Individual Taxation Law Project: Income Tax Assessment Act 1997

VerifiedAdded on 2020/10/23

|12

|3619

|164

Project

AI Summary

This project delves into the intricacies of individual taxation law within the Australian context. It commences with an overview of key topics addressed by Taxation Ruling 2018/4 and the divisions within the Income Tax Assessment Act 1997 that pertain to tax offsets. The project then examines the top tax rate applicable to Australian residents in the 2018/19 tax year, along with an example of a capital gains tax-exempt asset, and explores the CGT event B1 and the formula in s4-10(3) ITAA 1997. Furthermore, it analyzes the significance of the High Court case FC of T v Day 2008 ATC 20-064 in relation to deductions, clarifies the difference between marginal and average tax rates, and touches upon consumption tax. The project subsequently addresses specific tax deductions available to Australian resident taxpayers, including business expenses, phone and internet usage, childcare costs, losses due to theft, and election expenses. It then proceeds to a case study involving capital gains tax, detailing the calculation methods and implications. The project concludes by summarizing the key findings and providing relevant references.

Individual Taxation Law project

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION ...............................................................................................................................3

QUESTION 1.......................................................................................................................................3

Topic cover by Taxation ruling 2018/4.............................................................................................3

Division of the Income Tax Assessment Act 1997 details available tax offsets...............................3

Top tax rate applicable to a resident taxpayer in the 2018/19 tax year............................................3

One example of an asset that is exempt from capital gains tax........................................................4

CGT event B1 s104-15 tax...............................................................................................................4

Formula contained in s4-10(3) ITAA 1997......................................................................................4

Significance of the High Court case, FC of T v Day 2008 ATC 20-064 in the topic of deductions 4

Difference between marginal rate of tax and average rate of tax.....................................................4

Consumption tax...............................................................................................................................5

QUESTION 2.......................................................................................................................................5

Tax deduction available to an Australian resident taxpayer are as follows:.....................................5

a........................................................................................................................................................5

b. ......................................................................................................................................................5

c. ......................................................................................................................................................6

d. ......................................................................................................................................................6

e. ......................................................................................................................................................7

QUESTION 3.......................................................................................................................................7

QUESTION 4.......................................................................................................................................8

QUESTION 5.......................................................................................................................................8

CONCLUSION ...................................................................................................................................9

REFERENCES................................................................................................................11

INTRODUCTION ...............................................................................................................................3

QUESTION 1.......................................................................................................................................3

Topic cover by Taxation ruling 2018/4.............................................................................................3

Division of the Income Tax Assessment Act 1997 details available tax offsets...............................3

Top tax rate applicable to a resident taxpayer in the 2018/19 tax year............................................3

One example of an asset that is exempt from capital gains tax........................................................4

CGT event B1 s104-15 tax...............................................................................................................4

Formula contained in s4-10(3) ITAA 1997......................................................................................4

Significance of the High Court case, FC of T v Day 2008 ATC 20-064 in the topic of deductions 4

Difference between marginal rate of tax and average rate of tax.....................................................4

Consumption tax...............................................................................................................................5

QUESTION 2.......................................................................................................................................5

Tax deduction available to an Australian resident taxpayer are as follows:.....................................5

a........................................................................................................................................................5

b. ......................................................................................................................................................5

c. ......................................................................................................................................................6

d. ......................................................................................................................................................6

e. ......................................................................................................................................................7

QUESTION 3.......................................................................................................................................7

QUESTION 4.......................................................................................................................................8

QUESTION 5.......................................................................................................................................8

CONCLUSION ...................................................................................................................................9

REFERENCES................................................................................................................11

INTRODUCTION

In UK, taxation aspect involves payment at three levels of government namely local, central

and devolved. Tax authorities do several amendments in rules and regulations with the motive to

ensure smooth functioning of such process. By referring concerned laws business entities and

individuals can determine tax obligations more effectually. The present report is based on different

case situations which in turn provides deeper insight about deductions available with regards to

expenses incurred and income generated. Further, it will also develop understanding about Income

Tax Assessment Act (1997) and associated rulings.

QUESTION 1

Topic cover by Taxation ruling 2018/4

Taxation ruling 2018/4 convers the topic of effective life of assets which gets depreciated

after certain period of time. By this way companies or valuator can determine declining value of

any asset (Woellner and et.al., 2016).

Division of the Income Tax Assessment Act 1997 details available tax offsets

In Division 13 tax offsets details are available. Furthermore, division 61 also applicable to tax

offsets as subdivision 61-A deals with dependant and determine who is applicable to tax offset

and subdivision 61-D describes low or middle income tax offset (Fitzpatrick, 2019).

Top tax rate applicable to a resident taxpayer in the 2018/19 tax year

As per Australian taxation system 2018/19 Australian resident have to pay taxes on their

income according to set tax rate. Top tax rate is illustrated as below:

Income slap Tax Rate Tax payable on income

$0-18200 0% No tax need to be paid by

individual on that income

slap

$18201-37000 19% Above $18200 individual

will have to pay 19c for

every $1

$37001-90000 32.5% Individual will have to pay

32.5%3572plus of amount

more than 37000

In UK, taxation aspect involves payment at three levels of government namely local, central

and devolved. Tax authorities do several amendments in rules and regulations with the motive to

ensure smooth functioning of such process. By referring concerned laws business entities and

individuals can determine tax obligations more effectually. The present report is based on different

case situations which in turn provides deeper insight about deductions available with regards to

expenses incurred and income generated. Further, it will also develop understanding about Income

Tax Assessment Act (1997) and associated rulings.

QUESTION 1

Topic cover by Taxation ruling 2018/4

Taxation ruling 2018/4 convers the topic of effective life of assets which gets depreciated

after certain period of time. By this way companies or valuator can determine declining value of

any asset (Woellner and et.al., 2016).

Division of the Income Tax Assessment Act 1997 details available tax offsets

In Division 13 tax offsets details are available. Furthermore, division 61 also applicable to tax

offsets as subdivision 61-A deals with dependant and determine who is applicable to tax offset

and subdivision 61-D describes low or middle income tax offset (Fitzpatrick, 2019).

Top tax rate applicable to a resident taxpayer in the 2018/19 tax year

As per Australian taxation system 2018/19 Australian resident have to pay taxes on their

income according to set tax rate. Top tax rate is illustrated as below:

Income slap Tax Rate Tax payable on income

$0-18200 0% No tax need to be paid by

individual on that income

slap

$18201-37000 19% Above $18200 individual

will have to pay 19c for

every $1

$37001-90000 32.5% Individual will have to pay

32.5%3572plus of amount

more than 37000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

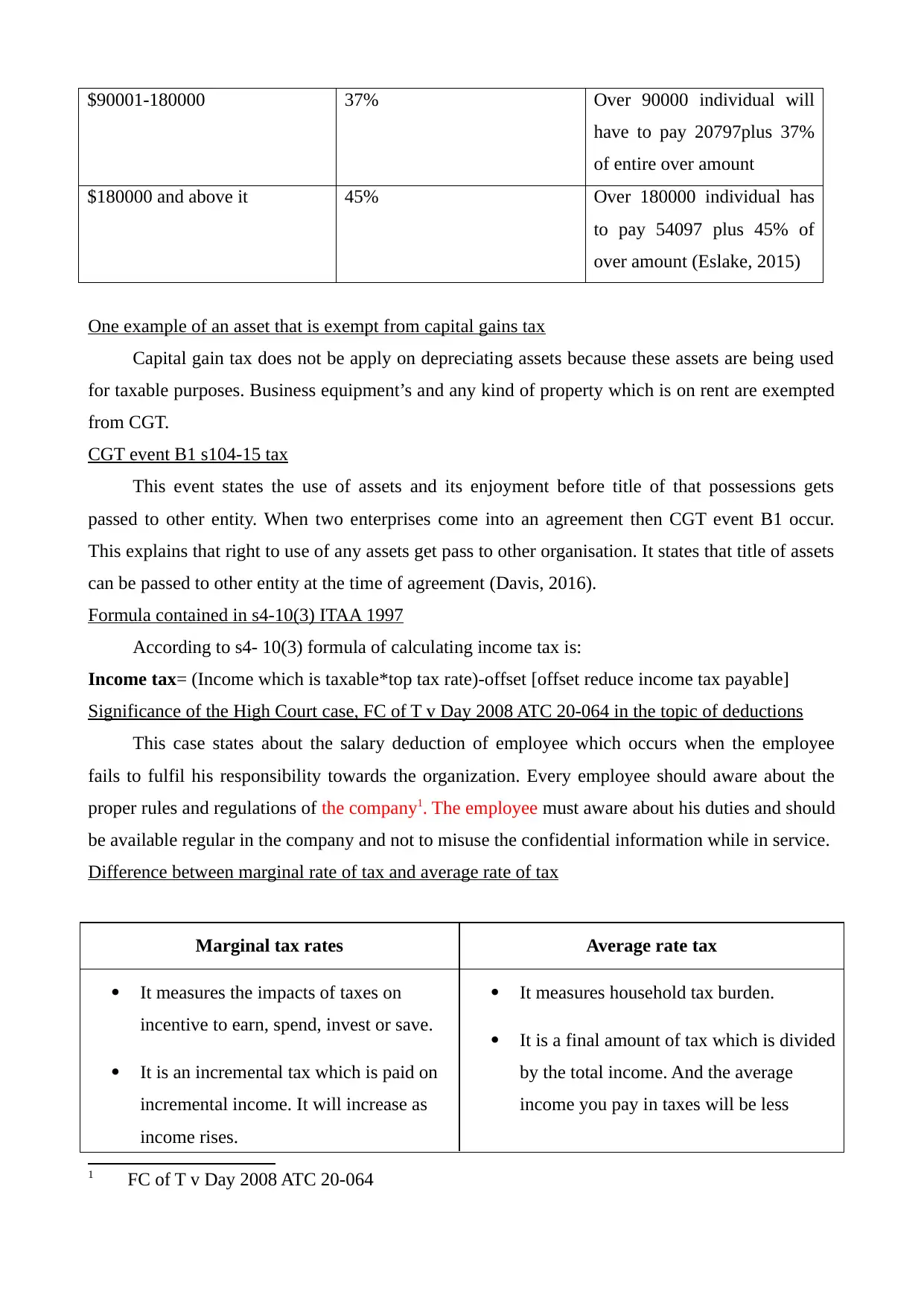

$90001-180000 37% Over 90000 individual will

have to pay 20797plus 37%

of entire over amount

$180000 and above it 45% Over 180000 individual has

to pay 54097 plus 45% of

over amount (Eslake, 2015)

One example of an asset that is exempt from capital gains tax

Capital gain tax does not be apply on depreciating assets because these assets are being used

for taxable purposes. Business equipment’s and any kind of property which is on rent are exempted

from CGT.

CGT event B1 s104-15 tax

This event states the use of assets and its enjoyment before title of that possessions gets

passed to other entity. When two enterprises come into an agreement then CGT event B1 occur.

This explains that right to use of any assets get pass to other organisation. It states that title of assets

can be passed to other entity at the time of agreement (Davis, 2016).

Formula contained in s4-10(3) ITAA 1997

According to s4- 10(3) formula of calculating income tax is:

Income tax= (Income which is taxable*top tax rate)-offset [offset reduce income tax payable]

Significance of the High Court case, FC of T v Day 2008 ATC 20-064 in the topic of deductions

This case states about the salary deduction of employee which occurs when the employee

fails to fulfil his responsibility towards the organization. Every employee should aware about the

proper rules and regulations of the company1. The employee must aware about his duties and should

be available regular in the company and not to misuse the confidential information while in service.

Difference between marginal rate of tax and average rate of tax

Marginal tax rates Average rate tax

It measures the impacts of taxes on

incentive to earn, spend, invest or save.

It is an incremental tax which is paid on

incremental income. It will increase as

income rises.

It measures household tax burden.

It is a final amount of tax which is divided

by the total income. And the average

income you pay in taxes will be less

1 FC of T v Day 2008 ATC 20-064

have to pay 20797plus 37%

of entire over amount

$180000 and above it 45% Over 180000 individual has

to pay 54097 plus 45% of

over amount (Eslake, 2015)

One example of an asset that is exempt from capital gains tax

Capital gain tax does not be apply on depreciating assets because these assets are being used

for taxable purposes. Business equipment’s and any kind of property which is on rent are exempted

from CGT.

CGT event B1 s104-15 tax

This event states the use of assets and its enjoyment before title of that possessions gets

passed to other entity. When two enterprises come into an agreement then CGT event B1 occur.

This explains that right to use of any assets get pass to other organisation. It states that title of assets

can be passed to other entity at the time of agreement (Davis, 2016).

Formula contained in s4-10(3) ITAA 1997

According to s4- 10(3) formula of calculating income tax is:

Income tax= (Income which is taxable*top tax rate)-offset [offset reduce income tax payable]

Significance of the High Court case, FC of T v Day 2008 ATC 20-064 in the topic of deductions

This case states about the salary deduction of employee which occurs when the employee

fails to fulfil his responsibility towards the organization. Every employee should aware about the

proper rules and regulations of the company1. The employee must aware about his duties and should

be available regular in the company and not to misuse the confidential information while in service.

Difference between marginal rate of tax and average rate of tax

Marginal tax rates Average rate tax

It measures the impacts of taxes on

incentive to earn, spend, invest or save.

It is an incremental tax which is paid on

incremental income. It will increase as

income rises.

It measures household tax burden.

It is a final amount of tax which is divided

by the total income. And the average

income you pay in taxes will be less

1 FC of T v Day 2008 ATC 20-064

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

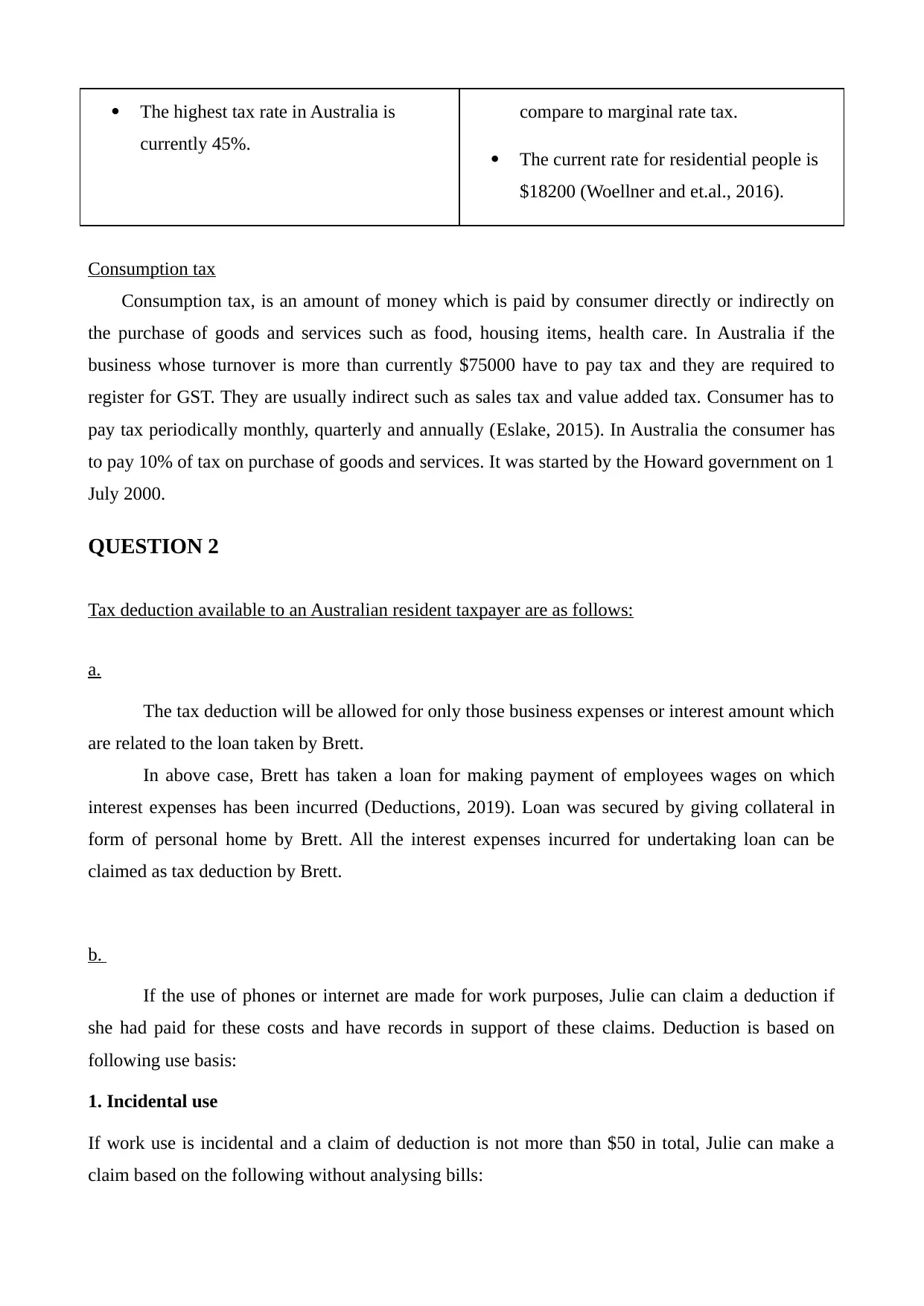

The highest tax rate in Australia is

currently 45%.

compare to marginal rate tax.

The current rate for residential people is

$18200 (Woellner and et.al., 2016).

Consumption tax

Consumption tax, is an amount of money which is paid by consumer directly or indirectly on

the purchase of goods and services such as food, housing items, health care. In Australia if the

business whose turnover is more than currently $75000 have to pay tax and they are required to

register for GST. They are usually indirect such as sales tax and value added tax. Consumer has to

pay tax periodically monthly, quarterly and annually (Eslake, 2015). In Australia the consumer has

to pay 10% of tax on purchase of goods and services. It was started by the Howard government on 1

July 2000.

QUESTION 2

Tax deduction available to an Australian resident taxpayer are as follows:

a.

The tax deduction will be allowed for only those business expenses or interest amount which

are related to the loan taken by Brett.

In above case, Brett has taken a loan for making payment of employees wages on which

interest expenses has been incurred (Deductions, 2019). Loan was secured by giving collateral in

form of personal home by Brett. All the interest expenses incurred for undertaking loan can be

claimed as tax deduction by Brett.

b.

If the use of phones or internet are made for work purposes, Julie can claim a deduction if

she had paid for these costs and have records in support of these claims. Deduction is based on

following use basis:

1. Incidental use

If work use is incidental and a claim of deduction is not more than $50 in total, Julie can make a

claim based on the following without analysing bills:

currently 45%.

compare to marginal rate tax.

The current rate for residential people is

$18200 (Woellner and et.al., 2016).

Consumption tax

Consumption tax, is an amount of money which is paid by consumer directly or indirectly on

the purchase of goods and services such as food, housing items, health care. In Australia if the

business whose turnover is more than currently $75000 have to pay tax and they are required to

register for GST. They are usually indirect such as sales tax and value added tax. Consumer has to

pay tax periodically monthly, quarterly and annually (Eslake, 2015). In Australia the consumer has

to pay 10% of tax on purchase of goods and services. It was started by the Howard government on 1

July 2000.

QUESTION 2

Tax deduction available to an Australian resident taxpayer are as follows:

a.

The tax deduction will be allowed for only those business expenses or interest amount which

are related to the loan taken by Brett.

In above case, Brett has taken a loan for making payment of employees wages on which

interest expenses has been incurred (Deductions, 2019). Loan was secured by giving collateral in

form of personal home by Brett. All the interest expenses incurred for undertaking loan can be

claimed as tax deduction by Brett.

b.

If the use of phones or internet are made for work purposes, Julie can claim a deduction if

she had paid for these costs and have records in support of these claims. Deduction is based on

following use basis:

1. Incidental use

If work use is incidental and a claim of deduction is not more than $50 in total, Julie can make a

claim based on the following without analysing bills:

1. $0.25 for work calls made from land line.

2. $0.75 for work calls made from mobile.

3. $0.10 for text messages sent from mobile.

2. Usage is itemised on bills

On having a phone plan, Julie will receive an itemised bill in which she needs to determine her

percentage of work use over a four-week representative period which can then be applied to the full

year (Claiming mobile phone, internet and home phone expenses, 2019). This could include:

1. the number of work calls made as a percentage of total calls

2. the amount of time spent on work calls as a percentage of your total calls

3. the amount of data downloaded for work purposes as a percentage of total downloads.

Julie has incurred a bill of $500 for mobile phone and determined that 60% of her total calls

was related to work. So, she will be able to claim a deduction of $0.75 for work calls made from

mobile.

c.

As per some tax jurisdictions, only the parent having the lower net income is able to claim

the expenses related to the child care. If the child is under the age of 13 years or is a special child or

disabled dependent, a tax credit of up to 35% of the qualifying expenses can be claimed by the

parent. A qualifying expense is a service which is provided by the care provider like a daycare

center, summer camp, or babysitter etc.

The maximum limit for claim is 35% of expenses up to $3,000 for one child. Or 35% up to

$6,000 if having two or more children or dependants (Can You Write Off Babysitting Expenses?

2019).

In case of Sally, she paid $1,200 to babysitter and thus is liable for claiming the tax

deduction of 35% of expenses incurred on baby care i.e. 35% of $1,200.

d.

As per the INCOME TAX ASSESSMENT ACT 1997 - SECT 25.45, any kind of loss

incurred due to theft etc. can be claim under tax deduction in following manner:

Company can deduct such loss in respect of money as the loss was caused by theft done by

Jerry, one of the long term employees. Jerrry has stolen the goods from the business having worth

of $20,000 during the tax year.

2. $0.75 for work calls made from mobile.

3. $0.10 for text messages sent from mobile.

2. Usage is itemised on bills

On having a phone plan, Julie will receive an itemised bill in which she needs to determine her

percentage of work use over a four-week representative period which can then be applied to the full

year (Claiming mobile phone, internet and home phone expenses, 2019). This could include:

1. the number of work calls made as a percentage of total calls

2. the amount of time spent on work calls as a percentage of your total calls

3. the amount of data downloaded for work purposes as a percentage of total downloads.

Julie has incurred a bill of $500 for mobile phone and determined that 60% of her total calls

was related to work. So, she will be able to claim a deduction of $0.75 for work calls made from

mobile.

c.

As per some tax jurisdictions, only the parent having the lower net income is able to claim

the expenses related to the child care. If the child is under the age of 13 years or is a special child or

disabled dependent, a tax credit of up to 35% of the qualifying expenses can be claimed by the

parent. A qualifying expense is a service which is provided by the care provider like a daycare

center, summer camp, or babysitter etc.

The maximum limit for claim is 35% of expenses up to $3,000 for one child. Or 35% up to

$6,000 if having two or more children or dependants (Can You Write Off Babysitting Expenses?

2019).

In case of Sally, she paid $1,200 to babysitter and thus is liable for claiming the tax

deduction of 35% of expenses incurred on baby care i.e. 35% of $1,200.

d.

As per the INCOME TAX ASSESSMENT ACT 1997 - SECT 25.45, any kind of loss

incurred due to theft etc. can be claim under tax deduction in following manner:

Company can deduct such loss in respect of money as the loss was caused by theft done by

Jerry, one of the long term employees. Jerrry has stolen the goods from the business having worth

of $20,000 during the tax year.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Business has to suffer loss, which was caused by theft and stealing made by Jerry, so this

will be considered as loss in respect of money of $20,000 and will be deducted in for form tax

deduction from the taxable income of business2. Also, loss caused on behalf of embezzlement,

larceny, defalcation or misappropriation by the employee or agent, other than an individual

employed solely for private purposes will be treated as loss in respect of money and claimed as tax

deduction.

e.

A deduction related to the election expenses by including a candidates cost of contesting can

be claimed in following manner:

1. The local government election - expenses incurred for the local government body election

has deduction criteria which cannot exceed $1,000 for each election contested, even if the

expenditure is incurred in more than one year of income.

2. State or territory election.

3. Federal election.

After claiming deduction for any election expense and receiving of reimbursement, the tax

payer has to include such reimbursement amount as income on tax return (Election expenses, 2019).

In above case, expenditure is incurred in contesting a local government election of $5,000

out of which $2,000 spent on a big election party. The deduction claimable is only $1,000 which has

to be included as income on tax return, after receiving reimbursement of $1,000.

Claim related to union election expenses is not provided if there is no continuity of office.

Election or re-election expenses are not incurred in performing union duties and hence not

deductible.

QUESTION 3

A. The liability of capital gain taxes arises when a asset is sold at a profits of loss or a price of

higher or lower then its acquisition cost. For this give scenario Andy owns land and a lease at a

premium/ Both the lease and land are still in possession of Andy there is on lease transaction

regarding any one of them. So on capital gain liability arises in this case.

B. Indexation method:

CPI for the quarter when CGT event happened (march)/ CPI for the quarter when expenditure was

2 INCOME TAX ASSESSMENT ACT 1997 - SECT 25.45.

will be considered as loss in respect of money of $20,000 and will be deducted in for form tax

deduction from the taxable income of business2. Also, loss caused on behalf of embezzlement,

larceny, defalcation or misappropriation by the employee or agent, other than an individual

employed solely for private purposes will be treated as loss in respect of money and claimed as tax

deduction.

e.

A deduction related to the election expenses by including a candidates cost of contesting can

be claimed in following manner:

1. The local government election - expenses incurred for the local government body election

has deduction criteria which cannot exceed $1,000 for each election contested, even if the

expenditure is incurred in more than one year of income.

2. State or territory election.

3. Federal election.

After claiming deduction for any election expense and receiving of reimbursement, the tax

payer has to include such reimbursement amount as income on tax return (Election expenses, 2019).

In above case, expenditure is incurred in contesting a local government election of $5,000

out of which $2,000 spent on a big election party. The deduction claimable is only $1,000 which has

to be included as income on tax return, after receiving reimbursement of $1,000.

Claim related to union election expenses is not provided if there is no continuity of office.

Election or re-election expenses are not incurred in performing union duties and hence not

deductible.

QUESTION 3

A. The liability of capital gain taxes arises when a asset is sold at a profits of loss or a price of

higher or lower then its acquisition cost. For this give scenario Andy owns land and a lease at a

premium/ Both the lease and land are still in possession of Andy there is on lease transaction

regarding any one of them. So on capital gain liability arises in this case.

B. Indexation method:

CPI for the quarter when CGT event happened (march)/ CPI for the quarter when expenditure was

2 INCOME TAX ASSESSMENT ACT 1997 - SECT 25.45.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

incurred

indexation value:

112.6//90.3= 1.25

Current value of land after indexation:

40000* 1.25= 49878.18

Capital gain= 800000- 49878.18

750121.81

As the property is held by the John for more than 1 year he is eligible to get a 50% discount hence

(750121/2) 375060.9 is taxable.

C. the capital gain taxation is applicable of the capital gains by two methods the indexation

method and the discounting method (How to calculate capital gains tax, 2019). Under the

discounting method if the property is held by a Australian resident fro more one year then a 50%

of the discount is granted to them over the total amount of capital gains. The remaining amount is

added in the taxable income of the assess and then the tax is charged on it.

For the given case the capital gain of $30000 is chargeable to capital gain tax. Both Olivia

and Jamie is allows a 50% discount over this gain as they are resident of Australia and owns the

house for more than 1 years. So $150000 is chargeable to the income tax.

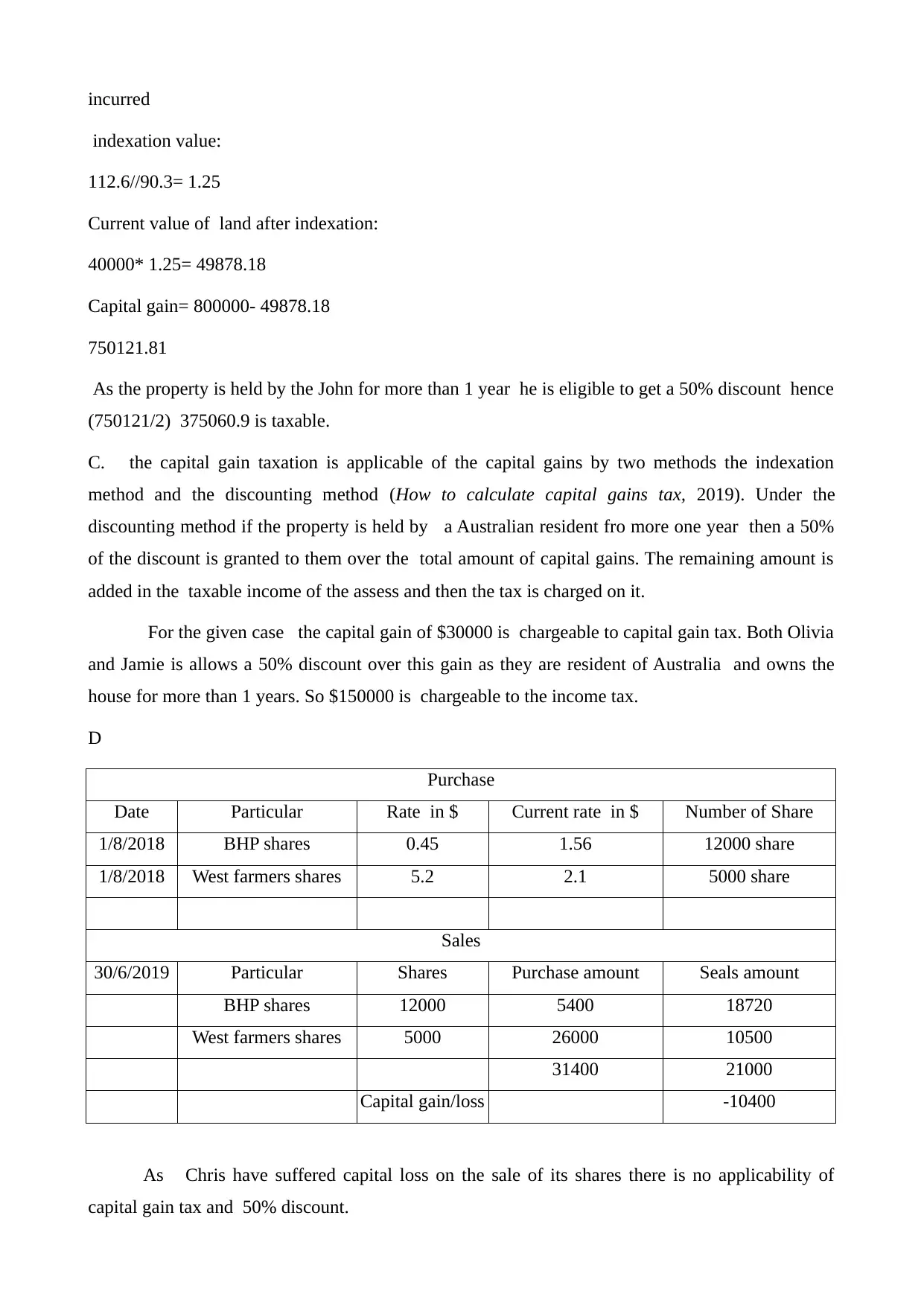

D

Purchase

Date Particular Rate in $ Current rate in $ Number of Share

1/8/2018 BHP shares 0.45 1.56 12000 share

1/8/2018 West farmers shares 5.2 2.1 5000 share

Sales

30/6/2019 Particular Shares Purchase amount Seals amount

BHP shares 12000 5400 18720

West farmers shares 5000 26000 10500

31400 21000

Capital gain/loss -10400

As Chris have suffered capital loss on the sale of its shares there is no applicability of

capital gain tax and 50% discount.

indexation value:

112.6//90.3= 1.25

Current value of land after indexation:

40000* 1.25= 49878.18

Capital gain= 800000- 49878.18

750121.81

As the property is held by the John for more than 1 year he is eligible to get a 50% discount hence

(750121/2) 375060.9 is taxable.

C. the capital gain taxation is applicable of the capital gains by two methods the indexation

method and the discounting method (How to calculate capital gains tax, 2019). Under the

discounting method if the property is held by a Australian resident fro more one year then a 50%

of the discount is granted to them over the total amount of capital gains. The remaining amount is

added in the taxable income of the assess and then the tax is charged on it.

For the given case the capital gain of $30000 is chargeable to capital gain tax. Both Olivia

and Jamie is allows a 50% discount over this gain as they are resident of Australia and owns the

house for more than 1 years. So $150000 is chargeable to the income tax.

D

Purchase

Date Particular Rate in $ Current rate in $ Number of Share

1/8/2018 BHP shares 0.45 1.56 12000 share

1/8/2018 West farmers shares 5.2 2.1 5000 share

Sales

30/6/2019 Particular Shares Purchase amount Seals amount

BHP shares 12000 5400 18720

West farmers shares 5000 26000 10500

31400 21000

Capital gain/loss -10400

As Chris have suffered capital loss on the sale of its shares there is no applicability of

capital gain tax and 50% discount.

QUESTION 4

A. The prises won by a Australian resident in the game shows and other lotteries and the gifts

received in small amounts are not taxable in Australia n taxation provisions. So the price amount of

$2000 received is not taxable for the income year 2018-2019.

B. The amount received from the employer as travel expenses fr the work are not taxable in the

individual taxable income tax. Hence not charged to the tax (Amounts not included as income,

2019). However if the some amount is used for personal purpose it the amount used is chargeable

to income tax. The the amount $120 is not chargeable to tax. $380 will be added in the assessable

income of the employee.

C. The I phone given by client is considers as a gift and since the amount is not to huge i.e. $1000

it will not be added in assessable income.

D. The damage compensation is not a a income which have occurred from any reasonable source

of income. Hence its not a assessable income under the Australian taxation rules.

E. Since the shares are still in the possession of tax payer and there is no transaction of buying and

selling have been does, no incomes have arises. Moreover, the share price do not becomes part of

assessable income.

QUESTION 5

Taxability of any person is highly depended upon their residential status in country. ATO (The

Australian Taxation office) has made several standards related to immigration and border protection

that helps in determining tax liability of resident. As in the case Nisue came from Nepal to

Australia. Various factors are taken into account in order to determine Nisu residential status. These

elements are as below described:

Income

If the person is generating income from Australian resources, then individual is liable to pay

tax to Australian government. For example, income can be generated from employment, rental,

pension, capital gain on assets etc. In the case of Nisu he came here with educational purpose and

started working part time (Fitzpatrick, 2019). But the actual reason of coming to this country was

education hence he cannot be considered as resident of Australia and he is not liable to pay tax.

Superannuation test states that government employees working on public service post overseas are

only considered as Australian resident but Nisu was working a part time employee in bookshop

hence he was not a government workers in Australia hence he is not resident of Australia for tax

purpose.

This is another major factor that need to be considered in order to determine residency tax

A. The prises won by a Australian resident in the game shows and other lotteries and the gifts

received in small amounts are not taxable in Australia n taxation provisions. So the price amount of

$2000 received is not taxable for the income year 2018-2019.

B. The amount received from the employer as travel expenses fr the work are not taxable in the

individual taxable income tax. Hence not charged to the tax (Amounts not included as income,

2019). However if the some amount is used for personal purpose it the amount used is chargeable

to income tax. The the amount $120 is not chargeable to tax. $380 will be added in the assessable

income of the employee.

C. The I phone given by client is considers as a gift and since the amount is not to huge i.e. $1000

it will not be added in assessable income.

D. The damage compensation is not a a income which have occurred from any reasonable source

of income. Hence its not a assessable income under the Australian taxation rules.

E. Since the shares are still in the possession of tax payer and there is no transaction of buying and

selling have been does, no incomes have arises. Moreover, the share price do not becomes part of

assessable income.

QUESTION 5

Taxability of any person is highly depended upon their residential status in country. ATO (The

Australian Taxation office) has made several standards related to immigration and border protection

that helps in determining tax liability of resident. As in the case Nisue came from Nepal to

Australia. Various factors are taken into account in order to determine Nisu residential status. These

elements are as below described:

Income

If the person is generating income from Australian resources, then individual is liable to pay

tax to Australian government. For example, income can be generated from employment, rental,

pension, capital gain on assets etc. In the case of Nisu he came here with educational purpose and

started working part time (Fitzpatrick, 2019). But the actual reason of coming to this country was

education hence he cannot be considered as resident of Australia and he is not liable to pay tax.

Superannuation test states that government employees working on public service post overseas are

only considered as Australian resident but Nisu was working a part time employee in bookshop

hence he was not a government workers in Australia hence he is not resident of Australia for tax

purpose.

This is another major factor that need to be considered in order to determine residency tax

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

purpose of any person. That means that if person has improved their living style and if there is

changes in working arrangement prior coming to Australia then individual will be liable to pay tax

to Australian government. In the case of Nisu, he was living on rent prior and now as well with lots

of friends. There is no changes occurred in his lifestyle and living standards hence he would not be

applicable for tax (Australian resident for tax purposes, explained, 2016). Domicile test shows that

if the person has permanent home in Australia then only will considered as resident of Australia.

But Nisu was living on rent and having no permanent home hence he is not resident of that nation.

Time to stay in country

If an individual stay in Australia for more than 183 days, then person is considered as

resident of country and individual is liable to pay tax to Australian authorities. As in the case of

Nisu, he arrives in Australia on 30th December 2018 from Nepal for educational purpose. Due to

some family concerns he had to leave Australia on 30th June 2019. Total staying period of Nisu in

Australia is 182 days which is less than 183 days. That shows that he is not liable to pay tax to

Australian government (Davis, 2016). By considering these factors Nisu would not be considered

as resident for tax purpose.

CONCLUSION

By summing up this report, it has been concluded that the capital gain tax liability arises when

a asset is sold at the profit or loss as compared to its acquisition cost. The gifts and amount

received from the employers have different tax application as gift under employer till a specific

limit are not taxable. Besides this, it can be inferred that one can reduce tax liability by taking into

account deductions available in relation to wages, interest payment, election expenses etc. It can be

summarized from the evaluation that domicile test provides high level of assistance in determining

whether one is Australian resident for income tax purpose or not.

changes in working arrangement prior coming to Australia then individual will be liable to pay tax

to Australian government. In the case of Nisu, he was living on rent prior and now as well with lots

of friends. There is no changes occurred in his lifestyle and living standards hence he would not be

applicable for tax (Australian resident for tax purposes, explained, 2016). Domicile test shows that

if the person has permanent home in Australia then only will considered as resident of Australia.

But Nisu was living on rent and having no permanent home hence he is not resident of that nation.

Time to stay in country

If an individual stay in Australia for more than 183 days, then person is considered as

resident of country and individual is liable to pay tax to Australian authorities. As in the case of

Nisu, he arrives in Australia on 30th December 2018 from Nepal for educational purpose. Due to

some family concerns he had to leave Australia on 30th June 2019. Total staying period of Nisu in

Australia is 182 days which is less than 183 days. That shows that he is not liable to pay tax to

Australian government (Davis, 2016). By considering these factors Nisu would not be considered

as resident for tax purpose.

CONCLUSION

By summing up this report, it has been concluded that the capital gain tax liability arises when

a asset is sold at the profit or loss as compared to its acquisition cost. The gifts and amount

received from the employers have different tax application as gift under employer till a specific

limit are not taxable. Besides this, it can be inferred that one can reduce tax liability by taking into

account deductions available in relation to wages, interest payment, election expenses etc. It can be

summarized from the evaluation that domicile test provides high level of assistance in determining

whether one is Australian resident for income tax purpose or not.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Woellner, R. and et.al., 2016. Australian Taxation Law 2016. OUP Catalogue.

Davis, K. T., 2016. Dividend imputation and the Australian financial system. Kevin Davis' Dividend

Imputation and the Australian Financial System'JASSA: The Finsia Journal of Applied

Finance. 1. pp.35-40.

Eslake, S., 2015, September. Reforming the Australian taxation system: a principled approach.

In address to the Australian Financial Review's Tax Forum Summit (Vol. 22).

Fitzpatrick, K., 2019, February. The Australian Taxation Office's approaches to aggressive tax

planning. In Centre for Tax System Integrity Third International Conference on'Responsive

Regulation: International perspectives on taxation'. Canberra, 24-25 July 2003.. Centre for Tax

System Integrity (CTSI), Research School of Social Sciences, The Australian National

University.

Online

Amounts not included as income. 2019. [Online]. Available

through<https://www.ato.gov.au/Individuals/Income-and-deductions/Income-you-must-

declare/Amounts-not-included-as-income/>.

Australian resident for tax purposes, explained. 2016. [Online]. Available through

<https://www.quillgroup.com.au/blog/australian-resident-for-tax-purposes-explained/>

Can You Write Off Babysitting Expenses?. 2019. [Online]. Available through:

<https://kidsit.com/babysitting-expenses-parent-tax-guide>.

Claiming mobile phone, internet and home phone expenses. 2019. [Online]. Available through:

<https://www.ato.gov.au/Individuals/Income-and-deductions/Deductions-you-can-claim/Other-

deductions/Claiming-mobile-phone,-internet-and-home-phone-expenses/>.

Deductions. 2019. [Online]. Available through: <https://www.ato.gov.au/Business/Income-and-

deductions-for-business/Deductions/>.

Election expenses. 2019. [Online]. Available through: <https://www.ato.gov.au/Individuals/Income-

and-deductions/Deductions-you-can-claim/Other-deductions/Election-expenses/>.

How to calculate capital gains tax. 2019. [Online]. Available

through<https://www.echoice.com.au/guides/capital-gains-tax-calculated/>.

INCOME TAX ASSESSMENT ACT 1997 - SECT 25.45. 2019. [Online]. Available through:

<http://classic.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s25.45.html>.

FC of T v Day 2008 ATC 20-064

Books and Journals

Woellner, R. and et.al., 2016. Australian Taxation Law 2016. OUP Catalogue.

Davis, K. T., 2016. Dividend imputation and the Australian financial system. Kevin Davis' Dividend

Imputation and the Australian Financial System'JASSA: The Finsia Journal of Applied

Finance. 1. pp.35-40.

Eslake, S., 2015, September. Reforming the Australian taxation system: a principled approach.

In address to the Australian Financial Review's Tax Forum Summit (Vol. 22).

Fitzpatrick, K., 2019, February. The Australian Taxation Office's approaches to aggressive tax

planning. In Centre for Tax System Integrity Third International Conference on'Responsive

Regulation: International perspectives on taxation'. Canberra, 24-25 July 2003.. Centre for Tax

System Integrity (CTSI), Research School of Social Sciences, The Australian National

University.

Online

Amounts not included as income. 2019. [Online]. Available

through<https://www.ato.gov.au/Individuals/Income-and-deductions/Income-you-must-

declare/Amounts-not-included-as-income/>.

Australian resident for tax purposes, explained. 2016. [Online]. Available through

<https://www.quillgroup.com.au/blog/australian-resident-for-tax-purposes-explained/>

Can You Write Off Babysitting Expenses?. 2019. [Online]. Available through:

<https://kidsit.com/babysitting-expenses-parent-tax-guide>.

Claiming mobile phone, internet and home phone expenses. 2019. [Online]. Available through:

<https://www.ato.gov.au/Individuals/Income-and-deductions/Deductions-you-can-claim/Other-

deductions/Claiming-mobile-phone,-internet-and-home-phone-expenses/>.

Deductions. 2019. [Online]. Available through: <https://www.ato.gov.au/Business/Income-and-

deductions-for-business/Deductions/>.

Election expenses. 2019. [Online]. Available through: <https://www.ato.gov.au/Individuals/Income-

and-deductions/Deductions-you-can-claim/Other-deductions/Election-expenses/>.

How to calculate capital gains tax. 2019. [Online]. Available

through<https://www.echoice.com.au/guides/capital-gains-tax-calculated/>.

INCOME TAX ASSESSMENT ACT 1997 - SECT 25.45. 2019. [Online]. Available through:

<http://classic.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s25.45.html>.

FC of T v Day 2008 ATC 20-064

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.