A Comprehensive Report on VAT Regulations and Compliance in Finance

VerifiedAdded on 2020/12/18

|16

|4419

|216

Report

AI Summary

This report provides a comprehensive overview of Value Added Tax (VAT) regulations, focusing on compliance, reporting, and the implications for businesses. It begins with an introduction to indirect taxes and specifically VAT, explaining its core concept as a tax on the value added to goods and services. The main body delves into understanding VAT regulations, including sources of information like the UK government's HMRC website and publications, and details the interactions between organizations and relevant government agencies. It outlines VAT registration requirements, the information required on business documentation for VAT-registered businesses, the requirements and frequency of reporting for various VAT schemes (annual, cash, flat rate, and standard), and the importance of maintaining knowledge of changes in codes of practice, regulations, and legislation. The report then discusses completing VAT returns accurately and in a timely manner, covering data extraction from accounting systems, calculation of inputs and outputs, calculation of VAT due, and the completion and submission of returns within statutory time limits. It also addresses understanding VAT penalties and making adjustments for previous errors, including implications for non-compliance and procedures for correcting errors. Finally, the report touches on communicating VAT information, specifically informing managers about the impact of VAT payments on cash flows and advising relevant people of changes in VAT legislation's effects on organization's recording system. The report concludes by summarizing the key aspects of VAT regulations and compliance. References to books and journals are also included.

Indirect Tax

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

1 Understand VAT Regulations.......................................................................................................3

1.1 Sources of Information on VAT.......................................................................................3

1.2 Interaction of Organisation with Relevant Government Agency.....................................4

1.3 VAT Registration Requirements......................................................................................4

1.4 Information Included on Business Documentation of VAT Registered Businesses........5

1.5 Requirements and the Frequency of Reporting for VAT Schemes..................................5

1.6 Maintenance of Knowledge of Changes to Codes of Practise, Regulation or Legislation6

2 Complete VAT Returns Accurately and in a Timely Manner......................................................7

2.1 Extract Relevant Data for a Specific Period from the Accounting System......................7

2.2 Calculation of relevant inputs and outputs.......................................................................7

2.3 Calculation of the VAT due to or from the relevant tax authority820.............................9

2.4 Completion and Submission of VAT Return and Payment Associated within the Statutory

Time Limits..........................................................................................................................10

3 Understanding the VAT Penalties and making Adjustments for Previous Errors......................12

3.1 Implications and Penalties for Organisations which Fails to Follow VAT Regulations12

3.2 Making and Adjusting Previously Identified VAT Errors.............................................12

Communicating VAT Information................................................................................................13

4.1 Informing Managers about the Impact of VAT Payment on Cash Flows and Financial

Forecasts of Business...........................................................................................................13

4.2 Advising Relevant People of Changes in VAT Legislation's Effects on Organisations

Recording System.................................................................................................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

Books and Journals...............................................................................................................15

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

1 Understand VAT Regulations.......................................................................................................3

1.1 Sources of Information on VAT.......................................................................................3

1.2 Interaction of Organisation with Relevant Government Agency.....................................4

1.3 VAT Registration Requirements......................................................................................4

1.4 Information Included on Business Documentation of VAT Registered Businesses........5

1.5 Requirements and the Frequency of Reporting for VAT Schemes..................................5

1.6 Maintenance of Knowledge of Changes to Codes of Practise, Regulation or Legislation6

2 Complete VAT Returns Accurately and in a Timely Manner......................................................7

2.1 Extract Relevant Data for a Specific Period from the Accounting System......................7

2.2 Calculation of relevant inputs and outputs.......................................................................7

2.3 Calculation of the VAT due to or from the relevant tax authority820.............................9

2.4 Completion and Submission of VAT Return and Payment Associated within the Statutory

Time Limits..........................................................................................................................10

3 Understanding the VAT Penalties and making Adjustments for Previous Errors......................12

3.1 Implications and Penalties for Organisations which Fails to Follow VAT Regulations12

3.2 Making and Adjusting Previously Identified VAT Errors.............................................12

Communicating VAT Information................................................................................................13

4.1 Informing Managers about the Impact of VAT Payment on Cash Flows and Financial

Forecasts of Business...........................................................................................................13

4.2 Advising Relevant People of Changes in VAT Legislation's Effects on Organisations

Recording System.................................................................................................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

Books and Journals...............................................................................................................15

INTRODUCTION

Indirect Taxes are those taxes which are applied by the State or Central Government on

the Goods and Services and not on the income or property of an individual. These taxes are

added to the price of some goods or services. The example can be custom duty charges, VAT,

CST, imports, excise duty charges, etc. The assignment will focus on VAT, a type of Indirect

Tax. VAT stands for Value Added Tax. As from its name it is clear that this type of tax is

imposed on the price of a good over its “price value”. In other words, it can be said that the

amount added over the price of a certain good is called VAT. Further this assignment will

provide understanding of different VAT Regulations, and filing the VAT in timely manner, and

the legal actions taken when an organisation fails to follow these regulations.

MAIN BODY

1 Understand VAT Regulations

1.1 Sources of Information on VAT

As for collecting the information or any query related to VAT Charges can be known

from the official website of UK Government. The HMRC (HM Revenue and Customs) Pages of

the website provides all the information regarding all the taxes, and their relevant charges. The

taxpayers whether people or the organisations can find answers to their questions regarding VAT

charges (Avi-Yonah and Clausing, 2017).

A web chat facility is also provided in order to solve the unanswered questions.

Taxpayers can also use online enquiry form or place their questions by writing to HMRC for

guidance or advice on their doubts. The Government is also launching new publications to the

related change if any occur in the tax rates of any good can be easily known by accessing the

official page of HMRC.

Usually the queries of the taxpayers are solved on the website as they put their questions

on the website and also get their answers too there. It also helps in clearing the same queries

which others do have. Moreover, there is also a telephone line where the queries are solved by

contacting via phone and get the answers.

For different types of goods, the amount of VAT charged is different. The tax rates are

classified in three different rates (Bucheli and et. al., 2013). These are the standard rates, reduced

Indirect Taxes are those taxes which are applied by the State or Central Government on

the Goods and Services and not on the income or property of an individual. These taxes are

added to the price of some goods or services. The example can be custom duty charges, VAT,

CST, imports, excise duty charges, etc. The assignment will focus on VAT, a type of Indirect

Tax. VAT stands for Value Added Tax. As from its name it is clear that this type of tax is

imposed on the price of a good over its “price value”. In other words, it can be said that the

amount added over the price of a certain good is called VAT. Further this assignment will

provide understanding of different VAT Regulations, and filing the VAT in timely manner, and

the legal actions taken when an organisation fails to follow these regulations.

MAIN BODY

1 Understand VAT Regulations

1.1 Sources of Information on VAT

As for collecting the information or any query related to VAT Charges can be known

from the official website of UK Government. The HMRC (HM Revenue and Customs) Pages of

the website provides all the information regarding all the taxes, and their relevant charges. The

taxpayers whether people or the organisations can find answers to their questions regarding VAT

charges (Avi-Yonah and Clausing, 2017).

A web chat facility is also provided in order to solve the unanswered questions.

Taxpayers can also use online enquiry form or place their questions by writing to HMRC for

guidance or advice on their doubts. The Government is also launching new publications to the

related change if any occur in the tax rates of any good can be easily known by accessing the

official page of HMRC.

Usually the queries of the taxpayers are solved on the website as they put their questions

on the website and also get their answers too there. It also helps in clearing the same queries

which others do have. Moreover, there is also a telephone line where the queries are solved by

contacting via phone and get the answers.

For different types of goods, the amount of VAT charged is different. The tax rates are

classified in three different rates (Bucheli and et. al., 2013). These are the standard rates, reduced

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

rates and the zero rates. All these details regarding these charges on certain goods are mentioned

over the website.

Another source of information for the companies in UK is publications provided by

IDBE (Inter-Departmental Business Register). Companies can also take information related to

VAT from the publications provided by IDBR(Cornelsen and et. al., 2014).

1.2 Interaction of Organisation with Relevant Government Agency

The organisations can make the payment of their VAT or Sales Tax to this Department.

Companies have to file their taxes to this Department. The companies can also appoint an agent

to deal with HMRC on their behalf such as a professional tax accountant or tax advisor, or

someone from voluntary organisation. For checking the compliance related to tax payments, the

organisations can directly contact to this department. The companies may also put their tax

related disputes and can get satisfactory resolution for them. In addition to this, the Department

is also providing a letter on tax payment by which the companies can appeal against the tax

charged.

Organisations have to file their return to this department and the payment of their bills are

also done here with this Department (Figari and Paulus, 2012). It does not depend whether the

organisation is a joint venture, or partnership or sole trader, all the queries and payments related

to tax are completed here.

1.3 VAT Registration Requirements

There are different requirements for businesses in order to get registered for VAT. Most

of the businesses are registered online such as the partnerships, sole traders, self-employed,

limited companies, trusts, local authorities and a group of companies can also register under a

single VAT Number.

For getting registered for VAT, the first initial requirement is a legal identification such

as I.D. Card or Passport of the applicant in case the company is Limited Liability Partnership

(Higgins and et. al., 2016). The second requirement is the copy of the Memorandum of

Association of the company which it has to submit to the HMRC Department. In addition to this,

some questions will also be asked from the applicant such as the brief of the business going to

start and the activities which will be usually undertaken, the starting date of business or when

will the business start, and any idea of turnover that the business will have. In the documents list,

the National Insurance Number will also be required, Tax Identifier i.e., Unique Taxpayer's

over the website.

Another source of information for the companies in UK is publications provided by

IDBE (Inter-Departmental Business Register). Companies can also take information related to

VAT from the publications provided by IDBR(Cornelsen and et. al., 2014).

1.2 Interaction of Organisation with Relevant Government Agency

The organisations can make the payment of their VAT or Sales Tax to this Department.

Companies have to file their taxes to this Department. The companies can also appoint an agent

to deal with HMRC on their behalf such as a professional tax accountant or tax advisor, or

someone from voluntary organisation. For checking the compliance related to tax payments, the

organisations can directly contact to this department. The companies may also put their tax

related disputes and can get satisfactory resolution for them. In addition to this, the Department

is also providing a letter on tax payment by which the companies can appeal against the tax

charged.

Organisations have to file their return to this department and the payment of their bills are

also done here with this Department (Figari and Paulus, 2012). It does not depend whether the

organisation is a joint venture, or partnership or sole trader, all the queries and payments related

to tax are completed here.

1.3 VAT Registration Requirements

There are different requirements for businesses in order to get registered for VAT. Most

of the businesses are registered online such as the partnerships, sole traders, self-employed,

limited companies, trusts, local authorities and a group of companies can also register under a

single VAT Number.

For getting registered for VAT, the first initial requirement is a legal identification such

as I.D. Card or Passport of the applicant in case the company is Limited Liability Partnership

(Higgins and et. al., 2016). The second requirement is the copy of the Memorandum of

Association of the company which it has to submit to the HMRC Department. In addition to this,

some questions will also be asked from the applicant such as the brief of the business going to

start and the activities which will be usually undertaken, the starting date of business or when

will the business start, and any idea of turnover that the business will have. In the documents list,

the National Insurance Number will also be required, Tax Identifier i.e., Unique Taxpayer's

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Reference Number (UTR), Certificate of Incorporation, Business Bank Account Details all these

are required and must be provided in front of the Department in order to get registered. Further,

in case the business is already established, the applicant must provide all the information of the

business for the past two years. A business must be registered having a turnover to be more than

of £85,000 within a period of next 30 days. There are also some exemptions where there is no

need to register for VAT so it is necessary to register VAT only in case the business is to sell

goods and services (Jaramillo Baanante, 2013).

1.4 Information Included on Business Documentation of VAT Registered Businesses

The information which are included on the Business Documentation of a business are as

follow as:

Date of Commencement: The Date when the business was started or will start is to be

provided to the Department.

Expected Turnover; The applicant must tell the current turnover or the expected turnover

of the business in case the business is newly established.

Address of Business: The complete address where the business will be situated or is

situated is to be provided to HRMC.

Contact Details: The mobile number, email address and the website of the business

should be provided for getting registered.

Full Shareholder Listing and Holding: The name and number of shareholders of the

company should also be stated during the registration(Kaplanoglou, 2015).

Full Names of Director/Secretary: If the company is a Limited Company than it is a must

to provide the full name of the secretary and director of the company.

Description of the Business; In order to get registered, the information about the business

activity that it is going to carry on should be mentioned.

1.5 Requirements and the Frequency of Reporting for VAT Schemes

Annual Accounting Scheme; Generally, the businesses registered under VAT fill their

returns and payments 4 times during a year to HMRC. The Annual Accounting Scheme

provides businesses to pay their annual bills in quarterly or on monthly basis, but they

have to submit only one VAT Return per year. In accordance to this scheme, a VAT

Registered business must submit a VAT Return four times per year(VAT Annual

Accounting Scheme, 2018). For making these advance payments of VAT Bill, the

are required and must be provided in front of the Department in order to get registered. Further,

in case the business is already established, the applicant must provide all the information of the

business for the past two years. A business must be registered having a turnover to be more than

of £85,000 within a period of next 30 days. There are also some exemptions where there is no

need to register for VAT so it is necessary to register VAT only in case the business is to sell

goods and services (Jaramillo Baanante, 2013).

1.4 Information Included on Business Documentation of VAT Registered Businesses

The information which are included on the Business Documentation of a business are as

follow as:

Date of Commencement: The Date when the business was started or will start is to be

provided to the Department.

Expected Turnover; The applicant must tell the current turnover or the expected turnover

of the business in case the business is newly established.

Address of Business: The complete address where the business will be situated or is

situated is to be provided to HRMC.

Contact Details: The mobile number, email address and the website of the business

should be provided for getting registered.

Full Shareholder Listing and Holding: The name and number of shareholders of the

company should also be stated during the registration(Kaplanoglou, 2015).

Full Names of Director/Secretary: If the company is a Limited Company than it is a must

to provide the full name of the secretary and director of the company.

Description of the Business; In order to get registered, the information about the business

activity that it is going to carry on should be mentioned.

1.5 Requirements and the Frequency of Reporting for VAT Schemes

Annual Accounting Scheme; Generally, the businesses registered under VAT fill their

returns and payments 4 times during a year to HMRC. The Annual Accounting Scheme

provides businesses to pay their annual bills in quarterly or on monthly basis, but they

have to submit only one VAT Return per year. In accordance to this scheme, a VAT

Registered business must submit a VAT Return four times per year(VAT Annual

Accounting Scheme, 2018). For making these advance payments of VAT Bill, the

estimation is made through the payment of last bill and the amount is settled at the end of

year whether the difference is paid by the business or it can apply for Refund in case

more amount is paid.

Cash Accounting Scheme: The Cash Accounting VAT Scheme is a method in which the

VAT is recorded on the basis of payment made and received. For getting registered under

this VAT Scheme, the business must have a turnover of equals to or less than £1.35

Million. The frequency of submitting VAT in this method is four times a year.

Flat Rate Accounting Scheme: The Scheme is also known as VAT FRS. Under this

scheme, VAT is paid by the business as a fixed percentage of its annual turnover and the

amount is paid quarterly to HMRC. The scheme was mainly introduced for the small

businesses to reduce the burden imposed while operating through VAT. The requirement

is to be registered under VAT and must have a turnover of under £ 150,000.

Standard Accounting Scheme: Under this method of reporting VAT, a business records

and pays VAT when it issues invoices whether for purchase or sale. The companies

registered under this scheme submit their VAT Return four times a year. Both the

outstanding and refunds of the companies will be settled on quarterly basis (Lustig and

Higgins, 2013). The requirement to register under this scheme is that the turnover of the

company must be above £1,350,000.

1.6 Maintenance of Knowledge of Changes to Codes of Practise, Regulation or Legislation

Every business wants to avoid the government intervention in its business operations. In

this case of VAT submission, a business must be aware and up-to-date about the changes made

by HMRC in filing the VAT Return and any alteration or addition in the existing laws by HMRC

should properly taken into consideration by the business. It will help in smooth running of their

business and will help in avoiding unwanted fines or penalties. The business should maintain

proper business records and files of return so that the business working can be accomplished

without any problem (Lustig and et. al., 2012). Proper knowledge of Codes of Practise will make

business to run according to the changes made by the Department. It will also enhance the

relationship between the stakeholders and the company. The stakeholders of company will be

satisfied as the image of company is clear in the market. It will also enhance the Brand Image of

the company as there will no difference in the records and the actual working of the company.

The company's accounts are reflecting the same as they are saying. These changes in the

year whether the difference is paid by the business or it can apply for Refund in case

more amount is paid.

Cash Accounting Scheme: The Cash Accounting VAT Scheme is a method in which the

VAT is recorded on the basis of payment made and received. For getting registered under

this VAT Scheme, the business must have a turnover of equals to or less than £1.35

Million. The frequency of submitting VAT in this method is four times a year.

Flat Rate Accounting Scheme: The Scheme is also known as VAT FRS. Under this

scheme, VAT is paid by the business as a fixed percentage of its annual turnover and the

amount is paid quarterly to HMRC. The scheme was mainly introduced for the small

businesses to reduce the burden imposed while operating through VAT. The requirement

is to be registered under VAT and must have a turnover of under £ 150,000.

Standard Accounting Scheme: Under this method of reporting VAT, a business records

and pays VAT when it issues invoices whether for purchase or sale. The companies

registered under this scheme submit their VAT Return four times a year. Both the

outstanding and refunds of the companies will be settled on quarterly basis (Lustig and

Higgins, 2013). The requirement to register under this scheme is that the turnover of the

company must be above £1,350,000.

1.6 Maintenance of Knowledge of Changes to Codes of Practise, Regulation or Legislation

Every business wants to avoid the government intervention in its business operations. In

this case of VAT submission, a business must be aware and up-to-date about the changes made

by HMRC in filing the VAT Return and any alteration or addition in the existing laws by HMRC

should properly taken into consideration by the business. It will help in smooth running of their

business and will help in avoiding unwanted fines or penalties. The business should maintain

proper business records and files of return so that the business working can be accomplished

without any problem (Lustig and et. al., 2012). Proper knowledge of Codes of Practise will make

business to run according to the changes made by the Department. It will also enhance the

relationship between the stakeholders and the company. The stakeholders of company will be

satisfied as the image of company is clear in the market. It will also enhance the Brand Image of

the company as there will no difference in the records and the actual working of the company.

The company's accounts are reflecting the same as they are saying. These changes in the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

legislation sometimes come up with some opportunities and risks so the help of tax consultant

can be taken to identify the opportunities and avoiding the risks.

The implementation of changes in the policies related top VAT provides many non

financial benefits to the company. One of the main benefit is the improved liability management.

It also helps in reducing the incidents of civil frauds and in creating a good image of the

companies operating well in paying taxes (Lustig, Pessino and Scott, 2014).

2 Complete VAT Returns Accurately and in a Timely Manner

2.1 Extract Relevant Data for a Specific Period from the Accounting System

Example 1- For VAT payable:

Sales Book £ 268475

Less: Credit Note £ 4608

Total £ 263867

Cash Book £ 8952

EU Acquisitions £ 19542

Correction of error £ 1869

Grand Total £ 294230

For Input VAT:

Purchase Book £186920

Less: Credit Notes £ 1920

Total £ 185000

Cash Book £ 8450

Petty Cash Book £140

EU Acquisitions £ 21450

Bad Debt Relief £ 7050

Grand Total £ 222090

2.2 Calculation of relevant inputs and outputs

VAT payable:

Sales Sales Value (£) VAT Payable (£)

Standard Supplies 192600 21950.5

can be taken to identify the opportunities and avoiding the risks.

The implementation of changes in the policies related top VAT provides many non

financial benefits to the company. One of the main benefit is the improved liability management.

It also helps in reducing the incidents of civil frauds and in creating a good image of the

companies operating well in paying taxes (Lustig, Pessino and Scott, 2014).

2 Complete VAT Returns Accurately and in a Timely Manner

2.1 Extract Relevant Data for a Specific Period from the Accounting System

Example 1- For VAT payable:

Sales Book £ 268475

Less: Credit Note £ 4608

Total £ 263867

Cash Book £ 8952

EU Acquisitions £ 19542

Correction of error £ 1869

Grand Total £ 294230

For Input VAT:

Purchase Book £186920

Less: Credit Notes £ 1920

Total £ 185000

Cash Book £ 8450

Petty Cash Book £140

EU Acquisitions £ 21450

Bad Debt Relief £ 7050

Grand Total £ 222090

2.2 Calculation of relevant inputs and outputs

VAT payable:

Sales Sales Value (£) VAT Payable (£)

Standard Supplies 192600 21950.5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Exempt Supplies 22917 -

Zero Rated Supplies 29850 -

Exports 18500 -

Sales Book £ 22850.50

Less: Credit Note £ 900.00

Total £ 21950.50

Cash Book £ 1085

EU Acquisitions £ 2250.00

Correction of error £ 190.85

Grand Total £ 25476.35

Input VAT:

Purchase Purchase Value (£) VAT Input (£)

Standard Supplies 156240 11260

Exempt Supplies 14130 -

Zero Rated Supplies 13560 -

Exports 1070 -

Purchase Book £11510

Less: Credit Notes £ 250.00

Total £ 11260.00

Cash Book £ 820

Petty Cash Book £28.70

EU Acquisitions £ 2460.00

Bad Debt Relief £ 705.00

Grand Total £ 15273.70

Input Tax:

Zero Rated Supplies 29850 -

Exports 18500 -

Sales Book £ 22850.50

Less: Credit Note £ 900.00

Total £ 21950.50

Cash Book £ 1085

EU Acquisitions £ 2250.00

Correction of error £ 190.85

Grand Total £ 25476.35

Input VAT:

Purchase Purchase Value (£) VAT Input (£)

Standard Supplies 156240 11260

Exempt Supplies 14130 -

Zero Rated Supplies 13560 -

Exports 1070 -

Purchase Book £11510

Less: Credit Notes £ 250.00

Total £ 11260.00

Cash Book £ 820

Petty Cash Book £28.70

EU Acquisitions £ 2460.00

Bad Debt Relief £ 705.00

Grand Total £ 15273.70

Input Tax:

Purchase Day Book contain £11510 of total input and the figure of £250 is the input VAT

total of purchase return day book out of which £11260 whole is standard supply input.

Cash Book contain £ 820 and Petty Cash Book contain £ 28.70 are taken from the total of

the VAT analysis column of the cash book.

EU Acquisition are the purchases made from another EU state.

Bad debt relief is a amount owing which a supplier writes off in the books because the

bad is unlikely even to be paid off- the buyer may have 'gone bust' for example.

Output Tax:

Sales Day Book contain £ 22850.50 of total output and the figure of £ 900 is the output

VAT total of sales return day book out of which £ 21950.50 whole is standard supply

output (Raj, 2017).

Cash Book contain £ 1085 which are taken from the total of the VAT analysis column of

the cash book.

Correction of error is the case in which business owes a net £ 190.85 which could be

caused due to amount of input VAT included has been too high or amount of output VAT

included has been too low (Kumar, 2014).

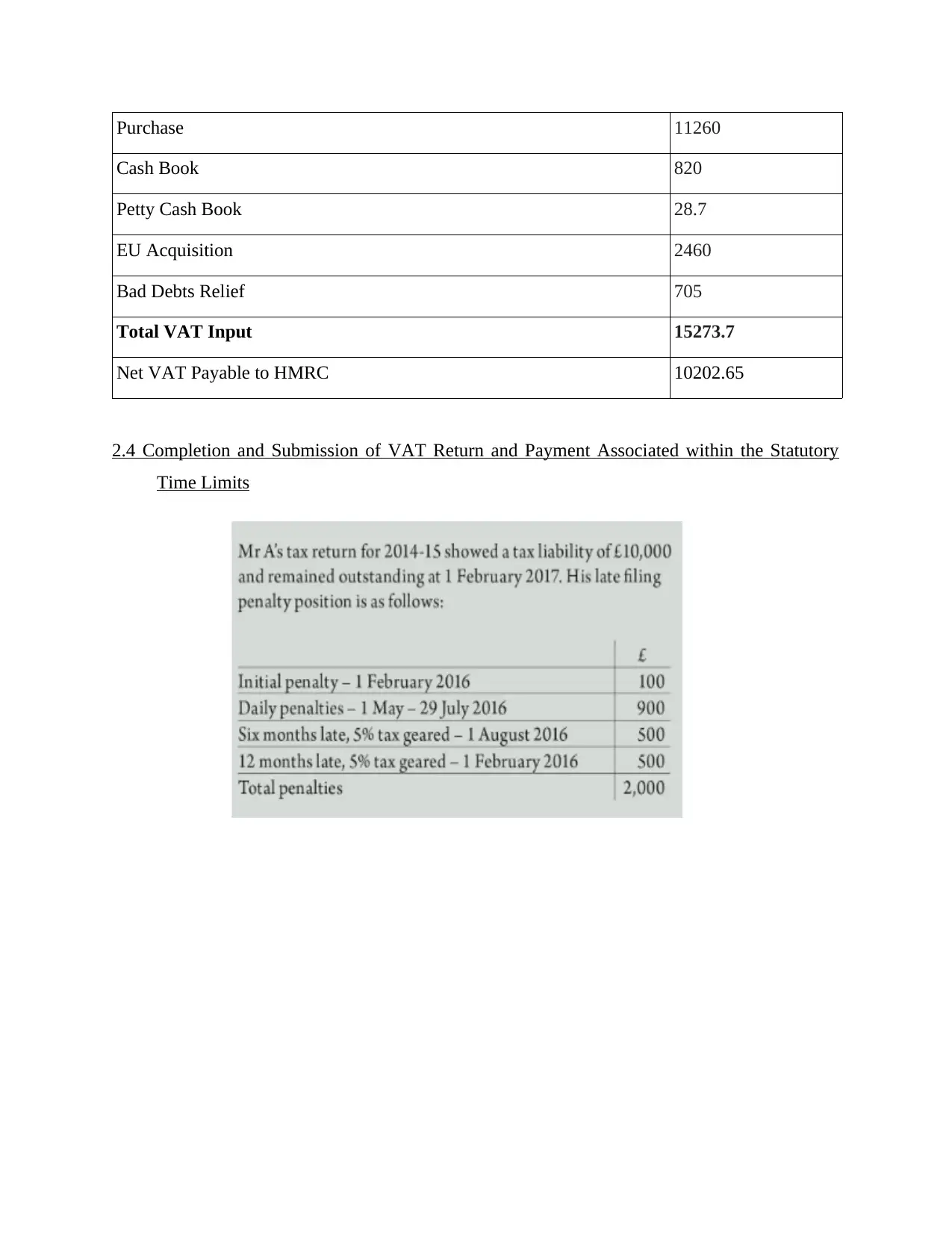

2.3 Calculation of the VAT due to or from the relevant tax authority820

The authority for VAT and custom in UK is HM Revenue and Custom. The VAT due to

or from is analysed by HMRC only. The calculations of VAT due to or from HMRC in the given

case are as follows:

Particulars Amount (£)

VAT output:

Sales 21950.5

Cash Book 1085

EU Acquisitions 2250

Correction of error 190.85

Total VAT output 25476.35

VAT Input:

total of purchase return day book out of which £11260 whole is standard supply input.

Cash Book contain £ 820 and Petty Cash Book contain £ 28.70 are taken from the total of

the VAT analysis column of the cash book.

EU Acquisition are the purchases made from another EU state.

Bad debt relief is a amount owing which a supplier writes off in the books because the

bad is unlikely even to be paid off- the buyer may have 'gone bust' for example.

Output Tax:

Sales Day Book contain £ 22850.50 of total output and the figure of £ 900 is the output

VAT total of sales return day book out of which £ 21950.50 whole is standard supply

output (Raj, 2017).

Cash Book contain £ 1085 which are taken from the total of the VAT analysis column of

the cash book.

Correction of error is the case in which business owes a net £ 190.85 which could be

caused due to amount of input VAT included has been too high or amount of output VAT

included has been too low (Kumar, 2014).

2.3 Calculation of the VAT due to or from the relevant tax authority820

The authority for VAT and custom in UK is HM Revenue and Custom. The VAT due to

or from is analysed by HMRC only. The calculations of VAT due to or from HMRC in the given

case are as follows:

Particulars Amount (£)

VAT output:

Sales 21950.5

Cash Book 1085

EU Acquisitions 2250

Correction of error 190.85

Total VAT output 25476.35

VAT Input:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Purchase 11260

Cash Book 820

Petty Cash Book 28.7

EU Acquisition 2460

Bad Debts Relief 705

Total VAT Input 15273.7

Net VAT Payable to HMRC 10202.65

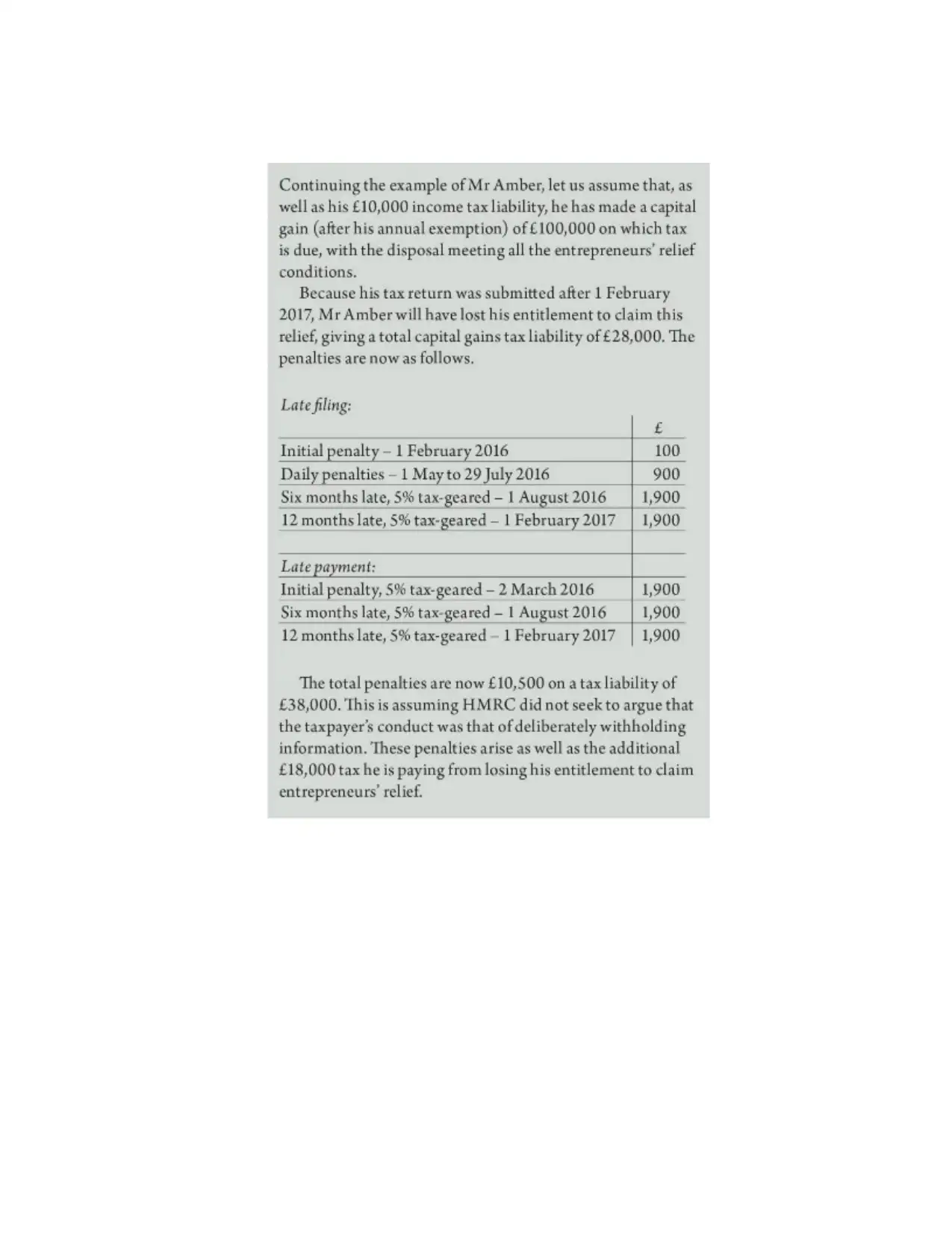

2.4 Completion and Submission of VAT Return and Payment Associated within the Statutory

Time Limits

Cash Book 820

Petty Cash Book 28.7

EU Acquisition 2460

Bad Debts Relief 705

Total VAT Input 15273.7

Net VAT Payable to HMRC 10202.65

2.4 Completion and Submission of VAT Return and Payment Associated within the Statutory

Time Limits

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3 Understanding the VAT Penalties and making Adjustments for Previous

Errors

3.1 Implications and Penalties for Organisations which Fails to Follow VAT Regulations

The HMRC Department charges different penalties for different types of failures by the

organisations. It penalises the company in case it is unauthorised to issue invoices or is not

registered for VAT and the amount depends upon the disclosure or non disclosure of the fact

about the wrongdoing. The tax rates will increase if the company is not filing their return on

time. Additional Costs will be incurred by the company in case of breach of the legislations

(Mason and Stephenson Jr, 2017). The businesses registered under VAT may face harsh

penalties if any incorrect import data is recorded in the books and the penalty charged can be £

500 for each such misrepresentation of records. It will be charged even if the company is not

involved in any kind of fraudulent activity ever before.

In case when business is going on without approval from HMRC, it will be liable for

criminal conviction and penalty which can be of £ 10,000. Every business can apply before 30th

June of every year in case if the business is of fulfilment business which is started before 1st

April of the same year. The Department can charge a penalty of £ 500 if the business is not

applying for registration before the due date provided by them.

After registering business for VAT, it is the duty of business to make ensure that it is

following the rules and guidelines of VAT in a timely and correct manner. For not following

rules and laws of VAT, the business will be liable to pay surcharge of 2% of the outstanding tax

of the previous year, in case the annual turnover of the company is equal to or less than £

150.000(VAT Returns, 2018).

3.2 Making and Adjusting Previously Identified VAT Errors

Under Section 4, VAT Errors which are made deliberately and carelessly will be liable to

pat the penalty. However, HMRC is also providing grounds to companies for covering their

errors(Correcting VAT errors on a return already submitted, 2018).

In case business find out errors in their VAT records, then they have to inform HMRC

and follow the guidelines mentioned in Section 4 so that corrections can be made (Mills and et.

al., 2012). The help of tax advisor can be taken in order to remove the errors in VAT records.

Errors

3.1 Implications and Penalties for Organisations which Fails to Follow VAT Regulations

The HMRC Department charges different penalties for different types of failures by the

organisations. It penalises the company in case it is unauthorised to issue invoices or is not

registered for VAT and the amount depends upon the disclosure or non disclosure of the fact

about the wrongdoing. The tax rates will increase if the company is not filing their return on

time. Additional Costs will be incurred by the company in case of breach of the legislations

(Mason and Stephenson Jr, 2017). The businesses registered under VAT may face harsh

penalties if any incorrect import data is recorded in the books and the penalty charged can be £

500 for each such misrepresentation of records. It will be charged even if the company is not

involved in any kind of fraudulent activity ever before.

In case when business is going on without approval from HMRC, it will be liable for

criminal conviction and penalty which can be of £ 10,000. Every business can apply before 30th

June of every year in case if the business is of fulfilment business which is started before 1st

April of the same year. The Department can charge a penalty of £ 500 if the business is not

applying for registration before the due date provided by them.

After registering business for VAT, it is the duty of business to make ensure that it is

following the rules and guidelines of VAT in a timely and correct manner. For not following

rules and laws of VAT, the business will be liable to pay surcharge of 2% of the outstanding tax

of the previous year, in case the annual turnover of the company is equal to or less than £

150.000(VAT Returns, 2018).

3.2 Making and Adjusting Previously Identified VAT Errors

Under Section 4, VAT Errors which are made deliberately and carelessly will be liable to

pat the penalty. However, HMRC is also providing grounds to companies for covering their

errors(Correcting VAT errors on a return already submitted, 2018).

In case business find out errors in their VAT records, then they have to inform HMRC

and follow the guidelines mentioned in Section 4 so that corrections can be made (Mills and et.

al., 2012). The help of tax advisor can be taken in order to remove the errors in VAT records.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.