Indirect Tax: VAT Regulations and Reporting in the UK

VerifiedAdded on 2020/12/26

|15

|4151

|418

Report

AI Summary

This report provides a detailed overview of Value Added Tax (VAT) regulations and practices within the United Kingdom. It begins with an introduction to indirect taxes and the concept of VAT, emphasizing its role in the UK's taxation system. The report then delves into the sources of information on VAT, including the HMRC website and other channels, and explains how organizations should interact with the relevant government agencies. It covers VAT registration requirements, the information that must be included on business documentation, and various VAT schemes such as annual accounting, cash accounting, flat rate, and standard schemes. The report further discusses maintaining up-to-date knowledge of changes to codes of practice, regulations, or legislation. It includes practical examples of calculating VAT due, completing VAT returns, and addressing VAT penalties and errors. The report also addresses the impact of VAT payments on an organization's cash flow and financial forecasts, as well as the importance of communicating VAT information to relevant parties. The report concludes with a summary of the key findings and a list of references used in the report.

Indirect tax

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

Understand VAT regulation........................................................................................................3

1.1 Identify sources of information on VAT...............................................................................3

1.2 Explain how an organisation should interact with the relevant government agency............4

1.3 Explain VAT registration requirements................................................................................4

1.4 Identify the information that must be included on business documentation of VAT

registered businesses...................................................................................................................5

1.5 Explanation over requirements and the frequency of reporting for these VAT schemes.....6

1.6 Maintain an up-to-date knowledge of changes to codes of practice, regulation or

legislation....................................................................................................................................6

Complete VAT returns accurately and in a timely manner.........................................................7

2.3 Calculate the VAT due to, or from, the relevant tax authority.............................................8

2.4 Completion of VAT return and any associated payment within the statutory time limits...9

Understand VAT penalties and make adjustments for previous errors.......................................9

3.1 Explain the implications and penalties for an organisation resulting from failure to abide

by VAT regulations.....................................................................................................................9

3.2 Make adjustments and declarations for any errors or omissions identified in previous VAT

periods.......................................................................................................................................10

Communicate VAT information...............................................................................................11

4.1 Critical analysis of an impacts of VAT payment on the organisation’s cash flow and

financial forecasts......................................................................................................................11

4.2 Advise relevant people for changes into the VAT legislation............................................11

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................3

Understand VAT regulation........................................................................................................3

1.1 Identify sources of information on VAT...............................................................................3

1.2 Explain how an organisation should interact with the relevant government agency............4

1.3 Explain VAT registration requirements................................................................................4

1.4 Identify the information that must be included on business documentation of VAT

registered businesses...................................................................................................................5

1.5 Explanation over requirements and the frequency of reporting for these VAT schemes.....6

1.6 Maintain an up-to-date knowledge of changes to codes of practice, regulation or

legislation....................................................................................................................................6

Complete VAT returns accurately and in a timely manner.........................................................7

2.3 Calculate the VAT due to, or from, the relevant tax authority.............................................8

2.4 Completion of VAT return and any associated payment within the statutory time limits...9

Understand VAT penalties and make adjustments for previous errors.......................................9

3.1 Explain the implications and penalties for an organisation resulting from failure to abide

by VAT regulations.....................................................................................................................9

3.2 Make adjustments and declarations for any errors or omissions identified in previous VAT

periods.......................................................................................................................................10

Communicate VAT information...............................................................................................11

4.1 Critical analysis of an impacts of VAT payment on the organisation’s cash flow and

financial forecasts......................................................................................................................11

4.2 Advise relevant people for changes into the VAT legislation............................................11

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

Indirect tax is a tax, which basically levied on goods & services rather than on income or

profits. This tax is an amount which is collected by an intermediary from the person who bears

the ultimate economic burden of the tax. Such indirect tax involves the custom duties levied on

imports, excise duty on production, sales tax, value added tax(VAT) etc. which involves transfer

of amount from one person to another (Keen, 2013). This report will focus on concept of VAT

and its various practices related to it. Also, report will talk over taxation system in the entire

United Kingdom, which will put light on identifying the sources of information of VAT, how an

organisation should interact with relevant government agencies. This assessment will clearly talk

about registration of VAT and various requirements includes documents and other information.

Also, the report will cover updated knowledge of changes which took place regarding code of

practice, regulation or legislation etc. Lastly, this report will talk about implication and penalties

for business entities resulted from failure to follow VAT regulations.

Understand VAT regulation

1.1 Identify sources of information on VAT

It is valuable & profitable to get the right sources of information/data regarding the VAT

collection. In United Kingdom, VAT collection is facilitated by proper IT infrastructure & also

by the support of various government entities. The HMRC pages of the UK government website

www.gov.uk is the major source of information covering all the taxes, where advisable data/info,

guidance and publication are available to download (Cloisonnes, 2017). HMRC usually expects

taxpayers to find the answers to any queries on their website, however there is a telephone

enquiry line and web chat facility that can deal with unanswered problems. Taxpayers can also

the online enquiry website or form or write to HMRC by post for advice or information on VAT

collection. Also, people can get exact knowledge of VAT to be paid through paying nominal

amount of 3 pounds to assess right amount of VAT they needs to pay during the financial years.

Also, these sources are highly protected & sustained through password shield and cyber

protection. These sources consists of tax levied on purchasing of any value addition products,

reveals how much is being to be paid along with quarterly basis payment.

Indirect tax is a tax, which basically levied on goods & services rather than on income or

profits. This tax is an amount which is collected by an intermediary from the person who bears

the ultimate economic burden of the tax. Such indirect tax involves the custom duties levied on

imports, excise duty on production, sales tax, value added tax(VAT) etc. which involves transfer

of amount from one person to another (Keen, 2013). This report will focus on concept of VAT

and its various practices related to it. Also, report will talk over taxation system in the entire

United Kingdom, which will put light on identifying the sources of information of VAT, how an

organisation should interact with relevant government agencies. This assessment will clearly talk

about registration of VAT and various requirements includes documents and other information.

Also, the report will cover updated knowledge of changes which took place regarding code of

practice, regulation or legislation etc. Lastly, this report will talk about implication and penalties

for business entities resulted from failure to follow VAT regulations.

Understand VAT regulation

1.1 Identify sources of information on VAT

It is valuable & profitable to get the right sources of information/data regarding the VAT

collection. In United Kingdom, VAT collection is facilitated by proper IT infrastructure & also

by the support of various government entities. The HMRC pages of the UK government website

www.gov.uk is the major source of information covering all the taxes, where advisable data/info,

guidance and publication are available to download (Cloisonnes, 2017). HMRC usually expects

taxpayers to find the answers to any queries on their website, however there is a telephone

enquiry line and web chat facility that can deal with unanswered problems. Taxpayers can also

the online enquiry website or form or write to HMRC by post for advice or information on VAT

collection. Also, people can get exact knowledge of VAT to be paid through paying nominal

amount of 3 pounds to assess right amount of VAT they needs to pay during the financial years.

Also, these sources are highly protected & sustained through password shield and cyber

protection. These sources consists of tax levied on purchasing of any value addition products,

reveals how much is being to be paid along with quarterly basis payment.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

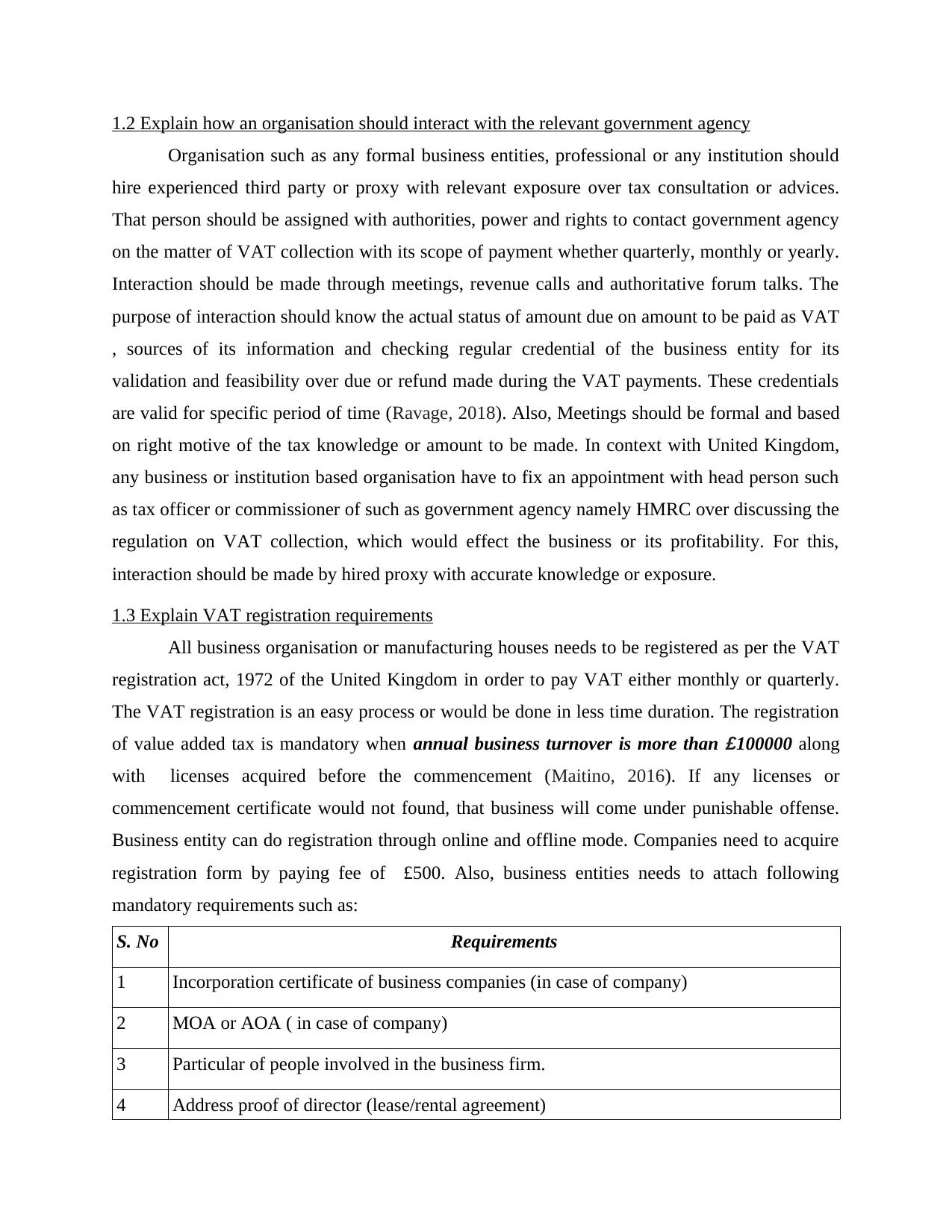

1.2 Explain how an organisation should interact with the relevant government agency

Organisation such as any formal business entities, professional or any institution should

hire experienced third party or proxy with relevant exposure over tax consultation or advices.

That person should be assigned with authorities, power and rights to contact government agency

on the matter of VAT collection with its scope of payment whether quarterly, monthly or yearly.

Interaction should be made through meetings, revenue calls and authoritative forum talks. The

purpose of interaction should know the actual status of amount due on amount to be paid as VAT

, sources of its information and checking regular credential of the business entity for its

validation and feasibility over due or refund made during the VAT payments. These credentials

are valid for specific period of time (Ravage, 2018). Also, Meetings should be formal and based

on right motive of the tax knowledge or amount to be made. In context with United Kingdom,

any business or institution based organisation have to fix an appointment with head person such

as tax officer or commissioner of such as government agency namely HMRC over discussing the

regulation on VAT collection, which would effect the business or its profitability. For this,

interaction should be made by hired proxy with accurate knowledge or exposure.

1.3 Explain VAT registration requirements

All business organisation or manufacturing houses needs to be registered as per the VAT

registration act, 1972 of the United Kingdom in order to pay VAT either monthly or quarterly.

The VAT registration is an easy process or would be done in less time duration. The registration

of value added tax is mandatory when annual business turnover is more than £100000 along

with licenses acquired before the commencement (Maitino, 2016). If any licenses or

commencement certificate would not found, that business will come under punishable offense.

Business entity can do registration through online and offline mode. Companies need to acquire

registration form by paying fee of £500. Also, business entities needs to attach following

mandatory requirements such as:

S. No Requirements

1 Incorporation certificate of business companies (in case of company)

2 MOA or AOA ( in case of company)

3 Particular of people involved in the business firm.

4 Address proof of director (lease/rental agreement)

Organisation such as any formal business entities, professional or any institution should

hire experienced third party or proxy with relevant exposure over tax consultation or advices.

That person should be assigned with authorities, power and rights to contact government agency

on the matter of VAT collection with its scope of payment whether quarterly, monthly or yearly.

Interaction should be made through meetings, revenue calls and authoritative forum talks. The

purpose of interaction should know the actual status of amount due on amount to be paid as VAT

, sources of its information and checking regular credential of the business entity for its

validation and feasibility over due or refund made during the VAT payments. These credentials

are valid for specific period of time (Ravage, 2018). Also, Meetings should be formal and based

on right motive of the tax knowledge or amount to be made. In context with United Kingdom,

any business or institution based organisation have to fix an appointment with head person such

as tax officer or commissioner of such as government agency namely HMRC over discussing the

regulation on VAT collection, which would effect the business or its profitability. For this,

interaction should be made by hired proxy with accurate knowledge or exposure.

1.3 Explain VAT registration requirements

All business organisation or manufacturing houses needs to be registered as per the VAT

registration act, 1972 of the United Kingdom in order to pay VAT either monthly or quarterly.

The VAT registration is an easy process or would be done in less time duration. The registration

of value added tax is mandatory when annual business turnover is more than £100000 along

with licenses acquired before the commencement (Maitino, 2016). If any licenses or

commencement certificate would not found, that business will come under punishable offense.

Business entity can do registration through online and offline mode. Companies need to acquire

registration form by paying fee of £500. Also, business entities needs to attach following

mandatory requirements such as:

S. No Requirements

1 Incorporation certificate of business companies (in case of company)

2 MOA or AOA ( in case of company)

3 Particular of people involved in the business firm.

4 Address proof of director (lease/rental agreement)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5 Company or individual PAN card/passport/driving licensees.

6 ID proof of director (passport/driving licensees)

7 In case of partnership, deed will be required

8 Passport size photo of director of the firm

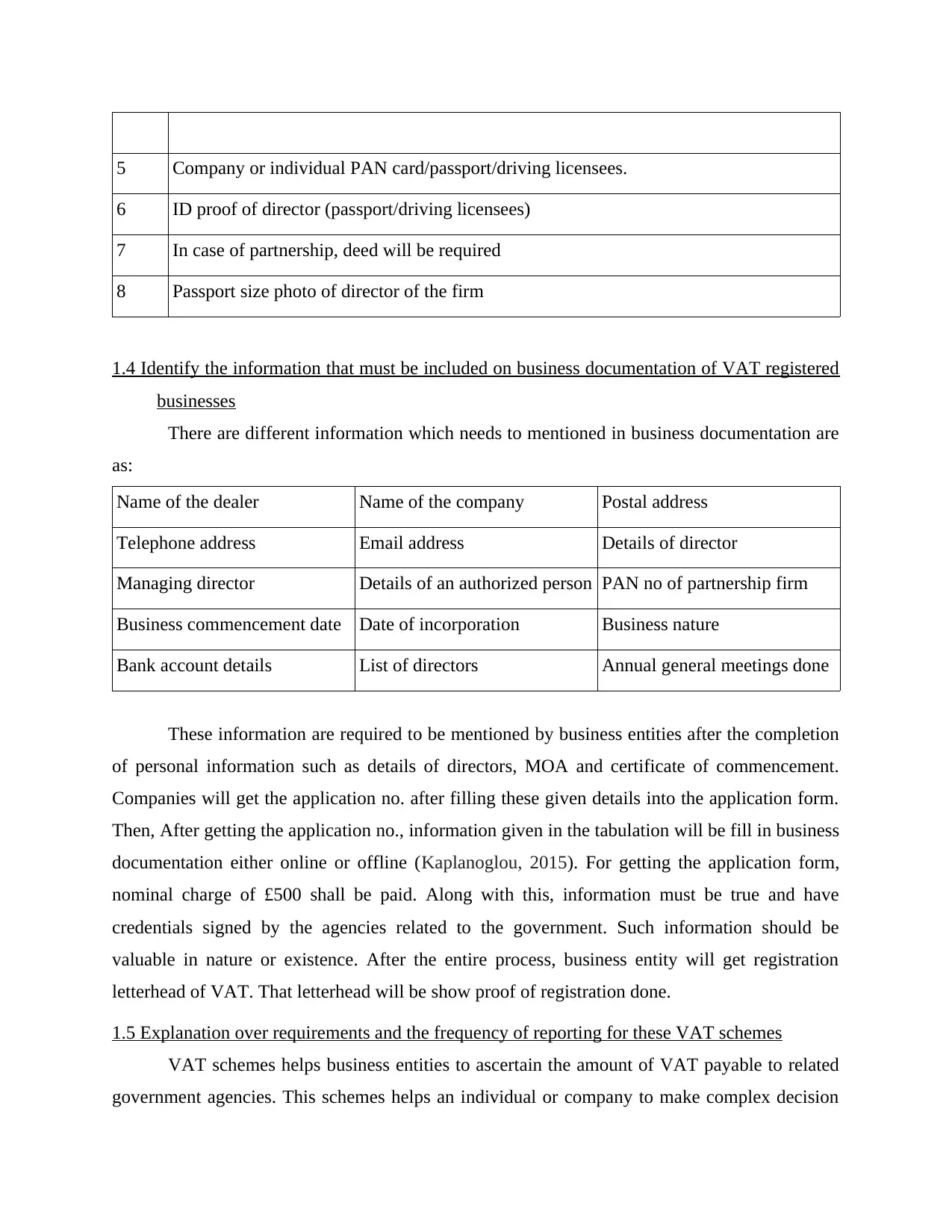

1.4 Identify the information that must be included on business documentation of VAT registered

businesses

There are different information which needs to mentioned in business documentation are

as:

Name of the dealer Name of the company Postal address

Telephone address Email address Details of director

Managing director Details of an authorized person PAN no of partnership firm

Business commencement date Date of incorporation Business nature

Bank account details List of directors Annual general meetings done

These information are required to be mentioned by business entities after the completion

of personal information such as details of directors, MOA and certificate of commencement.

Companies will get the application no. after filling these given details into the application form.

Then, After getting the application no., information given in the tabulation will be fill in business

documentation either online or offline (Kaplanoglou, 2015). For getting the application form,

nominal charge of £500 shall be paid. Along with this, information must be true and have

credentials signed by the agencies related to the government. Such information should be

valuable in nature or existence. After the entire process, business entity will get registration

letterhead of VAT. That letterhead will be show proof of registration done.

1.5 Explanation over requirements and the frequency of reporting for these VAT schemes

VAT schemes helps business entities to ascertain the amount of VAT payable to related

government agencies. This schemes helps an individual or company to make complex decision

6 ID proof of director (passport/driving licensees)

7 In case of partnership, deed will be required

8 Passport size photo of director of the firm

1.4 Identify the information that must be included on business documentation of VAT registered

businesses

There are different information which needs to mentioned in business documentation are

as:

Name of the dealer Name of the company Postal address

Telephone address Email address Details of director

Managing director Details of an authorized person PAN no of partnership firm

Business commencement date Date of incorporation Business nature

Bank account details List of directors Annual general meetings done

These information are required to be mentioned by business entities after the completion

of personal information such as details of directors, MOA and certificate of commencement.

Companies will get the application no. after filling these given details into the application form.

Then, After getting the application no., information given in the tabulation will be fill in business

documentation either online or offline (Kaplanoglou, 2015). For getting the application form,

nominal charge of £500 shall be paid. Along with this, information must be true and have

credentials signed by the agencies related to the government. Such information should be

valuable in nature or existence. After the entire process, business entity will get registration

letterhead of VAT. That letterhead will be show proof of registration done.

1.5 Explanation over requirements and the frequency of reporting for these VAT schemes

VAT schemes helps business entities to ascertain the amount of VAT payable to related

government agencies. This schemes helps an individual or company to make complex decision

making on a matter value added tax clarification towards any problem or issues. Introduction

over these various schemes has to be done with support of administration and remove burden of

accounting to facilitates ease of doing businesses (Ekundayo, 2016). Also, these schemes has

been resulted for small business & manufacturing units to be rid off from burden such as poor

financial position, decreasing revenue as well as improper management etc. To facilitate small

business, various schemes are as follow:

Annual accounting scheme: This scheme has initiated with purpose to make accounting

ease for small business & manufacturing to track their accounting system for assessing VAT

amount. This scheme facilitates suggestion of paying the VAT either instalments or yearly basis

to remove the expected burden.

Cash accounting scheme: This scheme will help small companies to calculate their cash

in hand to remove burden of filling VAT return for strengthen strong financial position. It gives

the maximum priority to cash purchase and sales to eliminate the credit burden to increase profit.

Flat rate scheme: Under this scheme, flat scheme has required to available with business

organisation for simplifying the VAT concept and removal of cascading effect on this indirect

tax., which is tax to be paid on tax. This considers the annual turnover of business for bringing

companies in actual slab rates of this scheme.

Standard scheme: This scheme will provide assurance to the VAT payer over giving

relief such rebate, refunds, discounts etc. This scheme has initiated to provide financial strength

to the tax payers.

1.6 Maintain an up-to-date knowledge of changes to codes of practice, regulation or legislation

In context with United Kingdom, taxation or collection of VAT should be done with

ethical code of conduct with fair practices. It is important to maintain the each and every

data/info related to VAT payer, due amount of VAT to be paid, filling the return etc. All these

practices must be done in accordance with legal ethics mentioned in the UK laws related to

financial aspects (Weber, 2013). When taking about the United Kingdom, legislations has

changed over the period of time, regarding any unethical practices related to VAT collections. In

2016, UK government has comes up with amendments in their Taxation regulation act, 1982

which has been disclosed that, if any company founded in any illegal indirect taxation practices,

they must be punishable either with higher penalty or case will send to the courts for fair

over these various schemes has to be done with support of administration and remove burden of

accounting to facilitates ease of doing businesses (Ekundayo, 2016). Also, these schemes has

been resulted for small business & manufacturing units to be rid off from burden such as poor

financial position, decreasing revenue as well as improper management etc. To facilitate small

business, various schemes are as follow:

Annual accounting scheme: This scheme has initiated with purpose to make accounting

ease for small business & manufacturing to track their accounting system for assessing VAT

amount. This scheme facilitates suggestion of paying the VAT either instalments or yearly basis

to remove the expected burden.

Cash accounting scheme: This scheme will help small companies to calculate their cash

in hand to remove burden of filling VAT return for strengthen strong financial position. It gives

the maximum priority to cash purchase and sales to eliminate the credit burden to increase profit.

Flat rate scheme: Under this scheme, flat scheme has required to available with business

organisation for simplifying the VAT concept and removal of cascading effect on this indirect

tax., which is tax to be paid on tax. This considers the annual turnover of business for bringing

companies in actual slab rates of this scheme.

Standard scheme: This scheme will provide assurance to the VAT payer over giving

relief such rebate, refunds, discounts etc. This scheme has initiated to provide financial strength

to the tax payers.

1.6 Maintain an up-to-date knowledge of changes to codes of practice, regulation or legislation

In context with United Kingdom, taxation or collection of VAT should be done with

ethical code of conduct with fair practices. It is important to maintain the each and every

data/info related to VAT payer, due amount of VAT to be paid, filling the return etc. All these

practices must be done in accordance with legal ethics mentioned in the UK laws related to

financial aspects (Weber, 2013). When taking about the United Kingdom, legislations has

changed over the period of time, regarding any unethical practices related to VAT collections. In

2016, UK government has comes up with amendments in their Taxation regulation act, 1982

which has been disclosed that, if any company founded in any illegal indirect taxation practices,

they must be punishable either with higher penalty or case will send to the courts for fair

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

decision making. It was noticed that illegal code of practice has been reduced and favourable

regulations has arrived (Akhor, 2015). Currently, UK government is under serious process to

bring effective changes in their money flow system, which is the reason for unethical taxation

practices. This involves the tax theft, paying the amount of VAT by showing less business

turnover etc. Finally, It is necessary to have the true & fair code of conduct for maintaining the

taxation decorum in an effective way.

Complete VAT returns accurately and in a timely manner

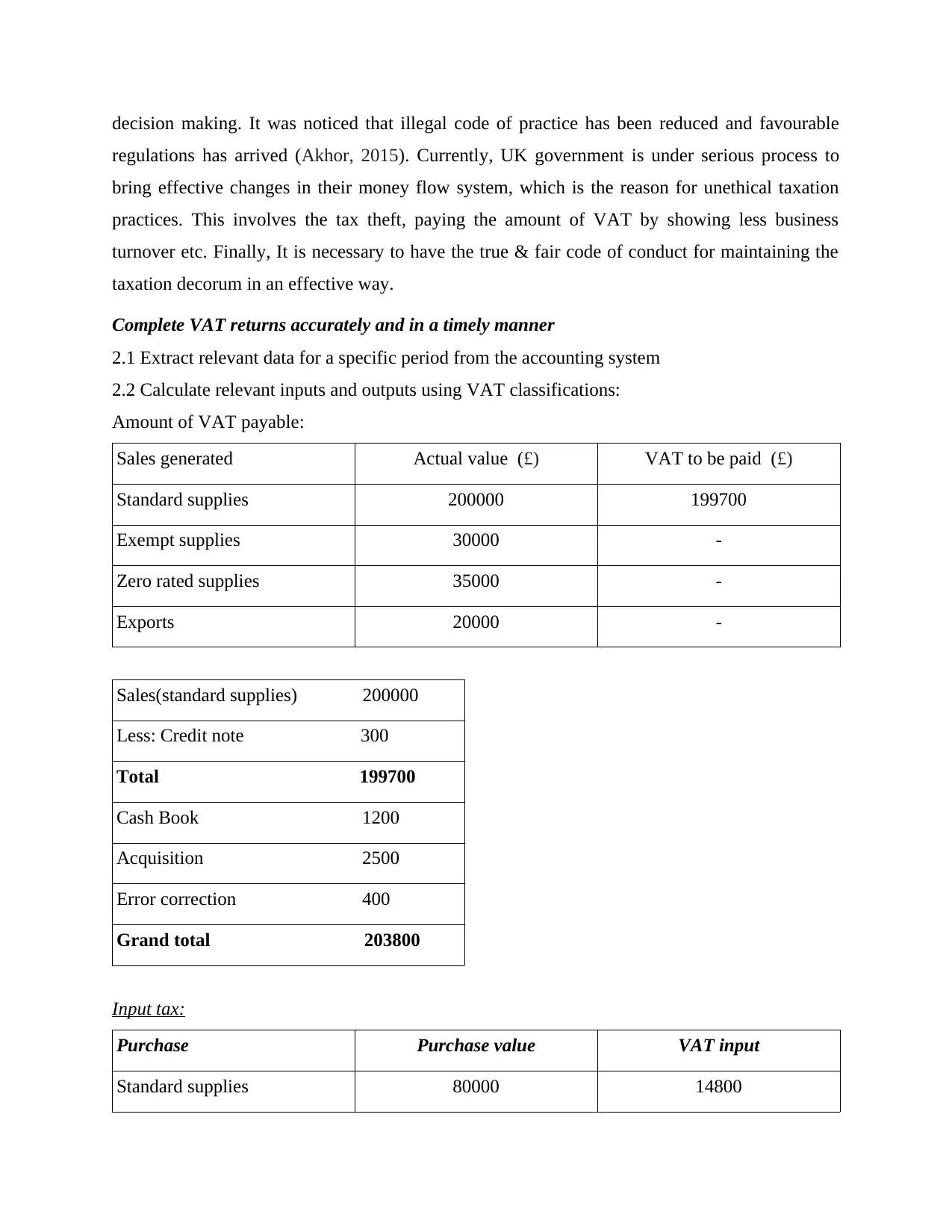

2.1 Extract relevant data for a specific period from the accounting system

2.2 Calculate relevant inputs and outputs using VAT classifications:

Amount of VAT payable:

Sales generated Actual value (£) VAT to be paid (£)

Standard supplies 200000 199700

Exempt supplies 30000 -

Zero rated supplies 35000 -

Exports 20000 -

Sales(standard supplies) 200000

Less: Credit note 300

Total 199700

Cash Book 1200

Acquisition 2500

Error correction 400

Grand total 203800

Input tax:

Purchase Purchase value VAT input

Standard supplies 80000 14800

regulations has arrived (Akhor, 2015). Currently, UK government is under serious process to

bring effective changes in their money flow system, which is the reason for unethical taxation

practices. This involves the tax theft, paying the amount of VAT by showing less business

turnover etc. Finally, It is necessary to have the true & fair code of conduct for maintaining the

taxation decorum in an effective way.

Complete VAT returns accurately and in a timely manner

2.1 Extract relevant data for a specific period from the accounting system

2.2 Calculate relevant inputs and outputs using VAT classifications:

Amount of VAT payable:

Sales generated Actual value (£) VAT to be paid (£)

Standard supplies 200000 199700

Exempt supplies 30000 -

Zero rated supplies 35000 -

Exports 20000 -

Sales(standard supplies) 200000

Less: Credit note 300

Total 199700

Cash Book 1200

Acquisition 2500

Error correction 400

Grand total 203800

Input tax:

Purchase Purchase value VAT input

Standard supplies 80000 14800

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

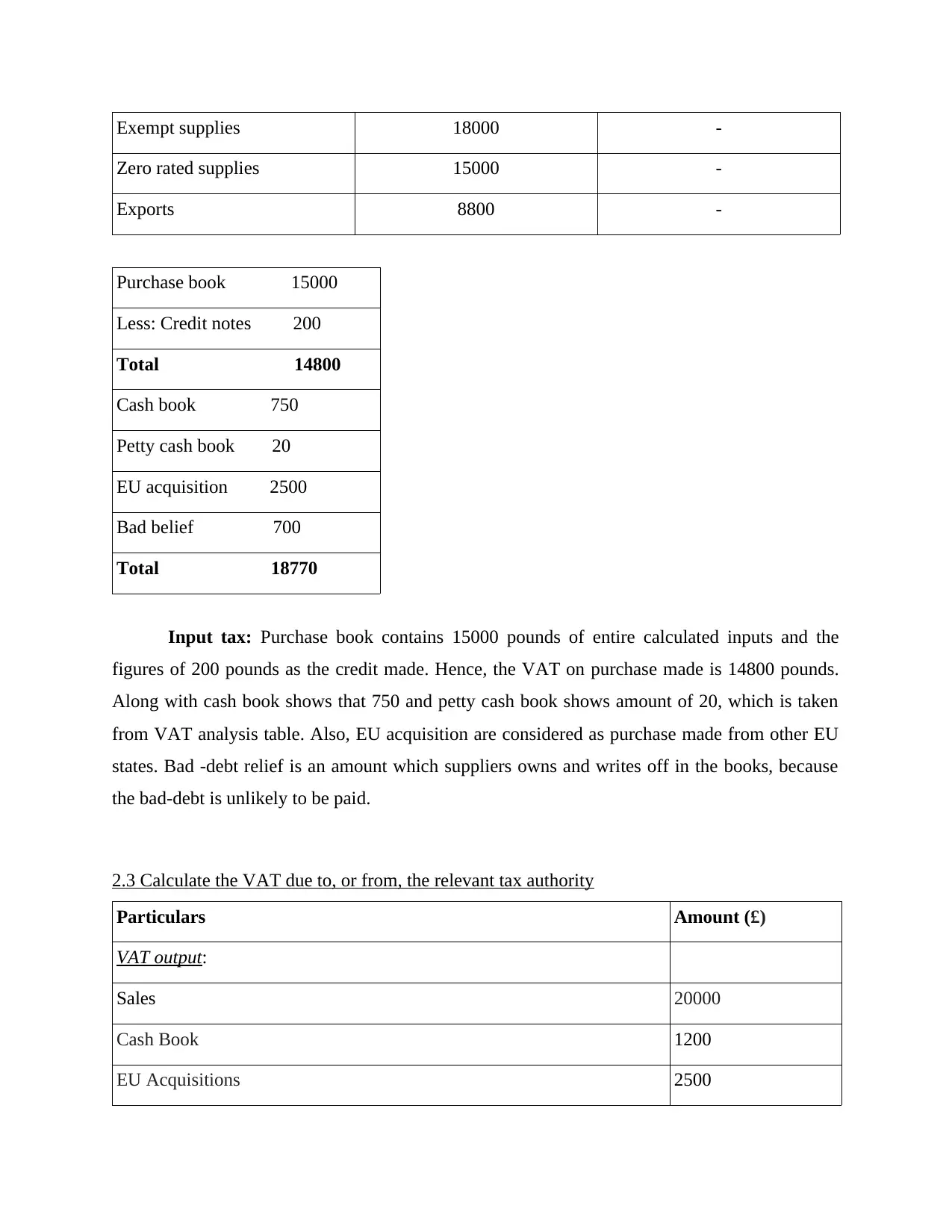

Exempt supplies 18000 -

Zero rated supplies 15000 -

Exports 8800 -

Purchase book 15000

Less: Credit notes 200

Total 14800

Cash book 750

Petty cash book 20

EU acquisition 2500

Bad belief 700

Total 18770

Input tax: Purchase book contains 15000 pounds of entire calculated inputs and the

figures of 200 pounds as the credit made. Hence, the VAT on purchase made is 14800 pounds.

Along with cash book shows that 750 and petty cash book shows amount of 20, which is taken

from VAT analysis table. Also, EU acquisition are considered as purchase made from other EU

states. Bad -debt relief is an amount which suppliers owns and writes off in the books, because

the bad-debt is unlikely to be paid.

2.3 Calculate the VAT due to, or from, the relevant tax authority

Particulars Amount (£)

VAT output:

Sales 20000

Cash Book 1200

EU Acquisitions 2500

Zero rated supplies 15000 -

Exports 8800 -

Purchase book 15000

Less: Credit notes 200

Total 14800

Cash book 750

Petty cash book 20

EU acquisition 2500

Bad belief 700

Total 18770

Input tax: Purchase book contains 15000 pounds of entire calculated inputs and the

figures of 200 pounds as the credit made. Hence, the VAT on purchase made is 14800 pounds.

Along with cash book shows that 750 and petty cash book shows amount of 20, which is taken

from VAT analysis table. Also, EU acquisition are considered as purchase made from other EU

states. Bad -debt relief is an amount which suppliers owns and writes off in the books, because

the bad-debt is unlikely to be paid.

2.3 Calculate the VAT due to, or from, the relevant tax authority

Particulars Amount (£)

VAT output:

Sales 20000

Cash Book 1200

EU Acquisitions 2500

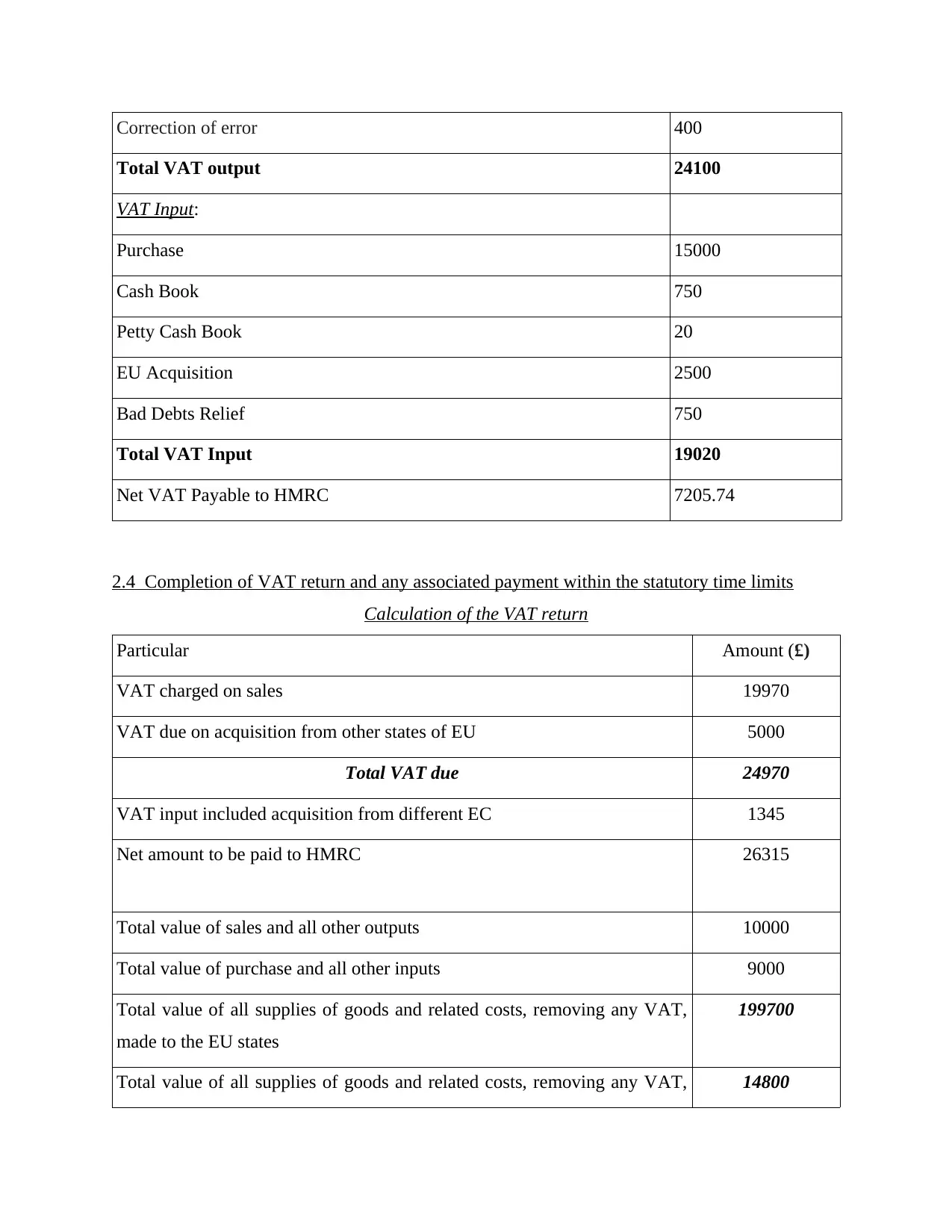

Correction of error 400

Total VAT output 24100

VAT Input:

Purchase 15000

Cash Book 750

Petty Cash Book 20

EU Acquisition 2500

Bad Debts Relief 750

Total VAT Input 19020

Net VAT Payable to HMRC 7205.74

2.4 Completion of VAT return and any associated payment within the statutory time limits

Calculation of the VAT return

Particular Amount (£)

VAT charged on sales 19970

VAT due on acquisition from other states of EU 5000

Total VAT due 24970

VAT input included acquisition from different EC 1345

Net amount to be paid to HMRC 26315

Total value of sales and all other outputs 10000

Total value of purchase and all other inputs 9000

Total value of all supplies of goods and related costs, removing any VAT,

made to the EU states

199700

Total value of all supplies of goods and related costs, removing any VAT, 14800

Total VAT output 24100

VAT Input:

Purchase 15000

Cash Book 750

Petty Cash Book 20

EU Acquisition 2500

Bad Debts Relief 750

Total VAT Input 19020

Net VAT Payable to HMRC 7205.74

2.4 Completion of VAT return and any associated payment within the statutory time limits

Calculation of the VAT return

Particular Amount (£)

VAT charged on sales 19970

VAT due on acquisition from other states of EU 5000

Total VAT due 24970

VAT input included acquisition from different EC 1345

Net amount to be paid to HMRC 26315

Total value of sales and all other outputs 10000

Total value of purchase and all other inputs 9000

Total value of all supplies of goods and related costs, removing any VAT,

made to the EU states

199700

Total value of all supplies of goods and related costs, removing any VAT, 14800

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

from other EU states

Total VAT due amount is £24970 Return will be forward to HMRC on 27th January,

which is due on quarterly basis from date 25 October, 2018. Also, the next due date will be 25

April, 2019 (Peitz, 2014). There is a penalty of 200 pounds, because of 5 days late transaction

enrolment. The Vat will be paid through online banking via HMRC payment id, which was given

previously after the registration made.

Understand VAT penalties and make adjustments for previous errors

3.1 Explain the implications and penalties for an organisation resulting from failure to abide by

VAT regulations

It is necessary to follow the VAT related legislations to make its existence effective and

suitable to generate the revenue for the government. As everyone knows that, taxation is the

main income source of income for government, irrespective of whatever the country resources.

For that, it is necessary to impose several penalties or strict punishments to avoid any informal

practices of the VAT (Reisinger, 2014). In context with United Kingdom, if any business entity

or sole proprietor found guilty in any failure of VAT regulation, hat person will cover under the

category of defaulter. Also, after being declared as defaulter, they will be punishable with huge

fines or penalties. Some cases such as (Robert Martin CC/FS 1, 2015) shows that, if any entity

fails to pay the annual VAT amount, that person will be penalized with fines or punishable

amount, which completely depends on amount of VAT due for the mentioned date (Phillips,

2014). Suppose, entity fails to get registered after getting the application no, they will fine

penalized as certain circumstances:

Conditions Amount of penalties

Register after the one month from the date of

application

£200

Register after two months £300

Implication of these penalties would effect legal existence or credential of the business

entities. Also, these punishable offense would destroy the image of the business image or they

Total VAT due amount is £24970 Return will be forward to HMRC on 27th January,

which is due on quarterly basis from date 25 October, 2018. Also, the next due date will be 25

April, 2019 (Peitz, 2014). There is a penalty of 200 pounds, because of 5 days late transaction

enrolment. The Vat will be paid through online banking via HMRC payment id, which was given

previously after the registration made.

Understand VAT penalties and make adjustments for previous errors

3.1 Explain the implications and penalties for an organisation resulting from failure to abide by

VAT regulations

It is necessary to follow the VAT related legislations to make its existence effective and

suitable to generate the revenue for the government. As everyone knows that, taxation is the

main income source of income for government, irrespective of whatever the country resources.

For that, it is necessary to impose several penalties or strict punishments to avoid any informal

practices of the VAT (Reisinger, 2014). In context with United Kingdom, if any business entity

or sole proprietor found guilty in any failure of VAT regulation, hat person will cover under the

category of defaulter. Also, after being declared as defaulter, they will be punishable with huge

fines or penalties. Some cases such as (Robert Martin CC/FS 1, 2015) shows that, if any entity

fails to pay the annual VAT amount, that person will be penalized with fines or punishable

amount, which completely depends on amount of VAT due for the mentioned date (Phillips,

2014). Suppose, entity fails to get registered after getting the application no, they will fine

penalized as certain circumstances:

Conditions Amount of penalties

Register after the one month from the date of

application

£200

Register after two months £300

Implication of these penalties would effect legal existence or credential of the business

entities. Also, these punishable offense would destroy the image of the business image or they

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

could involved under the legal court cases. These punishable offense would result in conducting

of fair & legal working of VAT and results in its effectiveness.

3.2 Make adjustments and declarations for any errors or omissions identified in previous VAT

periods

For making VAT effective , it is necessary to identify & analyse various adjustment and

changes into the previous VAT system. Also, there is the requirements of declaration to be made

for collective decision making while paying VAT by the tax payers (Decoster, 2016). There are

various ways which would facilitate the removal of the errors or omission such as being declared

as defaulter, guilty and tucked in VAT crime offense which is as follows:

Any error correction or omission should be done through VAT policies which is

stated under the Taxation regulation act, 1982 which was amended in 2015 to

bring transparency for effective decision making regarding paying an annual

VAT (Savage, 2012).

The rectification of this error should be done with traditional arrangement of

taxation to protect tax payers from any illegal offense.

Government of United Kingdom should provide temporary relief scheme's for

rectification of particular errors. It is beneficial to structure of an effective VAT

system, with motive to raise revenue for the government.

Communicate VAT information

4.1 Critical analysis of an impacts of VAT payment on the organisation’s cash flow and financial

forecasts

VAT payments are used to be made on monthly, quarterly or yearly basis. These payment

are required to be pre-decided before making the financial statements or forecast the financial

position (Capéau, 2014). Filling of the VAT generates the cash outflow from the financial

records of any entities or single entity. In context with United Kingdom, it has put financial

burden on small business, because of paying criteria based on quarterly basis. There are certain

cases regarding VAT payments and its impact on financial forecasts are as follows:

Penalties: Any sudden penalties for payment failure or being as defaulter, it creates the

situation for tax on tax, which is termed as Cascading effects.

of fair & legal working of VAT and results in its effectiveness.

3.2 Make adjustments and declarations for any errors or omissions identified in previous VAT

periods

For making VAT effective , it is necessary to identify & analyse various adjustment and

changes into the previous VAT system. Also, there is the requirements of declaration to be made

for collective decision making while paying VAT by the tax payers (Decoster, 2016). There are

various ways which would facilitate the removal of the errors or omission such as being declared

as defaulter, guilty and tucked in VAT crime offense which is as follows:

Any error correction or omission should be done through VAT policies which is

stated under the Taxation regulation act, 1982 which was amended in 2015 to

bring transparency for effective decision making regarding paying an annual

VAT (Savage, 2012).

The rectification of this error should be done with traditional arrangement of

taxation to protect tax payers from any illegal offense.

Government of United Kingdom should provide temporary relief scheme's for

rectification of particular errors. It is beneficial to structure of an effective VAT

system, with motive to raise revenue for the government.

Communicate VAT information

4.1 Critical analysis of an impacts of VAT payment on the organisation’s cash flow and financial

forecasts

VAT payments are used to be made on monthly, quarterly or yearly basis. These payment

are required to be pre-decided before making the financial statements or forecast the financial

position (Capéau, 2014). Filling of the VAT generates the cash outflow from the financial

records of any entities or single entity. In context with United Kingdom, it has put financial

burden on small business, because of paying criteria based on quarterly basis. There are certain

cases regarding VAT payments and its impact on financial forecasts are as follows:

Penalties: Any sudden penalties for payment failure or being as defaulter, it creates the

situation for tax on tax, which is termed as Cascading effects.

VAT rate changes: Continuous increase into the VAT rates would create burden on value

addition of products or services. Also, it could effect revenue out of an each product.

Regular payments: Monthly payments of value added tax would burdened on working

capital of the company, because of regular outflow of funds.

Credit purchase: If any business entity is buying value addition on goods & services for

credit basis, it would create pressure to pay current VAT payment on next purchase period.

Hence, it would impact the purchasing parity of the business unit.

4.2 Advise relevant people for changes into the VAT legislation

For affectivity in VAT regulations, there are different people's such as government bodies

, tax consulting agencies, accountants, suppliers, investor etc. As, it was previously discussed

that valid amendments are made to Taxation regulation act, 1082 regarding imposing of various

strict penalties, fines, charges along with punishable cases to be made (Callan, 2015). This has

auto-advised the given various entities to be fair over the matter of proper VAT regulations. It is

necessary to inform suppliers over the sustainable transferring of goods from one place to

another, investor's to invest with keep in mind proper value added tax system. Accountants to fill

VAT return as per stated norms & policies. They are required to fill the return with fair & ethical

code of conducts. This amended regulation has comes up with penalties, fines, court charges and

imprisonment up-to 1 year minimum, if person founds the default in case of taxation theft,

misuse of amount, transfer the amount to prevent from paying the VAT etc. This regulation is

necessary to ensure pure & suitable practice going into the taxation system of the United

Kingdom.

addition of products or services. Also, it could effect revenue out of an each product.

Regular payments: Monthly payments of value added tax would burdened on working

capital of the company, because of regular outflow of funds.

Credit purchase: If any business entity is buying value addition on goods & services for

credit basis, it would create pressure to pay current VAT payment on next purchase period.

Hence, it would impact the purchasing parity of the business unit.

4.2 Advise relevant people for changes into the VAT legislation

For affectivity in VAT regulations, there are different people's such as government bodies

, tax consulting agencies, accountants, suppliers, investor etc. As, it was previously discussed

that valid amendments are made to Taxation regulation act, 1082 regarding imposing of various

strict penalties, fines, charges along with punishable cases to be made (Callan, 2015). This has

auto-advised the given various entities to be fair over the matter of proper VAT regulations. It is

necessary to inform suppliers over the sustainable transferring of goods from one place to

another, investor's to invest with keep in mind proper value added tax system. Accountants to fill

VAT return as per stated norms & policies. They are required to fill the return with fair & ethical

code of conducts. This amended regulation has comes up with penalties, fines, court charges and

imprisonment up-to 1 year minimum, if person founds the default in case of taxation theft,

misuse of amount, transfer the amount to prevent from paying the VAT etc. This regulation is

necessary to ensure pure & suitable practice going into the taxation system of the United

Kingdom.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.