Financial Distress Prediction in Indonesian Manufacturing Industry

VerifiedAdded on 2023/04/21

|22

|8279

|487

Report

AI Summary

This discussion paper, "Predicting Financial Distress in Indonesian Manufacturing Industry," by Muhammad Rifqi and Yoshio Kanazaki, explores the development and evaluation of financial distress prediction models using financial ratios from Indonesian manufacturing companies listed on the Indonesian Stock Exchange between 2003 and 2011. The study employs both traditional statistical methods (Logistic Regression and Discriminant Analysis) and a modern tool (Neural Network) to analyze 23 financial ratios related to liquidity, profitability, leverage, and cash position. The research identifies key ratios contributing to financial distress and constructs prediction models. The results indicate that the ratios identified by logistic regression and the model built on that basis is more appropriate than those derived from discriminant analysis. The paper also highlights the performance of a neural network model, while acknowledging the lack of definitive proof of its absolute superiority over traditional methods. The study uses the book value of total debt exceeding the book value of total assets as a definition of financial distress and discusses the challenges of using bankruptcy data in developing countries, which led to the focus on financial distress prediction. The paper also includes a review of existing literature, including models by Altman, Ohlson, Fulmer, and Shirata, and concludes by outlining potential areas for future research.

Data Science and Service Research

Discussion Paper

Discussion Paper No. 62

Predicting Financial Distress in Indonesian

Manufacturing Industry

MUHAMMAD RIFQI and YOSHIO KANAZAKI

June, 2016

May 2016

Center for Data Science and Service Research

Graduate School of Economic and Management

Tohoku University

27-1 Kawauchi, Aobaku

Sendai 980-8576, JAPAN

Discussion Paper

Discussion Paper No. 62

Predicting Financial Distress in Indonesian

Manufacturing Industry

MUHAMMAD RIFQI and YOSHIO KANAZAKI

June, 2016

May 2016

Center for Data Science and Service Research

Graduate School of Economic and Management

Tohoku University

27-1 Kawauchi, Aobaku

Sendai 980-8576, JAPAN

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

Predicting Financial Distress in Indonesian Manufacturing

Industry

MUHAMMAD RIFQI and YOSHIO KANAZAKI *

ABSTRACT

We attempt to develop and evaluate financial distress prediction models using

financial ratios derived from financial statements of companies in Indonesian

manufacturing industry. The samples are manufacturing companies listed in

Indonesian Stock Exchange during 2003-2011. The models employ two kinds of

methods: traditional statistical modeling (Logistic Regression and Discriminant

Analysis) and modern modeling tool (Neural Network). We evaluate 23 financial

ratios (that measure a company’s liquidity, profitability, leverage, and cash

position) and are able to identify a set of ratios that significantly contribute to

financial distress condition of the companies in sample group. By utilizing those

ratios, prediction models are developed and evaluated based on accuracy and

error rates to determine the best model. The result shows that the ratios

identified by logistic regression and the model built on that basis is more

appropriate than those derived from discriminant analysis. The research also

shows that although the best performing prediction model is a neural network

model, but we have no solid proof of neural network’s absolute superiority over

traditional modeling methods.

Keywords: financial distress, prediction model, discriminant analysis, logistic

regression, neural network.

1. INTRODUCTION

The topic of financial distress prediction has been attracting many researchers’ attention,

especially those in accounting field. Financial distress prediction models have been created

to cope with financial difficulties condition faced by companies, especially in post-crisis

period (Shirata, 1998). The development of prediction models started when Beaver

introduced a simple univariate analysis of financial ratios to predict future bankruptcy

(Beaver, 1966). Since then, many researchers have been struggling to develop financial

distress prediction techniques using statistical models. The most popular example was

* Graduate School of Economics and Management, Tohoku University, Sendai, Japan

This work was supported by JSPS KAKENHI Grant Number JP25380385.

Predicting Financial Distress in Indonesian Manufacturing

Industry

MUHAMMAD RIFQI and YOSHIO KANAZAKI *

ABSTRACT

We attempt to develop and evaluate financial distress prediction models using

financial ratios derived from financial statements of companies in Indonesian

manufacturing industry. The samples are manufacturing companies listed in

Indonesian Stock Exchange during 2003-2011. The models employ two kinds of

methods: traditional statistical modeling (Logistic Regression and Discriminant

Analysis) and modern modeling tool (Neural Network). We evaluate 23 financial

ratios (that measure a company’s liquidity, profitability, leverage, and cash

position) and are able to identify a set of ratios that significantly contribute to

financial distress condition of the companies in sample group. By utilizing those

ratios, prediction models are developed and evaluated based on accuracy and

error rates to determine the best model. The result shows that the ratios

identified by logistic regression and the model built on that basis is more

appropriate than those derived from discriminant analysis. The research also

shows that although the best performing prediction model is a neural network

model, but we have no solid proof of neural network’s absolute superiority over

traditional modeling methods.

Keywords: financial distress, prediction model, discriminant analysis, logistic

regression, neural network.

1. INTRODUCTION

The topic of financial distress prediction has been attracting many researchers’ attention,

especially those in accounting field. Financial distress prediction models have been created

to cope with financial difficulties condition faced by companies, especially in post-crisis

period (Shirata, 1998). The development of prediction models started when Beaver

introduced a simple univariate analysis of financial ratios to predict future bankruptcy

(Beaver, 1966). Since then, many researchers have been struggling to develop financial

distress prediction techniques using statistical models. The most popular example was

* Graduate School of Economics and Management, Tohoku University, Sendai, Japan

This work was supported by JSPS KAKENHI Grant Number JP25380385.

2

Altman Z-Score model which utilizes 5 different financial ratios in his prediction model

(Altman, 1968). Other notable models include Ohlson model in 1980 (Ohlson, 1980), Fulmer

model in 1984 (Fulmer, 1984), and Springate model in 1978 (Springate, 1978). Besides

western researchers, accounting researchers from Asia also present their models, such as

Shirata who presented her first model in 1998 and then updating it in 2003 (the updated

version, being known as SAF2002 model, is widely used in Japan). Sung, Chang, and Lee

(1999) analyzes financial pattern and significant financial ratios to discriminate future

bankrupt companies under different macroeconomic circumstances. Bae (2012) develops a

distress prediction model based on radial basis support vector machine (RSVM) for

companies in South Korean manufacturing industry. In the case of Indonesia, there have

been several but still limited models developed by researchers to predict financial distress.

Indonesian researchers focused mainly on Indonesian manufacturing Industry, such as

Luciana (2003) and Brahmana (2005).

It is important to note that “financial distress” and “bankruptcy” is not the same thing.

Financial distress typically takes place before bankruptcy; therefore it can be considered as

an indicator of bankruptcy (Luciana, 2003). Due to the convenience in obtaining the legal

data and the relatively efficient process of bankruptcy filing, most researchers that use US

companies in their study use the legal definition of bankruptcy in their prediction models. In

other words, they classify the firms which filed for bankruptcy in legal court as the

“bankrupt” group, thus they are developing bankruptcy prediction models, not financial

distress prediction models. Same thing also applies in relatively developed countries where

the bankruptcy filing process can be conducted efficiently, such as Canada (Springate, 1978)

and Japan (Shirata, 1998). Meanwhile, some other researchers use delisting status from the

exchange as their bankruptcy proxy, for example Shumway (2001).

However, for researchers who take the companies in developing economies as their

sample, using legal definition of bankruptcy might pose a grave problem. This is due to the

fact that bankruptcy filing process in a developing country typically takes years to complete,

so it will be a long process until a company can be declared bankrupt. For example, in the

case of Indonesia, a bankruptcy filing process in court usually takes a considerably long time

to undergo, and the data of bankruptcy filing is very hard to obtain from Indonesian

Corporate Court (Zu’amah, 2005). If they decided to use the bankruptcy data for their

prediction models, there will be a significant amount of time lag between the date of

bankruptcy declaration and the financial numbers they use to predict the bankruptcy event,

thus greatly reducing the relevance of their model to predicting the bankruptcy event. Due

to this problem, the researchers in developing countries resort to an alternative strategy:

they use “financial distress” status instead of “bankruptcy” status, thus making their

Altman Z-Score model which utilizes 5 different financial ratios in his prediction model

(Altman, 1968). Other notable models include Ohlson model in 1980 (Ohlson, 1980), Fulmer

model in 1984 (Fulmer, 1984), and Springate model in 1978 (Springate, 1978). Besides

western researchers, accounting researchers from Asia also present their models, such as

Shirata who presented her first model in 1998 and then updating it in 2003 (the updated

version, being known as SAF2002 model, is widely used in Japan). Sung, Chang, and Lee

(1999) analyzes financial pattern and significant financial ratios to discriminate future

bankrupt companies under different macroeconomic circumstances. Bae (2012) develops a

distress prediction model based on radial basis support vector machine (RSVM) for

companies in South Korean manufacturing industry. In the case of Indonesia, there have

been several but still limited models developed by researchers to predict financial distress.

Indonesian researchers focused mainly on Indonesian manufacturing Industry, such as

Luciana (2003) and Brahmana (2005).

It is important to note that “financial distress” and “bankruptcy” is not the same thing.

Financial distress typically takes place before bankruptcy; therefore it can be considered as

an indicator of bankruptcy (Luciana, 2003). Due to the convenience in obtaining the legal

data and the relatively efficient process of bankruptcy filing, most researchers that use US

companies in their study use the legal definition of bankruptcy in their prediction models. In

other words, they classify the firms which filed for bankruptcy in legal court as the

“bankrupt” group, thus they are developing bankruptcy prediction models, not financial

distress prediction models. Same thing also applies in relatively developed countries where

the bankruptcy filing process can be conducted efficiently, such as Canada (Springate, 1978)

and Japan (Shirata, 1998). Meanwhile, some other researchers use delisting status from the

exchange as their bankruptcy proxy, for example Shumway (2001).

However, for researchers who take the companies in developing economies as their

sample, using legal definition of bankruptcy might pose a grave problem. This is due to the

fact that bankruptcy filing process in a developing country typically takes years to complete,

so it will be a long process until a company can be declared bankrupt. For example, in the

case of Indonesia, a bankruptcy filing process in court usually takes a considerably long time

to undergo, and the data of bankruptcy filing is very hard to obtain from Indonesian

Corporate Court (Zu’amah, 2005). If they decided to use the bankruptcy data for their

prediction models, there will be a significant amount of time lag between the date of

bankruptcy declaration and the financial numbers they use to predict the bankruptcy event,

thus greatly reducing the relevance of their model to predicting the bankruptcy event. Due

to this problem, the researchers in developing countries resort to an alternative strategy:

they use “financial distress” status instead of “bankruptcy” status, thus making their

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

prediction models a little different in nature to those of developed countries. However, in

this study we will use the term “financial distress” and “bankruptcy” interchangeably.

It is necessary to understand that there is no single accurate definition of the term

“financial distress” itself. Hofer (1980) as noted in Luciana (2006) defines “financial distress”

as a condition in which a company suffers from negative net income for a consecutive period.

Luciana (2006) herself defines “financial distress” as a condition in which a company is

delisted as a consequence of having negative net income and negative equity. Whitaker

(1999) identifies the condition in which the cash flow of a company is less than the current

portion of company’s long-term debt as definition of company in “financial distress”. Keasey,

et. Al. (2009) and Asquith, Gertner, and Scharfstein (1994) classify a firm as “financially

distressed” if the company’s EBITDA is less than its financial expense for two consecutive

years. Lau (1987) prefers to see “financial distress” as a condition in which a company omits

or reduces dividend payment to its shareholders. In our study, we decided to use the

financial distress definition as stated by Ross (2008) and Luciana (2006), i.e. the book value

of total debt exceeding the book value of total asset.

The statistical methods used to analyze the variables and constructing the model also

vary between researchers. Early researchers in this field used discriminant analysis in their

studies. Beaver (1966) used univariate form of discriminant analysis in his paper, while

multivariate discriminate analysis was used by Altman (1968) in his Z-score model and

Springate (1984). Then Ohlson (1980) opened the alternative way by utilizing logistic

regression in bankruptcy prediction models. Zmijewski (1983) followed suit by also applying

logistic regression analysis in his model.

Revolutionary development of computer science in 1980s also gave rise to several

alternative methods of data analysis researchers can use in constructing prediction models.

Among those methods is neural network. The earliest financial distress study that utilized

neural network method was a study by Odom and Sharda (1990). Several notable researches

that used neural network include Tam and Kiang (1992), Zhang, et. Al. (1999), Atiya (2001),

Virag and Kristof (2005), and Rafiei, et. Al. (2011).

The remainder of the paper is organized as follows. Section 2 describes the data and sample

used in the study. Section 3 discusses the evaluation and selection of best variables to be

included in the model. Section 4 attempts to construct prediction models and analyze them

based on accuracy and error rate. Section 5 concludes the paper and discusses possible

future research ideas.

prediction models a little different in nature to those of developed countries. However, in

this study we will use the term “financial distress” and “bankruptcy” interchangeably.

It is necessary to understand that there is no single accurate definition of the term

“financial distress” itself. Hofer (1980) as noted in Luciana (2006) defines “financial distress”

as a condition in which a company suffers from negative net income for a consecutive period.

Luciana (2006) herself defines “financial distress” as a condition in which a company is

delisted as a consequence of having negative net income and negative equity. Whitaker

(1999) identifies the condition in which the cash flow of a company is less than the current

portion of company’s long-term debt as definition of company in “financial distress”. Keasey,

et. Al. (2009) and Asquith, Gertner, and Scharfstein (1994) classify a firm as “financially

distressed” if the company’s EBITDA is less than its financial expense for two consecutive

years. Lau (1987) prefers to see “financial distress” as a condition in which a company omits

or reduces dividend payment to its shareholders. In our study, we decided to use the

financial distress definition as stated by Ross (2008) and Luciana (2006), i.e. the book value

of total debt exceeding the book value of total asset.

The statistical methods used to analyze the variables and constructing the model also

vary between researchers. Early researchers in this field used discriminant analysis in their

studies. Beaver (1966) used univariate form of discriminant analysis in his paper, while

multivariate discriminate analysis was used by Altman (1968) in his Z-score model and

Springate (1984). Then Ohlson (1980) opened the alternative way by utilizing logistic

regression in bankruptcy prediction models. Zmijewski (1983) followed suit by also applying

logistic regression analysis in his model.

Revolutionary development of computer science in 1980s also gave rise to several

alternative methods of data analysis researchers can use in constructing prediction models.

Among those methods is neural network. The earliest financial distress study that utilized

neural network method was a study by Odom and Sharda (1990). Several notable researches

that used neural network include Tam and Kiang (1992), Zhang, et. Al. (1999), Atiya (2001),

Virag and Kristof (2005), and Rafiei, et. Al. (2011).

The remainder of the paper is organized as follows. Section 2 describes the data and sample

used in the study. Section 3 discusses the evaluation and selection of best variables to be

included in the model. Section 4 attempts to construct prediction models and analyze them

based on accuracy and error rate. Section 5 concludes the paper and discusses possible

future research ideas.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

2. DATA AND SAMPLE

Total sample for our study is 147 companies in Indonesian manufacturing industry over

the course of 9 years (2003-2011). Such time period is chosen due to the availability of data,

and also accounting for post-crisis recovery period. Also included in the sample are the

companies that were delisted from Indonesian Stock Exchange (IDX) and the companies

that changed their core industry either from or to manufacturing industry. We obtain the

data from 2 sources: OSIRIS database of Indonesian public companies and audited financial

statements publicly available from from IDX website (www.idx.co.id).

Among those 147 companies, we notice after analyzing the descriptive statistics that one

company is an outlier (MYRX 2009). In order to avoid misrepresentation and unreliable

model results, we decide to exclude the outlier from our sample. Moreover, we also exclude

11 companies with incomplete financial data. We also prepare a set of holdout sample to be

used as validation measures, in which we calculate the accuracy and error rates of resulting

models to see whether they perform well in the companies not included in the making of the

models.

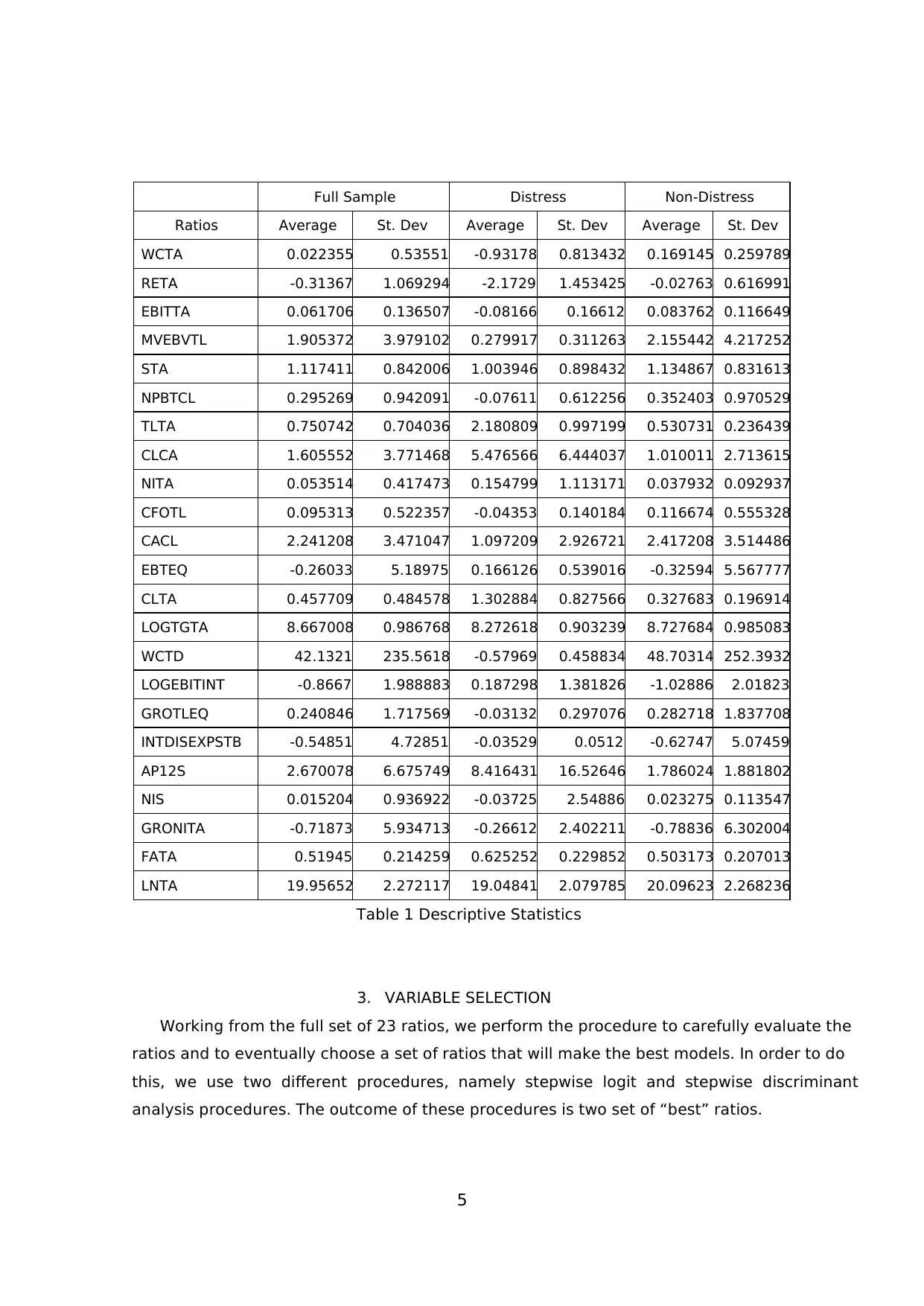

We examine as many as 23 ratios from each sample’s financial statements. We derive

and compile these 23 ratios from previous prediction models, including Altman (1968),

Ohlson (1980), Zmijewski (1983), Springate (1984), Fulmer (1984), Shirata (1998),

Brahmana (2005), and Luciana (2006). Full list of the ratios description is available in

Appendix I. Table 1 displays the descriptive statistics of training sample, split between

distress and non-distress sub-groups.

From the table, we are able to imply that most of the ratios are in-line with our logical

expectation. In overall, non-distress firms have substantially lower average debt level than

distress ones, either in terms of current liability, long-term debt, or total liability. However,

we notice an unexpected anomaly between distress and non-distress in terms of earnings.

The descriptive statistics indicates that distress firms have higher earnings in average than

non-distress firms. The distress sub-group posted higher NITA (0.154799), EBTEQ (0.166126),

LOGEBITINT ( 0.187298), and GRONITA (-0.26612) than non-distress one (0.037932, -0.78836,

-0.32594, and -1.02886respectively). Higher level of debt and higher earnings exhibited by

distress firms could indicate a tendency distress firms taking higher risk in its balance sheet

by intensively using financial leverage in order to achieve higher earnings.

Moreover, we could also notice from the table that distress firms have higher FATA in

average. This indicates that distress firms not only increase their risk on financial but also

on operating leverage front, by employing higher long-term investments which are usually

financed by debts.

2. DATA AND SAMPLE

Total sample for our study is 147 companies in Indonesian manufacturing industry over

the course of 9 years (2003-2011). Such time period is chosen due to the availability of data,

and also accounting for post-crisis recovery period. Also included in the sample are the

companies that were delisted from Indonesian Stock Exchange (IDX) and the companies

that changed their core industry either from or to manufacturing industry. We obtain the

data from 2 sources: OSIRIS database of Indonesian public companies and audited financial

statements publicly available from from IDX website (www.idx.co.id).

Among those 147 companies, we notice after analyzing the descriptive statistics that one

company is an outlier (MYRX 2009). In order to avoid misrepresentation and unreliable

model results, we decide to exclude the outlier from our sample. Moreover, we also exclude

11 companies with incomplete financial data. We also prepare a set of holdout sample to be

used as validation measures, in which we calculate the accuracy and error rates of resulting

models to see whether they perform well in the companies not included in the making of the

models.

We examine as many as 23 ratios from each sample’s financial statements. We derive

and compile these 23 ratios from previous prediction models, including Altman (1968),

Ohlson (1980), Zmijewski (1983), Springate (1984), Fulmer (1984), Shirata (1998),

Brahmana (2005), and Luciana (2006). Full list of the ratios description is available in

Appendix I. Table 1 displays the descriptive statistics of training sample, split between

distress and non-distress sub-groups.

From the table, we are able to imply that most of the ratios are in-line with our logical

expectation. In overall, non-distress firms have substantially lower average debt level than

distress ones, either in terms of current liability, long-term debt, or total liability. However,

we notice an unexpected anomaly between distress and non-distress in terms of earnings.

The descriptive statistics indicates that distress firms have higher earnings in average than

non-distress firms. The distress sub-group posted higher NITA (0.154799), EBTEQ (0.166126),

LOGEBITINT ( 0.187298), and GRONITA (-0.26612) than non-distress one (0.037932, -0.78836,

-0.32594, and -1.02886respectively). Higher level of debt and higher earnings exhibited by

distress firms could indicate a tendency distress firms taking higher risk in its balance sheet

by intensively using financial leverage in order to achieve higher earnings.

Moreover, we could also notice from the table that distress firms have higher FATA in

average. This indicates that distress firms not only increase their risk on financial but also

on operating leverage front, by employing higher long-term investments which are usually

financed by debts.

5

Full Sample Distress Non-Distress

Ratios Average St. Dev Average St. Dev Average St. Dev

WCTA 0.022355 0.53551 -0.93178 0.813432 0.169145 0.259789

RETA -0.31367 1.069294 -2.1729 1.453425 -0.02763 0.616991

EBITTA 0.061706 0.136507 -0.08166 0.16612 0.083762 0.116649

MVEBVTL 1.905372 3.979102 0.279917 0.311263 2.155442 4.217252

STA 1.117411 0.842006 1.003946 0.898432 1.134867 0.831613

NPBTCL 0.295269 0.942091 -0.07611 0.612256 0.352403 0.970529

TLTA 0.750742 0.704036 2.180809 0.997199 0.530731 0.236439

CLCA 1.605552 3.771468 5.476566 6.444037 1.010011 2.713615

NITA 0.053514 0.417473 0.154799 1.113171 0.037932 0.092937

CFOTL 0.095313 0.522357 -0.04353 0.140184 0.116674 0.555328

CACL 2.241208 3.471047 1.097209 2.926721 2.417208 3.514486

EBTEQ -0.26033 5.18975 0.166126 0.539016 -0.32594 5.567777

CLTA 0.457709 0.484578 1.302884 0.827566 0.327683 0.196914

LOGTGTA 8.667008 0.986768 8.272618 0.903239 8.727684 0.985083

WCTD 42.1321 235.5618 -0.57969 0.458834 48.70314 252.3932

LOGEBITINT -0.8667 1.988883 0.187298 1.381826 -1.02886 2.01823

GROTLEQ 0.240846 1.717569 -0.03132 0.297076 0.282718 1.837708

INTDISEXPSTB -0.54851 4.72851 -0.03529 0.0512 -0.62747 5.07459

AP12S 2.670078 6.675749 8.416431 16.52646 1.786024 1.881802

NIS 0.015204 0.936922 -0.03725 2.54886 0.023275 0.113547

GRONITA -0.71873 5.934713 -0.26612 2.402211 -0.78836 6.302004

FATA 0.51945 0.214259 0.625252 0.229852 0.503173 0.207013

LNTA 19.95652 2.272117 19.04841 2.079785 20.09623 2.268236

Table 1 Descriptive Statistics

3. VARIABLE SELECTION

Working from the full set of 23 ratios, we perform the procedure to carefully evaluate the

ratios and to eventually choose a set of ratios that will make the best models. In order to do

this, we use two different procedures, namely stepwise logit and stepwise discriminant

analysis procedures. The outcome of these procedures is two set of “best” ratios.

Full Sample Distress Non-Distress

Ratios Average St. Dev Average St. Dev Average St. Dev

WCTA 0.022355 0.53551 -0.93178 0.813432 0.169145 0.259789

RETA -0.31367 1.069294 -2.1729 1.453425 -0.02763 0.616991

EBITTA 0.061706 0.136507 -0.08166 0.16612 0.083762 0.116649

MVEBVTL 1.905372 3.979102 0.279917 0.311263 2.155442 4.217252

STA 1.117411 0.842006 1.003946 0.898432 1.134867 0.831613

NPBTCL 0.295269 0.942091 -0.07611 0.612256 0.352403 0.970529

TLTA 0.750742 0.704036 2.180809 0.997199 0.530731 0.236439

CLCA 1.605552 3.771468 5.476566 6.444037 1.010011 2.713615

NITA 0.053514 0.417473 0.154799 1.113171 0.037932 0.092937

CFOTL 0.095313 0.522357 -0.04353 0.140184 0.116674 0.555328

CACL 2.241208 3.471047 1.097209 2.926721 2.417208 3.514486

EBTEQ -0.26033 5.18975 0.166126 0.539016 -0.32594 5.567777

CLTA 0.457709 0.484578 1.302884 0.827566 0.327683 0.196914

LOGTGTA 8.667008 0.986768 8.272618 0.903239 8.727684 0.985083

WCTD 42.1321 235.5618 -0.57969 0.458834 48.70314 252.3932

LOGEBITINT -0.8667 1.988883 0.187298 1.381826 -1.02886 2.01823

GROTLEQ 0.240846 1.717569 -0.03132 0.297076 0.282718 1.837708

INTDISEXPSTB -0.54851 4.72851 -0.03529 0.0512 -0.62747 5.07459

AP12S 2.670078 6.675749 8.416431 16.52646 1.786024 1.881802

NIS 0.015204 0.936922 -0.03725 2.54886 0.023275 0.113547

GRONITA -0.71873 5.934713 -0.26612 2.402211 -0.78836 6.302004

FATA 0.51945 0.214259 0.625252 0.229852 0.503173 0.207013

LNTA 19.95652 2.272117 19.04841 2.079785 20.09623 2.268236

Table 1 Descriptive Statistics

3. VARIABLE SELECTION

Working from the full set of 23 ratios, we perform the procedure to carefully evaluate the

ratios and to eventually choose a set of ratios that will make the best models. In order to do

this, we use two different procedures, namely stepwise logit and stepwise discriminant

analysis procedures. The outcome of these procedures is two set of “best” ratios.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

Stepwise Logit Procedure

For the first set of ratios, namely “Set I”, we utilize the stepwise logit method and

procedure as proposed by Draper and Smith (1981). We set the minimum level of

significance to enter the model at 0.05 and the maximum level of significance before removal

at 0.10. This means that a ratio must have a high significance value (p-value lower or at

most 0.05, note that the higher the significance, the lower the p-value) in order for us to

include the ratio into the Set I. After successfully included in the model, the ratio must

continuously score a high significance value when we repeat the procedure and enter other

ratios in order for it to stay in the Set I. If the ratio scores low significance value (p-value

higher than 0.10), we drop the ratio from the model. The procedure is stopped when any of

the previously entered ratios are excluded from the model due to having low significance.

Of all the ratios being analyzed, TLTA seems to have the biggest significance level, thus

we include ratio TLTA in Set I. The inclusion of TLTA somehow seems to damage the

reliability of our analysis, since it always dominates the significance level of the model

produced. TLTA also makes all other variables not significant. While this may be a sign that

TLTA is the only ratio we need to build a solid prediction model, as we go through model

estimation process, we eventually find that the prediction model with a single TLTA ratio

actually scores lower prediction power to other prediction models. Thus, we decide to exclude

TLTA from the beginning of the stepwise logit procedure.

This procedure manages to produce a set of 3 ratios in order to build the first prediction

model. Hereafter we will classify this set as Set I. The selected ratios are represented in

table 2.

Ratios Coeff. S.E. Wald Sig. Exp(B)

WCTA -5.669 2.216 6.547 .011 .003

RETA -5.030 1.671 9.064 .003 .007

MVEBVTL -7.975 2.873 7.704 .006 .000

Constant -3.272 1.073 9.304 .002 .038

Table 2 Stepwise Logit Procedure

Stepwise Discriminant Analysis Procedure

We use the stepwise discriminant analysis procedure stated by Huberty and Olejnik

(2006) to evaluate the ratios and select a set of ratios to be included in our second set of

ratios, namely Set II. With regards to partial F value requirements, we set the minimum

level of partial F required to enter the model at 3.84 and the maximum level of significance

before removal at 2.71. This means that a ratio must have a high partial F (at least 3.84) in

order for us to include the ratio into the model 2. Partial F value of 3.84 is chosen because

Stepwise Logit Procedure

For the first set of ratios, namely “Set I”, we utilize the stepwise logit method and

procedure as proposed by Draper and Smith (1981). We set the minimum level of

significance to enter the model at 0.05 and the maximum level of significance before removal

at 0.10. This means that a ratio must have a high significance value (p-value lower or at

most 0.05, note that the higher the significance, the lower the p-value) in order for us to

include the ratio into the Set I. After successfully included in the model, the ratio must

continuously score a high significance value when we repeat the procedure and enter other

ratios in order for it to stay in the Set I. If the ratio scores low significance value (p-value

higher than 0.10), we drop the ratio from the model. The procedure is stopped when any of

the previously entered ratios are excluded from the model due to having low significance.

Of all the ratios being analyzed, TLTA seems to have the biggest significance level, thus

we include ratio TLTA in Set I. The inclusion of TLTA somehow seems to damage the

reliability of our analysis, since it always dominates the significance level of the model

produced. TLTA also makes all other variables not significant. While this may be a sign that

TLTA is the only ratio we need to build a solid prediction model, as we go through model

estimation process, we eventually find that the prediction model with a single TLTA ratio

actually scores lower prediction power to other prediction models. Thus, we decide to exclude

TLTA from the beginning of the stepwise logit procedure.

This procedure manages to produce a set of 3 ratios in order to build the first prediction

model. Hereafter we will classify this set as Set I. The selected ratios are represented in

table 2.

Ratios Coeff. S.E. Wald Sig. Exp(B)

WCTA -5.669 2.216 6.547 .011 .003

RETA -5.030 1.671 9.064 .003 .007

MVEBVTL -7.975 2.873 7.704 .006 .000

Constant -3.272 1.073 9.304 .002 .038

Table 2 Stepwise Logit Procedure

Stepwise Discriminant Analysis Procedure

We use the stepwise discriminant analysis procedure stated by Huberty and Olejnik

(2006) to evaluate the ratios and select a set of ratios to be included in our second set of

ratios, namely Set II. With regards to partial F value requirements, we set the minimum

level of partial F required to enter the model at 3.84 and the maximum level of significance

before removal at 2.71. This means that a ratio must have a high partial F (at least 3.84) in

order for us to include the ratio into the model 2. Partial F value of 3.84 is chosen because

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

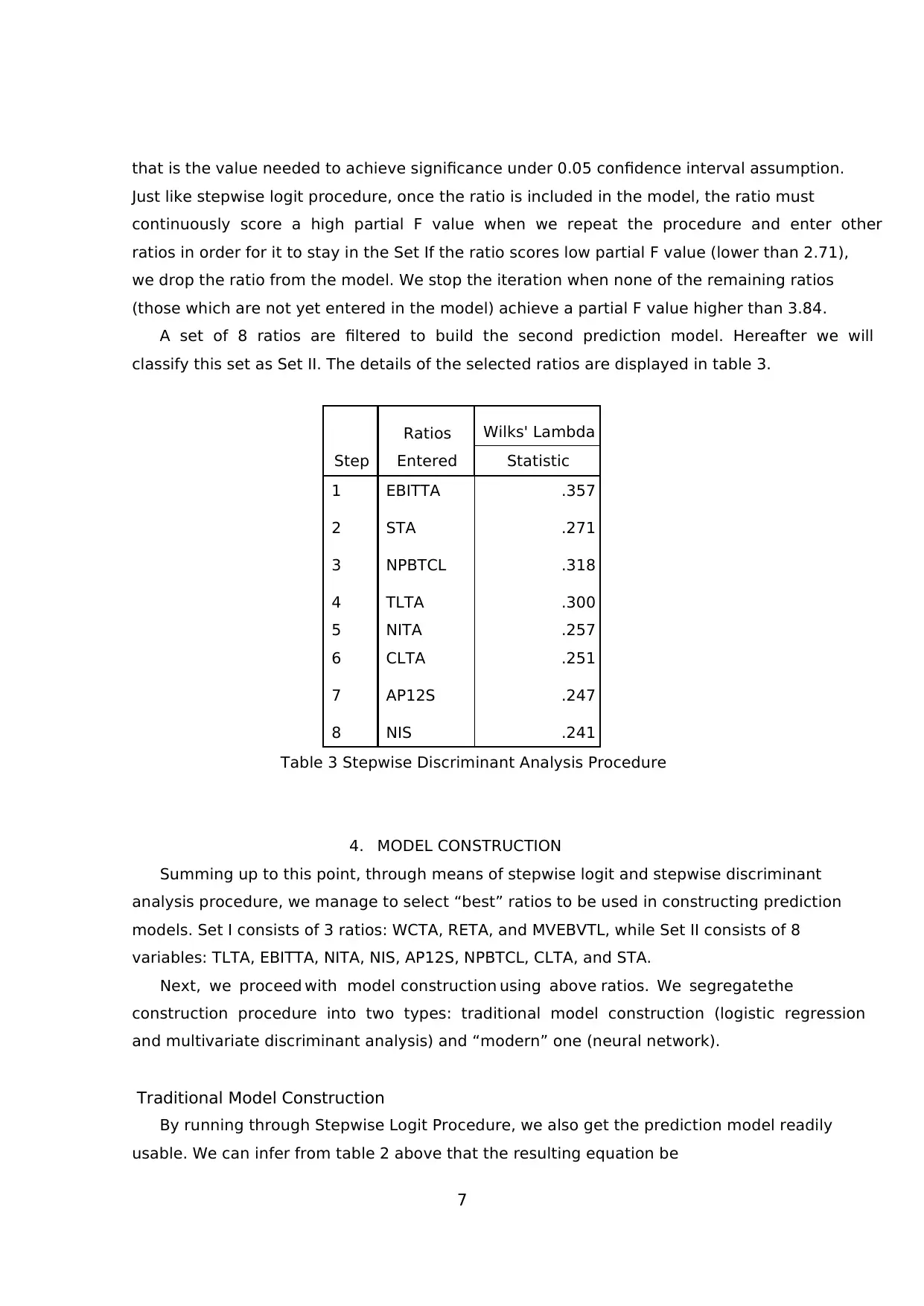

that is the value needed to achieve significance under 0.05 confidence interval assumption.

Just like stepwise logit procedure, once the ratio is included in the model, the ratio must

continuously score a high partial F value when we repeat the procedure and enter other

ratios in order for it to stay in the Set If the ratio scores low partial F value (lower than 2.71),

we drop the ratio from the model. We stop the iteration when none of the remaining ratios

(those which are not yet entered in the model) achieve a partial F value higher than 3.84.

A set of 8 ratios are filtered to build the second prediction model. Hereafter we will

classify this set as Set II. The details of the selected ratios are displayed in table 3.

Step

Ratios

Entered

Wilks' Lambda

Statistic

1 EBITTA .357

2 STA .271

3 NPBTCL .318

4 TLTA .300

5 NITA .257

6 CLTA .251

7 AP12S .247

8 NIS .241

Table 3 Stepwise Discriminant Analysis Procedure

4. MODEL CONSTRUCTION

Summing up to this point, through means of stepwise logit and stepwise discriminant

analysis procedure, we manage to select “best” ratios to be used in constructing prediction

models. Set I consists of 3 ratios: WCTA, RETA, and MVEBVTL, while Set II consists of 8

variables: TLTA, EBITTA, NITA, NIS, AP12S, NPBTCL, CLTA, and STA.

Next, we proceed with model construction using above ratios. We segregate the

construction procedure into two types: traditional model construction (logistic regression

and multivariate discriminant analysis) and “modern” one (neural network).

Traditional Model Construction

By running through Stepwise Logit Procedure, we also get the prediction model readily

usable. We can infer from table 2 above that the resulting equation be

that is the value needed to achieve significance under 0.05 confidence interval assumption.

Just like stepwise logit procedure, once the ratio is included in the model, the ratio must

continuously score a high partial F value when we repeat the procedure and enter other

ratios in order for it to stay in the Set If the ratio scores low partial F value (lower than 2.71),

we drop the ratio from the model. We stop the iteration when none of the remaining ratios

(those which are not yet entered in the model) achieve a partial F value higher than 3.84.

A set of 8 ratios are filtered to build the second prediction model. Hereafter we will

classify this set as Set II. The details of the selected ratios are displayed in table 3.

Step

Ratios

Entered

Wilks' Lambda

Statistic

1 EBITTA .357

2 STA .271

3 NPBTCL .318

4 TLTA .300

5 NITA .257

6 CLTA .251

7 AP12S .247

8 NIS .241

Table 3 Stepwise Discriminant Analysis Procedure

4. MODEL CONSTRUCTION

Summing up to this point, through means of stepwise logit and stepwise discriminant

analysis procedure, we manage to select “best” ratios to be used in constructing prediction

models. Set I consists of 3 ratios: WCTA, RETA, and MVEBVTL, while Set II consists of 8

variables: TLTA, EBITTA, NITA, NIS, AP12S, NPBTCL, CLTA, and STA.

Next, we proceed with model construction using above ratios. We segregate the

construction procedure into two types: traditional model construction (logistic regression

and multivariate discriminant analysis) and “modern” one (neural network).

Traditional Model Construction

By running through Stepwise Logit Procedure, we also get the prediction model readily

usable. We can infer from table 2 above that the resulting equation be

8

1 ; where:

1 y

distress e −

= +

3.272 5.669 5.03 7.975y WCTA RETA MVEBVTL= − − − − …….(1)

Variable distress implies the probability of company suffering from financial distress in

the next fiscal period, WCTA refers to Working Capital per Total Asset, RETA is Retained

Earnings per Total Asset, and MVEBVTL refers to Market Value of Equity divided by Book

Value of Total Liability.

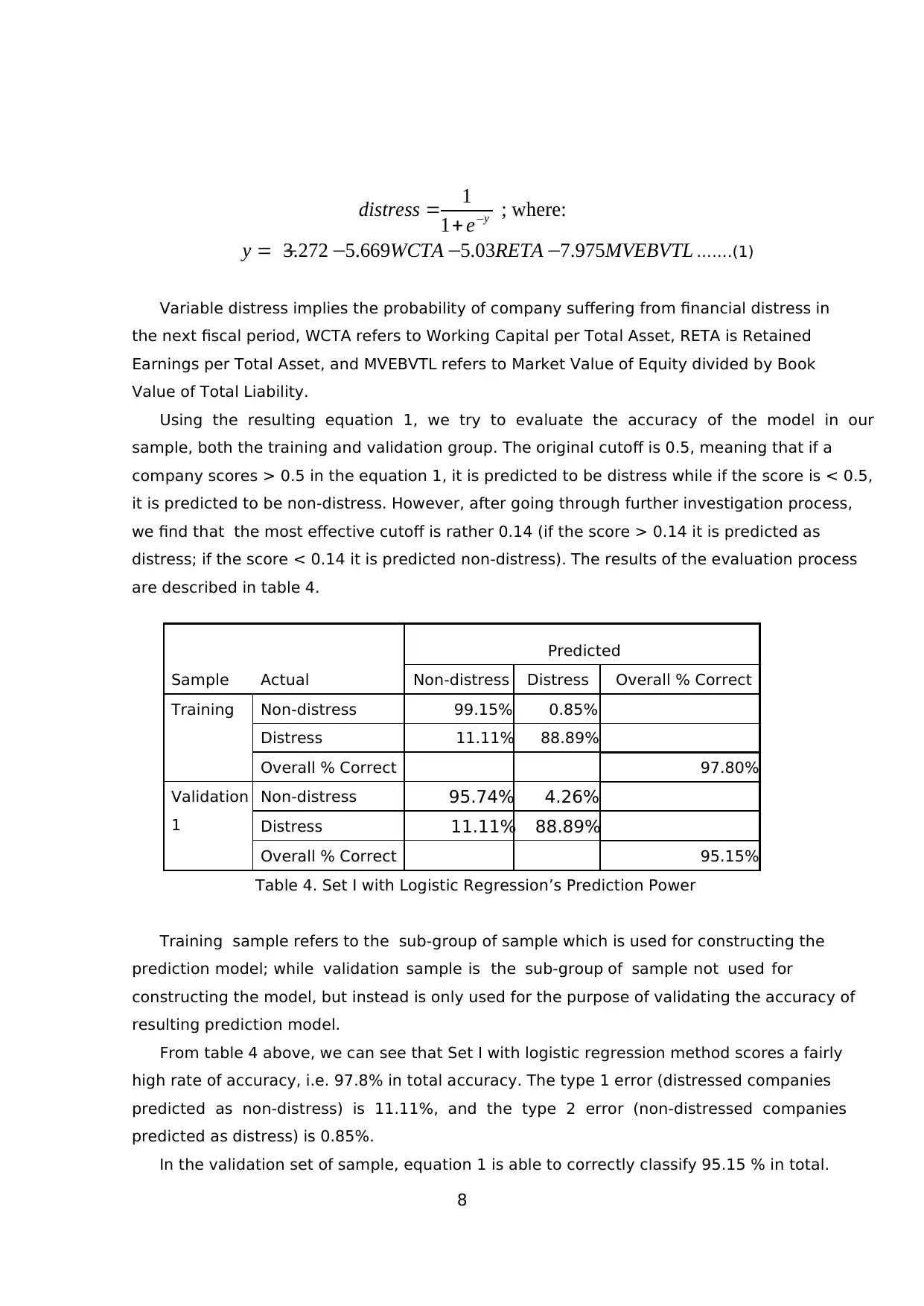

Using the resulting equation 1, we try to evaluate the accuracy of the model in our

sample, both the training and validation group. The original cutoff is 0.5, meaning that if a

company scores > 0.5 in the equation 1, it is predicted to be distress while if the score is < 0.5,

it is predicted to be non-distress. However, after going through further investigation process,

we find that the most effective cutoff is rather 0.14 (if the score > 0.14 it is predicted as

distress; if the score < 0.14 it is predicted non-distress). The results of the evaluation process

are described in table 4.

Sample Actual

Predicted

Non-distress Distress Overall % Correct

Training Non-distress 99.15% 0.85%

Distress 11.11% 88.89%

Overall % Correct 97.80%

Validation

1

Non-distress 95.74% 4.26%

Distress 11.11% 88.89%

Overall % Correct 95.15%

Table 4. Set I with Logistic Regression’s Prediction Power

Training sample refers to the sub-group of sample which is used for constructing the

prediction model; while validation sample is the sub-group of sample not used for

constructing the model, but instead is only used for the purpose of validating the accuracy of

resulting prediction model.

From table 4 above, we can see that Set I with logistic regression method scores a fairly

high rate of accuracy, i.e. 97.8% in total accuracy. The type 1 error (distressed companies

predicted as non-distress) is 11.11%, and the type 2 error (non-distressed companies

predicted as distress) is 0.85%.

In the validation set of sample, equation 1 is able to correctly classify 95.15 % in total.

1 ; where:

1 y

distress e −

= +

3.272 5.669 5.03 7.975y WCTA RETA MVEBVTL= − − − − …….(1)

Variable distress implies the probability of company suffering from financial distress in

the next fiscal period, WCTA refers to Working Capital per Total Asset, RETA is Retained

Earnings per Total Asset, and MVEBVTL refers to Market Value of Equity divided by Book

Value of Total Liability.

Using the resulting equation 1, we try to evaluate the accuracy of the model in our

sample, both the training and validation group. The original cutoff is 0.5, meaning that if a

company scores > 0.5 in the equation 1, it is predicted to be distress while if the score is < 0.5,

it is predicted to be non-distress. However, after going through further investigation process,

we find that the most effective cutoff is rather 0.14 (if the score > 0.14 it is predicted as

distress; if the score < 0.14 it is predicted non-distress). The results of the evaluation process

are described in table 4.

Sample Actual

Predicted

Non-distress Distress Overall % Correct

Training Non-distress 99.15% 0.85%

Distress 11.11% 88.89%

Overall % Correct 97.80%

Validation

1

Non-distress 95.74% 4.26%

Distress 11.11% 88.89%

Overall % Correct 95.15%

Table 4. Set I with Logistic Regression’s Prediction Power

Training sample refers to the sub-group of sample which is used for constructing the

prediction model; while validation sample is the sub-group of sample not used for

constructing the model, but instead is only used for the purpose of validating the accuracy of

resulting prediction model.

From table 4 above, we can see that Set I with logistic regression method scores a fairly

high rate of accuracy, i.e. 97.8% in total accuracy. The type 1 error (distressed companies

predicted as non-distress) is 11.11%, and the type 2 error (non-distressed companies

predicted as distress) is 0.85%.

In the validation set of sample, equation 1 is able to correctly classify 95.15 % in total.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

The characteristic of error is also quite acceptable, with type 1 error at 11.11% and type 2

error at 4.26%.

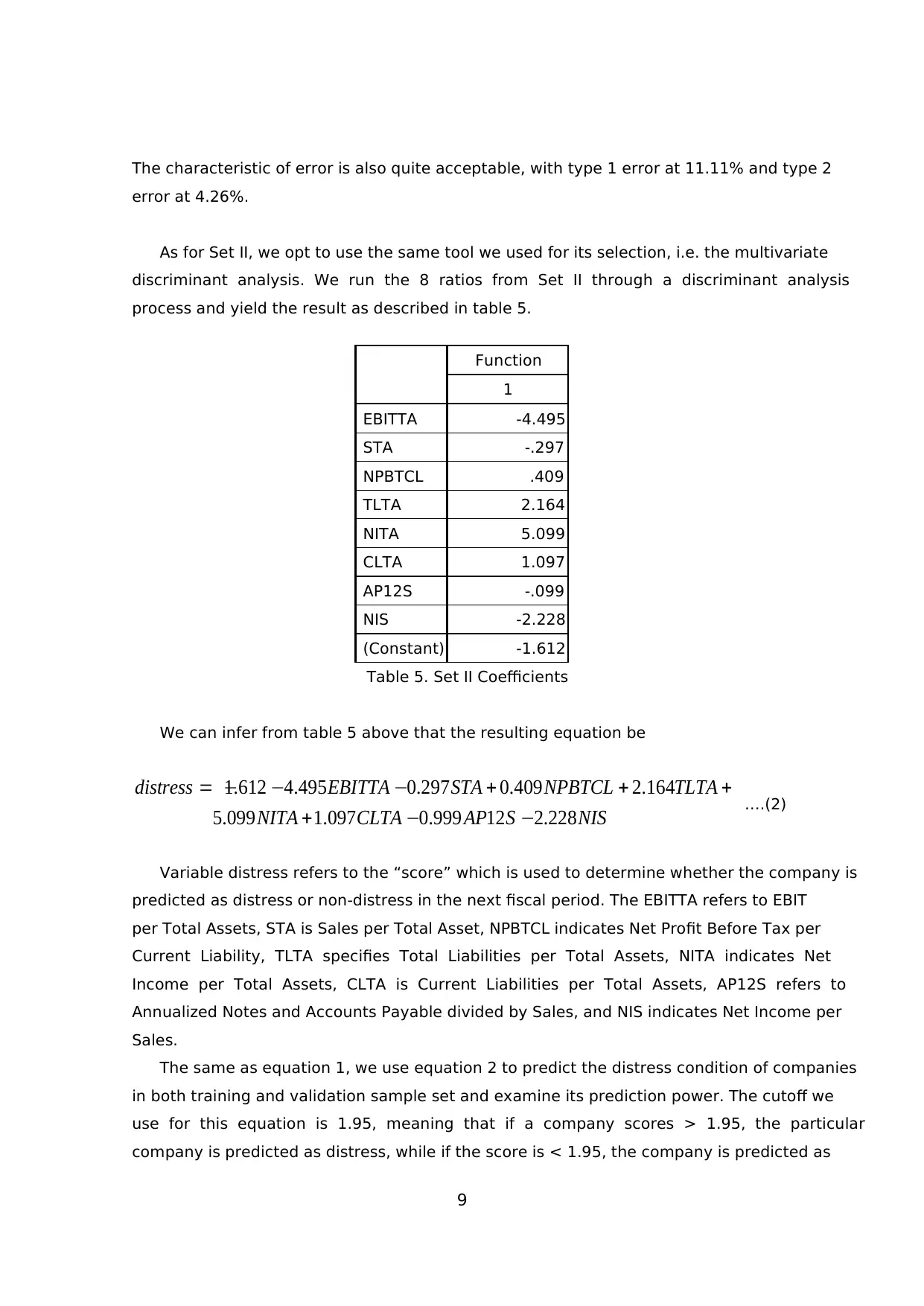

As for Set II, we opt to use the same tool we used for its selection, i.e. the multivariate

discriminant analysis. We run the 8 ratios from Set II through a discriminant analysis

process and yield the result as described in table 5.

Function

1

EBITTA -4.495

STA -.297

NPBTCL .409

TLTA 2.164

NITA 5.099

CLTA 1.097

AP12S -.099

NIS -2.228

(Constant) -1.612

Table 5. Set II Coefficients

We can infer from table 5 above that the resulting equation be

1.612 4.495 0.297 0.409 2.164

5.099 1.097 0.999 12 2.228

distress EBITTA STA NPBTCL TLTA

NITA CLTA AP S NIS

= − − − + + +

+ − − ….(2)

Variable distress refers to the “score” which is used to determine whether the company is

predicted as distress or non-distress in the next fiscal period. The EBITTA refers to EBIT

per Total Assets, STA is Sales per Total Asset, NPBTCL indicates Net Profit Before Tax per

Current Liability, TLTA specifies Total Liabilities per Total Assets, NITA indicates Net

Income per Total Assets, CLTA is Current Liabilities per Total Assets, AP12S refers to

Annualized Notes and Accounts Payable divided by Sales, and NIS indicates Net Income per

Sales.

The same as equation 1, we use equation 2 to predict the distress condition of companies

in both training and validation sample set and examine its prediction power. The cutoff we

use for this equation is 1.95, meaning that if a company scores > 1.95, the particular

company is predicted as distress, while if the score is < 1.95, the company is predicted as

The characteristic of error is also quite acceptable, with type 1 error at 11.11% and type 2

error at 4.26%.

As for Set II, we opt to use the same tool we used for its selection, i.e. the multivariate

discriminant analysis. We run the 8 ratios from Set II through a discriminant analysis

process and yield the result as described in table 5.

Function

1

EBITTA -4.495

STA -.297

NPBTCL .409

TLTA 2.164

NITA 5.099

CLTA 1.097

AP12S -.099

NIS -2.228

(Constant) -1.612

Table 5. Set II Coefficients

We can infer from table 5 above that the resulting equation be

1.612 4.495 0.297 0.409 2.164

5.099 1.097 0.999 12 2.228

distress EBITTA STA NPBTCL TLTA

NITA CLTA AP S NIS

= − − − + + +

+ − − ….(2)

Variable distress refers to the “score” which is used to determine whether the company is

predicted as distress or non-distress in the next fiscal period. The EBITTA refers to EBIT

per Total Assets, STA is Sales per Total Asset, NPBTCL indicates Net Profit Before Tax per

Current Liability, TLTA specifies Total Liabilities per Total Assets, NITA indicates Net

Income per Total Assets, CLTA is Current Liabilities per Total Assets, AP12S refers to

Annualized Notes and Accounts Payable divided by Sales, and NIS indicates Net Income per

Sales.

The same as equation 1, we use equation 2 to predict the distress condition of companies

in both training and validation sample set and examine its prediction power. The cutoff we

use for this equation is 1.95, meaning that if a company scores > 1.95, the particular

company is predicted as distress, while if the score is < 1.95, the company is predicted as

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

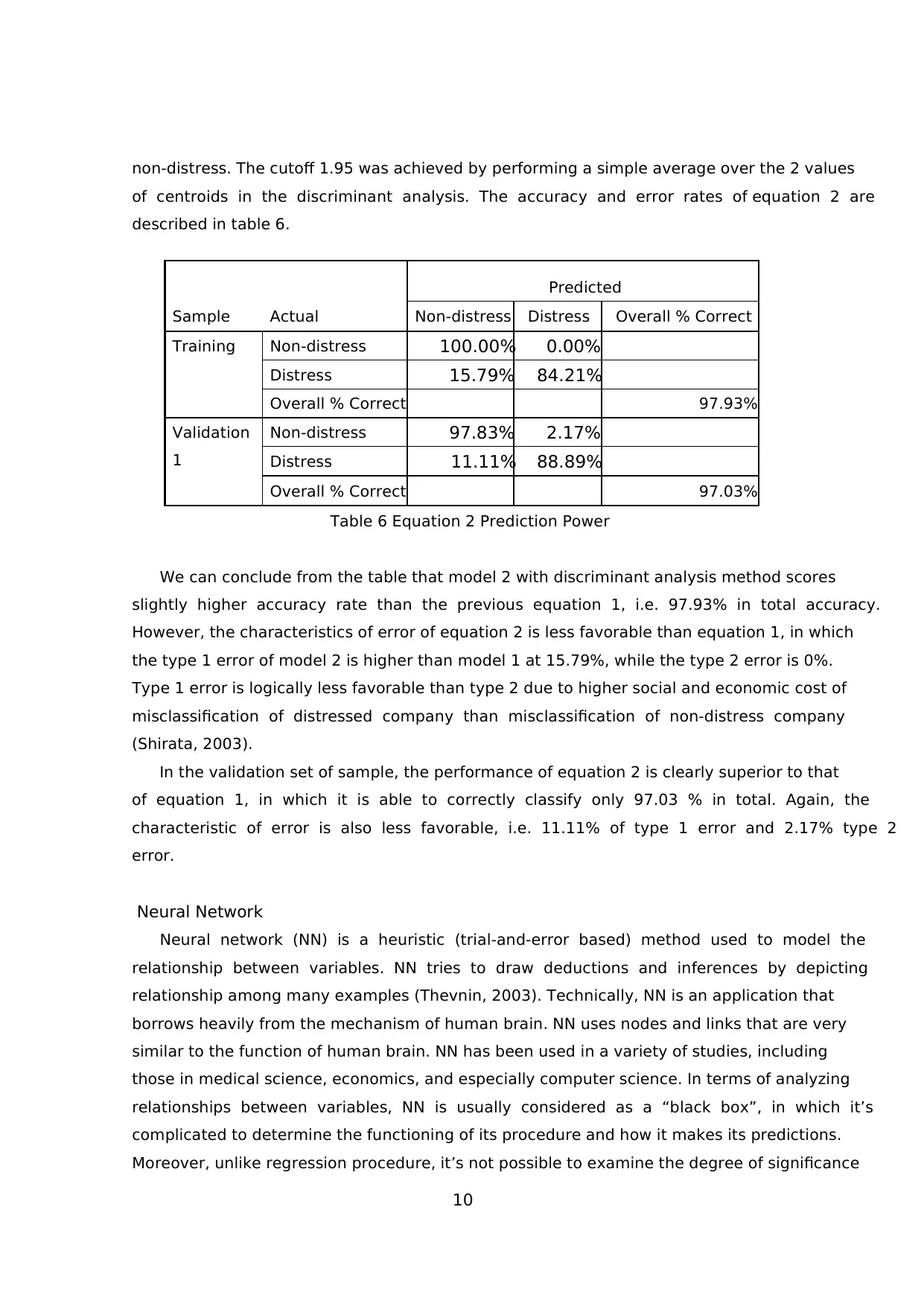

non-distress. The cutoff 1.95 was achieved by performing a simple average over the 2 values

of centroids in the discriminant analysis. The accuracy and error rates of equation 2 are

described in table 6.

Sample Actual

Predicted

Non-distress Distress Overall % Correct

Training Non-distress 100.00% 0.00%

Distress 15.79% 84.21%

Overall % Correct 97.93%

Validation

1

Non-distress 97.83% 2.17%

Distress 11.11% 88.89%

Overall % Correct 97.03%

Table 6 Equation 2 Prediction Power

We can conclude from the table that model 2 with discriminant analysis method scores

slightly higher accuracy rate than the previous equation 1, i.e. 97.93% in total accuracy.

However, the characteristics of error of equation 2 is less favorable than equation 1, in which

the type 1 error of model 2 is higher than model 1 at 15.79%, while the type 2 error is 0%.

Type 1 error is logically less favorable than type 2 due to higher social and economic cost of

misclassification of distressed company than misclassification of non-distress company

(Shirata, 2003).

In the validation set of sample, the performance of equation 2 is clearly superior to that

of equation 1, in which it is able to correctly classify only 97.03 % in total. Again, the

characteristic of error is also less favorable, i.e. 11.11% of type 1 error and 2.17% type 2

error.

Neural Network

Neural network (NN) is a heuristic (trial-and-error based) method used to model the

relationship between variables. NN tries to draw deductions and inferences by depicting

relationship among many examples (Thevnin, 2003). Technically, NN is an application that

borrows heavily from the mechanism of human brain. NN uses nodes and links that are very

similar to the function of human brain. NN has been used in a variety of studies, including

those in medical science, economics, and especially computer science. In terms of analyzing

relationships between variables, NN is usually considered as a “black box”, in which it’s

complicated to determine the functioning of its procedure and how it makes its predictions.

Moreover, unlike regression procedure, it’s not possible to examine the degree of significance

non-distress. The cutoff 1.95 was achieved by performing a simple average over the 2 values

of centroids in the discriminant analysis. The accuracy and error rates of equation 2 are

described in table 6.

Sample Actual

Predicted

Non-distress Distress Overall % Correct

Training Non-distress 100.00% 0.00%

Distress 15.79% 84.21%

Overall % Correct 97.93%

Validation

1

Non-distress 97.83% 2.17%

Distress 11.11% 88.89%

Overall % Correct 97.03%

Table 6 Equation 2 Prediction Power

We can conclude from the table that model 2 with discriminant analysis method scores

slightly higher accuracy rate than the previous equation 1, i.e. 97.93% in total accuracy.

However, the characteristics of error of equation 2 is less favorable than equation 1, in which

the type 1 error of model 2 is higher than model 1 at 15.79%, while the type 2 error is 0%.

Type 1 error is logically less favorable than type 2 due to higher social and economic cost of

misclassification of distressed company than misclassification of non-distress company

(Shirata, 2003).

In the validation set of sample, the performance of equation 2 is clearly superior to that

of equation 1, in which it is able to correctly classify only 97.03 % in total. Again, the

characteristic of error is also less favorable, i.e. 11.11% of type 1 error and 2.17% type 2

error.

Neural Network

Neural network (NN) is a heuristic (trial-and-error based) method used to model the

relationship between variables. NN tries to draw deductions and inferences by depicting

relationship among many examples (Thevnin, 2003). Technically, NN is an application that

borrows heavily from the mechanism of human brain. NN uses nodes and links that are very

similar to the function of human brain. NN has been used in a variety of studies, including

those in medical science, economics, and especially computer science. In terms of analyzing

relationships between variables, NN is usually considered as a “black box”, in which it’s

complicated to determine the functioning of its procedure and how it makes its predictions.

Moreover, unlike regression procedure, it’s not possible to examine the degree of significance

11

of each independent variable. Another major weakness of NN is that it is considerably more

complicated to use compared to a simple and ready-to-use equation produced by logistic

regression or discriminant analysis procedure. Thus a proven and good-performing NN

model might not be able to be exactly replicated by other researchers (for academic purpose)

or to be applied in practice by the common investor. However, unlike traditional statistical

tools which are incapable of identifying non-linear relationship, NN is able to identify either

linear or non-linear relationship that exists in the dataset (Khajanchi, 2002), thus making it

a relatively more powerful predictor than traditional statistical tools.

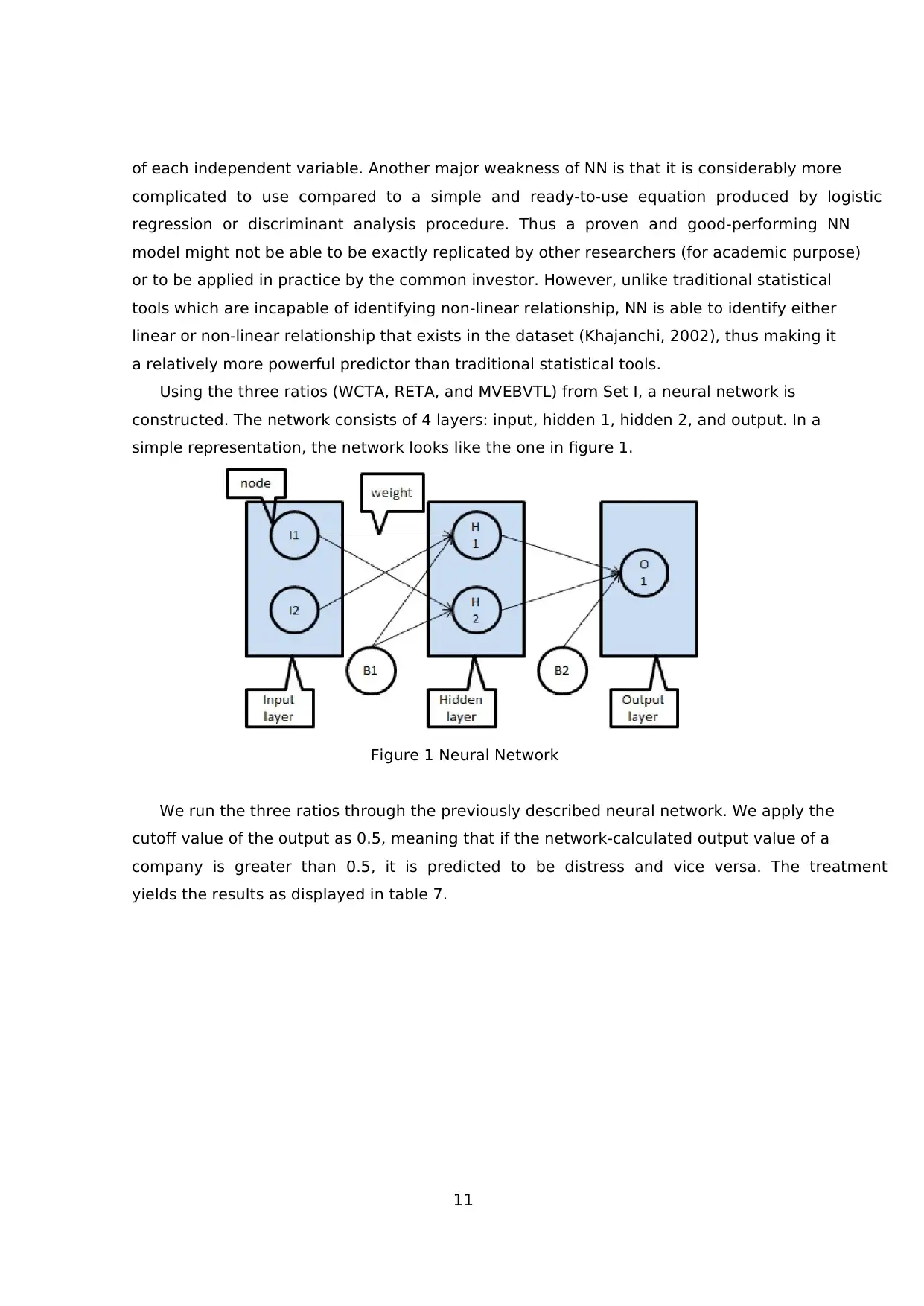

Using the three ratios (WCTA, RETA, and MVEBVTL) from Set I, a neural network is

constructed. The network consists of 4 layers: input, hidden 1, hidden 2, and output. In a

simple representation, the network looks like the one in figure 1.

Figure 1 Neural Network

We run the three ratios through the previously described neural network. We apply the

cutoff value of the output as 0.5, meaning that if the network-calculated output value of a

company is greater than 0.5, it is predicted to be distress and vice versa. The treatment

yields the results as displayed in table 7.

of each independent variable. Another major weakness of NN is that it is considerably more

complicated to use compared to a simple and ready-to-use equation produced by logistic

regression or discriminant analysis procedure. Thus a proven and good-performing NN

model might not be able to be exactly replicated by other researchers (for academic purpose)

or to be applied in practice by the common investor. However, unlike traditional statistical

tools which are incapable of identifying non-linear relationship, NN is able to identify either

linear or non-linear relationship that exists in the dataset (Khajanchi, 2002), thus making it

a relatively more powerful predictor than traditional statistical tools.

Using the three ratios (WCTA, RETA, and MVEBVTL) from Set I, a neural network is

constructed. The network consists of 4 layers: input, hidden 1, hidden 2, and output. In a

simple representation, the network looks like the one in figure 1.

Figure 1 Neural Network

We run the three ratios through the previously described neural network. We apply the

cutoff value of the output as 0.5, meaning that if the network-calculated output value of a

company is greater than 0.5, it is predicted to be distress and vice versa. The treatment

yields the results as displayed in table 7.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.