Comprehensive VAT and Indirect Tax Report - Finance Module

VerifiedAdded on 2021/01/08

|15

|3527

|42

Report

AI Summary

This report provides a comprehensive overview of Value Added Tax (VAT) in the UK, covering various aspects from the sources of VAT information, interaction with government agencies like HMRC, and the requirements for VAT registration. It delves into the information that must be included in business documentation for VAT-registered businesses, explores different VAT schemes used for reporting purposes, and emphasizes the importance of staying updated with relevant changes in legislation and codes of practice. The report also details the process of extracting data from accounting systems, calculating input and output VAT, and determining the VAT due to or from the tax authority. Furthermore, it addresses the implications and penalties for organizations failing to comply with VAT regulations and outlines the procedures for adjustments and declarations related to errors or omissions. Finally, the report discusses the importance of informing managers about the impact of VAT payments on cash flow and financial forecasts, as well as advising on changes in VAT legislation affecting recording systems.

INDIRECT TAX

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1 ..........................................................................................................................................3

1.1 Source of information on VAT..............................................................................................3

1.2 How organisation interact with government agency.............................................................3

1.3 Requirements of VAT registration.........................................................................................4

1.4 Information that must be included on business documentation of VAT registered business 5

1.5 VAT schemes required for reporting purposes......................................................................5

1.6 Be aware about relevant changes of legislation and codes of practices................................6

TASK 2............................................................................................................................................7

2.1 Extraction of Data from the accounting system.....................................................................7

2.2 Calculation of input and output for various VAT classifications sated payment under

statutory time limits.....................................................................................................................8

2.3 Calculating VAT due to/from the relevant tax authority.......................................................8

2.4 VAT return and any associated payment within the statutory time limit..............................9

TASK 3..........................................................................................................................................10

3.1 Implications and Penalties for an organisation resulting from failure to abide by VAT

regulations..................................................................................................................................10

3.2 Adjustments and declarations for any errors or omissions identified in previous VAT

periods........................................................................................................................................10

TASK 4..........................................................................................................................................12

4.1 Informing managers of the impact that the VAT payment may have on an organisation’s

cash flow and financial forecasts...............................................................................................12

4.2 Advise for changes in VAT legislation which would have an effect on an organisation’s

recording systems.......................................................................................................................12

CONCLUSION..............................................................................................................................13

REFERENCES .............................................................................................................................14

INTRODUCTION...........................................................................................................................3

TASK 1 ..........................................................................................................................................3

1.1 Source of information on VAT..............................................................................................3

1.2 How organisation interact with government agency.............................................................3

1.3 Requirements of VAT registration.........................................................................................4

1.4 Information that must be included on business documentation of VAT registered business 5

1.5 VAT schemes required for reporting purposes......................................................................5

1.6 Be aware about relevant changes of legislation and codes of practices................................6

TASK 2............................................................................................................................................7

2.1 Extraction of Data from the accounting system.....................................................................7

2.2 Calculation of input and output for various VAT classifications sated payment under

statutory time limits.....................................................................................................................8

2.3 Calculating VAT due to/from the relevant tax authority.......................................................8

2.4 VAT return and any associated payment within the statutory time limit..............................9

TASK 3..........................................................................................................................................10

3.1 Implications and Penalties for an organisation resulting from failure to abide by VAT

regulations..................................................................................................................................10

3.2 Adjustments and declarations for any errors or omissions identified in previous VAT

periods........................................................................................................................................10

TASK 4..........................................................................................................................................12

4.1 Informing managers of the impact that the VAT payment may have on an organisation’s

cash flow and financial forecasts...............................................................................................12

4.2 Advise for changes in VAT legislation which would have an effect on an organisation’s

recording systems.......................................................................................................................12

CONCLUSION..............................................................................................................................13

REFERENCES .............................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

In accounting term, indirect tax is commonly known as tax levy on firm or an individual

that have to paid by the third party to the government. In general it is defined as the tax collected

by the an organisation through supply chain procedure and that is further given to legal

authorities of the nation (Bahl, 2018). There are different types of tax such as sales tax or VAT,

excise duty, good and service tax etc. Indirect tax are not directly paid by the consumer to the

governance agency but the tax burden remain on the customer as they use different services or

buy different goods.

In this report, important information regarding to VAT rules, sources, registration

requirement etc. are shown. Report also discussed significant data relevant to VAT penalties and

specific adjustment and modification. Beside this report also described VAT return of current

and previous accounting year so that crucial decision can be taken.

TASK 1

1.1 Source of information on VAT

VAT is a kind of indirect tax that is basically imposed on the consumption of a particular

product and services and add values throughout the entire production process from point of

manufacture to sales. In UK this tax was introduced in 1973 and become the 3 largest source of

income to the government that help to invest that amount for the betterment of country.

Therefore it is very important to identify the different sources of information on VAT before

charging it on companies operation business in UK. Some of the common source of information

of value added tax is registration process of Taxpayer such as tax return paper, general reports

and statements, VAT annexes, information from tax payments, acknowledgement, form tax

department, risk analysis administration etc. Other sources of information related to VAT is that

companies can directly check the portal of HMRC and collect the suitable information to pay tax

and apply specific rules and regulation.

1.2 How organisation interact with government agency.

It is observed that while registering for VAT individual firm and large organisation must

follow the following procedure that have been formulated by UK government (Cnossen, 2013).

There are different step in the registration process such has form filling and other relevant

information. Thus it is assumed that companies find some problem while making themselves

In accounting term, indirect tax is commonly known as tax levy on firm or an individual

that have to paid by the third party to the government. In general it is defined as the tax collected

by the an organisation through supply chain procedure and that is further given to legal

authorities of the nation (Bahl, 2018). There are different types of tax such as sales tax or VAT,

excise duty, good and service tax etc. Indirect tax are not directly paid by the consumer to the

governance agency but the tax burden remain on the customer as they use different services or

buy different goods.

In this report, important information regarding to VAT rules, sources, registration

requirement etc. are shown. Report also discussed significant data relevant to VAT penalties and

specific adjustment and modification. Beside this report also described VAT return of current

and previous accounting year so that crucial decision can be taken.

TASK 1

1.1 Source of information on VAT

VAT is a kind of indirect tax that is basically imposed on the consumption of a particular

product and services and add values throughout the entire production process from point of

manufacture to sales. In UK this tax was introduced in 1973 and become the 3 largest source of

income to the government that help to invest that amount for the betterment of country.

Therefore it is very important to identify the different sources of information on VAT before

charging it on companies operation business in UK. Some of the common source of information

of value added tax is registration process of Taxpayer such as tax return paper, general reports

and statements, VAT annexes, information from tax payments, acknowledgement, form tax

department, risk analysis administration etc. Other sources of information related to VAT is that

companies can directly check the portal of HMRC and collect the suitable information to pay tax

and apply specific rules and regulation.

1.2 How organisation interact with government agency.

It is observed that while registering for VAT individual firm and large organisation must

follow the following procedure that have been formulated by UK government (Cnossen, 2013).

There are different step in the registration process such has form filling and other relevant

information. Thus it is assumed that companies find some problem while making themselves

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

register for VAT. Therefore government agency of UK have developed different methods for

organisation that help them to directly or indirectly interact with these agency and get the detail

information. UK governance have established HMRC that is responsible to provide basic

knowledge about the Tax laws and standard and collect VAT for the respective companies.

HMRC have different non ministerial and ministerial department that deliver information to the

management of firm related to VAT. The main duty of department is to acquire the detail

information about the ongoing tax rate, sudden changes in VAT act etc. that further help

companies to repay the annual tax. Government have also published legal online site that will

give best information to the registrar firm operating business in UK.

All the above mention method are useful for existing as well as new organisation that are

operating business in UK to get the exact knowledge about the value added tax rate and other

certain modification that are introduced by government in latest time.

1.3 Requirements of VAT registration

In accounting term, it is observed that companies holding business for more that 85000

pound are liable to register them under VAT. It is very important for an organisation to make

sure that they are dealing with their business in proper manner as they have made VAT

registration or not. This will help to increase their market share and increase goodwill as they are

following standard rules and regulation associated with value added tax. There are different ways

of registering a firm for VAT such as companies may fill the online form as most of the firm are

partnership and want paper less work that help in smooth functioning. Firm may also do offline

registration by hieing an agent that will do the paper work for them and opened VAT account

and provide necessary information such as VAT return, laws and regulation etc. After the

company will have the following VAT number from the HMRC department that help them to

pay the tax for the financial year. They offline process is as follows, like new or existing

companies will have to fill up the form such as VAT1A those are selling their goods from the

other part of nation, VAT1B for the importer and other VAT1C for those companies that are

willing to dispose their following assets (Cnossen, 2013). It is observed that offline registration is

consider to be lengthy process in which VAT number is given to register company after one

month. These number are then deliver individual firm or large organisation with the legal

certificate that they are under the VAT act 1994.

organisation that help them to directly or indirectly interact with these agency and get the detail

information. UK governance have established HMRC that is responsible to provide basic

knowledge about the Tax laws and standard and collect VAT for the respective companies.

HMRC have different non ministerial and ministerial department that deliver information to the

management of firm related to VAT. The main duty of department is to acquire the detail

information about the ongoing tax rate, sudden changes in VAT act etc. that further help

companies to repay the annual tax. Government have also published legal online site that will

give best information to the registrar firm operating business in UK.

All the above mention method are useful for existing as well as new organisation that are

operating business in UK to get the exact knowledge about the value added tax rate and other

certain modification that are introduced by government in latest time.

1.3 Requirements of VAT registration

In accounting term, it is observed that companies holding business for more that 85000

pound are liable to register them under VAT. It is very important for an organisation to make

sure that they are dealing with their business in proper manner as they have made VAT

registration or not. This will help to increase their market share and increase goodwill as they are

following standard rules and regulation associated with value added tax. There are different ways

of registering a firm for VAT such as companies may fill the online form as most of the firm are

partnership and want paper less work that help in smooth functioning. Firm may also do offline

registration by hieing an agent that will do the paper work for them and opened VAT account

and provide necessary information such as VAT return, laws and regulation etc. After the

company will have the following VAT number from the HMRC department that help them to

pay the tax for the financial year. They offline process is as follows, like new or existing

companies will have to fill up the form such as VAT1A those are selling their goods from the

other part of nation, VAT1B for the importer and other VAT1C for those companies that are

willing to dispose their following assets (Cnossen, 2013). It is observed that offline registration is

consider to be lengthy process in which VAT number is given to register company after one

month. These number are then deliver individual firm or large organisation with the legal

certificate that they are under the VAT act 1994.

1.4 Information that must be included on business documentation of VAT registered business

Nowadays, it is very important for large organisation or small companies to include the

crucial and relevant information on the following documents of the VAT registered business. It

is stated that companies have to compulsory to maintain basic business record in the digital

format that will further support to make effective decision for the improvement of companies

market value. Hence, business organisations accomplish this responsibility in a very well manner

since reported proofs of transactions is easy to follow with the certification and enrolment

according to the VAT system. A VAT certified business needs to consider following message

and report for due compliance. There are some important information that is required on the

business documents of registration that are mentioned below:

Date of trading according to business dealing

Yearly figures that are related to VAT

Detail list that shows the name of share holder, director and their holding.

Corporate, VAT number that help to determine the good that are sold by company.

Detail information about the business operation.

A particular document that describe that full address of business such as location, map

etc.

Detail invoice that give the brief knowledge about the supply of relevant product product

within company (Delgado, Lago‐Peñas and Mayor, 2015).

1.5 VAT schemes required for reporting purposes

In accounting term, there are number of VAT schemes that are helpful in reporting

frequency of value added tax as these kind of taxes are recorded and paid on the date of invoice.

It is assumed that business institution applying VAT regulation accountancy strategy are more

accurate and perform well in the competitive market. Some of the assorted reporting schemes are

discussed below:

Annual accounting- This is consider to one of the effective method of VAT act that is

basically valuable to small companies that make easy process for them to submit Vat report. As

this method allows the companies to put forward their single VAT return report on yearly basis.

The main requirement of this scheme is that it support in making annual budgets and cash-flows

statements which aid to reduce the paperwork for accountant. During the year they pay

instalments for expected liability for VAT with the balancing payments due with the return.

Nowadays, it is very important for large organisation or small companies to include the

crucial and relevant information on the following documents of the VAT registered business. It

is stated that companies have to compulsory to maintain basic business record in the digital

format that will further support to make effective decision for the improvement of companies

market value. Hence, business organisations accomplish this responsibility in a very well manner

since reported proofs of transactions is easy to follow with the certification and enrolment

according to the VAT system. A VAT certified business needs to consider following message

and report for due compliance. There are some important information that is required on the

business documents of registration that are mentioned below:

Date of trading according to business dealing

Yearly figures that are related to VAT

Detail list that shows the name of share holder, director and their holding.

Corporate, VAT number that help to determine the good that are sold by company.

Detail information about the business operation.

A particular document that describe that full address of business such as location, map

etc.

Detail invoice that give the brief knowledge about the supply of relevant product product

within company (Delgado, Lago‐Peñas and Mayor, 2015).

1.5 VAT schemes required for reporting purposes

In accounting term, there are number of VAT schemes that are helpful in reporting

frequency of value added tax as these kind of taxes are recorded and paid on the date of invoice.

It is assumed that business institution applying VAT regulation accountancy strategy are more

accurate and perform well in the competitive market. Some of the assorted reporting schemes are

discussed below:

Annual accounting- This is consider to one of the effective method of VAT act that is

basically valuable to small companies that make easy process for them to submit Vat report. As

this method allows the companies to put forward their single VAT return report on yearly basis.

The main requirement of this scheme is that it support in making annual budgets and cash-flows

statements which aid to reduce the paperwork for accountant. During the year they pay

instalments for expected liability for VAT with the balancing payments due with the return.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cash accounting- According to this strategy many small businesses and its finances are

able to prevent them to give over VAT to HMRC. This is because company without individual

receipts of sale from their consumers are not liable to pay tax. It is observed that small and new

business entity gives different credit polices to consumer to gain their commerce and realization

of income gates hold for future period. Imposing taxes earlier than realisation of income develop

difficulty of cash in the business entity. Thus the above mentioned scheme are used to resolve

these kind of issues.

Flat-rate scheme- An optional flat rate scheme is available to businesses for

simplification VAT accounting burden on small businesses with taxable turnover of £150000

(excluding VAT) or less. Adopting this scheme remove burden of detailed records of purchase

and sales. Flat rate percentage varies according to the main business activity of different

organisations (Keen, 2013).

1.6 Be aware about relevant changes of legislation and codes of practices.

It is observed that there are various changes and modification in policies and tax rate by

government of UK that need to consider by each firm operating their business in nation. These

help in managing and controlling business in effective manner. There are favourable information

needed to hold up to date such as:

Software programs

Daily Books of Accounts such as purchase, sales books and credit notes.

Statistical records

Important document that shows part return and rebates concession certificates etc.

able to prevent them to give over VAT to HMRC. This is because company without individual

receipts of sale from their consumers are not liable to pay tax. It is observed that small and new

business entity gives different credit polices to consumer to gain their commerce and realization

of income gates hold for future period. Imposing taxes earlier than realisation of income develop

difficulty of cash in the business entity. Thus the above mentioned scheme are used to resolve

these kind of issues.

Flat-rate scheme- An optional flat rate scheme is available to businesses for

simplification VAT accounting burden on small businesses with taxable turnover of £150000

(excluding VAT) or less. Adopting this scheme remove burden of detailed records of purchase

and sales. Flat rate percentage varies according to the main business activity of different

organisations (Keen, 2013).

1.6 Be aware about relevant changes of legislation and codes of practices.

It is observed that there are various changes and modification in policies and tax rate by

government of UK that need to consider by each firm operating their business in nation. These

help in managing and controlling business in effective manner. There are favourable information

needed to hold up to date such as:

Software programs

Daily Books of Accounts such as purchase, sales books and credit notes.

Statistical records

Important document that shows part return and rebates concession certificates etc.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 2

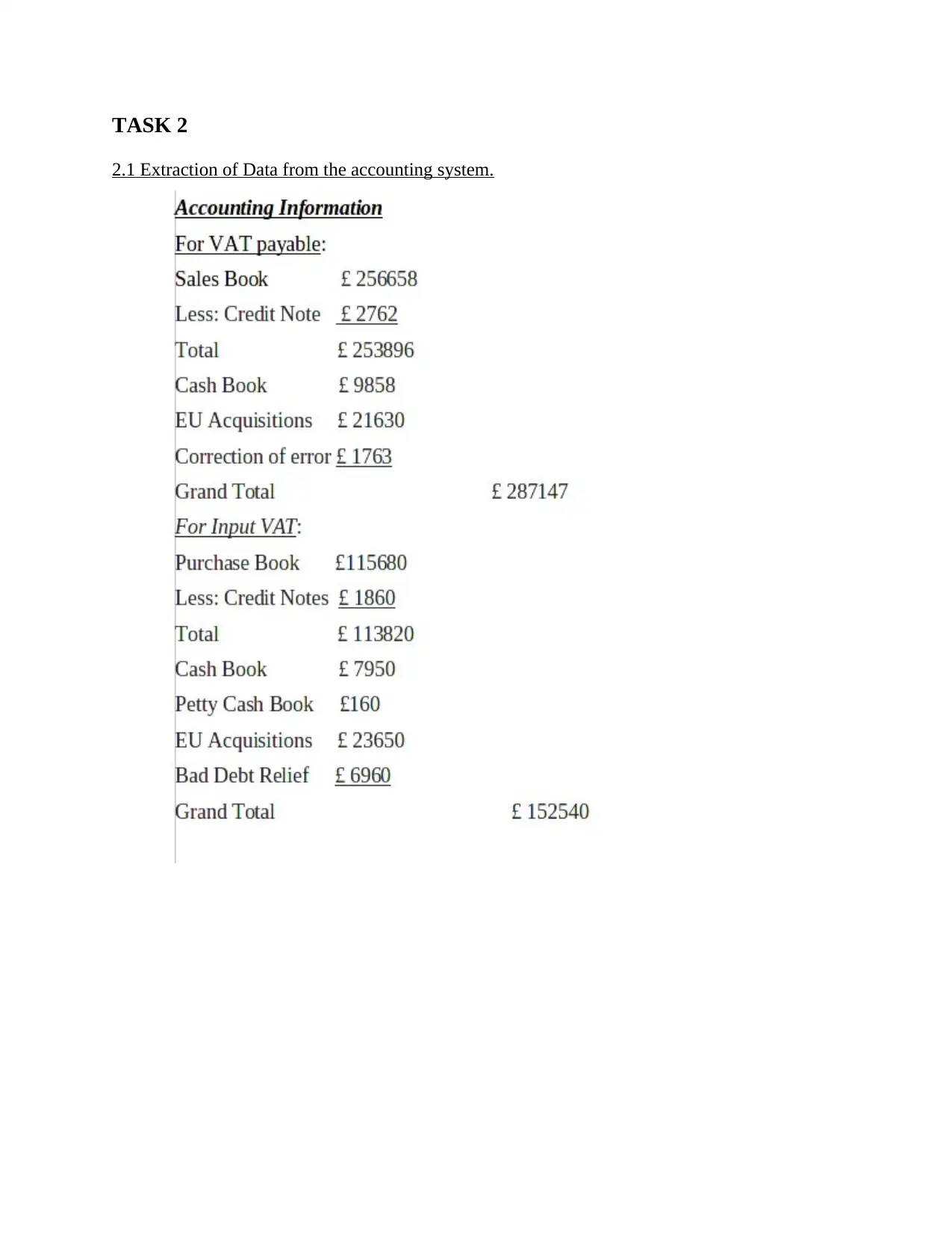

2.1 Extraction of Data from the accounting system.

2.1 Extraction of Data from the accounting system.

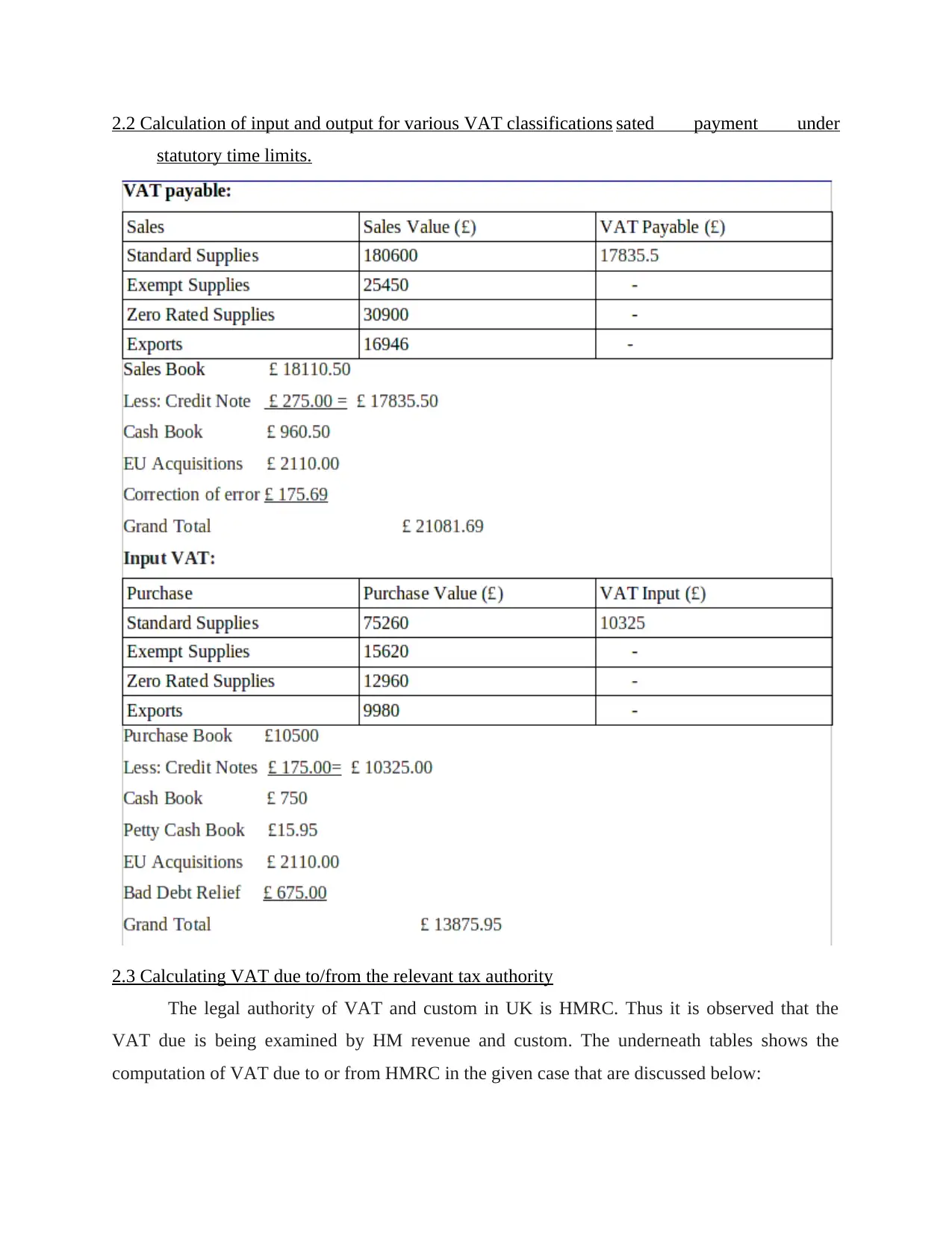

2.2 Calculation of input and output for various VAT classifications sated payment under

statutory time limits.

2.3 Calculating VAT due to/from the relevant tax authority

The legal authority of VAT and custom in UK is HMRC. Thus it is observed that the

VAT due is being examined by HM revenue and custom. The underneath tables shows the

computation of VAT due to or from HMRC in the given case that are discussed below:

statutory time limits.

2.3 Calculating VAT due to/from the relevant tax authority

The legal authority of VAT and custom in UK is HMRC. Thus it is observed that the

VAT due is being examined by HM revenue and custom. The underneath tables shows the

computation of VAT due to or from HMRC in the given case that are discussed below:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

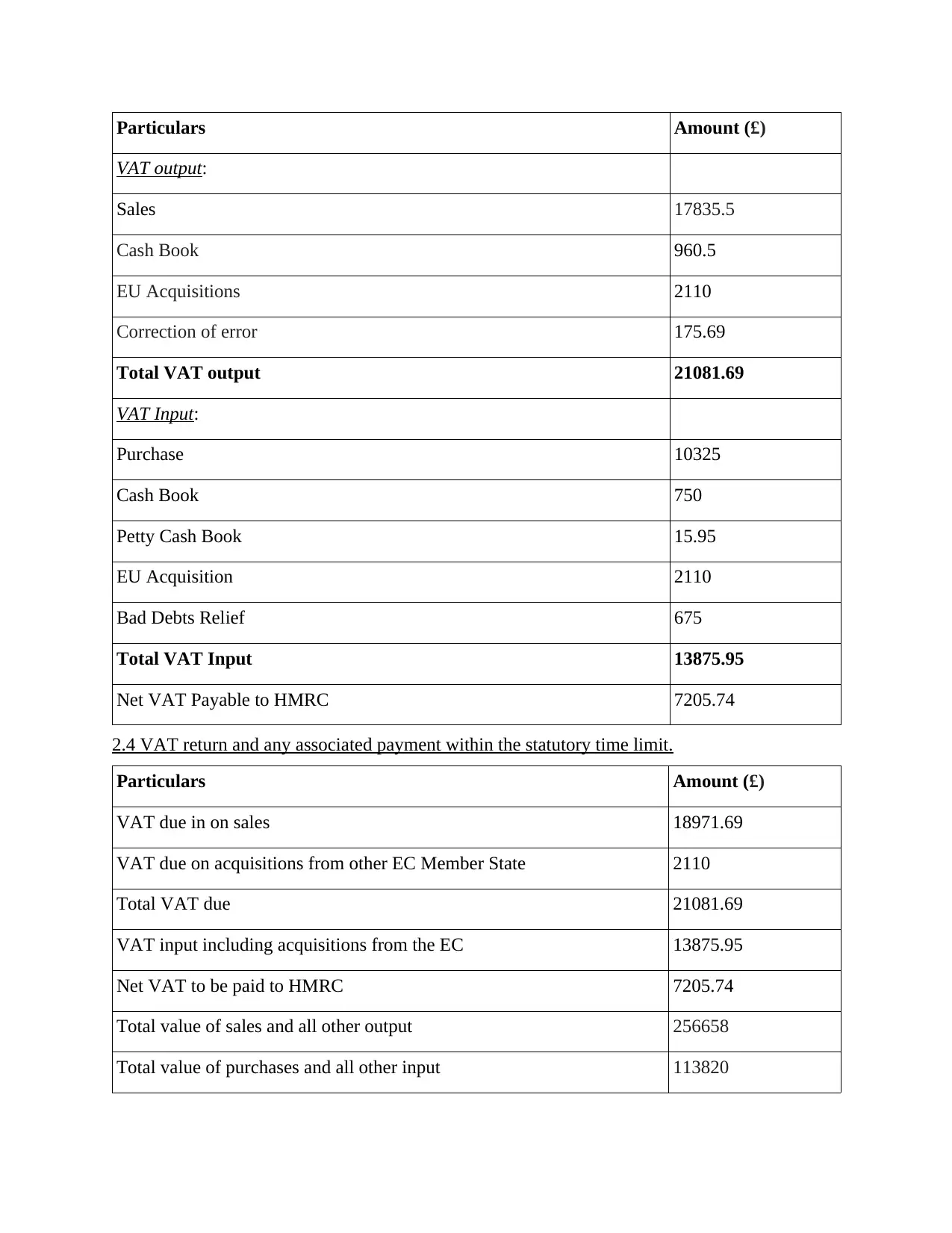

Particulars Amount (£)

VAT output:

Sales 17835.5

Cash Book 960.5

EU Acquisitions 2110

Correction of error 175.69

Total VAT output 21081.69

VAT Input:

Purchase 10325

Cash Book 750

Petty Cash Book 15.95

EU Acquisition 2110

Bad Debts Relief 675

Total VAT Input 13875.95

Net VAT Payable to HMRC 7205.74

2.4 VAT return and any associated payment within the statutory time limit.

Particulars Amount (£)

VAT due in on sales 18971.69

VAT due on acquisitions from other EC Member State 2110

Total VAT due 21081.69

VAT input including acquisitions from the EC 13875.95

Net VAT to be paid to HMRC 7205.74

Total value of sales and all other output 256658

Total value of purchases and all other input 113820

VAT output:

Sales 17835.5

Cash Book 960.5

EU Acquisitions 2110

Correction of error 175.69

Total VAT output 21081.69

VAT Input:

Purchase 10325

Cash Book 750

Petty Cash Book 15.95

EU Acquisition 2110

Bad Debts Relief 675

Total VAT Input 13875.95

Net VAT Payable to HMRC 7205.74

2.4 VAT return and any associated payment within the statutory time limit.

Particulars Amount (£)

VAT due in on sales 18971.69

VAT due on acquisitions from other EC Member State 2110

Total VAT due 21081.69

VAT input including acquisitions from the EC 13875.95

Net VAT to be paid to HMRC 7205.74

Total value of sales and all other output 256658

Total value of purchases and all other input 113820

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Total value of all supplies of goods and related costs, excluding any

VAT, to other EC Member States

265517

Total value of all acquisitions of goods and related costs, excluding any

VAT, from other EC Member States

128890

From the above calculation it has been observed that return for the year ending on 31st

Dec, that will be give to HMRC up-to 7th Feb. It is observed that company have to make payment

of about £7205.74 in this accounting year in case if company is not able to pay the amount then

they have to bear penalties. In order to avoid these charges company follows the VAT Act.

TASK 3

3.1 Implications and Penalties for an organisation resulting from failure to abide by VAT

regulations

If a taxable person, specifically registered VAT businesses, are unable to file their VAT

returns under the applicable schemes and statutory time limits, in that case, the organisation shall

be liable to pay a penalty known as ' Default Surcharge (Kenyon, Langley and Paquin, 2012)'. A

default surcharge is a type of penalty that is imposed on an organisation if they fail to pay their

VAT returns for a period of 12 months from date of filing the return. Within the 12 months

period, only a warning shall be given from HMRC to the concerned business with a penalty of

£100 from the day of default of filing return. This £100 penalty is charged on individual partners

in case of a partnership with only the representative partner having the right to appeal the

decision in court. HMRC has the right to charge penalty between 15% to 100% of the unpaid

amount owed by the business.

3.2 Adjustments and declarations for any errors or omissions identified in previous VAT periods

1. Declaration of errors or omissions identified in previous VAT periods:

It is necessary for registered businesses to declare disclosure of any kind of errors,

omissions or inaccuracies arising in the current or previous VAT periods. The tax authority,

HMRC, requires reporting of such errors by filling form VAT652 that has to be submitted to

VAT Correction Team. These errors can be categorised as follows:

an error identified above reporting threshold.

a deliberate error or a mistake made on purpose

an error made in a VAT period of less than four previous years.

VAT, to other EC Member States

265517

Total value of all acquisitions of goods and related costs, excluding any

VAT, from other EC Member States

128890

From the above calculation it has been observed that return for the year ending on 31st

Dec, that will be give to HMRC up-to 7th Feb. It is observed that company have to make payment

of about £7205.74 in this accounting year in case if company is not able to pay the amount then

they have to bear penalties. In order to avoid these charges company follows the VAT Act.

TASK 3

3.1 Implications and Penalties for an organisation resulting from failure to abide by VAT

regulations

If a taxable person, specifically registered VAT businesses, are unable to file their VAT

returns under the applicable schemes and statutory time limits, in that case, the organisation shall

be liable to pay a penalty known as ' Default Surcharge (Kenyon, Langley and Paquin, 2012)'. A

default surcharge is a type of penalty that is imposed on an organisation if they fail to pay their

VAT returns for a period of 12 months from date of filing the return. Within the 12 months

period, only a warning shall be given from HMRC to the concerned business with a penalty of

£100 from the day of default of filing return. This £100 penalty is charged on individual partners

in case of a partnership with only the representative partner having the right to appeal the

decision in court. HMRC has the right to charge penalty between 15% to 100% of the unpaid

amount owed by the business.

3.2 Adjustments and declarations for any errors or omissions identified in previous VAT periods

1. Declaration of errors or omissions identified in previous VAT periods:

It is necessary for registered businesses to declare disclosure of any kind of errors,

omissions or inaccuracies arising in the current or previous VAT periods. The tax authority,

HMRC, requires reporting of such errors by filling form VAT652 that has to be submitted to

VAT Correction Team. These errors can be categorised as follows:

an error identified above reporting threshold.

a deliberate error or a mistake made on purpose

an error made in a VAT period of less than four previous years.

The error reporting threshold limits an organisation's error frequency to the amount of

£10,000. Any error exceeding this threshold needs to be reported to HMRC ( Lam and Ravussin,

2017). To calculate the threshold, a net value of errors is computed by taking a total of all

additive taxes that are due to HMRC and deducting tax due from this amount. This has been

shown below:

Net Value of Errors = Total Additional tax due to HMRC - Tax Due

Errors or mistakes that have been made on purpose or are deliberate in nature must be

reported separately to HMRC in writing with supporting evidence. The evidence submitted must

include details of date of discovery of error, reasons amounting to cause of such errors and how

it occurred. On the basis of these documents, HMRC shall decide the amount of interest that

needs to be charged or penalty that needs to be paid or no action must be taken against the

organisation in question (Schenk, Thuronyi and Cui,2015).

An error identified in VAT period of less than 4 previous years by HMRC would attract a

certain amount of interest that would be charged against tax due for current period or a charge of

misdeclaration penalty to claim such amounts.

2. Adjustments of errors or omissions identified in previous VAT periods:

In order to address the problem of errors identified in current or previous VAT periods,

the HM Revenue and Customs Department has set up a Penalties for Errors Regime in 2009

under section 4 of the Act. For any type of error adjustments net value of errors must be

computed that would ascertain whether the error falls below or above the reporting threshold.

The adjusted amount can be included in the current VAT providing in following cases:

If the net value does not exceed £10,000 or

If the net value lies between £10,000 and £50,000 but does not exceed 1% of net outputs

mentioned in VAT return declaration for the period in which the error is discovered,

However, if net value of errors does not meet the above criteria or is categorised as a deliberate

error, a separate form- VAT652 must be filled and submitted to HMRC with details describing:

Reasons amounting to cause of such errors

accounting period of discovery of error

Type of error - input or output

Net Value of Errors- both under-declared and over-declared amounts

Computation summary for calculating Net Value

£10,000. Any error exceeding this threshold needs to be reported to HMRC ( Lam and Ravussin,

2017). To calculate the threshold, a net value of errors is computed by taking a total of all

additive taxes that are due to HMRC and deducting tax due from this amount. This has been

shown below:

Net Value of Errors = Total Additional tax due to HMRC - Tax Due

Errors or mistakes that have been made on purpose or are deliberate in nature must be

reported separately to HMRC in writing with supporting evidence. The evidence submitted must

include details of date of discovery of error, reasons amounting to cause of such errors and how

it occurred. On the basis of these documents, HMRC shall decide the amount of interest that

needs to be charged or penalty that needs to be paid or no action must be taken against the

organisation in question (Schenk, Thuronyi and Cui,2015).

An error identified in VAT period of less than 4 previous years by HMRC would attract a

certain amount of interest that would be charged against tax due for current period or a charge of

misdeclaration penalty to claim such amounts.

2. Adjustments of errors or omissions identified in previous VAT periods:

In order to address the problem of errors identified in current or previous VAT periods,

the HM Revenue and Customs Department has set up a Penalties for Errors Regime in 2009

under section 4 of the Act. For any type of error adjustments net value of errors must be

computed that would ascertain whether the error falls below or above the reporting threshold.

The adjusted amount can be included in the current VAT providing in following cases:

If the net value does not exceed £10,000 or

If the net value lies between £10,000 and £50,000 but does not exceed 1% of net outputs

mentioned in VAT return declaration for the period in which the error is discovered,

However, if net value of errors does not meet the above criteria or is categorised as a deliberate

error, a separate form- VAT652 must be filled and submitted to HMRC with details describing:

Reasons amounting to cause of such errors

accounting period of discovery of error

Type of error - input or output

Net Value of Errors- both under-declared and over-declared amounts

Computation summary for calculating Net Value

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.