Detailed Industry Analysis of Singapore's Banking Sector: OCBC Bank

VerifiedAdded on 2023/05/29

|14

|3094

|263

Report

AI Summary

This report provides a comprehensive industry analysis of the Singapore banking sector, using OCBC Bank as a case study. The analysis covers various aspects, including competitor analysis, examining the competitive landscape with a focus on local and foreign banks, their market positions, and product differentiation strategies. It also delves into the dominant economic features of the industry, such as market size, growth rate, and economies of scale. Furthermore, the report utilizes PESTEL analysis and Michael Porter's Five Forces to assess the market space and competitive dynamics, identifying key factors influencing the industry's attractiveness. Finally, it highlights the key success factors for banks in Singapore, such as technology adoption, accessibility, diversification, and cross-border presence, providing valuable insights into the industry's challenges and opportunities.

OCBC Bank 1

INDUSTRY ANALYSIS OF SINGAPORE’S BANKING INDUSTRY

By

Course Name

Tutor/ Professor

University Affiliation

Date

INDUSTRY ANALYSIS OF SINGAPORE’S BANKING INDUSTRY

By

Course Name

Tutor/ Professor

University Affiliation

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

OCBC Bank 2

Executive Summary

Singapore’s banking industry consists of 6 local banks and over 150 foreign banks. The

industry is very competitive with every competitor striving to position themselves in the local

and Asian-Pacific region market. The industry can be broadly divided into two segments which

are foreign banks and local banks. In 2017 the industry had a growth rate of 3.9% which is

expected to increase to around 4.3% by the end 2018. The industry is heavily affected by

external environment factors since it has little control over such forces. The major key Success

factors that influence the success of players in the industry are adoption of technology,

availability to everyone, diversification, and diversification.

Executive Summary

Singapore’s banking industry consists of 6 local banks and over 150 foreign banks. The

industry is very competitive with every competitor striving to position themselves in the local

and Asian-Pacific region market. The industry can be broadly divided into two segments which

are foreign banks and local banks. In 2017 the industry had a growth rate of 3.9% which is

expected to increase to around 4.3% by the end 2018. The industry is heavily affected by

external environment factors since it has little control over such forces. The major key Success

factors that influence the success of players in the industry are adoption of technology,

availability to everyone, diversification, and diversification.

OCBC Bank 3

Table of Contents

Executive Summary.....................................................................................................................................2

Table of Contents........................................................................................................................................3

Introduction.................................................................................................................................................4

Competitor Analysis....................................................................................................................................4

Dominant Economic Features......................................................................................................................6

Market Space...............................................................................................................................................7

Key Success Factors....................................................................................................................................9

Appendix...................................................................................................................................................11

References.................................................................................................................................................12

Table of Contents

Executive Summary.....................................................................................................................................2

Table of Contents........................................................................................................................................3

Introduction.................................................................................................................................................4

Competitor Analysis....................................................................................................................................4

Dominant Economic Features......................................................................................................................6

Market Space...............................................................................................................................................7

Key Success Factors....................................................................................................................................9

Appendix...................................................................................................................................................11

References.................................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

OCBC Bank 4

Introduction

This document focuses on the analysis of the banking industry in Singapore in which case

Oversea Chinese Banking Corporation (OCBC) has been used as the brand of choice. According

to 3E Accounting (2018), Singapore is among the leading finance hubs in the world courtesy of

its banking system. The banking industry is regulated by the Monetary of Authority of

Singapore. Singapore also has the fourth largest foreign exchange market in the world after

London, New York, and Tokyo. OCBC Bank is local bank in Singapore which was established

1932 from the merger of three local banks.

The document discusses into details the following issues; analysis of the industry

competition in which it analysis the number of players in the industry, their market position,

product differentiation, among other issues. Secondly, dominant economic features such as

market size, growth rate, economies of scale, and industry segments, among others. Thirdly,

market space analysis using external environment scanning and Michael Porter Five forces

approach. Fourth, the key Success factors that influence success of banks in the industry.

Competitor Analysis

Scope of industry competition refers to the breadth or narrowness of the level of

competition in a particular industry (Fu et al. 2014). Singapore’s banking industry is very

competitive since it is one of the best finance hubs in the world. The main areas of competition

include; management in which banks compete to hire the most skilled and talented individuals

whose input will give the bank a competitive edge. Secondly, market share in which banks

compete to dominate both the local market and the global markets. Thirdly, product and service

innovation in which every bank strives to have the most unique and attractive products in the

market (Fu et al. 2014).

Introduction

This document focuses on the analysis of the banking industry in Singapore in which case

Oversea Chinese Banking Corporation (OCBC) has been used as the brand of choice. According

to 3E Accounting (2018), Singapore is among the leading finance hubs in the world courtesy of

its banking system. The banking industry is regulated by the Monetary of Authority of

Singapore. Singapore also has the fourth largest foreign exchange market in the world after

London, New York, and Tokyo. OCBC Bank is local bank in Singapore which was established

1932 from the merger of three local banks.

The document discusses into details the following issues; analysis of the industry

competition in which it analysis the number of players in the industry, their market position,

product differentiation, among other issues. Secondly, dominant economic features such as

market size, growth rate, economies of scale, and industry segments, among others. Thirdly,

market space analysis using external environment scanning and Michael Porter Five forces

approach. Fourth, the key Success factors that influence success of banks in the industry.

Competitor Analysis

Scope of industry competition refers to the breadth or narrowness of the level of

competition in a particular industry (Fu et al. 2014). Singapore’s banking industry is very

competitive since it is one of the best finance hubs in the world. The main areas of competition

include; management in which banks compete to hire the most skilled and talented individuals

whose input will give the bank a competitive edge. Secondly, market share in which banks

compete to dominate both the local market and the global markets. Thirdly, product and service

innovation in which every bank strives to have the most unique and attractive products in the

market (Fu et al. 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

OCBC Bank 5

The banking industry in Singapore according MAS (2018) consists of 6 local banks and

over 150 foreign banks. The foreign banks are further classified into four categories which are;

full banks consisting of 27 banks, Wholesale banks consisting of 53 banks, offshore banks

consisting of 37 banks, and merchant banks consisting of 42 banks. The major players in the

industry measured by assets are; DBS (Development Bank of Singapore), OCBC, UOB (United

Overseas Bank), HSBC (The Hong Kong and Shanghai Banking Corporation), Standard

Chartered Bank, ABN-AMRO Singapore, Maybank, BNP Paribas, and Citi bank (MAS 2018).

OCBC bank has managed to secure the second position in terms of assets since it has total assets

of about 184 billion Singapore dollars (OCBC 2018).

Product differentiation refers to making a product to be unique so that it can be more

attractive in the market than what the competitors’ products (Camgöz Akdag and Zineldin 2011).

The major banks in Singapore have leveraged on technology to differentiate their products. The

major ways in which OCBC bank has differentiated its products include; introduction of the

OCBC Pay Anyone technology that allows customers to pay using phone numbers, email, or

even Facebook accounts. Secondly, FRANK by OCBC which offers customers with over 100

card designs. FRANK cards also enable customers to get discounts at various online retail shops

(The Financial Brand 2018).

OCBC bank competitors vary in their level of competition depending on their scope of

operation. The major competitors are Development Bank of Singapore and United Overseas

Bank since they are both local banks just as OCBC is, therefore, they have the same operational

privileges (MAS 2018). The second largest competitors of OCBC bank are the foreign bank

under the category of full banks such as Citi Bank, Standard Chartered, HSBC, Maybank, ABN

AMRO and BNP Paribas. This is because these banks are allowed by the banking law in

The banking industry in Singapore according MAS (2018) consists of 6 local banks and

over 150 foreign banks. The foreign banks are further classified into four categories which are;

full banks consisting of 27 banks, Wholesale banks consisting of 53 banks, offshore banks

consisting of 37 banks, and merchant banks consisting of 42 banks. The major players in the

industry measured by assets are; DBS (Development Bank of Singapore), OCBC, UOB (United

Overseas Bank), HSBC (The Hong Kong and Shanghai Banking Corporation), Standard

Chartered Bank, ABN-AMRO Singapore, Maybank, BNP Paribas, and Citi bank (MAS 2018).

OCBC bank has managed to secure the second position in terms of assets since it has total assets

of about 184 billion Singapore dollars (OCBC 2018).

Product differentiation refers to making a product to be unique so that it can be more

attractive in the market than what the competitors’ products (Camgöz Akdag and Zineldin 2011).

The major banks in Singapore have leveraged on technology to differentiate their products. The

major ways in which OCBC bank has differentiated its products include; introduction of the

OCBC Pay Anyone technology that allows customers to pay using phone numbers, email, or

even Facebook accounts. Secondly, FRANK by OCBC which offers customers with over 100

card designs. FRANK cards also enable customers to get discounts at various online retail shops

(The Financial Brand 2018).

OCBC bank competitors vary in their level of competition depending on their scope of

operation. The major competitors are Development Bank of Singapore and United Overseas

Bank since they are both local banks just as OCBC is, therefore, they have the same operational

privileges (MAS 2018). The second largest competitors of OCBC bank are the foreign bank

under the category of full banks such as Citi Bank, Standard Chartered, HSBC, Maybank, ABN

AMRO and BNP Paribas. This is because these banks are allowed by the banking law in

OCBC Bank 6

Singapore to offer a full range of banking services. The least competitors are the foreign banks

under the category of offshore banks since they do not deal with the Singapore dollar, therefore,

they cannot offer competition in the domestic market (MAS 2018).

OCBC bank can employ several competitive strategies to outsmart its competitors. The

strategies according to Tanwar (2013) include; Cost leadership which will involve reducing the

overall cost of operations without compromising the quality of their services. This will enable

OCBC to offer its products such as loans at favorable rates than its competitors thus attracting

more customers. Secondly, OCBC can differentiate its products by continuously innovating and

adding new features to the products so that they can be the most appealing in the market.

Thirdly, OCBC can adopt market development techniques such as agency banking. These

techniques will help OCBC to increase its geographical market coverage, increase its market

share, strengthen its brand, and benefit from mass selling.

Dominant Economic Features

Market Size refers to the total number of potential customers in a particular market

(Berry and Waldfogel 2010). Singapore’s banking sector has a very large market size since, in a

country of about 4 million people above the age of 15 years (Department of Statistics Singapore

2018), 96% of them have a bank account. Also, Singapore’s banks serve the entire Asian

continent whose population can be estimated to be approximately 4.5 billion (Worldometers

2018). This shows that there are still opportunities for Singaporean banks to expand their market

penetration rates and customer base.

The banking industry in Singapore is progressing well having registered a growth rate of

3.9% in 2017 and the rate is expected to increase to about 4.2% by the end of 2018 (MAS 2018).

Singapore to offer a full range of banking services. The least competitors are the foreign banks

under the category of offshore banks since they do not deal with the Singapore dollar, therefore,

they cannot offer competition in the domestic market (MAS 2018).

OCBC bank can employ several competitive strategies to outsmart its competitors. The

strategies according to Tanwar (2013) include; Cost leadership which will involve reducing the

overall cost of operations without compromising the quality of their services. This will enable

OCBC to offer its products such as loans at favorable rates than its competitors thus attracting

more customers. Secondly, OCBC can differentiate its products by continuously innovating and

adding new features to the products so that they can be the most appealing in the market.

Thirdly, OCBC can adopt market development techniques such as agency banking. These

techniques will help OCBC to increase its geographical market coverage, increase its market

share, strengthen its brand, and benefit from mass selling.

Dominant Economic Features

Market Size refers to the total number of potential customers in a particular market

(Berry and Waldfogel 2010). Singapore’s banking sector has a very large market size since, in a

country of about 4 million people above the age of 15 years (Department of Statistics Singapore

2018), 96% of them have a bank account. Also, Singapore’s banks serve the entire Asian

continent whose population can be estimated to be approximately 4.5 billion (Worldometers

2018). This shows that there are still opportunities for Singaporean banks to expand their market

penetration rates and customer base.

The banking industry in Singapore is progressing well having registered a growth rate of

3.9% in 2017 and the rate is expected to increase to about 4.2% by the end of 2018 (MAS 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

OCBC Bank 7

The industry life cycle consist of four stages which are; introduction, growth, maturity, and

decline (Martin and Sunley 2011). The banking industry in Singapore is currently in its growth

stage. This can be justified by the fact that the industry is registering increasing growth rates

every year and continues investment in technology to improve operational efficiency.

Economies of scale refers to the cost advantage experienced by an organization when it

buys, produces, distributes, and sells products and services in large scale (Hughes and Mester

2013). In Singapore’s banking industry, many banks enjoy economies of scale in areas such as;

product advertisement in which the adverts target a wide local and global market thus reducing

the cost of advertisement per unit. Product distribution in which case the banks have adopted

technology-based banking which enables them to serve a wide customer base at a lower cost.

The banking sector in Singapore has been segmented into two major segments which are

local banks and foreign banks. Foreign banks are further classified into full banks, Wholesale

banks, offshore banks, and Merchant banks (MAS 2018). OCBC Bank is in the category of local

banks and this gives it a competitive edge in the sense that, by being a local bank it is given full

banking rights by the banking act, unlike some foreign banks which are not allowed to handle the

Singapore dollar (MAS 2018).

Market Space

The PESTEL analysis of Singapore’s banking industry is as follows; Political factors

include; labor laws, trade restrictions, and taxation laws. Economic factors include inflation and

deflation which affects the value of money (OCBC 2018). Social factors include change in

customer behavior and demographics which forces banks to develop new products or

continuously improve existing products. Technological factors include the rapid growth of

The industry life cycle consist of four stages which are; introduction, growth, maturity, and

decline (Martin and Sunley 2011). The banking industry in Singapore is currently in its growth

stage. This can be justified by the fact that the industry is registering increasing growth rates

every year and continues investment in technology to improve operational efficiency.

Economies of scale refers to the cost advantage experienced by an organization when it

buys, produces, distributes, and sells products and services in large scale (Hughes and Mester

2013). In Singapore’s banking industry, many banks enjoy economies of scale in areas such as;

product advertisement in which the adverts target a wide local and global market thus reducing

the cost of advertisement per unit. Product distribution in which case the banks have adopted

technology-based banking which enables them to serve a wide customer base at a lower cost.

The banking sector in Singapore has been segmented into two major segments which are

local banks and foreign banks. Foreign banks are further classified into full banks, Wholesale

banks, offshore banks, and Merchant banks (MAS 2018). OCBC Bank is in the category of local

banks and this gives it a competitive edge in the sense that, by being a local bank it is given full

banking rights by the banking act, unlike some foreign banks which are not allowed to handle the

Singapore dollar (MAS 2018).

Market Space

The PESTEL analysis of Singapore’s banking industry is as follows; Political factors

include; labor laws, trade restrictions, and taxation laws. Economic factors include inflation and

deflation which affects the value of money (OCBC 2018). Social factors include change in

customer behavior and demographics which forces banks to develop new products or

continuously improve existing products. Technological factors include the rapid growth of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

OCBC Bank 8

banking technology which forces banks to increase their investment in technology (3E

Accounting 2018). Environmental factors have no much impact on the banking industry in

Singapore. The legal factors include; legislation such as the banking act of Singapore which

dictates how banks should conduct their operations, the Securities and Futures act which affects

the banks that deal with capital markets services (MAS 2018).

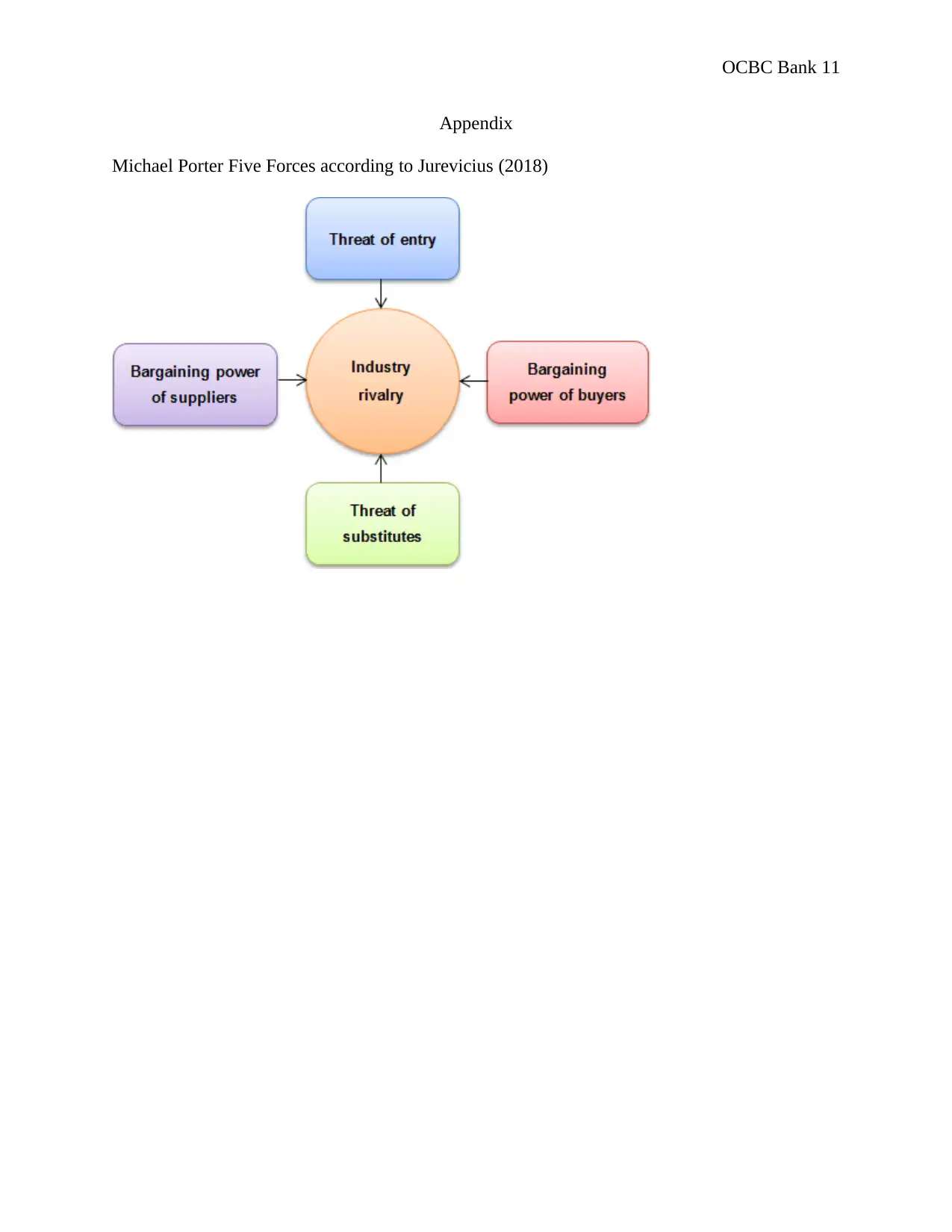

Michael Porter five forces

Competitive rivalry: OCBC bank faces competition from both local and foreign banks

although local banks such as DBS bank offer the highest competition. Threats of new entrants:

Singapore is an attractive financial hub and an open economy, therefore, new banks can easily be

established (MAS 2018). Threats of substitute products; the banking industry has minimal

threats from substitute products due to the nature of its products. The power of suppliers: the

suppliers of OCBC bank are the people who save their money in the bank. Their power ranges

from medium to high due to presence of other banks. The power of buyers; these are people who

obtain loans. They are less powerful due to the high switching cost.

The forces that are likely to strengthen include; competitive rivalry due to continues

product improvement and technology used by various banks. Secondly, threats of new entrants

due to favorable economic situations that attracts foreign banks. On the other hand, the force that

is likely to weaken is the bargaining power of buyers due to the high switching cost associated

with shifting from one bank to the other. This includes the creditworthiness profile and credit

terms, among others (Karim et al. 2010).

banking technology which forces banks to increase their investment in technology (3E

Accounting 2018). Environmental factors have no much impact on the banking industry in

Singapore. The legal factors include; legislation such as the banking act of Singapore which

dictates how banks should conduct their operations, the Securities and Futures act which affects

the banks that deal with capital markets services (MAS 2018).

Michael Porter five forces

Competitive rivalry: OCBC bank faces competition from both local and foreign banks

although local banks such as DBS bank offer the highest competition. Threats of new entrants:

Singapore is an attractive financial hub and an open economy, therefore, new banks can easily be

established (MAS 2018). Threats of substitute products; the banking industry has minimal

threats from substitute products due to the nature of its products. The power of suppliers: the

suppliers of OCBC bank are the people who save their money in the bank. Their power ranges

from medium to high due to presence of other banks. The power of buyers; these are people who

obtain loans. They are less powerful due to the high switching cost.

The forces that are likely to strengthen include; competitive rivalry due to continues

product improvement and technology used by various banks. Secondly, threats of new entrants

due to favorable economic situations that attracts foreign banks. On the other hand, the force that

is likely to weaken is the bargaining power of buyers due to the high switching cost associated

with shifting from one bank to the other. This includes the creditworthiness profile and credit

terms, among others (Karim et al. 2010).

OCBC Bank 9

The forces differ across segments in the sense that, OCBC bank faces higher competition

rivalry from the segment of local banks than from the segment of foreign banks. Secondly,

OCBC faces higher threats of new entrants from the foreign bank segment than from local bank

segment. This is due to the fact that many global banks that are not currently operating in

Singapore can easily start their operations in the country since the country has an open economy

(MAS 2018).

Industry attractiveness refers to the future profit potential of a market in relation to ease

of making profit. The banking sector in Singapore is very attractive since it is among the leading

global financial hubs. Thus it will be easy for banks based in Singapore to expand their

operations all over Asia and increase their profitability (Haw, et al. 2010). Also, the industry is

growing at a good rate which provides an opportunity for a firm to position itself in the market.

Understanding of consumer trends gives an organization a competitive edge. In

Singapore, the latest consumer trends in the banking sector include; many citizens in Singapore

are preferring online banking platforms to over-the-counter services so that they can remotely

access their bank accounts (Deloitte 2018). Secondly, the foreigners who work in Singapore are

preferring to have the travel credit cards so that they can easily use them in their home countries.

Key Success Factors

The main industry issues that affect success of banks in Singapore’s banking industry

include; Technology adoption which is the ability of a bank to offer its products using

information technologies such as mobile banking and online payment (3 E Accounting 2018).

Accessibility to everyone which refers to the ability of a bank to offer products that are

differentiated to suit the interest of different market segments (Deloitte 2018). Diversification

The forces differ across segments in the sense that, OCBC bank faces higher competition

rivalry from the segment of local banks than from the segment of foreign banks. Secondly,

OCBC faces higher threats of new entrants from the foreign bank segment than from local bank

segment. This is due to the fact that many global banks that are not currently operating in

Singapore can easily start their operations in the country since the country has an open economy

(MAS 2018).

Industry attractiveness refers to the future profit potential of a market in relation to ease

of making profit. The banking sector in Singapore is very attractive since it is among the leading

global financial hubs. Thus it will be easy for banks based in Singapore to expand their

operations all over Asia and increase their profitability (Haw, et al. 2010). Also, the industry is

growing at a good rate which provides an opportunity for a firm to position itself in the market.

Understanding of consumer trends gives an organization a competitive edge. In

Singapore, the latest consumer trends in the banking sector include; many citizens in Singapore

are preferring online banking platforms to over-the-counter services so that they can remotely

access their bank accounts (Deloitte 2018). Secondly, the foreigners who work in Singapore are

preferring to have the travel credit cards so that they can easily use them in their home countries.

Key Success Factors

The main industry issues that affect success of banks in Singapore’s banking industry

include; Technology adoption which is the ability of a bank to offer its products using

information technologies such as mobile banking and online payment (3 E Accounting 2018).

Accessibility to everyone which refers to the ability of a bank to offer products that are

differentiated to suit the interest of different market segments (Deloitte 2018). Diversification

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

OCBC Bank 10

which is the ability of bank to offer other products and services such as insurance and capital

markets services. Cross-border presence which refers to the acceptability of a bank in the Asian-

pacific region.

Some Key success factors such as adoption of technology and Cross-border presence are

consistent across segments. This is because whether a bank is a local or a foreign bank, it has to

invest in technology and be socially acceptable in the region in order to succeed in its operations.

On the other hand, some Key Success factors such as diversification and accessibility to

everyone may not apply to banks in the foreign banks segment. This is because not all foreign

banks have been licensed to operate as full banks in Singapore. Thus, some cannot venture into

capital market services (MAS 2018).

The various stages of an industry lifecycle demands unique strategies in each stage in

order to guarantee success (Stark 2015). In the introduction stage, the bank mainly focuses on a

particular line of products. Thus diversification does not apply. In the growth stage, investment

in technology is the major success factor for many banks (Deloitte 2018). In the Maturity stage

accessibility to everyone is the major key success factor that many banks focus on. In the decline

stage, the banks diversify their operations in order to serve new markets and sustain their

operations in the industry.

which is the ability of bank to offer other products and services such as insurance and capital

markets services. Cross-border presence which refers to the acceptability of a bank in the Asian-

pacific region.

Some Key success factors such as adoption of technology and Cross-border presence are

consistent across segments. This is because whether a bank is a local or a foreign bank, it has to

invest in technology and be socially acceptable in the region in order to succeed in its operations.

On the other hand, some Key Success factors such as diversification and accessibility to

everyone may not apply to banks in the foreign banks segment. This is because not all foreign

banks have been licensed to operate as full banks in Singapore. Thus, some cannot venture into

capital market services (MAS 2018).

The various stages of an industry lifecycle demands unique strategies in each stage in

order to guarantee success (Stark 2015). In the introduction stage, the bank mainly focuses on a

particular line of products. Thus diversification does not apply. In the growth stage, investment

in technology is the major success factor for many banks (Deloitte 2018). In the Maturity stage

accessibility to everyone is the major key success factor that many banks focus on. In the decline

stage, the banks diversify their operations in order to serve new markets and sustain their

operations in the industry.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

OCBC Bank 11

Appendix

Michael Porter Five Forces according to Jurevicius (2018)

Appendix

Michael Porter Five Forces according to Jurevicius (2018)

OCBC Bank 12

References

3E Accounting (2018). Singapore’s Banking Industry and Its Major Banks | Business in

Singapore. [online] 3E Accounting Firm Singapore. Available at:

https://www.3ecpa.com.sg/resources/miscellaneous-topics/singapore-banking-industry-and-its-

major-banks/ [Accessed 27 Nov. 2018].

Berry, S. and Waldfogel, J. (2010). Product quality and market size. The Journal of Industrial

Economics, 58(1), pp.1-31.

Camgöz Akdag, H. and Zineldin, M. (2011). Strategic positioning and quality determinants in

banking service. The TQM Journal, 23(4), pp.446-457.

Deloitte (2018). 2018 Banking Industry Outlook | Deloitte US. [online] Deloitte United States.

Available at: https://www2.deloitte.com/us/en/pages/financial-services/articles/banking-industry-

outlook.html [Accessed 27 Nov. 2018].

Department of Statistics Singapore (2018). Population and Population Structure - Latest Data.

[online] Base. Available at:

https://www.singstat.gov.sg/find-data/search-by-theme/population/population-and-population-

structure/latest-data [Accessed 27 Nov. 2018].

Fu, X.M., Lin, Y.R. and Molyneux, P. (2014). Bank competition and financial stability in Asia

Pacific. Journal of Banking & Finance, 38, pp.64-77.

Haw, I.M., Ho, S.S., Hu, B. and Wu, D. (2010). Concentrated control, institutions, and banking

sector: An international study. Journal of Banking & Finance, 34(3), pp.480-497.

References

3E Accounting (2018). Singapore’s Banking Industry and Its Major Banks | Business in

Singapore. [online] 3E Accounting Firm Singapore. Available at:

https://www.3ecpa.com.sg/resources/miscellaneous-topics/singapore-banking-industry-and-its-

major-banks/ [Accessed 27 Nov. 2018].

Berry, S. and Waldfogel, J. (2010). Product quality and market size. The Journal of Industrial

Economics, 58(1), pp.1-31.

Camgöz Akdag, H. and Zineldin, M. (2011). Strategic positioning and quality determinants in

banking service. The TQM Journal, 23(4), pp.446-457.

Deloitte (2018). 2018 Banking Industry Outlook | Deloitte US. [online] Deloitte United States.

Available at: https://www2.deloitte.com/us/en/pages/financial-services/articles/banking-industry-

outlook.html [Accessed 27 Nov. 2018].

Department of Statistics Singapore (2018). Population and Population Structure - Latest Data.

[online] Base. Available at:

https://www.singstat.gov.sg/find-data/search-by-theme/population/population-and-population-

structure/latest-data [Accessed 27 Nov. 2018].

Fu, X.M., Lin, Y.R. and Molyneux, P. (2014). Bank competition and financial stability in Asia

Pacific. Journal of Banking & Finance, 38, pp.64-77.

Haw, I.M., Ho, S.S., Hu, B. and Wu, D. (2010). Concentrated control, institutions, and banking

sector: An international study. Journal of Banking & Finance, 34(3), pp.480-497.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.