Individual Income Tax Assessment and Taxation Report - ACC00132

VerifiedAdded on 2023/06/07

|9

|1206

|304

Report

AI Summary

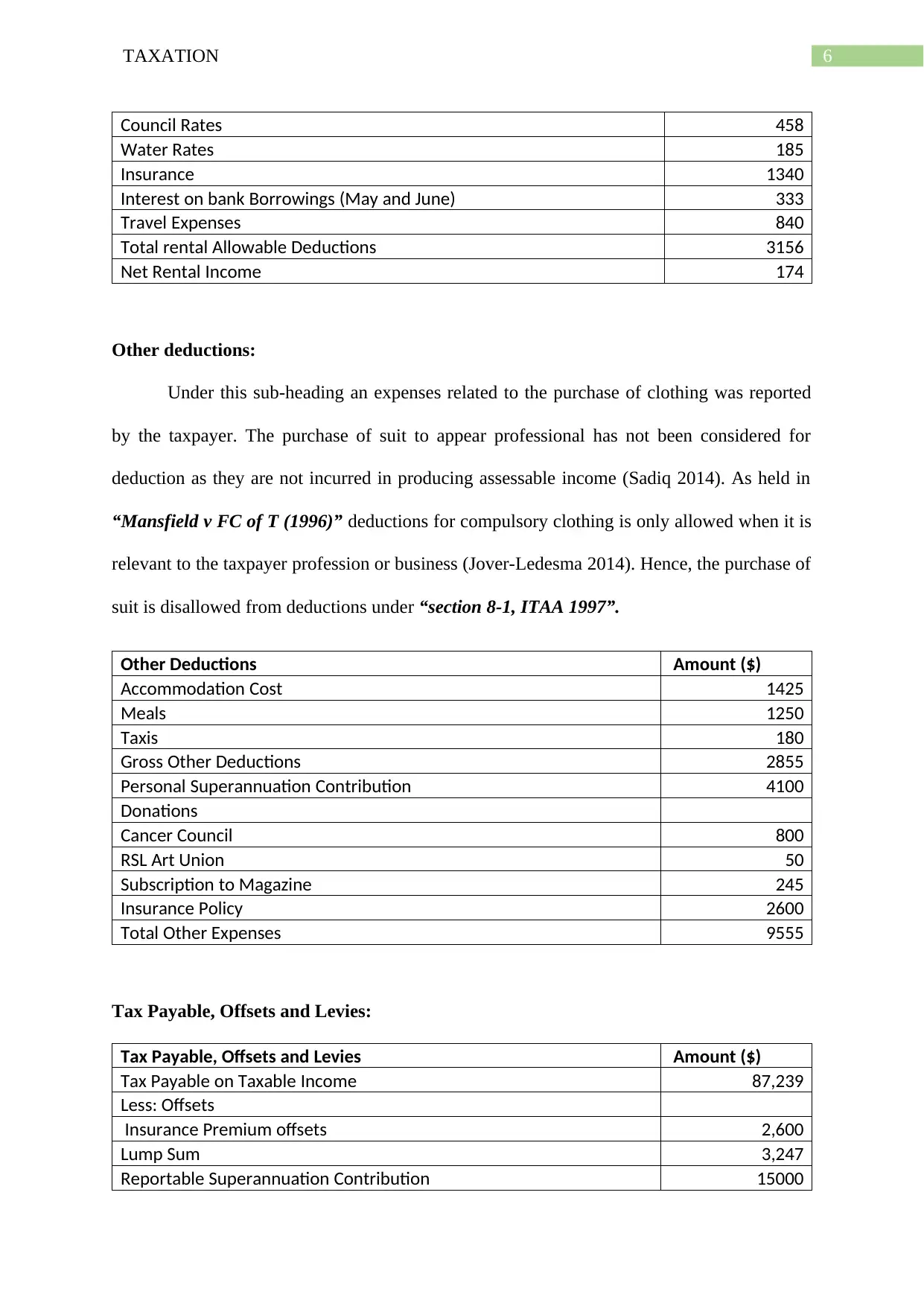

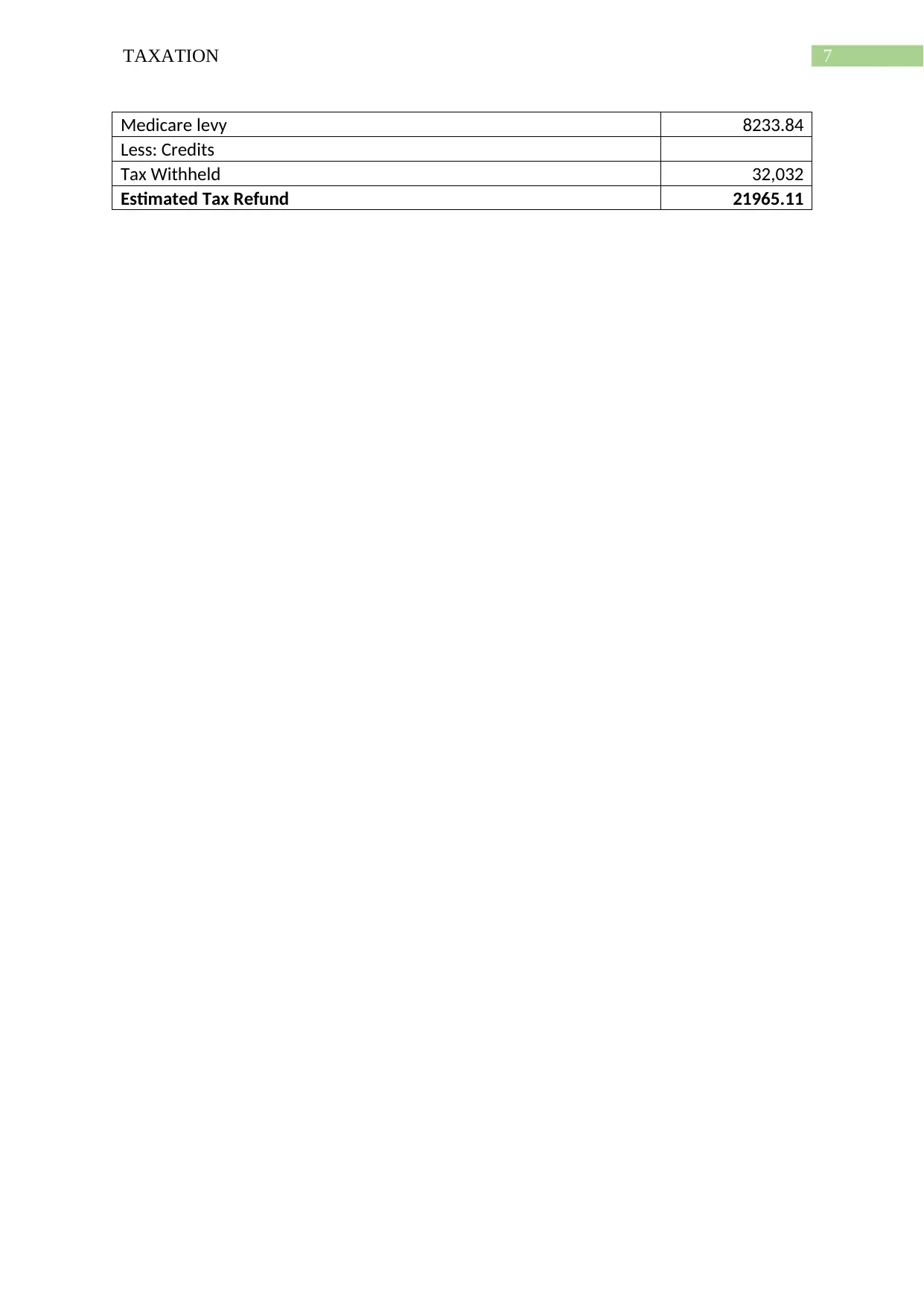

This report provides a comprehensive analysis of an individual's income tax return, addressing various aspects of taxation. It begins with a letter of advice to the client, offering guidance on their tax affairs. The report includes detailed work papers outlining employment income, work-related deductions, capital gains from investments (including shares inherited from a grandmother), and income from a rental property. It also examines other deductions, such as personal superannuation contributions and donations. The report calculates the tax payable, incorporating offsets like insurance premium offsets and credits for tax withheld. Furthermore, it includes references to relevant sections of the Income Tax Assessment Act 1997 (ITAA 1997) and other sources to support its findings. The report demonstrates the application of taxation principles to real-world financial scenarios, offering a practical understanding of income tax calculations and compliance.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.