unintentional or done unknowingly

3. for an accounting period that ends less than 4 years ago.

When the amount of the error is £10,000 or less, then the adjustments that can be made

comes under reporting threshold. Details of error is submitted in a report in the form VAT652

and it is send to the error correction team. After this, a notice is issued by HMRC to the applicant

specifying the tax or interest amount liability of the firms. Further, it provides two methods by

which errors can be corrected. They are:

Method 1: If the errors of a net value do not exceed £10,000 or net value is between

£10,000 to £50,000 but do not exceed 1% of the net output in the VAT return period.

Method 2: This method is applicable if the errors of a net value are between £10,000 to

£50,000 and that can not exceed more £50,00,000.

TASK 4

4.1 Impact of VAT payment on organization's cash flow and financial forecasts.

In the indirect tax, although the burden of tax is shifted to another person, then also its

affects the financial and cash flow of an organization negatively. Businesses provides goods on

increased to 5%, 10% or 15% if the mistake subsist.

2. Timely registration is important to avoid the penalty. The penalty in such case will be

@5% if registration is delayed by 9 months. 10% will be charged, in case of delay for 9

to 18 months and beyond 18 months, 15% will be charged as penalty. This will be

calculated on the VAT due (Kalotay, 2012).

The circumstances where, a firm attracts penalty can range from not getting registered

even when threshold limit has been exceeded or when it breaches rules or laws. It is compulsory

for every business to comply the legislation for saving the costs being incurred in the legal

consequences. Also, it increases the creditworthiness of the company.

3.2 Adjustments and declarations for any errors or omissions identified in previous VAT periods.

Errors or omissions can be avoided by recoding the details carefully. VAT Act and rules

provide the adjustments in which these can be corrected if made in the previous VAT returns.

However, it can be made right only if they are:

1. below the prescribed reporting threshold limit

2. the errors or mistakes were unintentional or done unknowingly

3. for an accounting period that ends less than 4 years ago.

When the amount of the error is £10,000 or less, then the adjustments that can be made

comes under reporting threshold. Details of error is submitted in a report in the form VAT652

and it is send to the error correction team. After this, a notice is issued by HMRC to the applicant

specifying the tax or interest amount liability of the firms. Further, it provides two methods by

which errors can be corrected. They are:

Method 1: If the errors of a net value do not exceed £10,000 or net value is between

£10,000 to £50,000 but do not exceed 1% of the net output in the VAT return period.

Method 2: This method is applicable if the errors of a net value are between £10,000 to

£50,000 and that can not exceed more £50,00,000.

TASK 4

4.1 Impact of VAT payment on organization's cash flow and financial forecasts.

In the indirect tax, although the burden of tax is shifted to another person, then also its

affects the financial and cash flow of an organization negatively. Businesses provides goods on

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

credit to customers and it takes time to realise the amount. It is calculated on the sales made even

if the payment has not been received. Meanwhile, VAT has to be paid on quarterly basis. The

This affect the cash flow because the outflow of cash is more than inflow in form of tax. Further,

the solvency becomes difficult when the company has to pay VAT before even receiving the

payment. It also impact the finance and budgets when taxes paid exceeds the amount realised

because of which the chances of its suimplications and penalties for an organisation resulting

from failure to abide brvival gets influenced in the long-term (Karakosta and et. al., 2014).

4.2 Advise relevant people of changes in VAT legislation which would have an effect on an

organization's recording systems.

The investors of an organization is interested in knowing the financial standing of the

company. Hence, details of calculations including the VAT are shown in those statements. Also,

it is used by the government for taxation purpose. Any changes in the VAT Act and rules will

affect the whole procedure of the organization that it uses in maintaining for recording

transaction. The firm will have to adapt the change and conduct its business accordingly, by

complying with the businesses. Such changes are taken care by accountants and taxation

department in an entity. They will notify the company about any difference between the old and

new method so that it does not face difficulties in future and costs can be saved. Along with this,

businesses should be aware of the amendments made by the government in the laws so that such

changes are accepted without causing delay.

CONCLUSION

From the above report, it has been concluded that indirect tax is applicable on the

businesses dealings in goods and services. Further, the tax burden can be shifted to another

person. VAT registration is compulsory for the firms, who has exceeded the threshold limits. The

regulations are followed to get the benefit of return and also, businesses should files the returns

within the prescribed statutory limit to avoid any penalty. Further, they should know about the

impact VAT leaves on financial and cash flow in order to save itself from any distressing

situations and to maintain a balance in its activities for sustainable growth.

if the payment has not been received. Meanwhile, VAT has to be paid on quarterly basis. The

This affect the cash flow because the outflow of cash is more than inflow in form of tax. Further,

the solvency becomes difficult when the company has to pay VAT before even receiving the

payment. It also impact the finance and budgets when taxes paid exceeds the amount realised

because of which the chances of its suimplications and penalties for an organisation resulting

from failure to abide brvival gets influenced in the long-term (Karakosta and et. al., 2014).

4.2 Advise relevant people of changes in VAT legislation which would have an effect on an

organization's recording systems.

The investors of an organization is interested in knowing the financial standing of the

company. Hence, details of calculations including the VAT are shown in those statements. Also,

it is used by the government for taxation purpose. Any changes in the VAT Act and rules will

affect the whole procedure of the organization that it uses in maintaining for recording

transaction. The firm will have to adapt the change and conduct its business accordingly, by

complying with the businesses. Such changes are taken care by accountants and taxation

department in an entity. They will notify the company about any difference between the old and

new method so that it does not face difficulties in future and costs can be saved. Along with this,

businesses should be aware of the amendments made by the government in the laws so that such

changes are accepted without causing delay.

CONCLUSION

From the above report, it has been concluded that indirect tax is applicable on the

businesses dealings in goods and services. Further, the tax burden can be shifted to another

person. VAT registration is compulsory for the firms, who has exceeded the threshold limits. The

regulations are followed to get the benefit of return and also, businesses should files the returns

within the prescribed statutory limit to avoid any penalty. Further, they should know about the

impact VAT leaves on financial and cash flow in order to save itself from any distressing

situations and to maintain a balance in its activities for sustainable growth.

REFERENCES

Books and journals:

Acosta‐Ormaechea and et. al., 2012. Tax Composition and Growth: A Broad Cross‐Country

Perspective. German Economic Review.

Alm, J., 2012. Measuring, explaining, and controlling tax evasion: lessons from theory,

experiments, and field studies. International Tax and Public Finance. 19(1). pp.54-77.

Amir and et. al., 2013. The impact of the Indonesian income tax reform: A CGE analysis.

Economic Modelling. 31. pp.492-501.

Collins, M., 2013. Estimating the direct and indirect tax contributions of households in ireland.

Kalotay, K., 2012. Indirect FDI. The Journal of World Investment & Trade. 13(4). pp.542-555.

Karakosta and et. al., 2014. Indirect tax harmonization and global public goods. International

Tax and Public Finance. 21(1). pp.29-49.

Keen, M. M., 2013. Targeting, cascading, and indirect tax design (No. 13-57). International

Monetary Fund.

Mathur, A. and Morris, A.C., 2014. Distributional effects of a carbon tax in broader US fiscal

reform. Energy Policy. 66. pp.326-334.

Schenk and et. al., 2015. Value added tax. Cambridge University Press.

Online:

Overview of digitalization of tax under HMRC. 2018. [Online]. Available through:

<https://www.gov.uk/government/publications/making-tax-digital/overview-of-making-

tax-digital>.

Books and journals:

Acosta‐Ormaechea and et. al., 2012. Tax Composition and Growth: A Broad Cross‐Country

Perspective. German Economic Review.

Alm, J., 2012. Measuring, explaining, and controlling tax evasion: lessons from theory,

experiments, and field studies. International Tax and Public Finance. 19(1). pp.54-77.

Amir and et. al., 2013. The impact of the Indonesian income tax reform: A CGE analysis.

Economic Modelling. 31. pp.492-501.

Collins, M., 2013. Estimating the direct and indirect tax contributions of households in ireland.

Kalotay, K., 2012. Indirect FDI. The Journal of World Investment & Trade. 13(4). pp.542-555.

Karakosta and et. al., 2014. Indirect tax harmonization and global public goods. International

Tax and Public Finance. 21(1). pp.29-49.

Keen, M. M., 2013. Targeting, cascading, and indirect tax design (No. 13-57). International

Monetary Fund.

Mathur, A. and Morris, A.C., 2014. Distributional effects of a carbon tax in broader US fiscal

reform. Energy Policy. 66. pp.326-334.

Schenk and et. al., 2015. Value added tax. Cambridge University Press.

Online:

Overview of digitalization of tax under HMRC. 2018. [Online]. Available through:

<https://www.gov.uk/government/publications/making-tax-digital/overview-of-making-

tax-digital>.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.