Indirect Tax VAT Report: UK VAT System, Calculations, and Compliance

VerifiedAdded on 2020/10/23

|15

|3968

|249

Report

AI Summary

This report provides a comprehensive overview of Value Added Tax (VAT) in the UK, beginning with an introduction to indirect taxes and the role of VAT. It identifies sources of information on VAT, including relevant legislation and government resources. The report details the legal requirements for VAT registration, business documentation, and various VAT schemes such as annual accounting, cash accounting, and flat rate accounting. It also covers changes to codes of practice, regulations, and legislation. The report includes a practical application by extracting data from an accounting system, calculating VAT liabilities, and completing a VAT return. Additionally, it explores the implications of non-compliance with VAT regulations and the impact of VAT payments on an organization's cash flow and financial forecasts. The report concludes with an analysis of potential changes in VAT legislation and their effects on business operations.

INDIRECT TAX

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 identification of sources of information on VAT..................................................................1

1.2 Explanation on organisation should interact with relevant government legacy....................1

1.3 Define the VAT legislation requirements..............................................................................2

1.4 Identification of information that must be included on business documentation of VAT

registered business.......................................................................................................................2

1.5 Define the requirements for these VAT schemes..................................................................3

1.6 Knowledge about changes to code of practices, regulation and legislation..........................4

TASK 2............................................................................................................................................4

2.1 Extracting the relevant data for a specific period through accounting system......................4

2.2 Calculating the relevant inputs and outputs as per VAT classifications...............................5

2.3 Measuring VAT as per relevant tax authority.......................................................................6

2.4 Completion of VAT return submission by associated payments within limits.....................7

TASK 3............................................................................................................................................8

3.1 Explaining the implications and penalties in Tesco as per failure to abide VAT regulations

.....................................................................................................................................................8

3.2 Make relevant declarations and adjustments for omissions and any errors as per previous

VAT periods................................................................................................................................9

TASK 4..........................................................................................................................................10

4.1 Inform managers the impact of VAT payment have on organization cash flows and

financial forecast........................................................................................................................10

4.2 Define changes in VAT legislation that could have effect on organization recording

system........................................................................................................................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 identification of sources of information on VAT..................................................................1

1.2 Explanation on organisation should interact with relevant government legacy....................1

1.3 Define the VAT legislation requirements..............................................................................2

1.4 Identification of information that must be included on business documentation of VAT

registered business.......................................................................................................................2

1.5 Define the requirements for these VAT schemes..................................................................3

1.6 Knowledge about changes to code of practices, regulation and legislation..........................4

TASK 2............................................................................................................................................4

2.1 Extracting the relevant data for a specific period through accounting system......................4

2.2 Calculating the relevant inputs and outputs as per VAT classifications...............................5

2.3 Measuring VAT as per relevant tax authority.......................................................................6

2.4 Completion of VAT return submission by associated payments within limits.....................7

TASK 3............................................................................................................................................8

3.1 Explaining the implications and penalties in Tesco as per failure to abide VAT regulations

.....................................................................................................................................................8

3.2 Make relevant declarations and adjustments for omissions and any errors as per previous

VAT periods................................................................................................................................9

TASK 4..........................................................................................................................................10

4.1 Inform managers the impact of VAT payment have on organization cash flows and

financial forecast........................................................................................................................10

4.2 Define changes in VAT legislation that could have effect on organization recording

system........................................................................................................................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................12

INTRODUCTION

An Indirect tax can be defined as taxation on any individuals and entity that is ultimately paid for

by the another person (Adachi, 2018 ). It is collected by an intermediary from the person who

bears the ultimate economic burden of tax. The some indirect taxes can be referred as the

consumption taxes and it can be termed out as value added tax. The present report will look over

the things as sources of information about the VAT and its legal requirements and information

that must be include on business documentation. Furthermore, calculation about the VAT return

will be given.

TASK 1

1.1 identification of sources of information on VAT.

VAT is termed out as “Value added tax”. On 1st January 1973 the UK has joined

European community and as a consequence purchase tax was replaced by Value Added Tax on 1

April 1073. The main aim of Tax is to raise profitability to finance government spending like any

other government (THE FINANCIAL ASPECT OF VAT AND HOW IT WILL AFFECT THE

BUSINESS’S CASH FLOW, 2018)). It is kind of consumption tax and in this revenue can be

generated with help of consumer spending. The seller of commodities and services will charge

this to the price. European union law requires that standard VAT rate will be at least 15% and the

reduction of rate will be till 5%. In addition to it, number of EU countries has have retained the

other rates for the specific product. Thus, it can be termed out as indirect Tax as it is collected

by firm on behalf of legal authorities.

1.2 Explanation on organisation should interact with relevant government legacy.

To run the organization, it is very essential to abide by laws and legislation set by Her

majesty Revenue and customs. Thus, firms can assist with issues like inheritance Tax on buying

and selling of property. The UK government is committed to creating the most competitive text

regimes. Thus, organisation are needed to be complied with all taxation polices set by the

department of HMRC in UK. In addition to this, the VAT registered business must report to the

HM revenue and customers about the amount of VAT charged. It is essential for organisation to

get registered itself at the time when value added tax turnover goes over £85,000 in the next 30

day period. On the other hand, the firm can also get voluntary registration if the turnover is

below £85,000 .

1

An Indirect tax can be defined as taxation on any individuals and entity that is ultimately paid for

by the another person (Adachi, 2018 ). It is collected by an intermediary from the person who

bears the ultimate economic burden of tax. The some indirect taxes can be referred as the

consumption taxes and it can be termed out as value added tax. The present report will look over

the things as sources of information about the VAT and its legal requirements and information

that must be include on business documentation. Furthermore, calculation about the VAT return

will be given.

TASK 1

1.1 identification of sources of information on VAT.

VAT is termed out as “Value added tax”. On 1st January 1973 the UK has joined

European community and as a consequence purchase tax was replaced by Value Added Tax on 1

April 1073. The main aim of Tax is to raise profitability to finance government spending like any

other government (THE FINANCIAL ASPECT OF VAT AND HOW IT WILL AFFECT THE

BUSINESS’S CASH FLOW, 2018)). It is kind of consumption tax and in this revenue can be

generated with help of consumer spending. The seller of commodities and services will charge

this to the price. European union law requires that standard VAT rate will be at least 15% and the

reduction of rate will be till 5%. In addition to it, number of EU countries has have retained the

other rates for the specific product. Thus, it can be termed out as indirect Tax as it is collected

by firm on behalf of legal authorities.

1.2 Explanation on organisation should interact with relevant government legacy.

To run the organization, it is very essential to abide by laws and legislation set by Her

majesty Revenue and customs. Thus, firms can assist with issues like inheritance Tax on buying

and selling of property. The UK government is committed to creating the most competitive text

regimes. Thus, organisation are needed to be complied with all taxation polices set by the

department of HMRC in UK. In addition to this, the VAT registered business must report to the

HM revenue and customers about the amount of VAT charged. It is essential for organisation to

get registered itself at the time when value added tax turnover goes over £85,000 in the next 30

day period. On the other hand, the firm can also get voluntary registration if the turnover is

below £85,000 .

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1.3 Define the VAT legislation requirements.

The HMRC has recently announced the proposed changes and this all are needed to be

introduced in the finance bill 2018. Thus, VAT legislation requirement has been discussed in

below presented manner as-

The organization must registered for value Added Tax with HM Revenue and Customs

(HMRC). If the taxable turnover is more than £85,000.

Any kind of supply made in the UK is not exempt from VAT. Thus, taxable supplier will

be inclusive at time when they are zero rated for VAT.

The VAT is charged on services that are imported from place outside the EU.

The commodities and services that comes to the United Kingdom from the other

European union member state, on also VAT will be charged.

The standard rate of VAT is 20% on the most of good and services.

The 5% VAT has been reduced from the fuel and power consume at home and by

charities, women sanity products, children car seats, residential conversions and

residential renovation and alteration.

The 0% VAT will be charged on the certain good and services and this as books,

newspaper, most public transport service, prescription dispensed to patient by a registered

pharmacist.

The Rate of VAT will not be charged on the exempt supplied. They are those who do not

meet the definition of taxable supplies. These as are- insurance, betting, gambling,

lotteries, providing credit and certain education and training.

1.4 Identification of information that must be included on business documentation of VAT

registered business.

INFORMATION TO BE DISCLOSED ON COMPANY DOCUMENT

This is legal requirement to disclose some extent of information on company documents. These

as are letterheads, compliment slips, invoices, purchase orders, website and email message are

all considered to be company documents (Song and 2018). These as are-

letterheads- Name of the company.

Name of company- It must be end with Ltd or world limited. (In case if the name of trade

under is differ from firm name then it is necessary to show certificate of incorporation).

The entity registered office address.

2

The HMRC has recently announced the proposed changes and this all are needed to be

introduced in the finance bill 2018. Thus, VAT legislation requirement has been discussed in

below presented manner as-

The organization must registered for value Added Tax with HM Revenue and Customs

(HMRC). If the taxable turnover is more than £85,000.

Any kind of supply made in the UK is not exempt from VAT. Thus, taxable supplier will

be inclusive at time when they are zero rated for VAT.

The VAT is charged on services that are imported from place outside the EU.

The commodities and services that comes to the United Kingdom from the other

European union member state, on also VAT will be charged.

The standard rate of VAT is 20% on the most of good and services.

The 5% VAT has been reduced from the fuel and power consume at home and by

charities, women sanity products, children car seats, residential conversions and

residential renovation and alteration.

The 0% VAT will be charged on the certain good and services and this as books,

newspaper, most public transport service, prescription dispensed to patient by a registered

pharmacist.

The Rate of VAT will not be charged on the exempt supplied. They are those who do not

meet the definition of taxable supplies. These as are- insurance, betting, gambling,

lotteries, providing credit and certain education and training.

1.4 Identification of information that must be included on business documentation of VAT

registered business.

INFORMATION TO BE DISCLOSED ON COMPANY DOCUMENT

This is legal requirement to disclose some extent of information on company documents. These

as are letterheads, compliment slips, invoices, purchase orders, website and email message are

all considered to be company documents (Song and 2018). These as are-

letterheads- Name of the company.

Name of company- It must be end with Ltd or world limited. (In case if the name of trade

under is differ from firm name then it is necessary to show certificate of incorporation).

The entity registered office address.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The permanent and register number of company.

Place of registration- in country the registration has made must be shown. It would be in

‘England & Wales’ or ‘Scotland’.

Other information as-

Correspondence address

Telephone, FAX number and e-main address

The number of VAT.

General nature of the firm unless obvious from the firm name.

Compliment slips- with the letterheads the compliment slip must be show and it is

inclusive of company name, registered office address, the company registration number

and place etc.

Invoices- This will be inclusive of things as-

Company name

Business address of the company

VAT registration number

Date of supply

Type of supply

Description about the good and services

Total payable exclusion of VAT

Rate of VAT

Amount of VAT

Rate of cash discount offered.

1.5 Define the requirements for these VAT schemes.

The VAT retail scheme will be helpful in terms to calculate the amount of VAT in simpler

manner. Thus, there are three standard VAT retail scheme are defined as-

Annual accounting- This is scheme that aids to small business by allowing them to

submit only one VAT return annually rather than the normal four ( Ilzetzki, 2018.).

During the year instalments based on estimated liability for the year with balancing

payment due with the return.

3

Place of registration- in country the registration has made must be shown. It would be in

‘England & Wales’ or ‘Scotland’.

Other information as-

Correspondence address

Telephone, FAX number and e-main address

The number of VAT.

General nature of the firm unless obvious from the firm name.

Compliment slips- with the letterheads the compliment slip must be show and it is

inclusive of company name, registered office address, the company registration number

and place etc.

Invoices- This will be inclusive of things as-

Company name

Business address of the company

VAT registration number

Date of supply

Type of supply

Description about the good and services

Total payable exclusion of VAT

Rate of VAT

Amount of VAT

Rate of cash discount offered.

1.5 Define the requirements for these VAT schemes.

The VAT retail scheme will be helpful in terms to calculate the amount of VAT in simpler

manner. Thus, there are three standard VAT retail scheme are defined as-

Annual accounting- This is scheme that aids to small business by allowing them to

submit only one VAT return annually rather than the normal four ( Ilzetzki, 2018.).

During the year instalments based on estimated liability for the year with balancing

payment due with the return.

3

Cash accounting scheme- This scheme is method of VAT in which information is

recorded on the basis of payments made or received rather then the issues of tax invoice

etc.

Flat rate accounting scheme- Under this, the VAT Flat rate scheme, the amount of tax

is calculated by multiplying the flat rate of VAT and that will be inclusive of turnover.

Thus, rate are set by the HMRC and vary depending on industry sector from 4 to 14.5%.

Standard scheme- The standard rate accounting scheme is the method in which the rate

is recorded and paid on the basis of when invoices are issued (Phillips and et.al., 2018).

Under the standard accounting rate scheme, the bushiness works as to submit a VAT

return four times in the year.

1.6 Knowledge about changes to code of practices, regulation and legislation.

Code of practices will be issued as part of the contractual disclosure facility and it is

solely used by HMRC Fraud investigation (Schippers and Verhaeren, 2018). In this, code of

practices set out the protocols and procedures that HMRc expect to work under. Thus, the code

of practices for profit audit and other complained intervention is set of guidelines for when

revenue is computing.

TASK 2

2.1 Extracting the relevant data for a specific period through accounting system

In order to analyse the taxes by considering the VAT system of UK which has have

ascertained through Taxation authority in UK. However, there have been creation of a business

scenario on which the relevant VAT rates will be charged and computation of VAT payable have

been measured.

There have been use of financial disclosure sales revenue generated by Tesco in the year

2018. Similarly, it has been assumed that Mrs. XYZ have several gains and expenses in the

accounting year 2018 which are to be measured on the on the basis of current tax threshold

presented by HMRC with respect to measure the taxable liabilities (Baumeister and et.al, 2017).

Thus, the list of revenue and expense has been recorded such as:

Particulars

Details

(in £)

Sales revenue 20000

fuel expenses 1000

food and beverages 1200

4

recorded on the basis of payments made or received rather then the issues of tax invoice

etc.

Flat rate accounting scheme- Under this, the VAT Flat rate scheme, the amount of tax

is calculated by multiplying the flat rate of VAT and that will be inclusive of turnover.

Thus, rate are set by the HMRC and vary depending on industry sector from 4 to 14.5%.

Standard scheme- The standard rate accounting scheme is the method in which the rate

is recorded and paid on the basis of when invoices are issued (Phillips and et.al., 2018).

Under the standard accounting rate scheme, the bushiness works as to submit a VAT

return four times in the year.

1.6 Knowledge about changes to code of practices, regulation and legislation.

Code of practices will be issued as part of the contractual disclosure facility and it is

solely used by HMRC Fraud investigation (Schippers and Verhaeren, 2018). In this, code of

practices set out the protocols and procedures that HMRc expect to work under. Thus, the code

of practices for profit audit and other complained intervention is set of guidelines for when

revenue is computing.

TASK 2

2.1 Extracting the relevant data for a specific period through accounting system

In order to analyse the taxes by considering the VAT system of UK which has have

ascertained through Taxation authority in UK. However, there have been creation of a business

scenario on which the relevant VAT rates will be charged and computation of VAT payable have

been measured.

There have been use of financial disclosure sales revenue generated by Tesco in the year

2018. Similarly, it has been assumed that Mrs. XYZ have several gains and expenses in the

accounting year 2018 which are to be measured on the on the basis of current tax threshold

presented by HMRC with respect to measure the taxable liabilities (Baumeister and et.al, 2017).

Thus, the list of revenue and expense has been recorded such as:

Particulars

Details

(in £)

Sales revenue 20000

fuel expenses 1000

food and beverages 1200

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

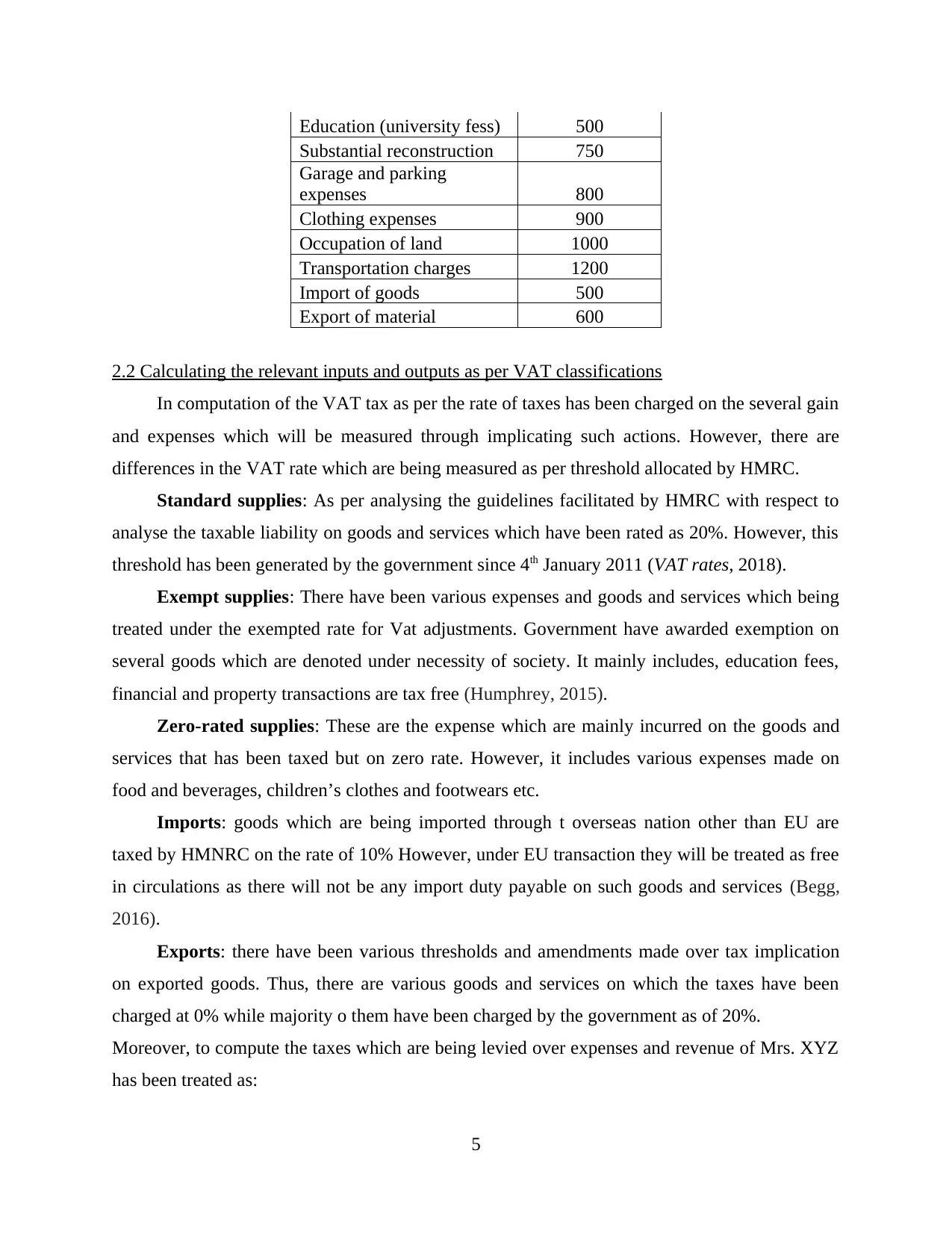

Education (university fess) 500

Substantial reconstruction 750

Garage and parking

expenses 800

Clothing expenses 900

Occupation of land 1000

Transportation charges 1200

Import of goods 500

Export of material 600

2.2 Calculating the relevant inputs and outputs as per VAT classifications

In computation of the VAT tax as per the rate of taxes has been charged on the several gain

and expenses which will be measured through implicating such actions. However, there are

differences in the VAT rate which are being measured as per threshold allocated by HMRC.

Standard supplies: As per analysing the guidelines facilitated by HMRC with respect to

analyse the taxable liability on goods and services which have been rated as 20%. However, this

threshold has been generated by the government since 4th January 2011 (VAT rates, 2018).

Exempt supplies: There have been various expenses and goods and services which being

treated under the exempted rate for Vat adjustments. Government have awarded exemption on

several goods which are denoted under necessity of society. It mainly includes, education fees,

financial and property transactions are tax free (Humphrey, 2015).

Zero-rated supplies: These are the expense which are mainly incurred on the goods and

services that has been taxed but on zero rate. However, it includes various expenses made on

food and beverages, children’s clothes and footwears etc.

Imports: goods which are being imported through t overseas nation other than EU are

taxed by HMNRC on the rate of 10% However, under EU transaction they will be treated as free

in circulations as there will not be any import duty payable on such goods and services (Begg,

2016).

Exports: there have been various thresholds and amendments made over tax implication

on exported goods. Thus, there are various goods and services on which the taxes have been

charged at 0% while majority o them have been charged by the government as of 20%.

Moreover, to compute the taxes which are being levied over expenses and revenue of Mrs. XYZ

has been treated as:

5

Substantial reconstruction 750

Garage and parking

expenses 800

Clothing expenses 900

Occupation of land 1000

Transportation charges 1200

Import of goods 500

Export of material 600

2.2 Calculating the relevant inputs and outputs as per VAT classifications

In computation of the VAT tax as per the rate of taxes has been charged on the several gain

and expenses which will be measured through implicating such actions. However, there are

differences in the VAT rate which are being measured as per threshold allocated by HMRC.

Standard supplies: As per analysing the guidelines facilitated by HMRC with respect to

analyse the taxable liability on goods and services which have been rated as 20%. However, this

threshold has been generated by the government since 4th January 2011 (VAT rates, 2018).

Exempt supplies: There have been various expenses and goods and services which being

treated under the exempted rate for Vat adjustments. Government have awarded exemption on

several goods which are denoted under necessity of society. It mainly includes, education fees,

financial and property transactions are tax free (Humphrey, 2015).

Zero-rated supplies: These are the expense which are mainly incurred on the goods and

services that has been taxed but on zero rate. However, it includes various expenses made on

food and beverages, children’s clothes and footwears etc.

Imports: goods which are being imported through t overseas nation other than EU are

taxed by HMNRC on the rate of 10% However, under EU transaction they will be treated as free

in circulations as there will not be any import duty payable on such goods and services (Begg,

2016).

Exports: there have been various thresholds and amendments made over tax implication

on exported goods. Thus, there are various goods and services on which the taxes have been

charged at 0% while majority o them have been charged by the government as of 20%.

Moreover, to compute the taxes which are being levied over expenses and revenue of Mrs. XYZ

has been treated as:

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Particulars

Details

(in £)

VAT

rates

Amount

(in £)

Sales revenue 20000 20% 4000

fuel expenses 1000 5% 50

food and beverages 1200 0% 0

Education (university fess) 500 Exempted 0

Substantial reconstruction 750 0% 0

Garage and parking

expenses 800 Exempted 0

Clothing expenses 900 0% 0

Occupation of land 1000 Exempted 0

Transportation charges 1200 0% 0

Import of goods 500 10% 50

Export of material 600 20% 120

2.3 Measuring VAT as per relevant tax authority

In relation with analysing the VAT returns of due to HMRC there have been measurement

of the tax which are to be payable by Tesco in the respecting year 2018. Moreover, it has been

measured by implicating standard and flat rate techniques for analysing VAT payable such as:

Particulars

Standard VAT scheme

(in £)

Flat rate VAT

scheme

(in £)

Sales of Tesco 57500 57500

vat at 20% 11500 11500

sales incl. vat 69000 69000

VAT on cost 1080

Flat rate% (assumed 10%) 6900

VAT due to HMRC 70080 6900

Gain on Flat rate scheme 63180

Interpretation: As per the analysed VAT payable through standard VAT scheme and

Flat Rate VAT scheme on which there has been analysis made by government to analyse and

comprised the data set accordingly. Therefore, the gains Tesco will have as if they implicate the

VAT through Flat rate VAT scheme which have reflected the differences between standard and

flat rate techniques such as 70080- 6900 that is 63180.

Computing VAT payable

6

Details

(in £)

VAT

rates

Amount

(in £)

Sales revenue 20000 20% 4000

fuel expenses 1000 5% 50

food and beverages 1200 0% 0

Education (university fess) 500 Exempted 0

Substantial reconstruction 750 0% 0

Garage and parking

expenses 800 Exempted 0

Clothing expenses 900 0% 0

Occupation of land 1000 Exempted 0

Transportation charges 1200 0% 0

Import of goods 500 10% 50

Export of material 600 20% 120

2.3 Measuring VAT as per relevant tax authority

In relation with analysing the VAT returns of due to HMRC there have been measurement

of the tax which are to be payable by Tesco in the respecting year 2018. Moreover, it has been

measured by implicating standard and flat rate techniques for analysing VAT payable such as:

Particulars

Standard VAT scheme

(in £)

Flat rate VAT

scheme

(in £)

Sales of Tesco 57500 57500

vat at 20% 11500 11500

sales incl. vat 69000 69000

VAT on cost 1080

Flat rate% (assumed 10%) 6900

VAT due to HMRC 70080 6900

Gain on Flat rate scheme 63180

Interpretation: As per the analysed VAT payable through standard VAT scheme and

Flat Rate VAT scheme on which there has been analysis made by government to analyse and

comprised the data set accordingly. Therefore, the gains Tesco will have as if they implicate the

VAT through Flat rate VAT scheme which have reflected the differences between standard and

flat rate techniques such as 70080- 6900 that is 63180.

Computing VAT payable

6

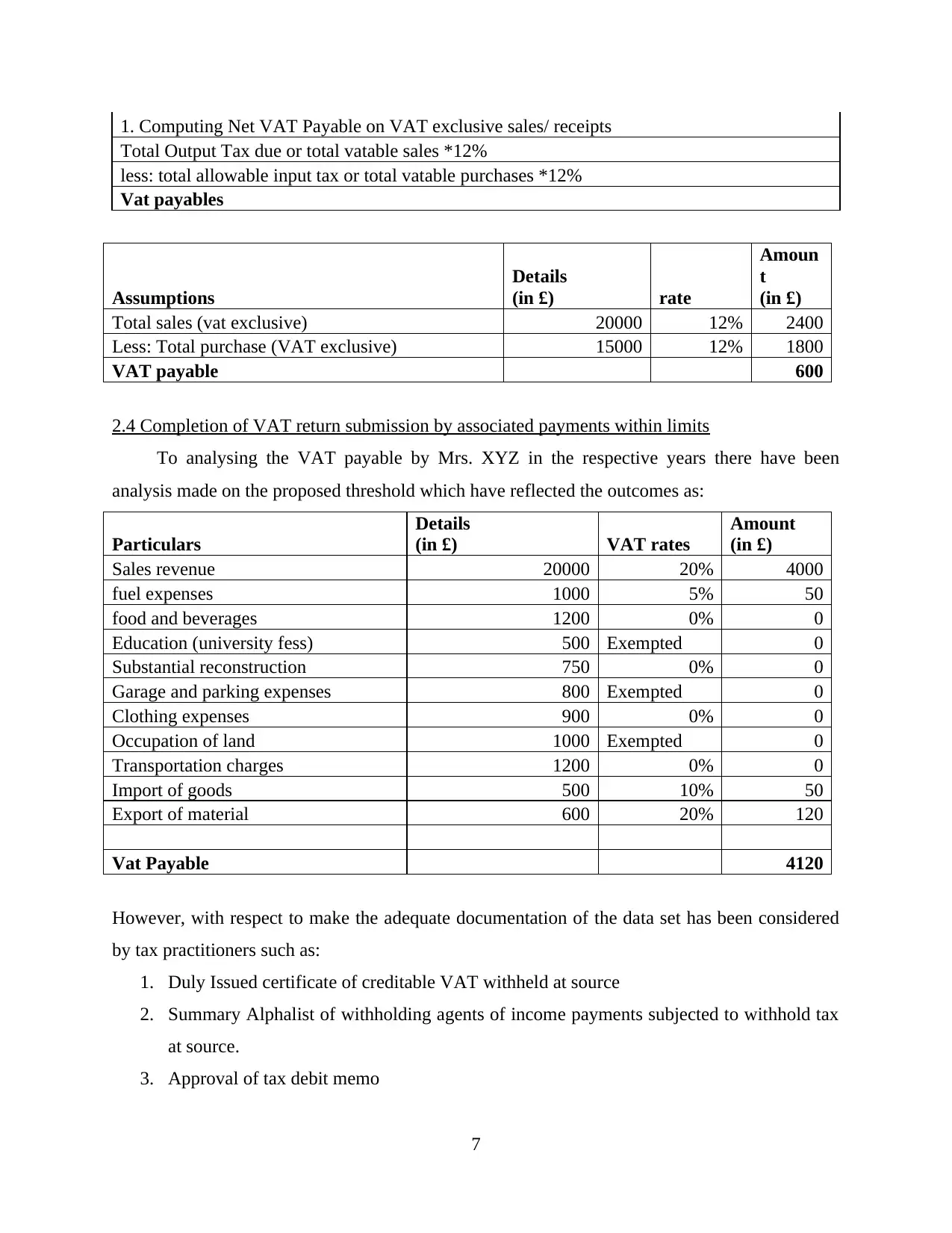

1. Computing Net VAT Payable on VAT exclusive sales/ receipts

Total Output Tax due or total vatable sales *12%

less: total allowable input tax or total vatable purchases *12%

Vat payables

Assumptions

Details

(in £) rate

Amoun

t

(in £)

Total sales (vat exclusive) 20000 12% 2400

Less: Total purchase (VAT exclusive) 15000 12% 1800

VAT payable 600

2.4 Completion of VAT return submission by associated payments within limits

To analysing the VAT payable by Mrs. XYZ in the respective years there have been

analysis made on the proposed threshold which have reflected the outcomes as:

Particulars

Details

(in £) VAT rates

Amount

(in £)

Sales revenue 20000 20% 4000

fuel expenses 1000 5% 50

food and beverages 1200 0% 0

Education (university fess) 500 Exempted 0

Substantial reconstruction 750 0% 0

Garage and parking expenses 800 Exempted 0

Clothing expenses 900 0% 0

Occupation of land 1000 Exempted 0

Transportation charges 1200 0% 0

Import of goods 500 10% 50

Export of material 600 20% 120

Vat Payable 4120

However, with respect to make the adequate documentation of the data set has been considered

by tax practitioners such as:

1. Duly Issued certificate of creditable VAT withheld at source

2. Summary Alphalist of withholding agents of income payments subjected to withhold tax

at source.

3. Approval of tax debit memo

7

Total Output Tax due or total vatable sales *12%

less: total allowable input tax or total vatable purchases *12%

Vat payables

Assumptions

Details

(in £) rate

Amoun

t

(in £)

Total sales (vat exclusive) 20000 12% 2400

Less: Total purchase (VAT exclusive) 15000 12% 1800

VAT payable 600

2.4 Completion of VAT return submission by associated payments within limits

To analysing the VAT payable by Mrs. XYZ in the respective years there have been

analysis made on the proposed threshold which have reflected the outcomes as:

Particulars

Details

(in £) VAT rates

Amount

(in £)

Sales revenue 20000 20% 4000

fuel expenses 1000 5% 50

food and beverages 1200 0% 0

Education (university fess) 500 Exempted 0

Substantial reconstruction 750 0% 0

Garage and parking expenses 800 Exempted 0

Clothing expenses 900 0% 0

Occupation of land 1000 Exempted 0

Transportation charges 1200 0% 0

Import of goods 500 10% 50

Export of material 600 20% 120

Vat Payable 4120

However, with respect to make the adequate documentation of the data set has been considered

by tax practitioners such as:

1. Duly Issued certificate of creditable VAT withheld at source

2. Summary Alphalist of withholding agents of income payments subjected to withhold tax

at source.

3. Approval of tax debit memo

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4. Approval of tax credit certificate

5. Receiving the authorisation letter.

TASK 3

3.1 Explaining the implications and penalties in Tesco as per failure to abide VAT regulations

In accordance with the VAT guidelines and notice issued under VAT notice 700 that states

various penalties and sanctions against the organisations which are facing such issues. However,

this rate is being chargeable on every trade of goods and services as well as expenses payable by

individual as well as corporation in a year (Trandafir, 2016). Thus, analysing such impacts will

be adequate and effective with reference to have effective tax collection among the government.

Moreover, there are several penalties which are being enforced by government among the society

such as:

There will be record of default by HMRC as if this authority does not receive the VAT

return within time limit.

There will be records of a default if HMRC found that the complete payment of VAT is

due and does not reach to their account within deadline.

However, there have been payment of surcharge on the annual turnover of the organisation as

if they found defaulted and do not meet the deadline of the VAT return such as:

8

5. Receiving the authorisation letter.

TASK 3

3.1 Explaining the implications and penalties in Tesco as per failure to abide VAT regulations

In accordance with the VAT guidelines and notice issued under VAT notice 700 that states

various penalties and sanctions against the organisations which are facing such issues. However,

this rate is being chargeable on every trade of goods and services as well as expenses payable by

individual as well as corporation in a year (Trandafir, 2016). Thus, analysing such impacts will

be adequate and effective with reference to have effective tax collection among the government.

Moreover, there are several penalties which are being enforced by government among the society

such as:

There will be record of default by HMRC as if this authority does not receive the VAT

return within time limit.

There will be records of a default if HMRC found that the complete payment of VAT is

due and does not reach to their account within deadline.

However, there have been payment of surcharge on the annual turnover of the organisation as

if they found defaulted and do not meet the deadline of the VAT return such as:

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

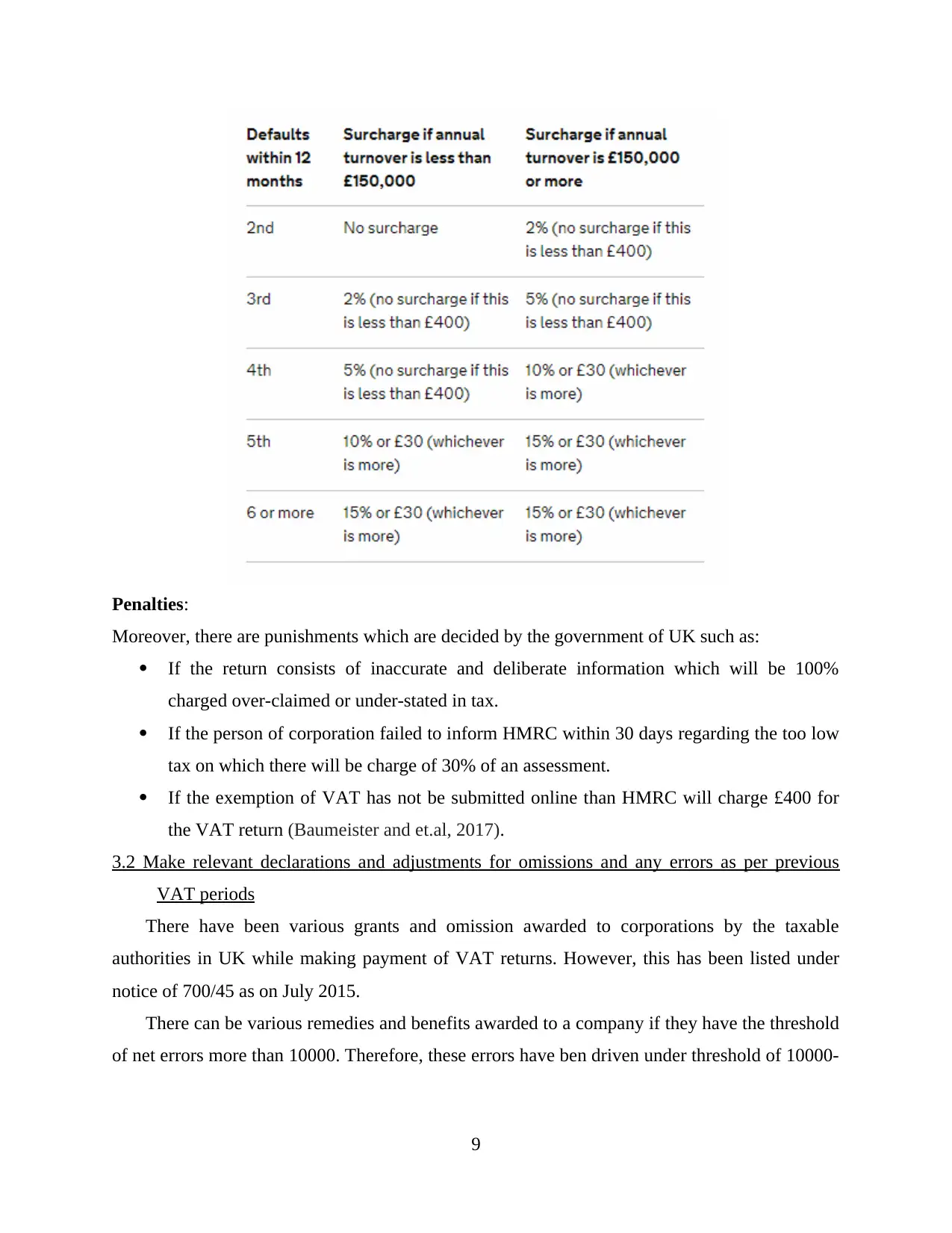

Penalties:

Moreover, there are punishments which are decided by the government of UK such as:

If the return consists of inaccurate and deliberate information which will be 100%

charged over-claimed or under-stated in tax.

If the person of corporation failed to inform HMRC within 30 days regarding the too low

tax on which there will be charge of 30% of an assessment.

If the exemption of VAT has not be submitted online than HMRC will charge £400 for

the VAT return (Baumeister and et.al, 2017).

3.2 Make relevant declarations and adjustments for omissions and any errors as per previous

VAT periods

There have been various grants and omission awarded to corporations by the taxable

authorities in UK while making payment of VAT returns. However, this has been listed under

notice of 700/45 as on July 2015.

There can be various remedies and benefits awarded to a company if they have the threshold

of net errors more than 10000. Therefore, these errors have ben driven under threshold of 10000-

9

Moreover, there are punishments which are decided by the government of UK such as:

If the return consists of inaccurate and deliberate information which will be 100%

charged over-claimed or under-stated in tax.

If the person of corporation failed to inform HMRC within 30 days regarding the too low

tax on which there will be charge of 30% of an assessment.

If the exemption of VAT has not be submitted online than HMRC will charge £400 for

the VAT return (Baumeister and et.al, 2017).

3.2 Make relevant declarations and adjustments for omissions and any errors as per previous

VAT periods

There have been various grants and omission awarded to corporations by the taxable

authorities in UK while making payment of VAT returns. However, this has been listed under

notice of 700/45 as on July 2015.

There can be various remedies and benefits awarded to a company if they have the threshold

of net errors more than 10000. Therefore, these errors have ben driven under threshold of 10000-

9

5000 and will be in the next assessment year. Along with this, if the report has been made before

4 years which affects in limiting the needs to be notified by companies to HMRC.

TASK 4

4.1 Inform managers the impact of VAT payment have on organization cash flows and financial

forecast.

Financial managers and other concerned authorities must have idea about the impact of

cash flows and financial forecast ( Harris and et.al., 2018). Thus, cash flow forecast is the part of

enterprise financial forecast. Furthermore, financial consequences lead to shuffle in the whole

procedures of cash flows. In addition to this, the impact on VAT on cost of production will lead

many producers to seek lower cost of raw material to compensate for the value added percentage.

Yes, it is true to said that VAT affects the cash flow forecast but is not included in the

profit forecast. Thus, reason of collecting the VAT on behalf of HR revenue & customs is not a

kind of trading activity and this also excluded from the profit forecast. In this, the financial

decision made by the importers and marginal cost on VAT can be compensated with the help of

seeking the most export markets. However, VAT do not affect the cash flow of business.

4.2 Define changes in VAT legislation that could have effect on organization recording system.

The Value added tax do not reflect in the income and expenditure of the cash glow. In

order to have impact it is main under the daily day book and cash book and it directly impact the

cash flow of company (Adachi, 2018). The VAT record can be kept on paper, electronically or

an part of software program. This kind of record must be accurate, complete and readable. Thus,

HMRC can visit organisation in order to inspect the record keeping and charge the penalty of

records. Furthermore, the VAT records must be made for the at least 6 years and for the 10 years

if there is the use of VAT on Moss service ( VAT record keeping, 2018). Generally, Value Added

tax is charged on purchase and sale. In order to record the import VAT, there is need to create an

expense separately by manually calculating the VAT applicable for the good and services.

CONCLUSION

10

4 years which affects in limiting the needs to be notified by companies to HMRC.

TASK 4

4.1 Inform managers the impact of VAT payment have on organization cash flows and financial

forecast.

Financial managers and other concerned authorities must have idea about the impact of

cash flows and financial forecast ( Harris and et.al., 2018). Thus, cash flow forecast is the part of

enterprise financial forecast. Furthermore, financial consequences lead to shuffle in the whole

procedures of cash flows. In addition to this, the impact on VAT on cost of production will lead

many producers to seek lower cost of raw material to compensate for the value added percentage.

Yes, it is true to said that VAT affects the cash flow forecast but is not included in the

profit forecast. Thus, reason of collecting the VAT on behalf of HR revenue & customs is not a

kind of trading activity and this also excluded from the profit forecast. In this, the financial

decision made by the importers and marginal cost on VAT can be compensated with the help of

seeking the most export markets. However, VAT do not affect the cash flow of business.

4.2 Define changes in VAT legislation that could have effect on organization recording system.

The Value added tax do not reflect in the income and expenditure of the cash glow. In

order to have impact it is main under the daily day book and cash book and it directly impact the

cash flow of company (Adachi, 2018). The VAT record can be kept on paper, electronically or

an part of software program. This kind of record must be accurate, complete and readable. Thus,

HMRC can visit organisation in order to inspect the record keeping and charge the penalty of

records. Furthermore, the VAT records must be made for the at least 6 years and for the 10 years

if there is the use of VAT on Moss service ( VAT record keeping, 2018). Generally, Value Added

tax is charged on purchase and sale. In order to record the import VAT, there is need to create an

expense separately by manually calculating the VAT applicable for the good and services.

CONCLUSION

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.