Comprehensive Report on Indirect Tax: VAT Regulations and Compliance

VerifiedAdded on 2021/01/01

|14

|3898

|104

Report

AI Summary

This report provides a comprehensive overview of Value Added Tax (VAT) regulations, focusing on compliance and reporting requirements. It details the sources of VAT information, the interaction between organizations and the relevant governance agency (HMRC), and the requirements for VAT registration. The report outlines the information that must be included on business documents for VAT-registered businesses, and it explains various VAT schemes like annual accounting, cash accounting, flat-rate, and standard rate schemes. Furthermore, the report covers the importance of maintaining up-to-date knowledge of changes to VAT regulations, the process of extracting relevant data from accounting systems, and the calculation of VAT liabilities. It also addresses the completion and submission of VAT returns, along with the implications and penalties for non-compliance. Finally, the report discusses the impact of VAT payments on cash flow and financial forecasts, offering advice on communicating changes in VAT legislation to relevant stakeholders.

Indirect Tax

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Sources of VAT information.................................................................................................1

1.2 Manner in which organisations interact with the relevant governance agency.....................2

1.3 Requirements of VAT registration........................................................................................2

1.4 Information that must be included on business documents of VAT registered businesses. .3

1.5 Requirements and frequency of reporting of following VAT schemes................................3

1.6 Maintain an up-to-date knowledge of changes to code of practice, regulation or legislation

.....................................................................................................................................................4

TASK 2............................................................................................................................................5

2.1 Extract relevant data for a specific period from the accounting system...............................5

2.2 Calculation of relevant inputs and outputs using VAT classifications.................................5

2.3 Calculation of VAT due to, or from the relevant tax authority.............................................7

2.4 Complete and submit a VAT return and any associated payment within the statutory time

limits............................................................................................................................................8

TASK 3............................................................................................................................................9

3.1 Implications and penalties for an organisation resulting from failure to abide by VAT

regulations...................................................................................................................................9

3.2 Adjustments and declarations for any errors or omissions identified in previous VAT

period...........................................................................................................................................9

TASK 4..........................................................................................................................................10

4.1 Information to managers of the impact that VAT payments may have on an organisation's

cash flow and financial forecasts..............................................................................................10

4.2 Advise to revenant people of changes in VAT legislation which would have an effect on

an organisation's recording system............................................................................................10

CONCLUSION..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Sources of VAT information.................................................................................................1

1.2 Manner in which organisations interact with the relevant governance agency.....................2

1.3 Requirements of VAT registration........................................................................................2

1.4 Information that must be included on business documents of VAT registered businesses. .3

1.5 Requirements and frequency of reporting of following VAT schemes................................3

1.6 Maintain an up-to-date knowledge of changes to code of practice, regulation or legislation

.....................................................................................................................................................4

TASK 2............................................................................................................................................5

2.1 Extract relevant data for a specific period from the accounting system...............................5

2.2 Calculation of relevant inputs and outputs using VAT classifications.................................5

2.3 Calculation of VAT due to, or from the relevant tax authority.............................................7

2.4 Complete and submit a VAT return and any associated payment within the statutory time

limits............................................................................................................................................8

TASK 3............................................................................................................................................9

3.1 Implications and penalties for an organisation resulting from failure to abide by VAT

regulations...................................................................................................................................9

3.2 Adjustments and declarations for any errors or omissions identified in previous VAT

period...........................................................................................................................................9

TASK 4..........................................................................................................................................10

4.1 Information to managers of the impact that VAT payments may have on an organisation's

cash flow and financial forecasts..............................................................................................10

4.2 Advise to revenant people of changes in VAT legislation which would have an effect on

an organisation's recording system............................................................................................10

CONCLUSION..............................................................................................................................11

.......................................................................................................................................................11

REFERENCES..............................................................................................................................12

REFERENCES..............................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Indirect taxes are applied on the manufacture or sale of goods and services. These are

initially paid to the government by an intermediary, who then adds the amount of indirect tax in

the value of goods and burden of tax is passed to the end user. An indirect tax is collected by the

one entity and paid to the government and incidence of tax is on the ultimate consumer. Indirect

tax is collected in form of sales tax, Value Added Tax and Goods and Service tax. Price of the

product got increased by imposing indirect tax. In United Kingdom Value Added Tax (VAT)

was introduced in the year 1973 and it is third largest source of revenue for the government

(Albayrak, 2017). It is administrated and collected by HM Revenue and Costumes through the

Value Added Tax Act 1994. In this project to understand VAT regulations full information is

mentioned. Information regarding complete VAT returns accurately and in a timely manner is

provided. VAT penalties and adjustments for previous year and communication of VAT

information is discussed.

TASK 1

1.1 Sources of VAT information

Application of VAT is on manufacture or sales of goods and services. Tax is considered

as one of the most important source of revenue for government of the country. Tax system in a

country is segregated in two sectors and for collection of tax such as VAT information is

required by the government. Information to impose tax is collected from books that are

maintained by businesses to record their financial information. Sales and purchase book in an

organisation defines about the quantity that is purchase and sole during the year. This

information is important to be collected by the government to decided the amount of VAT to be

imposed on the business entities. Together with this details regarding a manufacture is collected

from the books that provide information regarding quantity manufactured by the company. Sales

return books and purchase return books also includes information that is important for VAT

calculations (Arunatilake, Inchauste and Lustig, 2017). Debit and credit not reduces the amount

of tax needs to be paid to the government. So all the documents that are specified are considered

as primary source of information for VAT.

1

Indirect taxes are applied on the manufacture or sale of goods and services. These are

initially paid to the government by an intermediary, who then adds the amount of indirect tax in

the value of goods and burden of tax is passed to the end user. An indirect tax is collected by the

one entity and paid to the government and incidence of tax is on the ultimate consumer. Indirect

tax is collected in form of sales tax, Value Added Tax and Goods and Service tax. Price of the

product got increased by imposing indirect tax. In United Kingdom Value Added Tax (VAT)

was introduced in the year 1973 and it is third largest source of revenue for the government

(Albayrak, 2017). It is administrated and collected by HM Revenue and Costumes through the

Value Added Tax Act 1994. In this project to understand VAT regulations full information is

mentioned. Information regarding complete VAT returns accurately and in a timely manner is

provided. VAT penalties and adjustments for previous year and communication of VAT

information is discussed.

TASK 1

1.1 Sources of VAT information

Application of VAT is on manufacture or sales of goods and services. Tax is considered

as one of the most important source of revenue for government of the country. Tax system in a

country is segregated in two sectors and for collection of tax such as VAT information is

required by the government. Information to impose tax is collected from books that are

maintained by businesses to record their financial information. Sales and purchase book in an

organisation defines about the quantity that is purchase and sole during the year. This

information is important to be collected by the government to decided the amount of VAT to be

imposed on the business entities. Together with this details regarding a manufacture is collected

from the books that provide information regarding quantity manufactured by the company. Sales

return books and purchase return books also includes information that is important for VAT

calculations (Arunatilake, Inchauste and Lustig, 2017). Debit and credit not reduces the amount

of tax needs to be paid to the government. So all the documents that are specified are considered

as primary source of information for VAT.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1.2 Manner in which organisations interact with the relevant governance agency

Revenue and customs (HMRC) is responsible for making sure money is available with

the government to fund UK's public services and for helping families and individuals. HMRC set

out to use digital communications to help customers to get their tax affairs right by improving

access to information and increasing usage. Individuals, small businesses and agents consumer

survey supports business strategy of HMRC (Boadway and Song, 2016). Organisation is

committed to supporting tax credits consumers to claim the tax credit they are entitled to.

Providing communication channels that are effective and meet consumers needs is the key to

achieve the set goals. Organisations can interact with HMRC by phoning the tax credits

helplines, writing to the organisation and by visiting local enquiry centre. HMRC to have

effective communication with the business entities has introduced digital channels of

communication. This online system helps businesses to get the required information quickly.

Providing online interaction enhance more ways of communication to the general public.

Communication to HMRC reduces confusions and conflicts between business organisations and

government entities.

1.3 Requirements of VAT registration

Business organisations needs to get registered under VAT regulations when turnover is

expected to goes over £85,000 in next 30 days. Another condition is when VAT taxable turnover

is more then £85,000 over the last 12 months. To apply for VAT registration there are two

methods one is online and other is through filling a written form. To register for VAT

application must be filled to HM Revenue and customs department. For online registration form

is filled with VAT online service with HMEC. VAT registration certificate is provided within 14

working days. Documents that are required for registration are as follows-

Unique Taxpayer's Reference number(UTR)

Permanent Account Number

Certificate of incorporation and details of business

Turnover details of the company

Past two years information of the company

Businesses that are dealing in sale and purchases of goods that are exempted from VAT

regulations are not required to get registered (VAT registration, 2018). Insurance service and

education business is exempt from VAT regulations. Organisations can also make voluntary

2

Revenue and customs (HMRC) is responsible for making sure money is available with

the government to fund UK's public services and for helping families and individuals. HMRC set

out to use digital communications to help customers to get their tax affairs right by improving

access to information and increasing usage. Individuals, small businesses and agents consumer

survey supports business strategy of HMRC (Boadway and Song, 2016). Organisation is

committed to supporting tax credits consumers to claim the tax credit they are entitled to.

Providing communication channels that are effective and meet consumers needs is the key to

achieve the set goals. Organisations can interact with HMRC by phoning the tax credits

helplines, writing to the organisation and by visiting local enquiry centre. HMRC to have

effective communication with the business entities has introduced digital channels of

communication. This online system helps businesses to get the required information quickly.

Providing online interaction enhance more ways of communication to the general public.

Communication to HMRC reduces confusions and conflicts between business organisations and

government entities.

1.3 Requirements of VAT registration

Business organisations needs to get registered under VAT regulations when turnover is

expected to goes over £85,000 in next 30 days. Another condition is when VAT taxable turnover

is more then £85,000 over the last 12 months. To apply for VAT registration there are two

methods one is online and other is through filling a written form. To register for VAT

application must be filled to HM Revenue and customs department. For online registration form

is filled with VAT online service with HMEC. VAT registration certificate is provided within 14

working days. Documents that are required for registration are as follows-

Unique Taxpayer's Reference number(UTR)

Permanent Account Number

Certificate of incorporation and details of business

Turnover details of the company

Past two years information of the company

Businesses that are dealing in sale and purchases of goods that are exempted from VAT

regulations are not required to get registered (VAT registration, 2018). Insurance service and

education business is exempt from VAT regulations. Organisations can also make voluntary

2

registration under VAT without crossing the turnover limit of £85,000. companies that are not

established in UK and business activities are performed in UK then VAT registration can be

done on the basis of place of performance of business activities.

1.4 Information that must be included on business documents of VAT registered businesses

Businesses that are registered under VAT have unique registration number and become a

business entity in the eyes of the government (Figari and Paulus, 2012). Registration under VAT

increases documentation of the business as all the information regarding business is required to

be recorded. After registration following information must be included in business documents-

Unique Corporate Identification Number of businesses

Time and date of supply of goods must be intentioned in invoice

Name, address and registration number of the supplier must be maintained in the invoice.

Each goods are provided with identification number that number must be maintained in

the invoice

Rate of VAT that is applied on the goods must be mentioned

Discount offered by the organisation must be maintained in the documents

Invoices that are issued by the business entity must contain VAT registration number so

that credit can be availed for the input VAT amount.

1.5 Requirements and frequency of reporting of following VAT schemes

Business organisations that are registered under VAT finds it difficult to keep record

various business transactions and comply with the regulations of the VAT act. Returns for the

VAT registered needs to be filled on regular basis to avoid any legal complications with the

government department. These schemes helps in improving cash flow and if turnover is below £

1.35 million then it is beneficial for businesses (VAT accounting schemes, 2019).

Annual accounting: This scheme allows business organisations to pay VAT on account

in either nine monthly or three quarterly payments. A single annual VAT return which is

used to work out any balance owned by businesses or due from HMRC. During the year

instalment is based on an estimated liability for the year and balance is paid with the

return filled. This scheme helps in budgeting and reduces paperwork.

Cash accounting: The cash accounting VAT scheme is a method of reporting taxes on

the basis of payments made or received. This scheme follows the principals of cash

accounting and income is recorded when it is received and expenses are recorded in the

3

established in UK and business activities are performed in UK then VAT registration can be

done on the basis of place of performance of business activities.

1.4 Information that must be included on business documents of VAT registered businesses

Businesses that are registered under VAT have unique registration number and become a

business entity in the eyes of the government (Figari and Paulus, 2012). Registration under VAT

increases documentation of the business as all the information regarding business is required to

be recorded. After registration following information must be included in business documents-

Unique Corporate Identification Number of businesses

Time and date of supply of goods must be intentioned in invoice

Name, address and registration number of the supplier must be maintained in the invoice.

Each goods are provided with identification number that number must be maintained in

the invoice

Rate of VAT that is applied on the goods must be mentioned

Discount offered by the organisation must be maintained in the documents

Invoices that are issued by the business entity must contain VAT registration number so

that credit can be availed for the input VAT amount.

1.5 Requirements and frequency of reporting of following VAT schemes

Business organisations that are registered under VAT finds it difficult to keep record

various business transactions and comply with the regulations of the VAT act. Returns for the

VAT registered needs to be filled on regular basis to avoid any legal complications with the

government department. These schemes helps in improving cash flow and if turnover is below £

1.35 million then it is beneficial for businesses (VAT accounting schemes, 2019).

Annual accounting: This scheme allows business organisations to pay VAT on account

in either nine monthly or three quarterly payments. A single annual VAT return which is

used to work out any balance owned by businesses or due from HMRC. During the year

instalment is based on an estimated liability for the year and balance is paid with the

return filled. This scheme helps in budgeting and reduces paperwork.

Cash accounting: The cash accounting VAT scheme is a method of reporting taxes on

the basis of payments made or received. This scheme follows the principals of cash

accounting and income is recorded when it is received and expenses are recorded in the

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

period they paid. This resolves the issue that involves in regarding to the pre payments of

taxes made before their realisation (Savage and Callan, 2015).

Flat-rate scheme: Rate of tax differs on the basis of various goods. Flat rate scheme

helps small businesses to simplify VAT returns. Flat rate is used depends on the industry

and same amount of VAT is paid to HMRC as if full calculation of VAT is carried out.

Requirements to apply this scheme is that taxable turnover of the business organisation in

the next year will be no more then £150000. once this scheme is adopted then will

continue to apply until total business income exceeds £230000.

Standard rate scheme: Under standard rate scheme quarterly VAT return will be filled

on the basis on the basis of sales and cost. Payment of VAT amount will be the difference

between the input tax and output tax. This reduces problem of cash flow for small

businesses.

1.6 Maintain an up-to-date knowledge of changes to code of practice, regulation or legislation

Every organisation needs to have up-to-date knowledge of changes to code of practice,

regulation or legislation to perform all the business activities effectively. Maintaining full record

of the changes proper knowledge of the statistics is required. Keeping the changes recorded

helps to prepare all the financial and accounting documents more reliable as all the regulations

are complied with to prepare the records (Hillman, 2013). Code of practice, legislation and

regulations that are followed by business entities provides smooth functioning of business

operations. Government regulations are effectively complied and quality of recording various

business transactions are improved with current and improved knowledge. Changes in code of

conduct and regulations are based on the issues that arises by following current regulations.

Updated knowledge of code of conduct and legislations reduces loop holes that creates various

issues in the businesses. Preparing financial documents and managing business as per new code

of conduct reduces government intervention. This also increases public image of the business

that follows all the legal compliances.

TASK 2

2.1 Extract relevant data for a specific period from the accounting system

Extraction of data for filling the return of VAT for the quarter ending 31st December,

2018 (Jaramillo Baanante, 2013).

4

taxes made before their realisation (Savage and Callan, 2015).

Flat-rate scheme: Rate of tax differs on the basis of various goods. Flat rate scheme

helps small businesses to simplify VAT returns. Flat rate is used depends on the industry

and same amount of VAT is paid to HMRC as if full calculation of VAT is carried out.

Requirements to apply this scheme is that taxable turnover of the business organisation in

the next year will be no more then £150000. once this scheme is adopted then will

continue to apply until total business income exceeds £230000.

Standard rate scheme: Under standard rate scheme quarterly VAT return will be filled

on the basis on the basis of sales and cost. Payment of VAT amount will be the difference

between the input tax and output tax. This reduces problem of cash flow for small

businesses.

1.6 Maintain an up-to-date knowledge of changes to code of practice, regulation or legislation

Every organisation needs to have up-to-date knowledge of changes to code of practice,

regulation or legislation to perform all the business activities effectively. Maintaining full record

of the changes proper knowledge of the statistics is required. Keeping the changes recorded

helps to prepare all the financial and accounting documents more reliable as all the regulations

are complied with to prepare the records (Hillman, 2013). Code of practice, legislation and

regulations that are followed by business entities provides smooth functioning of business

operations. Government regulations are effectively complied and quality of recording various

business transactions are improved with current and improved knowledge. Changes in code of

conduct and regulations are based on the issues that arises by following current regulations.

Updated knowledge of code of conduct and legislations reduces loop holes that creates various

issues in the businesses. Preparing financial documents and managing business as per new code

of conduct reduces government intervention. This also increases public image of the business

that follows all the legal compliances.

TASK 2

2.1 Extract relevant data for a specific period from the accounting system

Extraction of data for filling the return of VAT for the quarter ending 31st December,

2018 (Jaramillo Baanante, 2013).

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

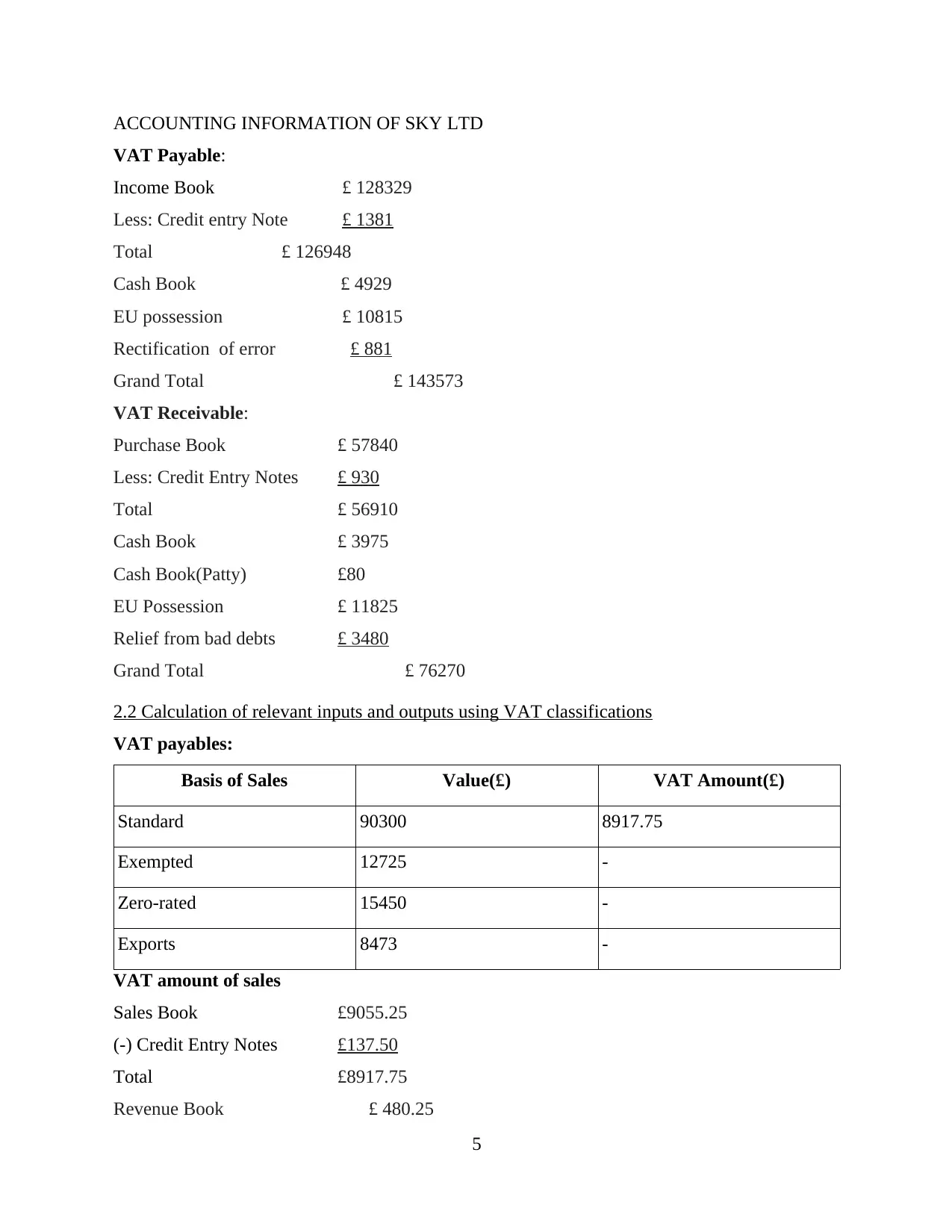

ACCOUNTING INFORMATION OF SKY LTD

VAT Payable:

Income Book £ 128329

Less: Credit entry Note £ 1381

Total £ 126948

Cash Book £ 4929

EU possession £ 10815

Rectification of error £ 881

Grand Total £ 143573

VAT Receivable:

Purchase Book £ 57840

Less: Credit Entry Notes £ 930

Total £ 56910

Cash Book £ 3975

Cash Book(Patty) £80

EU Possession £ 11825

Relief from bad debts £ 3480

Grand Total £ 76270

2.2 Calculation of relevant inputs and outputs using VAT classifications

VAT payables:

Basis of Sales Value(£) VAT Amount(£)

Standard 90300 8917.75

Exempted 12725 -

Zero-rated 15450 -

Exports 8473 -

VAT amount of sales

Sales Book £9055.25

(-) Credit Entry Notes £137.50

Total £8917.75

Revenue Book £ 480.25

5

VAT Payable:

Income Book £ 128329

Less: Credit entry Note £ 1381

Total £ 126948

Cash Book £ 4929

EU possession £ 10815

Rectification of error £ 881

Grand Total £ 143573

VAT Receivable:

Purchase Book £ 57840

Less: Credit Entry Notes £ 930

Total £ 56910

Cash Book £ 3975

Cash Book(Patty) £80

EU Possession £ 11825

Relief from bad debts £ 3480

Grand Total £ 76270

2.2 Calculation of relevant inputs and outputs using VAT classifications

VAT payables:

Basis of Sales Value(£) VAT Amount(£)

Standard 90300 8917.75

Exempted 12725 -

Zero-rated 15450 -

Exports 8473 -

VAT amount of sales

Sales Book £9055.25

(-) Credit Entry Notes £137.50

Total £8917.75

Revenue Book £ 480.25

5

EU possession £ 1055

Rectification of error £ 87.85

Grand Total £10540.85

VAT Receivable:

Basis of Purchase Value(£) VAT Amount(£)

Standard 37630 5162.5

Exempted 7810 -

Zero-rated 6480 -

Exports 4990 -

VAT amount on Purchases

Purchase Book £ 5250

Less: Credit Entry Notes £ 87.5

Total £ 5337.5

Cash Book £ 375

Cash Book(Patty) £ 8

EU Possession £ 1050

Relief from bad debts £ 337.5

Grand Total £ 7108

NOTE:

EU possession includes purchases made from another European Union country.

Relief of bad debts means amount that is written as bad debts in books are returned by a

debtor and considered as revenue (Jaramillo, 2014).

Amount of petty cash is £ 750 and amount of VAT is £ 15.95 taken from VAT column in

cash or revenue book.

Correction of error includes amount of VAT that is also required to be adjusted.

2.3 Calculation of VAT due to, or from the relevant tax authority

HMRC is authorised to collect tax for the amount of VAT IN UK. Calculations for the

amount of VAT due to and due from is as follows:

6

Rectification of error £ 87.85

Grand Total £10540.85

VAT Receivable:

Basis of Purchase Value(£) VAT Amount(£)

Standard 37630 5162.5

Exempted 7810 -

Zero-rated 6480 -

Exports 4990 -

VAT amount on Purchases

Purchase Book £ 5250

Less: Credit Entry Notes £ 87.5

Total £ 5337.5

Cash Book £ 375

Cash Book(Patty) £ 8

EU Possession £ 1050

Relief from bad debts £ 337.5

Grand Total £ 7108

NOTE:

EU possession includes purchases made from another European Union country.

Relief of bad debts means amount that is written as bad debts in books are returned by a

debtor and considered as revenue (Jaramillo, 2014).

Amount of petty cash is £ 750 and amount of VAT is £ 15.95 taken from VAT column in

cash or revenue book.

Correction of error includes amount of VAT that is also required to be adjusted.

2.3 Calculation of VAT due to, or from the relevant tax authority

HMRC is authorised to collect tax for the amount of VAT IN UK. Calculations for the

amount of VAT due to and due from is as follows:

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

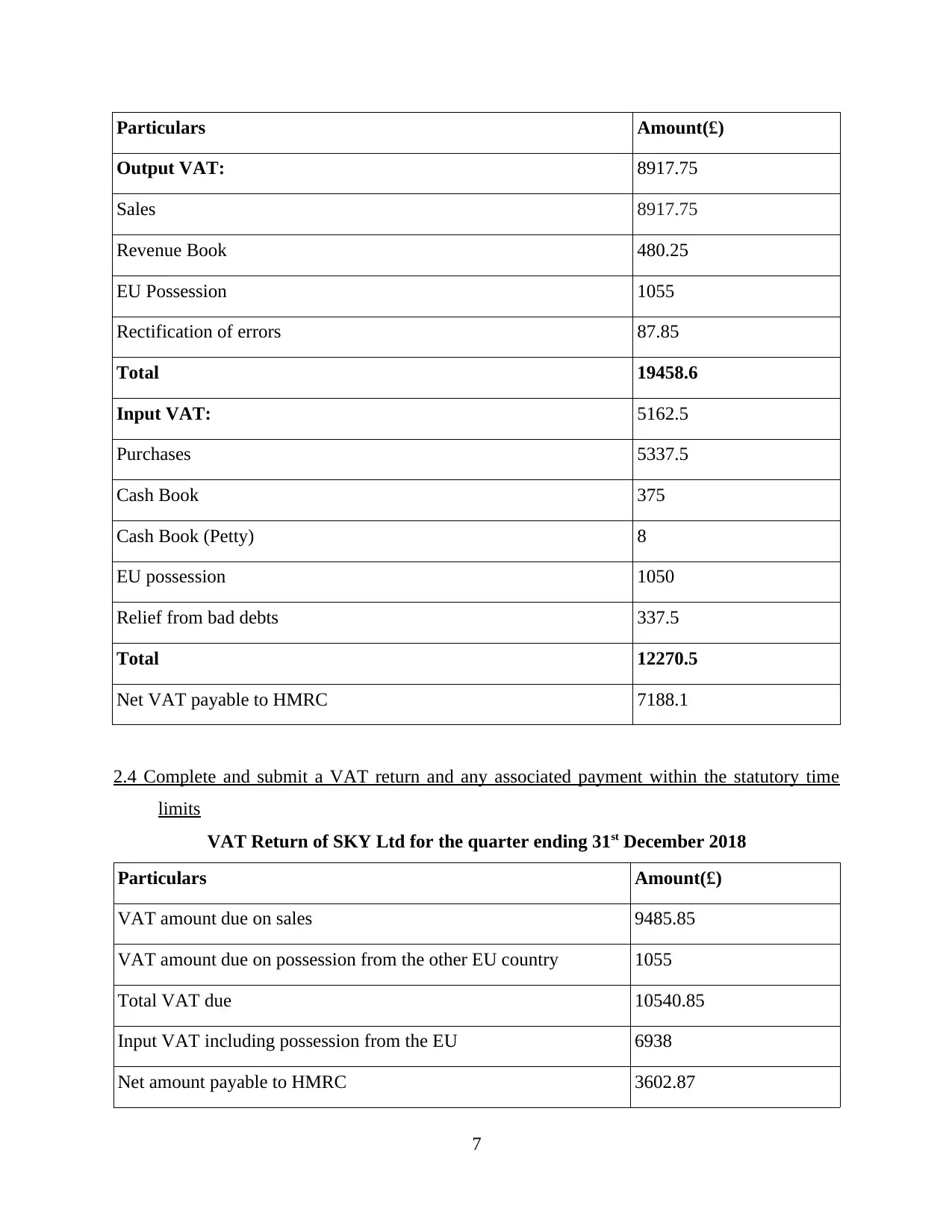

Particulars Amount(£)

Output VAT: 8917.75

Sales 8917.75

Revenue Book 480.25

EU Possession 1055

Rectification of errors 87.85

Total 19458.6

Input VAT: 5162.5

Purchases 5337.5

Cash Book 375

Cash Book (Petty) 8

EU possession 1050

Relief from bad debts 337.5

Total 12270.5

Net VAT payable to HMRC 7188.1

2.4 Complete and submit a VAT return and any associated payment within the statutory time

limits

VAT Return of SKY Ltd for the quarter ending 31st December 2018

Particulars Amount(£)

VAT amount due on sales 9485.85

VAT amount due on possession from the other EU country 1055

Total VAT due 10540.85

Input VAT including possession from the EU 6938

Net amount payable to HMRC 3602.87

7

Output VAT: 8917.75

Sales 8917.75

Revenue Book 480.25

EU Possession 1055

Rectification of errors 87.85

Total 19458.6

Input VAT: 5162.5

Purchases 5337.5

Cash Book 375

Cash Book (Petty) 8

EU possession 1050

Relief from bad debts 337.5

Total 12270.5

Net VAT payable to HMRC 7188.1

2.4 Complete and submit a VAT return and any associated payment within the statutory time

limits

VAT Return of SKY Ltd for the quarter ending 31st December 2018

Particulars Amount(£)

VAT amount due on sales 9485.85

VAT amount due on possession from the other EU country 1055

Total VAT due 10540.85

Input VAT including possession from the EU 6938

Net amount payable to HMRC 3602.87

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

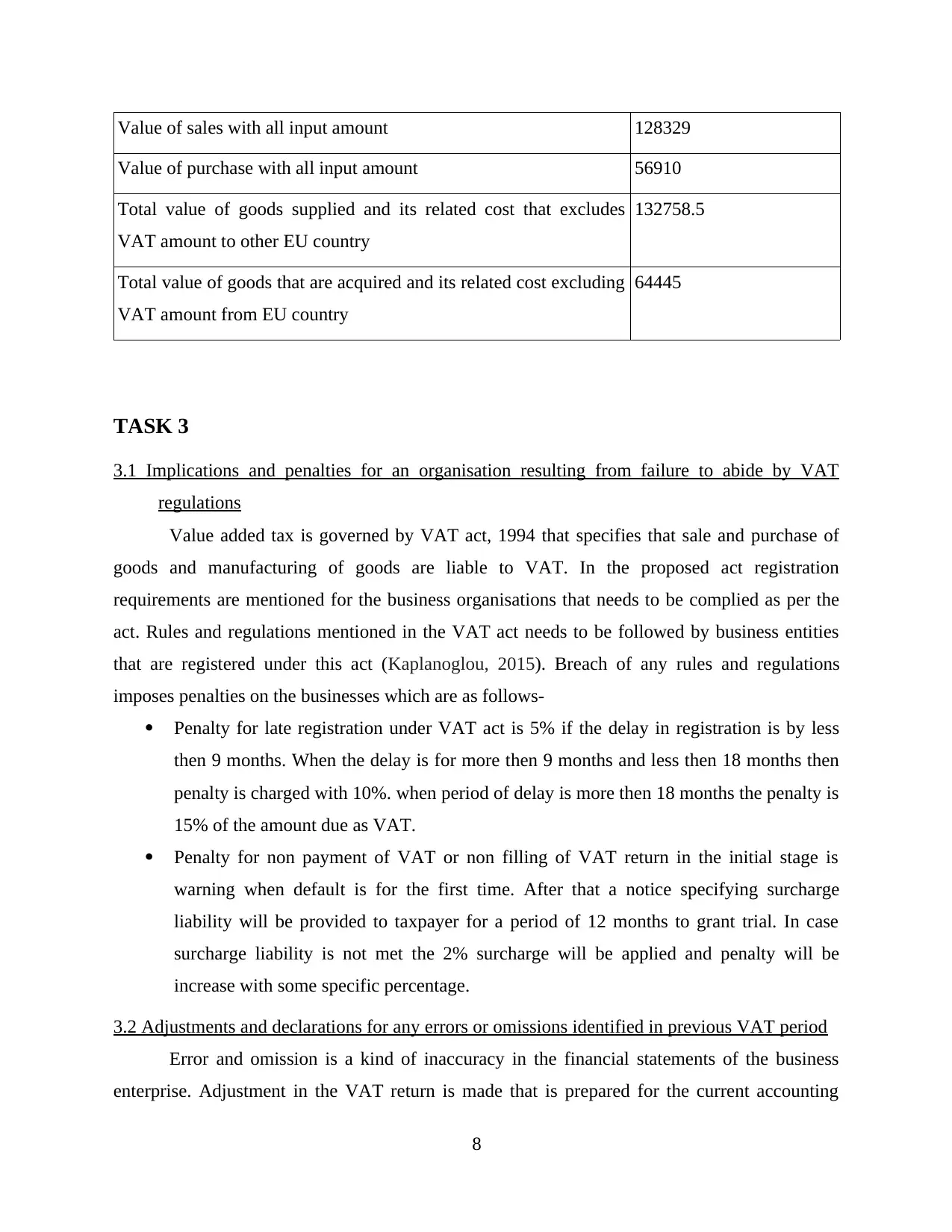

Value of sales with all input amount 128329

Value of purchase with all input amount 56910

Total value of goods supplied and its related cost that excludes

VAT amount to other EU country

132758.5

Total value of goods that are acquired and its related cost excluding

VAT amount from EU country

64445

TASK 3

3.1 Implications and penalties for an organisation resulting from failure to abide by VAT

regulations

Value added tax is governed by VAT act, 1994 that specifies that sale and purchase of

goods and manufacturing of goods are liable to VAT. In the proposed act registration

requirements are mentioned for the business organisations that needs to be complied as per the

act. Rules and regulations mentioned in the VAT act needs to be followed by business entities

that are registered under this act (Kaplanoglou, 2015). Breach of any rules and regulations

imposes penalties on the businesses which are as follows-

Penalty for late registration under VAT act is 5% if the delay in registration is by less

then 9 months. When the delay is for more then 9 months and less then 18 months then

penalty is charged with 10%. when period of delay is more then 18 months the penalty is

15% of the amount due as VAT.

Penalty for non payment of VAT or non filling of VAT return in the initial stage is

warning when default is for the first time. After that a notice specifying surcharge

liability will be provided to taxpayer for a period of 12 months to grant trial. In case

surcharge liability is not met the 2% surcharge will be applied and penalty will be

increase with some specific percentage.

3.2 Adjustments and declarations for any errors or omissions identified in previous VAT period

Error and omission is a kind of inaccuracy in the financial statements of the business

enterprise. Adjustment in the VAT return is made that is prepared for the current accounting

8

Value of purchase with all input amount 56910

Total value of goods supplied and its related cost that excludes

VAT amount to other EU country

132758.5

Total value of goods that are acquired and its related cost excluding

VAT amount from EU country

64445

TASK 3

3.1 Implications and penalties for an organisation resulting from failure to abide by VAT

regulations

Value added tax is governed by VAT act, 1994 that specifies that sale and purchase of

goods and manufacturing of goods are liable to VAT. In the proposed act registration

requirements are mentioned for the business organisations that needs to be complied as per the

act. Rules and regulations mentioned in the VAT act needs to be followed by business entities

that are registered under this act (Kaplanoglou, 2015). Breach of any rules and regulations

imposes penalties on the businesses which are as follows-

Penalty for late registration under VAT act is 5% if the delay in registration is by less

then 9 months. When the delay is for more then 9 months and less then 18 months then

penalty is charged with 10%. when period of delay is more then 18 months the penalty is

15% of the amount due as VAT.

Penalty for non payment of VAT or non filling of VAT return in the initial stage is

warning when default is for the first time. After that a notice specifying surcharge

liability will be provided to taxpayer for a period of 12 months to grant trial. In case

surcharge liability is not met the 2% surcharge will be applied and penalty will be

increase with some specific percentage.

3.2 Adjustments and declarations for any errors or omissions identified in previous VAT period

Error and omission is a kind of inaccuracy in the financial statements of the business

enterprise. Adjustment in the VAT return is made that is prepared for the current accounting

8

period (Karanfil and Özkaya, 2013). As per section 4 of VAT act, adjustments can be made if the

errors fall under any criteria mentioned bellow-

Reporting of the transaction is done below threshold

Financial statements are presented but they are not deliberated

Errors must be related to the accounting period that ends less then 4 years ago

Adjustment regarding errors in the VAT return can be made when the amount involved is

£10000 or less. HMRC must be reported about the errors that are related to VAT return in form

VAT652. This form is submitted through online site to the error correction team. Deliberated

errors must be reported separately to HMRC in writing along with the supporting documents.

There are two methods of reporting an error-

Method 1: If the net value involved in the error does not exceed £10000 or it is between

£10000 and £50000 but do not exceed 1% of the net output value of VAT for a period. .

Method 2: This method is adopted when net value is between £10000 and £50000 that

can exceed up to £5000000.

TASK 4

4.1 Information to managers of the impact that VAT payments may have on an organisation's

cash flow and financial forecasts

Payment of taxes have a huge impact on the financial position of the company as cash

flows are affected by payments. Amount of tax paid by business entities is more then amount

generated as inflow as input taxes is considered as negative position (Kumar, 2014). All the

activities of the business are related with availability of finances in the company. Businesses

grants credit to its distributors to run the business and gain a competitive advantage. There is a

time gap between sales and realisation of revenue. Taxes are paid to the government on the basis

of sales made irrespective of the collection is made or not. This is a complex situation for

organisations as revenue is not realised yet and burden of tax rises. Managers of the businesses

makes planning for future activities and it is effected by the cash flow position of the company.

They must be informed about all the information that may affect their future planning to achieve

organisational goals.

9

errors fall under any criteria mentioned bellow-

Reporting of the transaction is done below threshold

Financial statements are presented but they are not deliberated

Errors must be related to the accounting period that ends less then 4 years ago

Adjustment regarding errors in the VAT return can be made when the amount involved is

£10000 or less. HMRC must be reported about the errors that are related to VAT return in form

VAT652. This form is submitted through online site to the error correction team. Deliberated

errors must be reported separately to HMRC in writing along with the supporting documents.

There are two methods of reporting an error-

Method 1: If the net value involved in the error does not exceed £10000 or it is between

£10000 and £50000 but do not exceed 1% of the net output value of VAT for a period. .

Method 2: This method is adopted when net value is between £10000 and £50000 that

can exceed up to £5000000.

TASK 4

4.1 Information to managers of the impact that VAT payments may have on an organisation's

cash flow and financial forecasts

Payment of taxes have a huge impact on the financial position of the company as cash

flows are affected by payments. Amount of tax paid by business entities is more then amount

generated as inflow as input taxes is considered as negative position (Kumar, 2014). All the

activities of the business are related with availability of finances in the company. Businesses

grants credit to its distributors to run the business and gain a competitive advantage. There is a

time gap between sales and realisation of revenue. Taxes are paid to the government on the basis

of sales made irrespective of the collection is made or not. This is a complex situation for

organisations as revenue is not realised yet and burden of tax rises. Managers of the businesses

makes planning for future activities and it is effected by the cash flow position of the company.

They must be informed about all the information that may affect their future planning to achieve

organisational goals.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.