ECON15: Information Asymmetry, Risks, and Investor Solutions Report

VerifiedAdded on 2022/12/29

|20

|5246

|59

Report

AI Summary

This report, prepared for an Economics 15 course, delves into the concept of information asymmetry, exploring two primary forms: adverse selection and moral hazard. It examines how these asymmetries create risks within financial markets, including market freezes, credit rationing, and complications in financial contracts. The report further analyzes the implications of these risks, such as maturity mismatches and deterioration of balance sheets, which can lead to financial instability. It provides insights into the challenges faced by both lenders and borrowers, as well as the strategies investors can employ to mitigate the negative impacts. Furthermore, the report includes a case study that analyzes economic and accounting profits, the role of managerial economics, and the difference between entrepreneurs and managers. The report also examines the roles of entrepreneurs and managers within an organization.

Running head: ECONOMICS

Economics

Name of the Student:

Name of the University:

Author note:

Economics

Name of the Student:

Name of the University:

Author note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ECONOMICS

TASK 1: ESSAY

Topic: Explain two forms of information asymmetry. Discuss the risks they might cause in

financial market and explain how investors can overcome these risks.

Information asymmetry is a common feature in economics. It is also known as

information failure. As stated by Courtney, Dutta and Li (2017), asymmetric information occurs

in situations where one party in an economic transaction possesses more information than the

other party. It is a common incidence in a transaction where the seller possesses more knowledge

about the product or service than the buyers. Thus, almost all economic transactions in all types

of markets involve information asymmetry.

As seen from the World Bank publication (2012), in the welfare theorem of economics, it

says that prices, in a competitive economy with no externalities, would adjust in a manner which

leads to resource allocation in a Pareto optimal way. However, the assumption of this theorem is

that all the parties should equally know the characteristics of all the products traded in the market

and when this assumption fails to hold then, information asymmetry arises, resulting in price

distortion and resource allocation that is not Pareto optimal. The standard government

inventions, like, monopoly regulation for creating a competitive environment, or implementing

fiscal policies for alleviating the effects of the externalities, are not much effective in restoring

optimality in case of asymmetric information. In the context of finance, as per the Modigliani-

Miller theorem, a firm’s value is independent of the financial structure of the firm. The

organizations have agreed to the existence of asymmetric information and the provision of

incentives is used to align the interests of the managers and the employees with that of the

stakeholders (Brusov et al. 2018).

TASK 1: ESSAY

Topic: Explain two forms of information asymmetry. Discuss the risks they might cause in

financial market and explain how investors can overcome these risks.

Information asymmetry is a common feature in economics. It is also known as

information failure. As stated by Courtney, Dutta and Li (2017), asymmetric information occurs

in situations where one party in an economic transaction possesses more information than the

other party. It is a common incidence in a transaction where the seller possesses more knowledge

about the product or service than the buyers. Thus, almost all economic transactions in all types

of markets involve information asymmetry.

As seen from the World Bank publication (2012), in the welfare theorem of economics, it

says that prices, in a competitive economy with no externalities, would adjust in a manner which

leads to resource allocation in a Pareto optimal way. However, the assumption of this theorem is

that all the parties should equally know the characteristics of all the products traded in the market

and when this assumption fails to hold then, information asymmetry arises, resulting in price

distortion and resource allocation that is not Pareto optimal. The standard government

inventions, like, monopoly regulation for creating a competitive environment, or implementing

fiscal policies for alleviating the effects of the externalities, are not much effective in restoring

optimality in case of asymmetric information. In the context of finance, as per the Modigliani-

Miller theorem, a firm’s value is independent of the financial structure of the firm. The

organizations have agreed to the existence of asymmetric information and the provision of

incentives is used to align the interests of the managers and the employees with that of the

stakeholders (Brusov et al. 2018).

2ECONOMICS

Information asymmetry results in an imbalance of power in the economic transactions,

which can lead to market failure. Examples of this are adverse selection and moral hazard.

Asymmetric information often extends to non-economic behavior. It is seen that as the private

firs generally possess more information than the regulators regarding the actions that could take

place in the absence of regulations, the effectiveness of regulations are decreased (Cai et al.

2015). On the other hand, asymmetric information also refers to the division and specialization

of knowledge applied to all types of economic trade and there are both economic advantages and

disadvantages of asymmetric information. Bergh et al. (2019) stated that, in a financial

transaction between a stockbroker and a non-investment professional, the knowledge of the

stockbroker is more valuable than that of the non-investment professional, who might be

interested in stock trading. On the contrary, the disadvantages of information asymmetry results

in market failures, adverse selection and moral hazard.

Adverse selection is an effect of asymmetric information. As stated by Lauermann and

Wolinsky (2016), adverse selection refers to the situation, in which two or more individuals or

agents are about to agree on an economic trade and one of the parties happens to have some

information about the product or service that the other(s) do not have. On the other hand, moral

hazard refers to a situation where one party takes more risks as the costs that could occur due to

the economic transaction could be borne by the other party who is not taking the risks (Roberts

2015).

As highlighted by Stroebel (2016), adverse selection causes arrangements, which allows

for market segmentation as per the unobserved quality of the product or service. For example,

banks and insurance companies screen the customers by using the collateral requirements and

deductibles. The sellers send signal about the quality of their products through the product

Information asymmetry results in an imbalance of power in the economic transactions,

which can lead to market failure. Examples of this are adverse selection and moral hazard.

Asymmetric information often extends to non-economic behavior. It is seen that as the private

firs generally possess more information than the regulators regarding the actions that could take

place in the absence of regulations, the effectiveness of regulations are decreased (Cai et al.

2015). On the other hand, asymmetric information also refers to the division and specialization

of knowledge applied to all types of economic trade and there are both economic advantages and

disadvantages of asymmetric information. Bergh et al. (2019) stated that, in a financial

transaction between a stockbroker and a non-investment professional, the knowledge of the

stockbroker is more valuable than that of the non-investment professional, who might be

interested in stock trading. On the contrary, the disadvantages of information asymmetry results

in market failures, adverse selection and moral hazard.

Adverse selection is an effect of asymmetric information. As stated by Lauermann and

Wolinsky (2016), adverse selection refers to the situation, in which two or more individuals or

agents are about to agree on an economic trade and one of the parties happens to have some

information about the product or service that the other(s) do not have. On the other hand, moral

hazard refers to a situation where one party takes more risks as the costs that could occur due to

the economic transaction could be borne by the other party who is not taking the risks (Roberts

2015).

As highlighted by Stroebel (2016), adverse selection causes arrangements, which allows

for market segmentation as per the unobserved quality of the product or service. For example,

banks and insurance companies screen the customers by using the collateral requirements and

deductibles. The sellers send signal about the quality of their products through the product

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ECONOMICS

warrantees to the customers while they do not provide much information about product itself. In

other words, the markets are not segmented on the basis of inherent information, such as,

warrantees and deductibles, rather it is done from a menu of contracts, which includes elements

like high deductible with low insurance premium or low deductibles with high insurance

premium, or for the product market, low price with no warrantee and high price with one year

warrantee, offered to the agents leading to self-selection based on the price and it reveals their

private information. Sellers of high quality products prefer to charge higher price with one year

warrantee for the products while sellers of low quality products would prefer not to give any

warrantee and hence would opt for lower price. In such situations, the buyers do not have better

information about the products and they make their selection based on little information (Lester

et al. 2019). Thus, adverse selection is a common form of information asymmetry.

On the contrary, moral hazard arises in situations where information asymmetry occurs

after two or more individuals enter into agreements (Roberts 2015). Principal-agent problem is a

common feature of moral hazard. In this problem, one party (principal) hires another party

(agent) for a particular task or activity. As stated by Hennessy and Wolf (2018), once the

principal and agent sign the contract, the agent can either take up a hidden action, non-

observable for the principal, or can obtain hidden information about some of the characteristics

of the working environment that cannot be acquired by the principal. In this case, the agents are

provided with same menu of contracts which must take into consideration the asymmetries that

could arise in the future and hence, address the incentives problems. Thus, when an insurance

company provides an insurance contract to a car driver, it cannot observe if the driver is working

carelessly, causing accidents and claiming insurance money. Albertazzi et al. (2016) argued that

warrantees to the customers while they do not provide much information about product itself. In

other words, the markets are not segmented on the basis of inherent information, such as,

warrantees and deductibles, rather it is done from a menu of contracts, which includes elements

like high deductible with low insurance premium or low deductibles with high insurance

premium, or for the product market, low price with no warrantee and high price with one year

warrantee, offered to the agents leading to self-selection based on the price and it reveals their

private information. Sellers of high quality products prefer to charge higher price with one year

warrantee for the products while sellers of low quality products would prefer not to give any

warrantee and hence would opt for lower price. In such situations, the buyers do not have better

information about the products and they make their selection based on little information (Lester

et al. 2019). Thus, adverse selection is a common form of information asymmetry.

On the contrary, moral hazard arises in situations where information asymmetry occurs

after two or more individuals enter into agreements (Roberts 2015). Principal-agent problem is a

common feature of moral hazard. In this problem, one party (principal) hires another party

(agent) for a particular task or activity. As stated by Hennessy and Wolf (2018), once the

principal and agent sign the contract, the agent can either take up a hidden action, non-

observable for the principal, or can obtain hidden information about some of the characteristics

of the working environment that cannot be acquired by the principal. In this case, the agents are

provided with same menu of contracts which must take into consideration the asymmetries that

could arise in the future and hence, address the incentives problems. Thus, when an insurance

company provides an insurance contract to a car driver, it cannot observe if the driver is working

carelessly, causing accidents and claiming insurance money. Albertazzi et al. (2016) argued that

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ECONOMICS

the world or market with perfect information is hypothetical and an optimal contract in a moral

hazard environment must trade of the insurance and the incentive provisions.

It can be inferred that information asymmetry causes various types of risks in the

financial market. As stated by Kirabaeva (2011), adverse selection often lead to market freezes

and liquidity hoarding, which reflects buyers’ beliefs that most of the securities that are offered

for sale are of poor quality. Various risk factors such as uncertainties about the value of the

assets, flight to liquidity and underestimation of the systematic risks can intensify the impacts of

adverse selection in particular markets and proliferate the effects to the entire financial system.

The author also stated that government intervention can moderate the problems of adverse

selection in the financial markets. The effectiveness of the policy responses depends on the cause

of a market freeze.

Fishman and Parker (2015) pointed out that adverse selection in the financial markets can

happen through several channels, such as, rise in the interest rates, deterioration of the balance

sheets of the financial institutions, and maturity mismatch and all these lead to the risk of

financial instability. Due to adverse selection for asymmetric information, a small rise in the rate

of interest may result in large reduction in the lending. Higher rate of interest raises the

likelihood that the high-quality borrowers withdraw from the market, which aggravates the

problem of adverse selection. Thus, the average quality of the borrowers falls, resulting in further

rise of the interest rate as a security measure. Extreme adverse selection can lead to a collapse of

the credit market. It can also lead the banks to impose credit rationing, that is, imposing

quantitative limits on lending to particular borrowers (Ambrose, Conklin and Yoshida 2016).

Another risk of asymmetric information is the complication in financial contract. There can be

differences in the projects in terms of their distribution of returns and the actual distribution ratio

the world or market with perfect information is hypothetical and an optimal contract in a moral

hazard environment must trade of the insurance and the incentive provisions.

It can be inferred that information asymmetry causes various types of risks in the

financial market. As stated by Kirabaeva (2011), adverse selection often lead to market freezes

and liquidity hoarding, which reflects buyers’ beliefs that most of the securities that are offered

for sale are of poor quality. Various risk factors such as uncertainties about the value of the

assets, flight to liquidity and underestimation of the systematic risks can intensify the impacts of

adverse selection in particular markets and proliferate the effects to the entire financial system.

The author also stated that government intervention can moderate the problems of adverse

selection in the financial markets. The effectiveness of the policy responses depends on the cause

of a market freeze.

Fishman and Parker (2015) pointed out that adverse selection in the financial markets can

happen through several channels, such as, rise in the interest rates, deterioration of the balance

sheets of the financial institutions, and maturity mismatch and all these lead to the risk of

financial instability. Due to adverse selection for asymmetric information, a small rise in the rate

of interest may result in large reduction in the lending. Higher rate of interest raises the

likelihood that the high-quality borrowers withdraw from the market, which aggravates the

problem of adverse selection. Thus, the average quality of the borrowers falls, resulting in further

rise of the interest rate as a security measure. Extreme adverse selection can lead to a collapse of

the credit market. It can also lead the banks to impose credit rationing, that is, imposing

quantitative limits on lending to particular borrowers (Ambrose, Conklin and Yoshida 2016).

Another risk of asymmetric information is the complication in financial contract. There can be

differences in the projects in terms of their distribution of returns and the actual distribution ratio

5ECONOMICS

is known to the entrepreneur but not to the other party in the transaction, which can result in

complications (Mahoney and Weyl 2017). Lastly, maturity mismatch in another important risk in

the financial market arising from adverse selection. Many financial organizations finance long

term investment with short term debt and the resulting maturity mismatch makes them more

vulnerable to economic shocks (Converse 2018). Furthermore, it is highlighted by Goodhart and

Perotti (2015), maturity mismatch can deteriorate the balance sheets, which was one of the major

reasons for the global financial crisis in 2007-09. The deterioration in the balance sheets

increases credit risk of the financial institution.

Thus, to address the risks arising from the adverse selection problem, the banks should

limit the supply of loans. This way the banks can reduce the average default risk and therefore

can alleviate adverse-selection problems (Jiménez et al. 2017). Another way for reducing the

risks from adverse selection is asking for collateral for the loan (Stroebel 2016). With the

presence of collateral, even if the borrower defaults, the lender can recover the losses by selling

the collateral. Therefore, the asymmetric information regarding the borrower’s default

probability becomes less significant.

Moral hazard also bears some risk, such as, borrowers might engage in the activities

which are undesirable for the lenders as that might make the borrowers less likely to pay back

the loans. Thus, Cvitanić, Possamaï and Touzi (2016) stated that moral hazard creates a situation

in which one party has the incentive to take unusual risks in the business as the party is unlikely

to suffer the potential losses. The risks of moral hazard mostly arise in the businesses of

insurance and also in employer-employee relationships. Thus, as the insurance provider cannot

control the actions of the individual or the party who took insurance, it bears the risk of adverse

consequences, similarly, in the employer-employee relationships, the employers face the risk of

is known to the entrepreneur but not to the other party in the transaction, which can result in

complications (Mahoney and Weyl 2017). Lastly, maturity mismatch in another important risk in

the financial market arising from adverse selection. Many financial organizations finance long

term investment with short term debt and the resulting maturity mismatch makes them more

vulnerable to economic shocks (Converse 2018). Furthermore, it is highlighted by Goodhart and

Perotti (2015), maturity mismatch can deteriorate the balance sheets, which was one of the major

reasons for the global financial crisis in 2007-09. The deterioration in the balance sheets

increases credit risk of the financial institution.

Thus, to address the risks arising from the adverse selection problem, the banks should

limit the supply of loans. This way the banks can reduce the average default risk and therefore

can alleviate adverse-selection problems (Jiménez et al. 2017). Another way for reducing the

risks from adverse selection is asking for collateral for the loan (Stroebel 2016). With the

presence of collateral, even if the borrower defaults, the lender can recover the losses by selling

the collateral. Therefore, the asymmetric information regarding the borrower’s default

probability becomes less significant.

Moral hazard also bears some risk, such as, borrowers might engage in the activities

which are undesirable for the lenders as that might make the borrowers less likely to pay back

the loans. Thus, Cvitanić, Possamaï and Touzi (2016) stated that moral hazard creates a situation

in which one party has the incentive to take unusual risks in the business as the party is unlikely

to suffer the potential losses. The risks of moral hazard mostly arise in the businesses of

insurance and also in employer-employee relationships. Thus, as the insurance provider cannot

control the actions of the individual or the party who took insurance, it bears the risk of adverse

consequences, similarly, in the employer-employee relationships, the employers face the risk of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ECONOMICS

misuse of the company resources by the employees. The mortgage scrutinization is a reason for

moral hazard which is one of the major reasons of subprime meltdown and global financial crisis

of 2007-09 (Nehf 2017).

Various measures can be taken to reduce moral hazard issues and the risks, such as,

incentives, immoral behavior and regular monitoring. The financial institutions can make build

in incentives, that is, a contract that gives an incentive to the borrowers for insuring the products

themselves and the financial institutions pay less amount as insurance (Allen et al. 2015). The

institutions should also make measures to penalize the bad behavior to mitigate the risk of moral

hazard that can be taken by borrowers. Furthermore, these institutions can introduce performance

related pay for the labor market to reduce the risks of moral hazard in the employer employee

relationship and those can be taken done on the basis of performance evaluation and a penalty

option, such as, no guarantee of a job in lifetime (Boden and Galizzi 2016).

misuse of the company resources by the employees. The mortgage scrutinization is a reason for

moral hazard which is one of the major reasons of subprime meltdown and global financial crisis

of 2007-09 (Nehf 2017).

Various measures can be taken to reduce moral hazard issues and the risks, such as,

incentives, immoral behavior and regular monitoring. The financial institutions can make build

in incentives, that is, a contract that gives an incentive to the borrowers for insuring the products

themselves and the financial institutions pay less amount as insurance (Allen et al. 2015). The

institutions should also make measures to penalize the bad behavior to mitigate the risk of moral

hazard that can be taken by borrowers. Furthermore, these institutions can introduce performance

related pay for the labor market to reduce the risks of moral hazard in the employer employee

relationship and those can be taken done on the basis of performance evaluation and a penalty

option, such as, no guarantee of a job in lifetime (Boden and Galizzi 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ECONOMICS

TASK 2: CASE STUDY

Answers to Question 1

a) Economic profit refers to the difference between the revenue earned from the output sales

and the opportunity cost of the inputs used. It subtracts both the implicit and explicit costs

of the business from the total revenue. On the other hand, accounting profit refers to the

difference between the gross revenue and the explicit cost or deductible expenses (Kaplan

and Atkinson 2015). John PLC will be interested in their economic profit as it indicates

how well the resources were utilized by the company. There can be an accounting profit

yet the company can face economic loss.

b) Managerial economics refers to the integration of the economic theories with the business

practices for facilitating the decision making and forward planning by the management of

any organization. Thus, nature of managerial economics is to enhance the technical and

conceptual skill of the manager to increase their efficiency in decision making for

production, inventory, cost, marketing, financial, human resources and for other

miscellaneous activities for achieving business objectives (Salvatore 2015). Scope of

managerial economic lies in forward planning. By integrating economic theories it

enables the managers to apply strategic tools to achieve profitability in the long run

through production and cost analysis, resource allocation, demand analysis and

forecasting, price policies, capital management and profit maximization (Froeb, McCann

and Ward 2015).

c) The primary difference between entrepreneurs and managers is their role within the

organization. While an entrepreneur is the owner of an organization and is a risk taker,

TASK 2: CASE STUDY

Answers to Question 1

a) Economic profit refers to the difference between the revenue earned from the output sales

and the opportunity cost of the inputs used. It subtracts both the implicit and explicit costs

of the business from the total revenue. On the other hand, accounting profit refers to the

difference between the gross revenue and the explicit cost or deductible expenses (Kaplan

and Atkinson 2015). John PLC will be interested in their economic profit as it indicates

how well the resources were utilized by the company. There can be an accounting profit

yet the company can face economic loss.

b) Managerial economics refers to the integration of the economic theories with the business

practices for facilitating the decision making and forward planning by the management of

any organization. Thus, nature of managerial economics is to enhance the technical and

conceptual skill of the manager to increase their efficiency in decision making for

production, inventory, cost, marketing, financial, human resources and for other

miscellaneous activities for achieving business objectives (Salvatore 2015). Scope of

managerial economic lies in forward planning. By integrating economic theories it

enables the managers to apply strategic tools to achieve profitability in the long run

through production and cost analysis, resource allocation, demand analysis and

forecasting, price policies, capital management and profit maximization (Froeb, McCann

and Ward 2015).

c) The primary difference between entrepreneurs and managers is their role within the

organization. While an entrepreneur is the owner of an organization and is a risk taker,

8ECONOMICS

who takes financial risks for his company, a manager is not the owner, but an employee

of the organization and is not a risk taker, but is responsible for managing and

administering group of people (Paul and Shrivatava 2015). Thus, in the context of John

PLC, the entrepreneurship skill is beneficial for risk taking ventures, while managerial

skills are beneficial for successful organization and synchronization of all the

departments for efficient functioning.

Answers to Question 2

a) Externality refers to the benefit or cost to a third party who is not directly involved in the

economic activity generating externalities or has no control on the creation of the benefit

or cost (Pal 2015). It can be both positive and negative. As John PLC is construction

company, it generates positive externality by constructing residential and commercial

buildings while the pollution generated from the construction activities is the negative

externality for the people living nearby.

b) Fixed cost refers to the overhead cost that remains same and unaffected irrespective of

the level of output. Fixed costs for John PLC includes the lease or rent for the building,

electricity charge, equipment cost, utility charges, insurance, and interest payments. On

the other hand, variable costs are those that vary with the level of output produced. When

production increases (decreases), variable cost increases (decreases). The costs of

manufacturing or construction increases with the number of units supplied by the

company, which is the variable cost (Chen and Koebel 2017).

c) Similar to any other organization, one of the primary objectives of John PLC is to grow

its business and increase profit. Thus, John PLC will want to grow for growing its profit,

achieving economies of scale, and capturing larger market share. However, the most

who takes financial risks for his company, a manager is not the owner, but an employee

of the organization and is not a risk taker, but is responsible for managing and

administering group of people (Paul and Shrivatava 2015). Thus, in the context of John

PLC, the entrepreneurship skill is beneficial for risk taking ventures, while managerial

skills are beneficial for successful organization and synchronization of all the

departments for efficient functioning.

Answers to Question 2

a) Externality refers to the benefit or cost to a third party who is not directly involved in the

economic activity generating externalities or has no control on the creation of the benefit

or cost (Pal 2015). It can be both positive and negative. As John PLC is construction

company, it generates positive externality by constructing residential and commercial

buildings while the pollution generated from the construction activities is the negative

externality for the people living nearby.

b) Fixed cost refers to the overhead cost that remains same and unaffected irrespective of

the level of output. Fixed costs for John PLC includes the lease or rent for the building,

electricity charge, equipment cost, utility charges, insurance, and interest payments. On

the other hand, variable costs are those that vary with the level of output produced. When

production increases (decreases), variable cost increases (decreases). The costs of

manufacturing or construction increases with the number of units supplied by the

company, which is the variable cost (Chen and Koebel 2017).

c) Similar to any other organization, one of the primary objectives of John PLC is to grow

its business and increase profit. Thus, John PLC will want to grow for growing its profit,

achieving economies of scale, and capturing larger market share. However, the most

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ECONOMICS

common risks that are associated with business growth are the fall in the quality of

products and services, underdeveloped and inadequate operational infrastructure and

systems, lack of production and technological flexibility, increased synchronization and

coordination issues and lack of proper human resources fit for the job roles and

responsibilities (Ward 2016).

d) Five different types of mergers are conglomerate, horizontal merger, market extension

merger, production extension and vertical merger (Tarba et al 2016). Conglomerate refers

to the merger between two unrelated businesses. Horizontal merger happens between

companies involved in direct competition in terms of the product lines and markets. On

the other hand, vertical merger occurs between companies along same supply chain.

Market extension merger happens between companies selling similar products or services

in different markets and product extension merger occurs between companies selling

different but related products in the same market.

Answer to question 3

a) Factors that affect the supply of John PLC are price of the products, cost of production,

technology, natural conditions, transport prices, factor prices and their availability,

government policies and price of related products. Thus, as John PLC is a construction

company, the easy availability of raw materials at a lower price, lower cost of production,

and increasing prices of units are the major factors that can increase its supply.

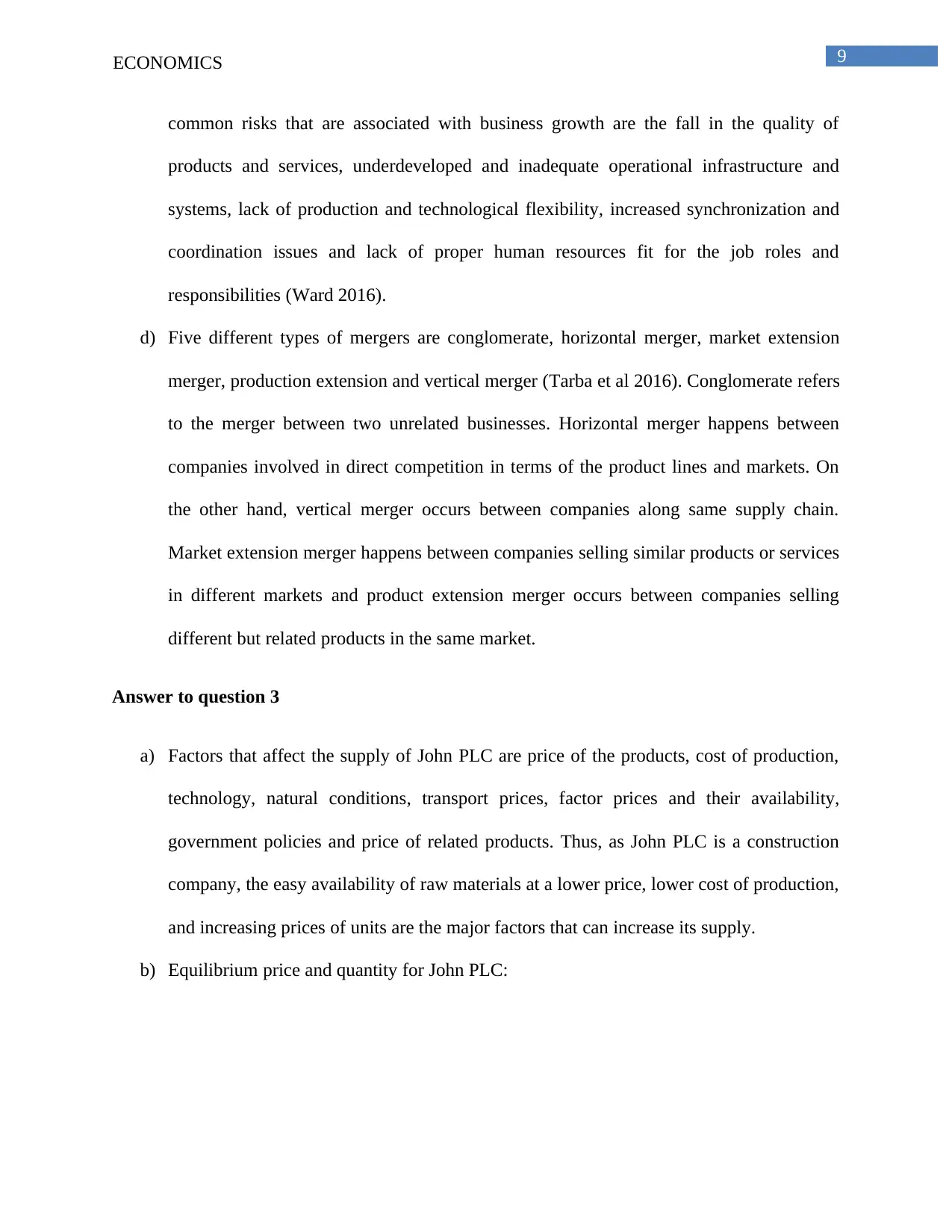

b) Equilibrium price and quantity for John PLC:

common risks that are associated with business growth are the fall in the quality of

products and services, underdeveloped and inadequate operational infrastructure and

systems, lack of production and technological flexibility, increased synchronization and

coordination issues and lack of proper human resources fit for the job roles and

responsibilities (Ward 2016).

d) Five different types of mergers are conglomerate, horizontal merger, market extension

merger, production extension and vertical merger (Tarba et al 2016). Conglomerate refers

to the merger between two unrelated businesses. Horizontal merger happens between

companies involved in direct competition in terms of the product lines and markets. On

the other hand, vertical merger occurs between companies along same supply chain.

Market extension merger happens between companies selling similar products or services

in different markets and product extension merger occurs between companies selling

different but related products in the same market.

Answer to question 3

a) Factors that affect the supply of John PLC are price of the products, cost of production,

technology, natural conditions, transport prices, factor prices and their availability,

government policies and price of related products. Thus, as John PLC is a construction

company, the easy availability of raw materials at a lower price, lower cost of production,

and increasing prices of units are the major factors that can increase its supply.

b) Equilibrium price and quantity for John PLC:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Price (£)

Quantity

Qs

QD

0

10

20

30

40

50

60

70

100 200 300 400 500 600 700

E

10ECONOMICS

c) Price elasticity of supply =

% change in quantity =

% change in price =

Hence, Price elasticity of supply = 40/40 = 1

% Change in quantity

% Change in price

(600-400)

(600+400)

/2

*100

(60-40)

(60+40)/2

*100

= (200/500)*100 = 40

= (20/50)*100 = 40

Quantity

Qs

QD

0

10

20

30

40

50

60

70

100 200 300 400 500 600 700

E

10ECONOMICS

c) Price elasticity of supply =

% change in quantity =

% change in price =

Hence, Price elasticity of supply = 40/40 = 1

% Change in quantity

% Change in price

(600-400)

(600+400)

/2

*100

(60-40)

(60+40)/2

*100

= (200/500)*100 = 40

= (20/50)*100 = 40

11ECONOMICS

d) It is seen that John PLC has unit elasticity of supply. In other words, when price elasticity of

supply is 1, a certain percentage change in the price results in equal percentage change in the

quantity supplied.

It implies that whenever there is a certain percentage change in price, the total revenue remains

same as the quantity supplied changes at the same percentage (Senthilnathan 2016).

Answer to Question 4

a) Law of diminishing returns state that when one input in the production process is

increased, other inputs remaining fixed, there will be a point at which further additions of

the input yields diminishing increases in the output (Cheung et al. 2016).

This law is considered at a short run basis because input quantity can be fixed in the short

run and all the inputs are variable in the long run. The law of diminishing return holds

only when one input is variable and others are fixed, which is possible only in the short

run.

b) Marginal product is the additional output produced by employing an additional unit of the

variable input, while average product refers to the output per unit of the factor inputs

(Fabinger and Weyl 2016). The relationship between average product and marginal

product has three dimensions:

When average product is rising, marginal product lies above the average product.

When average product is decreasing, marginal product lies below the average

product

When average product is maximum, the marginal product equals average product.

d) It is seen that John PLC has unit elasticity of supply. In other words, when price elasticity of

supply is 1, a certain percentage change in the price results in equal percentage change in the

quantity supplied.

It implies that whenever there is a certain percentage change in price, the total revenue remains

same as the quantity supplied changes at the same percentage (Senthilnathan 2016).

Answer to Question 4

a) Law of diminishing returns state that when one input in the production process is

increased, other inputs remaining fixed, there will be a point at which further additions of

the input yields diminishing increases in the output (Cheung et al. 2016).

This law is considered at a short run basis because input quantity can be fixed in the short

run and all the inputs are variable in the long run. The law of diminishing return holds

only when one input is variable and others are fixed, which is possible only in the short

run.

b) Marginal product is the additional output produced by employing an additional unit of the

variable input, while average product refers to the output per unit of the factor inputs

(Fabinger and Weyl 2016). The relationship between average product and marginal

product has three dimensions:

When average product is rising, marginal product lies above the average product.

When average product is decreasing, marginal product lies below the average

product

When average product is maximum, the marginal product equals average product.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.